Adaptive Weighted Regression Channel (AWRC)Short Description:

The Adaptive Weighted Regression Channel (AWRC) is an advanced technical analysis tool that plots a dynamic regression channel based on the recent price action. The centerline is a linear regression (trendline) fitted to the selected price source over a rolling window. The channel boundaries are placed above and below the regression line by a user-selected multiple of the weighted standard deviation.

What makes AWRC unique is its ability to optionally weight each bar’s importance in the regression using Volume, ATR (Average True Range), or Recency Decay, offering a channel that can adapt to market volatility, participation, or trend acceleration.

Parameter Explanations:

length: Number of bars for the regression window (how many recent candles are included). Higher values = smoother, less sensitive channel.

StdDev Multiplier (mult): Controls the channel width. 2.0 is classic; higher = wider channels, lower = tighter.

Enable Weighting?: Turn ON to activate weighting of each bar. If OFF, all bars are equally weighted (classic regression channel).

Weight Type: Select what to use for weights (only active if Enable Weighting is ON):

"Volume": Higher volume bars have more influence on the regression.

"ATR": Bars with higher volatility (as measured by ATR) have more influence.

"Decay": More recent bars are given more weight (controlled by Decay parameter).

Decay: If Weight Type is "Decay", this controls the rate of recency decay. (e.g. 0.98 = slow decay; 0.90 = fast decay; values close to 1 mean a longer memory.)

Source for the calculation (src): Selects which price is regressed. Default is hl2 (average of high and low); you can choose close, open, etc.

Recommended Parameters:

For general use: length = 34, mult = 2.0, Enable Weighting = OFF, src = hl2

For volume-aware channel: Enable Weighting = ON, Weight Type = "Volume"

For volatility sensitivity: Enable Weighting = ON, Weight Type = "ATR"

For extra focus on recent price: Enable Weighting = ON, Weight Type = "Decay", Decay = 0.95 or 0.98

For swing trading: length = 21–55, mult = 1.5–2.5

For intraday/scalping: length = 10–20, mult = 1.0–1.5

Usage Tips:

The regression line shows the "best fit" trend for the selected window.

The channel captures the typical range; price breaking outside the channel can signal strength, exhaustion, or breakout.

Volume and ATR weighting help the channel adapt to market participation or volatility spikes.

Decay weighting locks onto the most recent trend direction quickly.

Adjust parameters to fit your timeframe and market volatility.

Use AWRC to spot trending moves, reversals, or overextensions.

Try different weighting and channel settings to match your trading style!

Cari skrip untuk "scalping"

Mohammad - Auto TrendLinesMohammad - Auto TrendLines

Overview

An advanced automatic trendline detection system that identifies and draws both major and minor trendlines based on pivot highs and lows. This indicator uses sophisticated algorithms to detect market structure and automatically plot relevant trendlines, helping traders identify key support and resistance levels without manual chart analysis.

Key Features

Automatic Detection: Identifies pivot points and connects them to form trendlines without manual intervention

Multi-Level Analysis: Distinguishes between Major and Minor trendlines, both External and Internal

Smart Validation: Only draws trendlines that haven't been violated by price action

Comprehensive Alerts: 16 different alert conditions for breaks and reactions to trendlines

Fully Customizable: Complete control over colors, styles, widths, and display preferences for each trendline type

How It Works

The indicator uses a ZigZag algorithm with configurable pivot periods to identify significant highs and lows. It then connects these points to form trendlines, validating them against historical price action to ensure they remain relevant. The system categorizes trendlines into Major/Minor and External/Internal based on their significance in the market structure.

Use Cases

This indicator is particularly useful for:

Identifying trend continuations and potential reversals

Finding optimal entry and exit points based on trendline breaks

Setting stop-loss levels using trendline support/resistance

Confirming trade setups with multiple timeframe analysis

Automating trendline detection for systematic trading strategies

Settings/Parameters

Pivot Period: Controls the sensitivity of pivot detection (default: 5)

Display Options: Toggle visibility for each of the 8 trendline types

Style Customization: Adjust color, line style, width, and extension for each trendline

Alert Configuration: Enable/disable alerts for breaks and reactions to each trendline type

Delete Previous: Option to remove old trendlines when new ones are formed

How to Use

Add the indicator to your chart and adjust the Pivot Period based on your trading timeframe

Configure which trendline types you want to display (Major/Minor, External/Internal, Up/Down)

Set up alerts for the specific trendline interactions you want to monitor

Look for price reactions at trendlines for potential trade entries

Use trendline breaks as confirmation for trend changes

Signals

Break Alerts: Triggered when price closes beyond a trendline

React Alerts: Triggered when price touches but respects a trendline

Major External: Most significant trendlines based on major pivot points

Major Internal: Secondary major trendlines within the trend structure

Minor External: Short-term trendlines for intraday movements

Minor Internal: Smallest scale trendlines for precise entries

Trendline Types Explained

Up Trendlines: Connect ascending lows, act as support

Down Trendlines: Connect descending highs, act as resistance

External: Connect the outermost pivots

Internal: Connect pivots within the major structure

Best Timeframes

Works effectively on all timeframes:

Scalping: 1m, 5m, 15m charts

Day Trading: 15m, 1H, 4H charts

Swing Trading: 4H, Daily, Weekly charts

Position Trading: Daily, Weekly, Monthly charts

Important Notes

The indicator repaints trendlines as new pivots form - this is by design to maintain accuracy

Historical trendlines that have been broken are automatically extended to show past levels

Use multiple timeframe analysis for best results

Combine with other indicators for trade confirmation

Always use proper risk management

Alert Integration

This indicator uses the TradingFinder Alert Library for enhanced alert functionality, providing detailed notifications for all trendline interactions.

Version History

v6: Current version with full alert integration and enhanced trendline validation

Disclaimer: This indicator is for educational and informational purposes only. Past performance does not guarantee future results. Always conduct your own analysis and use proper risk management when trading.

Note: This is an overlay indicator that draws directly on your price chart. Ensure you have sufficient chart history loaded for optimal performance.

Superdupermegadeduper signals by BrenFX🚀 Superdupermegadeduper Signals by BrenFX

Overview

The Superdupermegadeduper Signals indicator is a comprehensive trading system that combines multiple advanced technical analysis concepts to identify high-probability trading opportunities. This indicator integrates supply/demand zone analysis, dynamic trendline detection, and multi-confirmation signal generation to provide traders with precise entry, stop-loss, and take-profit levels.

🎯 Key Features

Supply & Demand Zone Detection

Intelligent Zone Identification: Automatically detects high-probability supply and demand zones based on price action and touch frequency

Customizable Zone Strength: Set minimum touches required for zone validation (2-10 touches)

Visual Zone Display: Clear visual representation with customizable colors and transparency

Zone Extension: Projects zones forward for future reference

Dynamic Trendline Analysis

Multi-Touch Trendline Detection: Identifies significant support and resistance trendlines with configurable minimum touch requirements

Automatic Trendline Drawing: Draws and extends trendlines automatically with custom colors

Deviation Tolerance: Configurable deviation percentage for trendline validation

Breakout & Retest Signals: Detects trendline breakouts and subsequent pullback retests

Advanced Signal Generation

Dual Signal Types:

Zone Reversal Signals: Based on supply/demand zone interactions

Trendline Breakout Signals: Based on trendline breaks with pullback confirmation

Multi-Confirmation System:

Volume confirmation (optional)

RSI filter integration

Candlestick pattern confirmation

Pullback verification

Professional Trade Management

Multiple Stop Loss Methods:

ATR-based dynamic stops

Zone-based stops

Fixed point stops

Automatic Level Calculation: Entry, stop-loss, and take-profit levels calculated automatically

Real-Time Trade Table: Live display of current trade levels and parameters

Customizable Table Position: Place trade information anywhere on your chart

Alert System

Comprehensive Alerts: Get notified instantly when signals are generated

Detailed Alert Messages: Include entry price, stop-loss, and take-profit levels

Frequency Control: Once-per-bar alert frequency to avoid spam

📊 How It Works

Signal Logic

Zone Analysis: The indicator scans for areas where price has repeatedly found support or resistance

Trendline Detection: Identifies significant trend lines by connecting pivot points with multiple touches

Confirmation Process: Multiple filters ensure signal quality:

Price action confirmation (multiple bullish/bearish candles)

Volume above average (optional)

RSI oversold/overbought conditions (optional)

Entry Timing: Signals are generated when all confirmations align

Buy Signals Generated When:

Price reaches a demand zone with bullish reversal confirmation, OR

Price breaks above resistance trendline and retests successfully

Sell Signals Generated When:

Price reaches a supply zone with bearish reversal confirmation, OR

Price breaks below support trendline and retests successfully

⚙️ Configuration Options

Supply/Demand Settings

Zone Strength: Minimum touches required (2-10)

Lookback Period: Historical bars to analyze (10-100)

Zone Extension: Forward projection length (1-20 bars)

Trendline Settings

Lookback Period: Historical analysis range (20-200 bars)

Minimum Touches: Required pivot connections (2-5)

Deviation Tolerance: Allowable price variance (0.01-1.0%)

Signal Filters

Reversal Confirmation: Required confirmation candles (1-5)

Pullback Confirmation: Retest validation period (1-5)

Volume Filter: Above-average volume requirement

RSI Filter: Overbought/oversold confirmation

Trade Management

Stop Loss Methods: ATR, Zone-based, or Fixed points

ATR Multiplier: Risk adjustment (0.5-5.0x)

Take Profit: Fixed point target (1.0-50.0 points)

📈 Best Practices

Recommended Settings

For Scalping: Lower zone strength (2-3), shorter lookback periods

For Swing Trading: Higher zone strength (4-6), longer lookback periods

For Trend Following: Enable trendline signals, use ATR-based stops

Risk Management

Always use the provided stop-loss levels

Consider position sizing based on stop-loss distance

Monitor the trade table for real-time level updates

Use alerts to avoid missing opportunities

🎨 Visual Elements

Supply Zones: Red semi-transparent rectangles

Demand Zones: Green semi-transparent rectangles

Resistance Lines: Red trendlines

Support Lines: Green trendlines

Buy Signals: Green "BUY" labels below bars

Sell Signals: Red "SELL" labels above bars

Trade Table: Comprehensive trade information display

💡 Tips for Success

Combine with Market Structure: Use on clean trends and at key support/resistance levels

Multiple Timeframe Analysis: Confirm signals on higher timeframes

Volume Confirmation: Enable volume filter for higher quality signals

Risk Management: Never risk more than 1-2% per trade

Backtesting: Test settings on historical data before live trading

⚠️ Important Notes

This indicator works best in trending markets

Signals are more reliable when multiple confirmations align

Always consider fundamental analysis and market conditions

Past performance does not guarantee future results

Practice proper risk management at all times

🔧 Technical Specifications

Pine Script Version: 6

Overlay: Yes

Max Objects: 500 boxes, 500 lines

Performance: Optimized for real-time analysis

Compatibility: Works on all timeframes and instruments

Developed by BrenFX | Advanced Trading Signals for Professional Traders

Remember: Trading involves risk. This indicator is a tool to assist in analysis and should not be the sole basis for trading decisions. Always use proper risk management and consider your financial situation before trading.

🔁 A.X.I.S Fibonacci Engine V2 – Smart Projected Pathway🔁 A.X.I.S Fibonacci Engine V2 – Smart Projected Pathway indicator

The A.X.I.S Fibonacci Engine V2 is a next-generation Fibonacci projection tool designed for traders seeking advanced, adaptive levels that respond to true multi-timeframe market structure. Built from the ground up for active traders—scalpers, swing traders, and position players—it fuses traditional Fibonacci logic with dynamic price projection and smart anchor logic.

How It Works:

Multi-Timeframe Anchoring:

Anchors your Fibonacci levels to High Timeframe (HTF) pivots for powerful bias and “macro” market structure, while also utilizing Low Timeframe (LTF) swing detection for precise “micro” projection and pathway analysis.

Dynamic Pathway Projection:

Beyond static lines, this engine allows Fibonacci levels to be projected forward, following the price path between significant swings—giving you projected targets and active “pathways” instead of just fixed retracement bands.

Trend-Adaptive Logic:

Determines bullish/bearish bias based on where HTF price closes relative to a moving average (HTF EMA-20), meaning the plotted fibs automatically adjust to uptrends or downtrends. No need to guess direction.

Auto-Cleanup & Smart Management:

Old lines and labels are deleted automatically to keep your chart clean, and levels are recalculated with every new significant swing (“leg”)—no manual intervention needed.

Key Features:

Multi-Timeframe Input:

Choose both HTF (for “anchor” pivots) and LTF (for “projection” pivots) independently.

Fine-tune swing sensitivity for both anchors and pathway pivots.

Classic + Projected Mode:

Choose between standard horizontal Fibs or enable Dynamic Pathway Mode to project levels diagonally into future bars, creating “fib pathways.”

Color Customization:

Individualize bullish/bearish fib colors, line style (solid, dashed, dotted), thickness, label position, and transparency.

Special “golden zone” highlighting for the most critical levels (0.618/0.786).

Visual Anchors:

Optionally plot markers for HTF swing pivots for extra clarity.

Chart Cleanliness:

Script manages and deletes its own objects—no more chart clutter!

Real-Time Auto-Update:

All levels and pathways update in real time as market structure changes.

User-Friendly Labels:

Toggle on/off fib level labels, with position and background adjustments.

Practical Trading Applications:

Swing/Position Trading:

Use HTF pivots for macro context, then project LTF fibs into the future for potential reversal/extension targets.

Scalping:

Deploy on lower timeframes with micro pivots for intraday levels and short-term projected moves.

Dynamic Take-Profit & Entry Zones:

Identify evolving TP and re-entry zones as price carves out new swings, even in choppy or trending conditions.

Trend Confirmation:

Let the engine determine trend direction, so your fibs are always aligned with prevailing momentum.

How to Use:

Add to Chart:

Apply the indicator to any chart or timeframe.

Set Your Anchors:

Pick the HTF (anchor) and LTF (projection) timeframes.

Adjust swing sensitivity (lookback) as needed.

Enable/Disable Dynamic Pathway:

For regular fibs, leave off.

For projected “pathways,” turn it ON—lines will project forward along the likely path of the next move.

Adjust Colors, Labels, and Styles:

Fine-tune everything for clarity and your personal style.

Watch for Changes:

As new pivots form, the script will update levels in real time, keeping your roadmap fresh.

(Optional) Show Macro Swings:

Toggle on/off to plot markers for the most recent HTF pivots.

Who Is It For?

Day traders, scalpers, and swing traders wanting true projected price targets—not just static fibs.

Traders tired of redrawing fibs after every new swing.

Anyone who wants a clean, dynamic, and truly adaptive fib tool that blends macro and micro market structure into one engine.

What Makes It Different?

True multi-timeframe awareness:

Adapts to both macro (HTF) and micro (LTF) structure.

Automatic trend recognition:

Fibs align with price action—no manual flipping.

Projected, not just static:

See where fib levels could land, not just where they were.

Cleanest chart management:

Deletes its own lines and labels on every update—no mess, ever.

Note:

This tool is for educational and informational purposes only. Not financial advice. Always use proper risk management!

Any issues or feature requests? Drop a comment below or reach out!

Happy trading and welcome to the A.X.I.S revolution.

— I5X-Albatross

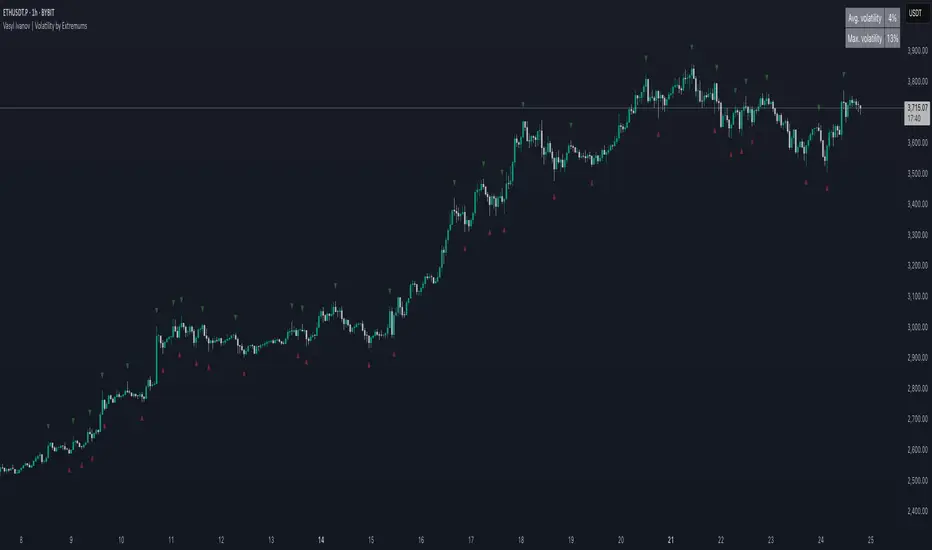

Vasyl Ivanov | Volatility by Extremums"Volatility by Extremums" is an original technical indicator designed to measure market volatility based on the analysis of price extreme points. Unlike traditional volatility indicators that use standard statistical methods, this indicator calculates volatility as a percentage price change between local maximums and minimums, providing a more accurate understanding of actual price fluctuations in the market.

Unique Methodology

The indicator uses an innovative approach to volatility calculation:

Extremum Detection: The algorithm automatically identifies local maximums and minimums based on configurable parameters, including lookback period and minimum distance between extremums, measured in ATR (Average True Range) units.

Relative Volatility Calculation: For each pair of adjacent extremums, volatility is calculated using the formula: (|Max - Min| / Max) × 100%, where volatility is expressed as a percentage of the maximum value in the pair.

Result Aggregation: The indicator computes two key metrics:

Average volatility - arithmetic mean of all calculated volatility values

Maximum volatility - highest volatility value between extremums during the analyzed period

Technical Parameters

Main Settings:

Lookback (1000): Number of bars for historical analysis

Extremums Bars Lookback (10): Period for extremum search

Extremums Minimal Distance (2 ATR): Minimum distance between extremums for noise filtering

ATR Period (30): Average True Range calculation period

ATR Average Period (20): ATR averaging period

Visualization:

Color-coded extremums: Bullish extremums marked in green, bearish in red

Information table: Displays current average and maximum volatility values in the top-right corner of the chart

Dynamic markers: Automatic placement of ▼ and ▲ symbols on corresponding extremums

Practical Applications

Market Condition Analysis

The indicator helps traders identify:

High volatility periods: When average volatility exceeds historical norms, indicating potential for large price movements

Consolidation phases: Low volatility values signal periods of energy accumulation before potential breakouts

Extreme movements: Maximum volatility shows the largest price swings, which may indicate important market events

Risk Management

Volatility data enables:

Position size adaptation based on current market volatility

Dynamic stop-loss setting corresponding to market activity levels

Optimal entry point selection during periods of reduced volatility

Trading Strategies

The indicator is effective for:

Breakout strategies: Low volatility often precedes strong directional movements

Counter-trend trading: Extremely high volatility values may signal potential reversals

Scalping: Understanding current volatility level helps choose appropriate instruments and timeframes

Advantages Over Traditional Indicators

Unlike standard volatility measures such as standard deviation or ATR, this indicator:

Focuses on actual extremums: Analyzes real price reversal points rather than abstract statistical indicators

Adapts to market conditions: Uses ATR to determine significant extremums, filtering market noise

Provides contextual information: Shows not only current volatility but also historical maximum, helping assess the relative significance of current movements

Usage Recommendations

Parameter Optimization:

For intraday trading: Reduce Lookback period to 200-500 bars

For position trading: Increase minimum distance between extremums to 3-4 ATR

For high-volatility assets: Set ATR period to shorter periods (14-21)

Combining with Other Indicators:

Best results are achieved when used together with:

Trend indicators to determine overall market direction

Oscillators for precise entry and exit timing

Volume indicators to confirm movement strength

Technical Limitations

Users should consider:

The indicator is based on historical data and does not guarantee future results

Requires sufficient historical data for correct operation (minimum 100 bars)

Most effective on liquid markets with clearly defined extremums

"Volatility by Extremums" represents an innovative approach to market volatility analysis, providing traders with a unique tool for understanding price dynamics and making informed trading decisions based on actual market extremums.

NEO CLOUD + Kinetic Compass CombinedThis is a comprehensive technical analysis indicator combining three powerful trading systems:

📊 NEO CLOUD System:

- Trend identification system based on dual EMA range filters

- Provides dynamic cloud fill for intuitive trend direction and strength visualization

- Supports Fast/Normal/Slow trend length settings

- Fully customizable colors including cloud fill and signal arrows

🧭 KINETIC COMPASS System:

- Modified trend indicator based on EMA100 for high-precision trend tracking

- Dual-layer exit signal system to optimize exit timing

- Integrated EMA50/100/200 multi-timeframe confirmation

- Gradient fill effects for clear support/resistance visualization

- Independent control over buy/sell signals and exit signals display

📈 DUAL SUPERTREND System:

- Two independent Supertrend indicators with separate parameters

- Selective display control - show one, both, or neither

- Dynamic support/resistance lines that adapt to market volatility

- Adjustable transparency fill areas

🚀 Combined Features:

- MEGA Alerts: Super alerts triggered when multiple systems align

- Independent Switches: Each system can be enabled/disabled separately

- Color Customization: Full personalization of all visual elements

- Candle Coloring: Support for NEO or Kinetic candle coloring schemes

- Signal Filtering: Choose to show or hide various types of trading signals

💡 Usage Recommendations:

- Beginners: Start with single system, then combine after familiarization

- Trend Trading: Focus on NEO CLOUD direction and Kinetic trend lines

- Scalping: Use exit signals and Supertrend for precise entry/exit points

- Signal Confirmation: Wait for multiple system alignment for higher success rate

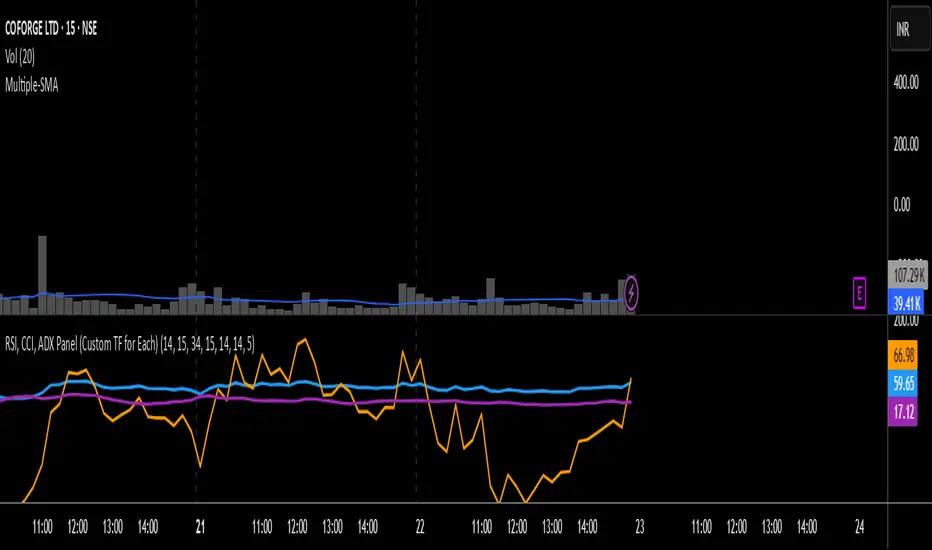

RSI, CCI, ADX Panel (Custom TF for Each)RSI, CCI, and ADX Combined – Multi-Timeframe, Fully Customizable Panel Indicator for TradingView

Overview

This Pine Script indicator integrates the Relative Strength Index (RSI), Commodity Channel Index (CCI), and Average Directional Index (ADX) into a single, clean panel for effortless technical analysis. Each indicator operates independently, with customizable length, smoothing, and time frame for maximum flexibility. Traders can now monitor momentum, trend strength, and overbought/oversold conditions across different time frames—all in one place.

Key Features

Independent Controls: Set length, smoothing (ADX), and time frame individually for each indicator via the settings panel.

Multi-Timeframe Support: Each oscillator (RSI, CCI, ADX) can be calculated on its own time frame, enabling nuanced inter-timeframe analysis.

Customizable Visualization: Adjust line color and thickness for each indicator to match your chart style.

Clean, Non-Overlay Display: All three indicators are plotted in a dedicated panel beneath the price chart, reducing clutter.

Reference Levels: Includes standard reference lines for oversold/overbought (RSI, CCI) and trend threshold (ADX) for quick visual cues.

Usage Ideas

Swing Trading: Compare short- and long-term momentum using different time frames for RSI, CCI, and ADX.

Trend Confirmation: Use ADX to filter RSI and CCI signals—only trade overbought/oversold conditions during strong trends.

Divergence Hunting: Spot divergences between time frames for early reversal signals.

Scalping: Set RSI and CCI to lower time frames for entry, while monitoring higher timeframe ADX for trend context.

How to Install

Paste the script into the Pine Editor on TradingView.

Add to chart. Adjust settings as desired.

Save as a template for quick reuse on any chart—all your custom settings will be preserved.

Customization

Edit lengths and time frames in the indicator’s settings dialog.

Toggle reference lines on/off as needed.

Fine-tune line appearance (color, thickness) for clarity.

Note:

This indicator does not provide automated buy/sell signals. It is a customizable analytical tool for manual or semi-automated trading. Use in combination with other technical or fundamental analysis for best results.

Combine Momentum, Trend, and Volatility—Seamlessly and Visually—With One Indicator.

TREV Candles - Range-Based Trend ReversalTREV Candles - Range-Based Trend Reversal Chart Implementation

What is a Trend Reversal (TREV) Chart?

A Trend Reversal chart, also known as a Point & Figure chart variation, is a unique charting method that focuses on price movement thresholds rather than time intervals. Unlike traditional candlestick charts where each candle represents a fixed time period, TREV candles form only when price moves by predefined amounts in ticks.

TREV charts eliminate time-based noise and focus purely on significant price movements, making them ideal for identifying genuine trend changes and continuation patterns.

How TREV Candles Work

This indicator implements true TREV logic with two critical thresholds:

Trend Size: The number of ticks price must move in the current direction to form a trend continuation candle

Reversal Size: The number of ticks price must move against the current direction to form a reversal candle and change the overall trend direction

Key TREV Rules Enforced:

Direction Changes Only Through Reversals: You cannot go from bullish trend directly to bearish trend - a reversal candle must occur first

Threshold-Based Formation: Candles form only when price thresholds are breached, not on time

Logical Wick Placement: Wicks only appear on the "open" side of candles where price temporarily moved against the formation direction

Multiple Candles Per Bar: When price moves significantly, several TREV candles can form within a single time-based bar

Four Distinct Candle Types

Bullish Trend (Green): Continues upward movement when trend threshold is hit

Bearish Trend (Red): Continues downward movement when trend threshold is hit

Bullish Reversal (Blue): Changes from bearish to bullish direction when reversal threshold is breached

Bearish Reversal (Orange): Changes from bullish to bearish direction when reversal threshold is breached

Practical Trading Applications

Trend Identification: Clear visual representation of when trends are continuing vs. reversing

Noise Reduction: Filters out insignificant price movements that don't meet threshold requirements

Support/Resistance: TREV levels often act as significant support and resistance zones

Breakout Confirmation: When price forms multiple trend candles in succession, it confirms strong directional movement

Reversal Signals: Reversal candles provide early warning of potential trend changes

Technical Implementation Features

Intelligent Price Path Processing: Analyzes the assumed price path within each bar (Low→High→Close for bullish bars, High→Low→Close for bearish bars)

Automatic Tick Size Detection: Works with any instrument by automatically detecting the correct tick size

Manual Override Option: Allows manual tick size specification for custom analysis

Impossible Scenario Prevention: Built-in logic prevents impossible wick configurations and direction changes

PineScript Optimization: Efficient state management and drawing limits handling for smooth performance

Comprehensive Styling Options

Each of the four candle types offers complete visual customization:

Body Colors: Independent color settings for each candle type's body

Border Colors: Separate border color customization

Border Styles: Choose from solid, dashed, or dotted borders

Wick Colors: Individual wick color settings for each candle type

Default Color Scheme:

🟢 Bullish Trend: Green body and wicks

🔵 Bullish Reversal: Blue body and wicks

🔴 Bearish Trend: Red body and wicks

🟠 Bearish Reversal: Orange body and wicks

Configuration Guidelines

Trend Size: Larger values create fewer, more significant trend candles. Smaller values increase sensitivity

Reversal Size: Should typically be smaller than trend size. Controls how easily the trend direction can change

Tick Size: Use "auto" for most instruments. Manual override useful for custom point values or backtesting

Ideal Use Cases

Swing Trading: Identify major trend changes and continuation patterns

Scalping: Use smaller thresholds to catch quick reversals and momentum shifts

Position Trading: Use larger thresholds to filter noise and focus on major trend moves

Multi-Timeframe Analysis: Compare TREV patterns across different threshold settings

Support/Resistance Trading: TREV close levels often become significant price zones

Why This Implementation is Superior

True TREV Logic: Enforces proper trend reversal rules that many implementations ignore

No Impossible Scenarios: Prevents wicks on both sides of candles and impossible direction changes

Professional Visualization: Clean, customizable appearance suitable for serious analysis

Performance Optimized: Handles large datasets without lag or drawing limit issues

Educational Value: Helps traders understand the difference between time-based and threshold-based charting

Perfect for traders who want to see beyond time-based noise and focus on what price is actually doing - moving in significant, measurable amounts that matter for trading decisions.

Mohammad - OBs, BOS, S/R, Elliott Waves & Trend LinesProfessional Trading Indicator System - Technical Analysis Suite

Overview

Advanced technical analysis system integrating ICT/SMC methodologies with classical analysis tools. Features seven analytical components for comprehensive market structure analysis.

Components

1. Order Blocks (ICT/SMC)

Identifies institutional accumulation/distribution zones acting as future support/resistance.

Detection: Automatic identification based on price rejection patterns

Management: Dynamic updates and removal of invalidated blocks

Configuration: Sensitivity levels (High/Medium/Low), ATR-based parameters

Visual: Green support, red resistance with transparency

2. Break of Structure (BOS)

Detects significant structural breaks indicating trend changes.

Method: 5-bar swing point formation

Display: White horizontal lines with labels

Range: 50-bar maximum lookback

3. Support & Resistance

Classical horizontal levels from significant price pivots.

Analysis: 300-bar historical scan

Filter: 10-point duplicate tolerance

Display: Maximum 15 levels within 5% of current price

4. Fair Value Gaps (FVG)

Price inefficiencies that often get filled on return.

Types: Bullish gaps (up) and bearish gaps (down)

Size: Minimum 0.1 ATR or 5 points

Management: Auto-removal when filled

5. Elliott Wave Analysis

Advanced pattern recognition for impulse and corrective waves.

Patterns: 5-wave impulse (1-2-3-4-5), 3-wave corrective (A-B-C)

Adaptive: Auto-adjusts to timeframe (3-10 depth range)

Display: Small dots with large numbers, starts from hidden point 0

6. 45-Degree Momentum Lines

Revolutionary projection system based on consecutive candle sequences.

Bearish Lines (Red):

Trigger: 5+ consecutive red candles

Start: HIGH of first red candle

Labels: B1-B5

Bullish Lines (Green):

Trigger: 5+ consecutive green candles

Start: LOW of first green candle

Labels: T1-T5

Specifications:

Angle: 45° using ATR * 0.15

Extension: 30 bars forward

Display: 5 most recent patterns

7. Classical Trend Lines

Multi-touch diagonal support/resistance detection.

Validation: Minimum touch requirements

Tolerance: ATR-based touch detection

Display: Blue lines with optional labels

Configuration Summary

Global Settings:

Show/hide each component individually

Customizable colors and line widths

Label size options

Performance:

50-bar periodic cleanup

Maximum object limits (500 each)

Conditional processing on bar close

Trading Applications

Scalping: Order Blocks + FVGs + 45° Lines

Day Trading: All components with BOS emphasis

Swing Trading: Elliott Waves + Trend Lines

Position Trading: Major levels + Elliott Waves

Key Strategies:

Use 45° line bounces for entries

Combine Order Blocks with 45° lines for confluence

Confirm BOS breaks with 45° line violations

Place stops beyond projection lines

Technical Requirements

Platform: TradingView Pine Script v5

Minimum: 300 historical bars

Optimal: 15m-4H timeframes

Performance: Moderate CPU usage

Color Scheme

Green: Bullish/Support (#26a69a)

Red: Bearish/Resistance (#ef5350)

White: BOS/S&R lines

Blue: Elliott Waves/Trend Lines

Customizable: 45° projection lines

Risk Disclaimer

Educational tool only. Not financial advice. Combine with risk management and personal analysis. Past performance doesn't guarantee future results. Trading involves substantial risk.

EMA Curl Strength+EMA Curl Strength+

Description:

This indicator provides a statistically normalized view of EMA slope momentum using Z-score transformation. By evaluating the rate of change of an EMA and comparing it against its historical behavior, the script highlights momentum shifts in a dynamic, adaptive way.

⸻

How It Works:

• Calculates the slope (percentage change) of a chosen EMA.

• Normalizes the slope using Z-score over a custom lookback period.

• Smooths the resulting signal and computes two signal lines for comparison.

• Assigns dynamic colors based on user-defined Z-score thresholds for mild, moderate, and strong momentum in both directions.

⸻

Visual Features:

• Gradient fill between the Z Curl Line and Signal 1 to highlight slope acceleration.

• Histogram showing the difference between the Z Curl Line and its signal.

• Optional signal crossover shapes between configurable pairs (e.g., Z Curl vs. Signal).

• Background highlights when the Z Curl Line exceeds ±2, indicating strong trending behavior.

⸻

Customization:

• Adjustable EMA length, smoothing lengths, signal lengths, histogram smoothing, and Z-score lookback.

• Separate color controls for:

• Z-score strength bands (mild/moderate/strong up/down)

• Histogram bars

• Signal lines

• Background highlight zones

• Crossover shapes

⸻

Use Cases:

• Momentum Confirmation: Confirm strength when Z Curl exceeds ±2 with matching background highlights.

• Trend Entry Timing: Look for trades when Z Curl crosses above or below the 0-line.

• Scalping: Capture quick directional moves when momentum accelerates.

• Trend Following: Use strong Z Curl values to confirm trade direction and filter sideways action.

• Divergence Detection: Spot divergences between price and Z Curl movement to anticipate reversals.

Pivot Channel LevelsPivot Channel Levels

Indicator Description

“Pivot Channel Levels” is an advanced technical analysis tool that identifies key price pivots (highs and lows) and creates dynamic support and resistance levels based on the wicks of candles at these points (or bodies if wicks are minimal). The indicator analyzes the volume at the time of a pivot’s formation, displaying its value and percentage change relative to the volume’s simple moving average (SMA).

It does not generate buy/sell signals but provides a clear visualization of market structure, helping traders identify potential price reaction zones and assess the strength of market movements.

Why Are Wicks Important?

Candle wicks at price pivots indicate significant market reactions in key areas. Depending on the context, they may signal rejection, testing, or absorption of a support or resistance level. Long wicks often appear where large players are active, and the marked zones are frequently retested. The indicator allows for quick identification and observation of their impact on future price action.

Why Use It?

- Precise Support and Resistance Levels: The indicator draws price channels based on candle wicks at pivots (or bodies if wicks are absent), enabling better identification of zones where price may react.

- Volume Analysis: It shows how the volume at a pivot differs from the average, indicating potential activity by large players or key market moments.

- Visual Clarity: Colored lines, channel fills, and clear labels facilitate quick chart analysis, even on short timeframes.

- Flexibility: Adjustable pivot length, volume average, and label colors allow customization to various trading strategies.

How It Works

- Pivot Detection: Automatically identifies local highs and lows based on the “Pivot Length” parameter (default: 20 candles). This means a pivot appears on the chart with a 20-candle delay. Reducing this value allows faster pivot detection (after fewer candles), increasing their number but potentially generating more noise.

- Channel Creation: Draws support and resistance levels based on the wicks of candles at pivot points (or bodies if wicks are minimal) with a delay to confirm zones. A pivot channel is drawn until the next pivot is identified, but if not previously broken, it remains valid as active support or resistance.

- Volume Analysis: Displays the volume at the pivot’s formation and its percentage change relative to the volume’s SMA.

- Visualization: Pivot and channel levels are shown as lines with fills, and labels display volume and its deviation from the average.

Trading Applications

- Swing Trading: Use pivot levels and channels to identify price reversal points or consolidation zones.

- Scalping: Monitor price reactions to channels on short timeframes, especially with high volume.

- Faster Pivot Identification: Switch to a lower timeframe (e.g., from H1 to M15) to identify pivots more quickly, allowing earlier reactions to price changes.

- Market Context Analysis: High volume at pivots may indicate significant levels likely to be retested.

- Combining with Other Tools: The indicator pairs well with Fibonacci retracement, supply/demand zones, or oscillators like RSI.

Settings and Customization

- Pivot Length: Determines how many candles back and forward are analyzed to detect pivots (default: 20). A smaller value increases sensitivity, a larger one enhances stability.

- Volume Average: Length of the SMA for volume (default: 20). Adjust to better reflect market characteristics.

- Label Colors: Choose colors for bullish and bearish pivot labels to match your chart style.

Usage Examples

- Identifying Key Zones: If the price approaches a pivot level with high volume (e.g., +50% relative to SMA), it may signal strong support or resistance.

- Breakout Confirmation: A channel breakout with high volume can indicate trend continuation.

- Price Reaction Analysis: Long wicks at pivots with high volume may signal level rejection by large players.

Notes for Users

- The indicator performs best on highly liquid markets (e.g., Forex, indices, cryptocurrencies).

- On short timeframes (e.g., M1, M5), it may generate more noise—adjust “Pivot Length” to suit your needs.

- Consider combining with other indicators to confirm signals derived from pivot and volume analysis.

VSA-Stopping VolumeVSA Stopping Volume Indicator

Stopping Volume occurs when candles show decreasing body sizes (narrow spreads) while volume steadily increases.

Example chart:

As you see:

3 consecutive candles in same direction (all green OR all red)

Body sizes (spreads) decreasing progressively: Candle 1 > Candle 2 > Candle 3

Volume increasing progressively: Volume 1 < Volume 2 < Volume 3

This pattern indicates price absorption - increased buying/selling pressure but declining price movement, often signaling exhaustion and potential reversal.

Indicator Features

This indicator detects Stopping Volume candlestick clusters with two signal types:

🔹 BUY/SELL Signals: Generated when pattern occurs at support/resistance zones

🔹 Directional Alerts (▲-green, ▼-red): Generated when pattern occurs outside key levels

Trading Guidelines:

⚠️ Auto-drawn S/R zones are reference only - manual level plotting recommended for accuracy

📊 Best for scalping: M5, M10, M15 timeframes

🛡️ Stop Loss: Place beyond the S/R zone you're trading

🎯 Take Profit: Based on your risk management

Key Concept: Volume expansion + price contraction = potential reversal, especially at SnR levels.

Perfect for scalpers looking to catch reversals at critical zones!

52SIGNAL RECIPE Directional Consistency Index═══ 52SIGNAL RECIPE Directional Consistency Index (DCI) ═══

◆ Overview

52SIGNAL Directional Consistency Index (DCI) is a technical indicator that measures the directional consistency of market movements. This indicator focuses on the consistency of direction rather than the magnitude of price changes, analyzing the strength of market trends and providing more reliable trend analysis by filtering out noise to reflect only meaningful price movements.

─────────────────────────────────────

◆ Key Features

• Direction-Focused Analysis: Concentrates solely on directional consistency rather than magnitude of price changes

• Noise Filtering: Ignores insignificant price movements through minimum percentage change settings

• Trend Exhaustion Detection: Identifies potential trend reversals as values approach ±0.5 levels

• Intuitive Visualization: Instant recognition of trend direction through color changes based on rising/falling zones

• Multi-Market Application: Adaptable to various financial markets including stocks, cryptocurrencies, and forex

─────────────────────────────────────

◆ Technical Foundation

■ Directional Calculation

• Basic Principle: Counts only the up/down movement of each candle to measure directional consistency

• Calculation Method: Determines direction based on percentage change between current close and previous close

• Direction Values: Simplified into Rising (+1), Falling (-1), or Insignificant Change (0)

• Averaging: DCI calculated as the moving average of direction values over the specified period

■ Noise Filtering Mechanism

• Minimum Percentage Change: The minimum percent change required to consider a price movement significant

• Filtering Effect: Movements smaller than the minimum change are excluded from direction calculation (treated as 0)

• Enhanced Reliability: Adjustable filtering strength for optimization across different market environments

─────────────────────────────────────

◆ Practical Applications

■ Trend Identification & Reversal Prediction

• Early Uptrend Detection:

▶ When DCI enters the 0 to +0.3 range

▶ When recent directional consistency begins to consistently rise

• Early Downtrend Detection:

▶ When DCI enters the 0 to -0.3 range

▶ When recent directional consistency begins to consistently fall

• Trend Reversal Signals:

▶ When DCI approaches +0.5 (uptrend exhaustion, potential downward reversal)

▶ When DCI approaches -0.5 (downtrend exhaustion, potential upward reversal)

■ Trading Strategy Implementation

• Trend Following Strategies:

▶ Consider buying when DCI crosses above the 0 line

▶ Consider selling when DCI crosses below the 0 line

• Reversal Trading:

▶ Consider taking profits or short positions when DCI approaches +0.5

▶ Consider long positions when DCI approaches -0.5

• Divergence Confirmation:

▶ Weakening uptrend signal when price rises but DCI weakens

▶ Weakening downtrend signal when price falls but DCI strengthens

─────────────────────────────────────

◆ Advanced Setting Options

■ Period (Length) Settings

• Short-term Analysis: 5-10 days (faster signals, more sensitive responses)

• Medium-term Analysis: 10-20 days (balanced signals, recommended default)

• Long-term Analysis: 20-30 days (slower signals, long-term trend identification)

■ Minimum Percentage Change Settings

• Low Volatility Markets: 0.05-0.2% (suitable for forex markets)

• Medium Volatility Markets: 0.3-0.5% (suitable for stock markets)

• High Volatility Markets: 0.5-1.0% (suitable for cryptocurrency markets)

■ Settings by Trading Style

• Scalping: Lower period (5-10), lower minimum change (0.05-0.1%)

• Day Trading: Medium period (10-15), medium minimum change (0.2-0.3%)

• Swing Trading: Higher period (15-25), higher minimum change (0.3-0.5%)

─────────────────────────────────────

◆ Synergy with Other Indicators

• Moving Averages: Strengthen signals by confirming moving average crossovers when DCI crosses the 0 line

• RSI: Combine DCI trend direction with RSI overbought/oversold levels to confirm entry points

• MACD: Enhance reliability by pairing DCI directional signals with MACD momentum confirmation

• Bollinger Bands: Analyze volatility by checking Bollinger Band expansion/contraction when DCI approaches ±0.5

─────────────────────────────────────

◆ Conclusion

52SIGNAL Directional Consistency Index (DCI) is a powerful tool for objectively measuring market directionality and visualizing trend strength. The noise filtering through minimum percentage change settings can be adjusted to match your trading style and market characteristics for optimal results. Its ability to identify early trend stages and detect overextended zones provides traders with important entry and exit points. When used in conjunction with other technical indicators, it can significantly enhance the reliability of trading decisions.

─────────────────────────────────────

※ Disclaimer: Past performance does not guarantee future results. Always use appropriate risk management strategies.

═══ 52SIGNAL 방향성 일관성 지수 (DCI) ═══

◆ 개요

52SIGNAL 방향성 일관성 지수(DCI)는 시장의 방향성 일관성을 측정하는 기술적 지표입니다. 이 지표는 가격 변화의 크기가 아닌 방향의 일관성에 중점을 두어 시장의 추세 강도를 분석하고, 노이즈 필터링 기능을 통해 의미 있는 가격 변동만을 반영하여 더 신뢰할 수 있는 추세 분석을 제공합니다.

─────────────────────────────────────

◆ 주요 특징

• 방향성 중심 분석: 가격 변화의 크기가 아닌 방향성에만 집중하여 추세의 일관성 측정

• 노이즈 필터링: 최소 변화율 설정을 통해 의미 없는 작은 가격 변동을 무시

• 추세 과열 감지: ±0.5 수준에 접근할 때 추세 전환 가능성 식별

• 직관적인 시각화: 상승/하락 구간에 따른 색상 변화로 추세 방향 즉각 인식

• 다양한 시장 적용: 주식, 암호화폐, 외환 등 다양한 금융 시장에 적용 가능

─────────────────────────────────────

◆ 기술적 기반

■ 방향성 계산

• 기본 원리: 각 캔들의 상승/하락 여부만 카운트하여 방향의 일관성 측정

• 계산 방법: 현재 종가와 이전 종가의 퍼센트 변화를 기준으로 방향 판단

• 방향 값: 상승(+1), 하락(-1), 의미 없는 변화(0)로 단순화

• 평균화: 설정된 기간 동안의 방향 값의 이동평균으로 DCI 산출

■ 노이즈 필터링 메커니즘

• 최소 변화율: 의미 있는 가격 변동으로 인정할 최소 퍼센트 변화

• 필터링 효과: 최소 변화율보다 작은 변동은 방향 계산에서 제외(0으로 처리)

• 신뢰도 향상: 필터링 강도 조절을 통해 다양한 시장 환경에 최적화 가능

─────────────────────────────────────

◆ 실용적 응용

■ 추세 식별 및 전환점 예측

• 상승 추세 초입:

▶ DCI가 0에서 +0.3 사이로 진입할 때

▶ 최근 방향성이 일관되게 상승하기 시작할 때

• 하락 추세 초입:

▶ DCI가 0에서 -0.3 사이로 진입할 때

▶ 최근 방향성이 일관되게 하락하기 시작할 때

• 추세 전환 신호:

▶ DCI가 +0.5에 가까워질 때 (상승 추세 과열, 하락 전환 가능성)

▶ DCI가 -0.5에 가까워질 때 (하락 추세 과열, 상승 전환 가능성)

■ 트레이딩 전략 적용

• 추세 추종 전략:

▶ DCI가 0선을 위로 돌파할 때 매수 고려

▶ DCI가 0선을 아래로 돌파할 때 매도 고려

• 반전 트레이딩:

▶ DCI가 +0.5에 근접할 때 이익실현 또는 매도 포지션 고려

▶ DCI가 -0.5에 근접할 때 매수 포지션 고려

• 다이버전스 확인:

▶ 가격은 상승하나 DCI가 약화될 때 상승 추세 약화 신호

▶ 가격은 하락하나 DCI가 강화될 때 하락 추세 약화 신호

─────────────────────────────────────

◆ 고급 설정 옵션

■ 기간(Length) 설정

• 단기 분석: 5-10일 (빠른 신호, 민감한 반응)

• 중기 분석: 10-20일 (균형 잡힌 신호, 기본 권장)

• 장기 분석: 20-30일 (느린 신호, 장기 추세 식별)

■ 최소 변화율(Minimum % Change) 설정

• 저변동성 시장: 0.05-0.2% (외환 시장에 적합)

• 중변동성 시장: 0.3-0.5% (주식 시장에 적합)

• 고변동성 시장: 0.5-1.0% (암호화폐 시장에 적합)

■ 트레이딩 스타일별 설정

• 스캘핑: 낮은 기간(5-10), 낮은 최소 변화율(0.05-0.1%)

• 데이 트레이딩: 중간 기간(10-15), 중간 최소 변화율(0.2-0.3%)

• 스윙 트레이딩: 높은 기간(15-25), 높은 최소 변화율(0.3-0.5%)

─────────────────────────────────────

◆ 다른 지표와의 시너지

• 이동평균선: DCI가 0선을 돌파할 때 이동평균 교차 확인으로 신호 강화

• RSI: DCI의 추세 방향과 RSI의 과매수/과매도 수준을 결합하여 진입점 확인

• MACD: DCI의 방향성 신호와 MACD의 모멘텀 확인을 결합하여 신뢰도 향상

• 볼린저 밴드: DCI가 ±0.5에 근접할 때 볼린저 밴드 확장/수축 확인으로 변동성 분석

─────────────────────────────────────

◆ 결론

52SIGNAL 방향성 일관성 지수(DCI)는 시장의 방향성을 객관적으로 측정하고 추세의 강도를 시각화하는 강력한 도구입니다. 최소 변화율 설정을 통한 노이즈 필터링은 각자의 트레이딩 성향과 시장 특성에 맞게 조정할 수 있어 최적의 효과를 누릴 수 있습니다. 추세의 초기 단계를 식별하고 과열 구간을 감지하는 능력은 트레이더에게 중요한 진입 및 퇴출 포인트를 제공합니다. 다른 기술적 지표와 함께 사용하면 트레이딩 결정의 신뢰도를 크게 향상시킬 수 있습니다.

─────────────────────────────────────

※ 면책 조항: 과거 성과가 미래 결과를 보장하지 않습니다. 항상 적절한 리스크 관리 전략을 사용하세요.

TIME-SPLT ACADEMY INDICATOR# TIME-SPLT ACADEMY CISD + FVG + TSM FRACTALS - Comprehensive Market Structure Analysis Tool

## Overview

This indicator combines three essential market structure analysis components into a unified trading tool: Change in State Direction (CISD), Fair Value Gaps (FVG), and TSM Fractals. This integration provides traders with a complete framework for identifying market structure breaks, price imbalances, and key pivot levels on any timeframe.

## Component 1: CISD (Change in State Direction)

**What it is:** CISD identifies significant breaks in market structure by tracking when price decisively breaks above previous swing highs (bullish CISD) or below previous swing lows (bearish CISD). This concept is fundamental to understanding trend changes and continuation patterns.

**How it works:**

- Monitors swing highs and lows using customizable pivot periods

- Tracks when price closes above a previous swing high (bullish structure break)

- Tracks when price closes below a previous swing low (bearish structure break)

- Draws horizontal lines from the pivot point to the break point with "CISD" labels

- Works on multiple timeframes simultaneously

**Trading Applications:**

- Identifies trend changes and continuation signals

- Provides entry signals on structure breaks

- Helps determine market bias and direction

## Component 2: FVG (Fair Value Gaps)

**What it is:** Fair Value Gaps are price imbalances that occur when there's a gap between the high of one candle and the low of another candle two periods later, with the middle candle not filling this gap. These represent areas where price moved inefficiently and often return to "fill" the gap.

**How it works:**

- Analyzes 3-candle patterns to identify gaps

- Bearish FVG: Gap between low and high where price dropped leaving unfilled space above

- Bullish FVG: Gap between high and low where price rose leaving unfilled space below

- Tracks 8 different candle body combinations for each direction (up, down, doji patterns)

- Monitors gap mitigation when price returns to fill the imbalance

- Changes color when gaps are partially or fully mitigated

**Gap Detection Logic:**

- Bearish FVG patterns: DDD, DDJ, JDD, UDJ, JDU, UDD, DDU, UDU

- Bullish FVG patterns: DUD, DUJ, JUD, UUJ, JUU, UUD, DUU, UUU

- (D=Down candle, U=Up candle, J=Doji candle)

**Trading Applications:**

- High-probability reversal zones when price returns to FVGs

- Support and resistance levels

- Target areas for limit orders

- Risk management reference points

## Component 3: TSM Fractals

**What it is:** TSM Fractals identify significant pivot highs and lows using Williams Fractal methodology. These mark potential reversal points and key support/resistance levels.

**How it works:**

- Identifies fractal highs: peaks where the center candle's high is higher than surrounding candles

- Identifies fractal lows: valleys where the center candle's low is lower than surrounding candles

- Uses customizable lookback periods (default 15) for fractal identification

- Displays horizontal lines with "$" symbols at fractal levels

- Maintains a configurable number of recent fractals on the chart

**Trading Applications:**

- Key support and resistance levels

- Potential reversal zones

- Confluence with other analysis tools

- Stop loss placement reference points

## Why This Combination Works

**Synergistic Analysis:** Each component provides different but complementary information:

1. **CISD** shows when market structure changes, indicating trend shifts or continuation

2. **FVGs** reveal where price has moved inefficiently and may return for rebalancing

3. **Fractals** highlight key pivot points that often act as support/resistance

**Trading Edge:** The combination allows for:

- **Entry Confirmation:** Wait for CISD breaks near unfilled FVGs at fractal levels

- **Risk Management:** Use FVG boundaries and fractal levels for stop placement

- **Target Selection:** Project moves to opposite FVGs or fractal levels

- **Market Context:** Understand whether you're trading with or against structure

## Key Features

**Multi-Timeframe CISD:**

- Customizable timeframe settings (Minute, Hour, Day, Week, Month)

- Adjustable swing length for pivot identification

- Customizable line styles, widths, and colors

- Optional alerts on structure breaks

**Advanced FVG Management:**

- Automatic gap size filtering

- Real-time mitigation tracking

- Color-coded active vs. mitigated gaps

- Optional pip value labels

- Large gap alerts for significant imbalances

**Intelligent Fractal Display:**

- Configurable fractal periods

- Maximum fractal count management

- Clean visual presentation

- Historical fractal preservation

## Settings & Customization

**CISD Settings:**

- Timeframe selection and multipliers

- Swing length adjustment (default 7)

- Line styling options

- Color customization for bullish/bearish breaks

- Alert toggle options

**FVG Settings:**

- Show/hide toggles for each direction

- Minimum gap size filtering

- Alert threshold for large gaps

- Color schemes for active and mitigated gaps

- Optional size labels in pips

**Fractal Settings:**

- Fractal period adjustment (default 15)

- Maximum display count (default 10)

- Show/hide toggle

## Educational Value

This indicator teaches traders to:

- Understand market structure concepts

- Recognize price inefficiencies

- Identify key pivot points

- Combine multiple analysis methods

- Develop systematic trading approaches

## Use Cases

**Swing Trading:** Identify major structure breaks with FVG confluence

**Day Trading:** Use lower timeframe CISDs with intraday FVGs

**Scalping:** Quick entries at FVG mitigation near fractal levels

**Position Trading:** Higher timeframe structure analysis with major FVGs

## Technical Implementation

- Utilizes Pine Script v6 for optimal performance

- Efficient array management for historical data

- Real-time calculations without repainting

- Memory-optimized box and line management

- Multi-timeframe data handling with proper security functions

This comprehensive tool eliminates the need for multiple separate indicators, providing everything needed for complete market structure analysis in one cohesive package. The educational component helps traders understand not just what the signals are, but why they work and how to use them effectively in different market conditions.

Order Flow Delta Matrix Pro @MaxMaserati 2.0Order Flow Delta Matrix Pro @MaxMaserati 2.0

Institutional-level order flow analysis

This advanced indicator displays institutional order flow data in an easy-to-read time-series matrix, revealing hidden buying and selling pressure that drives price movements.

KEY FEATURES

🔥 REAL-TIME DELTA TRACKING

- Delta Row: Net buying vs selling pressure per time period

- Live Countdown: Shows exact time remaining until next candle close

- Extended historical view for pattern recognition

CUSTOMIZABLE ROWS (Toggle On/Off)

- Max Delta: Highest buying pressure spikes (accumulation zones)

- *Min Delta: Lowest selling pressure spikes (distribution zones)

- Cumulative Delta: Running total showing institutional bias

- Delta/Volume Ratio: Quality of directional flow vs total volume

- Session Delta: Net flow since session start

- Volume: Raw transaction volume with high-volume highlighting

ADVANCED CONTROLS

- Time Direction: View oldest→newest OR newest→oldest

- 12/24 Hour Format: Choose your preferred time display

- Current Time Highlighting: Blue highlight on active time period

- Full Color Customization: Adapt to any chart theme

- Smart Sensitivity: Low/Normal/High modes for different markets

🎓 HOW TO USE IT

🟢 BULLISH SIGNALS

- Positive Delta Spikes: Look for green +500K+ delta values

- Rising Cumulative Delta: Upward trending cumulative line = institutional accumulation

- High Max Delta: Strong buying pressure at support levels

🔴 BEARISH SIGNALS

- Negative Delta Spikes: Look for red -500K+ delta values

- Falling Cumulative Delta: Downward trending cumulative = institutional distribution

- High Min Delta: Strong selling pressure at resistance levels

PRO TECHNIQUES

-Divergence Analysis: Price goes up but cumulative delta goes down = potential reversal

- Volume Confirmation: High delta + high volume = strong institutional conviction

- Session Bias: Positive session delta = bullish bias, negative = bearish bias

BEST USED FOR

- Scalping: 1-5 minute timeframes for quick institutional flow detection

- Day Trading: 15-60 minute timeframes for session bias and reversal spots

- Volume Profile: Combine with volume profile for complete order flow picture

- Futures Trading: Excellent for ES, NQ, crude oil, forex majors

PRO TIPS

1. Watch for Delta Divergences - Most reliable reversal signal

2. High Volume + High Delta = Institutional activity

3. Session Delta Direction = Overall market bias

4. Blue highlighted column= Current live data

5. Use with Support/Resistance for entry/exit timing

IMPORTANT NOTES

- Works on ALL timeframes and ALL markets

- Real-time updates for live trading decisions

- Historical data available for backtesting strategies

- No repainting - all signals are final and reliable

The matrix format makes complex data easy to interpret, giving a significant edge in understanding market dynamics and smart money order timing.

TEMA with Slope Color [MrBuCha]This TEMA indicator is particularly useful for trend following strategies. The key innovation here is using a higher timeframe (default 1-hour) to get a broader perspective on the trend direction, while the color-coding makes it immediately obvious whether the momentum is bullish (blue) or bearish (orange).

The 200-period length makes this more suitable for swing trading rather than day trading, as it filters out short-term noise and focuses on significant trend movements.

//

What is TEMA and How Does It Work?

TEMA (Triple Exponential Moving Average) is a technical indicator that builds upon the standard EMA to reduce lag and provide faster response to price changes. The calculation process is:

EMA1 = EMA of closing price with specified length

EMA2 = EMA of EMA1 with the same length

EMA3 = EMA of EMA2 with the same length

TEMA = 3 × (EMA1 - EMA2) + EMA3

This formula helps reduce the lag inherent in smoothing calculations, making TEMA more responsive to price movements compared to other moving averages.

Default Values

Length: 200 periods

Timeframe: "60" (1 hour)

Slope Colors

Blue: When TEMA is trending upward (tema_current > tema_previous)

Orange: When TEMA is trending downward (tema_current ≤ tema_previous)

Pros and Cons Summary

Advantages:

Fast Response: Reduces lag better than SMA and regular EMA

Easy to Use: Color-coded slope makes trend direction immediately visible

Multi-timeframe Capability: Can display TEMA from higher timeframes

Trend Following: Excellent for identifying trend direction

Visual Clarity: Clear color signals help with quick decision making

Disadvantages:

False Signals: Prone to whipsaws in sideways/choppy markets

Noise in Volatility: Frequent color changes during high volatility periods

Not Suitable for Scalping: Length of 200 is quite long for short-term trading

Still Lagging: Despite improvements, it remains a lagging indicator

Requires Confirmation: Should be used with other indicators for better accuracy

Best Use Cases:

Medium to long-term trend following

Identifying major trend changes

Multi-timeframe analysis

Combine with momentum oscillators for confirmation

Trading Tips:

Wait for color confirmation before entering trades

Use higher timeframe TEMA for overall trend bias

Combine with support/resistance levels

Avoid trading during consolidation periods

VWAP Fibonacci S&R with Bell CurveThis indicator is a sophisticated trading tool that combines three powerful technical analysis concepts to identify high-probability trading opportunities. Let me break down how it works:

Core Components:

1. VWAP (Volume Weighted Average Price)

Calculates the average price weighted by volume over a specified period

Acts as a dynamic support/resistance level that institutions often use

Can reset daily, weekly, or monthly depending on your trading timeframe

The yellow line on your chart represents the current VWAP

2. Bell Curve Probability Analysis

Measures how far the current price deviates from the VWAP in statistical terms

Calculates a Z-score (standard deviations away from the mean)

Creates probability bands around the VWAP based on price volatility

The theory: extreme deviations from VWAP tend to revert back to the mean

3. Fibonacci Retracement Levels

Uses recent highs and lows to calculate key Fibonacci levels (38.2%, 50%, 61.8%)

These levels often act as support and resistance zones

Combined with VWAP analysis for confluence trading

How the Signals Work:

BUY Signals (Green arrows below candles)

Generated when either condition is met:

Mean Reversion Buy: Price is below VWAP + high probability of reversion + extreme statistical deviation

Fibonacci Support Buy: Price is above VWAP + near key Fibonacci support levels (38.2% or 50%)

SELL Signals (Red arrows above candles)

Generated when either condition is met:

Mean Reversion Sell: Price is above VWAP + high probability of reversion + extreme statistical deviation

Fibonacci Resistance Sell: Price is below VWAP + near key Fibonacci resistance levels (61.8% or 50%)

Visual Elements

Yellow Line: Main VWAP

Blue Bands: Probability zones based on standard deviation

Orange/White/Purple Lines: Key Fibonacci levels (38.2%, 50%, 61.8%)

Yellow Background: High probability mean reversion zones

⚠ Symbol: Extreme deviation warning (Z-score > 2.5)

The Information Table

Shows real-time statistics:

VWAP: Current VWAP value

Distance: How far price is from VWAP (percentage)

Z-Score: Statistical measure of deviation (>2 is significant)

Reversion %: Probability of mean reversion

Fib 50%: Key Fibonacci midpoint level

Status: Current signal state

Trading Logic

The indicator works on the principle that:

Extreme deviations from VWAP are unsustainable and tend to revert

Fibonacci levels provide natural support/resistance zones

Volume confirmation ensures the move has institutional backing

Statistical probability helps time entries when odds are favorable

Best Use Cases

Scalping: Quick mean reversion trades when price gets too far from VWAP

Swing Trading: Using Fibonacci levels with VWAP for longer-term positions

Risk Management: Avoiding trades when probability is low

Confluence Trading: Waiting for multiple signals to align

Multi-Timeframe MA Breakout/Breakdown Analysis📊 Overview

This sophisticated Pine Script indicator revolutionizes breakout/breakdown analysis by distinguishing between fake and genuine signals using a unique swing-level validation methodology. Unlike traditional moving average crossovers, this system validates price movements against historical swing points, providing traders with high-probability entry and exit signals across multiple timeframes.

🎯 Core Trading Methodology

The Swing Validation Concept:

Traditional MA breakouts often fail because they don't consider the context of previous price action. This indicator solves this by:

Recording swing levels when each MA is initially crossed

Validating subsequent crosses against these historical swing points

Classifying signals as fake or genuine based on this validation

Tracking signal evolution as price action develops

Signal Classification System:

🔻 Breakdown Analysis:

Fake Breakdown: Price cuts below MA but stays above the swing low from previous MA cut

Genuine Breakdown: Price cuts below MA and falls below the swing low from previous MA cut

Validation Chain: EMA 50 validates against EMA 20 swing low, EMA 100 against EMA 50 swing low, EMA 200 against EMA 100 swing low

🔺 Breakout Analysis:

Fake Breakout: Price crosses above MA but stays below the swing high from previous MA cross

Genuine Breakout: Price crosses above MA and exceeds the swing high from previous MA cross

Validation Chain: EMA 50 validates against EMA 20 swing high, EMA 100 against EMA 50 swing high, EMA 200 against EMA 100 swing high

📈 Signal Interpretation Guide

Visual Chart Signals:

Breakdown Signals:

🔻 Orange Triangle Down + "FAKE BREAKDOWN": Potential reversal opportunity - price likely to bounce

🔻 Red Triangle Down + "GENUINE BREAKDOWN": Trend continuation - expect further downside

🔺 Lime Triangle Up + "BULLISH REVERSAL": Strong buy signal after fake breakdown validation

Breakout Signals:

🔺 Orange Triangle Up + "FAKE BREAKOUT": Potential reversal opportunity - price likely to decline

🔺 Dark Red Triangle Up + "GENUINE BREAKOUT": Trend continuation - expect further upside

🔻 Fuchsia Triangle Down + "BEARISH REVERSAL": Strong sell signal after fake breakout validation

Multi-Timeframe Analysis Table:

Signal Column Interpretation:

"FAKE BD" (Orange): Fake breakdown detected - watch for bullish reversal

"GENUINE BD" (Red): Genuine breakdown - bearish continuation likely

"FAKE BO" (Orange): Fake breakout detected - watch for bearish reversal

"GENUINE BO" (Dark Red): Genuine breakout - bullish continuation likely

"BULLISH" (Lime): Bullish reversal confirmed - strong buy signal

"BEARISH" (Fuchsia): Bearish reversal confirmed - strong sell signal

Trend Column:

"BULL" (Green): EMAs in bullish sequence (20>50>100>200)

"BEAR" (Red): EMAs in bearish sequence (20<50<100<200)

"SIDE" (Gray): Sideways/mixed EMA alignment

Status Column:

"Above 200" (Green): Price above 200 EMA - bullish bias

"Below 200" (Red): Price below 200 EMA - bearish bias

"At 200" (Gray): Price at 200 EMA - neutral

💡 Trading Strategies

Strategy 1: Fake Signal Reversal Trading

For Long Entries (Fake Breakdown Reversal):

Wait for fake breakdown signal (orange triangle down)

Confirm bullish reversal (lime triangle up) when price reclaims EMAs

Enter long on bullish reversal confirmation

Stop loss below the swing low that validated the fake breakdown

Target next resistance level or previous swing high

For Short Entries (Fake Breakout Reversal):

Wait for fake breakout signal (orange triangle up)

Confirm bearish reversal (fuchsia triangle down) when price falls below EMAs

Enter short on bearish reversal confirmation

Stop loss above the swing high that validated the fake breakout

Target next support level or previous swing low

Strategy 2: Genuine Signal Trend Following

For Trend Continuation Longs:

Identify genuine breakout (dark red triangle up)

Confirm higher timeframe alignment (4H/1D showing bullish trend)

Enter on pullback to broken resistance (now support)

Stop loss below the validation swing high

Target measured move or next major resistance

For Trend Continuation Shorts:

Identify genuine breakdown (red triangle down)

Confirm higher timeframe alignment (4H/1D showing bearish trend)

Enter on pullback to broken support (now resistance)

Stop loss above the validation swing low

Target measured move or next major support

Strategy 3: Multi-Timeframe Confluence

High-Probability Setups:

Align signals across timeframes (15M signal + 4H trend confirmation)

Look for confluence (multiple timeframes showing same signal type)

Prioritize higher timeframe signals for swing/position trades

Use lower timeframes for precise entry timing

⚠️ Risk Management Rules

Position Sizing:

Fake signal trades: Reduce position size (higher risk, higher reward)

Genuine signal trades: Standard position size (trend following)

Multi-timeframe confluence: Increase position size (higher probability)

Stop Loss Guidelines:

Fake breakdown longs: Stop below validation swing low

Fake breakout shorts: Stop above validation swing high

Genuine signals: Stop beyond the MA that was broken

Reversals: Stop beyond the reversal invalidation level

Take Profit Strategies:

Scale out at key resistance/support levels

Trail stops using the 20 EMA for trend following

Take partial profits at 1:2 risk/reward ratio

Let winners run on strong trend continuation signals

🔧 Best Practices

Signal Validation:

Wait for candle close before acting on signals

Check volume confirmation on breakouts/breakdowns

Consider market context (news, earnings, etc.)

Avoid trading during low liquidity periods

Timeframe Selection:

Scalping: 15M signals with 4H trend filter

Day Trading: 4H signals with 1D trend filter

Swing Trading: 1D signals with 1W trend filter

Position Trading: 1W signals for major moves

Market Conditions:

Trending Markets: Focus on genuine signals for continuation

Range-Bound Markets: Focus on fake signals for reversals

High Volatility: Reduce position sizes and widen stops

Low Volatility: Look for breakout setups with volume

📋 Advanced Tips

Signal Evolution Monitoring:

Watch for signal transitions (fake becoming genuine or vice versa)

Adjust positions when signal classification changes

Use alerts to stay informed of signal updates

Monitor multiple timeframes for comprehensive analysis

Confluence Factors:

Support/Resistance levels at signal points

Volume spikes on genuine signals

RSI divergences with fake signals

Fibonacci retracements at reversal points

Common Pitfalls to Avoid:

Don't chase signals after significant moves

Don't ignore higher timeframe trends

Don't overtrade on every signal

Don't neglect risk management rules

🎯 Quick Reference

Bullish Signals Priority:

Bullish Reversal (Lime) - Highest priority

Fake Breakdown (Orange) - High probability reversal

Genuine Breakout (Dark Red) - Trend continuation

Bearish Signals Priority:

Bearish Reversal (Fuchsia) - Highest priority

Fake Breakout (Orange) - High probability reversal

Genuine Breakdown (Red) - Trend continuation

Multi-Timeframe Hierarchy:

1W: Major trend direction

1D: Intermediate trend and swing levels

4H: Short-term trend and entry timing

15M: Precise entry and exit points

⚡ Pro Tip: The most powerful signals occur when fake signals reverse into genuine signals in the opposite direction, creating high-momentum moves with excellent risk/reward ratios.

Disclaimer: This indicator is for educational purposes. Always combine with proper risk management, additional technical analysis, and fundamental research before making trading decisions. Past performance does not guarantee future results.

PhenLabs - Market Fluid Dynamics📊 Market Fluid Dynamics -

Version: PineScript™ v6

📌 Description

The Market Fluid Dynamics - Phen indicator is a new thinking regarding market analysis by modeling price action, volume, and volatility using a fluid system. It attempts to offer traders control over more profound market forces, such as momentum (speed), resistance (thickness), and buying/selling pressure. By visualizing such dynamics, the script allows the traders to decide on the prevailing market flow, its power, likely continuations, and zones of calmness and chaos, and thereby allows improved decision-making.

This measure avoids the usual difficulty of reconciling multiple, often contradictory, market indications by including them within a single overarching model. It moves beyond traditional binary indicators by providing a multi-dimensional view of market behavior, employing fluid dynamic analogs to describe complex interactions in an accessible manner.

🚀 Points of Innovation

Integrated Fluid Dynamics Model: Combines velocity, viscosity, pressure, and turbulence into a single indicator.

Normalized Metrics: Uses ATR and other normalization techniques for consistent readings across different assets and timeframes.

Dynamic Flow Visualization: Main flow line changes color and intensity based on direction and strength.

Turbulence Background: Visually represents market stability with a gradient background, from calm to turbulent.

Comprehensive Dashboard: Provides an at-a-glance summary of key fluid dynamic metrics.

Multi-Layer Smoothing: Employs several layers of EMA smoothing for a clearer, more responsive main flow line.

🔧 Core Components

Velocity Component: Measures price momentum (first derivative of price), normalized by ATR. It indicates the speed and direction of price changes.

Viscosity Component: Represents market resistance to price changes, derived from ATR relative to its historical average. Higher viscosity suggests it’s harder for prices to move.

Pressure Component: Quantifies the force created by volume and price range (close - open), normalized by ATR. It reflects buying or selling pressure.

Turbulence Detection: Calculates a Reynolds number equivalent to identify market stability, ranging from laminar (stable) to turbulent (chaotic).