Validated Order Blocks with Fib LevelsThis indicator automatically identifies and displays Smart Money Concepts (SMC) order blocks based on market structure breaks:

How it works:

Bearish Order Blocks (Red): Marks the last bullish candle before a swing high. The OB becomes valid when price breaks below the previous swing low, indicating institutional selling zones. Drawn from the candle's close (body top) to its low (bottom wick).

Bullish Order Blocks (Green): Marks the last bearish candle before a swing low. The OB becomes valid when price breaks above the previous swing high, indicating institutional buying zones. Drawn from the candle's high (top wick) to its close (body bottom).

Features:

Three Fibonacci retracement levels (50%, 75%, 100%) for each order block

Fib 100% faces downward on bearish OBs and upward on bullish OBs

Auto-validation: OBs are removed when price closes through them

Customizable: Adjustable swing detection, timeframe selection, and OB display limits

Optional Break of Structure (BOS) markers to show when OBs activate

Works on any timeframe with HTF analysis support

Perfect for identifying key institutional support/resistance zones and potential reversal areas.

Siklus

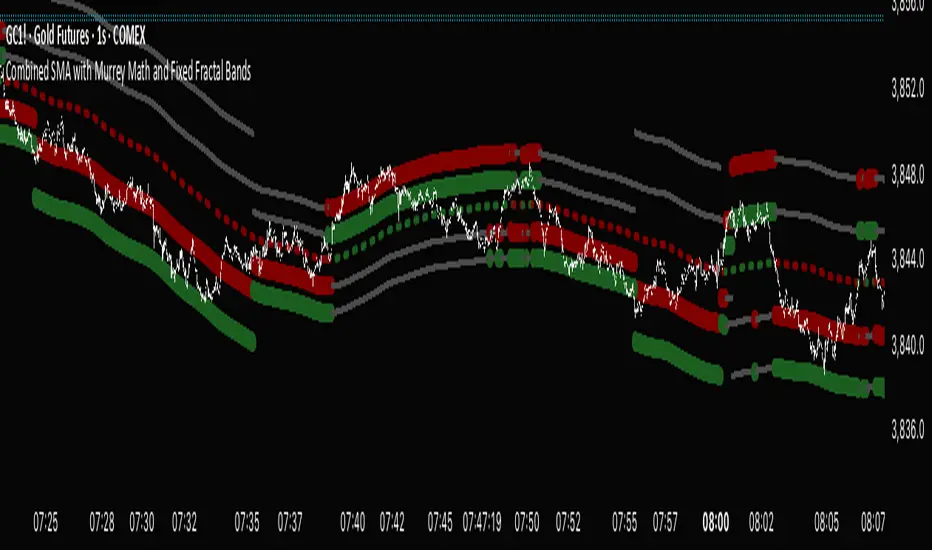

Combined SMA with Murrey Math and Fixed Fractal Bands "Combined SMA with Murrey Math and Fixed Fractal Bands" , overlaying a Simple Moving Average (SMA), Murrey Math (MM) bands, and fixed fractal bands on a price chart. Here's a brief description of its functionality:Inputs:SMA Length: Configurable period for the SMA (default: 180 bars).

Resolution: Optional custom timeframe for data.

Frame Size for MM: Lookback period for Murrey Math calculations (default: 180 bars, adjustable via multiplier).

Ignore Wicks: Option to use open/close prices instead of high/low for MM calculations.

Fixed Fractal Size: Fixed distance in points for fractal bands (default: 1.22).

Shade 3/8-5/8 Overlap: Option to highlight overlapping regions between SMA-centered and absolute MM bands.

Data Source:Uses open, close, high, and low prices from the specified ticker and timeframe.

Optionally ignores wicks (high/low) for MM calculations, using max/min of open/close instead.

SMA Calculation:Computes a Simple Moving Average (SMA) based on the closing price and user-defined length.

Murrey Math Bands:Absolute MM Bands: Calculated using a dynamic range based on the highest/lowest prices over a lookback period, scaled logarithmically to create 13 levels (from -3/8 to +3/8, with 8/8 as the midpoint). These adapt to price action.

SMA-Centered MM Bands: Constructs MM bands relative to the SMA, with levels (0/8 to 8/8) spaced by a calculated increment derived from the absolute MM range.

Colors bands dynamically (green for bullish, red for bearish, gray for neutral) based on changes in the 4/8 level or increment, with labels indicating "Higher," "Lower," or "Same" states.

Fixed Fractal Bands:Plots six fixed-distance bands (±1, ±2, ±3) around the SMA, using a user-defined point value (default: 1.22).

Overlaps and Shading:Detects overlaps between SMA-centered and absolute MM bands at key levels (7/8-8/8, 0/8-1/8, and optionally 3/8-5/8).

Shades overlapping regions with distinct colors (red for 7/8-8/8, green for 0/8-1/8, blue for 3/8-5/8).

Fills specific SMA-centered MM regions (3/8-5/8, 0/8-1/8, 7/8-8/8) for visual emphasis.

Visualization:Plots SMA-centered MM bands, absolute MM bands, and fixed fractal bands as stepped lines with varying colors and transparency.

Displays a table at the bottom-right showing the current MM increment value.

Adds labels when the 4/8 level or increment changes, indicating trend direction.

In summary, this indicator combines a user-defined SMA with Murrey Math bands (both absolute and SMA-centered) and fixed fractal bands to provide a multi-level support/resistance framework. It highlights dynamic price levels, trend direction, and key overlaps, aiding traders in identifying potential reversal or consolidation zones.

Hurst‑Millard FLD Normalized 2.0 – Signals "Hurst-Millard FLD Normalized 2.0 – Signals" indicator. It analyzes price data using a combination of moving averages (MAs) and the Hurst exponent to decompose price movements into trend, swing, and noise components, generating buy and sell signals. Here's a brief overview of its functionality:Inputs and Modes:Offers Auto Mode (cycle-based) and Manual Mode for configuring three moving averages: Long-Term (LT), Mid-Term (MT), and Short-Term (ST).

Auto Mode calculates MA lengths and offsets based on user-defined target cycle lengths (e.g., LT: 400 bars, MT: 100 bars, ST: 25 bars) with predefined offset ratios (0.2, 0.333, 0.5 respectively).

Manual Mode allows direct input of MA lengths and offsets.

Moving Averages:Computes Simple Moving Averages (SMAs) for LT, MT, and ST based on the closing price.

Applies forward-shifting to simulate future price behavior (e.g., maLongFwd shifts the LT MA by the specified offset).

Decomposition:Trend: Derived from the forward-shifted LT MA (maLongFwd).

Swing: Calculated as the difference between MT and LT MAs, scaled as a percentage of the closing price and amplified (using ATR or a manual factor).

Noise: Calculated as the difference between ST and MT MAs, similarly scaled and amplified.

Hurst Exponent:Estimates the Hurst exponent to measure the persistence or mean-reversion of the noise component.

Uses a 50-bar lookback period, smoothed with a 5-period SMA.

Signal Generation:Generates buy signals when the noise component is less than the swing component and their difference is within a user-defined proximity threshold (default: 25% of swing).

Generates sell signals when noise exceeds swing within the same threshold.

Signals are plotted as diamond shapes at the calculated proximity price level.

Visualization:Plots the trend, swing, and noise components as lines with customizable colors and gradient intensity based on their relative strength.

Optional debugging plots for raw forward-shifted MAs and proximity thresholds.

Displays a periodic debug table (every 100 bars) showing key metrics like close price, MAs, trend, swing, noise, Hurst exponent, and more.

Additional Features:Supports ATR-based amplification for scaling swing and noise.

Allows customization of signal colors, diamond offsets, and proximity thresholds.

Includes debugging options to visualize raw MAs and proximity bands.

In summary, this indicator uses cycle-based or manually configured MAs to break down price action into trend, swing, and noise, calculates the Hurst exponent for noise analysis, and generates buy/sell signals based on the relationship between swing and noise within a proximity threshold. It’s designed for traders to identify potential trend reversals or continuations.

Breaout and followthroughThis indicator is designed to identify and highlight a single, powerful entry signal at the beginning of a new trend. It filters for high-volatility breakout bars that show strong directional conviction, helping traders catch the initial momentum of a potential move. It will only paint one bullish or bearish signal after a trend change is detected, preventing repeat signals during a sustained move.

Core Concept

The indicator combines four key concepts to generate high-probability signals:

Trend Direction: It first establishes the overall trend (bullish or bearish) using a configurable Exponential or Simple Moving Average (EMA/SMA).

Volatility Expansion: It looks for bars with a larger-than-average range by comparing the bar's size to the Average True Range (ATR). This helps identify moments of increased market interest.

Closing Strength (IBS): It uses the Internal Bar Strength (IBS) to measure directional conviction. A high IBS (closing near the top) suggests bullish strength, while a low IBS (closing near the bottom) suggests bearish pressure.

Breakout Confirmation: As an optional but powerful filter, it can confirm the signal by ensuring the bar is breaking above the high or below the low of a user-defined number of previous bars.

A signal is only generated on the first bar that meets all these criteria after the price crosses the trend-defining moving average, making it ideal for capturing the start of a new swing.

Features

Bullish Signals (Green): Highlights the first bar in an uptrend that is larger than the ATR, closes with a high IBS (>70), and optionally breaks out above the recent highs.

Bearish Signals (Red): Highlights the first bar in a downtrend that is larger than the ATR, closes with a low IBS (<30), and optionally breaks out below the recent lows.

"First Signal Only" Logic: The script is hard-coded to show only the initial signal in a new trend, filtering out noise and redundant signals.

Fully Customizable Trend Filter:

Choose between EMA or SMA for trend definition.

Set the MA length (default is a short-term 7-period MA).

Option to show or hide the moving average on the chart.

Optional Breakout Filter:

Enable or disable the requirement for the signal bar to break the high/low of previous bars.

Customize the lookback period for the breakout confirmation.

How to Use

This indicator can be used as a primary signal for a trend-following or momentum-based trading system.

Look for a Green Bar (Bullish Signal): This suggests the start of a potential uptrend. Consider it a signal for a long entry. A logical stop-loss could be placed below the low of the highlighted signal bar.

Look for a Red Bar (Bearish Signal): This suggests the start of a potential downtrend. Consider it a signal for a short entry. A logical stop-loss could be placed above the high of the highlighted signal bar.

Adjust Settings: Use the settings menu to configure the indicator to your preferred market and timeframe. A longer Trend MA Length will result in fewer, more long-term signals, while a shorter length will be more responsive.

As with any tool, this indicator is best used in conjunction with other forms of analysis, such as market structure, support/resistance levels, and proper risk management.

M Killzones[by vetrivel]Cool free style Session indicator, Inspired by TJR trader session times and it's easily changeable. Really this session times changes everything. Basic requirement to use this Discipline and Mindset

Dominance Signal Apex [CHE]]Dominance Signal Apex — Triple-confirmed entry markers with stateful guardrails

Summary

This indicator focuses on entry timing by plotting markers only when three conditions align: a closed-bar Heikin-Ashi bias, a monotonic stack of super-smoother filters, and the current HMA slope. A compact state machine provides guardrails: it starts a directional state on closed-bar Heikin-Ashi bias, maintains it only while the smoother stack remains ordered, and renders a marker only if HMA slope agrees. This design aims for selective signals and reduces isolated prints during mixed conditions. Markers fade over time to visualize the age and persistence of the current state.

Motivation: Why this design?

Common triggers flip frequently in noise or react late when regimes shift. The core idea is to gate entry markers through a closed-bar state plus independent filter alignment. The state machine limits premature prints, removes markers when alignment breaks, and uses the HMA as a final directional gate. The result is fewer mixed-context entries and clearer clusters during sustained trends.

What’s different vs. standard approaches?

Reference baseline: Single moving-average slope or classic MA cross signals.

Architecture differences:

Multi-length two-pole super-smoother stack with strict ordering checks.

Closed-bar Heikin-Ashi bias to start a directional state.

HMA slope as a final gate for rendering markers.

Time-based alpha fade to surface state age.

Practical effect: Entry markers appear in clusters during aligned regimes and are suppressed when conditions diverge, improving selectivity.

How it works (technical)

Measurements: Four recursive super-smoother series on price at short to medium horizons. Up regime means each shorter smoother sits below the next longer one; down regime is the inverse.

State machine: On bar close, positive Heikin-Ashi bias starts a bull state and negative bias starts a bear state. The state terminates the moment the smoother ordering breaks relative to the prior bar.

Rendering gate: A marker prints only if the active state agrees with the current HMA slope. The HMA is plotted and colored by slope for context.

Normalization and clamping: Marker transparency transitions from a starting to an ending alpha across a fixed number of bars, clamped within the allowed range.

Initialization: Persistent variables track state and bar-count since state start; Heikin-Ashi open is seeded on the first valid bar.

HTF/security: None used. State updates are closed-bar, which reduces repaint paths.

Bands: Smoothed high, low, centerline, and offset bands are computed but not rendered.

Parameter Guide

Show Markers — Toggle rendering — Default: true — Hides markers without changing logic.

Bull Color / Bear Color — Visual colors — Defaults: bright green / red — Aesthetic only.

Start Alpha / End Alpha — Transparency range — Defaults: one hundred / fifty, within zero to one hundred — Controls initial visibility and fade endpoint.

Steps — Fade length in bars — Default: eight, minimum one — Longer values extend the visual memory of a state.

Smoother Length — Internal band smoothing — Default: twenty-one, minimum two — Affects computed bands only; not drawn.

Band Multiplier — Internal band offset — Default: one point zero — No impact on markers.

Source — Input for HMA — Default: close — Align with your workflow.

Length — HMA length — Default: fifty, minimum one — Larger values reduce flips; smaller values react faster.

Reading & Interpretation

Entry markers:

Bull marker (below bar): Closed-bar Heikin-Ashi bias is positive, smoother stack remains aligned for up regime, and HMA slope is rising.

Bear marker (above bar): Closed-bar Heikin-Ashi bias is negative, smoother stack remains aligned for down regime, and HMA slope is falling.

Fade: Transparency progresses over the configured steps, indicating how long the current state has persisted.

Practical Workflows & Combinations

Trend following: Focus on marker clusters aligned with HMA color. Add structure filters such as higher highs and higher lows or lower highs and lower lows to avoid counter-trend entries.

Exits/Stops: Consider exiting or reducing risk when smoother ordering breaks, when HMA color flips, or when marker cadence thins out.

Multi-asset/Multi-TF: Suitable for liquid crypto, FX, indices, and equities. On lower timeframes, shorten HMA length and fade steps for faster response.

Behavior, Constraints & Performance

Repaint/confirmation: State transitions and marker eligibility are decided on closed bars; live bars do not commit state changes until close.

security()/HTF: Not used.

Resources: Declared max bars back of one thousand five hundred; recursive filters and persistent states; no explicit loops.

Known limits: Some delay around sharp turns; brief states may start in noisy phases but are quickly revoked when alignment fails; HMA gating can miss very early reversals.

Sensible Defaults & Quick Tuning

Start here: Keep defaults.

Too many flips: Increase HMA length and raise fade steps.

Too sluggish: Decrease HMA length and reduce fade steps.

Markers too faint/bold: Adjust start and end alpha toward lower or higher opacity.

What this indicator is—and isn’t

A selective entry-marker layer that prints only under triple confirmation with stateful guardrails. It is not a full system, not predictive, and does not handle risk. Combine with market structure, risk controls, and position management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

ARGT Possible entry and exit points:This is just an observation, and not any type of financial advice.

]To identify key entry and exit points. In addition, this is based on YTD and yearly charts. This is a work in progress.

SuperScript Filtered (Stable)🔎 What This Indicator Does

The indicator is a trend and momentum filter.

It looks at multiple well-known technical tools (T3 moving averages, RSI, TSI, and EMA trend) and assigns a score to the current market condition.

• If most tools are bullish → score goes up.

• If most tools are bearish → score goes down.

• Only when the score is very strong (above +75 or below -75), it prints a Buy or Sell signal.

This helps traders focus only on high-probability setups instead of reacting to every small wiggle in price.

________________________________________

⚙️ How It Works

1. T3 Trend Check

o Compares a fast and slow T3 moving average.

o If the fast T3 is above the slow T3 → bullish signal.

o If it’s below → bearish signal.

2. RSI Check

o Uses the Relative Strength Index.

o If RSI is above 50 → bullish momentum.

o If RSI is below 50 → bearish momentum.

3. TSI Check

o Uses the True Strength Index.

o If TSI is above its signal line → bullish momentum.

o If TSI is below → bearish momentum.

4. EMA Trend Check

o Looks at two exponential moving averages (fast and slow).

o If price is above both → bullish.

o If price is below both → bearish.

5. Score System

o Each condition contributes +25 (bullish) or -25 (bearish).

o The total score can range from -100 to +100.

o Score ≥ +75 → Strong Buy

o Score ≤ -75 → Strong Sell

6. Signal Filtering

o Only one buy is allowed until a sell appears (and vice versa).

o A minimum bar gap is enforced between signals to avoid clutter.

________________________________________

📊 How It Appears on the Chart

• Green “BUY” label below candles → when multiple signals agree and the market is strongly bullish.

• Red “SELL” label above candles → when multiple signals agree and the market is strongly bearish.

• Background softly shaded green or red → highlights bullish or bearish conditions.

No messy tables, no clutter — just clear trend-based entries.

________________________________________

🎯 How Traders Can Use It

This indicator is designed to help traders by:

1. Filtering Noise

o Instead of reacting to every small crossover or RSI blip, it waits until at least 3–4 conditions agree.

o This avoids entering weak trades.

2. Identifying Strong Trend Shifts

o When a Buy or Sell arrow appears, it usually signals a shift in momentum that can lead to a larger move.

3. Reducing Overtrading

o By limiting signals, traders won’t be tempted to jump in and out unnecessarily.

4. Trade Confirmation

o Traders can use the signals as confirmation for their own setups.

o Example: If your strategy says “go long” and the indicator also shows a strong Buy, that trade has more conviction.

5. Alert Automation

o Built-in alerts mean you don’t have to watch the chart all day.

o You’ll be notified only when a strong signal appears.

________________________________________

⚡ When It Helps the Most

• Works best in trending markets (bullish or bearish).

• Very useful on higher timeframes (1h, 4h, daily) for swing trading.

• Can also work on lower timeframes (5m, 15m) if combined with higher timeframe trend filtering.

________________________________________

👉 In short

This indicator is a signal filter + trend detector. It combines four powerful tools into one scoring system, and only tells you to act when the odds are stacked in your favor.

________________________________________

Debt Refinance Cycle + Liquidity vs BTC (Wk) — Overlay Part 1Debt Refi Cycle - Overlay script (BTC + Liquidity + DRCI/Z normalized to BTC range)

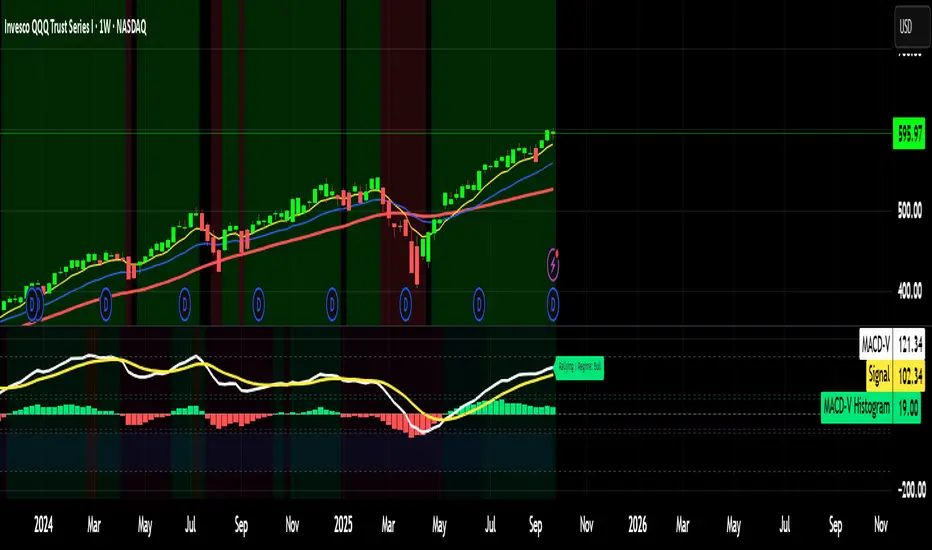

MACD-V MomentumThe MACD-V (Moving Average Convergence Divergence – Volatility Normalized) is an award-winning momentum indicator created by Alex Spiroglou, CFTe, DipTA (ATAA). It improves on the traditional MACD by normalizing momentum with volatility, solving several well-known limitations of classic indicators:

✅ Time stability – readings are consistent across history

✅ Cross-market comparability – works equally on stocks, crypto, forex, and commodities

✅ Objective momentum framework – universal thresholds at +150 / -150, +50 / -50

✅ Cleaner signals – reduces false signals in ranges and lag in high momentum

By dividing the MACD spread by ATR, the indicator expresses momentum in volatility units, allowing meaningful comparison across timeframes and markets.

MACD-V defines seven objective momentum states:

Risk (Oversold): below -150

Rebounding: -150 to +50 and above signal

Rallying: +50 to +150 and above signal

Risk (Overbought): above +150

Retracing: above -50 and below signal

Reversing: -150 to -50 and below signal

Ranging: between -50 and +50 for N bars

Optional background tints highlight the active regime (Bull above 200-MA, Bear below 200-MA).

Rare extremes (e.g., MACD-V < -100 in a bull regime) are tagged for additional context.

Use Cases

Identify and track momentum lifecycles across any market

Spot rare extremes for potential reversal opportunities

Filter out low-momentum whipsaws in ranging conditions

Compare momentum strength across multiple symbols

Support systematic and rule-based strategy development

SCTI - D14SCTI - D14 Comprehensive Technical Analysis Suite

English Description

SCTI D14 is an advanced multi-component technical analysis indicator designed for professional traders and analysts. This comprehensive suite combines multiple analytical tools into a single, powerful indicator that provides deep market insights across various timeframes and methodologies.

Core Components:

1. EMA System (Exponential Moving Averages)

13 customizable EMA lines with periods ranging from 8 to 2584

Fibonacci-based periods (8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584)

Color-coded visualization for easy trend identification

Individual toggle controls for each EMA line

2. TFMA (Multi-Timeframe Moving Averages)

Cross-timeframe analysis with 3 independent EMA calculations

Real-time labels showing trend direction and price relationships

Customizable timeframes for each moving average

Percentage deviation display from current price

3. PMA (Precision Moving Average Cloud)

7-layer moving average system with customizable periods

Fill areas between moving averages for trend visualization

Support and resistance zone identification

Dynamic color-coded trend clouds

4. VWAP (Volume Weighted Average Price)

Multiple anchor points (Session, Week, Month, Quarter, Year, Earnings, Dividends, Splits)

Standard deviation bands for volatility analysis

Automatic session detection and anchoring

Statistical price level identification

5. Advanced Divergence Detector

12 technical indicators for divergence analysis (MACD, RSI, Stochastic, CCI, Williams %R, Bias, Momentum, OBV, VW-MACD, CMF, MFI, External)

Regular and hidden divergences detection

Bullish and bearish signals with visual confirmation

Customizable sensitivity and filtering options

Real-time alerts for divergence formations

6. Volume Profile & Node Analysis

Comprehensive volume distribution analysis

Point of Control (POC) identification

Value Area High/Low (VAH/VAL) calculations

Volume peaks and troughs detection

Support and resistance levels based on volume

7. Smart Money Concepts

Market structure analysis with Break of Structure (BOS) and Change of Character (CHoCH)

Internal and swing structure detection

Equal highs and lows identification

Fair Value Gaps (FVG) detection and visualization

Liquidity zones and institutional flow analysis

8. Trading Sessions

9 major trading sessions (Asia, Sydney, Tokyo, Shanghai, Hong Kong, Europe, London, New York, NYSE)

Real-time session status and countdown timers

Session volume and performance tracking

Customizable session boxes and labels

Statistical session analysis table

Key Features:

Modular Design: Enable/disable any component independently

Real-time Analysis: Live updates with market data

Multi-timeframe Support: Works across all chart timeframes

Customizable Alerts: Set alerts for any detected pattern or signal

Professional Visualization: Clean, organized display with customizable colors

Performance Optimized: Efficient code for smooth chart performance

Use Cases:

Trend Analysis: Identify market direction using multiple EMA systems

Entry/Exit Points: Use divergences and structure breaks for timing

Risk Management: Utilize volume profiles and session analysis for better positioning

Multi-timeframe Analysis: Confirm signals across different timeframes

Institutional Analysis: Track smart money flows and market structure

Perfect For:

Day traders seeking comprehensive market analysis

Swing traders needing multi-timeframe confirmation

Professional analysts requiring detailed market structure insights

Algorithmic traders looking for systematic signal generation

---

中文描述

SCTI - D14是一个先进的多组件技术分析指标,专为专业交易者和分析师设计。这个综合套件将多种分析工具整合到一个强大的指标中,在各种时间框架和方法论中提供深度市场洞察。

核心组件:

1. EMA系统(指数移动平均线)

13条可定制EMA线,周期从8到2584

基于斐波那契的周期(8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584)

颜色编码可视化,便于趋势识别

每条EMA线的独立切换控制

2. TFMA(多时间框架移动平均线)

跨时间框架分析,包含3个独立的EMA计算

实时标签显示趋势方向和价格关系

每个移动平均线的可定制时间框架

显示与当前价格的百分比偏差

3. PMA(精密移动平均云)

7层移动平均系统,周期可定制

移动平均线间填充区域用于趋势可视化

支撑阻力区域识别

动态颜色编码趋势云

4. VWAP(成交量加权平均价格)

多个锚点(交易时段、周、月、季、年、财报、分红、拆股)

标准差带用于波动性分析

自动时段检测和锚定

统计价格水平识别

5. 高级背离检测器

12个技术指标用于背离分析(MACD、RSI、随机指标、CCI、威廉姆斯%R、Bias、动量、OBV、VW-MACD、CMF、MFI、外部指标)

常规和隐藏背离检测

看涨看跌信号配视觉确认

可定制敏感度和过滤选项

背离形成的实时警报

6. 成交量分布与节点分析

全面的成交量分布分析

控制点(POC)识别

价值区域高/低点(VAH/VAL)计算

成交量峰值和低谷检测

基于成交量的支撑阻力水平

7. 聪明钱概念

市场结构分析,包括结构突破(BOS)和结构转变(CHoCH)

内部和摆动结构检测

等高等低识别

公允价值缺口(FVG)检测和可视化

流动性区域和机构资金流分析

8. 交易时区

9个主要交易时段(亚洲、悉尼、东京、上海、香港、欧洲、伦敦、纽约、纽交所)

实时时段状态和倒计时器

时段成交量和表现跟踪

可定制时段框和标签

统计时段分析表格

主要特性:

模块化设计:可独立启用/禁用任何组件

实时分析:随市场数据实时更新

多时间框架支持:适用于所有图表时间框架

可定制警报:为任何检测到的模式或信号设置警报

专业可视化:清洁、有序的显示界面,颜色可定制

性能优化:高效代码确保图表流畅运行

使用场景:

趋势分析:使用多重EMA系统识别市场方向

入场/出场点:利用背离和结构突破进行时机选择

风险管理:利用成交量分布和时段分析进行更好定位

多时间框架分析:在不同时间框架间确认信号

机构分析:跟踪聪明钱流向和市场结构

适用于:

寻求全面市场分析的日内交易者

需要多时间框架确认的摆动交易者

需要详细市场结构洞察的专业分析师

寻求系统化信号生成的算法交易者

Уровни SL/TP и значение ATR первого часаSession Range SL/TP Levels with Advanced ATR

Overview

The Session Range SL/TP Levels indicator is a comprehensive tool designed for session-based trading strategies, particularly for breakouts. It identifies the high and low of a user-defined time range (e.g., the Asian session) and uses a sophisticated, customizable Average True Range (ATR) calculation to project key Stop Loss (SL) and Take Profit (TP) levels.

This indicator helps traders visualize potential entry and exit points based on the volatility of a specific trading session, with all crucial data presented in a clean on-screen table.

Key Features

Customizable Trading Session: Define any time range to establish your core trading zone. The indicator will automatically find the high and low of this period.

Advanced ATR Calculation: The indicator uses an ATR calculated on a 5-minute timeframe for higher precision. You can customize:

The ATR length and smoothing method (RMA, SMA, EMA, WMA).

A unique percentage reduction from the ATR to create a more conservative volatility buffer.

Volatility-Based SL/TP Levels: Automatically calculates and plots multiple SL and TP levels for both long and short scenarios based on user-defined multipliers of the modified ATR.

Comprehensive On-Screen Display: A detailed on-screen table provides all critical data at a glance, including:

The original 5-min ATR value.

The modified ATR after the percentage reduction.

Three custom ATR-multiple values for quick reference.

All calculated SL and TP price levels for both Long and Short setups.

Copy-Friendly Data Logging: With a single click in the settings, you can print all calculated values into the Pine Logs panel, allowing for easy copying and pasting into other applications or trading journals.

How to Use

Define Your Session: In the settings, enter the time for the trading session you want to analyze (e.g., "0200-0300" for a part of the Asian session).

Identify the Range: The indicator will draw the high and low of this session once the time period is complete.

Plan Your Trade: The calculated levels provide potential targets for breakout trades.

For a Long Trade: If the price breaks above the session high, the green Take Profit lines (TP1, TP2, TP3) serve as potential exit points, while the Stop Loss (Long) level serves as a volatility-based stop.

For a Short Trade: If the price breaks below the session low, the red Take Profit lines serve as potential targets, with the Stop Loss (Short) level as the corresponding stop.

Reference the Table: Use the on-screen table to see the exact price levels and ATR values without needing to hover over the lines.

ATR Regime Study [CHE] ATR Regime Study — ATR percentile regimes with clear bands, table and live label

Summary

This study classifies volatility into five regimes by converting ATR into a percentile rank over a rolling window, plotted on a standardized scale between zero and one hundred. Colored bands mark regime thresholds, while a compact table and an optional label report the current percentile and regime. The standardized scale makes symbols and timeframes easier to compare than raw ATR values. Implemented in Pine v6 as a separate pane (overlay set to false), it is a context tool to adapt tactics and risk handling to the prevailing volatility environment.

Motivation: Why this design?

Raw ATR varies with price scale and asset characteristics, which makes regime comparison inconsistent and leads to poor transfer of settings across symbols and timeframes. The core idea is to transform ATR into a percentile rank within a user-defined lookback, then map it into discrete regimes. This yields a stable, interpretable context signal that shifts slower than raw ATR while still responding to genuine volatility changes.

What’s different vs. standard approaches?

Reference baseline: Traditional ATR plots or ATR bands using fixed multipliers.

Architecture differences:

Percentile ranking of ATR within a rolling window.

Five discrete regimes with fixed thresholds at ninety, seventy, thirty, and ten.

Visual fills between thresholds plus a live table and a last-bar label.

Practical effect: You read a single normalized line between zero and one hundred with consistent thresholds. This improves cross-asset comparison and makes regime shifts obvious at a glance.

How it works (technical)

The script computes ATR over a configurable length, then converts that series to a percentile rank over a configurable number of bars. The percentile is naturally scaled and limited between zero and one hundred. That value is mapped to one of five regimes: above ninety (Extreme), between seventy and ninety (Elevated), between thirty and seventy (Normal), between ten and thirty (Calm), and below ten (Squeeze). Horizontal guide lines mark the thresholds, and fills shade the regions. A table is created once and updated on each bar to show regime definitions and highlight the current row. An optional label on the last bar displays the current percentile and regime. No higher-timeframe requests are used, so repaint risk is limited to normal live-bar fluctuation until the bar closes.

Parameter Guide

ATR length — Effect: Controls how fast ATR reacts to new ranges. Default: fourteen. Trade-offs/Tips: Increase to reduce noise in choppy markets; decrease to react faster during regime changes.

Percentile window (bars) — Effect: Number of bars used for the percentile ranking. Default: two hundred fifty-two. Trade-offs/Tips: Larger windows stabilize the percentile but slow adaptation after structural regime shifts; smaller windows adapt faster but may flip more often.

Table › Show — Effect: Toggles the regime overview table. Default: enabled. Trade-offs/Tips: Disable on constrained layouts to reduce visual clutter.

Table › Position — Effect: Anchors the table in a chart corner. Default: Top Right. Trade-offs/Tips: Choose a corner that avoids overlapping other panels or drawings.

Label › Show — Effect: Toggles a last-bar label with current percentile and regime. Default: enabled. Trade-offs/Tips: Useful for quick reads; disable if it obscures other annotations.

Reading & Interpretation

The white line shows ATR percentile between zero and one hundred. Crossing above seventy signals an elevated volatility environment; above ninety indicates event-driven extremes. Between thirty and seventy represents typical conditions. Between ten and thirty indicates calm conditions that often suit mean reversion. Below ten reflects compression, where breakout probability often increases. The colored bands visually reinforce these ranges. The table summarizes regime definitions and highlights the current state. The last-bar label mirrors the current percentile and regime for quick inspection.

Practical Workflows & Combinations

Trend following: Prefer continuation tactics when the percentile holds in the Normal or Elevated bands and structure confirms higher highs and higher lows. Consider wider stops and partial position sizing as percentile rises.

Mean reversion: Favor fades in Calm regimes within defined ranges; use structure filters and time-of-day constraints to avoid low-liquidity whipsaws.

Breakout preparation: Track compressions below ten; plan entries only with structure confirmation and risk caps, since compressions can persist.

Multi-asset/Multi-TF: Defaults travel well on daily charts. For intraday, reduce the percentile window to align with session dynamics. Combine with trend or market structure tools for confirmation.

Behavior, Constraints & Performance

Repaint/confirmation: The percentile updates during live bars and stabilizes on close; closed bars do not repaint.

security/HTF: Not used. If you add higher-timeframe aggregation externally, account for standard repaint caveats.

Resources: Declared maximum bars back is two thousand; limits for lines and labels are five hundred each. A short loop updates the table rows; arrays are used for table content only.

Known limits: Regime boundaries are fixed; assets with persistent volatility shifts may require window retuning. Low-liquidity periods and gaps can produce abrupt percentile changes. ATR is direction-agnostic and should be paired with trend or structure context.

Sensible Defaults & Quick Tuning

Start with ATR length fourteen and percentile window two hundred fifty-two on daily charts.

Too many flips: Increase ATR length or increase the percentile window.

Too sluggish: Decrease the percentile window or reduce ATR length.

Intraday noise: Keep ATR length moderate and reduce the window to a session-appropriate size; optionally hide the label to declutter.

Compressed markets: Maintain defaults but rely more on structure and volume filters before acting.

What this indicator is—and isn’t

This is a volatility regime context layer that standardizes ATR into interpretable regimes. It is not a complete trading system, not predictive, and not a stand-alone entry signal. Use it alongside structure analysis, confirmation tools, and disciplined risk management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

Jasons Bullish Reversal DetectorThis bullish reversal detector is designed to spot higher-quality turning points instead of shallow bounces. At its core, it looks for candles closing above the 20-period SMA, a MACD bullish crossover, and RSI strength above 50. On top of that, it layers in “depth” filters: price must reclaim and retest a long-term baseline (like the 200-period VWMA), momentum should confirm with RSI and +DI leading, short-term EMAs need to slope upward, and conditions like overheated ATR or strong downside ADX will block false signals. When all of these align, the script flags a depth-confirmed bullish reversal, aiming to highlight spots where structure, momentum, and volatility all support a sustainable shift upward.

4 Stages of StockThis script uses 40Weekly MA to baseline larges trends in the stock. This is based on Puru's idea of 4 Stage of Stock.

Stage 1 (Basing)

Stage 2 (Advancing)

Stage 3 (Topping)

Stage 4 (Declining)

This is best viewed and understood on weekly charts.

Opening Range BoxThis indicator, called the "Opening Range Box," is a visual tool that helps you track the start of key trading sessions like London and New York.

It does three main things:

Finds the Daily 'First Move': It automatically calculates the High and Low reached during the first 30 minutes (or whatever time you set) of each defined session.

Draws a Box: It immediately draws a colored, transparent box on your chart from the moment the session starts. This box acts as a clear reference for the session's initial boundaries.

Extends the Levels: After the initial 30 minutes are over, the box stops growing vertically (it locks in the OR High/Low) but continues to stretch out horizontally for the rest of the trading session. This allows you to easily see how the price reacts to the opening levels throughout the day.

In short: It visually highlights the most important price levels established at the very beginning of the major market sessions.

Pattern Match & Forward Projection – Weekly (EN)

Overview

This indicator searches for recurring price patterns in weekly data and projects their average forward performance.

The logic is based on historical pattern repetition: it scans past price sequences similar to the most recent one, then aggregates their forward returns to estimate potential outcomes.

⚠️ Important: The indicator is designed for weekly timeframe only. Using it on daily or intraday charts will trigger an error message.

Settings (Inputs)

Pattern Settings

Pattern length (weeks): Number of weeks used to define the reference pattern.

Forward length (weeks): Number of weeks into the future to evaluate after each pattern match.

Lookback (weeks): Historical window to scan for past pattern matches.

Normalize by shape (z-score): If enabled, patterns are normalized by z-score, focusing on shape similarity rather than absolute values.

Distance threshold (Euclidean): Maximum allowed Euclidean distance between the reference pattern and historical candidates. Smaller values = stricter matching.

Min. required matches: Minimum number of valid matches needed for analysis.

Quality Filters

Min required Hit%: Minimum percentage of positive outcomes (upside forward returns) required for the pattern to be considered valid.

Return filter mode:

Either: absolute average return ≥ threshold

Long only: average return ≥ threshold

Short only: average return ≤ -threshold

Min avg return (%): Minimum average forward return threshold for validation.

Visual Options

Highlight historical matches (labels): Marks where in history similar patterns occurred.

Max match labels to draw: Caps the number of match markers shown to avoid clutter.

Draw average projection: Displays the average projected forward curve if conditions are met.

Show summary panel: Enables/disables the information panel.

Show weekly avg curve in panel: Adds a breakdown of average returns week by week.

Projection color: Choose the color of the projected forward curve.

What the Screen Shows

Summary Panel (top-left by default)

Total matches found in history

Matches with valid forward data

Average, minimum, and maximum distance (similarity measure)

Average forward return and Hit%

Distance threshold and normalization setting

Weekly average forward curve (if enabled)

Quality filter results (pass/fail)

Projection Curve (dotted line on price chart)

Drawn only if enough valid matches are found and filters are satisfied

Represents the average forward performance of historical matches, anchored at the current bar

Historical Match Labels (▲ markers)

Small arrows below past bars where similar patterns occurred

Tooltip: “Historical match”

Forecast Logic

The indicator does not predict the future in a deterministic way.

Instead, it relies on a pattern-matching algorithm:

The most recent N weeks (defined by Pattern length) are taken as the reference.

The algorithm scans the last Lookback (weeks) for segments with similar shape and magnitude.

Similarity is measured using Euclidean distance (optionally z-score normalized).

For each valid match, the subsequent Forward length weeks are collected.

These forward paths are averaged to generate a composite forward projection.

The summary panel reports whether the current setup passes the quality filters (Hit% and minimum average return).

Usage Notes

Best used as a contextual tool, not a standalone trading system.

Works only on weekly timeframe.

Quality filters help distinguish between noisy and statistically meaningful patterns.

A higher number of matches usually improves reliability, but very strict thresholds may reduce sample size.

📊 This tool is useful for traders who want to evaluate how similar historical setups have behaved and to visualize potential forward paths in a statistically aggregated way.

Best MA Finder: Sharpe/Sortino ScannerThis script, Best MA Finder: Sharpe/Sortino Scanner, is a tool designed to identify the moving average (SMA or EMA) that best acts as a dynamic trend threshold on a chart, based on risk-adjusted historical performance. It scans a wide range of MA lengths (SMA or EMA) and selects the one whose simple price vs MA crossover delivered the strongest results using either the Sharpe ratio or the Sortino ratio. Reading it is intuitive: when price spent time above the selected MA, conditions were on average more favorable in the backtest; below, less favorable. It is a trend and risk gauge, not an overbought or oversold signal.

What it does:

- Runs individual long-only crossover backtests for many MA lengths across short to very long horizons.

- For each length, measures the total number of trades, the annualized Sharpe ratio, and the annualized Sortino ratio.

- Uses the chosen metric value (Sharpe or Sortino) as the score to rank candidates.

- Applies a minimum trade filter to discard statistically weak results.

- Optionally applies a local stability filter to prefer a length that also outperforms its close neighbors by at least a small margin.

- Selects the optimal MA and displays it on the chart with a concise summary table.

How to use it:

- Choose MA type: SMA or EMA.

- Choose the metric: Sharpe or Sortino.

- Set the minimum trade count to filter out weak samples.

- Select the risk-free mode:

Auto: uses a short-term risk-free rate for USD-priced symbols when available.

Manual: you provide a risk-free ticker.

None: no risk-free rate.

- Optionally enable stability controls: neighbor radius and epsilon.

- Toggle the on-chart summary table as needed.

On-chart output:

- The selected optimal MA is plotted.

- The optional table shows MA length, number of trades, chosen metric value annualized, and the annual risk-free rate used.

Key features:

- Risk-adjusted optimization via Sharpe or Sortino for fair, comparable assessment.

- Broad MA scan with SMA and EMA support.

- Optional stability filter to avoid one-off spikes.

- Clear and auditable presentation directly on the chart.

Use cases:

- Traders who want a defensible, data-driven trend threshold without manual trial and error.

- Swing and trend-following workflows across timeframes and asset classes.

- Quick SMA vs EMA comparisons using risk-adjusted results.

Limitations:

- Not a full trading strategy with position sizing, costs, funding, slippage, or stops.

- Long-only, one position at a time.

- Discrete set of MA lengths, not a continuous optimizer.

- Requires sufficient price history and, if used, a reliable risk-free series.

This script is open-source and built from original logic. It does not replicate closed-source scripts or reuse significant external components.

30-10-3 MAX,min dynamicsSupported timeframes: The script works only on timeframes of 1 minute or lower (including second-based timeframes).

Displayed levels: The highs and lows of the last closed candle are plotted for the 30-minute, 10-minute, and 3-minute timeframes.

Updates: The levels update only when a candle closes in the respective timeframe (e.g., every 30 minutes for the 30m levels).

Visualization: Dashed lines for highs and lows (blue for 30m, green for 10m, red for 3m).

Labels indicating "Max 30m", "Min 30m", etc., positioned above the highs and below the lows.

Period Separator - MTF with Price LevelsPeriod Separator - MTF with Price Levels

A customizable multi-timeframe period separator indicator that displays a user-defined number of vertical lines with corresponding horizontal price levels.

Key Features:

Multi-Timeframe Support: Works with all timeframes from 1-minute to yearly (12M, 3M, M, W, D, 4H, 1H, 15m, 5m, 1m)

Complete Price Level Analysis: Shows horizontal lines for High, Low, 0.75, 0.50, 0.25, and Open levels for all visible periods between vertical separators

Seconds Chart Compatibility: Special 1-minute separator option for seconds timeframes

Full Customization: Independent color, style, and width settings for all lines

Smart Alerts: Optional price break alerts for high/low levels with sound options

Clean Memory Management: Automatically manages line objects to prevent chart clutter

Sliding Window Display: Set exactly how many vertical separator lines to show (1-20), with older lines automatically removed as new periods begin

Perfect for:

Session/period analysis with controlled visual complexity

Support/resistance level identification across multiple periods

Fibonacci-style level trading between defined time periods

Clean chart presentation with limited historical data display

Settings:

Number of Vertical Lines: Controls exactly how many period separators are visible

All price levels can be toggled on/off independently

Comprehensive styling options for professional chart presentation

Ideal for traders who want period-based analysis without overwhelming their charts with too many historical lines.

30-10-3 MAX,min dinamici Supported timeframes: The script works only on timeframes of 1 minute or lower (including second-based timeframes).

Displayed levels: The highs and lows of the last closed candle are plotted for the 30-minute, 10-minute, and 3-minute timeframes.

Updates: The levels update only when a candle closes in the respective timeframe (e.g., every 30 minutes for the 30m levels).

Visualization: Dashed lines for highs and lows (blue for 30m, green for 10m, red for 3m).

Labels indicating "Max 30m", "Min 30m", etc., positioned above the highs and below the lows.

Mystic Pulse V2.0 [CHE] Mystic Pulse V2.0 — Adaptive DI streaks with gradient intensity for clearer trend persistence

Summary

Mystic Pulse V2.0 measures directional persistence by counting how often the positive or negative directional index strengthens and dominates. These counts drive gradient colors for bars, wicks, and helper plots, so intensity reflects local momentum rather than absolute values. A windowed normalization and gamma control adapt the visuals to recent conditions, preventing one regime from overpowering the next. The result is an immediate, at-a-glance read of trend direction and stamina without relying on crossovers alone.

Motivation: Why this design?

Classical DI and ADX signals can flip during choppy phases or feel sluggish in calm regimes. This script focuses on persistence: it increments a positive or negative streak only when the corresponding directional pressure both strengthens compared with the prior bar and dominates the other side. Simple OHLC pre-smoothing reduces micro-noise, and local normalization keeps the scale relevant to the last segment of data, not a distant past.

What’s different vs. standard approaches?

Reference baseline: Traditional DI and ADX lines with crossovers and fixed-scale thresholds.

Architecture differences:

Wilder-style recursive smoothing on true range and directional movement.

Streak counters for positive and negative pressure that advance only on strengthening and dominance.

Windowed normalization and gamma shaping for visual intensity.

Wick coloring via `plotcandle` with forced overlay from a pane indicator.

Practical effect: Bars and wicks grow more vivid during sustained pressure and fade during indecision. The column plots show streak depth directly, which helps filter one-bar flips.

How it works (technical)

1. Pre-smoothing: Open, high, low, and close are averaged over a short simple moving window to dampen micro-ticks.

2. Directional inputs: True range and directional movement are formed from the smoothed prices, then recursively smoothed using a Wilder-style update that carries prior state forward.

3. DI comparison: The script derives positive and negative directional ratios relative to smoothed range. A side advances its streak when it increases compared with the previous bar and exceeds the opposite side. The other streak resets.

4. Trend score and color base: The difference between positive and negative streaks defines the active side.

5. Normalization and gamma: The absolute streak magnitude and each side’s streak are normalized within a rolling window. Gamma parameters reshape intensity so mid-range values are either compressed or emphasized.

6. Rendering:

Two column plots show positive and negative streak counts in the pane with gradient colors.

A square marker at the bottom uses the global gradient as a compact heat cue.

Bar colors on the main chart use either the gradient, neutral trend colors, or no paint depending on toggles.

Wick, border, and candle overlays are colored via `plotcandle` with forced overlay.

7. State handling: Smoothed values and counters persist across bars; initialization uses first available values without lookahead. No higher-timeframe requests are used, so repaint risk is limited to normal live-bar evolution.

Parameter Guide

Show neutral candles (fallback) — Paints main-chart bars in plain up or down colors when gradients are disabled — Default false — Use when you prefer simple up/down coloring.

Show last N shapes — Limits bottom square markers — Default 333 — Reduce if your chart gets cluttered.

ADX smoothing length — Controls the Wilder smoothing window for range and directional movement — Default 9 — Larger values increase stability but respond later.

OHLC SMA length — Pre-smoothing for inputs — Default 1 — Increase slightly on noisy assets to reduce flip risk.

Gradient barcolor — Enables gradient bar paint on the main chart — Default true — Turn off to use wicks only or neutral bars.

Wick coloring — Colors wicks, borders, and bodies via overlay — Default true — Disable if it conflicts with other overlays.

Gradient window — Lookback for local normalization — Default 100 — Shorter windows adapt faster; longer windows provide steadier intensity.

Gradient transparency — Overall transparency for gradient paints — Default 0 — Increase to make gradients subtler.

Gamma bars/shapes — Contrast for bar and shape intensity — Default 0.70 — Lower values brighten mid-tones; higher values compress them.

Gamma plots — Contrast for the column plots — Default 0.80 — Tune separately from bar intensity.

Wick transparency — Transparency for wick coloring — Default 0 — Raise to let price action show through.

Up/Down colors (dark and neon) — Base and accent colors for both directions — Defaults as provided — Adjust to match your chart theme.

Reading & Interpretation

Pane columns: The green column represents the positive streak count; the red column represents the negative streak count. Taller columns signal stronger persistence.

Gradient marker: The bottom square indicates the active side and persistence strength at a glance.

Main-chart bars and wicks: Color direction shows the dominant side; intensity reflects the normalized and gamma-shaped streak magnitude. Faded tones suggest weak or fading pressure.

Practical Workflows & Combinations

Trend following: Enter in the direction of the active side when the corresponding column expands over several bars. Confirm with structure such as higher highs and higher lows or lower highs and lower lows.

Exits and stops: Consider scaling out when intensity fades toward mid-range while structure stalls. Tighten stops after extended streaks or when wicks lose intensity.

Multi-asset/Multi-TF: Use defaults for liquid assets on intraday to swing timeframes. For highly volatile instruments, raise smoothing and the normalization window. For calm markets, lower them to regain sensitivity.

Behavior, Constraints & Performance

Repaint/confirmation: Values update during the live bar and stabilize after bar close. No historical repaint beyond normal live-bar updates.

security()/HTF: Not used; cross-timeframe repaint paths do not apply.

Resources: Declared `max_bars_back` two thousand; no explicit loops or arrays; plot and label limits are generous.

Known limits: Streak counters can remain elevated during slow reversals. Very short normalization windows can cause rapid intensity swings. Gaps or extreme spikes may temporarily distort intensity until the window adapts.

Sensible Defaults & Quick Tuning

Start with: ADX smoothing nine, OHLC SMA one, normalization window one hundred, gradient and wick coloring enabled, gamma around zero point seven to zero point eight.

Too many flips: Increase ADX smoothing and the normalization window; consider a small bump in OHLC SMA.

Too sluggish: Decrease ADX smoothing and the normalization window.

Colors overpower chart: Increase gradient and wick transparency or raise gamma to compress mid-tones.

What this indicator is—and isn’t

This is a visualization and signal layer that represents directional persistence and intensity. It does not issue trade entries or exits on its own and is not predictive. Use it alongside market structure, volume, and risk controls.

Disclaimer

The content, including any code, is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument. Trading involves substantial risk, including the possible loss of principal. Past performance is not indicative of future results. Always do your own research and consider consulting a qualified professional.

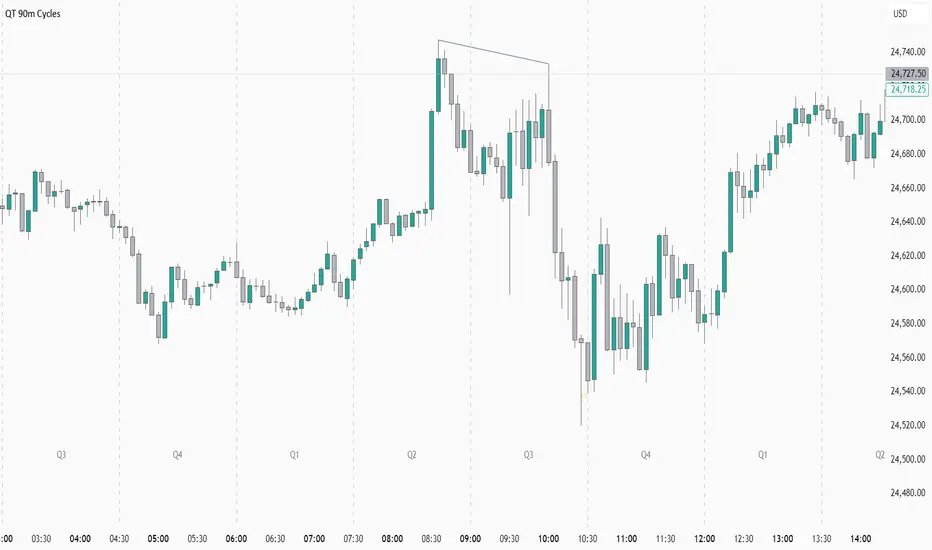

Quarterly Theory - 90m Cycles This Indicator Give you the Exact 90 mins cycles for the market and add background colors to each session over it.