BTC Future Gamma-Weighted Momentum Model (BGMM)The BTC Future Gamma-Weighted Momentum Model (BGMM) is a quantitative trading strategy that utilizes the Gamma-weighted average price (GWAP) in conjunction with a momentum-based approach to predict price movements in the Bitcoin futures market. The model combines the concept of weighted price movements with trend identification, where the Gamma factor amplifies the weight assigned to recent prices. It leverages the idea that historical price trends and weighting mechanisms can be utilized to forecast future price behavior.

Theoretical Background:

1. Momentum in Financial Markets:

Momentum is a well-established concept in financial market theory, referring to the tendency of assets to continue moving in the same direction after initiating a trend. Any observed market return over a given time period is likely to continue in the same direction, a phenomenon known as the “momentum effect.” Deviations from a mean or trend provide potential trading opportunities, particularly in highly volatile assets like Bitcoin.

Numerous empirical studies have demonstrated that momentum strategies, based on price movements, especially those correlating long-term and short-term trends, can yield significant returns (Jegadeesh & Titman, 1993). Given Bitcoin’s volatile nature, it is an ideal candidate for momentum-based strategies.

2. Gamma-Weighted Price Strategies:

Gamma weighting is an advanced method of applying weights to price data, where past price movements are weighted by a Gamma factor. This weighting allows for the reinforcement or reduction of the influence of historical prices based on an exponential function. The Gamma factor (ranging from 0.5 to 1.5) controls how much emphasis is placed on recent data: a value closer to 1 applies an even weighting across periods, while a value closer to 0 diminishes the influence of past prices.

Gamma-based models are used in financial analysis and modeling to enhance a model’s adaptability to changing market dynamics. This weighting mechanism is particularly advantageous in volatile markets such as Bitcoin futures, as it facilitates quick adaptation to changing market conditions (Black-Scholes, 1973).

Strategy Mechanism:

The BTC Future Gamma-Weighted Momentum Model (BGMM) utilizes an adaptive weighting strategy, where the Bitcoin futures prices are weighted according to the Gamma factor to calculate the Gamma-Weighted Average Price (GWAP). The GWAP is derived as a weighted average of prices over a specific number of periods, with more weight assigned to recent periods. The calculated GWAP serves as a reference value, and trading decisions are based on whether the current market price is above or below this level.

1. Long Position Conditions:

A long position is initiated when the Bitcoin price is above the GWAP and a positive price movement is observed over the last three periods. This indicates that an upward trend is in place, and the market is likely to continue in the direction of the momentum.

2. Short Position Conditions:

A short position is initiated when the Bitcoin price is below the GWAP and a negative price movement is observed over the last three periods. This suggests that a downtrend is occurring, and a continuation of the negative price movement is expected.

Backtesting and Application to Bitcoin Futures:

The model has been tested exclusively on the Bitcoin futures market due to Bitcoin’s high volatility and strong trend behavior. These characteristics make the market particularly suitable for momentum strategies, as strong upward or downward movements are often followed by persistent trends that can be captured by a momentum-based approach.

Backtests of the BGMM on the Bitcoin futures market indicate that the model achieves above-average returns during periods of strong momentum, especially when the Gamma factor is optimized to suit the specific dynamics of the Bitcoin market. The high volatility of Bitcoin, combined with adaptive weighting, allows the model to respond quickly to price changes and maximize trading opportunities.

Scientific Citations and Sources:

• Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65–91.

• Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637–654.

• Fama, E. F., & French, K. R. (1992). The Cross-Section of Expected Stock Returns. The Journal of Finance, 47(2), 427–465.

Cari skrip untuk "momentum"

Volatility Momentum Breakout StrategyDescription:

Overview:

The Volatility Momentum Breakout Strategy is designed to capture significant price moves by combining a volatility breakout approach with trend and momentum filters. This strategy dynamically calculates breakout levels based on market volatility and uses these levels along with trend and momentum conditions to identify trade opportunities.

How It Works:

1. Volatility Breakout:

• Methodology:

The strategy computes the highest high and lowest low over a defined lookback period (excluding the current bar to avoid look-ahead bias). A multiple of the Average True Range (ATR) is then added to (or subtracted from) these levels to form dynamic breakout thresholds.

• Purpose:

This method helps capture significant price movements (breakouts) while ensuring that only past data is used, thereby maintaining realistic signal generation.

2. Trend Filtering:

• Methodology:

A short-term Exponential Moving Average (EMA) is applied to determine the prevailing trend.

• Purpose:

Long trades are considered only when the current price is above the EMA, indicating an uptrend, while short trades are taken only when the price is below the EMA, indicating a downtrend.

3. Momentum Confirmation:

• Methodology:

The Relative Strength Index (RSI) is used to gauge market momentum.

• Purpose:

For long entries, the RSI must be above a mid-level (e.g., above 50) to confirm upward momentum, and for short entries, it must be below a similar threshold. This helps filter out signals during overextended conditions.

Entry Conditions:

• Long Entry:

A long position is triggered when the current closing price exceeds the calculated long breakout level, the price is above the short-term EMA, and the RSI confirms momentum (e.g., above 50).

• Short Entry:

A short position is triggered when the closing price falls below the calculated short breakout level, the price is below the EMA, and the RSI confirms momentum (e.g., below 50).

Risk Management:

• Position Sizing:

Trades are sized to risk a fixed percentage of account equity (set here to 5% per trade in the code, with each trade’s stop loss defined so that risk is limited to approximately 2% of the entry price).

• Stop Loss & Take Profit:

A stop loss is placed a fixed ATR multiple away from the entry price, and a take profit target is set to achieve a 1:2 risk-reward ratio.

• Realistic Backtesting:

The strategy is backtested using an initial capital of $10,000, with a commission of 0.1% per trade and slippage of 1 tick per bar—parameters chosen to reflect conditions faced by the average trader.

Important Disclaimers:

• No Look-Ahead Bias:

All breakout levels are calculated using only past data (excluding the current bar) to ensure that the strategy does not “peek” into future data.

• Educational Purpose:

This strategy is experimental and provided solely for educational purposes. Past performance is not indicative of future results.

• User Responsibility:

Traders should thoroughly backtest and paper trade the strategy under various market conditions and adjust parameters to fit their own risk tolerance and trading style before live deployment.

Conclusion:

By integrating volatility-based breakout signals with trend and momentum filters, the Volatility Momentum Breakout Strategy offers a unique method to capture significant price moves in a disciplined manner. This publication provides a transparent explanation of the strategy’s components and realistic backtesting parameters, making it a useful tool for educational purposes and further customization by the TradingView community.

Adaptive Momentum Reversion StrategyThe Adaptive Momentum Reversion Strategy: An Empirical Approach to Market Behavior

The Adaptive Momentum Reversion Strategy seeks to capitalize on market price dynamics by combining concepts from momentum and mean reversion theories. This hybrid approach leverages a Rate of Change (ROC) indicator along with Bollinger Bands to identify overbought and oversold conditions, triggering trades based on the crossing of specific thresholds. The strategy aims to detect momentum shifts and exploit price reversions to their mean.

Theoretical Framework

Momentum and Mean Reversion: Momentum trading assumes that assets with a recent history of strong performance will continue in that direction, while mean reversion suggests that assets tend to return to their historical average over time (Fama & French, 1988; Poterba & Summers, 1988). This strategy incorporates elements of both, looking for periods when momentum is either overextended (and likely to revert) or when the asset’s price is temporarily underpriced relative to its historical trend.

Rate of Change (ROC): The ROC is a straightforward momentum indicator that measures the percentage change in price over a specified period (Wilder, 1978). The strategy calculates the ROC over a 2-period window, making it responsive to short-term price changes. By using ROC, the strategy aims to detect price acceleration and deceleration.

Bollinger Bands: Bollinger Bands are used to identify volatility and potential price extremes, often signaling overbought or oversold conditions. The bands consist of a moving average and two standard deviation bounds that adjust dynamically with price volatility (Bollinger, 2002).

The strategy employs two sets of Bollinger Bands: one for short-term volatility (lower band) and another for longer-term trends (upper band), with different lengths and standard deviation multipliers.

Strategy Construction

Indicator Inputs:

ROC Period: The rate of change is computed over a 2-period window, which provides sensitivity to short-term price fluctuations.

Bollinger Bands:

Lower Band: Calculated with a 18-period length and a standard deviation of 1.7.

Upper Band: Calculated with a 21-period length and a standard deviation of 2.1.

Calculations:

ROC Calculation: The ROC is computed by comparing the current close price to the close price from rocPeriod days ago, expressing it as a percentage.

Bollinger Bands: The strategy calculates both upper and lower Bollinger Bands around the ROC, using a simple moving average as the central basis. The lower Bollinger Band is used as a reference for identifying potential long entry points when the ROC crosses above it, while the upper Bollinger Band serves as a reference for exits, when the ROC crosses below it.

Trading Conditions:

Long Entry: A long position is initiated when the ROC crosses above the lower Bollinger Band, signaling a potential shift from a period of low momentum to an increase in price movement.

Exit Condition: A position is closed when the ROC crosses under the upper Bollinger Band, or when the ROC drops below the lower band again, indicating a reversal or weakening of momentum.

Visual Indicators:

ROC Plot: The ROC is plotted as a line to visualize the momentum direction.

Bollinger Bands: The upper and lower bands, along with their basis (simple moving averages), are plotted to delineate the expected range for the ROC.

Background Color: To enhance decision-making, the strategy colors the background when extreme conditions are detected—green for oversold (ROC below the lower band) and red for overbought (ROC above the upper band), indicating potential reversal zones.

Strategy Performance Considerations

The use of Bollinger Bands in this strategy provides an adaptive framework that adjusts to changing market volatility. When volatility increases, the bands widen, allowing for larger price movements, while during quieter periods, the bands contract, reducing trade signals. This adaptiveness is critical in maintaining strategy effectiveness across different market conditions.

The strategy’s pyramiding setting is disabled (pyramiding=0), ensuring that only one position is taken at a time, which is a conservative risk management approach. Additionally, the strategy includes transaction costs and slippage parameters to account for real-world trading conditions.

Empirical Evidence and Relevance

The combination of momentum and mean reversion has been widely studied and shown to provide profitable opportunities under certain market conditions. Studies such as Jegadeesh and Titman (1993) confirm that momentum strategies tend to work well in trending markets, while mean reversion strategies have been effective during periods of high volatility or after sharp price movements (De Bondt & Thaler, 1985). By integrating both strategies into one system, the Adaptive Momentum Reversion Strategy may be able to capitalize on both trending and reverting market behavior.

Furthermore, research by Chan (1996) on momentum-based trading systems demonstrates that adaptive strategies, which adjust to changes in market volatility, often outperform static strategies, providing a compelling rationale for the use of Bollinger Bands in this context.

Conclusion

The Adaptive Momentum Reversion Strategy provides a robust framework for trading based on the dual concepts of momentum and mean reversion. By using ROC in combination with Bollinger Bands, the strategy is capable of identifying overbought and oversold conditions while adapting to changing market conditions. The use of adaptive indicators ensures that the strategy remains flexible and can perform across different market environments, potentially offering a competitive edge for traders who seek to balance risk and reward in their trading approaches.

References

Bollinger, J. (2002). Bollinger on Bollinger Bands. McGraw-Hill Professional.

Chan, L. K. C. (1996). Momentum, Mean Reversion, and the Cross-Section of Stock Returns. Journal of Finance, 51(5), 1681-1713.

De Bondt, W. F., & Thaler, R. H. (1985). Does the Stock Market Overreact? Journal of Finance, 40(3), 793-805.

Fama, E. F., & French, K. R. (1988). Permanent and Temporary Components of Stock Prices. Journal of Political Economy, 96(2), 246-273.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Trend Research.

Adaptive Squeeze Momentum StrategyThe Adaptive Squeeze Momentum Strategy is a versatile trading algorithm designed to capitalize on periods of low volatility that often precede significant price movements. By integrating multiple technical indicators and customizable settings, this strategy aims to identify optimal entry and exit points for both long and short positions.

Key Features:

Long/Short Trade Control:

Toggle Options: Easily enable or disable long and short trades according to your trading preferences or market conditions.

Flexible Application: Adapt the strategy for bullish, bearish, or neutral market outlooks.

Squeeze Detection Mechanism:

Bollinger Bands and Keltner Channels: Utilizes the convergence of Bollinger Bands inside Keltner Channels to detect "squeeze" conditions, indicating a potential breakout.

Dynamic Squeeze Length: Calculates the average squeeze duration to adapt to changing market volatility.

Momentum Analysis:

Linear Regression: Applies linear regression to price changes over a specified momentum length to gauge the strength and direction of momentum.

Dynamic Thresholds: Sets momentum thresholds based on standard deviations, allowing for adaptive sensitivity to market movements.

Momentum Multiplier: Adjustable setting to fine-tune the aggressiveness of momentum detection.

Trend Filtering:

Exponential Moving Average (EMA): Implements a trend filter using an EMA to align trades with the prevailing market direction.

Customizable Length: Adjust the EMA length to suit different trading timeframes and assets.

Relative Strength Index (RSI) Filtering:

Overbought/Oversold Signals: Incorporates RSI to avoid entering trades during overextended market conditions.

Adjustable Levels: Set your own RSI oversold and overbought thresholds for personalized signal generation.

Advanced Risk Management:

ATR-Based Stop Loss and Take Profit:

Adaptive Levels: Uses the Average True Range (ATR) to set stop loss and take profit points that adjust to market volatility.

Custom Multipliers: Modify ATR multipliers for both stop loss and take profit to control risk and reward ratios.

Minimum Volatility Filter: Ensures trades are only taken when market volatility exceeds a user-defined minimum, avoiding periods of low activity.

Time-Based Exit:

Holding Period Multiplier: Defines a maximum holding period based on the momentum length to reduce exposure to adverse movements.

Automatic Position Closure: Closes positions after the specified holding period is reached.

Session Filtering:

Trading Session Control: Limits trading to predefined market hours, helping to avoid illiquid periods.

Custom Session Times: Set your preferred trading session to match market openings, closings, or specific timeframes.

Visualization Tools:

Indicator Plots: Displays Bollinger Bands, Keltner Channels, and trend EMA on the chart for visual analysis.

Squeeze Signals: Marks squeeze conditions on the chart, providing clear visual cues for potential trade setups.

Customization Options:

Indicator Parameters: Fine-tune lengths and multipliers for Bollinger Bands, Keltner Channels, momentum calculation, and ATR.

Entry Filters: Choose to use trend and RSI filters to refine trade entries based on your strategy.

Risk Management Settings: Adjust stop loss, take profit, and holding periods to match your risk tolerance.

Trade Direction Control: Enable or disable long and short trades independently to align with your market strategy or compliance requirements.

Time Settings: Modify the trading session times and enable or disable the time filter as needed.

Use Cases:

Trend Traders: Benefit from aligning entries with the broader market trend while capturing breakout movements.

Swing Traders: Exploit periods of low volatility leading to significant price swings.

Risk-Averse Traders: Utilize advanced risk management features to protect capital and manage exposure.

Disclaimer:

This strategy is a tool to assist in trading decisions and should be used in conjunction with other analyses and risk management practices. Past performance is not indicative of future results. Always test the strategy thoroughly and adjust settings to suit your specific trading style and market conditions.

Open DriveOpen Drive is a market profile concept introduced by Jim Dalton. It occurs when the price moves directionally and persistently for the first 30 minutes from the cash market open.

It is necessary to use 30-minute bars as there needs to be enough time to measure an extreme move of the cash open. This means there will be fewer trades than other strategies using faster time periodicities.

The script finds open drives from these time points 0700/ 0800 and 1300/1430.

The entry signal also has a breakout threshold using the 5-bar high and 5-bar low to only take trades moving away from the prior 5-bar range. This weeds out most mid-range trades and small range expansion bars.

If the price has had a strong move from the open and has broken either below the prior 5-bar low or above the prior 5-bar high by an amount equal to the prior 5-bar range a trade is entered in the direction of the move.

The Exit criteria; exit after 3 bars which is 90mins when using a 30min periodicity.

Note, this script is shared to show that momentum generated on or around the cash open tends to persist. The entry and exits of this strategy are quite naive but there are plenty of ways to take more aggressive entries on faster time frames when an open drive occurs. The times chosen for this strategy will suit stock index futures mainly. The user can experiment with other futures products and their corresponding pit/ cash open hours.

Google "open drive market profile" for more information on open drives and market profile concepts.

Happy trading!

ALMASTO – Pro Trend & Momentum (v1.1)ALMASTO — Pro Trend & Momentum Strategy

Description:

This strategy is designed for precision trading in both Forex (FX) and Crypto markets.

It combines multi-timeframe trend confirmation (EMA200), momentum filters (RSI, MACD, ADX), and ATR-based dynamic risk management.

ALMASTO — Pro Trend & Momentum Strategy automatically manages take-profit levels, stop-loss, and breakeven adjustments once TP1 is reached — providing a structured and emotion-free trading approach.

Optimal Use

Works best on lower timeframes (5m–15m) with strong liquidity sessions.

Optimized for pairs like EURUSD, XAUUSD, and BTCUSDT.

Built for trend-following setups and momentum reversals with high volatility confirmation.

Recommended Settings

🔹 Forex – 5m

EMA Fast = 34, EMA Slow = 200, HTF = 1H

RSI (14): Long ≥ 55 / Short ≤ 45

MACD (8 / 21 / 5), ADX Len 10 / Min 27

ATR Len 7, Stop Loss = ATR × 2.1

TP1 = 1.1 RR, TP2 = 2.3 RR

Session = 07:00–11:00 & 12:30–16:00 (Exchange Time)

Risk = 0.8% per trade

🔹 Forex – 15m

EMA Fast = 50, EMA Slow = 200, HTF = 4H

RSI (14): Long ≥ 53 / Short ≤ 47

MACD (12 / 26 / 9), ADX Min 24

ATR Len 10, SL = ATR × 1.9

TP1 = 1.2 RR, TP2 = 2.6 RR

Risk = 1.0% per trade

🔹 Crypto – 5m (BTC/USDT)

EMA Fast = 34, EMA Slow = 200, HTF = 4H

RSI (14): Long ≥ 56 / Short ≤ 44

MACD (8 / 21 / 5), ADX Min 30

ATR Len 7, SL = ATR × 2.2

TP1 = 1.0 RR, TP2 = 2.5 RR

Session = 00:00–06:00 & 12:00–22:00 (UTC)

Risk = 0.5% per trade

Core Features

✅ Auto breakeven after TP1

✅ Dual take-profit system (1:1 & 1:2 RR)

✅ ATR-based stop & trailing logic

✅ Filters for session time, volume, and volatility

✅ Candle-body vs ATR size filter to avoid noise

✅ Optional cooldown between trades

Important Notes

Use bar close confirmation only (barstate.isconfirmed) to avoid repainting on lower timeframes.

Adjust commission (0.01–0.03%) and slippage (1–2 ticks) in Strategy Tester for realistic results.

Avoid low-liquidity hours (after 21:00 UTC for FX / after midnight for crypto).

Backtest using realistic broker data (e.g., BlackBull Markets / Bybit / Binance Futures).

Best results occur during London & New York sessions with moderate volatility.

⚠️ Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice.

Use proper risk management and test thoroughly before using on live accounts.

Developed by KING FX Labs

Built and optimized by Yousef Almasto — combining advanced price-action logic, multi-timeframe EMA structure, and volatility-adaptive ATR management.

Tested across Forex, Gold, and Crypto markets to ensure consistent performance and minimal drawdown.

📈 “Precision Trading. Zero Emotion. Pure Momentum.”

TASC 2024.01 Gap Momentum System█ OVERVIEW

TASC's January 2024 edition of Traders' Tips features an article titled “Gap Momentum” by Perry J. Kaufman. The article discusses how a trader might create a momentum strategy based on opening gap data. This script implements the Gap Momentum system presented therein.

█ CONCEPTS

In the article, Perry J. Kaufman introduces Gap Momentum as a cumulative series constructed in the same way as On-Balance Volume (OBV) , but using gap openings (today’s open minus yesterday’s close).

To smoothen the resulting time series (i.e., obtain the " signal line "), the author applies a simple moving average . Subsequently, he proposes the following two trading rules for a long-only trading system:

• Enter a long position when the signal line is moving higher.

• Exit when the signal line is moving lower.

█ CALCULATIONS

The calculation of Gap Momentum involves the following steps:

1. Calculate the ratio of the sum of positive gaps over the past N days to the sum of negative gaps (absolute values) over the same time period.

2. Add the resulting gap ratio to the cumulative time series. This time series is the Gap Momentum.

3. Keep moving forward, as in an N-day moving average.

RSI Momentum Trend MM with Risk Per Trade [MTF]This is a comprehensive and highly customizable trend-following strategy based on RSI momentum. The core logic identifies strong directional moves when the RSI crosses user-defined thresholds, combined with an EMA trend confirmation. It is designed for traders who want granular control over their strategy's parameters, from signal generation to risk management and exit logic.

This script evolves a simple concept into a powerful backtesting tool, allowing you to test various money management and trade management theories across different timeframes.

Key Features

- RSI Momentum Signals: Uses RSI crosses above a "Positive" level or below a "Negative" level to generate trend signals. An EMA filter ensures entries align with the immediate trend.

- Multi-Timeframe (MTF) Analysis: The core RSI and EMA signals can be calculated on a higher timeframe (e.g., using 4H signals to trade on a 1H chart) to align trades with the larger trend. This feature helps to reduce noise and improve signal quality.

Advanced Money Management

- Risk per Trade %: Calculate position size based on a fixed percentage of equity you want to risk per trade.

- Full Equity: A more aggressive option to open each position with 100% of the available strategy equity.

Flexible Exit Logic: Choose from three distinct exit strategies to match your trading style

- Percentage (%) Based: Set a fixed Stop Loss and Take Profit as a percentage of the entry price.

- ATR Multiplier: Base your Stop Loss and Take Profit on the Average True Range (ATR), making your exits adaptive to market volatility.

- Trend Reversal: A true trend-following mode. A long position is held until an opposite "Negative" signal appears, and a short position is held until a "Positive" signal appears. This allows you to "let your winners run."

Backtest Date Range Filter: Easily configure a start and end date to backtest the strategy's performance during specific market periods (e.g., bull markets, bear markets, or high-volatility periods).

How to Use

RSI Settings

- Higher Timeframe: Set the timeframe for signal calculation. This must be higher than your chart's timeframe.

- RSI Length, Positive above, Negative below: Configure the core parameters for the RSI signals.

Money Management

Position Sizing Mode

- Choose "Risk per Trade" to use the Risk per Trade (%) input for precise risk control.

- Choose "Full Equity" to use 100% of your capital for each trade.

- Risk per Trade (%): Define the percentage of your equity to risk on a single trade (only works with the corresponding sizing mode).

SL/TP Calculation Mode

Select your preferred exit method from the dropdown. The strategy will automatically use the relevant inputs (e.g., % values, ATR Multiplier values, or the trend reversal logic).

Backtest Period Settings

Use the Start Date and End Date inputs to isolate a specific period for your backtest analysis.

License & Disclaimer

© waranyu.trkm — MIT License.

This script is for educational purposes only and should not be considered financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and risk assessment before making any trading decisions.

RTB - Momentum Breakout Strategy V3

📈 RTB - Momentum Breakout Strategy V3 is a directional breakout strategy based on momentum. It combines exponential moving averages (EMAs), RSI, and recent support/resistance levels to detect breakout entries with trend confirmation. The system includes dynamic risk management using ATR-based stop-loss and trailing stop levels. Webhook alerts are supported for external automated trading integrations.

🔎 The strategy was backtested using default parameters on BTCUSDT Futures (Bybit) with 4-hour timeframe and a 0.05% commission per trade.

⚠️ This script is for educational purposes only and does not constitute financial advice. Always do your own research before trading.

Chande Momentum Oscillator (CMO) Buy Sell Strategy [TradeDots]The "Chande Momentum Oscillator (CMO) Buy Sell Strategy" leverages the CMO indicator to identify short-term buy and sell opportunities.

HOW DOES IT WORK

The standard CMO indicator measures the difference between recent gains and losses, divided by the total price movement over the same period. However, this version of the CMO has some limitations.

The primary disadvantage of the original CMO is its responsiveness to short-term volatility, making the signals less smooth and more erratic, especially in fluctuating markets. This instability can lead to misleading buy or sell signals.

To address this, we integrated the concept from the Moving Average Convergence Divergence (MACD) indicator. By applying a 9-period exponential moving average (EMA) to the CMO line, we obtained a smoothed signal line. This line acts as a filter, identifying confirmed overbought or oversold states, thereby reducing the number of false signals.

Similar to the MACD histogram, we generate columns representing the difference between the CMO and its signal line, reflecting market momentum. We use this momentum indicator as a criterion for entry and exit points. Trades are executed when there's a convergence of CMO and signal lines during an oversold state, and they are closed when the CMO line diverges from the signal line, indicating increased selling pressure.

APPLICATION

Since the 9-period EMA smooths the CMO line, it's less susceptible to extreme price fluctuations. However, this smoothing also makes it more challenging to breach the original +50 and -50 benchmarks.

To increase trading opportunities, we've tightened the boundary ranges. Users can customize the target benchmark lines in the settings to adjust for the volatility of the underlying asset.

The 'cool down period' is essentially the number of bars that await before the next signal generation. This feature is employed to dodge the occurrence of multiple signals in a short period.

DEFAULT SETUP

Commission: 0.01%

Initial Capital: $10,000

Equity per Trade: 80%

Signal Cool Down Period: 5

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

Simple Momentum Strategy Based on SMA, EMA and VolumeA simple, non short selling (long positions only, i.e. buy low and sell high) strategy. Strategy makes use of simple SMA, EMA and Volume indicators to attempt to enter the market at the most optimum time (i.e. when momentum and price are moving upwards). Optimum time is defined mainly by picking best timing for price moves higher based on upwards momentum.

This script is targeted / meant for an average/typical trader or investor. This is why a non short selling approach was selected for optimisation for this strategy because "typpical", "average" traders and investors usually use basic (i.e. minimum fees / free membership) exchanges that would not usually offer short selling functionality (at least without additional fees). The assumption used here is that only advanced and sophisticated traders and investors would pay for advanced trading platforms that enable short selling, have a risk appetite for short selling and thus use short selling as a strategy.

The results of the strategy are:

In an overall roughly bearish market (backward testing from beginning to end of 2018) i.e. the market immediately following the highs of around 20k USD per BTC, this strategy made a loss of £3231 USD on trades of a maximum of 1 BTC per long position.

But in an overall bullish market, it makes a profit of about $6800 USD from beginning of 2019 onwards by trading a maximum of 1 BTC per long position.

NOTE: All trading involves high risk. Most strategies use past performance and behaviour as indicators of future performance and that is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations too. One limitation is that unlike an actual performance record, simulated results do not represent actual trading and since the trades have not actually been executed, the results of those trades themselves do not have any influence on actual market results, which in real life they would have had (no matter how minor). Additionally, simulated results may have under or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also, by their nature, designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

Slope Failure (Momentum Stall) STRATEGY//======================================================================================

// SLOPE FAILURE (MOMENTUM STALL) STRATEGY

//--------------------------------------------------------------------------------------

// WHAT THIS STRATEGY DOES

// -----------------------

// This strategy trades **momentum failure**, not trend direction.

//

// Instead of predicting where price will go, it detects when **momentum can no longer

// continue in its current direction** and briefly fades that failure.

//

// Core idea:

// - Momentum expands → slope grows

// - Momentum stalls → slope collapses or flips

// - That stall represents **state transition**, not noise

//

// The system exploits these transitions repeatedly at short horizons.

//

//--------------------------------------------------------------------------------------

// HOW MOMENTUM IS MEASURED

// ------------------------

// 1. Source price (optionally smoothed)

// 2. First derivative (slope = price - price )

// 3. Optional smoothing of the slope itself

//

// The slope represents **instantaneous directional force**, not trend bias.

//

//--------------------------------------------------------------------------------------

// ENTRY LOGIC (SLOPE FAILURE)

// ---------------------------

// • Bull Slope Failure (SHORT):

// - Prior slope was sufficiently positive

// - Current slope collapses to zero or below

// → Upward momentum failed → enter SHORT

//

// • Bear Slope Failure (LONG):

// - Prior slope was sufficiently negative

// - Current slope rises to zero or above

// → Downward momentum failed → enter LONG

//

// Optional:

// - Minimum slope band can be enforced to avoid weak/noisy failures

//

//--------------------------------------------------------------------------------------

// EXIT LOGIC

// ----------

// Primary exits are **force-based**, not price-based:

//

// • Longest Slope Local Turn (optional):

// - Detects when the strongest slope in a recent window has occurred

// - Exits when momentum starts decaying from that extreme

//

// • Percent Stop Loss (optional):

// - Fixed % protection relative to entry price

//

// The strategy does NOT rely on profit targets.

// Winners are exited when **momentum decays**, not when price "looks good".

//

//--------------------------------------------------------------------------------------

// POSITION SIZING

// ---------------

// This strategy supports **percent-of-equity sizing**, computed dynamically:

//

// position size = (account equity × % allocation) / price

//

// This allows:

// - P&L to scale smoothly

// - Drawdowns to remain proportional

// - The same logic to work across symbols and account sizes

//

//--------------------------------------------------------------------------------------

// STRATEGY CHARACTERISTICS

// ------------------------

// • High trade count

// • Win rate near ~45–50%

// • Small, fast losers

// • Slightly larger winners

// • Very low drawdown

//

// This profile is intentionally designed for **scalability**, not prediction.

//

//--------------------------------------------------------------------------------------

// IMPORTANT NOTES

// ---------------

// • This is NOT a trend-following strategy

// • This is NOT a mean-reversion guess

// • This is a momentum **state-transition detector**

//

// The edge comes from structure + exits + sizing — not indicators.

//

//======================================================================================

Warrior Trading Momentum Strategy

# 🚀 Warrior Trading Momentum Strategy - Day Trading Excellence

## Strategy Overview

This comprehensive Pine Script strategy replicates the proven methodologies taught by Ross Cameron and the Warrior Trading community. Designed for active day traders, it identifies high-probability momentum setups with strict risk management protocols.

## 📈 Core Trading Setups

### 1. Gap and Go Trading

- **Primary Focus**: Stocks gapping up 2%+ with volume confirmation

- **Entry Logic**: Breakout above gap open with momentum validation

- **Volume Filter**: 2x average volume requirement for quality setups

### 2. ABCD Pattern Recognition

- **Pattern Detection**: Automated identification of classic ABCD reversal patterns

- **Validation**: A-B and C-D move relationship analysis

- **Entry Trigger**: D-point breakout with volume confirmation

### 3. VWAP Momentum Plays

- **Strategy**: Entries near VWAP with bounce confirmation

- **Distance Filter**: Configurable percentage distance for optimal entries

- **Direction Bias**: Above VWAP bullish momentum validation

### 4. Red to Green Reversals

- **Setup**: Reversal patterns after consecutive red candles

- **Confirmation**: Volume spike with bullish close required

- **Momentum**: Trend change validation with RSI support

### 5. Breakout Momentum

- **Logic**: Breakouts above recent highs with volume

- **Filters**: EMA20 and RSI confirmation for quality

- **Trend**: Established momentum direction validation

## ⚡ Key Features

### Smart Risk Management

- **Position Sizing**: Automatic calculation based on account risk percentage

- **Stop Loss**: 2 ATR-based stops for volatility adjustment

- **Take Profit**: Configurable risk-reward ratios (default 1:2)

- **Trailing Stops**: Profit protection with adjustable triggers

### Advanced Filtering System

- **Time Filters**: Market hours trading with lunch hour avoidance

- **Volume Confirmation**: Multi-timeframe volume analysis

- **Momentum Indicators**: RSI and moving average trend validation

- **Quality Control**: Multiple confirmation layers for signal accuracy

### PDT-Friendly Design

- **Trade Limiting**: Built-in daily trade counter for accounts under $25K

- **Selective Trading**: Priority scoring system for A+ setups only

- **Quality over Quantity**: Maximum 2-3 high-probability trades per day

## 🎯 Optimal Usage

### Best Timeframes

- **Primary**: 5-minute charts for entry timing

- **Secondary**: 1-minute for precise execution

- **Context**: Daily charts for gap analysis

### Ideal Market Conditions

- **Volatility**: High-volume, momentum-driven markets

- **Stocks**: Market cap $100M+, average volume 1M+ shares

- **Sectors**: Technology, biotech, growth stocks with news catalysts

### Account Requirements

- **Minimum**: $500+ for proper position sizing

- **Recommended**: $25K+ for unlimited day trading

- **Risk Tolerance**: Active day trading experience preferred

## 📊 Performance Optimization

### Entry Criteria (All Must Align)

1. ✅ Time filter (market hours, avoid lunch)

2. ✅ Volume spike (2x+ average volume)

3. ✅ Momentum confirmation (RSI 50-80)

4. ✅ Trend alignment (above EMA20)

5. ✅ Pattern completion (setup-specific)

### Risk Parameters

- **Maximum Risk**: 1-2% per trade

- **Position Size**: 25% of account maximum

- **Stop Loss**: 2 ATR below entry

- **Take Profit**: 2:1 risk-reward minimum

## 🔧 Customization Options

### Gap Trading Settings

- Minimum gap percentage threshold

- Volume multiplier requirements

- Gap validation criteria

### Pattern Recognition

- ABCD ratio parameters

- Swing point sensitivity

- Pattern completion filters

### Risk Management

- Risk-reward ratio adjustment

- Maximum daily trade limits

- Trailing stop trigger levels

### Time and Session Filters

- Trading session customization

- Lunch hour avoidance toggle

- Market condition filters

## ⚠️ Important Disclaimers

### Risk Warning

- **High Risk**: Day trading involves substantial risk of loss

- **Capital Requirements**: Only trade with risk capital

- **Experience**: Strategy requires active monitoring and experience

- **Market Conditions**: Performance varies with market volatility

### PDT Considerations

- **Day Trading Rules**: Accounts under $25K limited to 3 day trades per 5 days

- **Compliance**: Strategy includes trade counting for PDT compliance

- **Alternative**: Consider swing trading modifications for smaller accounts

### Backtesting vs Live Trading

- **Slippage**: Real trading involves execution delays and slippage

- **Commissions**: Factor in broker fees for accurate performance

- **Market Impact**: Large positions may affect fill prices

- **Psychological Factors**: Live trading involves emotional challenges

## 📚 Educational Value

This strategy serves as an excellent learning tool for understanding:

- Professional day trading methodologies

- Risk management principles

- Pattern recognition techniques

- Volume and momentum analysis

- Multi-timeframe analysis

## 🤝 Community and Support

Based on proven Warrior Trading methodologies with active community support. Strategy includes comprehensive plotting and information tables for educational purposes and trade analysis.

---

**Disclaimer**: This strategy is for educational purposes. Past performance does not guarantee future results. Always practice proper risk management and never risk more than you can afford to lose.

**Tags**: #DayTrading #Momentum #WarriorTrading #GapAndGo #ABCD #VWAP #PatternTrading #RiskManagement

Dual Momentum StrategyThis Pine Script™ strategy implements the "Dual Momentum" approach developed by Gary Antonacci, as presented in his book Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk (McGraw Hill Professional, 2014). Dual momentum investing combines relative momentum and absolute momentum to maximize returns while minimizing risk. Relative momentum involves selecting the asset with the highest recent performance between two options (a risky asset and a safe asset), while absolute momentum considers whether the chosen asset has a positive return over a specified lookback period.

In this strategy:

Risky Asset (SPY): Represents a stock index fund, typically more volatile but with higher potential returns.

Safe Asset (TLT): Represents a bond index fund, which generally has lower volatility and acts as a hedge during market downturns.

Monthly Momentum Calculation: The momentum for each asset is calculated based on its price change over the last 12 months. Only assets with a positive momentum (absolute momentum) are considered for investment.

Decision Rules:

Invest in the risky asset if its momentum is positive and greater than that of the safe asset.

If the risky asset’s momentum is negative or lower than the safe asset's, the strategy shifts the allocation to the safe asset.

Scientific Reference

Antonacci's work on dual momentum investing has shown the strategy's ability to outperform traditional buy-and-hold methods while reducing downside risk. This approach has been reviewed and discussed in both academic and investment publications, highlighting its strong risk-adjusted returns (Antonacci, 2014).

Reference: Antonacci, G. (2014). Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk. McGraw Hill Professional.

Chande Momentum Oscillator StrategyThe Chande Momentum Oscillator (CMO) Trading Strategy is based on the momentum oscillator developed by Tushar Chande in 1994. The CMO measures the momentum of a security by calculating the difference between the sum of recent gains and losses over a defined period. The indicator offers a means to identify overbought and oversold conditions, making it suitable for developing mean-reversion trading strategies (Chande, 1997).

Strategy Overview:

Calculation of the Chande Momentum Oscillator (CMO):

The CMO formula considers both positive and negative price changes over a defined period (commonly set to 9 days) and computes the net momentum as a percentage.

The formula is as follows:

CMO=100×(Sum of Gains−Sum of Losses)(Sum of Gains+Sum of Losses)

CMO=100×(Sum of Gains+Sum of Losses)(Sum of Gains−Sum of Losses)

This approach distinguishes the CMO from other oscillators like the RSI by using both price gains and losses in the numerator, providing a more symmetrical measurement of momentum (Chande, 1997).

Entry Condition:

The strategy opens a long position when the CMO value falls below -50, signaling an oversold condition where the price may revert to the mean. Research in mean-reversion, such as by Poterba and Summers (1988), supports this approach, highlighting that prices often revert after sharp movements due to overreaction in the markets.

Exit Conditions:

The strategy closes the long position when:

The CMO rises above 50, indicating that the price may have become overbought and may not provide further upside potential.

Alternatively, the position is closed 5 days after the buy signal is triggered, regardless of the CMO value, to ensure a timely exit even if the momentum signal does not reach the predefined level.

This exit strategy aligns with the concept of time-based exits, reducing the risk of prolonged exposure to adverse price movements (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages the well-known phenomenon of mean-reversion in financial markets. According to research by Jegadeesh and Titman (1993), prices tend to revert to their mean over short periods following strong movements, creating opportunities for traders to profit from temporary deviations.

The CMO captures this mean-reversion behavior by monitoring extreme price conditions. When the CMO reaches oversold levels (below -50), it signals potential buying opportunities, whereas crossing overbought levels (above 50) indicates conditions for selling.

Market Efficiency and Overreaction:

The strategy takes advantage of behavioral inefficiencies and overreactions, which are often the drivers behind sharp price movements (Shiller, 2003). By identifying these extreme conditions with the CMO, the strategy aims to capitalize on the market’s tendency to correct itself when price deviations become too large.

Optimization and Parameter Selection:

The 9-day period used for the CMO calculation is a widely accepted timeframe that balances responsiveness and noise reduction, making it suitable for capturing short-term price fluctuations. Studies in technical analysis suggest that oscillators optimized over such periods are effective in detecting reversals (Murphy, 1999).

Performance and Backtesting:

The strategy's effectiveness is confirmed through backtesting, which shows that using the CMO as a mean-reversion tool yields profitable opportunities. The use of time-based exits alongside momentum-based signals enhances the reliability of the strategy by ensuring that trades are closed even when the momentum signal alone does not materialize.

Conclusion:

The Chande Momentum Oscillator Trading Strategy combines the principles of momentum measurement and mean-reversion to identify and capitalize on short-term price fluctuations. By using a widely tested oscillator like the CMO and integrating a systematic exit approach, the strategy effectively addresses both entry and exit conditions, providing a robust method for trading in diverse market environments.

References:

Chande, T. S. (1997). The New Technical Trader: Boost Your Profit by Plugging into the Latest Indicators. John Wiley & Sons.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Strategy Myth-Busting #11 - TrendMagic+SqzMom+CDV - [MYN]This is part of a new series we are calling "Strategy Myth-Busting" where we take open public manual trading strategies and automate them. The goal is to not only validate the authenticity of the claims but to provide an automated version for traders who wish to trade autonomously.

Our 11th one is an automated version of the "Magic Trading Strategy : Most Profitable Indicator : 1 Minute Scalping Strategy Crypto" strategy from "Fx MENTOR US" who doesn't make any official claims but given the indicators he was using, it looked like on the surface that this might actually work. The strategy author uses this on the 1 minute and 3 minute timeframes on mostly FOREX and Heiken Ashi candles but as the title of his strategy indicates is designed for Crypto. So who knows..

To backtest this accurately and get a better picture we resolved the Heiken Ashi bars to standard candlesticks . Even so, I was unable to sustain any consistency in my results on either the 1 or 3 min time frames and both FOREX and Crypto. 10000% Busted.

This strategy uses a combination of 3 open-source public indicators:

Trend Magic by KivancOzbilgic

Squeeze Momentum by LazyBear

Cumulative Delta Volume by LonesomeTheBlue

Trend Magic consists of two main indicators to validate momentum and volatility. It uses an ATR like a trailing Stop to determine the overarching momentum and CCI as a means to validate volatility. Together these are used as the primary indicator in this strategy. When the CCI is above 0 this is confirmation of a volatility event is occurring with affirmation based upon current momentum (ATR).

The CCI volatility indicator gets confirmation by the the Cumulative Delta Volume indicator which calculates the difference between buying and selling pressure. Volume Delta is calculated by taking the difference of the volume that traded at the offer price and the volume that traded at the bid price. The more volume that is traded at the bid price, the more likely there is momentum in the market.

And lastly the Squeeze Momentum indicator which uses a combination of Bollinger Bands, Keltner Channels and Momentum are used to again confirm momentum and volatility. During periods of low volatility, Bollinger bands narrow and trade inside Keltner channels. They can only contract so much before it can’t contain the energy it’s been building. When the Bollinger bands come back out, it explodes higher. When we see the histogram bar exploding into green above 0 that is a clear confirmation of increased momentum and volatile. The opposite (red) below 0 is true when there are low periods. This indicator is used as a means to really determine when there is premium selling plays going on leading to big directional movements again confirming the positive or negative momentum and volatility direction.

If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

Trading Rules

1 - 3 min candles

FOREX or Crypto

Stop loss at swing high/low | 1.5 risk/ratio

Long Condition

Trend Magic line is Blue ( CCI is above 0) and above the current close on the bar

Squeeze Momentum's histogram bar is green/lime

Cumulative Delta Volume line is green

Short Condition

Trend Magic line is Red ( CCI is below 0) and below the current close on the bar

Squeeze Momentum's histogram bar is red/maroon

Cumulative Delta Volume line is peach

Mustang Algo - Momentum Trend Zone Backtest🐎 MUSTANG ALGO - Momentum Trend Zone Strategy

A complete trading system combining MACD momentum analysis with visual trend zones, full backtesting capabilities, and advanced risk management tools.

══════════════════════════════════════════════════════════════════════════

🔹 OVERVIEW

Mustang Algo transforms traditional MACD analysis into a powerful visual trading system. It instantly identifies market bias through colored background zones and provides clear entry/exit signals with customizable stop loss and take profit management.

══════════════════════════════════════════════════════════════════════════

🔹 KEY FEATURES

✅ Visual Trend Zones (Green = Bullish | Red = Bearish)

✅ Clear Buy/Sell Triangles on Chart

✅ Full Backtesting Engine

✅ Multiple Stop Loss Types

✅ Multiple Take Profit Types

✅ Trailing Stop Option

✅ Time Filter for Backtesting

✅ Real-time Info Panel

✅ Customizable Alerts

══════════════════════════════════════════════════════════════════════════

🔹 HOW IT WORKS

The strategy uses a smoothed MACD system to detect trend changes:

- MACD Line (White): Fast EMA minus Slow EMA - shows raw momentum

- Signal Line (Yellow): EMA of MACD - shows smoothed trend direction

- Trend Zone: Changes when the smoothed signal line crosses zero

- Entry Signals: Generated at zone transitions

When the trend line crosses above zero → GREEN zone → BUY signal 🔺

When the trend line crosses below zero → RED zone → SELL signal 🔻

══════════════════════════════════════════════════════════════════════════

🔹 STOP LOSS OPTIONS

🛑 Percentage: Fixed percentage from entry price

🛑 ATR-Based: Dynamic SL based on market volatility

🛑 Fixed Points: Set number of points/pips

🛑 Swing Low/High: Uses recent swing levels as stops

══════════════════════════════════════════════════════════════════════════

🔹 TAKE PROFIT OPTIONS

🎯 Percentage: Fixed percentage target

🎯 ATR-Based: Dynamic TP based on volatility

🎯 Fixed Points: Set number of points/pips

🎯 Risk Reward: Automatic TP based on R:R ratio (e.g., 2:1, 3:1)

══════════════════════════════════════════════════════════════════════════

🔹 TRAILING STOP

📈 Percentage-Based: Trail by a fixed percentage

📈 ATR-Based: Trail using ATR multiplier for dynamic adjustment

══════════════════════════════════════════════════════════════════════════

🔹 SETTINGS

MACD Parameters:

- Fast Length (default: 12)

- Slow Length (default: 26)

- Signal Length (default: 9)

- Trend Smoothing (default: 5)

Risk Management:

- Enable/Disable Stop Loss

- Enable/Disable Take Profit

- Enable/Disable Trailing Stop

- Customize all SL/TP parameters

Visual Options:

- Show/Hide Buy/Sell Triangles

- Show/Hide SL/TP Lines

- Show/Hide Labels

Time Filter:

- Set Start Date for backtest

- Set End Date for backtest

══════════════════════════════════════════════════════════════════════════

🔹 SIGNALS EXPLAINED

🟢 GREEN TRIANGLE (Below Bar):

Bullish zone detected - Consider LONG entry

🔴 RED TRIANGLE (Above Bar):

Bearish zone detected - Consider SHORT entry

🟢 GREEN BACKGROUND:

Currently in bullish trend zone

🔴 RED BACKGROUND:

Currently in bearish trend zone

══════════════════════════════════════════════════════════════════════════

🔹 INFO PANEL

The real-time info panel (top right) displays:

- Current Trend Zone status

- MACD value

- Signal Line value

- Active SL Type

- Active TP Type

══════════════════════════════════════════════════════════════════════════

🔹 ALERTS

Set up alerts for:

🔔 Buy Signals: "🐎 Mustang Algo: BUY Signal on {ticker} at {price}"

🔔 Sell Signals: "🐎 Mustang Algo: SELL Signal on {ticker} at {price}"

══════════════════════════════════════════════════════════════════════════

🔹 BEST PRACTICES

1. Use higher timeframes (1H, 4H, Daily) for more reliable signals

2. Combine with price action and support/resistance levels

3. Adjust ATR multipliers based on asset volatility

4. Use Risk Reward ratio for consistent risk management

5. Backtest on your preferred asset before live trading

══════════════════════════════════════════════════════════════════════════

🔹 RECOMMENDED TIMEFRAMES

⏱️ Scalping: 5M, 15M (more signals, more noise)

⏱️ Day Trading: 1H, 4H (balanced signals)

⏱️ Swing Trading: Daily, Weekly (fewer but stronger signals)

══════════════════════════════════════════════════════════════════════════

🔹 MARKETS

Works on all markets:

📈 Forex

📈 Crypto

📈 Stocks

📈 Indices

📈 Commodities

📈 Futures

══════════════════════════════════════════════════════════════════════════

🐎 RIDE THE TREND WITH MUSTANG ALGO!

══════════════════════════════════════════════════════════════════════════

⚠️ DISCLAIMER

This indicator/strategy is for educational and informational purposes only. It is not financial advice. Trading involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Always use proper risk management, do your own research, and consider consulting a financial advisor before making any trading decisions. Use at your own risk.

══════════════════════════════════════════════════════════════════════════

📝 VERSION HISTORY

v1.0 - Initial Release

- MACD-based trend detection

- Visual trend zones

- Multiple SL/TP options

- Full backtesting support

- Trailing stop functionality

- Time filter

- Info panel

- Alert system

══════════════════════════════════════════════════════════════════════════

💬 FEEDBACK

If you find this strategy useful, please leave a comment or suggestion!

Your feedback helps improve future updates.

🐎 Happy Trading!

EMA 12-26-100 Momentum Strategy# Triple EMA Multi-Signal Momentum Strategy

## 📊 Overview

**Triple EMA Multi-Signal** is a comprehensive trend-following momentum strategy designed specifically for cryptocurrency markets. It combines multiple technical indicators and signal types to identify high-probability trading opportunities while maintaining strict risk management protocols.

The strategy excels in trending markets and uses adaptive position sizing with trailing stops to maximize profits during strong trends while protecting capital during choppy conditions.

## 🎯 Core Algorithm

### Triple EMA System

The strategy employs a three-layer EMA system to identify trend direction and strength:

- **Fast EMA (12)**: Quick response to price changes

- **Slow EMA (26)**: Confirmation of trend direction

- **Trend EMA (100)**: Overall market bias filter

Trades are only taken when all three EMAs align in the same direction, ensuring we trade with the dominant trend.

### Multi-Signal Confirmation (8 Signal Types)

The strategy requires at least 1-2 confirmed signals from multiple independent sources before entering a position:

1. **EMA Crossover** - Fast EMA crossing Slow EMA (primary signal)

2. **MACD Cross** - MACD line crossing signal line (momentum confirmation)

3. **RSI Reversal** - RSI bouncing from oversold/overbought zones

4. **Price Action** - Strong bullish/bearish candles (>60% of range)

5. **Volume Spike** - Above-average volume confirmation

6. **Breakout** - Price breaking 20-period high/low with volume

7. **Pullback to EMA** - Trend continuation after healthy retracement

8. **Bollinger Bounce** - Price bouncing from BB bands

This multi-signal approach significantly reduces false signals and improves win rate.

## 💰 Risk Management

### Position Sizing

- Default: 20-25% of equity per trade

- Adjustable based on risk tolerance

- Smaller positions recommended for leveraged trading

### Stop Loss & Take Profit

- **Stop Loss**: 2.0% (tight control of risk)

- **Take Profit**: 5.5% (2.75:1 reward-to-risk ratio)

- Both levels are fixed at entry to avoid emotional decisions

### Trailing Stop System

- Activates after 1.8% profit

- Trails at 1.3% below current price

- Locks in profits during extended trends

- Automatically adjusts as price moves in your favor

### Maximum Hold Time

- 36-48 hours maximum (configurable)

- Designed to minimize funding rate costs on futures

- Forces position closure to avoid excessive exposure

- Helps maintain capital velocity

## 📈 Key Features

### Trend Filters

- **ADX Filter**: Ensures sufficient trend strength (threshold: 20)

- **EMA Alignment**: All three EMAs must confirm trend direction

- **RSI Boundaries**: Avoids extreme overbought/oversold entries

### Volume Analysis

- Volume must exceed 20-period moving average

- Configurable multiplier (default: 1.0x)

- Helps identify institutional participation

### Automatic Exit Conditions

1. Take Profit target reached

2. Stop Loss triggered

3. Trailing stop activated

4. Trend reversal (EMA cross in opposite direction)

5. Maximum hold time exceeded

## 🎮 Recommended Settings

### For Spot Trading (Conservative)

```

Position Size: 15-20%

Stop Loss: 2.5%

Take Profit: 6.0%

Max Hold: 72 hours

Leverage: 1x

```

### For Futures 3-5x Leverage (Balanced)

```

Position Size: 12-15%

Stop Loss: 2.0%

Take Profit: 5.5%

Max Hold: 36 hours

Trailing: Active

```

### For Aggressive Trading 5-10x (High Risk)

```

Position Size: 8-12%

Stop Loss: 1.5%

Take Profit: 4.5%

Max Hold: 24 hours

ADX Filter: Disabled

```

## 📊 Performance Metrics

### Backtested Results (BTC/USDT 1H, 2 years)

- **Total Return**: ~19% (spot) / ~75% (5x leverage)*

- **Total Trades**: 240-300

- **Win Rate**: 49-52%

- **Profit Factor**: 1.25-1.50

- **Max Drawdown**: ~18-22%

- **Average Trade**: 0.5-3 days

*Leverage results exclude funding rates and real-world slippage

### Optimal Timeframes

- **1 Hour**: Best for active trading (recommended)

- **4 Hour**: More stable, fewer signals

- **15 Min**: High frequency (requires monitoring)

### Best Performing Assets

- BTC/USDT (most tested)

- ETH/USDT

- Major altcoins with good liquidity

- Not recommended for low-cap or illiquid pairs

## ⚙️ How to Use

1. **Add to Chart**: Apply strategy to 1H BTC/USDT chart

2. **Adjust Settings**: Configure risk parameters based on your preference

3. **Review Signals**: Green = Long, Red = Short, labels show signal count

4. **Monitor Performance**: Check strategy tester for detailed statistics

5. **Optimize**: Use strategy optimization to find best parameters for your market

## 🎨 Visual Indicators

The strategy provides clear visual feedback:

- **EMA Lines**: Blue (Fast), Red (Slow), Orange (Trend)

- **BUY/SELL Labels**: Show entry points with signal count

- **Stop/Target Lines**: Red (SL), Green (TP) displayed during active trades

- **Background Color**: Light green (long), light red (short) when in position

- **Info Panel**: Shows current trend, RSI, ADX, and volume status

## ⚠️ Important Notes

### Risk Disclaimer

- This strategy is for educational purposes only

- Past performance does not guarantee future results

- Cryptocurrency trading involves substantial risk

- Only trade with capital you can afford to lose

- Always use proper position sizing and risk management

### Limitations

- Performs poorly in sideways/choppy markets

- Requires sufficient liquidity for best execution

- Backtests do not include:

- Real-world slippage (especially during volatility)

- Funding rates (for perpetual futures)

- Exchange downtime or connection issues

- Emotional trading decisions

### For Futures Trading

If using this strategy on futures with leverage:

- Reduce position size proportionally to leverage

- Account for funding rates (~0.01% per 8h)

- Set max hold time to minimize funding costs

- Use lower leverage (3-5x max recommended)

- Monitor liquidation price carefully

## 🔧 Customization

All parameters are fully customizable:

- EMA periods (fast/slow/trend)

- MACD settings (12/26/9)

- RSI levels (30/70)

- Stop Loss / Take Profit percentages

- Trailing stop activation and offset

- Volume multiplier

- ADX threshold

- Maximum hold time

## 📚 Strategy Logic

The strategy follows this decision tree:

```

1. Check Trend Direction (EMA alignment)

↓

2. Scan for Entry Signals (8 types)

↓

3. Confirm with Filters (ADX, Volume, RSI)

↓

4. Enter Position with Fixed SL/TP

↓

5. Monitor for Exit Conditions:

- TP Hit → Close with profit

- SL Hit → Close with loss

- Trailing Active → Follow price

- Trend Reversal → Close position

- Max Time → Force close

```

## 🎓 Best Practices

1. **Start Conservative**: Use smaller position sizes initially

2. **Track Performance**: Monitor actual vs backtested results

3. **Optimize Regularly**: Market conditions change, adapt parameters

4. **Combine with Analysis**: Don't rely solely on automated signals

5. **Manage Emotions**: Stick to the system, avoid manual overrides

6. **Paper Trade First**: Test on demo before risking real capital

## 📞 Support & Updates

This strategy is actively maintained and updated based on:

- Market condition changes

- User feedback and suggestions

- Performance optimization

- Bug fixes and improvements

## 🏆 Conclusion

Triple EMA Multi-Signal Strategy offers a robust, systematic approach to cryptocurrency trading by combining trend following, momentum indicators, and strict risk management. Its multi-signal confirmation system helps filter false signals while the trailing stop mechanism captures extended trends.

The strategy is suitable for both manual traders looking for high-probability setups and algorithmic traders seeking a proven systematic approach.

**Remember**: No strategy wins 100% of the time. Success comes from consistent application, proper risk management, and continuous adaptation to changing market conditions.

---

*Version: 1.0*

*Last Updated: November 2025*

*Tested on: BTC/USDT, ETH/USDT (1H, 4H timeframes)*

*Recommended Capital: $5,000+ for optimal position sizing*

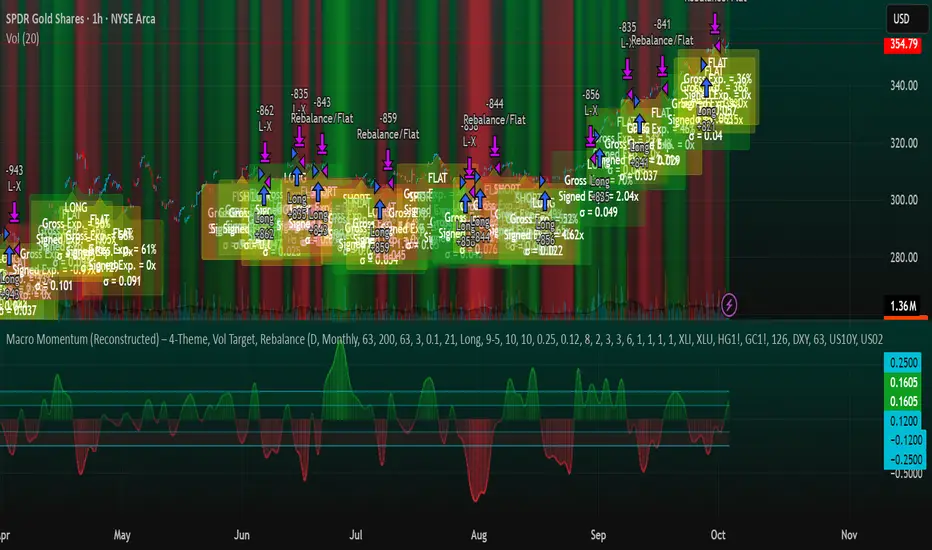

Macro Momentum – 4-Theme, Vol Target, RebalanceMacro Momentum — 4-Theme, Vol Target, Rebalance

Purpose. A macro-aware strategy that blends four economic “themes”—Business Cycle, Trade/USD, Monetary Policy, and Risk Sentiment—into a single, smoothed Composite signal. It then:

gates entries/exits with hysteresis bands,

enforces optional regime filters (200-day bias), and

sizes the position via volatility targeting with caps for long/short exposure.

It’s designed to run on any chart (index, ETF, futures, single stocks) while reading external macro proxies on a chosen Signal Timeframe.

How it works (high level)

Build four theme signals from robust macro proxies:

Business Cycle: XLI/XLU and Copper/Gold momentum, confirmed by the chart’s price vs a long SMA (default 200D).

Trade / USD: DXY momentum (sign-flipped so a rising USD is bearish for risk assets).

Monetary Policy: 10Y–2Y curve slope momentum and 10Y yield trend (steepening & falling 10Y = risk-on; rising 10Y = risk-off).

Risk Sentiment: VIX momentum (bearish if higher) and HYG/IEF momentum (bullish if credit outperforms duration).

Normalize & de-noise.

Optional Winsorization (MAD or stdev) clamps outliers over a lookback window.

Optional Z-score → tanh mapping compresses to ~ for stable weighting.

Theme lines are SMA-smoothed; the final Composite is LSMA-smoothed (linreg).

Decide direction with hysteresis.

Enter/hold long when Composite ≥ Entry Band; enter/hold short when Composite ≤ −Entry Band.

Exit bands are tighter than entry bands to avoid whipsaws.

Apply regime & direction constraints.

Optional Long-only above 200MA (chart symbol) and/or Short-only below 200MA.

Global Direction control (Long / Short / Both) and Invert switch.

Size via volatility targeting.

Realized close-to-close vol is annualized (choose 9-5 or 24/7 market profile).

Target exposure = TargetVol / RealizedVol, capped by Max Long/Max Short multipliers.

Quantity is computed from equity; futures are rounded to whole contracts.

Rebalance cadence & execution.

Trades are placed on Weekly / Monthly / Quarterly rebalance bars or when the sign of exposure flips.

Optional ATR stop/TP for single-stock style risk management.

Inputs you’ll actually tweak

General

Signal Timeframe: Where macro is sampled (e.g., D/W).

Rebalance Frequency: Weekly / Monthly / Quarterly.

ROC & SMA lengths: Defaults for theme momentum and the 200D regime filter.

Normalization: Z-score (tanh) on/off.

Winsorization

Toggle, lookback, multiplier, MAD vs Stdev.

Risk / Sizing

Target Annualized Vol & Realized Vol Lookback.

Direction (Long/Short/Both) and Invert.

Max long/short exposure caps.

Advanced Thresholds

Theme/Composite smoothing lengths.

Entry/Exit bands (hysteresis).

Regime / Execution

Long-only above 200MA, Short-only below 200MA.

Stops/TP (optional)

ATR length and SL/TP multiples.

Theme Weights

Per-theme scalars so you can push/pull emphasis (e.g., overweight Policy during rate cycles).

Macro Proxies

Symbols for each theme (XLI, XLU, HG1!, GC1!, DXY, US10Y, US02Y, VIX, HYG, IEF). Swap to alternatives as needed (e.g., UUP for DXY).

Signals & logic (under the hood)

Business Cycle = ½ ROC(XLI/XLU) + ½ ROC(Copper/Gold), then confirmed by (price > 200SMA ? +1 : −1).

Trade / USD = −ROC(DXY).

Monetary Policy = 0.6·ROC(10Y–2Y) − 0.4·ROC(10Y).

Risk Sentiment = −0.6·ROC(VIX) + 0.4·ROC(HYG/IEF).

Each theme → (optional Winsor) → (robust z or scaled ROC) → tanh → SMA smoothing.

Composite = weighted average → LSMA smoothing → compare to bands → dir ∈ {−1,0,+1}.

Rebalance & flips. Orders fire on your chosen cadence or when the sign of exposure changes.

Position size. exposure = clamp(TargetVol / realizedVol, maxLong/Short) × dir.

Note: The script also exposes Gross Exposure (% equity) and Signed Exposure (× equity) as diagnostics. These can help you audit how vol-targeting and caps translate into sizing over time.

Visuals & alerts

Composite line + columns (color/intensity reflect direction & strength).

Entry/Exit bands with green/red fills for quick polarity reads.

Hidden plots for each Theme if you want to show them.

Optional rebalance labels (direction, gross & signed exposure, σ).

Background heatmap keyed to Composite.

Alerts

Enter/Inc LONG when Composite crosses up (and on rebalance bars).

Enter/Inc SHORT when Composite crosses down (and on rebalance bars).

Exit to FLAT when Composite returns toward neutral (and on rebalance bars).

Practical tips

Start higher timeframes. Daily signals with Monthly rebalance are a good baseline; weekly signals with quarterly rebalances are even cleaner.

Tune Entry/Exit bands before anything else. Wider bands = fewer trades and less noise.

Weights reflect regime. If policy dominates markets, raise Monetary Policy weight; if credit stress drives moves, raise Risk Sentiment.

Proxies are swappable. Use UUP for USD, or futures-continuous symbols that match your data plan.

Futures vs ETFs. Quantity auto-rounds for futures; ETFs accept fractional shares. Check contract multipliers when interpreting exposure.

Caveats

Macro proxies can repaint at the selected signal timeframe as higher-TF bars form; that’s intentional for macro sampling, but test live.

Vol targeting assumes reasonably stationary realized vol over the lookback; if markets regime-shift, revisit volLook and targetVol.

If you disable normalization/winsorization, themes can become spikier; expect more hysteresis band crossings.

What to change first (quick start)

Set Signal Timeframe = D, Rebalance = Monthly, Z-score on, Winsor on (MAD).

Entry/Exit bands: 0.25 / 0.12 (defaults), then nudge until trade count and turnover feel right.

TargetVol: try 10% for diversified indices; lower for single stocks, higher for vol-sell strategies.

Leave weights = 1.0 until you’ve inspected the four theme lines; then tilt deliberately.

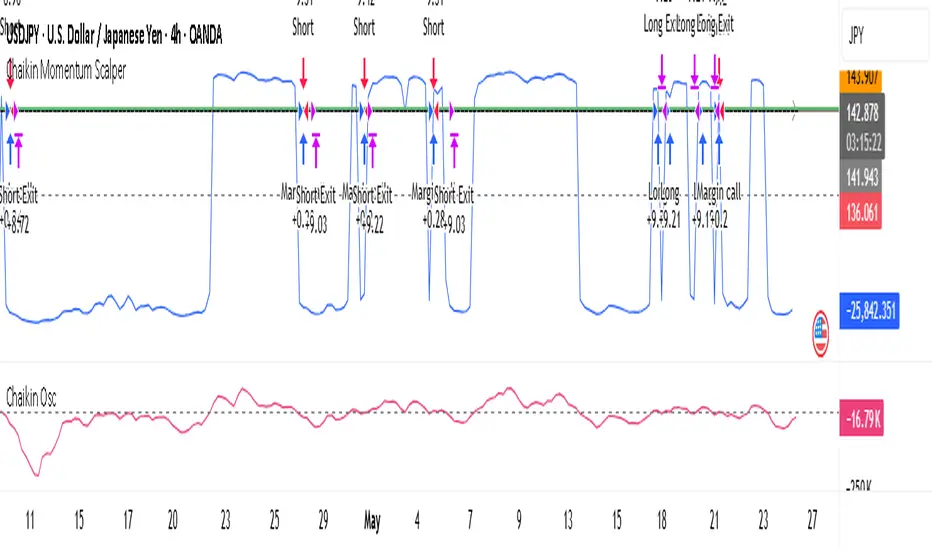

Chaikin Momentum Scalper🎯 Overview

The Chaikin Momentum Scalper is a powerful trading strategy designed to identify momentum shifts in the market and ride the trend for maximum profits. This strategy is ideal for trading the USD/JPY currency pair on a 15-minute chart, making it perfect for high-frequency trading (HFT). Whether you’re starting with a small account of $1,000 or managing a larger portfolio, this strategy can scale to suit your needs.

________________________________________

🔑 How the Strategy Works

Here’s how the Chaikin Momentum Scalper identifies trade opportunities:

1️⃣ Momentum Detection

The core of this strategy is the Chaikin Oscillator, a tool that measures the flow of money into or out of a market. It helps us understand whether buyers (bulls) or sellers (bears) are in control.

• When the indicator crosses above zero, it signals that buying momentum is picking up – a buying opportunity.

• When the indicator crosses below zero, it signals that selling momentum is increasing – a selling opportunity.

2️⃣ Trend Confirmation

We don’t just jump into trades based on momentum alone. We also use a 200-period simple moving average (SMA) to confirm the overall trend.

• If the price is above the SMA, it confirms an uptrend, so we look for buy trades.

• If the price is below the SMA, it confirms a downtrend, so we look for sell trades.

This way, we align our trades with the broader market direction for higher success rates.

3️⃣ Volatility & Risk Management

We use a tool called the Average True Range (ATR) to measure market volatility. This helps us:

• Set a stop-loss (where we’ll exit the trade if the market moves against us) at a safe distance from our entry point.

• Set a take-profit (where we’ll lock in profits) at a target that’s larger than the stop-loss, ensuring a good reward-to-risk ratio.

This approach adapts to the market’s behavior, tightening stops in calmer conditions and widening them when volatility increases.

________________________________________

📈 Why This Strategy Works

✅ It combines momentum and trend-following principles, increasing the chances of trading in the right direction.

✅ It dynamically adjusts risk levels based on market volatility, keeping losses small and profits big.

✅ It’s scalable – perfect for both small accounts (like $1,000) and larger, corporate-sized portfolios.

✅ It has been deep-backtested on USD/JPY 15-minute charts, proving its consistency across different market conditions.

________________________________________

📝 Important Notes

📌 This strategy is best used for USD/JPY on a 15-minute chart, making it great for high-frequency trading while you continue to build and refine your trading system.