均线趋势过滤器 (MA_trend Signal/Noise Filter)双语简介

中文:

这款指标是一个基于“信噪比”思想的终极趋势过滤器。它通过比较快速和慢速EMA均线之间的差值(即信号)与ATR(平均真实波幅,代表噪音)来判断市场趋势。只有当信号的强度超过噪音的指定倍数时,才会确认趋势的有效性。该指标可帮助交易者过滤掉噪音,精确捕捉强势趋势,避免误操作。

English:

This indicator is the Ultimate Trend Filter based on the Signal-to-Noise ratio concept. It compares the difference between the fast and slow EMA (Signal) to the ATR (Noise) to determine market trends. A trend is confirmed only when the signal strength exceeds the noise by a specified multiplier. This indicator helps traders filter out noise and accurately capture strong trends, avoiding false signals.

Utilitas Pine

FX Sessions (DTS)FX Sessions (DST-Safe)

This indicator highlights the four main Forex trading sessions — Sydney, Tokyo, London, and New York — using the local timezone of each market.

• DST handled automatically: Sessions shift correctly when London or New York move clocks forward/back.

• Clear visualization: Light background shading for each session, with the London–New York overlap emphasized for peak liquidity.

• Customizable: Toggle individual sessions, labels, and the on-chart legend table.

• Intraday focus: Works best on lower timeframes (1m–1h) for identifying active trading hours and volatility windows.

Use this tool to instantly spot when liquidity and volatility are likely to increase, so you know where to focus your trading.

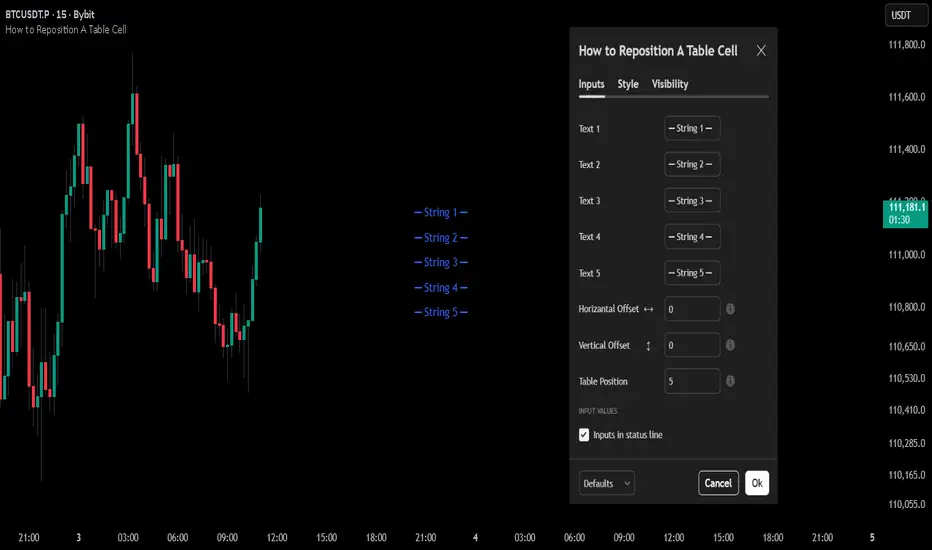

How to Reposition A Table CellOVERVIEW

Using table functions in Pine Script is one of the most effective methods for reporting and interpreting data in a readable manner. However, the built-in capabilities for dynamically repositioning table location are limited. To extend these limitations, a small intervention to the script may be required. This indicator exemplifies how such intervention can be modeled.

CONCEPTS

This indicator provides comprehensive control over table positioning through several user-defined parameters that work together to create flexible display options.

Text Parameters : These five string inputs allow users to define the content displayed in the table. Each parameter accepts custom text that will be displayed as separate rows within the table cell. (The relevant parameters are designed as examples. When implementing the code into your own scripts, you can use series string variables instead of the those inputs.)

Horizontal Offset : This integer parameter controls the horizontal positioning of the table content. Negative values shift the table content to the left, while positive values move it to the right. The offset is multiplied by a spacing factor (currently set to 4) to provide more noticeable movement. This parameter is particularly useful when you need to avoid overlapping with other chart elements or align multiple indicators.

Vertical Offset : This integer parameter manages the vertical positioning by adding line breaks above or below the content. Negative values push the content downward by adding line breaks at the beginning, while positive values elevate the content by adding line breaks at the end. This creates effective vertical spacing without affecting the table's base position.

Table Position : This parameter accepts values from 1 to 9, corresponding to the standard TradingView table positions arranged in a 3x3 grid format (1-3: top row, 4-6: middle row, 7-9: bottom row). This serves as the base positioning before any offset adjustments are applied, providing users with familiar reference points for initial placement.

FUNCTION

The core functionality centers on the custom f_position() function, which processes text positioning based on horizontal and vertical offset values. For vertical positioning, it adds line breaks before or after content depending on the offset direction. For horizontal positioning, it splits the text by rows and adds calculated spaces to each row, maintaining proper alignment across multi-line content. The spacing uses a fixed multiplier of 4, providing good balance between precision and visible movement.

ORIGINALITY & NOTES

Tihs indicator,

introduces a novel approach to table positioning that goes beyond TradingView's standard 9-position limitation by implementing custom offset calculations that allow pixel-level control over table placement.

serves as an educational resource, demonstrating advanced Pine Script techniques for UI manipulation that can be adapted for various custom indicator developments.

is particularly valuable for developers creating complex dashboard layouts or educational materials where precise positioning is crucial. The modular design of the positioning function makes it easily adaptable for other projects requiring similar functionality.

I hope it helps everyone, Always combine with risk management principles and market context awareness. I hope it helps everyone. Trade as safely as possible. Best of luck!

Market Spiralyst [Hapharmonic]Hello, traders and creators! 👋

Market Spiralyst: Let's change the way we look at analysis, shall we? I've got to admit, I scratched my head on this for weeks, Haha :). What you're seeing is an exploration of what's possible when code meets art on financial charts. I wanted to try blending art with trading, to do something new and break away from the same old boring perspectives. The goal was to create a visual experience that's not just analytical, but also relaxing and aesthetically pleasing.

This work is intended as a guide and a design example for all developers, born from the spirit of learning and a deep love for understanding the Pine Script™ language. I hope it inspires you as much as it challenged me!

🧐 Core Concept: How It Works

Spiralyst is built on two distinct but interconnected engines:

The Generative Art Engine: At its core, this indicator uses a wide range of mathematical formulas—from simple polygons to exotic curves like Torus Knots and Spirographs—to draw beautiful, intricate shapes directly onto your chart. This provides a unique and dynamic visual backdrop for your analysis.

The Market Pulse Engine: This is where analysis meets art. The engine takes real-time data from standard technical indicators (RSI and MACD in this version) and translates their states into a simple, powerful "Pulse Score." This score directly influences the appearance of the "Scatter Points" orbiting the main shape, turning the entire artwork into a living, breathing representation of market momentum.

🎨 Unleash Your Creativity! This Is Your Playground

We've included 25 preset shapes for you... but that's just the starting point !

The real magic happens when you start tweaking the settings yourself. A tiny adjustment can make a familiar shape come alive and transform in ways you never expected.

I'm genuinely excited to see what your imagination can conjure up! If you create a shape you're particularly proud of or one that looks completely unique, I would love to see it. Please feel free to share a screenshot in the comments below. I can't wait to see what you discover! :)

Here's the default shape to get you started:

The Dynamic Scatter Points: Reading the Pulse

This is where the magic happens! The small points scattered around the main shape are not just decorative; they are the visual representation of the Market Pulse Score.

The points have two forms:

A small asterisk (`*`): Represents a low or neutral market pulse.

A larger, more prominent circle (`o`): Represents a high, strong market pulse.

Here’s how to read them:

The indicator calculates the Pulse Strength as a percentage (from 0% to 100%) based on the total score from the active indicators (RSI and MACD). This percentage determines the ratio of circles to asterisks.

High Pulse Strength (e.g., 80-100%): Most of the scatter points will transform into large circles (`o`). This indicates that the underlying momentum is strong and It could be an uptrend. It's a visual cue that the market is gaining strength and might be worth paying closer attention to.

Low Pulse Strength (e.g., 0-20%): Most or all of the scatter points will remain as small asterisks (`*`). This suggests weak, neutral, or bearish momentum.

The key takeaway: The more circles you see, the stronger the bullish momentum is according to the active indicators. Watch the artwork "breathe" as the circles appear and disappear with the market's rhythm!

And don't worry about the shape you choose; the scatter points will intelligently adapt and always follow the outer boundary of whatever beautiful form you've selected.

How to Use

Getting started with Spiralyst is simple:

Choose Your Canvas: Start by going into the settings and picking a `Shape` and `Palette` from the "Shape Selection & Palette" group that you find visually appealing. This is your canvas.

Tune Your Engine: Go to the "Market Pulse Engine" settings. Here, you can enable or disable the RSI and MACD scoring engines. Want to see the pulse based only on RSI? Just uncheck the MACD box. You can also fine-tune the parameters for each indicator to match your trading style.

Read the Vibe: Observe the scatter points. Are they mostly small asterisks or are they transforming into large, vibrant circles? Use this visual feedback as a high-level gauge of market momentum.

Check the Dashboard: For a precise breakdown, look at the "Market Pulse Analysis" table on the top-right. It gives you the exact values, scores, and total strength percentage.

Explore & Experiment: Play with the different shapes and color palettes! The core analysis remains the same, but the visual experience can be completely different.

⚙️ Settings & Customization

Spiralyst is designed to be highly customizable.

Shape Selection & Palette: This is your main control panel. Choose from over 25 unique shapes, select a color palette, and adjust the line extension style ( `extend` ) or horizontal position ( `offsetXInput` ).

scatterLabelsInput: This setting controls the total number of points (both asterisks and circles) that orbit the main shape. Think of it as adjusting the density or visual granularity of the market pulse feedback.

The Market Pulse engine will always calculate its strength as a percentage (e.g., 75%). This percentage is then applied to the `scatterLabelsInput` number you've set to determine how many points transform into large circles.

Example: If the Pulse Strength is 75% and you set this to `100` , approximately 75 points will become circles. If you increase it to `200` , approximately 150 points will transform.

A higher number provides a more detailed, high-resolution view of the market pulse, while a lower number offers a cleaner, more minimalist look. Feel free to adjust this to your personal visual preference; the underlying analytical percentage remains the same.

Market Pulse Engine:

`⚙️ RSI Settings` & `⚙️ MACD Settings`: Each indicator has its own group.

Enable Scoring: Use the checkbox at the top of each group to include or exclude that indicator from the Pulse Score calculation. If you only want to use RSI, simply uncheck "Enable MACD Scoring."

Parameters: All standard parameters (Length, Source, Fast/Slow/Signal) are fully adjustable.

Individual Shape Parameters (01-25): Each of the 25+ shapes has its own dedicated group of settings, allowing you to fine-tune every aspect of its geometry, from the number of petals on a flower to the windings of a knot. Feel free to experiment!

For Developers & Pine Script™ Enthusiasts

If you are a developer and wish to add more indicators (e.g., Stochastic, CCI, ADX), you can easily do so by following the modular structure of the code. You would primarily need to:

Add a new `PulseIndicator` object for your new indicator in the `f_getMarketPulse()` function.

Add the logic for its scoring inside the `calculateScore()` method.

The `calculateTotals()` method and the dashboard table are designed to be dynamic and will automatically adapt to include your new indicator!

One of the core design philosophies behind Spiralyst is modularity and scalability . The Market Pulse engine was intentionally built using User-Defined Types (UDTs) and an array-based structure so that adding new indicators is incredibly simple and doesn't require rewriting the main logic.

If you want to add a new indicator to the scoring engine—let's use the Stochastic Oscillator as a detailed example—you only need to modify three small sections of the code. The rest of the script, including the adaptive dashboard, will update automatically.

Here’s your step-by-step guide:

#### Step 1: Add the User Inputs

First, you need to give users control over your new indicator. Find the `USER INTERFACE: INPUTS` section and add a new group for the Stochastic settings, right after the MACD group.

Create a new group name: `string GRP_STOCH = "⚙️ Stochastic Settings"`

Add the inputs: Create a boolean to enable/disable it, and then add the necessary parameters (`%K`, `%D`, `Smooth`). Use the `active` parameter to link them to the enable/disable checkbox.

// Add this code block right after the GRP_MACD and MACD inputs

string GRP_STOCH = "⚙️ Stochastic Settings"

bool stochEnabledInput = input.bool(true, "Enable Stochastic Scoring", group = GRP_STOCH)

int stochKInput = input.int(14, "%K Length", minval=1, group = GRP_STOCH, active = stochEnabledInput)

int stochDInput = input.int(3, "%D Smoothing", minval=1, group = GRP_STOCH, active = stochEnabledInput)

int stochSmoothInput = input.int(3, "Smooth", minval=1, group = GRP_STOCH, active = stochEnabledInput)

#### Step 2: Integrate into the Pulse Engine (The "Factory")

Next, go to the `f_getMarketPulse()` function. This function acts as a "factory" that builds and configures the entire market pulse object. You need to teach it how to build your new Stochastic indicator.

Update the function signature: Add the new `stochEnabledInput` boolean as a parameter.

Calculate the indicator: Add the `ta.stoch()` calculation.

Create a `PulseIndicator` object: Create a new object for the Stochastic, populating it with its name, parameters, calculated value, and whether it's enabled.

Add it to the array: Simply add your new `stochPulse` object to the `array.from()` list.

Here is the complete, updated `f_getMarketPulse()` function :

// Factory function to create and calculate the entire MarketPulse object.

f_getMarketPulse(bool rsiEnabled, bool macdEnabled, bool stochEnabled) =>

// 1. Calculate indicator values

float rsiVal = ta.rsi(rsiSourceInput, rsiLengthInput)

= ta.macd(close, macdFastInput, macdSlowInput, macdSignalInput)

float stochVal = ta.sma(ta.stoch(close, high, low, stochKInput), stochDInput) // We'll use the main line for scoring

// 2. Create individual PulseIndicator objects

PulseIndicator rsiPulse = PulseIndicator.new("RSI", str.tostring(rsiLengthInput), rsiVal, na, 0, rsiEnabled)

PulseIndicator macdPulse = PulseIndicator.new("MACD", str.format("{0},{1},{2}", macdFastInput, macdSlowInput, macdSignalInput), macdVal, signalVal, 0, macdEnabled)

PulseIndicator stochPulse = PulseIndicator.new("Stoch", str.format("{0},{1},{2}", stochKInput, stochDInput, stochSmoothInput), stochVal, na, 0, stochEnabled)

// 3. Calculate score for each

rsiPulse.calculateScore()

macdPulse.calculateScore()

stochPulse.calculateScore()

// 4. Add the new indicator to the array

array indicatorArray = array.from(rsiPulse, macdPulse, stochPulse)

MarketPulse pulse = MarketPulse.new(indicatorArray, 0, 0.0)

// 5. Calculate final totals

pulse.calculateTotals()

pulse

// Finally, update the function call in the main orchestration section:

MarketPulse marketPulse = f_getMarketPulse(rsiEnabledInput, macdEnabledInput, stochEnabledInput)

#### Step 3: Define the Scoring Logic

Now, you need to define how the Stochastic contributes to the score. Go to the `calculateScore()` method and add a new case to the `switch` statement for your indicator.

Here's a sample scoring logic for the Stochastic, which gives a strong bullish score in oversold conditions and a strong bearish score in overbought conditions.

Here is the complete, updated `calculateScore()` method :

// Method to calculate the score for this specific indicator.

method calculateScore(PulseIndicator this) =>

if not this.isEnabled

this.score := 0

else

this.score := switch this.name

"RSI" => this.value > 65 ? 2 : this.value > 50 ? 1 : this.value < 35 ? -2 : this.value < 50 ? -1 : 0

"MACD" => this.value > this.signalValue and this.value > 0 ? 2 : this.value > this.signalValue ? 1 : this.value < this.signalValue and this.value < 0 ? -2 : this.value < this.signalValue ? -1 : 0

"Stoch" => this.value > 80 ? -2 : this.value > 50 ? 1 : this.value < 20 ? 2 : this.value < 50 ? -1 : 0

=> 0

this

#### That's It!

You're done. You do not need to modify the dashboard table or the total score calculation.

Because the `MarketPulse` object holds its indicators in an array , the rest of the script is designed to be adaptive:

The `calculateTotals()` method automatically loops through every indicator in the array to sum the scores and calculate the final percentage.

The dashboard code loops through the `enabledIndicators` array to draw the table. Since your new Stochastic indicator is now part of that array, it will appear automatically when enabled!

---

Remember, this is your playground! I'm genuinely excited to see the unique shapes you discover. If you create something you're proud of, feel free to share it in the comments below.

Happy analyzing, and may your charts be both insightful and beautiful! 💛

Swing Z | Zillennial Technologies Inc.Swing Z by Zillennial Technologies Inc. is an advanced algorithmic framework built specifically for cryptocurrency markets. It integrates multiple layers of technical analysis into a single decision-support tool, generating buy and sell signals only when several independent confirmations align.

Core Concept

Swing Z fuses trend structure, momentum oscillators, volatility signals, and price action tools to capture high-probability trading opportunities in volatile crypto environments.

Trend Structure (EMA 9, 21, 50, 200)

Short-term EMAs (9 & 21) detect immediate momentum shifts.

Longer-term EMAs (50 & 200) define the broader trend and dynamic support/resistance.

Momentum & Confirmation Layer

RSI measures relative strength and market conditions.

MACD crossovers confirm momentum shifts and trend continuations.

Volatility & Market Pressure

TTM Squeeze highlights compression zones likely to precede breakouts.

Volume analysis confirms conviction behind directional moves.

VWAP (Volume Weighted Average Price) establishes intraday value zones and institutional benchmarks.

Price Action Filters

Fibonacci retracements are integrated to identify key reversal and continuation levels.

Signals are produced only when multiple conditions agree, reducing noise and improving reliability in fast-moving crypto markets.

Features

Tailored for cryptocurrency trading across major pairs (BTC, ETH, and altcoins).

Works effectively on swing and trend-based timeframes (1H–1D).

Combines trend, momentum, volatility, and price action into a single framework.

Generates clear Buy/Sell markers and integrates with TradingView alerts.

How to Use

Apply to a clean chart for the clearest visualization.

Use Swing Z as a swing trading tool, aligning entries with both trend structure and momentum confirmation.

Combine with your own stop-loss, take-profit, and position sizing rules.

Avoid application on non-standard chart types such as Renko, Heikin Ashi, or Point & Figure, which may distort results.

Disclaimer

Swing Z is designed as a decision-support tool, not financial advice.

All backtesting should use realistic risk, commission, and slippage assumptions.

Past results do not guarantee future performance.

Signals do not repaint but may adjust as new data develops in real-time.

Why Swing Z is original & useful:

Swing Z unifies EMA trend structure, RSI, MACD, TTM Squeeze, VWAP, Fibonacci retracements, and volume analysis into a single algorithmic framework. This multi-confirmation approach improves accuracy by requiring consensus across trend, momentum, volatility, and price action — a design made specifically for the challenges and volatility of cryptocurrency markets.

How to avoid repainting when using security() - viewing optionsHow to avoid repainting when using the security() - Edited PineCoders FAQ with more viewing options

This may be of value to a limited few, but I've introduced a set of Boolean inputs to PineCoders' original script because viewing all the various security lines at once was giving me a brain cramp. I wanted to study each behavior one-by-one. This version (also updated to PineScript v6) will allow users to selectively display each, or any combination, of the security plots. Each plot was updated to include a condition tied to its corresponding input, ensuring it only appears when explicitly enabled. The label-rendering logic only displays when its related plot is active; however, I've also added an input that allows you to remove all labels, enabling you to see the price action more clearly (the labels can sometimes obscure what you want to see). Run this script in replay mode to view the nuanced differences between the 12 methods while selecting/deselecting the desired plots (selecting all at once can be overcrowded and confusing).

All thanks and credit to PineCoders--these changes I made only provide more control over what’s shown on the chart without altering the core structure or intent of the original script. It helped me, so I thought I should share it. If I inadvertently messed something up, please let me know, and I will try to fix it.

I set the defaults for viewing monthly security functions on the daily timeframe. Only the first 2 security functions plot with the default settings, so change the settings as needed. Be sure to read the original notes and detailed explanations in the PineCoders posting "How to avoid repainting when using security() - PineCoders FAQ."

Bottom line, you should use one of the two functions: f_secureSecurity or f_security, depending on what you are trying to do. Hopefully, this script will make it a little easier for the visual learner to understand why (use replay mode or watch live price action on a lower timeframe).

Previous Day OHLC Dashboard (Last N Days)Indicator: Previous Day OHLC Dashboard (Multi-Day)

This indicator displays a dashboard-style table on your chart that shows the Open, High, Low, and Close (OHLC) of the previous trading days. It’s designed to help traders quickly reference key daily levels that often act as important support and resistance zones.

🔑 Features:

Dashboard Table: Shows OHLC data for the last N trading days (default = 3, up to 10).

Customizable Appearance:

Change the position of the dashboard (Top-Right, Top-Left, Bottom-Right, Bottom-Left).

Adjust text size (Tiny → Huge).

Customize colors for header, labels, and each OHLC column.

Yesterday’s OHLC Lines (optional): Plots horizontal lines on the chart for the previous day’s Open, High, Low, and Close.

Intraday & Multi-Timeframe Compatible: Works on all timeframes below Daily — values update automatically from the daily chart.

📊 Use Cases:

Quickly identify yesterday’s key levels for intraday trading.

Track how current price reacts to previous day’s support/resistance.

Keep a multi-day reference for trend bias and range context.

⚙️ How it Works:

The indicator pulls daily OHLC values using request.security() with lookahead_on to ensure prior day’s values are extended across the next session.

These values are displayed in a compact table for quick reference.

Optionally, the most recent daily levels (D-1) are plotted as chart lines.

✅ Perfect for day traders, scalpers, and swing traders who rely on yesterday’s price action to plan today’s trades.

WAE SHK Teyla 3MDesigned to detect high-pressure market moments, where momentum and volume converge to trigger explosive moves. Ideal as an entry trigger in scalping strategies, especially when paired with STC and ST-MA.

10 AM Reversal/Continuation Zone BY DAN GESPlots the high and low between 9.30 - 10:00am ET

Colours the zone between those two levels.

Highlights when price breaks above or below that zone after 10:00am

Goldbach Time Indicator🔧 Key Fixes Applied:

1. Time Validation & Bounds Checking:

Hour/Minute Bounds: Ensures hours stay 0-23, minutes stay 0-59

Edge Case Handling: Prevents invalid time calculations from causing missing data

UTC Conversion Safety: Better handling of timezone edge cases

2. Enhanced Value Validation:

NA Checking: Validates all calculated values before using them

Goldbach Detection: Only flags valid, non-NA values as Goldbach hits

Plot Safety: Prevents plotting invalid or NA values that could cause gaps

3. Improved Plot Logic:

Core Level Colors: Blue for core levels (29,35,71,77), yellow/lime/orange for regular hits

Debug Mode Enhanced: Shows all calculations with gray dots when enabled

Better Filtering: Only plots positive, valid values for minus calculations

4. Background vs Dots Issue:

The large green/blue background you see suggests the indicator is detecting Goldbach times correctly, but the dots weren't plotting due to validation issues. This should now be fixed.

Index Position Size Calculator for [US30 / US100 / SP500]What it does

This tool helps you size positions consistently for index trades on US30 (Dow Jones), NAS100 (Nasdaq-100), and SP500 (S&P 500). Enter your account balance, risk %, and your planned Entry / Stop-Loss / Target and the script calculates:

• Position Size (rounded to your lot/contract step)

• Risk-to-Reward (R/R)

• Potential P/L in USD based on your inputs

• Visual Entry / SL / TP lines with green/red zones and concise labels

Supported contract styles

Choose a preset for common products (e.g., CFD $1/pt, YM/NQ/ES futures, MYM/MNQ/MES micros) or override the economics yourself. You remain in control of the two key levers:

• $/point — how many dollars you gain/lose per 1 index point per contract/lot

• Point size — how many price units equal 1 index point on your chart (often 1.0, but some brokers use 0.1 or 0.5)

Inputs

• Account Balance ($) and Risk % per trade

• Index: US30 / NAS100 / SP500

• Contract: CFD / Futures (YM, NQ, ES) / Micros (MYM, MNQ, MES)

• $/point: auto from Contract or manual override

• Point size: auto from Index or manual override

• Position size step: rounding (e.g., 1 for futures, 0.01 for CFDs)

• Entry / SL / TP: typed values (snapped to tick), with on-chart zones and labels

• Display toggles for lines and labels

How the math works

• StopPoints = |Entry − SL| ÷ PointSize

• ProfitPoints = |TP − Entry| ÷ PointSize

• Position Size = (AccountBalance × Risk%) ÷ (StopPoints × $/point)

• R/R = ProfitPoints ÷ StopPoints

• Potential P/L = PositionSize × Points × $/point

How to use (quick start)

1. Select Index and Contract.

2. Confirm $/point and Point size match your broker’s specs.

3. Enter Entry / SL / TP for the trade idea.

4. Read the Position Size, R/R, and Potential P/L in the info box.

5. Adjust for fees, spreads, and slippage as needed.

Notes & limitations

• Broker symbols can vary. Always verify $/point and Point size for your instrument before risking capital.

• The script does not place orders and does not generate trade signals; it’s a sizing/visualization tool.

• Results can differ across brokers due to pricing, spreads, minimum lot sizes, and execution rules.

• Use on the intended indices; you’ll see a reminder if you load it elsewhere.

Changelog highlights

• Pine v6, constant-safe inputs, tick-snapping, global fills (no local-scope errors).

• Robust label handling and optional minimal chart markers.

Disclaimer

This script is provided for educational purposes only and does not constitute financial advice or a recommendation to buy or sell any security or derivative. Trading involves risk, including the possible loss of principal. Always do your own research, verify contract specifications with your broker, and consider testing in a demo environment before trading live.

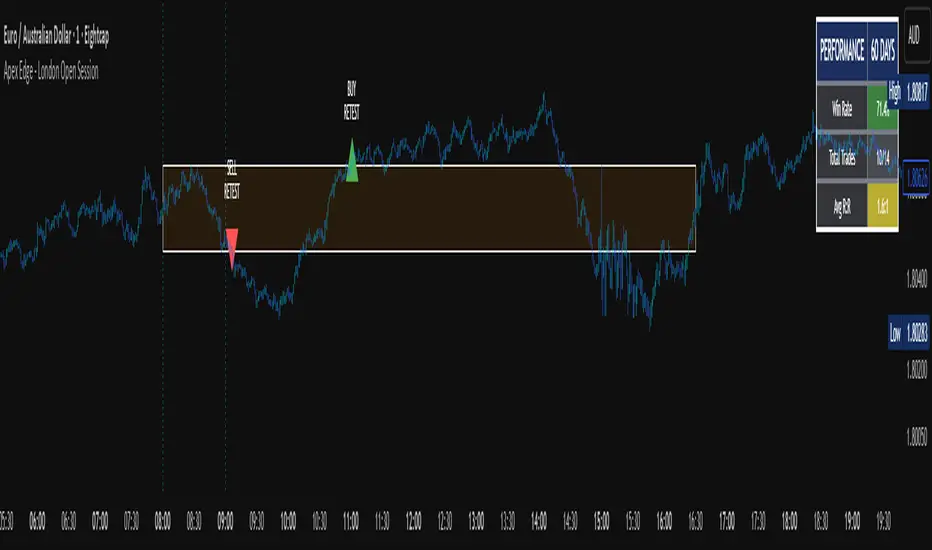

Apex Edge - London Open Session# Apex Edge - London Open Session Trading System

## Overview

The London Open Session indicator captures institutional price action during the first hour of the London forex session (8:00-9:00 AM GMT) and identifies high-probability breakout and retest opportunities. This system tracks the session's high/low range and generates precise entry signals when price breaks or retests these key institutional levels.

## Core Strategy

**Session Tracking**: Automatically identifies and marks the London Open session boundaries, creating a trading zone from the first hour's price range.

**Dual Entry Logic**:

- **Breakout Entries**: Triggers when price closes beyond the session high/low and continues in that direction

- **Retest Entries**: Activates when price returns to test the broken level as new support/resistance

**Performance Analytics**: Built-in win rate tracking displays real-time performance statistics over user-defined lookback periods, enabling data-driven optimization for each currency pair.

## Key Features

### Automated Zone Detection

- Precise London session timing with timezone offset controls

- Visual session boundaries with customizable colours

- Automatic high/low range calculation and display

### Smart Entry System

- Breakout confirmation requiring candle close beyond zone

- Retest detection with configurable pip distance tolerance

- Separate risk/reward ratios for breakout vs retest entries

- Visual entry arrows with clear trade direction labels

### Performance HUD

- Real-time win rate calculation over customizable periods (7-365 days)

- Total trades tracking with win/loss breakdown

- Average risk-reward ratio display

- Color-coded performance metrics (green >70%, yellow >50%, red <50%)

### PineConnector Integration

- Direct MT4/MT5 execution via PineConnector alerts

- Proper forex pip calculations for all currency pairs

- Customizable risk percentage per trade

- Symbol override capability for broker compatibility

- Automatic SL/TP level calculation in pips

## Critical Usage Requirements

### Pair-Specific Optimization

Each currency pair requires individual optimization due to varying volatility characteristics, institutional participation levels, and typical price ranges during London hours. The performance HUD is essential for identifying optimal settings before live trading.

**Recommended Testing Process**:

1. Apply indicator to desired currency pair and timeframe

2. Experiment with session timing - while 8:00-9:00 AM GMT is standard, some pairs may show improved performance with alternative hourly windows (e.g., 7:00-8:00 AM or 9:00-10:00 AM)

3. Adjust Stop Loss distances, Risk/Reward ratios, and Retest distances

4. Monitor win rate over 30+ day periods using the performance HUD

5. Only proceed with live alerts once consistent 60%+ win rates are achieved

6. Create separate optimized chart setups for each profitable pair/timeframe combination

### Timeframe Specifications

This indicator is specifically designed and tested for:

- **1-minute charts**: Optimal for capturing immediate institutional reactions

- **5-minute charts**: Balanced approach between noise reduction and opportunity frequency

Higher timeframes generally produce inferior results due to increased noise and reduced institutional edge during the London session window.

## Settings Configuration

### Session Timing

- **London Open/Close Hours**: Adjust for your chart's timezone

- **Rectangle End Time**: Set to 4:30 PM to stop signals before NY session close

- **Timezone Offset**: Ensure accurate London session capture

### Entry Parameters

- **Retest Distance**: 3-8 pips depending on pair volatility

- **Stop Loss Pips**: Separate settings for breakouts (10-15 pips) and retests (8-12 pips)

- **Risk/Reward Ratios**: Independent ratios for different entry types

### PineConnector Setup

- **License ID**: Your PineConnector license key

- **Symbol Override**: MT4/MT5 symbol names if different from TradingView

- **Risk Percentage**: Position size as percentage of account balance

- **Prefix/Comment**: Organize trades in terminal

## Manual Trading Limitations

Without PineConnector automation, traders face significant practical challenges:

**Settings Management**: Each currency pair requires different optimized parameters. Switching between charts means manually adjusting multiple settings each time, creating potential for errors and missed opportunities.

**Timing Sensitivity**: London Open signals can occur rapidly during high-volatility periods. Manual execution may result in slippage or missed entries.

**Multi-Pair Monitoring**: Tracking 4-11 currency pairs simultaneously while manually adjusting settings for each switch becomes impractical for most traders.

**Parameter Consistency**: Risk of using suboptimal settings when quickly switching between pairs, potentially compromising the careful optimization work.

## Recommended Workflow

1. **Historical Testing**: Use win rate HUD to identify profitable pairs and optimal parameters

2. **Demo Automation**: Test PineConnector alerts on demo accounts with optimized settings

3. **Live Implementation**: Deploy alerts only on proven profitable pair/timeframe combinations

4. **Ongoing Monitoring**: Regular review of performance metrics to maintain edge

## Risk Disclaimer

This indicator provides analysis tools and automation capabilities but does not guarantee profitable trading outcomes. Past performance does not predict future results. Users should thoroughly backtest and demo trade before risking live capital. The London session strategy works best during specific market conditions and may underperform during low volatility or unusual market environments.

## Support Requirements

Successful implementation requires:

- Basic understanding of London session market dynamics

- PineConnector subscription for automation features

- Patience for proper optimization process

- Realistic expectations about win rates and drawdown periods

This system is designed for serious traders willing to invest time in proper optimization and risk management rather than plug-and-play solutions.

CM Indicator About Indicator:-

1) This is best Indicator for trend identification.

2) This is based on 42 EMA with Upper Band and Lower bands for trend identification.

3) This should be used for Line Bar chart only.

4) Line bar chart should be used at 1 hour for 15 line breaks.

How to Use:-

1) To go with trend is best use of this indicator.

2) This is for stocks and options not for index. Indicator used for Stocks at one hour and options for 10-15 minutes line break.

3) There will be 5% profitability defined for each entry, 3 entries with profit are best posible in same continuous trend 4 and 5th entry is in riskier zone in continuous trend.

4) Loss will only happen if there is trend reversal.

5) Loss could only be one trade of profit out of three profitable trades.

6) Back tested on 200 stocks and 100 options.

Auto Daily High/Low/50%This indicator automatically plots the current daily high and low, as well as the midrange.

Script Info BannerThe script includes a small template displaying the username, script name, and date of analysis. This feature is implemented to establish credibility and prevent unauthorized use of the analysis.

Chart-Only Scanner — Pro Table v2.5.1Chart-Only Scanner — Pro Table v2.5

User Manual (Pine Script v6)

What this tool does (in one line)

A compact, on-chart table that scores the current chart symbol (or an optional override) using momentum, volume, trend, volatility, and pattern checks—so you can quickly decide UP, DOWN, or WAIT.

Quick Start (90 seconds)

Add the indicator to any chart and timeframe (1m…1M).

Leave “Override chart symbol” = OFF to auto-use the chart’s symbol.

Choose your layout:

Row (wide horizontal strip), or Grid (title + labeled cells).

Pick a size preset (Micro, Small, Medium, Large, Mobile).

Optional: turn on “Use Higher TF (EMA 20/50)” and set HTF Multiplier (e.g., 4 ⇒ if chart is 15m, HTF is 60m).

Watch the table:

DIR (↑/↓/→), ROC%, MOM, VOL, EMA stack, HTF, REV, SCORE, ACT.

Add an alert if you want: the script fires when |SCORE| ≥ Action threshold.

What to expect

A small table appears on the chart corner you choose, updating each bar (or only at bar close if you keep default smart-update).

The ACT cell shows 🔥 (strong), 👀 (medium), or ⏳ (weak).

Panels & Settings (every option explained)

Core

Momentum Period: Lookback for rate-of-change (ROC%). Shorter = more reactive; longer = smoother.

ROC% Threshold: Minimum absolute ROC% to call direction UP (↑) or DOWN (↓); otherwise →.

Require Volume Confirmation: If ON and VOL ≤ 1.0, the SCORE is forced to 0 (prevents low-volume false positives).

Override chart symbol + Custom symbol: By default, the indicator uses the chart’s symbol. Turn this ON to lock to a specific ticker (e.g., a perpetual).

Higher TF

Use Higher TF (EMA 20/50): Compares EMA20 vs EMA50 on a higher timeframe.

HTF Multiplier: Higher TF = (chart TF × multiplier).

Example: on 3H chart with multiplier 2 ⇒ HTF = 6H.

Volatility & Oscillators

ATR Length: Used to show ATR% (ATR relative to price).

RSI Length: Standard RSI; colors: green ≤30 (oversold), red ≥70 (overbought).

Stoch %K Length: With %D = SMA(%K, 3).

MACD Fast/Slow/Signal: Standard MACD values; we display Line, Signal, Histogram (L/S/H).

ADX Length (Wilder): Wilder’s smoothing (internal derivation); also shows +DI / −DI if you enable the ADX column.

EMAs / Trend

EMA Fast/Mid/Slow: We compute EMA(20/50/200) by default (editable).

EMA Stack: Bull if Fast > Mid > Slow; Bear if Fast < Mid < Slow; Flat otherwise.

Benchmark (optional, OFF by default)

Show Relative Strength vs Benchmark: Displays RS% = ROC(symbol) − ROC(benchmark) over the Momentum Period.

Benchmark Symbol: Ticker used for comparison (e.g., BTCUSDT as a market proxy).

Columns (show/hide)

Toggle which fields appear in the table. Hiding unused fields keeps the layout clean (especially on mobile).

Display

Layout Mode:

Row = a single two-row strip; each column is a metric.

Grid = a title row plus labeled pairs (label/value) arranged in rows.

Size Preset: Micro, Small, Medium, Large, Mobile change text size and the grid density.

Table Corner: Where the panel sits (e.g., Top Right).

Opaque Table Background: ON = dark card; OFF = transparent(ish).

Update Every Bar: ON = update intra-bar; OFF = smart update (last bar / real-time / confirmed history).

Action threshold (|score|): The cutoff for 🔥 and alert firing (default 70).

How to read each field

CHART: The active symbol name (or your custom override).

DIR: ↑ (ROC% > threshold), ↓ (ROC% < −threshold), → otherwise.

ROC%: Rate of change over Momentum Period.

Formula: (Close − Close ) / Close × 100.

MOM: A scaled momentum score: min(100, |ROC%| × 10).

VOL: Volume ratio vs 20-bar SMA: Volume / SMA(Volume,20).

1.5 highlights as yellow (significant participation).

ATR%: (ATR / Close) × 100 (volatility relative to price).

RSI: Colored for extremes: ≤30 green, ≥70 red.

Stoch K/D: %K and %D numbers.

MACD L/S/H: Line, Signal, Histogram. Histogram color reflects sign (green > 0, red < 0).

ADX, +DI, −DI: Trend strength and directional components (Wilder). ADX ≥ 25 is highlighted.

EMA 20/50/200: Current EMA values (editable lengths).

STACK: Bull/Bear/Flat as defined above.

VWAP%: (Close − VWAP) / Close × 100 (premium/discount to VWAP).

HTF: ▲ if HTF EMA20 > EMA50; ▼ if <; · if flat/off.

RS%: Symbol’s ROC% − Benchmark ROC% (positive = outperforming).

REV (reversal):

🟢 Eng/Pin = bullish engulfing or bullish pin detected,

🔴 Eng/Pin = bearish engulfing or bearish pin,

· = none.

SCORE (absolute shown as a number; sign shown via DIR and ACT):

Components:

base = MOM × 0.4

volBonus = VOL > 1.5 ? 20 : VOL × 13.33

htfBonus = use_mtf ? (HTF == DIR ? 30 : HTF == 0 ? 15 : 0) : 0

trendBonus = (STACK == DIR) ? 10 : 0

macdBonus = 0 (placeholder for future versions)

scoreRaw = base + volBonus + htfBonus + trendBonus + macdBonus

SCORE = DIR ≥ 0 ? scoreRaw : −scoreRaw

If Require Volume Confirmation and VOL ≤ 1.0 ⇒ SCORE = 0.

ACT:

🔥 if |SCORE| ≥ threshold

👀 if 50 < |SCORE| < threshold

⏳ otherwise

Practical examples

Strong long (trend + participation)

DIR = ↑, ROC% = +3.2, MOM ≈ 32, VOL = 1.9, STACK = Bull, HTF = ▲, REV = 🟢

SCORE: base(12.8) + volBonus(20) + htfBonus(30) + trend(10) ≈ 73 → ACT = 🔥

Action idea: look for longs on pullbacks; confirm risk with ATR%.

Weak long (no volume)

DIR = ↑, ROC% = +1.0, but VOL = 0.8 and Require Volume Confirmation = ON

SCORE forced to 0 → ACT = ⏳

Action: wait for volume > 1.0 or turn off confirmation knowingly.

Bearish reversal warning

DIR = →, REV = 🔴 (bearish engulfing), RSI = 68, HTF = ▼

SCORE may be mid-range; ACT = 👀

Action: watch for breakdown and rising VOL.

Alerts (how to use)

The script calls alert() whenever |SCORE| ≥ Action threshold.

To receive pop-ups, sounds, or emails: click “⏰ Alerts” in TradingView, choose this indicator, and pick “Any alert() function call.”

The alert message includes: symbol, |SCORE|, DIR.

Layout, Size, and Corner tips

Row is best when you want a compact status ribbon across the top.

Grid is clearer on big screens or when you enable many columns.

Size:

Mobile = one pair per row (tall, readable)

Micro/Small = dense; good for many fields

Large = presentation/screenshots

Corner: If the table overlaps price, change the corner or set Opaque Background = OFF.

Repaint & timeframe behavior

Default smart update prefers stability (last bar / live / confirmed history).

For a stricter, “close-only” behavior (less repaint): turn Update Every Bar = OFF and avoid Heikin Ashi when you want raw market OHLC (HA modifies price inputs).

HTF logic is derived from a clean, integer multiple of your chart timeframe (via multiplier). It works with 3H/4H and any TF.

Performance notes

The script analyzes one symbol (chart or override) with multiple metrics using efficient tuple requests.

If you later want a multi-symbol grid, do it with pages (10–15 per page + rotate) to stay within platform limits (recommended future add-on).

Troubleshooting

No table visible

Ensure the indicator is added and not hidden.

Try toggling Opaque Background or switch Corner (it might be behind other drawings).

Keep Columns count reasonable for the chosen Size.

If you turned ON Override, verify the Custom symbol exists on your data provider.

Numbers look different on HA candles

Heikin Ashi modifies OHLC; switch to regular candles if you need raw price metrics.

3H/4H issues

Use integer HTF Multiplier (e.g., 2, 4). The tool builds the correct string internally; no manual timeframe strings needed.

Power user tips

Volume gating: keeping Require Volume Confirmation = ON filters most fake moves; if you’re a scalper, reduce strictness or turn it off.

Action threshold: 60–80 is typical. Higher = fewer but stronger signals.

Benchmark RS%: great for spotting leaders/laggards; positive RS% = outperformance vs benchmark.

Change policy & safety

This version doesn’t alter your historical logic you tested (no radical changes).

Any future “radical” change (score weights, HTF logic, UI hiding data) will ship with a toggle and an Impact Statement so you can keep old behavior if you prefer.

Glossary (quick)

ROC%: Percent change over N bars.

MOM: Scaled momentum (0–100).

VOL ratio: Volume vs 20-bar average.

ATR%: ATR as % of price.

ADX/DI: Trend strength / direction components (Wilder).

EMA stack: Relationship between EMAs (bullish/bearish/flat).

VWAP%: Premium/discount to VWAP.

RS%: Relative strength vs benchmark.

Higher High Close 3 Days & Price ±5% 200 EMAScript by Raj Natarajan V 1

This script identifies stocks that are within +/- 5% of the 200 day EMA and within that sub-set, it identifies stocks that have had three consecutive days of higher highs.

Close Just Above 44MA with Uptrendpine editor code for indicator to identify stocks whose price closes just above MA 44 with MA 44 trending up on a daily chart for swing trading

My ScriptMulti-Timeframe Momentum Sync - 1 line

1,5,15 averaged into 1 line, WHY?

"YNOT", my boat's name.

Seems responsive and sensitive, no lag, this is just the beginning.

Smart Wick AnalyzerSmart Wick Analyzer (SWA)

Purpose: Highlight potential liquidity‑grab candles (long wicks) and turn them into actionable, rule‑based buy/sell signals with trend, volume, and cooldown filters.

Type: Indicator (not a strategy). Educational tool to contextualize wick events.

🧠 What This Script Does

SWA looks for candles where the wick is large relative to its body—a common signature of liquidity sweeps / rejection. It then adds three confirmations before marking a trade signal:

1. Wick Event

• Upper‑wick event (possible rejection from above)

• Lower‑wick event (possible rejection from below)

• Condition: wick length > body × Wick‑to‑Body Ratio

2. Context Filters

• Trend filter : closing price vs. SMA of lookbackBars

• Volume filter : current volume vs. average volume × volumeThreshold

3. Signal Hygiene

• Cooldown : prevents clustering; a minimum number of bars must pass before a new signal is allowed.

If a candle passes these checks:

• Buy Signal (triangle up): long lower wick + price above SMA + relative‑high volume + cooldown passed

• Sell Signal (triangle down): long upper wick + price below SMA + relative‑high volume + cooldown passed

The signal candle is also bar‑colored black for quick visual focus.

⸻

✳️ What the Dotted Lines Mean (including the green one)

On every signal bar the script draws two dotted horizontal levels, extended to the right:

• Open line of the signal candle

• Close line of the signal candle

• They use the signal color: green for Buy, red for Sell.

How to interpret (example: green = Buy signal):

• The green dotted close line represents the momentum validation level. If subsequent candles close above this line, it indicates follow‑through after the wick rejection (buyers defended into the close).

• The green dotted open line is a risk context / invalidation reference. If price falls back below it soon after the signal, the wick event may have failed or devolved into chop.

In your annotated chart: the candle initially looked constructive (“closing above could be positive momentum”), but later price failed and rotated down—hence a sell signal interpreted when an upper‑wick event occurred under down‑trend conditions.

⸻

⚙️ Inputs & What They Control

• Wick‑to‑Body Ratio (wickThreshold): how “extreme” a wick must be to count as a liquidity‑grab.

• Lookback Period (lookbackBars):

• SMA period for trend context

• Volume MA for relative‑volume check

• Volume Multiplier (volumeThreshold): strengthens/loosens volume confirmation.

• Cooldown Bars (cooldownBars): minimum spacing between consecutive signals.

• Enable Alerts (showAlerts): turns on alert conditions.

⸻

🔔 Alerts (exact titles)

• “SWA Buy Alert” — potential reversal / Buy signal detected

• “SWA Sell Alert” — potential reversal / Sell signal detected

⸻

📌 How to Use (practical guide)

1. Scan for the black‑colored signal candle and its dotted lines.

2. For Buy signals (green): Prefer continuation if price closes above the green close line within the next few bars. Manage risk using the open line or your own level.

3. For Sell signals (red): Prefer continuation if price closes below the red close line.

4. Avoid chasing during low‑volume / counter‑trend signals; the filters help, but structure (HTF trend, S/R, session context) still matters.

5. Use the cooldown to reduce noise on fast time frames.

⸻

✅ Why This Isn’t Just “Another Wick Indicator”

• The script does not flag every long‑wick; it requires trend alignment and relative volume to suggest participation.

• The two reference lines (open/close) provide post‑signal state tracking—a simple, visual framework to judge follow‑through vs. failure without additional tools.

• Cooldown logic discourages clustered, low‑quality repeats around the same zone.

⸻

⚠️ Notes & Limitations

• Works across markets/time frames, but wick behavior varies by instrument and session. Parameters may need adjustment.

• Signals are contextual, not guarantees. Consolidation and news spikes can invalidate wick reads.

• This indicator is not a strategy; it does not backtest performance on its own.

⸻

📄 Disclaimer

This tool is for educational purposes only and should be combined with personal analysis and risk management. Markets are uncertain; past behavior does not guarantee future results.