Buy/Sell Signals [WynTrader]My name is WynTrader. I cumulate 24 years of experience.

This Indicator produces Buy/Sell Signals using these features:

- Fast and Slow Moving averages (modifiable) optimized at EMA-8 and SMA-35

- Bollinger Bands (modifiable) optimized at Basis-18 and Multiplier-1

Also, the Buy/Sell Signals are conditioned by three Filters (optionable, modifiable) :

. Bollinger-Bands Lookback

. High-Low vs Candle Range %

. Distance from Fast and Slow Moving averages %

The Results Calculation presented in a Table are based :

- on the Current Chart Visible Range (optionable)

or

- on the specified TIme Frame Start and End Dates (modifiable)

The Table shows Calculation Results of the Buy and Sell Signals that are activated on the chart, with the Number of Trades (Signals), the Winning Points and the Win Rate %. The Buy&Hold starts calculation at the first Buy encountered.

So be surprised by my Buy/Sell Indicator. But always remember that the world is not perfect. The Graal Indicator, even with AI, doesn't already exist, maybe one day (all of us richier...), but not now. , depending on the chart product (stocks...), volatility, probabilities, unpredictable behaviour. , the moves, etc.

Enjoy

WynTrader

P. s. :

My name is WynTrader. I cumulate 24 years of experience. In 2001, I took an intensive technical analysis course taught by an exceptional friend, Cyril, who taught me everything I know. The foundation I gained through his teaching remains solid and relevant to this day, never failing me.

Before i made this Indicator, I have used many Trading View Buy/Sell Indicators using alone or combined RSI, SMI, OBV, MACD ATR, ADX, Neural, Fractal, Geometry, etc., that are already available for the Trading View community. A great thanks to those who give their time that help me build this tool.

Note that I'm not a programmer, so... ;-)

Siklus

BTC Flow Dashboard : Spot Premium + OI + Funding + Cycle SignalsSpot Premium vs Perpetual Basket (%):

Tracks how aggressively perps are trading relative to spot, a leading indicator of speculative activity and leverage buildup.

Aggregated Open Interest Z-Score:

A normalized view of OI expansion/contraction across major exchanges (Binance, BitMEX, Bybit, Kraken, etc.), highlighting when leverage enters overheated zones.

Composite Funding Rate Analysis:

Calculates a TWAP-smoothed funding composite across major venues, with optional APR scaling, showing where perpetual markets are paying for long or short exposure.

Confluence Signal Engine:

Dynamically flags bullish or bearish market conditions based on premium behavior and leverage environment — including over-leverage warnings that often precede volatility spikes.

Extreme Cycle Tops & Bottoms (Experimental):

Optional signal module that highlights historically significant extremes (e.g., 2020 bottom or 2021 top) based on statistical Z-score thresholds across the three core metrics.

Notes & Tips

Works best on weekly or monthly timeframes for macro cycle analysis.

Daily and 3D views provide short-term leverage context but may produce more frequent signals.

The Extreme Signal Engine is experimental — not a trading signal on its own, but a contextual tool to support macro decision-making.

Turtle Soup Multi Timeframe (D + 30m)

This indicator indicates when there is a turtle soup with a 30-minute timeframe aligned with a one-day timeframe.

US Construction Spending & Manufacturing Employment YoY % ChangeUsage Notes: Timeframe: Use a monthly chart, as TTLCONS and MANEMP are monthly data. Other timeframes result in interpolation.

Data Availability: As of October 2025, TTLCONS is available until July 2025 and MANEMP until August 2025 (automatically via TradingView).

The Unsung Heroes: Why C&M Are the True Indicators

Imagine the economy is a highly sensitive vehicle. Quarterly reported GDP is like a quarterly glance at the odometer—it's slow, often delayed, and clearly refers to the past. Anyone who wants to predict future developments needs something much faster.

This is where construction and manufacturing come into play. These two sectors are the machine builders of the economy and provide us with real-time feedback. They form the backbone of economic forecasting for several important reasons:

1. Monetary policy indicators: Both sectors are highly sensitive to monetary policy developments, such as interest rate changes. If developers are unable to finance large residential or commercial projects and manufacturers postpone capital-intensive factory expansions, for example, declines in construction demand would quickly affect other sectors.

2. The backbone of the secondary sector: These industries constitute the secondary sector of the economy, meaning they are concerned with the actual transformation and production of goods, not just the extraction of raw materials or the provision of intangible services. One could argue that while they only account for about 15% of GDP in the US, their impact is massive and cyclical.

3. The timeliness advantage: Forget quarterly lags. Both construction output and manufacturing employment data are released monthly. This timely, frequent data allows analysts to assess economic momentum much more quickly than if they had to wait for delayed GDP reports.

In the US, some analysts have even titled their articles with the bold claim: "Housing construction is the business cycle." Fluctuations in housing construction are frequent and large, and a decline in activity is almost always accompanied by a subsequent decline in GDP.

NF_PLASMA_SURGE 🧩 NF_PLASMA_SURGE (NightFury Systems)

Author: Lachin M. Akhmedov (aka NightFury)

⚙️ A volumetric impulse oscillator detecting real candle energy through body density, directional momentum, and normalized volatility thrust.

🧠 Core Concept:

Not another RSI. Not another MACD.

NF_PLASMA_SURGE isolates true directional impulse by measuring the physics of price:

Body Energy → how much of each candle’s range is real movement.

Volume Thrust → amplifies strong participation only.

Volatility Normalization → filters emotional spikes and fake momentum.

⚡ Outputs:

Toxic Green = Real buy impulse (surge ignition)

Red Inferno = Real sell impulse (energy drain)

⚡ marks = Charged bursts detected (|z| > threshold)

💫 Synergy:

Designed to integrate with NF_CYBER_FURY as its ignition companion —

Cyber powers the reactor; Plasma lights the core.

🧩 Recommended Stack:

NF_CYBER_FURY + NF_PLASMA_SURGE = The NightFury Reactor System

OPEX VIXEX datesUpdated ohlocracy's OPEX script till 2030

These dates are for standard equity, index, and ETF options expiration managed by OCC, with monthly expirations usually on the third Friday and weekly expirations on other Fridays, except holidays which cause adjustments to Thursdays or nearby trading days.

Quarterly options expiration dates in the US stock market are on the last trading day of the quarter, usually the last business day of March, June, September, and December.

These dates are the last trading day of each quarter, accounting for weekends and holidays when the market is closed. When the last calendar day falls on a weekend, the expiration is set to the last prior trading day.

The VIX monthly expiration is on the Wednesday prior to the stock market monthly opex (third Friday). When holidays affect these days, the expiration shifts to the business day before.

Experimental Supertrend [CHE]Experimental Supertrend — Combines EMA crossovers for trend regime detection with an adaptive ATR-based hull that selects the narrowest band to contain recent highs and lows, minimizing false breaks in varying volatility.

Summary

This indicator overlays a dynamic supertrend boundary around a midline derived from dual EMAs, using EMA crossovers to switch between bullish and bearish regimes. The hull adapts by evaluating multiple ATR periods and selecting the tightest one that fully encloses price action over a specified window, which helps in creating more stable trend lines that hug price without excessive gaps or breaches. Fills between the midline and hull provide visual cues for trend strength, darkening temporarily after regime changes to highlight transitions. Alerts trigger on crossovers, and markers label entry points, making it suitable for trend-following setups where standard supertrends might whipsaw. Overall, it offers robustness through auto-adjustment, reducing sensitivity to noise while maintaining responsiveness to genuine shifts.

Motivation: Why this design?

Standard supertrend indicators often flip prematurely in choppy markets due to fixed multipliers that do not account for localized volatility patterns, leading to frequent false signals and eroded confidence in trends. This design addresses that by incorporating an EMA-based regime filter for directional bias and an auto-adaptive hull that dynamically tunes the band width based on recent price containment needs. By prioritizing the narrowest effective enclosure, it avoids over-wide bands in calm periods that cause lag or under-wide ones in volatility spikes that invite breaks, providing a more consistent trailing reference without manual tweaking.

What’s different vs. standard approaches?

- Reference baseline: Diverges from the classic ATR-multiplier supertrend, which uses a single fixed period and constant factor applied to close or high/low deviations.

- Architecture differences:

- Auto-selection from candidate ATR lengths to find the optimal period for current conditions.

- Dynamic multiplier clamped between floor and cap values, adjusted by padding to ensure reliable containment.

- Regime-gated rendering, where hull position flips based on EMA relative positioning.

- Post-transition visual fading to emphasize change points without altering core logic.

- Practical effect: Charts show tighter, more reactive bands that rarely breach during trends, reducing visual clutter from flips; the adaptive nature means less intervention across assets, as the hull self-adjusts to volatility clusters rather than applying a one-size-fits-all scale.

How it works (technical)

The indicator first computes two EMAs from close prices using lengths derived from a preset pair or manual inputs, establishing a midline as their average. This midline serves as the central reference for the hull. True range values are then smoothed into multiple ATR candidates using exponential weighting over the specified lengths. For each candidate, deviations of recent highs and lows from the midline are ratioed against the ATR to determine a required multiplier that would enclose all extremes in the containment window—the highest ratio plus padding sets the base, clamped to user-defined bounds. Among valid candidates (those with sufficient history), the one yielding the narrowest overall band width is selected. The hull boundaries are then offset from the midline by this multiplier times the chosen ATR, and further smoothed with a fixed EMA to reduce jitter. Regime direction from EMA comparison gates which boundary acts as support or resistance, with initialization seeding arrays on the first bar to handle state persistence. No higher timeframe data is used, so all logic runs on the chart's native bars without lookahead.

Parameter Guide

EMA Pair — Selects preset lengths for fast and slow EMAs, influencing regime sensitivity and midline stability. Default: "21/55". Trade-offs/Tips: Faster pairs like "9/21" increase cross frequency for scalping but raise false signals; slower like "50/200" smooths for swings, potentially missing early turns. Use Manual for fine control.

Manual Fast — Sets fast EMA length when Manual mode is active; shorter values make regime switches quicker. Default: 21. Trade-offs/Tips: Lower than 10 risks over-reactivity; pair with slow at least double for clear separation.

Manual Slow — Sets slow EMA length when Manual mode is active; longer values anchor the midline more firmly. Default: 55. Trade-offs/Tips: Above 100 adds lag in trends; balance with fast to avoid perpetual neutrality.

ATR Lengths (comma-separated) — Defines candidate periods for ATR smoothing; more options allow finer auto-selection. Default: "7,10,14,21,28,35". Trade-offs/Tips: Fewer candidates speed computation but may miss optimal fits; keep under 10 for efficiency.

Containment Window — Number of recent bars the hull must fully enclose highs/lows of; larger windows favor stability. Default: 50. Trade-offs/Tips: Shorter (under 20) adapts faster to breaks but increases breach risk; longer smooths but delays response.

Min Multiplier Floor — Lowest allowed multiplier for hull width; prevents overly tight bands in low volatility. Default: 0.5. Trade-offs/Tips: Raise to 0.75 for conservative enclosures; too low allows pinches that flip easily.

Max Multiplier Cap — Highest allowed multiplier; caps expansion in spikes to avoid wide, lagging bands. Default: 1.0. Trade-offs/Tips: Lower to 0.75 tightens overall; higher permits more room but risks detachment from price.

Padding (+) — Adds buffer to the auto-multiplier for safer containment without exact touches. Default: 0.05. Trade-offs/Tips: Increase to 0.10 in gappy markets; minimal values hug closer but may still breach on outliers.

Fill Between (Mid ↔ Supertrend) — Toggles shaded area between midline and active hull for trend visualization. Default: true. Trade-offs/Tips: Disable for cleaner charts; pairs well with transparency tweaks.

Base Fill Transparency (0..100) — Sets default opacity of fills; higher values make them subtler. Default: 80. Trade-offs/Tips: Under 50 overwhelms price action; adjust with darken boost for emphasis.

Darken on Trend Change — Enables temporary opacity increase after regime shifts to spotlight transitions. Default: true. Trade-offs/Tips: Off for steady visuals; on aids spotting reversals in real-time.

Darken Fade Bars — Duration in bars for the darken effect to ramp back to base; longer prolongs highlight. Default: 8. Trade-offs/Tips: Shorter (4-6) for fast-paced charts; longer holds attention on changes.

Darken Boost at Change (Δ transp) — Intensity of opacity reduction at crossover; higher values make shifts more prominent. Default: 50. Trade-offs/Tips: Cap at 70 to avoid blackout; tune down if fades obscure details.

Show Supertrend Line — Displays the active hull boundary as a line. Default: true. Trade-offs/Tips: Hide for fill-only views; linewidth fixed at 3 for visibility.

Show EMA Cross Markers — Places circles and labels at crossover points for entry cues. Default: true. Trade-offs/Tips: Disable in clutter; labels show "Buy"/"Sell" at absolute positions.

Alert: EMA Cross Up (Long) — Triggers notification on bullish crossover. Default: true. Trade-offs/Tips: Pair with filters; once-per-bar frequency.

Alert: EMA Cross Down (Short) — Triggers notification on bearish crossover. Default: true. Trade-offs/Tips: Use for exits; ensure broker integration.

Show Debug — Reveals internal diagnostics like selected ATR details (if implemented). Default: false. Trade-offs/Tips: Enable for troubleshooting selections; minimal overhead.

Reading & Interpretation

Bullish regime shows a green line below price as support, with upward fill from midline; bearish uses red line above as resistance, downward fill. Crossovers flip the active boundary, marked by tiny green/red circles and "Buy"/"Sell" labels at the hull level. Fills start at base transparency but darken sharply at changes, fading over the specified bars to signal fresh momentum. If the hull rarely breaches during trends, containment is effective; frequent touches without flips indicate tight adaptation. Debug mode (when enabled) overlays text or plots for selected length and multiplier, helping verify auto-choices.

Practical Workflows & Combinations

- Trend following: Enter long on green "Buy" label above prior low structure; confirm with higher high. Trail stops along the green hull line, tightening as fills stabilize post-fade.

- Exits/Stops: Conservative exit on opposite crossover or hull breach; aggressive hold until fade completes if volume supports. Use darken boost as a volatility cue—high delta suggests waiting for confirmation.

- Multi-asset/Multi-TF: Defaults suit forex/stocks on 15m-4h; for crypto, widen containment to 75 for gaps. Layer on volume oscillator for cross filters; avoid on low-liquidity assets where ATR candidates skew.

Behavior, Constraints & Performance

Closed-bar logic ensures signals confirm at bar end, with live bars updating hull adaptively but no repaints since no future data or security calls are used. Arrays persist ATR states across bars, initialized once with candidates parsed from string. Small fixed loops (over 6 lengths max, inner up to 50) run per bar, capped by max_bars_back=500 for history needs. Resources stay low with 500 labels/lines limits, but dense charts may hit on markers. Known limits include initial lag until containment history builds (50+ bars), potential wide bands on gaps, and suboptimal selections if candidates omit ideal lengths.

Sensible Defaults & Quick Tuning

Start with "21/55" pair, 50-window, 0.5-1.0 multipliers, and 80% transparency for balanced responsiveness on daily charts. For too many flips, raise min floor to 0.75 or add lengths like "42"; for sluggishness, shorten window to 30 or pick faster pair. In high-vol environments, boost padding to 0.10; for smoother visuals, extend fade bars to 12.

What this indicator is—and isn’t

This is a visualization and signal layer for trend regime and adaptive boundaries, aiding entry/exit timing in directional markets. It is not a standalone system—pair with price structure, risk sizing, and broader context. Not predictive of turns, just reactive to containment and crosses.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Happy trading

Chervolino

Crypto Cycle Radar (TOTAL / TOTAL2 / TOTAL3 / BTC.D / USDT.D)Crypto Cycle Radar (TOTAL / TOTAL2 / TOTAL3 / BTC.D / USDT.D)

Outside Candle Session Breakout [CHE]Outside Candle Session Breakout

Session - anchored HTF levels for clear market-structure and precise breakout context

Summary

This indicator is a relevant market-structure tool. It anchors the session to the first higher-timeframe bar, then activates only when the second bar forms an outside condition. Price frequently reacts around these anchors, which provides precise breakout context and a clear overview on both lower and higher timeframes. Robustness comes from close-based validation, an adaptive volatility and tick buffer, first-touch enforcement, optional retest, one-signal-per-session, cooldown, and an optional trend filter.

Pine version: v6. Overlay: true.

Motivation: Why this design?

Short-term breakout tools often trigger during noise, duplicate within the same session, or drift when volatility shifts. The core idea is to gate signals behind a meaningful structure event: a first-bar anchor and a subsequent outside bar on the session timeframe. This narrows attention to structurally important breaks while adaptive buffering and debouncing reduce false or mid-run triggers.

What’s different vs. standard approaches?

Baseline: Simple high-low breaks or fixed buffers without session context.

Architecture: Session-anchored first-bar high/low; outside-bar gate; close-based confirmation with an adaptive ATR and tick buffer; first-touch enforcement; optional retest window; one-signal-per-session and cooldown; optional EMA trend and slope filter; higher-timeframe aggregation with lookahead disabled; themeable visuals and a range fill between levels.

Practical effect: Cleaner timing at structurally relevant levels, fewer redundant or late triggers, and better multi-timeframe situational awareness.

How it works (technical)

The chart timeframe is mapped to an analysis timeframe and a session timeframe.

The first session bar defines the anchor high and low. The setup becomes active only after the next bar forms an outside range relative to that first bar.

While active, the script tracks these anchors and checks for a breakout beyond a buffered threshold, using closing prices or wicks by preference.

The buffer scales with volatility and is limited by a minimum tick floor. First-touch enforcement avoids mid-run confirmations.

Optional retest requires a pullback to the raw anchor followed by a new close beyond the buffered level within a user window.

Optional trend gating uses an EMA on the analysis timeframe, including an optional slope requirement and price-location check.

Higher-timeframe data is requested with lookahead disabled. Values can update during a forming higher-timeframe bar; waiting and confirmation mitigate timing shifts.

Parameter Guide

Enable Long / Enable Short — Direction toggles. Default: true / true. Reduces unwanted side.

Wait Candles — Minimum bars after outside confirmation before entries. Default: five. More waiting increases stability.

Close-based Breakout — Confirm on candle close beyond buffer. Default: true. For wick sensitivity, disable.

ATR Buffer — Enables adaptive volatility buffer. Default: true.

ATR Multiplier — Buffer scaling. Default: zero point two. Increase to reduce noise.

Ticks Buffer — Minimum buffer in ticks. Default: two. Protects in quiet markets.

Cooldown Bars — Blocks new signals after a trigger. Default: three.

One Signal per Session — Prevents duplicates within a session. Default: true.

Require Retest — Pullback to raw anchor before confirming. Default: false.

Retest Window — Bars allowed for retest completion. Default: five.

HTF Trend Filter — EMA-based gating. Default: false.

EMA Length — EMA period. Default: two hundred.

Slope — Require EMA slope direction. Default: true.

Price Above/Below EMA — Require price location relative to EMA. Default: true.

Show Levels / Highlight Session / Show Signals — Visual controls. Default: true.

Color Theme — “Blue-Green” (default), “Monochrome”, “Earth Tones”, “Classic”, “Dark”.

Time Period Box — Visibility, size, position, and colors for the info box. (Optional)

Reading & Interpretation

The two level lines represent the session’s first-bar high and low. The filled band illustrates the active session range.

“OUT” marks that the outside condition is confirmed and the setup is live.

“LONG” or “SHORT” appears only when the breakout clears buffer, debounce, and optional gates.

Background tint indicates sessions where the setup is valid.

Alerts fire on confirmed long or short breakout events.

Practical Workflows & Combinations

Trend-following: Keep close-based validation, ATR buffer near the default, one-signal-per-session enabled; add EMA trend and slope for directional bias.

Retest confirmation: Enable retest with a short window to prioritize cleaner continuation after a pullback.

Lower-timeframe scalping: Reduce waiting and cooldown slightly; keep a small tick buffer to filter micro-whips.

Swing and position context: Increase ATR multiplier and waiting; maintain once-per-session to limit duplicates.

Timeframe Tiers and Trader Profiles

The script adapts its internal mapping based on the chart timeframe:

Under fifteen minutes → Analysis: one minute; Session: sixty minutes. Useful for scalpers and high-frequency intraday reads.

Between fifteen and under sixty minutes → Analysis: fifteen minutes; Session: one day. Suits day traders who need intraday alignment to the daily session.

Between sixty minutes and under one day → Analysis: sixty minutes; Session: one week. Serves intraday-to-swing transitions and end-of-day planning.

Between one day and under one week → Analysis: two hundred forty minutes; Session: two weeks. Fits swing traders who monitor multi-day structure.

Between one week and under thirty days → Analysis: one day; Session: three months. Supports position traders seeking quarterly context.

Thirty days and above → Analysis: one day; Session: twelve months. Provides a broad annual anchor for macro context.

These tiers are designed to keep anchors meaningful across regimes while preserving responsiveness appropriate to the trader profile.

Behavior, Constraints & Performance

Signals can be validated on closed bars through close-based logic; enabling this reduces intrabar flicker.

Higher-timeframe values may evolve during a forming bar; waiting parameters and the outside-bar gate reduce, but do not remove, this effect.

Resource footprint is light; the script uses standard indicators and a single higher-timeframe request per stream.

Known limits: rare setups during very quiet periods, sensitivity to gaps, and reduced reliability on illiquid symbols.

Sensible Defaults & Quick Tuning

Start with close-based validation on, ATR buffer on with a multiplier near zero point two, tick buffer two, cooldown three, once-per-session on.

Too many flips: increase the ATR multiplier and cooldown; consider enabling the EMA filter and slope.

Too sluggish: reduce the ATR multiplier and waiting; disable retest.

Choppy conditions: keep close-based validation, increase tick buffer, shorten the retest window.

What this indicator is—and isn’t

This is a visualization and signal layer for session-anchored breakouts with stability gates. It is not a complete trading system, risk framework, or predictive engine. Combine it with structured analysis, position sizing, and disciplined risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Moyennes Mobiles Pertinentes ema21vert ma50 bleue ma200 rougeUtilisez sur un même script un indicateur avec plusieurs moyennes mobiles servant de supports

黄金专用LPPL特征检测(Log-Periodic Power Law Singularity)专门用于黄金走势的LPPL检测,在技术分析中,LPPL 奇点指的是对数周期幂律奇异性(Log-Periodic Power Law Singularity),它是对数周期幂律模型(LPPL)中的一个关键概念。以下是关于它的详细介绍:

提出者及背景:LPPL 模型是由研究市场泡沫的先驱者、物理学家迪迪埃・索尔内特(Didier Sornette)等人提出的。该模型结合了理性预期泡沫的经济理论、投资者的模仿和羊群行为的行为金融学以及分岔和相变的数学统计物理学,用于检测金融市场中的泡沫和预测市场转折点。

模型原理:LPPL 模型假设当市场出现泡沫时,资产价格会呈现出一种特殊的波动模式,这种模式由正反馈机制驱动。在泡沫形成过程中,投资者的模仿和跟风行为导致市场参与者的一致性和协同性急剧上升,价格出现 “快于指数” 的增长,同时伴随着加速的对数周期振荡。而 LPPL 奇点就是价格增长和振荡达到极限的那个有限时间点,在这个点之前,价格增长越来越快,振荡频率也越来越高,当到达奇点时,泡沫破裂,市场往往会出现急剧的反转和崩盘。

数学表达:LPPL 模型的数学公式较为复杂,其原始形式提出了一个由 3 个线性参数和 4 个非线性参数组成的函数。通过将这个函数与对数价格时间序列进行拟合,可以估计出模型的参数,进而确定奇点的时间位置等信息。

在金融市场中的应用:LPPL 模型及其中的奇点概念主要用于检测金融市场中的泡沫和预测市场的崩溃点。例如,在 2008 年石油价格泡沫和 2009 年上海股市泡沫等事件中,该模型都被用于分析和预测市场的转折点。不过,该模型也存在一定的局限性,比如对奇点具体点位的预测误差较大,而且市场情况复杂多变,可能会有强大的外力干扰等因素影响模型的准确性。

The LPPL model was proposed by physicist Didier Sornette, a pioneer in the study of market bubbles, and others. The model combines the economic theory of rational expectations bubbles, behavioral finance on investor imitation and herding behavior, and the mathematical statistical physics of bifurcations and phase transitions to detect bubbles in financial markets and predict market turning points.

Model Principle: The LPPL model posits that when a market bubble forms, asset prices exhibit a distinctive pattern of fluctuation driven by a positive feedback mechanism. During the bubble's formation, investors' imitation and bandwagon-following behavior lead to a sharp increase in consistency and coordination among market participants, resulting in "faster-than-exponential" price growth accompanied by accelerating logarithmic-periodic oscillations. The LPPL singularity is the finite point in time where price growth and oscillation reach their limits. Prior to this point, prices grow increasingly faster, and the frequency of oscillations increases. When the singularity is reached, the bubble bursts, and the market often experiences a sharp reversal and crash.

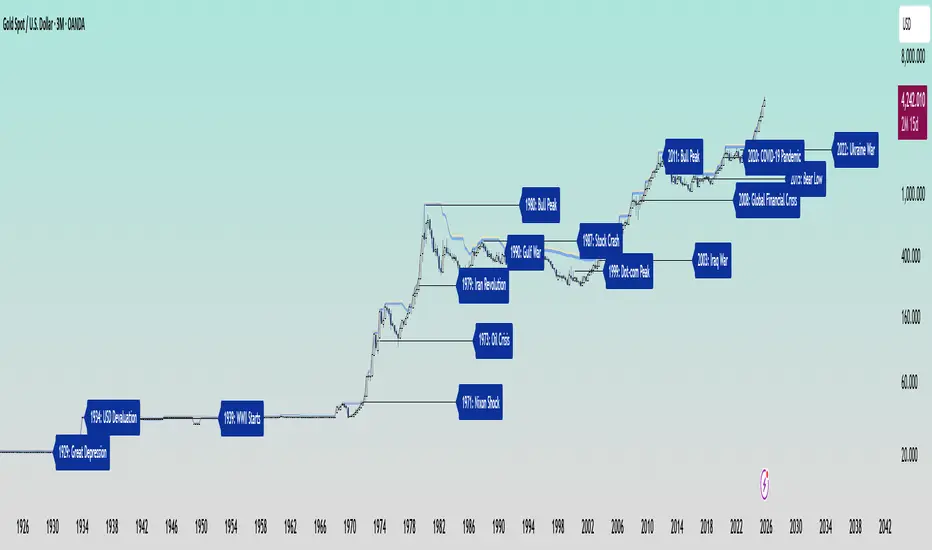

Gold and Bitcoin: The Evolution of Value!The Eternal Luster of Gold

In the dawn of time, when the earth was young and rivers whispered secrets to the stones, a wanderer named Elara found a gleam in the silt of a sun-kissed stream. It was pure gold, radiant like a captured star fallen from the heavens. She held it in her palm, feeling its warmth pulse like a heartbeat, and in that moment, humanity’s soul awakened to the allure of eternity.

As seasons turned to centuries, gold wove itself into the story of empires. In ancient Egypt, pharaohs crowned themselves with its glow, believing it to be the flesh of gods. It built pyramids that reached for the sky and tombs that guarded kings forever. Across the sands in Mesopotamia, merchants traded it for spices and silks, its weight a promise of power and trust.

Translation moment: Gold became the first universal symbol of value. People trusted it more than words or promises because it did not rust, fade, or vanish.

The Greeks saw in gold not only wealth but wisdom, the symbol of the sun’s eternal fire. Alexander the Great carried it across the continent, forging an empire of golden threads. Rome rose on its back, minting coins whose clink echoed through history.

Through the ages, gold endured the rush of California’s dreamers, the halls of Versailles, and the quiet vaults of modern fortunes. It has been both a curse and a blessing, the fuel of wars and the gift of love, whispering of beauty’s fragility and the human desire for something that lasts beyond the grave. In its shine, we see ourselves fragile yet forever chasing light.

The Digital Dawn of Bitcoin

Centuries later, under the glow of computer screens, a visionary named Satoshi dreamed of a new gold born not from the earth but from the ether of ideas. Bitcoin appeared in 2009 amid a world weary of banks and broken trust.

Like gold’s ancient gleam, Bitcoin was mined not with picks but with puzzles solved by machines. It promised freedom, a currency without kings, flowing from person to person, unbound by borders or empires.

Translation moment: Bitcoin works like digital gold. Instead of digging the ground, miners use computers to solve problems and unlock new coins. No one controls it, and that is what makes it powerful.

Through doubt and frenzy, it rose as a beacon for those seeking sovereignty in a digital world. Its volatility became its soul, a reminder that true value is built on belief. Bitcoin speaks to ingenuity and rebellion, a star of code guiding us toward a future where wealth is weightless yet profoundly honest.

Gold’s Cycles: Echoes of War and Crisis

In the early 20th century, gold was held under fixed prices until the Great Depression of 1929 shattered these illusions. The 1934 dollar devaluation lifted it from 20.67 to 35, restoring faith amid despair. When World War II erupted in 1939, gold’s role as a refuge was muted by controls, yet it quietly held its place as the world’s silent guardian.

The 1970s awakened its wild spirit. The Nixon Shock of 1971 freed gold from 35, sparking a bull run during the 1973 Oil Crisis. The 1979 Iranian Revolution led to a 1980 peak of 850, a leap of more than 2,000 percent, as investors sought safety from the chaos.

Translation moment: When fear rises, people rush to gold. Every major war or economic crisis has sent gold upward because it feels safe when paper money loses trust.

The 1987 stock crash caused brief dips, but the 1990 Gulf War reignited its glow. Around 2000, after the Dot-com Bust, gold found new life, climbing from $ 270 to over $1,900 during the 2008 Financial Crisis. It dipped to 1050 in 2015, then surged again past 2000 during the 2020 pandemic.

The 2022 Ukraine War added another chapter with prices climbing above 2700 by 2025. Across a century of crises, gold has risen whenever fear tested humanity’s resolve, teaching patience and fortitude through its quiet endurance.

Bitcoin’s Cycles: Echoes of Innovation and Crisis

Born from the ashes of the 2008 Financial Crisis, Bitcoin began its story at mere cents. It traded below $1 until 2011, when it reached $30 before crashing by 90 percent following the MTGOX collapse.

In 2013, it soared to 1242 only to fall again to 200 in 2015 as regulations tightened. The 2017 bull run lifted it to nearly 20000 before another long winter brought it to 3200 in 2018. Each fall taught resilience, each rise renewed belief.

During the 2020 pandemic, it fell below 5000 before rallying to 69000 in 2021. The Ukraine War and the FTX collapse of 2022 brought it down to 16000, but also proved its role in humanitarian aid. By 2024, the halving and ETF approvals helped it break 100000, marking Bitcoin’s rise as digital gold.

Translation moment: Bitcoin’s rhythm follows four-year halving cycles when mining rewards are cut in half. This keeps supply limited, which often triggers new bull runs as demand returns.

Every four years, it's halving cycles 2012, 2016, 2020, 2024, fueling new waves of adoption and correction. Bitcoin grows strongest in times of uncertainty, echoing humanity’s drive to evolve beyond limits.

The Harmony of Gold and Bitcoin Modern Parallels

In today’s markets, gold’s ancient glow meets Bitcoin’s electric pulse. As of October 17, 2025, their correlation stands near 0.85, close to its historic high of 0.9. Both rise as guardians against inflation and the erosion of trust in the dollar.

Gold trades near 4310 per ounce a record high while Bitcoin hovers around 104700 showing brief fractures in their unity. Gold offers the comfort of touch while Bitcoin provides the thrill of code. Together, they reflect fear and hope, the twin emotions that drive every market.

Translation moment: A correlation of 0.85 means they often move in the same direction. When fear or inflation rises, both gold and Bitcoin tend to rise in tandem.

Analysts warn of bubbles in stocks, gold, and crypto, yet optimism remains for Bitcoin’s growth through 2026, while gold holds its defensive strength.

Gold carries risks of storage cost and theft, but steadiness in chaos. Bitcoin carries volatility and regulatory challenges, but it also offers unmatched innovation and reach. One is the anchor, the other the dream, and both reward those who hold conviction through uncertainty.

Epilogue: The Timeless Balance

Gold and Bitcoin form a bridge between the ancient and the future. Gold, the earth’s eternal treasure, stands as a symbol of stability and truth. Bitcoin, the digital heir, shines with the spark of innovation and freedom.

Experts view gold as the ultimate inflation hedge, forged in fire and tested over centuries. They see Bitcoin as its digital counterpart, scarce by code and limitless in reach.

Gold’s weight grounds us in reality while Bitcoin’s light expands our imagination. In 2025, as gold surpasses $4,346 and Bitcoin hovers near $105,000, the wise investor sees not rivals but reflections.

Translation moment: Gold reminds us to protect what we have. Bitcoin reminds us to dream of what could be. Together, they balance caution and courage, the two forces every generation must master.

One whispers of legacy, the other of evolution, yet together they tell humanity’s oldest story, our unending quest to preserve value against time and to chase the light that never fades.

🙏 I ask (Allah) for guidance and success. 🤲

USCBBS-WDTGAL-RRPONTSYDThis is the U.S. Financial Market Net Liquidity.

The calculation method is to subtract the U.S. Treasury General Account balance (WDTGAL) and then the Overnight Reverse Repo balance (RRPONTSYD) from the Federal Reserve's balance sheet total (USCBBS).

Real Relative Strength Breakout & BreakdownReal Relative Strength Breakout & Breakdown Indicator

What It Does

Identifies high-probability trading setups by combining:

Technical Breakouts/Breakdowns - Price breaking support/resistance zones

Real Relative Strength (RRS) - Volatility-adjusted performance vs benchmark (SPY)

Key Insight: The strongest signals occur when price action contradicts market direction—breakouts during market weakness or breakdowns during market strength show exceptional buying/selling pressure.

Real Relative Strength (RRS) Calculation

RRS measures outperformance/underperformance on a volatility-adjusted basis:

Power Index = (Benchmark Price Move) / (Benchmark ATR)

RRS = (Stock Price Move - Power Index × Stock ATR) / Stock ATR

RRS (smoothed) = 3-period SMA of RRS

Interpretation:

RRS > 0 = Relative Strength (outperforming)

RRS < 0 = Relative Weakness (underperforming)

Signal Types

🟢 Large Green Triangle (Premium Long)

Condition: Breakout + RRS > 0

Meaning: Stock breaking resistance WHILE outperforming benchmark

Best when: Market is weak but stock breaks out anyway = exceptional strength

Use: High-conviction long entries

🔵 Small Blue Triangle (Standard Breakout)

Condition: Breakout + RRS ≤ 0

Meaning: Breaking resistance but underperforming benchmark

Typical: "Rising tide lifts all boats" scenario during market rally

Use: Lower conviction—may just be following market

🟠 Large Orange Triangle (Premium Short)

Condition: Breakdown + RRS < 0

Meaning: Stock breaking support WHILE underperforming benchmark

Best when: Market is strong but stock breaks down anyway = severe weakness

Use: High-conviction short entries

🔴 Small Red Triangle (Standard Breakdown)

Condition: Breakdown + RRS ≥ 0

Meaning: Breaking support but outperforming benchmark

Typical: Stock falling less than market during selloff

Use: Lower conviction—may recover when market does

Why Large Triangles Matter

Large signals show divergence = genuine institutional flow:

Stock breaking out while market falls → Aggressive buying despite headwinds

Stock breaking down while market rallies → Aggressive selling despite tailwinds

These setups reveal where real conviction lies, not just momentum-following behavior.

Quick Settings

RRS: 12-period lookback, 3-bar smoothing, vs SPY

Breakouts: 5-period pivots, 200-bar lookback, 3% zone width, 2 minimum tests

Session times for London (UTC 07:00–16:00 UTC)Session times for London (UTC 07:00–16:00 UTC). Shows the trading hours for the London Session Mon-Fri

Simplified Percentile ClusteringSimplified Percentile Clustering (SPC) is a clustering system for trend regime analysis.

Instead of relying on heavy iterative algorithms such as k-means, SPC takes a deterministic approach: it uses percentiles and running averages to form cluster centers directly from the data, producing smooth, interpretable market state segmentation that updates live with every bar.

Most clustering algorithms are designed for offline datasets, they require recomputation, multiple iterations, and fixed sample sizes.

SPC borrows from both statistical normalization and distance-based clustering theory , but simplifies them. Percentiles ensure that cluster centers are resistant to outliers , while the running mean provides a stable mid-point reference.

Unlike iterative methods, SPC’s centers evolve smoothly with time, ideal for charts that must update in real time without sudden reclassification noise.

SPC provides a simple yet powerful clustering heuristic that:

Runs continuously in a charting environment,

Remains interpretable and reproducible,

And allows traders to see how close the current market state is to transitioning between regimes.

Clustering by Percentiles

Traditional clustering methods find centers through iteration. SPC defines them deterministically using three simple statistics within a moving window:

Lower percentile (p_low) → captures the lower basin of feature values.

Upper percentile (p_high) → captures the upper basin.

Mean (mid) → represents the central tendency.

From these, SPC computes stable “centers”:

// K = 2 → two regimes (e.g., bullish / bearish)

=

// K = 3 → adds a neutral zone

=

These centers move gradually with the market, forming live regime boundaries without ever needing convergence steps.

Two clusters capture directional bias; three clusters add a neutral ‘range’ state.

Multi-Feature Fusion

While SPC can cluster a single feature such as RSI, CCI, Fisher Transform, DMI, Z-Score, or the price-to-MA ratio (MAR), its real strength lies in feature fusion. Each feature adds a unique lens to the clustering system. By toggling features on or off, traders can test how each dimension contributes to the regime structure.

In “Clusters” mode, SPC measures how far the current bar is from each cluster center across all enabled features, averages these distances, and assigns the bar to the nearest combined center. This effectively creates a multi-dimensional regime map , where each feature contributes equally to defining the overall market state.

The fusion distance is computed as:

dist := (rsi_d * on_off(use_rsi) + cci_d * on_off(use_cci) + fis_d * on_off(use_fis) + dmi_d * on_off(use_dmi) + zsc_d * on_off(use_zsc) + mar_d * on_off(use_mar)) / (on_off(use_rsi) + on_off(use_cci) + on_off(use_fis) + on_off(use_dmi) + on_off(use_zsc) + on_off(use_mar))

Because each feature can be standardized (Z-Score), the distances remain comparable across different scales.

Fusion mode combines multiple standardized features into a single smooth regime signal.

Visualizing Proximity - The Transition Gradient

Most indicators show binary or discrete conditions (e.g., bullish/bearish). SPC goes further, it quantifies how close the current value is to flipping into the next cluster.

It measures the distances to the two nearest cluster centers and interpolates between them:

rel_pos = min_dist / (min_dist + second_min_dist)

real_clust = cluster_val + (second_val - cluster_val) * rel_pos

This real_clust output forms a continuous line that moves smoothly between clusters:

Near 0.0 → firmly within the current regime

Around 0.5 → balanced between clusters (transition zone)

Near 1.0 → about to flip into the next regime

Smooth interpolation reveals when the market is close to a regime change.

How to Tune the Parameters

SPC includes intuitive parameters to adapt sensitivity and stability:

K Clusters (2–3): Defines the number of regimes. K = 2 for trend/range distinction, K = 3 for trend/neutral transitions.

Lookback: Determines the number of past bars used for percentile and mean calculations. Higher = smoother, more stable clusters. Lower = faster reaction to new trends.

Lower / Upper Percentiles: Define what counts as “low” and “high” states. Adjust to widen or tighten cluster ranges.

Shorter lookbacks react quickly to shifts; longer lookbacks smooth the clusters.

Visual Interpretation

In “Clusters” mode, SPC plots:

A colored histogram for each cluster (red, orange, green depending on K)

Horizontal guide lines separating cluster levels

Smooth proximity transitions between states

Each bar’s color also changes based on its assigned cluster, allowing quick recognition of when the market transitions between regimes.

Cluster bands visualize regime structure and transitions at a glance.

Practical Applications

Identify market regimes (bullish, neutral, bearish) in real time

Detect early transition phases before a trend flip occurs

Fuse multiple indicators into a single consistent signal

Engineer interpretable features for machine-learning research

Build adaptive filters or hybrid signals based on cluster proximity

Final Notes

Simplified Percentile Clustering (SPC) provides a balance between mathematical rigor and visual intuition. It replaces complex iterative algorithms with a clear, deterministic logic that any trader can understand, and yet retains the multidimensional insight of a fusion-based clustering system.

Use SPC to study how different indicators align, how regimes evolve, and how transitions emerge in real time. It’s not about predicting; it’s about seeing the structure of the market unfold.

Disclaimer

This indicator is intended for educational and analytical use.

It does not generate buy or sell signals.

Historical regime transitions are not indicative of future performance.

Always validate insights with independent analysis before making trading decisions.

ALISH WEEK LABELS THE ALISH WEEK LABELS

Overview

This indicator programmatically delineates each trading week and encapsulates its realized price range in a live-updating, filled rectangle. A week is defined in America/Toronto time from Monday 00:00 to Friday 16:00. Weekly market open to market close, For every week, the script draws:

a vertical start line at the first bar of Monday 00:00,

a vertical end line at the first bar at/after Friday 16:00, and

a white, semi-transparent box whose top tracks the highest price and whose bottom tracks the lowest price observed between those two temporal boundaries.

The drawing is timeframe-agnostic (M1 → 1D): the box expands in real time while the week is open and freezes at the close boundary.

Time Reference and Session Boundaries

All scheduling decisions are computed with time functions called using the fixed timezone string "America/Toronto", ensuring correct behavior across DST transitions without relying on chart timezone. The start condition is met at the first bar where (dayofweek == Monday && hour == 0 && minute == 0); on higher timeframes where an exact 00:00 bar may not exist, a fallback checks for the first Monday bar using ta.change(dayofweek). The close condition is met on the first bar at or after Friday 16:00 (Toronto), which guarantees deterministic closure on intraday and higher timeframes.

State Model

The indicator maintains minimal persistent state using var globals:

week_open (bool): whether the current weekly session is active.

wk_hi / wk_lo (float): rolling extrema for the active week.

wk_box (box): the graphical rectangle spanning × .

wk_start_line and a transient wk_end_line (line): vertical delimiters at the week’s start and end.

Two dynamic arrays (boxes, vlines) store object handles to support bounded history and deterministic garbage collection.

Update Cycle (Per Bar)

On each bar the script executes the following pipeline:

Start Check: If no week is open and the start condition is satisfied, instantiate wk_box anchored at the current bar_index, prime wk_hi/wk_lo with the bar’s high/low, create the start line, and push both handles to their arrays.

Accrual (while week_open): Update wk_hi/wk_lo using math.max/min with current bar extremes. Propagate those values to the active wk_box via box.set_top/bottom and slide box.set_right to the current bar_index to keep the box flush with live price.

Close Check: If at/after Friday 16:00, finalize the week by freezing the right edge (box.set_right), drawing the end line, pushing its handle, and flipping week_open false.

Retention Pruning: Enforce a hard cap on historical elements by deleting the oldest objects when counts exceed configured limits.

Drawing Semantics

The range container is a filled white rectangle (bgcolor = color.new(color.white, 100 − opacity)), with a solid white border for clear contrast on dark or light themes. Start/end boundaries are full-height vertical white lines (y1=+1e10, y2=−1e10) to guarantee visibility across auto-scaled y-axes. This approach avoids reliance on price-dependent anchors for the lines and is robust to large volatility spikes.

Multi-Timeframe Behavior

Because session logic is driven by wall-clock time in the Toronto zone, the indicator remains consistent across chart resolutions. On coarse timeframes where an exact boundary bar might not exist, the script legally approximates by triggering on the first available bar within or immediately after the boundary (e.g., Friday 16:00 occurs between two 4-hour bars). The box therefore represents the true realized high/low of the bars present in that timeframe, which is the correct visual for that resolution.

Inputs and Defaults

Weeks to keep (show_weeks_back): integer, default 40. Controls retention of historical boxes/lines to avoid UI clutter and resource overhead.

Fill opacity (fill_opacity): integer 0–100, default 88. Controls how solid the white fill appears; border color is fixed pure white for crisp edges.

Time zone is intentionally fixed to "America/Toronto" to match the strategy definition and maintain consistent historical backtesting.

Performance and Limits

Objects are reused only within a week; upon closure, handles are stored and later purged when history limits are exceeded. The script sets generous but safe caps (max_boxes_count/max_lines_count) to accommodate 40 weeks while preserving Editor constraints. Per-bar work is O(1), and pruning loops are bounded by the configured history length, keeping runtime predictable on long histories.

Edge Cases and Guarantees

DST Transitions: Using a fixed IANA time zone ensures Friday 16:00 and Monday 00:00 boundaries shift correctly when DST changes in Toronto.

Weekend Gaps/Holidays: If the market lacks bars exactly at boundaries, the nearest subsequent bar triggers the start/close logic; range statistics still reflect observed prices.

Live vs Historical: During live sessions the box edge advances every bar; when replaying history or backtesting, the same rules apply deterministically.

Scope (Intentional Simplicity)

This tool is strictly a visual framing indicator. It does not compute labels, statistics, alerts, or extended S/R projections. Its single responsibility is to clearly present the week’s realized range in the Toronto session window so you can layer your own execution or analytics on top.

Opening Range Breakout [Boomer]OBR. Set your time zone. Chose between 5min ,15min, 30min, 60min or 120 min with just a click.

⚡ Elite Momentum Pro🎯 Key Features

1. Smart Signal Engine

3 Signal Modes: Aggressive, Balanced, Conservative

7-Point Scoring System - Ensures high-quality signals

Anti-Flip Protection - Prevents rapid signal changes

Multiple confirmations: Supertrend, MACD, RSI, EMA alignment, momentum

2. Advanced Risk Management

3 Take Profit Levels (TP1, TP2, TP3) for scaling out

ATR-Based Dynamic Stops - Adapts to volatility

Customizable Risk:Reward (default 2.5:1)

Visual stop and target levels

3. Clean Visual Design

Color-coded price bars based on trend strength

EMA Ribbon (9, 21, 50, 200) for trend clarity

US30 Quarter Levels (125-point grid) by FxMogul🟦 US30 Quarter Levels — Trade the Index Like the Banks

Discover the Dow’s hidden rhythm.

This indicator reveals the institutional quarter levels that govern US30 — spaced every 125 points, e.g. 45125, 45250, 45375, 45500, 45625, 45750, 45875, 46000, and so on.

These are the liquidity magnets and reaction zones where smart money executes — now visualized directly on your chart.

💼 Why You Need It

See institutional precision: The Dow respects 125-point cycles — this tool exposes them.

Catch reversals before retail sees them: Every impulse and retracement begins at one of these zones.

Build confluence instantly: Perfectly aligns with your FVGs, OBs, and session highs/lows.

Trade like a professional: Turn chaos into structure, and randomness into rhythm.

⚙️ Key Features

Automatically plots US30 quarter levels (…125 / …250 / …375 / …500 / …625 / …750 / …875 / …000).

Color-coded hierarchy:

🟨 xx000 / xx500 → major institutional levels

⚪ xx250 / xx750 → medium-impact levels

⚫ xx125 / xx375 / xx625 / xx875 → intraday liquidity pockets

Customizable window size, label spacing, and line extensions.

Works across all timeframes — from 1-minute scalps to 4-hour macro swings.

Optimized for clean visualization with no clutter.

🎯 How to Use It

Identify liquidity sweeps: Smart money hunts stops at these quarter zones.

Align structure: Combine with session opens, order blocks, or FVGs.

Set precision entries & exits: Trade reaction-to-reaction with tight risk.

Plan daily bias: Watch how New York respects these 125-point increments.

🧭 Designed For

Scalpers, day traders, and swing traders who understand that US30 doesn’t move randomly — it moves rhythmically.

Perfect for traders using ICT, SMC, or liquidity-based frameworks.

⚡ Creator’s Note

“Every 125 points, the Dow breathes. Every 1000, it shifts direction.

Once you see the rhythm, you’ll never unsee it.”

— FxMogul

Time Line Indicator - by LMTime Line Indicator – by LM

Description:

The Time Line Indicator is a simple, clean, and customizable tool designed to visualize specific time periods within each hour directly in a dedicated indicator pane. It allows traders to mark important intraday minute ranges across multiple past hours, providing a clear visual reference for time-based analysis. This indicator is perfect for identifying recurring hourly windows, session patterns, or custom time-based events in your charts.

Unlike traditional overlays, this indicator does not interfere with price candles and draws its lines in a separate pane at the bottom of your chart for clarity.

Key Features:

Custom Hourly Lines:

Draw horizontal lines for a specific minute range within each hour, e.g., from the 45th minute to the 15th minute of the next hour.

Multi-Hour Support:

Choose how many past hours to display. The indicator will replicate the line for each selected hourly period, following the same minute logic.

Automatic Start/End Logic:

If your chosen start minute is in the previous hour, the line correctly begins at that time.

The end minute can cross into the next hour when applicable.

If the selected end minute does not yet exist in the current chart data, the line will extend to the latest available bar.

Dedicated Indicator Pane:

Lines appear in a fixed, non-intrusive y-axis within the indicator pane (overlay=false), keeping your price chart clean.

Customizable Appearance:

Line Color: Choose any color to match your chart theme.

Line Thickness: Adjust the width of the lines for better visibility.

Inputs:

Input Name Type Default Description

Line Color Color Orange The color of the horizontal lines.

Line Thickness Integer 2 The thickness of each line (1–5).

Start Minute Integer 5 The minute within the hour where the line begins (0–59).

End Minute Integer 25 The minute within the hour where the line ends (0–59).

Hours Back Integer 3 Number of past hours to display lines for.

Use Cases:

Intraday Analysis: Quickly visualize recurring minute ranges across multiple hours.

Session Tracking: Mark critical time windows for trading sessions or market events.

Pattern Recognition: Easily identify time-based patterns or setups without cluttering the price chart.

How It Works:

The indicator calculates the nearest bars corresponding to your start and end minutes.

It draws horizontal lines at a fixed y-axis value within the indicator pane.

Lines are drawn for each selected past hour, replicating the chosen minute span.

All logic respects the actual chart data; lines never extend into the future beyond the most recent bar.

Notes:

Overlay is set to false, so lines appear in a dedicated pane below the price chart.

The indicator is fully compatible with any timeframe. Lines adjust automatically to match the chart’s bar spacing.

You can change the number of hours displayed at any time without affecting existing lines.

If you want, I can also draft a shorter “TradingView Store / Public Library description” version under 500 characters for the “Short Description” field — concise and punchy for users scrolling through indicators.

Londen & New York Sessies (UTC+2)This script highlights the London and New York trading sessions on the chart, adjusted for UTC+2 timezone. It's designed to help traders easily visualize the most active and liquid periods of the Forex and global markets directly on their TradingView charts. The London session typically provides strong volatility, while the New York session brings increased momentum and overlaps with London for powerful trading opportunities. Ideal for intraday and session-based strategies.

Wyckoff Stage Approximator (MTF Alerts)Wyckoff Stage Approximator (MTF Context)

This indicator is a powerful tool designed for traders who use a top-down, multi-timeframe approach based on Wyckoff principles. Its primary function is to identify the market's current stage—consolidation (Stage 1) or trend (Stage 2)—on a higher Context (C) timeframe and project that analysis onto your lower Validation (V) and Entry (E) charts.

This ensures you are always trading in alignment with the "big picture" trend, preventing you from taking low-probability trades based on lower-timeframe noise.

Core Concept: Top-Down Analysis

The script solves a common problem for multi-timeframe traders: losing sight of the primary trend. By locking the background color to your chosen Context timeframe (e.g., 15-minute), you are constantly reminded of the market's true state.

🟡 Yellow Background (Stage 1): The Context timeframe is in consolidation. This is a time to be patient and wait for a clear directional bias to emerge.

🟢 Green Background (Stage 2 - Markup): The Context timeframe is in a confirmed uptrend. This is your green light to look for bullish pullback opportunities on your lower timeframes.

🔴 Red Background (Stage 2 - Markdown): The Context timeframe is in a confirmed downtrend. This is your signal to look for bearish rally opportunities.

How It Works

The indicator uses a combination of moving averages and trend strength to objectively define each stage:

Trend Alignment: It checks if the 5 EMA, 10 EMA, and 20 EMA are properly stacked above or below the 50 SMA to determine the potential trend direction.

Trend Strength: It uses the ADX to measure the strength of the trend. A trend is only confirmed as Stage 2 if the ADX is above a user-defined threshold (default is 23), filtering out weak or choppy moves.

Stage Definition: Any period that is not a confirmed, strong Stage 2 Markup or Markdown is classified as a Stage 1 consolidation phase.

Key Features

Multi-Timeframe (MTF) Projection: Select your master "Context" timeframe, and its analysis will be displayed on any chart you view.

Customizable Inputs: Easily adjust the moving average lengths and ADX threshold to fit your specific strategy and the asset you are trading.

Clear Visual Cues: The intuitive background coloring makes it easy to assess the market environment at a glance.

Stage Transition Alerts: Set up specific alerts to be notified the moment your Context timeframe shifts from a Stage 1 consolidation to a Stage 2 trend, ensuring you never miss a potential setup.

How to Use This Indicator

Add the indicator to your chart.

In the settings, set the "Context Timeframe" to your highest timeframe (e.g., "15" for 15-minute).

Create alerts for the "Stage 1 -> Stage 2" conditions.

When you receive an alert, it signals that a potential trend is beginning on your Context chart.

Switch to your lower Validation and Entry timeframes. The background color will confirm the higher-timeframe trend, giving you the confidence to look for your specific entry patterns.

Disclaimer: This tool is designed for confluence and environmental analysis. It is not a standalone signal generator. It should be used in conjunction with your own price action, volume, or order flow analysis to validate trade entries.