Strategy for UT Bot Alerts indicator Using the UT Bot alerts indicator by @QuantNomad, this strategy was designed for showing an example of how this indicator could be used, also, it has the goal to help some people from a group that use to use this indicator for their trading. Under any circumstance I recommend to use it without testing it before in real time.

Backtesting context: 2020-02-05 to 2023-02-25 of BTCUSD 4H by Tvc. Commissions: 0.03% for each entry, 0.03% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 3 indicators are used:

UT Bot Alerts indicator by Quantnomad

One Ema of 200 periods for indicate the trend

Atr stop loss from Gatherio

Trade conditions:

For longs:

Close price is higher than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our long signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as buy (open long position)

The other half will be closed when close price is lower than Atr and Ema from UT Bot cross under Atr. This will be showed as cl buy (close long position)

For shorts:

Close price is lower than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our short signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as sell (open short position)

The other half will be closed when close price is higher than Atr and Ema from UT Bot cross over Atr. This will be showed as cl sell (close short position)

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital

---> Do not forget to deactivate Trades on chart option in style settings for a cleaner look of the chart <---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Strategies for trending markets use to have more looses than wins and it takes a long time to get profits, so do not forget to be patient and consistent !

---> The strategy can still be improved, you can change some parameters depending of the asset and timeframe like risk/reward for taking profits, for break even, also the main parameters of the UT Bot Alerts <----

Cari skrip untuk "backtesting"

NIFTY 50 5mint StrategyThis is an intraday strategy for NIFTY50 Based First candle High and Low breakout.

The strategy takes user inputs for the start and end dates, start and end months, and start and end years, which define the time range to trade. The user can also specify the maximum number of trades to take during the time range and the length of the Exponential Moving Average ( EMA ) used in the strategy

In this strategy, the First candle's high and low are calculated and used as entry and exit points for trades. If the close price breaks above the First candle's high, a buy signal is generated. Conversely, if the close price breaks below the First candle's low, a sell signal is generated.

The strategy uses the Exponential Moving Average ( EMA ) as a filter to close entered positions either long or short, EMA also acts Target. If the close price falls below the EMA, a long position is closed, and if the close price rises above the EMA, a short position is closed or the PreviousCandleClose is above the First candle's high a short position is closed, When the PreviousCandleClose is below the First candle's low a long position is closed, First candle's high act as Stoploss

The strategy limits the number of trades taken within the specified time range, and if the time range is exceeded, all positions are closed.

Finally, the strategy plots the First candle's high and low, EMAs on the chart for visual reference.

Default settings work best with the 5mint candle, you may tweak settings according to your needs.

backtesting helps in interpreting how the trading strategy would have behaved in the past, and forward testing (paper trading) informs the traders how it would perform now.

Investments/swing trading strategy for different assetsStop worrying about catching the lowest price, it's almost impossible!: with this trend-following strategy and protection from bearish phases, you will know how to enter the market properly to obtain benefits in the long term.

Backtesting context: 1899-11-01 to 2023-02-16 of SPX by Tvc. Commissions: 0.05% for each entry, 0.05% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 5 indicators are used:

One Ema of 200 periods

Atr Stop loss indicator from Gatherio

Squeeze momentum indicator from LazyBear

Moving average convergence/divergence or Macd

Relative strength index or Rsi

Trade conditions:

There are three type of entries, one of them depends if we want to trade against a bearish trend or not.

---If we keep Against trend option deactivated, the rules for two type of entries are:---

First type of entry:

With the next rules, we will be able to entry in a pull back situation:

Squeeze momentum is under 0 line (red)

Close is above 200 Ema and close is higher than the past close

Histogram from macd is under 0 line and is higher than the past one

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

For closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Second type of entry:

With the next rules, we will not lose a possible bullish movement:

Close is above 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entry, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

---If we keep Against trend option activated, the rules are the same as the ones above, but with one more type of entry. This is more useful in weekly timeframes, but could also be used in daily time frame:---

Third type of entry:

Close is under 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entries, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Risk management

For calculating the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

If you activate break even using rsi, when rsi crosses under overbought zone break even will be activated. This can work in some assets.

---Important: In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Some assets and timeframes where the strategy has also worked:

BTCUSD : 4H, 1D, W

SPX (US500) : 4H, 1D, W

GOLD : 1D, W

SILVER : 1D, W

ETHUSD : 4H, 1D

DXY : 1D

AAPL : 4H, 1D, W

AMZN : 4H, 1D, W

META : 4H, 1D, W

(and others stocks)

BANKNIFTY : 4H, 1D, W

DAX : 1D, W

RUT : 1D, W

HSI : 1D, W

NI225 : 1D, W

USDCOP : 1D, W

Reinforced RSI - The Quant Science This strategy was designed and written with the goal of showing and motivating the community how to integrate our 'Probabilities' module with their own script.

We have recreated one of the simplest strategies used by many traders. The strategy only trades long and uses the overbought and oversold levels on the RSI indicator.

We added stop losses and take profits to offer more dynamism to the strategy. Then the 'Probabilities' module was integrated to create a probabilistic reinforcement on each trade.

Specifically, each trade is executed, only if the past probabilities of making a profitable trade is greater than or equal to 51%. This greatly increased the performance of the strategy by avoiding possible bad trades.

The backtesting was calculated on the NASDAQ:TSLA , on 15 minutes timeframe.

The strategy works on Tesla using the following parameters:

1. Lenght: 13

2. Oversold: 40

3. Overbought: 70

4. Lookback: 50

5. Take profit: 3%

6. Stop loss: 3%

Time period: January 2021 to date.

Our Probabilities Module, used in the strategy example:

Strategy: Range BreakoutWhat?

In the price action, levels have a significant role to play. Based on the price moving above/below the levels - the underlying instrument shows some price-action in the direction of breakout/breakdown.

There are plenty of ways level can be determined. Levels are the decision point to take a trade or not. But if we make the level derivation complex, then the execution may get hamper.

This strategy script, developed in PineScript v5, is our attempt at solving this problem at the core by providing this simple, yet elegant solution to this problem.

It's essentially an attempt to Trade Simple by drawing logical (horizontal) lines in the chart and take actions, after multiple associated parameters confirmation, on the breakout / breakdown of the levels.

How?

Let us explain how we are drawing the levels.

We are depending on some of the parameters as described below:

Open Range : During intraday movement, often if prices move beyond a particular level, it exibits more movement in the same swing in same direction. We found out, through our back testing for Indian Indices like NSE:NIFTY , NSE:BANKNIFTY or NSE:CNXFINANCE the first 15m (i.e 09:15 AM to 09:30 AM, IST) is one of such range. For Indian stocks, it is 9:15 to 9:45. And for MCX MCX:CRUDEOIL1! it's 5:00 pm to 6:00 pm. There are our first levels.

PDHCL : Previous Day High, Close, Low. This is our next level

VWAP : The rolling VWAP (volume weighted average price)

In the breakout/breakdown of the Open Range and Previous Day High/Low, we are taking the trade decisions as follows using CEST principle:

C onditions :

If current bar's (say you are in 5m timeframe) closing is broken out the Open Range High or Previous Day High, taken a Buy/Long decision (let's say buying a Call Option CE or selling a Put Option PE or buying the future or cash).

If current bar's (say you are in 5m timeframe) closing is broken down the Open Range Low or Previous Day Low, taken a Sell/Short decision (let's say buying a Put Option CE or selling a Call Option PE or selling the future or cash).

Additionally, and optionally (default ON, one can turn off): we are checking various other associated multiple confirmations as follows:

1. Momentum : Checking 14-period RSI value is more than 50 or less than 50 (all parameters like period, OB, OS ranges are configurable through settings)

2. Current bar's volume is more than the last 20 bars volume average. How much more - that multiplier is also configurable. (default is 1)

3. The breakout candle is bullish (green) or bearish (red).

E ntry :

All of these happens only on the closing of the candle . Means: Non Repainting! .

Clearly in the chart we are showing as green up arrow BO (breakout for buy) and red down arrow BD (breakdown for sell) to take your decision process smooth.

So, on the closing of the decision BO/BD candle we are entering the trade (with a thumping heart and nail biting ...)

S top Loss :

We are relying on the time tasted (last 40 years) mechanism of Average True Range (ATR) of default 14 period. This default period is also configurable.

So for Long trades: the 14 period ATR low band is the SL.

For Short trades: the 14 period ATR high band is the SL.

T arget :

We are depending on the thump rule of 1:2 Risk Reward. It's simple and effective. No fancy thing. We are closing the trade on double the favorable price movement compared to the SL placed. Of course, this RR ratio is confiurable from the settings, as usual.

What's Unqiue in it?

The utter simplicity of this trading mechanism. No fancy things like complex chart pattern, OI data, multiple candlestick patterns, Order flow analysis etc.

Simple level determination,

Marking clearly in the chart.

Making each parameter configurable in Settings and showing tooltip adjacent to the parameter to make you understand it better for your customization,

Wait for the candle close, thus eliminating the chances of repainting menace (as much as possible)

Additional momentum and volume check to trade entry confirmation.

Works with normal candlestick (nothing special ones like HA ...)

Showing everything as a Summary Table (which, again can be turned off optionally) overlaying at the bottom-right corner of the chart,

Optionally the Summary Table can be configured to alert you back (say you get it notified in your email or SMS).

That way, a single, simple, effective trade setup will ease your journey as smooth sail as possible.

Mentions

There are plenty of friends from whom time to time we borrowed some of the ideas while working closely together over last one year.

From tradingview community, we took the spirit of @zzzcrypto123 awesome work done long back (in 2020) as the indicator "ORB - Opening Range Breakout". (We tried to reach him for his explicit consent, unable to catch hold of him).

Some other publicly available materials we have consulted to get the additional checks (like RSI, volume).

Lat word

Use it please and thank you for your constant patronage in following us in this awesome platform. Let's keep growing together.

Disclaimer :

This piece of software does not come up with any warrantee or any rights of not changing it over the future course of time.

We are not responsible for any trading/investment decision you are taking out of the outcome of this indicator.

Fair Value Strategy UltimateThis is a strategy using an index's (SPX, NDX, RUT) Fair Value derived from Net Liquidity.

Net Liquidity function is simply: Fed Balance Sheet - Treasury General Account - Reverse Repo Balance

Formula for calculating the fair value of and Index using Net Liquidity looks like this: net_liquidity/1000000000/scalar - subtractor

The Index Fair Value is then subtracted from the Index value which creates an oscillating diff value.

When diff is greater than the overbought threshold, Index is considered overbought and we go short/sell.

When diff is less than the oversold signal, Index is considered oversold and we cover/buy.

The net liquidity values I calculate outside of TradingView. If you'd like the strategy to work for future dates, you'll need to update the reference to my NetLiquidityLibrary , which I update daily.

Parameters:

Index: SPX, NDX, RUT

Strategy: Short Only, Long Only, Long/Short

Inverse (bool): check if using an inverse ETF to go long instead of short.

Scalar (float)

Subtractor (int)

Overbought Threshold (int)

Oversold Threshold (int)

Start After Date: When the strategy should start trading

Close Date: Day to close open trades. I just like it to get complete results rather than the strategy ending with open trades.

Optimal Parameters:

I've optimized the parameters for each index using the python backtesting library and they are as follows =>

SPX

Scalar: 1.1

Subtractor: 1425

OB Threshold: 0

OS Threshold: -175

NDX

Scalar: 0.5

Subtractor: 250

OB Threshold: 0

OS Threshold: -25

RUT

Scalar: 3.2

Subtractor: 50

OB Threshold: 25

OS Threshold: -25

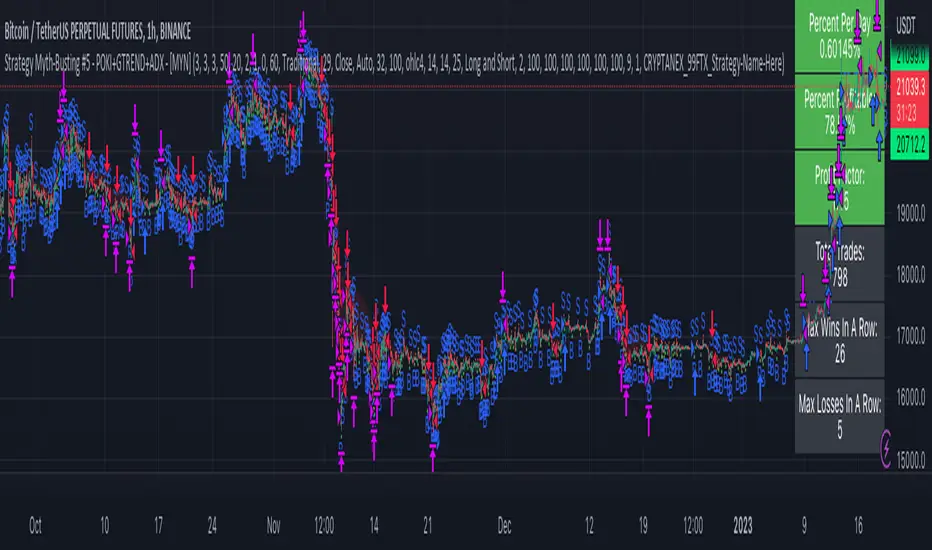

Strategy Myth-Busting #5 - POKI+GTREND+ADX - [MYN]This is part of a new series we are calling "Strategy Myth-Busting" where we take open public manual trading strategies and automate them. The goal is to not only validate the authenticity of the claims but to provide an automated version for traders who wish to trade autonomously.

Our fifth one we are automating is one of the strategies from "The Best 3 Buy And Sell Indicators on Tradingview + Confirmation Indicators ( The Golden Ones ))" from "Online Trading Signals (Scalping Channel)". No formal backtesting was done by them and resuructo messaged me asking if we could validate their claims.

Originally, we mimic verbatim the settings Online Trading Signals was using however weren't getting promising results. So before we stopped there we thought we might want to see if this could be improved on. So we adjusted the Renko Assignment modifier from ATR to Traditional and adjusted the value to be higher from 30 to 47. We also decided to try adding another signal confirmation to eliminate some of the ranged market conditions so we choose our favorite, ADX . Also, given we are using this on a higher time-frame we adjusted the G-Channel Trend detection source from close to OHLC4 to get better average price action indication and more accurate trend direction.

This strategy uses a combination of 2 open-source public indicators:

poki buy and sell Take profit and stop loss by RafaelZioni

G-Channel Trend Detection by jaggedsoft

Trading Rules

15m - 4h timeframe. We saw best results at the recommended 1 hour timeframe.

Long Entry:

When POKI triggers a buy signal

When G-Channel Trend Detection is in an upward trend (Green)

ADX Is above 25

Short Entry:

When POKI triggers a sell signal

When G-Channel Trend Detection is in an downward trend (red)

ADX Is above 25

If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

Super 8 - 30M BTCWelcome to Super 8, the ultimate automatic trading script for Pine!

This bad boy is designed to go both long and short, and it's equipped with all the tools you need to maximize your profits. Whether you're looking to take profit, set a trailing stop, or protect yourself with a stop loss, Super 8 has you covered.

But that's not all! Super 8 is also loaded with 8 powerful indicators to help you make informed decisions. We've got the EMA, ADX, SAR, MACD, VOLUME, BOLLINGER BANDS, DONCHIAN, and ATR all working together to give you the best possible trading experience.

And if you want to take it to the next level, Super 8 also has a feature that lets you use stepped entries in normal mode or incremental 1,2,3,... to improve your average price. Plus, if you're using trailing stop, you can activate the Backtest precision to use lower timeframes.

But what's in a name? Super 8 is called that because it's just that... super! It's tailored specifically for the OKX:BTCUSDT.P pair, so you know you're getting the best possible results. it's highly adjustable and can be used with any other pair. So no matter what market you're trading in, Super 8 has got you covered.

So if you want to level up your trading game, give Super 8 a try. You won't be disappointed.

Certain Risks of Live Algorithmic Trading:

Backtesting Cannot Assure Actual Results.

The relevant market might fail or behave unexpectedly.

Your broker may experience failures in its infrastructure, fail to execute your orders in a correct or timely fashion or reject your orders.

The system you use for generating trading orders, communicating those orders to your broker, and receiving queries and trading results from your broker may fail.

Time lag at various point in live trading might cause unexpected behavior.

The systems of third parties in addition to those of the provider from which we obtain various services, your broker, and the applicable securities market may fail or malfunction.

Simple SuperTrend Strategy for BTCUSD 4HHello guys!, If you are a swing trader and you are looking for a simple trend strategy, you should check this one. Based in the supertrend indicator, this strategy will help you to catch big movements in BTCUSD 4H and avoid losses as much as possible in consolidated situations of the market

This strategy was designed for BTCUSD in 4H timeframe

Backtesting context: 2020-01-02 to 2023-01-05 (The strategy has also worked in previous years)

Trade conditions:

Rules are actually simple, the most important thing is the risk and position management of this strategy

For long:

Once Supertrend changes from a downtrend to a uptrend, you enter into a long position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Now, just will be there two situations:

Once Supertrend changes from a uptrend to a downtrend, you close the other half of the initial long position.

If price goes againts the position, the position will be closed due to breakeven.

For short:

Once Supertrend changes from a uptrend to a downtrend, you enter into a short position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Like in the long position, just will be there two situations:

Once Supertrend changes from a downtrend to a uptrend, you close the other half of the initial short position.

If price goes againts the position, the position will be closed due to breakeven.

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, supertrend or positions.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

Signals meanings:

L for long position. CL for close long position.

S for short position. CS for close short position.

Tp for take profit (it also appears when the position is closed due to stop loss, this due to the script uses two kind of positions)

Exit due to break even or due to stop loss

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

The amount of trades closed in the backtest are not exactly the real ones. If you want to know the real ones, go to settings and change % of trade for first take profit to 100 for getting the real ones. In the backtest, the real amount of opened trades was of 194.

Indicators used:

Supertrend

Atr stop loss by garethyeo

This is the fist strategy that I publish in tradingview, I will be glad with you for any suggestion, support or advice for future scripts. Do not doubt in make any question you have and if you liked this content, leave a boost. I plan to bring more strategies and useful content for you!

ATR_RSI_Strategy v2 with no repaint [liwei666]🎲 Overview

🎯 this is a optimized version based on ATR_RSI_Strategy with no-repaint.

Sharpe ratio: 1.4, trade times: 116 ,

trade symbol: BINANCE:BTCUSDTPERP 15M

you can get same backtesting result with the correct settings.

🎲 Strategy Logic

🎯 the core logic is quite simple, use ATR and RSI and SMA

1. when price is in high volatility ( atr_value > atr_ma);

2. wait for a break signal (rsi_value > rsi_buy or rsi_value < rsi_sell);

3. entry Long or Short,use trailing stop-loss to max security and percent TP to keep profit.

🎲 Settings

🎯 there are 7 input properties in script, but I only finetune 4 of them ( bold field below ),

you may change other parameter to get better result by yourself.

atr_length: length to get atr value

atr_ma_length : length of smoothing atr value

atr_ma_norm_min : atr_ma normalized min value, filter high volatility ranges

atr_ma_norm_max : atr_ma normalized max value, filter high volatility ranges

rsi_length : length to get rsi value

rsi_entry: 50 +/- rsi_entry to get entry threshold

trailing_percent: trailing stop-loss percent

🎲 Usage

🎯 the commission set to 0.05% , part of exchange the commission is less than 0.05% in reality,

but I will still use 0.05% in my next script.

🎯 this script use 50% of equity to size positions follow general script position,

you can adjust the value to fix size or 100% of equity to compare result with other strategy,

but I still suggest you use 5-10% of equity for each strategy in reality.

🎯any questions please comment below. if there are any words violate House Rule, please tell me below and i will revise immediately

don't want be hiddened again 😂😂

Additionally, I plan to publish 20 profitable strategies in 2023;

let‘s witness it together!

Hope this strategy will be usefull for you :)

enjoy! 🚀🚀🚀

VWMA/SMA 3Commas BotThis strategy utilizes two pairs of different Moving Averages, two Volume-Weighted Moving Averages (VWMA) and two Simple Moving Averages (SMA).

There is a FAST and SLOW version of each VWMA and SMA.

The concept behind this strategy is that volume is not taken into account when calculating a Simple Moving Average.

Simple Moving Averages are often used to determine the dominant direction of price movement and to help a trader look past any short-term volatility or 'noise' from price movement, and instead determine the OVERALL direction of price movement so that one can trade in that direction (trend-following) or look for opportunities to trade AGAINST that direction (fading).

By comparing the different movements of a Volume-Weighted Moving Average against a Simple Moving Average of the same length, a trader can get a better picture of what price movements are actually significant, helping to reduce false signals that might occur from only using Simple Moving Averages.

The practical applications of this strategy are identifying dominant directional trends. These can be found when the Volume Weighted Moving Average is moving in the same direction as the Simple Moving Average, and ideally, tracking above it.

This would indicate that there is sufficient volume supporting an uptrend or downtrend, and thus gives traders additional confirmation to potentially look for a trade in that direction.

One can initially look for the Fast VWMA to track above the Fast SMA as your initial sign of bullish confirmation (reversed for downtrending markets). Then, when the Fast VWMA crosses over the Slow SMA, one can determine additional trend strength. Finally, when the Slow VWMA crosses over the Slow SMA, one can determine that the trend is truly strong.

Traders can choose to look for trade entries at either of those triggers, depending on risk tolerance and risk appetite.

Furthermore, this strategy can be used to identify divergence or weakness in trending movements. This is very helpful for identifying potential areas to exit one's trade or even look for counter-trend trades (reversals).

These moments occur when the Volume-Weighted Moving Average, either fast or slow, begins to trade in the opposite direction as their Simple Moving Average counterpart.

For instance, if price has been trending upwards for awhile, and the Fast VWMA begins to trade underneath the Fast SMA, this is an indication that volume is beginning to falter. Uptrends need appropriate volume to continue moving with momentum, so when we see volume begin to falter, it can be a potential sign of an upcoming reversal in trend.

Depending on how quickly one wants to enter into a movement, one could look for crosses of the Fast VWMA under/over the Fast SMA, crosses of the Fast VWMA over/under the Slow SMA, or crosses over/under of the Slow VWMA and the Slow SMA.

This concept was originally published here on TradingView by ProfitProgrammers.

Here is a link to his original indicator script:

I have added onto this concept by:

converting the original indicator into a strategy tester for backtesting

adding the ability to conveniently test long or short strategies, or both

adding the ability to calculate dynamic position sizes

adding the ability to calculate dynamic stop losses and take profit levels using the Average True Range

adding the ability to exit trades based on overbought/oversold crosses of the Stochastic RSI

conveniently switch between different thresholds or speeds of the Moving Average crosses to test different strategies on different asset classes

easily hook this strategy up to 3Commas for automation via their DCA bot feature

Full credit to ProfitProgrammers for the original concept and idea.

Any feedback or suggestions are greatly appreciated.

I11L - Meanreverter 4h---Overview---

The system buys fear and sells greed.

Its relies on a Relative Strength Index (RSI) and moving averages (MA) to find oversold and overbought states.

It seems to work best in market conditions where the Bond market has a negative Beta to Stocks.

Backtests in a longer Timeframe will clearly show this.

---Parameter---

Frequency: Smothens the RSI curve, helps to "remember" recent highs better.

RsiFrequency: A Frequency of 40 implies a RSI over the last 40 Bars.

BuyZoneDistance: Spacing between the different zones. A wider spacing reduces the amount of signals and icnreases the holding duration. Should be finetuned with tradingcosts in mind.

AvgDownATRSum: The multiple of the Average ATR over 20 Bars * amount of opentrades for your average down. I choose the ATR over a fixed percent loss to find more signals in low volatility environments and less in high volatility environments.

---Some of my thoughts---

Be very careful about the good backtesting performance in many US-Stocks because the System had a favourable environment since 1970.

Be careful about the survivorship bias as well.

52% of stocks from the S&P500 were removed since 2000.

I discount my Annual Results by 5% because of this fact.

You will find yourself quite often with very few signals because of the high market correlation.

My testing suggests that there is no expected total performance difference between a signal from a bad and a signal from a good market condition but a higher volatility.

I am sharing this strategy because i am currently not able to implement it as i want to and i think that meanreversion is starting to be taken more serious by traders.

The challange in implementing this strategy is that you need to be invested 100% of the time to retrieve the expected annual performance and to reduce the fat tail risk by market crashes.

Cipher_B (Finandy support)In this version of the script you can force to cancel your position after some amount of time indepedently on price action. For example, your bot open a short position with SL=1% and TP=2.4% but price did not reach any of this level over the course of to say 8 hours. In this case, position will be closed regardless of the price.

Other interesting features are volume and slope filters. Slope is essentially a derivative of price action. If you don't like to buy your instrument under high volatility, for example, if a trend goes down too fast then you can filter long position which could be opened according to the strategy. Same thing for volume filter. If the volume is too high/too low, you might want to escape such setup in your trading strategy.

Moreover, you can tune price shift for opening position. To say, if you believe that the signal for opening position comes too early everytime, you can force the strategy to buy at 1% lower price than the current price when the signal comes. Similar logic for short: open position price will be always higher than the price of the signal. If the price did not reach such level then position will be automatically cancel with a new signal arrival. Check the backtesting results to understand better the logic.

Strategy Myth-Busting #20 - HalfTrend+HullButterfly - [MYN]#20 on the Myth-Busting bench, we are automating the " I Found Super Easy 1 Minute Scalping System And Backtest It 100 Times " strategy from " Jessy Trading " who claims 30.58% net profit over 100 trades in a couple of weeks with a 51% win rate and profit factor of 1.56 on EURUSD .

This one surprised us quite a bit. Despite the title of this strategy indicating this is on the 1 min timeframe, the author demonstrates the backtesting manually on the 5 minute timeframe. Given the simplicity of this strategy only incorporating a couple of indicators, it's robustness being able to be profitable in both low and high timeframes and on multiple symbols was quite refreshing.

The 3 settings which we need to pay most attention to here is the Hull Butterfly length, HalfTrend amplitude and the Max Number Of Bars Between Hull and HalfTrend Trigger. Depending on the timeframe and symbol, these settings greatly impact the performance outcomes of the strategy. I've listed a couple of these below.

And as always, If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

This strategy uses a combination of 3 open-source public indicators:

Hull Butterfly Oscillator by LuxAlgo

HalfTrend by Everget

Trading Rules

5 min candles but higher / lower candles work too.

Stop loss at swing high/low

Take Profit 1.5x the risk

Long

Hull Butterfly gives us green column, Wait for HalfTrend to present an up arrow and enter trade.

Short

Hull Butterfly gives us a red column , Wait for HalfTrend to present a down arrow and enter trade.

Alternative Trading Settings for different time frames

1 Minute Timeframe

Move the Hull Butterfly length from the default 11 to 9

Move the HalfTrend Amplitude from the default 2 to 1

Enabling ADX Filter with a 25 threshold

2 Hour Timeframe

Move the HalfTrend Amplitude from the default 2 to 1

Laddered Take Profits from 14.5% to 19% with an 8% SL

Linear EDCA v1.2Strategy Description:

Linear EDCA (Linear Enhanced Dollar Cost Averaging) is an enhanced version of the DCA fixed investment strategy. It has the following features:

1. Take the 1100-day SMA as a reference indicator, enter the buy range below the moving average, and enter the sell range above the moving average

2. The order to buy and sell is carried out at different "speed", which are set with two linear functions, and you can change the slope of the linear function to achieve different trading position control purposes

3. This fixed investment is a low-frequency strategy and only works on a daily level cycle

----------------

Strategy backtest performance:

BTCUSD (September 2014~September 2022): Net profit margin 26378%, maximum floating loss 47.12% (2015-01-14)

ETHUSD (August 2018~September 2022): Net profit margin 1669%, maximum floating loss 49.63% (2018-12-14)

----------------

How the strategy works:

Buying Conditions:

The closing price of the day is below the 1100 SMA, and the ratio of buying positions is determined by the deviation of the closing price from the moving average and the buySlope parameter

Selling Conditions:

The closing price of the day is above the 1100 SMA, and the ratio of the selling position is determined by the deviation of the closing price and the moving average and the sellSlope parameter

special case:

When the sellOffset parameter>0, it will maintain a small buy within a certain range above the 1100 SMA to avoid prematurely starting to sell

The maximum ratio of a single buy position does not exceed defInvestRatio * maxBuyRate

The maximum ratio of a single sell position does not exceed defInvestRatio * maxSellRate

----------------

Version Information:

Current version v1.2 (the first officially released version)

v1.2 version setting parameter description:

defInvestRatio: The default fixed investment ratio, the strategy will calculate the position ratio of a single fixed investment based on this ratio and a linear function. The default 0.025 represents 2.5% of the position

buySlope: the slope of the linear function of the order to buy, used to control the position ratio of a single buy

sellSlope: the slope of the linear function of the order to sell, used to control the position ratio of a single sell

sellOffset: The offset of the order to sell. If it is greater than 0, it will keep a small buy within a certain range to avoid starting to sell too early

maxSellRate: Controls the maximum sell multiple. The maximum ratio of a single sell position does not exceed defInvestRatio * maxSellRate

maxBuyRate: Controls the maximum buy multiple. The maximum ratio of a single buy position does not exceed defInvestRatio * maxBuyRate

maPeriod: the length of the moving average, 1100-day MA is used by default

smoothing: moving average smoothing algorithm, SMA is used by default

useDateFilter: Whether to specify a date range when backtesting

settleOnEnd: If useDateFilter==true, whether to close the position after the end date

startDate: If useDateFilter==true, specify the backtest start date

endDate: If useDateFilter==true, specify the end date of the backtest

investDayofweek: Invest on the day of the week, the default is to close on Monday

intervalDays: The minimum number of days between each invest. Since it is calculated on a weekly basis, this number must be 7 or a multiple of 7

The v1.2 version data window indicator description (only important indicators are listed):

MA: 1100-day SMA

RoR%: floating profit and loss of the current position

maxLoss%: The maximum floating loss of the position. Note that this floating loss represents the floating loss of the position, and does not represent the floating loss of the overall account. For example, the current position is 1%, the floating loss is 50%, the overall account floating loss is 0.5%, but the position floating loss is 50%

maxGain%: The maximum floating profit of the position. Note that this floating profit represents the floating profit of the position, and does not represent the floating profit of the overall account.

positionPercent%: position percentage

positionAvgPrice: position average holding cost

--------------------------------

策略说明:

Linear EDCA(Linear Enhanced Dollar Cost Averaging)是一个DCA定投策略的增强版本,它具有如下特性:

1. 以1100日SMA均线作为参考指标,在均线以下进入定买区间,在均线以上进入定卖区间

2. 定买和定卖以不同的“速率”进行,它们用两条线性函数设定,并且你可以通过改变线性函数的斜率,以达到不同的买卖仓位控制的目的

3. 本定投作为低频策略,只在日级别周期工作

----------------

策略回测表现:

BTCUSD(2014年09月~2022年09月):净利润率26378%,最大浮亏47.12%(2015-01-14)

ETHUSD(2018年08~2022年09月):净利润率1669%,最大浮亏49.63%(2018-12-14)

----------------

策略工作原理:

买入条件:

当日收盘价在 1100 SMA 之下,由收盘价和均线的偏离度,以及buySlope参数决定买入仓位比例

卖出条件:

当日收盘价在 1100 SMA之上,由收盘价和均线的偏离度,以及sellSlope参数决定卖出仓位比例

特例:

当sellOffset参数>0,则在 1100 SMA以上一定范围内还会保持小幅买入,避免过早开始卖出

单次买入仓位比例最大不超过 defInvestRatio * maxBuyRate

单次卖出仓位比例最大不超过 defInvestRatio * maxSellRate

----------------

版本信息:

当前版本v1.2(第一个正式发布的版本)

v1.2版本设置参数说明:

defInvestRatio: 默认定投比例,策略会根据此比例和线性函数计算得出单次定投的仓位比例。默认0.025代表2.5%仓位

buySlope: 定买的线性函数斜率,用来控制单次买入的仓位倍率

sellSlope: 定卖的线性函数斜率,用来控制单次卖出的仓位倍率

sellOffset: 定卖的偏移度,如果大于0,则在一定范围内还会保持小幅买入,避免过早开始卖出

maxSellRate: 控制最大卖出倍率。单次卖出仓位比例最大不超过 defInvestRatio * maxSellRate

maxBuyRate: 控制最大买入倍率。单次买入仓位比例最大不超过 defInvestRatio * maxBuyRate

maPeriod: 均线长度,默认使用1100日MA

smoothing: 均线平滑算法,默认使用SMA

useDateFilter: 回测时是否要指定日期范围

settleOnEnd: 如果useDateFilter==true,在结束日之后是否平仓所持有的仓位平仓

startDate: 如果useDateFilter==true,指定回测开始日期

endDate: 如果useDateFilter==true,指定回测结束日期

investDayofweek: 每次在周几定投,默认在每周一收盘

intervalDays: 每次定投之间的最小间隔天数,由于是按周计算,所以此数字必须是7或7的倍数

v1.2版本数据窗口指标说明(只列出重要指标):

MA:1100日SMA

RoR%: 当前仓位的浮动盈亏

maxLoss%: 仓位曾经的最大浮动亏损,注意此浮亏代表持仓仓位的浮亏情况,并不代表整体账户浮亏情况。例如当前仓位是1%,浮亏50%,整体账户浮亏是0.5%,但仓位浮亏是50%

maxGain%: 仓位曾经的最大浮动盈利,注意此浮盈代表持仓仓位的浮盈情况,并不代表整体账户浮盈情况。

positionPercent%: 仓位持仓占比

positionAvgPrice: 仓位平均持仓成本

Catching the Bottom (by Coinrule)This script utilises the RSI and EMA indicators to enter and close the trade.

The relative strength index (RSI) is a momentum indicator used in technical analysis. RSI measures the speed and magnitude of a security's recent price changes to evaluate overvalued or undervalued conditions in the price of that security. The RSI is displayed as an oscillator (a line graph) on a scale of zero to 100. The RSI can do more than point to overbought and oversold securities. It can also indicate securities that may be primed for a trend reversal or corrective pullback in price. It can signal when to buy and sell. Traditionally, an RSI reading of 70 or above indicates an overbought situation. A reading of 30 or below indicates an oversold condition.

An exponential moving average (EMA) is a type of moving average (MA) that places a greater weight and significance on the most recent data points. The exponential moving average is also referred to as the exponentially weighted moving average. An exponentially weighted moving average reacts more significantly to recent price changes than a simple moving average simple moving average (SMA), which applies an equal weight to all observations in the period.

The strategy enters and exits the trade based on the following conditions.

ENTRY

RSI has a decrease of 3.

RSI <40.

EMA100 has crossed above the EMA50.

EXIT

RSI is greater than 65.

EMA9 has crossed above EMA50.

This strategy is back tested from 1 April 2022 to simulate how the strategy would work in a bear market and provides good returns.

Pairs that produce very strong results include ETH on the 5m timeframe, BNB on 5m timeframe, XRP on the 45m timeframe, MATIC on the 30m timeframe and MATIC on the 2H timeframe.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

RSI Buy & Sell Trading ScriptThis is my first attempt at a trading script using the RSI indicator for Buy & Sell signals (so please be nice but would appreciate any constructive comments).

Starting with $100 initial capital and using 10% per trade

You can select which month the backtesting starts

There is also a monthly table (sorry can’t remember who I got this from) that shows the total monthly profits, but you’ll need to turn it on by going into settings, Properties and in the Recalculate section tick the “On every tick” box

It should do the following:

Open Buy order if the RSI > 68 and the current Moving Average is greater than the previous Moving average

• TP1 = 50% of Order at 0.4%

• TP2 = 50% of order at 0.8%

• SL = 2% below entry

• Close Buy order if the RSI < 30

Open Sell order if the RSI < 28 and the current Moving Average is less than the previous Moving average

• TP1 = 50% of Order at 0.4%

• TP2 = 50% of order at 0.8%

• SL = 2% above entry

• Close Buy order if the RSI < 60

I would like to build on this if you have any ideas/ code that could help like the following:

• Move the SL to break even when it hits TP1

• Move the SL to TP1 when TP2 hits

• Moving take profit code so I can let the some of the trade stay in play (activate if it hits 1% profit and close trade if price retracts 0.5%)

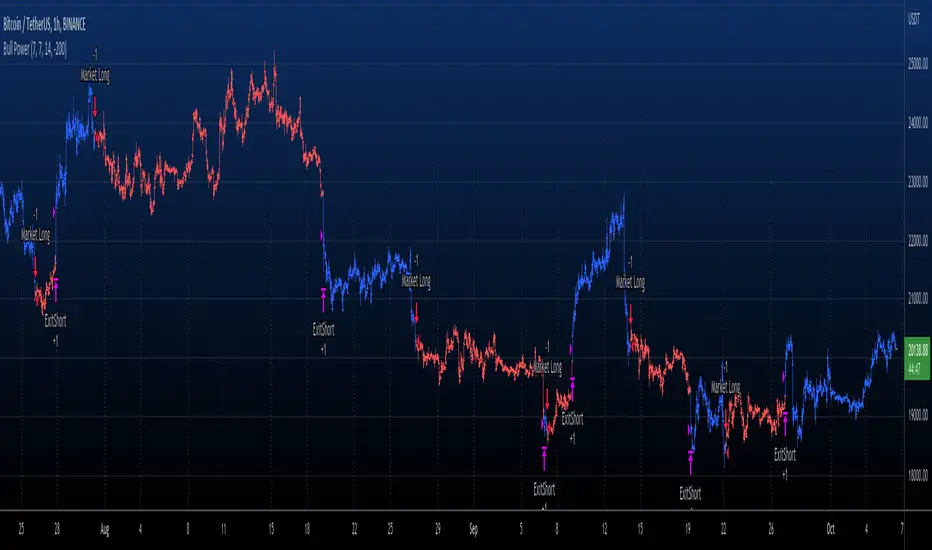

Elder Ray (Bull Power) TP and SL Developed by Dr Alexander Elder, the Elder-ray indicator measures buying

and selling pressure in the market. The Elder-ray is often used as part

of the Triple Screen trading system but may also be used on its own.

Dr Elder uses a 13-day exponential moving average (EMA) to indicate the

market consensus of value. Bull Power measures the ability of buyers to

drive prices above the consensus of value. Bear Power reflects the ability

of sellers to drive prices below the average consensus of value.

Bull Power is calculated by subtracting the 13-day EMA from the day's High.

Bear power subtracts the 13-day EMA from the day's Low.

WARNING:

- For purpose educate only

- This script to change bars colors.

HHLL Strategy This is simple Highest high and Lowest low strategy.

Buy when break HH+offset

Sell when break LL+offset

Offset = (HH-LL)/2

How to use Leverage in PineScriptI believe there are many friends who have been confused by the leverage problem of TradingView strategy, when backtesting, it is always unable to bring its own leverage, so it is impossible to do leverage sustained compounding, this key point, and many friends are looking forward to solve. In particular, the default_qty_value = 100, where 100 is the upper limit.

Here I have used the official RSI strategy for demonstration, using the qty to place orders. Through strategy.equity, leverage and close price, and rounding, directly calculate the specific number of contracts need to be opened.

I hope you can enjoy solving the leverage problem, and I look forward to your pointing out my problems and shortcomings to me. Thank you.

X48 - Strategy | MA Type Cross + TPSL | Future&Spot | V.2Thank You For Open Source Code, This Strategy Ref. By 1.Simple Strategy Like MA Crossover For Long/Short or Spot Trade, 2. CDC Action Zone V.2 for BarPaint

This Strategy Mixing With MA Crossover Strategy and BarPaint By CDC Action Zone and TP/SL by Varbara

### How To Use Strategy : Setting EMA/SMA Crossover EMA/SMA, Any Value If You Want

For Long Position : Cross Up

For Short Position : Cross Down

Can Use With Spot Trade : Cross Up = Buy, Cross Down = Sell

TP/SL When Your OrderSize Change From any % Of Your TP/SL Value

### In Strategy Setting

Intitial Capital = Ex. 200

Order Size = Should Be Money Management Not Use 100% of Capital Ex. 10% of Capital (200$) = Order Size 20$

StopLoss and Take Profit = If You Run Trend TF 4H+ or 1D+ You Can Change TP% = 1,000% for nonlimit and Stop Loss 5 - 20% from your order size

Ex. Stoploss 15% = OrderSize / 100 x %SL = 20$/100 x 15% = 3$ Loss from order size 20$ (if you not set stop loss.)

Base Currency = (Your Currency) # Ex. USD

Commission = (Your Trading Fee) # Ex. Future Fee Can Check At Binance Fee Rate > www.binance.com > Choose Your Fee Type, Ex. USD M Future (Regular User) = 0.02 (Maker), 0.04 (Taker)

Commission Symbol Type = % # (Ref. By Binance Fee Rate)

### Notice ####

Default Setting It's Realistic From Normal Life Ex. Capital 200$ / Ordersize 20$ (10%)/ Commission 0.1% (Buy+Sell) / Slippage = 2 / TP = 1000% (nonlimit) / SL = 15%/OrderSize

Low Risk But High Return, Good Luck

### Bot Auto Trade by X4815162342 ###

if you wanna try my bot auto trade X48-3in1-bot : Contact My Line ID : x4815x

Full Command Alert For This Strategy If You Wanna See It's

'{"ex":"'+markettype+'","side": "'+longcommand+'", "amount": "@{{strategy.order.contracts}}", "symbol": "{{ticker}}", "passphrase": "'+passphrase+'","leverage":"'+str.tostring(leveragex)+'"}'

'{"ex":"'+markettype+'","side": "'+shortcommand+'", "amount": "@{{strategy.order.contracts}}", "symbol": "{{ticker}}", "passphrase": "'+passphrase+'","leverage":"'+str.tostring(leveragex)+'"}'

But Easy Than Full Command Just Use Thisssssss !! Strategy Be Manage Auto Long and Short or TPSL Position

You Don't Do Anything Just Use This Message to Alerts Message

{{strategy.order.alert_message}}

### If you don't use bot but just looking for strategy test ####

Just Pass Bot Setting Function It's Nothing Effect For Strategy !!!!!!

Let's Enjoy With Your Strategy BackTest 😁

Remember Beware Max drawdown%. I'm Recommend Lower Than 10% It's Very Good.

Strategy Myth-Busting #3 - BB_BUY+SuperTrend - [MYN]This is part of a new series we are calling "Strategy Myth-Busting" where we take open public manual trading strategies and automate them. The goal is to not only validate the authenticity of the claims but to provide an automated version for traders who wish to trade autonomously.

Our third one we are automating is one of the strategies from "The Best 3 Buy And Sell Indicators on Tradingview + Confirmation Indicators ( The Golden Ones ))" from "Online Trading Signals (Scalping Channel)". No formal backtesting was done by them so wanted to validate their claims.

If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

This strategy uses a combination of 2 open-source public indicators:

BB_Buy and Sell by guikroth (default settings)

SuperTrend from TradingView's Technicals (default settings)

Trading Rules

15 min candles

Long

Long condition when BB_BUY indicates buy signal and SuperTrend is green

Short

Short condition when BB_BUY indicates Sell signal and SuperTrend is red

AlphaTrend StrategyThe strategy version of AlphaTrend indicator for backtesting and optimisation purposes for TradingView users:

Screener / Explorer version and an English explantion video will be published soon...

AlphaTrend's parameters are designed for daily and 4H charts, feel free to optimize on all time frames.

Hope you all use Alphatrend in your profitable trades.

Kıvanç