DynamicPeriodPublicDynamic Period Calculation Library

This library provides tools for adaptive period determination, useful for creating indicators or strategies that automatically adjust to market conditions.

Overview

The Dynamic Period Library calculates adaptive periods based on pivot points, enabling the creation of responsive indicators and strategies that adjust to market volatility.

Key Features

Dynamic Periods: Computes periods using distances between pivot highs and lows.

Customizable Parameters: Users can adjust detection settings and period constraints.

Robust Handling: Includes fallback mechanisms for cases with insufficient pivot data.

Use Cases

Adaptive Indicators: Build tools that respond to market volatility by adjusting their periods dynamically.

Dynamic Strategies: Enhance trading strategies by integrating pivot-based period adjustments.

Function: `dynamic_period`

Description

Calculates a dynamic period based on the average distances between pivot highs and lows.

Parameters

`left` (default: 5): Number of left-hand bars for pivot detection.

`right` (default: 5): Number of right-hand bars for pivot detection.

`numPivots` (default: 5): Minimum pivots required for calculation.

`minPeriod` (default: 2): Minimum allowed period.

`maxPeriod` (default: 50): Maximum allowed period.

`defaultPeriod` (default: 14): Fallback period if no pivots are found.

Returns

A dynamic period calculated based on pivot distances, constrained by `minPeriod` and `maxPeriod`.

Example

//@version=6

import CrimsonVault/DynamicPeriodPublic/1

left = input.int(5, "Left bars", minval = 1)

right = input.int(5, "Right bars", minval = 1)

numPivots = input.int(5, "Number of Pivots", minval = 2)

period = DynamicPeriodPublic.dynamic_period(left, right, numPivots)

plot(period, title = "Dynamic Period", color = color.blue)

Implementation Notes

Pivot Detection: Requires sufficient historical data to identify pivots accurately.

Edge Cases: Ensures a default period is applied when pivots are insufficient.

Constraints: Limits period values to a user-defined range for stability.

Techindicator

IndicatorsLibrary "Indicators"

cmf(lookback, n_to_smooth)

Calculates the Chaikin's Money Flow.

Parameters:

lookback (simple int)

n_to_smooth (simple int)

Returns: float The Money Flow value.

cmma(lookback, atr_length)

Calculates the CMMA (Close Minus Moving Average) indicator.

Parameters:

lookback (simple int)

atr_length (simple int)

Returns: float The CMMA value.

macd(fast_length, slow_length, n_to_smooth)

Calculates the normalized and scaled MACD.

Parameters:

fast_length (simple int)

slow_length (simple int)

n_to_smooth (simple int)

Returns: A tuple containing .

stochK(length, n_to_smooth)

Calculates a simplified Stochastic Oscillator.

Uses: 100 * ta.sma((close - lowest_low) / (highest_high - lowest_low), n_to_smooth)

Parameters:

length (simple int)

n_to_smooth (simple int)

Returns: float The Stochastic %K value.

williamsR(length)

Calculates the Williams %R using the stochK function.

Uses: -1 * (100 - stoch(length, 1))

Parameters:

length (simple int)

Returns: float The Williams %R value.

supertrendLibrary "supertrend"

supertrend : Library dedicated to different variations of supertrend

supertrend_atr(length, multiplier, atrMaType, source, highSource, lowSource, waitForClose, delayed)

supertrend_atr: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

length (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

delayed (simple bool) : : if set to true lags supertrend atr stop based on target levels.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_bands(bandType, maType, length, multiplier, source, highSource, lowSource, waitForClose, useTrueRange, useAlternateSource, alternateSource, sticky)

supertrend_bands: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

bandType (simple string) : : Type of band used - can be bb, kc or dc

maType (simple string) : : Moving Average type for Bands. This can be sma, ema, hma, rma, wma, vwma, swma

length (simple int) : : Band Length

multiplier (float) : : Std deviation or ATR multiplier for Bollinger Bands and Keltner Channel

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

useTrueRange (simple bool) : : Used for Keltner channel. If set to false, then high-low is used as range instead of true range

useAlternateSource (simple bool) : - Custom source is used for Donchian Chanbel only if useAlternateSource is set to true

alternateSource (float) : - Custom source for Donchian channel

sticky (simple bool) : : if set to true borders change only when price is beyond borders.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_zigzag(length, history, useAlternativeSource, alternativeSource, source, highSource, lowSource, waitForClose, atrlength, multiplier, atrMaType)

supertrend_zigzag: Zigzag pivot based supertrend

Parameters:

length (simple int) : : Zigzag Length

history (simple int) : : number of historical pivots to consider

useAlternativeSource (simple bool)

alternativeSource (float)

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrlength (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

zupertrend(length, history, useAlternativeSource, alternativeSource, source, highSource, lowSource, waitForClose, atrlength, multiplier, atrMaType)

zupertrend: Zigzag pivot based supertrend

Parameters:

length (simple int) : : Zigzag Length

history (simple int) : : number of historical pivots to consider

useAlternativeSource (simple bool)

alternativeSource (float)

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrlength (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

zsupertrend(zigzagpivots, history, source, highSource, lowSource, waitForClose, atrMaType, atrlength, multiplier)

zsupertrend: Same as zigzag supertrend. But, works on already calculated array rather than Calculating fresh zigzag

Parameters:

zigzagpivots (array) : : Precalculated zigzag pivots

history (simple int) : : number of historical pivots to consider

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

atrlength (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

taLibrary "ta"

Collection of all custom and enhanced TA indicators

ma(source, maType, length)

returns custom moving averages

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

Returns: moving average for the given type and length

atr(maType, length)

returns ATR with custom moving average

Parameters:

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

Returns: ATR for the given moving average type and length

atrpercent(maType, length)

returns ATR as percentage of close price

Parameters:

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

Returns: ATR as percentage of close price for the given moving average type and length

bb(source, maType, length, multiplier, sticky)

returns Bollinger band for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Bollinger band with custom moving average for given source, length and multiplier

bbw(source, maType, length, multiplier, sticky)

returns Bollinger bandwidth for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Bollinger Bandwidth for custom moving average for given source, length and multiplier

bpercentb(source, maType, length, multiplier, sticky)

returns Bollinger Percent B for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Bollinger Percent B for custom moving average for given source, length and multiplier

kc(source, maType, length, multiplier, useTrueRange, sticky)

returns Keltner Channel for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Keltner Channel for custom moving average for given souce, length and multiplier

kcw(source, maType, length, multiplier, useTrueRange, sticky)

returns Keltner Channel Width with custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Keltner Channel Width for custom moving average

kpercentk(source, maType, length, multiplier, useTrueRange, sticky)

returns Keltner Channel Percent K Width with custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Keltner Percent K for given moving average, source, length and multiplier

dc(length, useAlternateSource, alternateSource, sticky)

returns Custom Donchian Channel

Parameters:

length (simple int) : - donchian channel length

useAlternateSource (simple bool) : - Custom source is used only if useAlternateSource is set to true

alternateSource (float) : - Custom source

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel

dcw(length, useAlternateSource, alternateSource, sticky)

returns Donchian Channel Width

Parameters:

length (simple int) : - donchian channel length

useAlternateSource (simple bool) : - Custom source is used only if useAlternateSource is set to true

alternateSource (float) : - Custom source

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel width

dpercentd(length, useAlternateSource, alternateSource, sticky)

returns Donchian Channel Percent of price

Parameters:

length (simple int) : - donchian channel length

useAlternateSource (simple bool) : - Custom source is used only if useAlternateSource is set to true

alternateSource (float) : - Custom source

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel Percent D

oscillatorRange(source, method, highlowLength, rangeLength, sticky)

oscillatorRange - returns Custom overbought/oversold areas for an oscillator input

Parameters:

source (float) : - Osillator source such as RSI, COG etc.

method (simple string) : - Valid values for method are : sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

highlowLength (simple int) : - length on which highlow of the oscillator is calculated

rangeLength (simple int) : - length used for calculating oversold/overbought range - usually same as oscillator length

sticky (simple bool) : - overbought, oversold levels won't change unless crossed

Returns: Dynamic overbought and oversold range for oscillator input

oscillator(type, length, shortLength, longLength, source, highSource, lowSource, method, highlowLength, sticky)

oscillator - returns Choice of oscillator with custom overbought/oversold range

Parameters:

type (simple string) : - oscillator type. Valid values : cci, cmo, cog, mfi, roc, rsi, stoch, tsi, wpr

length (simple int) : - Oscillator length - not used for TSI

shortLength (simple int) : - shortLength only used for TSI

longLength (simple int) : - longLength only used for TSI

source (float) : - custom source if required

highSource (float) : - custom high source for stochastic oscillator

lowSource (float) : - custom low source for stochastic oscillator

method (simple string) : - Valid values for method are : sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

highlowLength (simple int) : - length on which highlow of the oscillator is calculated

sticky (simple bool) : - overbought, oversold levels won't change unless crossed

Returns: Oscillator value along with dynamic overbought and oversold range for oscillator input

PitchforkLibrary "Pitchfork"

Pitchfork class

method tostring(this)

Converts PitchforkTypes/Fork object to string representation

Namespace types: Fork

Parameters:

this (Fork) : PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork

method tostring(this)

Converts Array of PitchforkTypes/Fork object to string representation

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork array

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkProperties object to string representation

Namespace types: PitchforkProperties

Parameters:

this (PitchforkProperties) : PitchforkTypes/PitchforkProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkProperties

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkDrawingProperties object to string representation

Namespace types: PitchforkDrawingProperties

Parameters:

this (PitchforkDrawingProperties) : PitchforkTypes/PitchforkDrawingProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkDrawingProperties

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/Pitchfork object to string representation

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/Pitchfork

method createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing from PitchforkTypes/Pitchfork object

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/PitchforkDrawing object created

method createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing array from PitchforkTypes/Pitchfork array of objects

Namespace types: array

Parameters:

this (array) : array of PitchforkTypes/Pitchfork object

Returns: array of PitchforkTypes/PitchforkDrawing object created

method draw(this)

draws from PitchforkTypes/PitchforkDrawing object

Namespace types: PitchforkDrawing

Parameters:

this (PitchforkDrawing) : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object drawn

method delete(this)

deletes PitchforkTypes/PitchforkDrawing object

Namespace types: PitchforkDrawing

Parameters:

this (PitchforkDrawing) : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object deleted

method delete(this)

deletes underlying drawing of PitchforkTypes/Pitchfork object

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/Pitchfork object deleted

method delete(this)

deletes array of PitchforkTypes/PitchforkDrawing objects

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/PitchforkDrawing object

Returns: Array of PitchforkTypes/PitchforkDrawing object deleted

method delete(this)

deletes underlying drawing in array of PitchforkTypes/Pitchfork objects

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/Pitchfork object

Returns: Array of PitchforkTypes/Pitchfork object deleted

method clear(this)

deletes array of PitchforkTypes/PitchforkDrawing objects and clears the array

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/PitchforkDrawing object

Returns: void

method clear(this)

deletes array of PitchforkTypes/Pitchfork objects and clears the array

Namespace types: array

Parameters:

this (array) : Array of Pitchfork/Pitchfork object

Returns: void

PitchforkDrawingProperties

Pitchfork Drawing Properties object

Fields:

extend (series bool) : If set to true, forks are extended towards right. Default is true

fill (series bool) : Fill forklines with transparent color. Default is true

fillTransparency (series int) : Transparency at which fills are made. Only considered when fill is set. Default is 80

forceCommonColor (series bool) : Force use of common color for forks and fills. Default is false

commonColor (series color) : common fill color. Used only if ratio specific fill colors are not available or if forceCommonColor is set to true.

PitchforkDrawing

Pitchfork drawing components

Fields:

medianLine (Line type from Trendoscope/Drawing/2) : Median line of the pitchfork

baseLine (Line type from Trendoscope/Drawing/2) : Base line of the pitchfork

forkLines (array type from Trendoscope/Drawing/2) : fork lines of the pitchfork

linefills (array type from Trendoscope/Drawing/2) : Linefills between forks

Fork

Fork object property

Fields:

ratio (series float) : Fork ratio

forkColor (series color) : color of fork. Default is blue

include (series bool) : flag to include the fork in drawing. Default is true

PitchforkProperties

Pitchfork Properties

Fields:

forks (array) : Array of Fork objects

type (series string) : Pitchfork type. Supported values are "regular", "schiff", "mschiff", Default is regular

inside (series bool) : Flag to identify if to draw inside fork. If set to true, inside fork will be drawn

Pitchfork

Pitchfork object

Fields:

a (chart.point) : Pivot Point A of pitchfork

b (chart.point) : Pivot Point B of pitchfork

c (chart.point) : Pivot Point C of pitchfork

properties (PitchforkProperties) : PitchforkProperties object which determines type and composition of pitchfork

dProperties (PitchforkDrawingProperties) : Drawing properties for pitchfork

lProperties (LineProperties type from Trendoscope/Drawing/2) : Common line properties for Pitchfork lines

drawing (PitchforkDrawing) : PitchforkDrawing object

SnowdexUtilsLibrary "SnowdexUtils"

the various function that often use when create a strategy trading.

f_backtesting_date(train_start_date, train_end_date, test_date, deploy_date)

Backtesting within a specific window based on deployment and testing dates.

Parameters:

train_start_date (int) : the start date for training the strategy.

train_end_date (int) : the end date for training the strategy.

test_date (bool) : if true, backtests within the period from `train_end_date` to the current time.

deploy_date (bool) : if true, the strategy backtests up to the current time.

Returns: given time falls within the specified window for backtesting.

f_init_ma(ma_type, source, length)

Initializes a moving average based on the specified type.

Parameters:

ma_type (simple string) : the type of moving average (e.g., "RMA", "EMA", "SMA", "WMA").

source (float) : the input series for the moving average calculation.

length (simple int) : the length of the moving average window.

Returns: the calculated moving average value.

f_init_tp(side, entry_price, rr, sl_open_position)

Calculates the target profit based on entry price, risk-reward ratio, and stop loss. The formula is `tp = entry price + (rr * (entry price - stop loss))`.

Parameters:

side (bool) : the trading side (true for long, false for short).

entry_price (float) : the entry price of the position.

rr (float) : the risk-reward ratio.

sl_open_position (float) : the stop loss price for the open position.

Returns: the calculated target profit value.

f_round_up(number, decimals)

Rounds up a number to a specified number of decimals.

Parameters:

number (float)

decimals (int)

Returns: The rounded-up number.

f_get_pip_size()

Calculates the pip size for the current instrument.

Returns: Pip size adjusted for Forex instruments or 1 for others.

f_table_get_position(value)

Maps a string to a table position constant.

Parameters:

value (string) : String representing the desired position (e.g., "Top Right").

Returns: The corresponding position constant or `na` for invalid values.

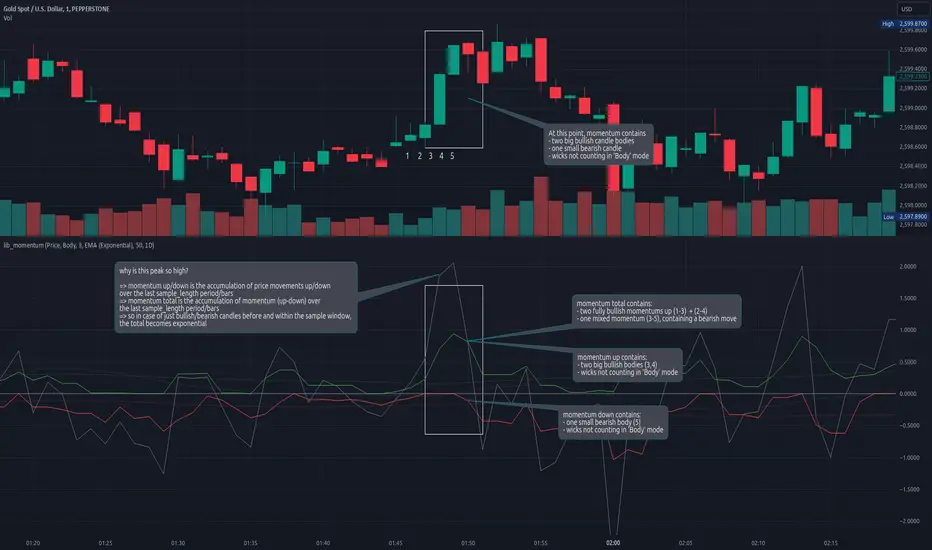

lib_momentumLibrary "lib_momentum"

This library calculates the momentum, derived from a sample range of prior candles. Depending on set MomentumType it either deduces the momentum from the price, volume, or a product of both. If price/product are selected, you can choose from SampleType if only candle body, full range from high to low or a combination of both (body counts full, wicks half for each direction) should be used. Optional: You can choose to normalize the results, dividing each value by its average (normalization_ma_length, normalization_ma). This will allow comparison between different instruments. For the normalization Moving Average you can choose any currently supported in my lib_no_delay.

get_momentum(momentum_type, sample_type, sample_length, normalization_ma_length, normalization_ma)

Parameters:

momentum_type (series MomentumType) : select one of MomentumType. to sample the price, volume or a product of both

sample_type (series SampleType) : select one of SampleType. to sample the body, total range from high to low or a combination of both (body count full, wicks half for each direction)

sample_length (simple int) : how many candles should be sampled (including the current)

normalization_ma_length (simple int) : if you want to normalize results (momentum / momentum average) this sets the period for the average. (default = 0 => no normalization)

normalization_ma (simple MovingAverage enum from robbatt/lib_no_delay/9) : is the type of moving average to normalize / compare with

Returns: returns the current momentum where the total line is not just (up - down) but also sampled over the sample_length and can therefore be used as trend indicator. If up/down fail to reach total's level it's a sign of decreasing momentum, if up/down exceed total the trend it's a sign of increasing momentum.

RawCuts_01Library "RawCuts_01"

A collection of functions by:

mutantdog

The majority of these are used within published projects, some useful variants have been included here aswell.

This is volume one consisting mainly of smaller functions, predominantly the filters and standard deviations from Weight Gain 4000.

Also included at the bottom are various snippets of related code for demonstration. These can be copied and adjusted according to your needs.

A full up-to-date table of contents is located at the top of the main script.

WEIGHT GAIN FILTERS

A collection of moving average type filters with adjustable volume weighting.

Based upon the two most common methods of volume weighting.

'Simple' uses the standard method in which a basic VWMA is analogous to SMA.

'Elastic' uses exponential method found in EVWMA which is analogous to RMA.

Volume weighting is applied according to an exponent multiplier of input volume.

0 >> volume^0 (unweighted), 1 >> volume^1 (fully weighted), use float values for intermediate weighting.

Additional volume filter switch for smoothing of outlier events.

DIVA MODULAR DEVIATIONS

A small collection of standard and absolute deviations.

Includes the weightgain functionality as above.

Basic modular functionality for more creative uses.

Optional input (ct) for external central tendency (aka: estimator).

Can be assigned to alternative filter or any float value. Will default to internal filter when no ct input is received.

Some other useful or related functions included at the bottom along with basic demonstration use.

weightgain_sma(src, len, xVol, fVol)

Simple Moving Average (SMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Standard Simple Moving Average with Simple Weight Gain applied.

weightgain_hsma(src, len, xVol, fVol)

Harmonic Simple Moving Average (hSMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Harmonic Simple Moving Average with Simple Weight Gain applied.

weightgain_gsma(src, len, xVol, fVol)

Geometric Simple Moving Average (gSMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Geometric Simple Moving Average with Simple Weight Gain applied.

weightgain_wma(src, len, xVol, fVol)

Linear Weighted Moving Average (WMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Basic Linear Weighted Moving Average with Simple Weight Gain applied.

weightgain_hma(src, len, xVol, fVol)

Hull Moving Average (HMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Basic Hull Moving Average with Simple Weight Gain applied.

diva_sd_sma(src, len, xVol, fVol, ct)

Standard Deviation (SD SMA): Diva / Weight Gain (Simple Volume)

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_sma().

Returns:

diva_sd_wma(src, len, xVol, fVol, ct)

Standard Deviation (SD WMA): Diva / Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_wma().

Returns:

diva_aad_sma(src, len, xVol, fVol, ct)

Average Absolute Deviation (AAD SMA): Diva / Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_sma().

Returns:

diva_aad_wma(src, len, xVol, fVol, ct)

Average Absolute Deviation (AAD WMA): Diva / Weight Gain (Simple Volume) .

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_wma().

Returns:

weightgain_ema(src, len, xVol, fVol)

Exponential Moving Average (EMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Exponential Moving Average with Elastic Weight Gain applied.

weightgain_dema(src, len, xVol, fVol)

Double Exponential Moving Average (DEMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Double Exponential Moving Average with Elastic Weight Gain applied.

weightgain_tema(src, len, xVol, fVol)

Triple Exponential Moving Average (TEMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Triple Exponential Moving Average with Elastic Weight Gain applied.

weightgain_rma(src, len, xVol, fVol)

Rolling Moving Average (RMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Rolling Moving Average with Elastic Weight Gain applied.

weightgain_drma(src, len, xVol, fVol)

Double Rolling Moving Average (DRMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Double Rolling Moving Average with Elastic Weight Gain applied.

weightgain_trma(src, len, xVol, fVol)

Triple Rolling Moving Average (TRMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Triple Rolling Moving Average with Elastic Weight Gain applied.

diva_sd_ema(src, len, xVol, fVol, ct)

Standard Deviation (SD EMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_ema().

Returns:

diva_sd_rma(src, len, xVol, fVol, ct)

Standard Deviation (SD RMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_rma().

Returns:

weightgain_vidya_rma(src, len, xVol, fVol)

VIDYA v1 RMA base (VIDYA-RMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: VIDYA v1, RMA base with Elastic Weight Gain applied.

weightgain_vidya_ema(src, len, xVol, fVol)

VIDYA v1 EMA base (VIDYA-EMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: VIDYA v1, EMA base with Elastic Weight Gain applied.

diva_sd_vidya_rma(src, len, xVol, fVol, ct)

Standard Deviation (SD VIDYA-RMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_vidya_rma().

Returns:

diva_sd_vidya_ema(src, len, xVol, fVol, ct)

Standard Deviation (SD VIDYA-EMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_vidya_ema().

Returns:

weightgain_sema(src, len, xVol, fVol)

Parameters:

src (float)

len (simple int)

xVol (float)

fVol (bool)

diva_sd_sema(src, len, xVol, fVol)

Parameters:

src (float)

len (simple int)

xVol (float)

fVol (bool)

diva_mad_mm(src, len, ct)

Median Absolute Deviation (MAD MM): Diva (no volume weighting).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

ct (float) : Central tendency (optional, na = bypass). Internal: ta.median()

Returns:

source_switch(slct, aux1, aux2, aux3, aux4)

Custom Source Selector/Switch function. Features standard & custom 'weighted' sources with additional aux inputs.

Parameters:

slct (string) : Choose from custom set of string values.

aux1 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

aux2 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

aux3 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

aux4 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

Returns: Float value, to be used as src input for other functions.

colour_gradient_ma_div(ma1, ma2, div, bull, bear, mid, mult)

Colour Gradient for plot fill between two moving averages etc, with seperate bull/bear and divergence strength.

Parameters:

ma1 (float) : Input for fast moving average (eg: bullish when above ma2).

ma2 (float) : Input for slow moving average (eg: bullish when below ma1).

div (float) : Input deviation/divergence value used to calculate strength of colour.

bull (color) : Colour when ma1 above ma2.

bear (color) : Colour when ma1 below ma2.

mid (color) : Neutral colour when ma1 = ma2.

mult (int) : Opacity multiplier. 100 = maximum, 0 = transparent.

Returns: Colour with transparency (according to specified inputs)

CandlestickPatternsLibrary "CandlestickPatterns"

zigzag(_low, _high, depth, deviation, backstep)

Parameters:

_low (float)

_high (float)

depth (int)

deviation (int)

backstep (int)

getTrend(trendType, currentClose, zz_downtrend, zz_uptrend, ema14, ema28)

Parameters:

trendType (string)

currentClose (float)

zz_downtrend (bool)

zz_uptrend (bool)

ema14 (float)

ema28 (float)

isInside(currentHigh, currentLow, currentClose, currentOpen, prevHigh, prevLow)

Parameters:

currentHigh (float)

currentLow (float)

currentClose (float)

currentOpen (float)

prevHigh (float)

prevLow (float)

checkMorningStar(open0, high0, low0, close0, open1, high1, low1, close1, open2, high2, low2, close2, innerCandleThreshold, closingMinThreshold, closingMaxThreshold, useDojiFilter, dojiSize, downTrend)

Parameters:

open0 (float)

high0 (float)

low0 (float)

close0 (float)

open1 (float)

high1 (float)

low1 (float)

close1 (float)

open2 (float)

high2 (float)

low2 (float)

close2 (float)

innerCandleThreshold (float)

closingMinThreshold (float)

closingMaxThreshold (float)

useDojiFilter (bool)

dojiSize (float)

downTrend (bool)

checkEveningStar(open0, high0, low0, close0, open1, high1, low1, close1, open2, high2, low2, close2, innerCandleThreshold, closingMinThreshold, closingMaxThreshold, useDojiFilter, dojiSize, upTrend)

Parameters:

open0 (float)

high0 (float)

low0 (float)

close0 (float)

open1 (float)

high1 (float)

low1 (float)

close1 (float)

open2 (float)

high2 (float)

low2 (float)

close2 (float)

innerCandleThreshold (float)

closingMinThreshold (float)

closingMaxThreshold (float)

useDojiFilter (bool)

dojiSize (float)

upTrend (bool)

checkHammerPattern(open, high, low, close, bodyAvg, shadowFactor, downTrend)

Parameters:

open (float)

high (float)

low (float)

close (float)

bodyAvg (float)

shadowFactor (float)

downTrend (bool)

checkInvertedHammerPattern(open, high, low, close, bodyAvg, shadowFactor, downTrend)

Parameters:

open (float)

high (float)

low (float)

close (float)

bodyAvg (float)

shadowFactor (float)

downTrend (bool)

checkHangingManPattern(open, high, low, close, bodyAvg, shadowFactor, upTrend)

Parameters:

open (float)

high (float)

low (float)

close (float)

bodyAvg (float)

shadowFactor (float)

upTrend (bool)

checkShootingStarPattern(open, high, low, close, bodyAvg, shadowFactor, upTrend)

Parameters:

open (float)

high (float)

low (float)

close (float)

bodyAvg (float)

shadowFactor (float)

upTrend (bool)

checkLevels(high0, high1, high2, low0, low1, low2, lookbackPeriod)

Parameters:

high0 (float)

high1 (float)

high2 (float)

low0 (float)

low1 (float)

low2 (float)

lookbackPeriod (int)

HTFBands█ OVERVIEW

Contains type and methods for drawing higher-timeframe bands of several types:

Bollinger bands

Parabolic SAR

Supertrend

VWAP

By copy pasting ready made code sections to your script you can add as many multi-timeframe bands as necessary.

█ HOW TO USE

Please see instructions in the code. (Important: first fold all sections of the script: press Cmd + K then Cmd + - (for Windows Ctrl + K then Ctrl + -)

█ FULL LIST OF FUNCTIONS AND PARAMETERS

atr2(length)

An alternate ATR function to the `ta.atr()` built-in, which allows a "series float"

`length` argument.

Parameters:

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The ATR value.

pine_supertrend2(factor, atrLength, wicks)

An alternate SuperTrend function to `supertrend()`, which allows a "series float"

`atrLength` argument.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when

reversing trend, or to use the close price. Optional. Default is false.

Returns: ( ) A tuple of the superTrend value and trend direction.

method getDefaultBandQ1(bandType)

For a given BandType returns its default Q1

Namespace types: series BandTypes

Parameters:

bandType (series BandTypes)

method getDefaultBandQ2(bandType)

For a given BandType returns its default Q2

Namespace types: series BandTypes

Parameters:

bandType (series BandTypes)

method getDefaultBandQ3(bandType)

For a given BandType returns its default Q3

Namespace types: series BandTypes

Parameters:

bandType (series BandTypes)

method init(this, bandsType, q1, q2, q3, vwapAnchor)

Initiates RsParamsBands for each band (used in htfUpdate() withi req.sec())

Namespace types: RsParamsBands

Parameters:

this (RsParamsBands)

bandsType (series BandTypes)

q1 (float) : (float) Depending on type: BB - length, SAR - AF start, ST - ATR's prd

q2 (float) : (float) Depending on type: BB - StdDev mult, SAR - AF step, ST - mult

q3 (float) : (float) Depending on type: BB - not used, SAR - AF max, ST - not used

vwapAnchor (series VwapAnchors) : (VwapAnchors) VWAP ahcnor

method init(this, bandsType, tf, showRecentBars, lblsShow, lblsMaxLabels, lblSize, lnMidClr, lnUpClr, lnLoClr, fill, fillClr, lnWidth, lnSmoothen)

Initialises object with params (incl. input). Creates arrays if any.

Namespace types: HtfBands

Parameters:

this (HtfBands)

bandsType (series BandTypes) : (BandTypes) Just used to enable/disable - if BandTypes.none then disable )

tf (string) : (string) Timeframe

showRecentBars (int) : (int) Only show over this number of recent bars

lblsShow (bool) : (bool) Show labels

lblsMaxLabels (int) : (int) Max labels to show

lblSize (string) : (string) Size of the labels

lnMidClr (color) : (color) Middle band color

lnUpClr (color) : (color) Upper band color

lnLoClr (color) : (color) Lower band color

fill (bool)

fillClr (color) : (color) Fill color

lnWidth (int) : (int) Line width

lnSmoothen (bool) : (bool) Smoothen the bands

method htfUpdateTuple(rsPrms, repaint)

(HTF) Calculates Bands within request.security(). Returns tuple . If any or all of the bands are not available returns na as their value.

Namespace types: RsParamsBands

Parameters:

rsPrms (RsParamsBands) : (RsParamsBands) Parameters of the band.

repaint (bool) : (bool) If true does not update on realtime bars.

Returns: A tuple (corresponds to fields in RsReturnBands)

method importRsRetTuple(this, htfBi, mid, up, lo, dir)

Imports a tuple returned from req.sec() into an HtfBands object

Namespace types: HtfBands

Parameters:

this (HtfBands) : (HtfBands) Object to import to

htfBi (int) : (float) Higher timeframe's bar index (Default = na)

mid (float)

up (float) : (float) Value of upper band (Default = na)

lo (float) : (float) Value of lower band (Default = na)

dir (int) : (int) Direction (for bands like Parabolic SAR) (Default = na)

method addUpdDrawings(this, rsPrms)

Draws band's labels

Namespace types: HtfBands

Parameters:

this (HtfBands)

rsPrms (RsParamsBands)

method update(this)

Sets band's values to na on intrabars if `smoothen` is set.

Namespace types: HtfBands

Parameters:

this (HtfBands)

method newRsParamsBands(this)

A wraper for RsParamsBands.new()

Namespace types: LO_A

Parameters:

this (LO_A)

method newHtfBands(this)

A wraper for HtfBands.new()

Namespace types: LO_B

Parameters:

this (LO_B)

RsParamsBands

Used to pass bands' params to req.sec()

Fields:

bandsType (series BandTypes) : (enum BandTypes) Type of the band (BB, SAR etc.)

q1 (series float) : (float) Depending on type: BB - length, SAR - AF start, ST - ATR's prd

q2 (series float) : (float) Depending on type: BB - StdDev mult, SAR - AF step, ST - mult

q3 (series float) : (float) Depending on type: BB - not used, SAR - AF max, ST - not used

vwapAnchor (series VwapAnchors)

RsReturnBands

Used to return bands' data from req.sec(). Params of the bands are in RsParamsBands

Fields:

htfBi (series float) : (float) Higher timeframe's bar index (Default = na)

upBand (series float) : (float) Value of upper band (Default = na)

loBand (series float) : (float) Value of lower band (Default = na)

midBand (series float) : (float) Value of middle band (Default = na)

dir (series int) : (float) Direction (for bands like Parabolic SAR) (Default = na)

BandsDrawing

Contains plot visualization parameters and stores and keeps track of lines, labels and other visual objects (not plots)

Fields:

lnMidClr (series color) : (color) Middle band color

lnLoClr (series color) : (color) Lower band color

lnUpClr (series color) : (color) Upper band color

fillUpClr (series color)

fillLoClr (series color)

lnWidth (series int) : (int) Line width

lnSmoothen (series bool) : (bool) Smoothen the bands

showHistory (series bool) : (bool) If true show bands lines, otherwise only current level

showRecentBars (series int) : (int) Only show over this number of recent bars

arLbl (array) : (label Labels

lblsMaxLabels (series int) : (int) Max labels to show

lblsShow (series bool) : (bool) Show labels

lblSize (series string) : (string) Size of the labels

HtfBands

Calcs and draws HTF bands

Fields:

rsRet (RsReturnBands) : (RsReturnBands) Bands' values

rsRetNaObj (RsReturnBands) : (RsReturnBands) Dummy na obj for returning from request.security()

rsPrms (RsParamsBands) : (RsParamsBands) Band parameters (for htfUpdate() called in req.sec() )

drw (BandsDrawing) : (BandsDrawing) Contains plot visualization parameters and stores and keeps track of lines, labels and other visual objects (not plots)

enabled (series bool) : (bool) Toggles bands on/off

tf (series string) : (string) Timeframe

LO_A

LO Library object, whose only purpose is to serve as a shorthand for library name in script code.

Fields:

dummy (series string)

LO_B

LO Library object, whose only purpose is to serve as a shorthand for library name in script code.

Fields:

dummy (series string)

HTFMAs█ OVERVIEW

Contains a type HTFMA used to return data on six moving averages from a higher timeframe.

Several types of MA's are supported.

█ HOW TO USE

Please see instructions in the code (in library description). (Important: first fold all sections of the script: press Cmd + K then Cmd + - (for Windows Ctrl + K then Ctrl + -)

█ FULL LIST OF FUNCTIONS AND PARAMETERS

method getMaType(this)

Enumerator function, given a key returns `enum MaTypes` value

Namespace types: series string, simple string, input string, const string

Parameters:

this (string)

method init(this, enableAll, ma1Enabled, ma1MaType, ma1Src, ma1Prd, ma2Enabled, ma2MaType, ma2Src, ma2Prd, ma3Enabled, ma3MaType, ma3Src, ma3Prd, ma4Enabled, ma4MaType, ma4Src, ma4Prd, ma5Enabled, ma5MaType, ma5Src, ma5Prd, ma6Enabled, ma6MaType, ma6Src, ma6Prd)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs)

enableAll (simple MaEnable)

ma1Enabled (bool)

ma1MaType (series MaTypes)

ma1Src (string)

ma1Prd (int)

ma2Enabled (bool)

ma2MaType (series MaTypes)

ma2Src (string)

ma2Prd (int)

ma3Enabled (bool)

ma3MaType (series MaTypes)

ma3Src (string)

ma3Prd (int)

ma4Enabled (bool)

ma4MaType (series MaTypes)

ma4Src (string)

ma4Prd (int)

ma5Enabled (bool)

ma5MaType (series MaTypes)

ma5Src (string)

ma5Prd (int)

ma6Enabled (bool)

ma6MaType (series MaTypes)

ma6Src (string)

ma6Prd (int)

method init(this, enableAll, tf, rngAtrQ, showRecentBars, lblsOffset, lblsShow, lnOffset, lblSize, lblStyle, smoothen, ma1lnClr, ma1lnWidth, ma1lnStyle, ma2lnClr, ma2lnWidth, ma2lnStyle, ma3lnClr, ma3lnWidth, ma3lnStyle, ma4lnClr, ma4lnWidth, ma4lnStyle, ma5lnClr, ma5lnWidth, ma5lnStyle, ma6lnClr, ma6lnWidth, ma6lnStyle, ma1ShowHistory, ma2ShowHistory, ma3ShowHistory, ma4ShowHistory, ma5ShowHistory, ma6ShowHistory, ma1ShowLabel, ma2ShowLabel, ma3ShowLabel, ma4ShowLabel, ma5ShowLabel, ma6ShowLabel)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

enableAll (series MaEnable)

tf (string)

rngAtrQ (int)

showRecentBars (int)

lblsOffset (int)

lblsShow (bool)

lnOffset (int)

lblSize (string)

lblStyle (string)

smoothen (bool)

ma1lnClr (color)

ma1lnWidth (int)

ma1lnStyle (string)

ma2lnClr (color)

ma2lnWidth (int)

ma2lnStyle (string)

ma3lnClr (color)

ma3lnWidth (int)

ma3lnStyle (string)

ma4lnClr (color)

ma4lnWidth (int)

ma4lnStyle (string)

ma5lnClr (color)

ma5lnWidth (int)

ma5lnStyle (string)

ma6lnClr (color)

ma6lnWidth (int)

ma6lnStyle (string)

ma1ShowHistory (bool)

ma2ShowHistory (bool)

ma3ShowHistory (bool)

ma4ShowHistory (bool)

ma5ShowHistory (bool)

ma6ShowHistory (bool)

ma1ShowLabel (bool)

ma2ShowLabel (bool)

ma3ShowLabel (bool)

ma4ShowLabel (bool)

ma5ShowLabel (bool)

ma6ShowLabel (bool)

method get(this, id)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs)

id (int)

method set(this, id, prop, val)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs)

id (int)

prop (string)

val (string)

method set(this, id, prop, val)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

id (int)

prop (string)

val (string)

method htfUpdateTuple(rsParams, repaint)

Namespace types: RsParamsMAs

Parameters:

rsParams (RsParamsMAs)

repaint (bool)

method clear(this)

Namespace types: MaDrawing

Parameters:

this (MaDrawing)

method importRsRetTuple(this, htfBi, ma1, ma2, ma3, ma4, ma5, ma6)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

htfBi (int)

ma1 (float)

ma2 (float)

ma3 (float)

ma4 (float)

ma5 (float)

ma6 (float)

method getDrw(this, id)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

id (int)

method setDrwProp(this, id, prop, val)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

id (int)

prop (string)

val (string)

method initDrawings(this, rsPrms, dispBandWidth)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

rsPrms (RsParamsMAs)

dispBandWidth (float)

method updateDrawings(this, rsPrms, dispBandWidth)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

rsPrms (RsParamsMAs)

dispBandWidth (float)

method update(this)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `RsParamsMAs` child `RsMaCalcParams` objects (into the first first `maCount` of them)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs) : (RsParamsMAs) Target object to import prop values to.

oCfg (objProps type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `RsParamsMAs` child `RsMaCalcParams` objects (into the first first `maCount` of them)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs) : (RsParamsMAs) Target object to import prop values to.

oCfg (objProps0 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `RsParamsMAs` child `RsMaCalcParams` objects (into the first first `maCount` of them)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs) : (RsParamsMAs) Target object to import prop values to.

oCfg (objProps1 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `RsParamsMAs` child `RsMaCalcParams` objects (into the first first `maCount` of them)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs) : (RsParamsMAs) Target object to import prop values to.

oCfg (objProps2 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `RsParamsMAs` child `RsMaCalcParams` objects (into the first first `maCount` of them)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs) : (RsParamsMAs) Target object to import prop values to.

oCfg (objProps3 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `RsParamsMAs` child `RsMaCalcParams` objects (into the first first `maCount` of them)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs) : (RsParamsMAs) Target object to import prop values to.

oCfg (objProps4 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `RsParamsMAs` child `RsMaCalcParams` objects (into the first first `maCount` of them)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs) : (RsParamsMAs) Target object to import prop values to.

oCfg (objProps5 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `RsParamsMAs` child `RsMaCalcParams` objects (into the first first `maCount` of them)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs) : (RsParamsMAs) Target object to import prop values to.

oCfg (objProps6 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs)

oCfg (objProps7 type from moebius1977/CSVParser/1)

maCount (int)

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `HTFMAs` child `MaDrawing` objects (into the first first `maCount` of them)

Namespace types: RsParamsMAs

Parameters:

this (RsParamsMAs) : (HTFMAs) Target object to import prop values to.

oCfg (objProps8 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `HTFMAs` child `MaDrawing` objects (into the first first `maCount` of them)

Namespace types: HTFMAs

Parameters:

this (HTFMAs) : (HTFMAs) Target object to import prop values to.

oCfg (objProps type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `HTFMAs` child `MaDrawing` objects (into the first first `maCount` of them)

Namespace types: HTFMAs

Parameters:

this (HTFMAs) : (HTFMAs) Target object to import prop values to.

oCfg (objProps0 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `HTFMAs` child `MaDrawing` objects (into the first first `maCount` of them)

Namespace types: HTFMAs

Parameters:

this (HTFMAs) : (HTFMAs) Target object to import prop values to.

oCfg (objProps1 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `HTFMAs` child `MaDrawing` objects (into the first first `maCount` of them)

Namespace types: HTFMAs

Parameters:

this (HTFMAs) : (HTFMAs) Target object to import prop values to.

oCfg (objProps2 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `HTFMAs` child `MaDrawing` objects (into the first first `maCount` of them)

Namespace types: HTFMAs

Parameters:

this (HTFMAs) : (HTFMAs) Target object to import prop values to.

oCfg (objProps3 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `HTFMAs` child `MaDrawing` objects (into the first first `maCount` of them)

Namespace types: HTFMAs

Parameters:

this (HTFMAs) : (HTFMAs) Target object to import prop values to.

oCfg (objProps4 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `HTFMAs` child `MaDrawing` objects (into the first first `maCount` of them)

Namespace types: HTFMAs

Parameters:

this (HTFMAs) : (HTFMAs) Target object to import prop values to.

oCfg (objProps5 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Imports HTF MAs settings from objProps (of any level) into `HTFMAs` child `MaDrawing` objects (into the first first `maCount` of them)

Namespace types: HTFMAs

Parameters:

this (HTFMAs) : (HTFMAs) Target object to import prop values to.

oCfg (objProps6 type from moebius1977/CSVParser/1) : (CSVP.objProps) (one of objProps types) an objProps, ... opjProps8 containing properties' values in a child objProps objects

maCount (int) : (int) Number of tgtObj's RsMaCalcParams childs of tgtObj to set (1 to 6, starting from 1)

Returns: this

method importConfig(this, oCfg, maCount)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

oCfg (objProps7 type from moebius1977/CSVParser/1)

maCount (int)

method importConfig(this, oCfg, maCount)

Namespace types: HTFMAs

Parameters:

this (HTFMAs)

oCfg (objProps8 type from moebius1977/CSVParser/1)

maCount (int)

method newRsParamsMAs(this)

Namespace types: LO

Parameters:

this (LO)

method newHTFMAs(this)

Namespace types: LO

Parameters:

this (LO)

RsMaCalcParams

Parameters of one MA (only calculation params needed within req.sec(), visual parameters are within htfMAs type)

Fields:

enabled (series bool)

maType (series MaTypes) : MA type options: SMA / EMA / WMA / ...

src (series string)

prd (series int) : MA period

RsParamsMAs

Collection of parameters of 6 MAs. Used to pass params to req.sec()

Fields:

ma1CalcParams (RsMaCalcParams)

ma2CalcParams (RsMaCalcParams)

ma3CalcParams (RsMaCalcParams)

ma4CalcParams (RsMaCalcParams)

ma5CalcParams (RsMaCalcParams)

ma6CalcParams (RsMaCalcParams)

RsReturnMAs

Used to return data from req.sec().

Fields:

htfBi (series int)

ma1 (series float)

ma2 (series float)

ma3 (series float)

ma4 (series float)

ma5 (series float)

ma6 (series float)

MaDrawing

MA's plot parameters plus drawing objects for MA's current level (line and label).

Fields:

lnClr (series color) : (color) MA plot line color (like in plot())

lnWidth (series int) : (int) MA plot line width (like in plot())

lnStyle (series string) : (string) MA plot line style (like in plot())

showHistory (series bool) : (bool) Whether to plot the MA on historical bars or only show current level to the right of the latest bar.

showLabel (series bool) : (bool) Whether to show the name of the MA to the right of the MA's level

ln (series line) : (line) line to show MA"s current level

lbl (series label) : (label) label showing MA's name

HTFMAs

Contains data and drawing parameters for MA's of one timeframe (MA calculation parameters for MA's of one timeframe are in a separate object RsParamsMAs)

Fields:

rsRet (RsReturnMAs) : (RsReturnMAs) Contains data returned from req.sec(). Is set to na in between HTF bar changes if smoothing is enabled.

rsRetLast (RsReturnMAs) : (RsReturnMAs) Contains a copy of data returned from req.sec() in case rsRet is set to na for smoothing.

rsRetNaObj (RsReturnMAs) : (RsReturnMAs) An empty object as `na` placeholder

ma1Drawing (MaDrawing) : (MaDrawing) MA drawing properties

ma2Drawing (MaDrawing) : (MaDrawing) MA drawing properties

ma3Drawing (MaDrawing) : (MaDrawing) MA drawing properties

ma4Drawing (MaDrawing) : (MaDrawing) MA drawing properties

ma5Drawing (MaDrawing) : (MaDrawing) MA drawing properties

ma6Drawing (MaDrawing) : (MaDrawing) MA drawing properties

enabled (series bool) : (bool ) Enables/disables all of the MAs of one timeframe.

tf (series string) : (string) Timeframe

showHistory (series bool) : (bool ) Plot MA line on historical bars

rngAtrQ (series int) : (int ) A multiplier for atr(14). Determines a range within which the MA's will be plotted. MA's too far away will not be plotted.

showRecentBars (series int) : (int ) Only plot MA on these recent bars

smoothen (series bool) : (bool ) Smoothen MA plot. If false the same HTF value is returned on all chart bars within a HTF bar (intrabars), so the plot looks like steps.

lblsOffset (series int) : (int ) Show MA name this number of bars to the right off last bar.

lblsShow (series bool) : (bool ) Show MA name

lnOffset (series int) : (int ) Start line showing current level of the MA this number of bars to the right off the last bar.

lblSize (series string) : (string) Label size

lblStyle (series string) : (string) Label style

lblTxtAlign (series string) : (string) Label text align

bPopupLabel (series bool) : (bool ) Show current MA value as a tooltip to MA's name.

LO

LO Library object, whose only purpose is to serve as a shorthand for library name in script code.

Fields:

dummy (series string)

movingAveragesUtilitiesLibrary "movingAveragesUtilities"

get_movingAverages_data(source, length_fast, length_medium, length_slow)

Parameters:

source (float)

length_fast (simple int)

length_medium (simple int)

length_slow (simple int)

gridUtilitiesLibrary "gridUtilities"

TODO: add library description here

get_fibonacciGrid_data(length, trend_direction, plot_grid, plot_labels, bars_to_right, include_levels)

: Gets and plots a fibonacci grid.

Parameters:

length (int) : (int): The direction flag that indicates where the trend is going.

trend_direction (string) : (string): Direction of the trend (Long, Short or Neutral)

plot_grid (bool) : (bool): Plots the fibonacci grid.

plot_labels (bool) : (bool): Plots the datatable.

bars_to_right (int) : (bool): Plots the datatable.

include_levels (bool) : (bool): Plots the datatable.

Returns: : Returns a map with the grid levels, as string with the direction of the grid and a map with the values for the dataTable.

bollingerBandsLibrary "bollingerBands"

Bollinger bands related functions

get_multiple_bollinger_bands(stdv1, stdv2, stdv3, stdv4, stdv5, stdv6, stdv7, length, source)

Parameters:

stdv1 (int)

stdv2 (int)

stdv3 (int)

stdv4 (int)

stdv5 (int)

stdv6 (int)

stdv7 (int)

length (simple int)

source (float)

get_bb_volatility(bb_highest, bb_lowest, ma_length, lookback)

Parameters:

bb_highest (float)

bb_lowest (float)

ma_length (simple int)

lookback (int)

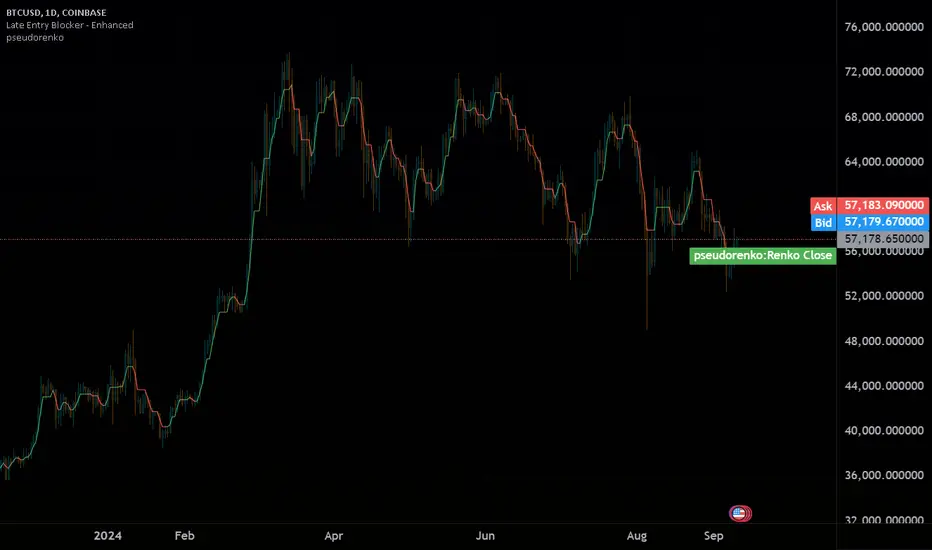

pseudorenko█ CALCULATE PSEUDO-RENKO VALUE

Calculates and returns the Pseudo-Renko Stabilized value (or close price) based on a given input value, along with the direction of the current Renko brick. This function adapts the traditional Renko brick size dynamically based on the volatility of the input value using a combination of SMA and EMA calculations. The calculated price represents the closing price of the most recent Pseudo-Renko brick, while the direction indicates the trend ( 1 for uptrend, -1 for downtrend).

Parameters:

* `val` :

* Type: ` float `

* Description: The input value upon which the Pseudo-Renko calculations are performed. You can use any price series or custom value as input.

* `sensitivity` :

* Type: ` float `

* Default Value: ` 1.0 `

* Description: Controls the sensitivity of the brick size to the volatility of the `val`. Higher values lead to larger bricks, resulting in a smoother Renko chart. Lower values produce smaller bricks, leading to a more reactive chart.

* Possible Values: Any positive float.

* `length` :

* Type: ` int `

* Default Value: ` 7 `

* Description: The length used for calculating the EMA and SMA in the dynamic brick size calculation. It influences how quickly the brick size adapts to changing volatility of the `val`.

* Possible Values: Any positive integer.

Return Values:

* `lastRenkoClose` :

* Type: ` float `

* Description: The closing price of the last completed Pseudo-Renko brick based on the `val`.

* `renkoDirection` :

* Type: ` int `

* Description: The direction of the current Pseudo-Renko brick based on the `val`:

* ` 1 `: Uptrend

* ` -1 `: Downtrend

* ` 0 `: No change (initially, or no brick change since the previous bar)

Example Usage:

//@version=5

indicator("Pseudo-Renko Stabilized (Val)", overlay=true)

// Get user inputs

sensitivityInput = input.float(0.1, "Sensitivity",0.01,step=0.01)

lengthInput = input.int(5, "Length",2)

// Example usage with the 'close' price as the input value

= pseudo_renko(math.avg(close,open), sensitivityInput, lengthInput)

// Plot the Renko close price

plot(renkoClose, "Renko Close", renkoDirection>0?color.aqua:color.orange,2)

// You can also use other values as input, such as:

// = pseudo_renko(high, sensitivityInput, lengthInput)

// = pseudo_renko(low, sensitivityInput, lengthInput)

This example demonstrates how to use the `pseudo_renko` function within an indicator. It takes user inputs for `sensitivity` and `length`, then calculates the Pseudo-Renko values using the average of the `close` and `open` prices as the `val`. The resulting `renkoClose` price is plotted on the chart, with a color change based on the `renkoDirection`. It also illustrates how you can use other values, like `high` and `low`, as input to the function.

Note: The Pseudo-Renko algorithm is based on adapting the Renko brick size dynamically based on the input `val`. This provides more flexibility compared to the normal, but is experimental. The `sensitivity` and `length` parameters, along with the choice of the `val`, offer further customization to tune the algorithm's behavior to your preference and trading style.

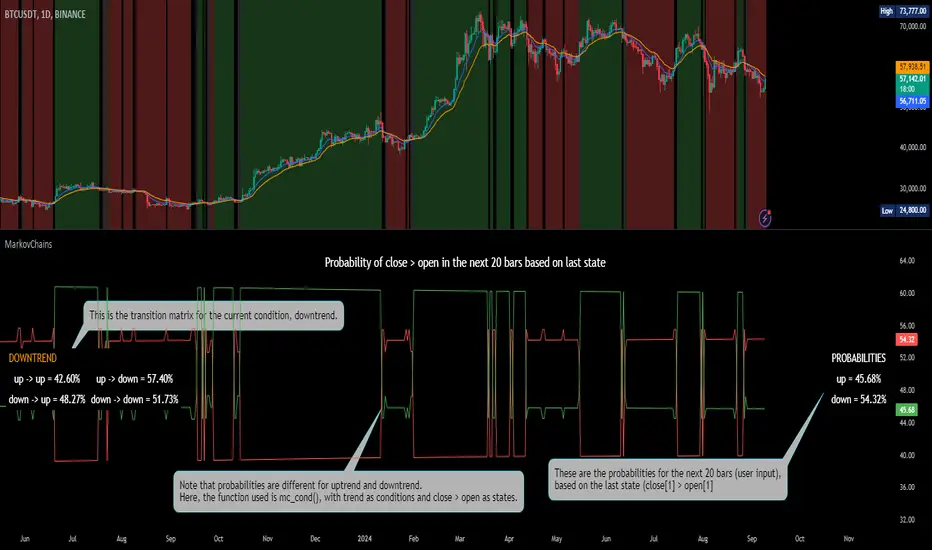

[ALGOA+] Markov Chains Library by @metacamaleoLibrary "MarkovChains"

Markov Chains library by @metacamaleo. Created in 09/08/2024.

This library provides tools to calculate and visualize Markov Chain-based transition matrices and probabilities. This library supports two primary algorithms: a rolling window Markov Chain and a conditional Markov Chain (which operates based on specified conditions). The key concepts used include Markov Chain states, transition matrices, and future state probabilities based on past market conditions or indicators.

Key functions:

- `mc_rw()`: Builds a transition matrix using a rolling window Markov Chain, calculating probabilities based on a fixed length of historical data.

- `mc_cond()`: Builds a conditional Markov Chain transition matrix, calculating probabilities based on the current market condition or indicator state.

Basically, you will just need to use the above functions on your script to default outputs and displays.

Exported UDTs include:

- s_map: An UDT variable used to store a map with dummy states, i.e., if possible states are bullish, bearish, and neutral, and current is bullish, it will be stored