Cari skrip untuk "algo"

Jurik Moving Average with Stair-StepJurik Moving Average with Stair-Step Filter — Precision Smoothing with Event-Driven Signal Filtering

📌 Version:

Built in Pine Script v6, leveraging the full JMA core with an added stair-step threshold filter for discrete, event-based signal generation.

📌 Overview:

This enhanced Jurik Moving Average (JMA) combines the low-lag smoothing algorithm with a custom stair-step logic layer that transforms continuous JMA output into state-based, noise-filtered movement.

While the traditional JMA provides ultra-smooth, adaptive trend detection, it still updates continuously with each price tick. The Stair-Step version introduces a quantized output — the JMA value remains unchanged until price moves by a user-defined amount (in ticks or absolute price units). The result is a “digital” trend line that updates only when meaningful change occurs, filtering out minor fluctuations and giving traders clearer, more actionable transitions.

📌 How It Works:

✅ Adaptive JMA Core: Dynamically adjusts smoothing to volatility for ultra-low lag.

✅ Stair-Step Logic: Holds the JMA value steady until the underlying line moves by a chosen threshold.

✅ Event-Driven Updates: Each “step” represents a statistically significant change in market direction.

✅ Tick / Price-Based Sensitivity: Tune the filter to the instrument’s volatility, spread, or cost structure.

This dual-layer system blends JMA’s continuous adaptability with discrete regime detection — turning a smooth line into a decision-ready trend model.

📌 How to Use:

🔹 Bias Detection: Each new step indicates a potential regime shift or breakout confirmation.

🔹 Noise Reduction: Ideal in choppy or range-bound markets where traditional MAs over-react.

🔹 Automated Systems: Use stair transitions as clean event triggers for entries, exits, or bias flips.

🔹 Scalping & Swing Trading: Thresholds can be sized by tick, ATR, or volatility to match timeframe and cost tolerance.

📌 Why This Version Is Unique:

This is not just another moving average — it’s a stateful JMA, adding event-driven decision logic to one of the market’s most precise filters.

🔹 Discretized Trend Mapping: Flat plateaus define stability; steps define momentum bursts.

🔹 Reduced Whipsaws: Only reacts when moves exceed statistical or cost thresholds.

🔹 Execution-Grade Precision: Perfect for algorithmic strategies needing fewer false flips.

📌 Example Use:

Combine with VWAP, ATR, or momentum oscillators to confirm bias shifts. In automated strategies, use stair flips as “go / stop” states to control position changes or trade size adjustments.

📌 Summary:

The Jurik Moving Average with Stair-Step Filter preserves JMA’s hallmark smoothness while delivering a structured, event-driven representation of market movement.

It’s precision smoothing — now with adaptive noise gating — designed for traders who demand clarity, stability, and algorithm-ready signal behavior.

📌 Disclaimer:

This indicator is not affiliated with or derived from any proprietary Jurik Research algorithms. It’s an independent implementation that applies similar adaptive-smoothing principles, extended with a stair-step filtering mechanism for discrete trend transitions.

XIV Trading Strategy This simple strategy uses VVIX , the VIX of VIX , to find BUY/SELL signals for XIV. The actual return of for this strategy is actually lower than what is produced by Tradingview's backtesting engine ( 525 % vs 221 % in my testing ) . More detail available in my blog.

Cheers

Algo.

ISM Indicator As a Strategy Here's a very easy code, plotting the ISM against the SPX. In this exercise, i wanted to see if one could use the ISM indicator only to generate buy/sell signal, and what would be the performance.

What is the ISM

The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.By monitoring the ISM Manufacturing Index, investors are able to better understand national economic conditions. When this index is increasing, investors can assume that the stock markets should increase because of higher corporate profits. The opposite can be thought of the bond markets, which may decrease as the ISM Manufacturing Index increases because of sensitivity to potential inflation.

Buy/Sell Signal

ISM above 50 usually good economic condition and vice versa when below 50 . For this code I used 48.50 as my buy/sell signal line.

Results

To test this on a longer time period, I use the SPX index instead of SPY. The results are surprisingly good. 76.92% profitability with 3.03 profit factor.

Conclusion

Investors could use the ISM with other indicators to determine better entry and exit point. I will see if combining the ISM with other custom indicators , could generate better result. Feel free to share your results here.

Cheers

Algo.

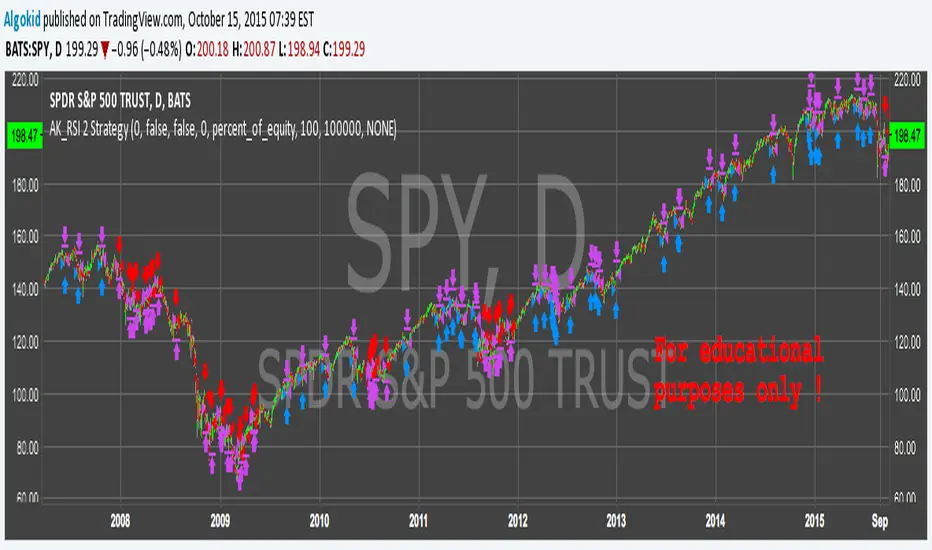

AK_RSI 2 Strategy ( based on Chris Moody RSI(2) indicator )Good Morning,

Republishing this in the script section to make the code visible to everyone. This strategy is based on Chris Moody's RSi(2) indicator. Good success rate on SPY. Again, this is for educational purposes only .

cheers

Algo

AK MACD BB INDICATOR V 1.00Here's my version of the MACD _BB . This is a great indicator to capture short term trends.

yellow candles = long

aqua candles = short

This indicator can be much better. I will work on it and publish an improved version (hopefully) soon. In the mean time , go ahead and play around with the code, and please share your findings :)

Cheers

Algo

AK TREND ID v1.00Hello,

"Are we at the top yet ? "........ " Is it a good time to invest ? " ......." Should I buy or sell ? " These are the many questions I hear and get on the daily basis. 1000's of investors do not know when to go in and out of the market. Most of them rely on the opinion of "experts" on television to make their investment decisions. Bad idea.Taking a systematic approach when investing, could save you a lot of time and headache. If there was only a way to know when to get in and out of the market !! hmmmm. The good news is that there many ways to do that. The bad news is , are you disciplined enough to follow it ?

I coded the AK_TREND ID specifically to identified trends in the SPX or SPY only . How does it work ? very simply , I simply plot the spread between the 3 month and 8 month moving average on the chart.

If the spread > 0 @ month end = BUY

if the spread < 0 @ month end = SELL

The AK TREND ID is a LAGGING Indicator , so it will not get you in at the very bottom or get you out at the very top. I did a backtest on the SPX from 1984 to 7/2/2014 (yesterday), The rule was to buy only when the AK TREND ID was green. let's look at the result:

14 trades : 11 W 3 L , 78.75 % winning %

Biggest winner (%) = 108 %

Biggest loser (%) = -10.7 %

Average Return = 27 %

Total Return since 1984 = 351.3 %

You can see the result in detail here : docs.google.com

Although the backtesting results are good, the AK TREND ID is not to be used as a trading system. It is simply design to let you know when to invest and when to get out. I'm working a more accurate version of this Indicator , that will use both technical and fundamental data. In the mean time , I hope this will give some of you piece of mind, and eliminate emotions from your trading decision. Feel free to modify the code as you wish, but please share your finding with the rest of Trading View community.

All the best

Algo

Risk Recommender — (Heatmap)📊 Risk Recommender — Per-Trade & Annualized (Heatmap Columns)

Estimate the optimal risk percentage for any market regime.

This tool dynamically recommends how much of your account equity to risk — either per trade or at a portfolio (annualized) level — using volatility as the guide.

⚙️ How it works

Two distinct modes give you flexibility:

1️⃣ Per-Trade (ATR-based)

• Calculates the current Average True Range (ATR) compared to its long-term baseline.

• When volatility is high (ATR ↑), risk per trade decreases to maintain constant dollar risk.

• When volatility is low (ATR ↓), risk per trade increases within your defined floor and ceiling.

• The display is normalized by stop distance (× ATR) and smoothed to avoid noise.

2️⃣ Annualized (Volatility Targeting)

• Computes realized volatility (standard deviation of log returns) and an EWMA forecast of future volatility.

• Blends current and forecast volatilities to estimate “effective” volatility.

• Scales your base risk so that portfolio volatility converges toward your chosen annual target (e.g., 20%).

• Useful for portfolio-level or systematic strategies that maintain constant volatility exposure.

🎨 Heatmap Visualization

The vertical column graph acts like a thermometer:

• 🟥 Red → “Reduce risk” (volatility high).

• 🟩 Green → “Increase risk” (volatility low).

• Smoothed and bounded between your Floor and Ceiling risk levels.

• Optional dotted guides mark those bounds.

• Label shows the current mode, recommended risk %, and key metrics (ATR ratio or effective volatility).

🔧 Key Inputs

• Base max risk per trade (%) — your normal per-trade risk budget.

• ATR length / Baseline ATR length — control sensitivity to short- vs. long-term volatility.

• Target annualized volatility (%) — portfolio volatility target for quant mode.

• λ (lambda) — smoothing factor for the EWMA volatility forecast (0.90–0.99 typical).

• Floor & Ceiling — clamps the output to avoid extreme sizing.

• Smoothing & Hysteresis — prevent rapid changes in risk recommendations.

🧮 Interpreting the Output

• “Recommended Risk (%)” = suggested portion of equity to risk on the next trade (or current exposure).

• In Per-Trade mode: reflects current ATR ÷ baseline ATR .

• In Annualized mode: reflects target volatility ÷ effective volatility .

• Use the color and height of the column as a quick visual cue for aggressiveness.

💡 Typical Use Cases

• Position-sizing overlay for discretionary traders.

• Volatility-targeting component for algorithmic or multi-asset systems.

• Educational tool to understand how volatility governs prudent risk management.

📘 Notes

• This indicator provides risk suggestions only ; it does not place trades.

• Works on any symbol or timeframe.

• Combine with your own strategy or alerts for full automation.

• All calculations use built-in Pine functions; no proprietary logic.

Tags:

#RiskManagement #ATR #Volatility #Quant #PositionSizing #SystematicTrading #AlgorithmicTrading #Portfolio #TradingStrategy #Heatmap #EWMA #Risk

Jurik Moving AverageJurik Moving Average (JMA) – Precision Smoothing with Adaptive Filtering

📌 Version: This script is written in Pine Script v6, utilizing advanced array handling and dynamic filtering for improved performance.

📌 Overview:

The Jurik Moving Average (JMA) was originally developed by Mark Jurik and is widely recognized for its ability to provide smooth trend-following signals with minimal lag. Unlike traditional moving averages, which suffer from a tradeoff between responsiveness and smoothness, JMA employs an adaptive smoothing algorithm that dynamically adjusts based on market conditions, reducing false signals while maintaining trend accuracy.

This version of JMA has been implemented in Pine Script v6 with enhancements that make it even more efficient for TradingView users. By utilizing advanced array-based calculations, logarithmic scaling, and cycle-based filtering, this implementation delivers an optimized, customizable, and high-performance smoothing indicator.

📌 How It Works:

✅ Adaptive Filtering: Dynamically adjusts smoothing based on price volatility.

✅ Cycle-Based Adjustments: Uses historical price action to fine-tune lag vs. responsiveness.

✅ Advanced Phase Control: Traders can shift the moving average forward or backward to optimize signal alignment.

Unlike existing open-source JMA implementations, this version features:

🔹 Enhanced Array-Based Calculations for better memory management & performance.

🔹 Logarithmic and Square Root Scaling to dynamically adjust phase & smoothing.

🔹 Improved Noise Reduction Techniques to minimize false breakouts.

📌 How to Use:

🔹 Trend Confirmation: Use JMA to validate trend direction and avoid whipsaws.

🔹 Trade Entries & Exits: Combine with price action or momentum indicators for refined entry/exit points.

🔹 Scalping & Swing Trading: Ideal for short-term and long-term strategies due to its adaptability.

📌 Why This Version is Unique:

This JMA expands on standard implementations by incorporating multi-level cycle smoothing, phase correction, and adaptive noise filtering. The result? A more precise, stable, and robust trend indicator that performs better than existing open-source versions.

Murrey Math

The Murrey Math indicator is a set of horizontal price levels, calculated from an algorithm developed by stock trader T.J. Murray.

The main concept behind Murrey Math is that prices tend to react and rotate at specific price levels. These levels are calculated by dividing the price range into fixed segments called "ranges", usually using a number of 8, 16, 32, 64, 128 or 256.

Murrey Math levels are calculated as follows:

1. A particular price range is taken, for example, 128.

2. Divide the current price by the range (128 in this example).

3. The result is rounded to the nearest whole number.

4. Multiply that whole number by the original range (128).

This results in the Murrey Math level closest to the current price. More Murrey levels are calculated and drawn by adding and subtracting multiples of the range to the initially calculated level.

Traders use Murrey Math levels as areas of possible support and resistance as it is believed that prices tend to react and pivot at these levels. They are also used to identify price patterns and possible entry and exit points in trading.

The Murrey Math indicator itself simply calculates and draws these horizontal levels on the price chart, allowing traders to easily visualize them and use them in their technical analysis.

HOW TO USE THIS INDICATOR?

To use the Murrey Math indicator effectively, here are some tips:

1. Choose the appropriate Murrey Math range : The Murrey Math range input (128 by default in the provided code) determines the spacing between the levels. Common ranges used are 8, 16, 32, 64, 128, and 256. A smaller range will give you more levels, while a larger range will give you fewer levels. Choose a range that suits the volatility and trading timeframe you're working with.

2. Identify potential support and resistance levels: The horizontal lines drawn by the indicator represent potential support and resistance levels based on the Murrey Math calculation. Prices often react or reverse at these levels, so they can be used to spot areas of interest for entries and exits.

3. Look for price reactions at the levels: Watch for price action like rejections, bounces, or breakouts at the Murrey Math levels. These reactions can signal potential trend continuation or reversal setups.

4. Trail stop-loss orders: You can place stop-loss orders just below/above the nearest Murrey Math level to manage risk if the price moves against your trade.

5. Set targets at future levels: Project potential profit targets by looking at upcoming Murrey Math levels in the direction of the trend.

7. Adjust range as needed: If prices are consistently breaking through levels without reacting, try adjusting the range input to a different value to see if it provides better levels.

In which asset can this indicator perform better?

The Murrey Math indicator can potentially perform well on any liquid financial asset that exhibits some degree of mean-reversion or trading range behavior. However, it may be more suitable for certain asset classes or trading timeframes than others.

Here are some assets and scenarios where the Murrey Math indicator can potentially perform better:

1. Forex Markets: The foreign exchange market is known for its ranging and mean-reverting nature, especially on higher timeframes like the daily or weekly charts. The Murrey Math levels can help identify potential support and resistance levels within these trading ranges.

2. Futures Markets: Futures contracts, such as those for commodities (e.g., crude oil, gold, etc.) or equity indices, often exhibit trading ranges and mean-reversion trends. The Murrey Math indicator can be useful in identifying potential turning points within these ranges.

3. Stocks with Range-bound Behavior: Some stocks, particularly those of large-cap companies, can trade within well-defined ranges for extended periods. The Murrey Math levels can help identify the boundaries of these ranges and potential reversal points.

4. I ntraday Trading: The Murrey Math indicator may be more effective on lower timeframes (e.g., 1-hour, 30-minute, 15-minute) for intraday trading, as prices tend to respect support and resistance levels more closely within shorter time periods.

5. Trending Markets: While the Murrey Math indicator is primarily designed for range-bound markets, it can also be used in trending markets to identify potential pullback or continuation levels.

Trend-Following & Breakout — Index Quant Strategy (NASDAQ)📈 Trend-Following & Breakout — Index Quant Strategy (NASDAQ & S&P 500)

Type: Invite-only strategy

Markets: NASDAQ 100 (NAS100 / US100 / NQ), S&P 500 (US500 / SPX), and other major equity indices.

🧠 Concept: Continuous trend model combining EWMAC (trend-following) and Donchian (breakout) signals, scaled by forecast strength and portfolio risk.

⚙️ Execution: Rebalances only on decision-bar closes, using hysteresis and a no-trade band to reduce churn.

📊 Default bias: Long-only — aligned with equity index drift.

🧩 How it works

• EWMAC Trend: Difference between fast and slow EMAs, normalized by an EWMA of absolute returns.

• Donchian Breakout: Distance beyond a 200-bar channel (Strict mode) or relative z-score position within it.

• Forecast combination: Weighted sum of trend and breakout points, clamped to ± capPoints.

• Hysteresis: Prevents quick sign flips near zero forecast.

• Risk scaling: Maps forecast strength to position size using equity × risk budget × ATR-based stop distance.

• Rebalance: Executes only if the required quantity change exceeds the Δqty threshold; can optionally block increases on Sundays (for CFDs).

⚙️ Default parameters

Deployed on NQ / US100 / NAS100 on Daily Timeframe

• Decision timeframe = 360 min (other options from 1 min to 1 week).

• Trend (EWMAC): Fast = 64, Slow = 256, Vol Norm = 32, Weight = 0.8.

• Breakout (Donchian): Length = 200, Mode = Strict, Weight = 0.2.

• Forecast scaling: ptsPerSigma = 1.0, capPoints = 10.

• Risk % per rebalance = 4 % of equity.

• ATR stop: ATR(14) × 1.0.

• No-trade band (Δqty) = 4 units.

• Hysteresis = 2 forecast points.

• Bias = Long-only (Neutral / Long-bias 50 % optional).

• Skip Sunday increases = false (default).

📋 Backtest properties (documented)

• Initial capital = 100 000 USD.

• Commission = 0.20 % per trade.

• Pyramiding = 10.

• Calc on every tick = false.

• Point value = 1 (for NAS100 CFD).

• No financing or slippage modeled.

• If using CFDs, account for overnight funding.

• On futures (NQ / ES), carry is implicit.

📊 Typical behaviour

• Many small scratches, a few large winners.

• Performs best during multi-week / multi-month trends.

• Underperforms in tight or volatile ranges.

• Average hold ≈ 30 – 90 days in historical tests.

💡 Risk and performance guide (illustrative)

Sharpe ≈ 1.25

Sortino ≈ 1.10 – 1.30

Max drawdown ≈ –18 % to –25 %

Annual volatility ≈ 24 – 28 %

CAGR ≈ 50 – 60 % (at 4 % risk)

Edge ratio ≈ 5 (MFE / MAE)

Historical backtests only — past performance does not guarantee future results.

🌍 Intended markets and timeframes

Optimized for NASDAQ 100 and S&P 500; also effective on similar indices (DAX, Dow Jones, FTSE).

Best on Daily or higher timeframes.

Aligns with long-term index drift — suitable for long-bias systematic trend portfolios.

⚠️ Limitations

• Backtests exclude CFD funding costs.

• Trend models will have losing streaks in range-bound markets.

• Designed for experienced traders seeking systematic exposure.

🔑 Requesting access

Send a private TradingView message to with the text:

“Request access to Trend-Following & Breakout — Index Quant Strategy.”

Access is granted only on explicit request.

For further information, see my TradingView Signature.

🆕 Release notes (v1.0)

• Initial release (360 min TF): EWMAC 64/256 + Donchian 200 Strict.

• Risk 4 %, ATR × 1.0, Long-only bias, hysteresis 2 pts, Δqty ≥ 4.

• Developed for NASDAQ 100 and S&P 500 indices.

• Implements continuous risk-scaled positioning and no-trade band logic.

🧾 Originality statement

This strategy is original work built entirely from TradingView built-ins (EMA, ATR, Highest, Lowest).

It does not reuse open-source invite-only code.

Any future reuse of open scripts will be done with explicit permission and credit.

Algorithm Predator - ProAlgorithm Predator - Pro: Advanced Multi-Agent Reinforcement Learning Trading System

Algorithm Predator - Pro combines four specialized market microstructure agents with a state-of-the-art reinforcement learning framework . Unlike traditional indicator mashups, this system implements genuine machine learning to automatically discover which detection strategies work best in current market conditions and adapts continuously without manual intervention.

Core Innovation: Rather than forcing traders to interpret conflicting signals, this system uses 15 different multi-armed bandit algorithms and a full reinforcement learning stack (Q-Learning, TD(λ) with eligibility traces, and Policy Gradient with REINFORCE) to learn optimal agent selection policies. The result is a self-improving system that gets smarter with every trade.

Target Users: Swing traders, day traders, and algorithmic traders seeking systematic signal generation with mathematical rigor. Suitable for stocks, forex, crypto, and futures on liquid instruments (>100k daily volume).

Why These Components Are Combined

The Fundamental Problem

No single indicator works consistently across all market regimes. What works in trending markets fails in ranging conditions. Traditional solutions force traders to manually switch indicators (slow, error-prone) or interpret all signals simultaneously (cognitive overload).

This system solves the problem through automated meta-learning: Deploy multiple specialized agents designed for specific market microstructure conditions, then use reinforcement learning to discover which agent (or combination) performs best in real-time.

Why These Specific Four Agents?

The four agents provide orthogonal failure mode coverage —each agent's weakness is another's strength:

Spoofing Detector - Optimal in consolidation/manipulation; fails in trending markets (hedged by Exhaustion Detector)

Exhaustion Detector - Optimal at trend climax; fails in range-bound markets (hedged by Liquidity Void)

Liquidity Void - Optimal pre-breakout compression; fails in established trends (hedged by Mean Reversion)

Mean Reversion - Optimal in low volatility; fails in strong trends (hedged by Spoofing Detector)

This creates complete market state coverage where at least one agent should perform well in any condition. The bandit system identifies which one without human intervention.

Why Reinforcement Learning vs. Simple Voting?

Traditional consensus systems have fatal flaws: equal weighting assumes all agents are equally reliable (false), static thresholds don't adapt, and no learning means past mistakes repeat indefinitely.

Reinforcement learning solves this through the exploration-exploitation tradeoff: Continuously test underused agents (exploration) while primarily relying on proven winners (exploitation). Over time, the system builds a probability distribution over agent quality reflecting actual market performance.

Mathematical Foundation: Multi-armed bandit problem from probability theory, where each agent is an "arm" with unknown reward distribution. The goal is to maximize cumulative reward while efficiently learning each arm's true quality.

The Four Trading Agents: Technical Explanation

Agent 1: 🎭 Spoofing Detector (Institutional Manipulation Detection)

Theoretical Basis: Market microstructure theory on order flow toxicity and information asymmetry. Based on research by Easley, López de Prado, and O'Hara on high-frequency trading manipulation.

What It Detects:

1. Iceberg Orders (Hidden Liquidity Absorption)

Method: Monitors volume spikes (>2.5× 20-period average) with minimal price movement (<0.3× ATR)

Formula: score += (close > open ? -2.5 : 2.5) when volume > vol_avg × 2.5 AND abs(close - open) / ATR < 0.3

Interpretation: Large volume without price movement indicates institutional absorption (buying) or distribution (selling) using hidden orders

Signal Logic: Contrarian—fade false breakouts caused by institutional manipulation

2. Spoofing Patterns (Fake Liquidity via Layering)

Method: Analyzes candlestick wick-to-body ratios during volume spikes

Formula: if upper_wick > body × 2 AND volume_spike: score += 2.0

Mechanism: Spoofing creates large wicks (orders pulled before execution) with volume evidence

Signal Logic: Wick direction indicates trapped participants; trade against the failed move

3. Post-Manipulation Reversals

Method: Tracks volume decay after manipulation events

Formula: if volume > vol_avg × 3 AND volume / volume < 0.3: score += (close > open ? -1.5 : 1.5)

Interpretation: Sharp volume drop after manipulation indicates exhaustion of manipulative orders

Why It Works: Institutional manipulation creates detectable microstructure anomalies. While retail traders see "mysterious reversals," this agent quantifies the order flow patterns causing them.

Parameter: i_spoof (sensitivity 0.5-2.0) - Controls detection threshold

Best Markets: Consolidations before breakouts, London/NY overlap windows, stocks with institutional ownership >70%

Agent 2: ⚡ Exhaustion Detector (Momentum Failure Analysis)

Theoretical Basis: Technical analysis divergence theory combined with VPIN reversals from market microstructure literature.

What It Detects:

1. Price-RSI Divergence (Momentum Deceleration)

Method: Compares 5-bar price ROC against RSI change

Formula: if price_roc > 5% AND rsi_current < rsi : score += 1.8

Mathematics: Second derivative detecting inflection points

Signal Logic: When price makes higher highs but momentum makes lower highs, expect mean reversion

2. Volume Exhaustion (Buying/Selling Climax)

Method: Identifies strong price moves (>5% ROC) with declining volume (<-20% volume ROC)

Formula: if price_roc > 5 AND vol_roc < -20: score += 2.5

Interpretation: Price extension without volume support indicates retail chasing while institutions exit

3. Momentum Deceleration (Acceleration Analysis)

Method: Compares recent 3-bar momentum to prior 3-bar momentum

Formula: deceleration = abs(mom1) < abs(mom2) × 0.5 where momentum significant (> ATR)

Signal Logic: When rate of price change decelerates significantly, anticipate directional shift

Why It Works: Momentum is lagging, but momentum divergence is leading. By comparing momentum's rate of change to price, this agent detects "weakening conviction" before reversals become obvious.

Parameter: i_momentum (sensitivity 0.5-2.0)

Best Markets: Strong trends reaching climax, parabolic moves, instruments with high retail participation

Agent 3: 💧 Liquidity Void Detector (Breakout Anticipation)

Theoretical Basis: Market liquidity theory and order book dynamics. Based on research into "liquidity holes" and volatility compression preceding expansion.

What It Detects:

1. Bollinger Band Squeeze (Volatility Compression)

Method: Monitors Bollinger Band width relative to 50-period average

Formula: bb_width = (upper_band - lower_band) / middle_band; triggers when < 0.6× average

Mathematical Foundation: Regression to the mean—low volatility precedes high volatility

Signal Logic: When volatility compresses AND cumulative delta shows directional bias, anticipate breakout

2. Volume Profile Gaps (Thin Liquidity Zones)

Method: Identifies sharp volume transitions indicating few limit orders

Formula: if volume < vol_avg × 0.5 AND volume < vol_avg × 0.5 AND volume > vol_avg × 1.5

Interpretation: Sudden volume drop after spike indicates price moved through order book to low-opposition area

Signal Logic: Price accelerates through low-liquidity zones

3. Stop Hunts (Liquidity Grabs Before Reversals)

Method: Detects new 20-bar highs/lows with immediate reversal and rejection wick

Formula: if new_high AND close < high - (high - low) × 0.6: score += 3.0

Mechanism: Market makers push price to trigger stop-loss clusters, then reverse

Signal Logic: Enter reversal after stop-hunt completes

Why It Works: Order book theory shows price moves fastest through zones with minimal liquidity. By identifying these zones before major moves, this agent provides early entry for high-reward breakouts.

Parameter: i_liquidity (sensitivity 0.5-2.0)

Best Markets: Range-bound pre-breakout setups, volatility compression zones, instruments prone to gap moves

Agent 4: 📊 Mean Reversion (Statistical Arbitrage Engine)

Theoretical Basis: Statistical arbitrage theory, Ornstein-Uhlenbeck mean-reverting processes, and pairs trading methodology applied to single instruments.

What It Detects:

1. Z-Score Extremes (Standard Deviation Analysis)

Method: Calculates price distance from 20-period and 50-period SMAs in standard deviation units

Formula: zscore_20 = (close - SMA20) / StdDev(50)

Statistical Interpretation: Z-score >2.0 means price is 2 standard deviations above mean (97.5th percentile)

Trigger Logic: if abs(zscore_20) > 2.0: score += zscore_20 > 0 ? -1.5 : 1.5 (fade extremes)

2. Ornstein-Uhlenbeck Process (Mean-Reverting Stochastic Model)

Method: Models price as mean-reverting stochastic process: dx = θ(μ - x)dt + σdW

Implementation: Calculates spread = close - SMA20, then z-score of spread vs. spread distribution

Formula: ou_signal = (spread - spread_mean) / spread_std

Interpretation: Measures "tension" pulling price back to equilibrium

3. Correlation Breakdown (Regime Change Detection)

Method: Compares 50-period price-volume correlation to 10-period correlation

Formula: corr_breakdown = abs(typical_corr - recent_corr) > 0.5

Enhancement: if corr_breakdown AND abs(zscore_20) > 1.0: score += zscore_20 > 0 ? -1.2 : 1.2

Why It Works: Mean reversion is the oldest quantitative strategy (1970s pairs trading at Morgan Stanley). While simple, it remains effective because markets exhibit periodic equilibrium-seeking behavior. This agent applies rigorous statistical testing to identify when mean reversion probability is highest.

Parameter: i_statarb (sensitivity 0.5-2.0)

Best Markets: Range-bound instruments, low-volatility periods (VIX <15), algo-dominated markets (forex majors, index futures)

Multi-Armed Bandit System: 15 Algorithms Explained

What Is a Multi-Armed Bandit Problem?

Origin: Named after slot machines ("one-armed bandits"). Imagine facing multiple slot machines, each with unknown payout rates. How do you maximize winnings?

Formal Definition: K arms (agents), each with unknown reward distribution with mean μᵢ. Goal: Maximize cumulative reward over T trials. Challenge: Balance exploration (trying uncertain arms to learn quality) vs. exploitation (using known-best arm for immediate reward).

Trading Application: Each agent is an "arm." After each trade, receive reward (P&L). Must decide which agent to trust for next signal.

Algorithm Categories

Bayesian Approaches (probabilistic, optimal for stationary environments):

Thompson Sampling

Bootstrapped Thompson Sampling

Discounted Thompson Sampling

Frequentist Approaches (confidence intervals, deterministic):

UCB1

UCB1-Tuned

KL-UCB

SW-UCB (Sliding Window)

D-UCB (Discounted)

Adversarial Approaches (robust to non-stationary environments):

EXP3-IX

Hedge

FPL-Gumbel

Reinforcement Learning Approaches (leverage learned state-action values):

Q-Values (from Q-Learning)

Policy Network (from Policy Gradient)

Simple Baseline:

Epsilon-Greedy

Softmax

Key Algorithm Details

Thompson Sampling (DEFAULT - RECOMMENDED)

Theoretical Foundation: Bayesian decision theory with conjugate priors. Published by Thompson (1933), rediscovered for bandits by Chapelle & Li (2011).

How It Works:

Model each agent's reward distribution as Beta(α, β) where α = wins, β = losses

Each step, sample from each agent's beta distribution: θᵢ ~ Beta(αᵢ, βᵢ)

Select agent with highest sample: argmaxᵢ θᵢ

Update winner's distribution after observing outcome

Mathematical Properties:

Optimality: Achieves logarithmic regret O(K log T) (proven optimal)

Bayesian: Maintains probability distribution over true arm means

Automatic Balance: High uncertainty → more exploration; high certainty → exploitation

⚠️ CRITICAL APPROXIMATION: This is a pseudo-random approximation of true Thompson Sampling. True implementation requires random number generation from beta distributions, which Pine Script doesn't provide. This version uses Box-Muller transform with market data (price/volume decimal digits) as entropy source. While not mathematically pure, it maintains core exploration-exploitation balance and learns agent preferences effectively.

When To Use: Best all-around choice. Handles non-stationary markets reasonably well, balances exploration naturally, highly sample-efficient.

UCB1 (Upper Confidence Bound)

Formula: UCB_i = reward_mean_i + sqrt(2 × ln(total_pulls) / pulls_i)

Interpretation: First term (exploitation) + second term (exploration bonus for less-tested arms)

Mathematical Properties:

Deterministic : Always selects same arm given same state

Regret Bound: O(K log T) — same optimality as Thompson Sampling

Interpretable: Can visualize confidence intervals

When To Use: Prefer deterministic behavior, want to visualize uncertainty, stable markets

EXP3-IX (Exponential Weights - Adversarial)

Theoretical Foundation: Adversarial bandit algorithm. Assumes environment may be actively hostile (worst-case analysis).

How It Works:

Maintain exponential weights: w_i = exp(η × cumulative_reward_i)

Select agent with probability proportional to weights: p_i = (1-γ)w_i/Σw_j + γ/K

After outcome, update with importance weighting: estimated_reward = observed_reward / p_i

Mathematical Properties:

Adversarial Regret: O(sqrt(TK log K)) even if environment is adversarial

No Assumptions: Doesn't assume stationary or stochastic reward distributions

Robust: Works even when optimal arm changes continuously

When To Use: Extreme non-stationarity, don't trust reward distribution assumptions, want robustness over efficiency

KL-UCB (Kullback-Leibler Upper Confidence Bound)

Theoretical Foundation: Uses KL-divergence instead of Hoeffding bounds. Tighter confidence intervals.

Formula (conceptual): Find largest q such that: n × KL(p||q) ≤ ln(t) + 3×ln(ln(t))

Mathematical Properties:

Tighter Bounds: KL-divergence adapts to reward distribution shape

Asymptotically Optimal: Better constant factors than UCB1

Computationally Intensive: Requires iterative binary search (15 iterations)

When To Use: Maximum sample efficiency needed, willing to pay computational cost, long-term trading (>500 bars)

Q-Values & Policy Network (RL-Based Selection)

Unique Feature: Instead of treating agents as black boxes with scalar rewards, these algorithms leverage the full RL state representation .

Q-Values Selection:

Uses learned Q-values: Q(state, agent_i) from Q-Learning

Selects agent via softmax over Q-values for current market state

Advantage: Selects based on state-conditional quality (which agent works best in THIS market state)

Policy Network Selection:

Uses neural network policy: π(agent | state, θ) from Policy Gradient

Direct policy over agents given market features

Advantage: Can learn non-linear relationships between market features and agent quality

When To Use: After 200+ RL updates (Q-Values) or 500+ updates (Policy Network) when models converged

Machine Learning & Reinforcement Learning Stack

Why Both Bandits AND Reinforcement Learning?

Critical Distinction:

Bandits treat agents as contextless black boxes: "Agent 2 has 60% win rate"

Reinforcement Learning adds state context: "Agent 2 has 60% win rate WHEN trend_score > 2 and RSI < 40"

Power of Combination: Bandits provide fast initial learning with minimal assumptions. RL provides state-dependent policies for superior long-term performance.

Component 1: Q-Learning (Value-Based RL)

Algorithm: Temporal Difference Learning with Bellman equation.

State Space: 54 discrete states formed from:

trend_state = {0: bearish, 1: neutral, 2: bullish} (3 values)

volatility_state = {0: low, 1: normal, 2: high} (3 values)

RSI_state = {0: oversold, 1: neutral, 2: overbought} (3 values)

volume_state = {0: low, 1: high} (2 values)

Total states: 3 × 3 × 3 × 2 = 54 states

Action Space: 5 actions (No trade, Agent 1, Agent 2, Agent 3, Agent 4)

Total state-action pairs: 54 × 5 = 270 Q-values

Bellman Equation:

Q(s,a) ← Q(s,a) + α ×

Parameters:

α (learning rate): 0.01-0.50, default 0.10 - Controls step size for updates

γ (discount factor): 0.80-0.99, default 0.95 - Values future rewards

ε (exploration): 0.01-0.30, default 0.10 - Probability of random action

Update Mechanism:

Position opens with state s, action a (selected agent)

Every bar position is open: Calculate floating P&L → scale to reward

Perform online TD update

When position closes: Perform terminal update with final reward

Gradient Clipping: TD errors clipped to ; Q-values clipped to for stability.

Why It Works: Q-Learning learns "quality" of each agent in each market state through trial and error. Over time, builds complete state-action value function enabling optimal state-dependent agent selection.

Component 2: TD(λ) Learning (Temporal Difference with Eligibility Traces)

Enhancement Over Basic Q-Learning: Credit assignment across multiple time steps.

The Problem TD(λ) Solves:

Position opens at t=0

Market moves favorably at t=3

Position closes at t=8

Question: Which earlier decisions contributed to success?

Basic Q-Learning: Only updates Q(s₈, a₈) ← reward

TD(λ): Updates ALL visited state-action pairs with decayed credit

Eligibility Trace Formula:

e(s,a) ← γ × λ × e(s,a) for all s,a (decay all traces)

e(s_current, a_current) ← 1 (reset current trace)

Q(s,a) ← Q(s,a) + α × TD_error × e(s,a) (update all with trace weight)

Lambda Parameter (λ): 0.5-0.99, default 0.90

λ=0: Pure 1-step TD (only immediate next state)

λ=1: Full Monte Carlo (entire episode)

λ=0.9: Balance (recommended)

Why Superior: Dramatically faster learning for multi-step tasks. Q-Learning requires many episodes to propagate rewards backwards; TD(λ) does it in one.

Component 3: Policy Gradient (REINFORCE with Baseline)

Paradigm Shift: Instead of learning value function Q(s,a), directly learn policy π(a|s).

Policy Network Architecture:

Input: 12 market features

Hidden: None (linear policy)

Output: 5 actions (softmax distribution)

Total parameters: 12 features × 5 actions + 5 biases = 65 parameters

Feature Set (12 Features):

Price Z-score (close - SMA20) / ATR

Volume ratio (volume / vol_avg - 1)

RSI deviation (RSI - 50) / 50

Bollinger width ratio

Trend score / 4 (normalized)

VWAP deviation

5-bar price ROC

5-bar volume ROC

Range/ATR ratio - 1

Price-volume correlation (20-period)

Volatility ratio (ATR / ATR_avg - 1)

EMA50 deviation

REINFORCE Update Rule:

θ ← θ + α × ∇log π(a|s) × advantage

where advantage = reward - baseline (variance reduction)

Why Baseline? Raw rewards have high variance. Subtracting baseline (running average) centers rewards around zero, reducing gradient variance by 50-70%.

Learning Rate: 0.001-0.100, default 0.010 (much lower than Q-Learning because policy gradients have high variance)

Why Policy Gradient?

Handles 12 continuous features directly (Q-Learning requires discretization)

Naturally maintains exploration through probability distribution

Can converge to stochastic optimal policy

Component 4: Ensemble Meta-Learner (Stacking)

Architecture: Level-1 meta-learner combines Level-0 base learners (Q-Learning, TD(λ), Policy Gradient).

Three Meta-Learning Algorithms:

1. Simple Average (Baseline)

Final_prediction = (Q_prediction + TD_prediction + Policy_prediction) / 3

2. Weighted Vote (Reward-Based)

weight_i ← 0.95 × weight_i + 0.05 × (reward_i + 1)

3. Adaptive Weighting (Gradient-Based) — RECOMMENDED

Loss Function: L = (y_true - ŷ_ensemble)²

Gradient: ∂L/∂weight_i = -2 × (y_true - ŷ_ensemble) × agent_contribution_i

Updates weights via gradient descent with clipping and normalization

Why It Works: Unlike simple averaging, meta-learner discovers which base learner is most reliable in current regime. If Policy Gradient excels in trending markets while Q-Learning excels in ranging, meta-learner learns these patterns and weights accordingly.

Feature Importance Tracking

Purpose: Identify which of 12 features contribute most to successful predictions.

Update Rule: importance_i ← 0.95 × importance_i + 0.05 × |feature_i × reward|

Use Cases:

Feature selection: Drop low-importance features

Market regime detection: Importance shifts reveal regime changes

Agent tuning: If VWAP deviation has high importance, consider boosting agents using VWAP

RL Position Tracking System

Critical Innovation: Proper reinforcement learning requires tracking which decisions led to outcomes.

State Tracking (When Signal Validates):

active_rl_state ← current_market_state (0-53)

active_rl_action ← selected_agent (1-4)

active_rl_entry ← entry_price

active_rl_direction ← 1 (long) or -1 (short)

active_rl_bar ← current_bar_index

Online Updates (Every Bar Position Open):

floating_pnl = (close - entry) / entry × direction

reward = floating_pnl × 10 (scale to meaningful range)

reward = clip(reward, -5.0, 5.0)

Update Q-Learning, TD(λ), and Policy Gradient

Terminal Update (Position Close):

Final Q-Learning update (no next Q-value, terminal state)

Update meta-learner with final result

Update agent memory

Clear position tracking

Exit Conditions:

Time-based: ≥3 bars held (minimum hold period)

Stop-loss: 1.5% adverse move

Take-profit: 2.0% favorable move

Market Microstructure Filters

Why Microstructure Matters

Traditional technical analysis assumes fair, efficient markets. Reality: Markets have friction, manipulation, and information asymmetry. Microstructure filters detect when market structure indicates adverse conditions.

Filter 1: VPIN (Volume-Synchronized Probability of Informed Trading)

Theoretical Foundation: Easley, López de Prado, & O'Hara (2012). "Flow Toxicity and Liquidity in a High-Frequency World."

What It Measures: Probability that current order flow is "toxic" (informed traders with private information).

Calculation:

Classify volume as buy or sell (close > close = buy volume)

Calculate imbalance over 20 bars: VPIN = |Σ buy_volume - Σ sell_volume| / Σ total_volume

Compare to moving average: toxic = VPIN > VPIN_MA(20) × sensitivity

Interpretation:

VPIN < 0.3: Normal flow (uninformed retail)

VPIN 0.3-0.4: Elevated (smart money active)

VPIN > 0.4: Toxic flow (informed institutions dominant)

Filter Logic:

Block LONG when: VPIN toxic AND price rising (don't buy into institutional distribution)

Block SHORT when: VPIN toxic AND price falling (don't sell into institutional accumulation)

Adaptive Threshold: If VPIN toxic frequently, relax threshold; if rarely toxic, tighten threshold. Bounded .

Filter 2: Toxicity (Kyle's Lambda Approximation)

Theoretical Foundation: Kyle (1985). "Continuous Auctions and Insider Trading."

What It Measures: Price impact per unit volume — market depth and informed trading.

Calculation:

price_impact = (close - close ) / sqrt(Σ volume over 10 bars)

impact_zscore = (price_impact - impact_mean) / impact_std

toxicity = abs(impact_zscore)

Interpretation:

Low toxicity (<1.0): Deep liquid market, large orders absorbed easily

High toxicity (>2.0): Thin market or informed trading

Filter Logic: Block ALL SIGNALS when toxicity > threshold. Most dangerous when price breaks from VWAP with high toxicity.

Filter 3: Regime Filter (Counter-Trend Protection)

Purpose: Prevent counter-trend trades during strong trends.

Trend Scoring:

trend_score = 0

trend_score += close > EMA8 ? +1 : -1

trend_score += EMA8 > EMA21 ? +1 : -1

trend_score += EMA21 > EMA50 ? +1 : -1

trend_score += close > EMA200 ? +1 : -1

Range:

Regime Classification:

Strong Bull: trend_score ≥ +3 → Block all SHORT signals

Strong Bear: trend_score ≤ -3 → Block all LONG signals

Neutral: -2 ≤ trend_score ≤ +2 → Allow both directions

Filter 4: Liquidity Boost (Signal Enhancer)

Unique: Unlike other filters (which block), this amplifies signals during low liquidity.

Logic: if volume < vol_avg × 0.7: agent_scores × 1.2

Why It Works: Low liquidity often precedes explosive moves (breakouts). By increasing agent sensitivity during compression, system catches pre-breakout signals earlier.

Technical Implementation & Approximations

⚠️ Critical Approximations Required by Pine Script

1. Thompson Sampling: Pseudo-Random Beta Distribution

Academic Standard: True random sampling from beta distributions using cryptographic RNG

This Implementation: Box-Muller transform for normal distribution using market data (price/volume decimal digits) as entropy source, then scale to beta distribution mean/variance

Impact: Not cryptographically random, may have subtle biases in specific price ranges, but maintains correct mean and approximate variance. Sufficient for bandit agent selection.

2. VPIN: Simplified Volume Classification

Academic Standard: Lee-Ready algorithm or exchange-provided aggressor flags with tick-by-tick data

This Implementation: Bar-based classification: if close > close : buy_volume += volume

Impact: 10-15% precision loss. Works well in directional markets, misclassifies in choppy conditions. Still captures order flow imbalance signal.

3. Policy Gradient: Simplified Per-Action Updates

Academic Standard: Full softmax gradient updating all actions (selected action UP, others DOWN proportionally)

This Implementation: Only updates selected action's weights

Impact: Valid approximation for small action spaces (5 actions). Slower convergence than full softmax but still learns optimal policy.

4. Kyle's Lambda: Simplified Price Impact

Academic Standard: Regression over multiple time scales with signed order flow

This Implementation: price_impact = Δprice_10 / sqrt(Σvolume_10); z_score calculation

Impact: 15-20% precision loss. No proper signed order flow. Still detects informed trading signals at extremes (>2σ).

5. Other Simplifications:

Hawkes Process: Fixed exponential decay (0.9) not MLE-optimized

Entropy: Ratio approximation not true Shannon entropy H(X) = -Σ p(x)·log₂(p(x))

Feature Engineering: 12 features vs. potential 100+ with polynomial interactions

RL Hybrid Updates: Both online and terminal (non-standard but empirically effective)

Overall Precision Loss Estimate: 10-15% compared to academic implementations with institutional data feeds.

Practical Trade-off: For retail trading with OHLCV data, these approximations provide 90%+ of the edge while maintaining full transparency, zero latency, no external dependencies, and runs on any TradingView plan.

How to Use: Practical Guide

Initial Setup (5 Minutes)

Select Trading Mode: Start with "Balanced" for most users

Enable ML/RL System: Toggle to TRUE, select "Full Stack" ML Mode

Bandit Configuration: Algorithm: "Thompson Sampling", Mode: "Switch" or "Blend"

Microstructure Filters: Enable all four filters, enable "Adaptive Microstructure Thresholds"

Visual Settings: Enable dashboard (Top Right), enable all chart visuals

Learning Phase (First 50-100 Signals)

What To Monitor:

Agent Performance Table: Watch win rates develop (target >55%)

Bandit Weights: Should diverge from uniform (0.25 each) after 20-30 signals

RL Core Metrics: "RL Updates" should increase when position open

Filter Status: "Blocked" count indicates filter activity

Optimization Tips:

Too few signals: Lower min_confidence to 0.25, increase agent sensitivities to 1.1-1.2

Too many signals: Raise min_confidence to 0.35-0.40, decrease agent sensitivities to 0.8-0.9

One agent dominates (>70%): Consider "Lock Agent" feature

Signal Interpretation

Dashboard Signal Status:

⚪ WAITING FOR SIGNAL: No agent signaling

⏳ ANALYZING...: Agent signaling but not confirmed

🟡 CONFIRMING 2/3: Building confirmation (2 of 3 bars)

🟢 LONG ACTIVE : Validated long entry

🔴 SHORT ACTIVE : Validated short entry

Kill Zone Boxes: Entry price (triangle marker), Take Profit (Entry + 2.5× ATR), Stop Loss (Entry - 1.5× ATR). Risk:Reward = 1:1.67

Risk Management

Position Sizing:

Risk per trade = 1-2% of capital

Position size = (Capital × Risk%) / (Entry - StopLoss)

Stop-Loss Placement:

Initial: Entry ± 1.5× ATR (shown in kill zone)

Trailing: After 1:1 R:R achieved, move stop to breakeven

Take-Profit Strategy:

TP1 (2.5× ATR): Take 50% off

TP2 (Runner): Trail stop at 1× ATR or use opposite signal as exit

Memory Persistence

Why Save Memory: Every chart reload resets the system. Saving learned parameters preserves weeks of learning.

When To Save: After 200+ signals when agent weights stabilize

What To Save: From Memory Export panel, copy all alpha/beta/weight values and adaptive thresholds

How To Restore: Enable "Restore From Saved State", input all values into corresponding fields

What Makes This Original

Innovation 1: Genuine Multi-Armed Bandit Framework

This implements 15 mathematically rigorous bandit algorithms from academic literature (Thompson Sampling from Chapelle & Li 2011, UCB family from Auer et al. 2002, EXP3 from Auer et al. 2002, KL-UCB from Garivier & Cappé 2011). Each algorithm maintains proper state, updates according to proven theory, and converges to optimal behavior. This is real learning, not superficial parameter changes.

Innovation 2: Full Reinforcement Learning Stack

Beyond bandits learning which agent works best globally, RL learns which agent works best in each market state. After 500+ positions, system builds 54-state × 5-action value function (270 learned parameters) capturing context-dependent agent quality.

Innovation 3: Market Microstructure Integration

Combines retail technical analysis with institutional-grade microstructure metrics: VPIN from Easley, López de Prado, O'Hara (2012), Kyle's Lambda from Kyle (1985), Hawkes Processes from Hawkes (1971). These detect informed trading, manipulation, and liquidity dynamics invisible to technical analysis.

Innovation 4: Adaptive Threshold System

Dynamic quantile-based thresholds: Maintains histogram of each agent's score distribution (24 bins, exponentially decayed), calculates 80th percentile threshold from histogram. Agent triggers only when score exceeds its own learned quantile. Proper non-parametric density estimation automatically adapts to instrument volatility, agent behavior shifts, and market regime changes.

Innovation 5: Episodic Memory with Transfer Learning

Dual-layer architecture: Short-term memory (last 20 trades, fast adaptation) + Long-term memory (condensed episodes, historical patterns). Transfer mechanism consolidates knowledge when STM reaches threshold. Mimics hippocampus → neocortex consolidation in human memory.

Limitations & Disclaimers

General Limitations

No Predictive Guarantee: Pattern recognition ≠ prediction. Past performance ≠ future results.

Learning Period Required: Minimum 50-100 bars for reliable statistics. Initial performance may be suboptimal.

Overfitting Risk: System learns patterns in historical data. May not generalize to unprecedented conditions.

Approximation Limitations: See technical implementation section (10-15% precision loss vs. academic standards)

Single-Instrument Limitation: No multi-asset correlation, sector context, or VIX integration.

Forward-Looking Bias Disclaimer

CRITICAL TRANSPARENCY: The RL system uses an 8-bar forward-looking window for reward calculation.

What This Means: System learns from rewards incorporating future price information (bars 101-108 relative to entry at bar 100).

Why Acceptable:

✅ Signals do NOT look ahead: Entry decisions use only data ≤ entry bar

✅ Learning only: Forward data used for optimization, not signal generation

✅ Real-time mirrors backtest: In live trading, system learns identically

⚠️ Implication: Dashboard "Agent Win%" reflects this 8-bar evaluation. Real-time performance may differ slightly if positions held longer, slippage/fees not captured, or market microstructure changes.

Risk Warnings

No Guarantee of Profit: All trading involves risk of loss

System Failures: Bugs possible despite extensive testing

Market Conditions: Optimized for liquid markets (>100k daily volume). Performance degrades in illiquid instruments, major news events, flash crashes

Broker-Specific Issues: Execution slippage, commission/fees, overnight financing costs

Appropriate Use

This Indicator Is:

✅ Entry trigger system

✅ Risk management framework (stop/target)

✅ Adaptive agent selection engine

✅ Learning system that improves over time

This Indicator Is NOT:

❌ Complete trading strategy (requires position sizing, portfolio management)

❌ Replacement for fundamental analysis

❌ Guaranteed profit generator

❌ Suitable for complete beginners without training

Recommended Complementary Analysis: Market context (support/resistance), volume profile, fundamental catalysts, correlation with related instruments, broader market regime

Recommended Settings by Instrument

Stocks (Large Cap, >$1B):

Mode: Balanced | ML/RL: Enabled, Full Stack | Bandit: Thompson Sampling, Switch

Agent Sensitivity: Spoofing 1.0-1.2, Exhaustion 0.9-1.1, Liquidity 0.8-1.0, StatArb 1.1-1.3

Microstructure: All enabled, VPIN 1.2, Toxicity 1.5 | Timeframe: 15min-1H

Forex Majors (EURUSD, GBPUSD):

Mode: Balanced to Conservative | ML/RL: Enabled, Full Stack | Bandit: Thompson Sampling, Blend

Agent Sensitivity: Spoofing 0.8-1.0, Exhaustion 0.9-1.1, Liquidity 0.7-0.9, StatArb 1.2-1.5

Microstructure: All enabled, VPIN 1.0-1.1, Toxicity 1.3-1.5 | Timeframe: 5min-30min

Crypto (BTC, ETH):

Mode: Aggressive to Balanced | ML/RL: Enabled, Full Stack | Bandit: Thompson Sampling OR EXP3-IX

Agent Sensitivity: Spoofing 1.2-1.5, Exhaustion 1.1-1.3, Liquidity 1.2-1.5, StatArb 0.7-0.9

Microstructure: All enabled, VPIN 1.4-1.6, Toxicity 1.8-2.2 | Timeframe: 15min-4H

Futures (ES, NQ, CL):

Mode: Balanced | ML/RL: Enabled, Full Stack | Bandit: UCB1 or Thompson Sampling

Agent Sensitivity: All 1.0-1.2 (balanced)

Microstructure: All enabled, VPIN 1.1-1.3, Toxicity 1.4-1.6 | Timeframe: 5min-30min

Conclusion

Algorithm Predator - Pro synthesizes academic research from market microstructure theory, reinforcement learning, and multi-armed bandit algorithms. Unlike typical indicator mashups, this system implements 15 mathematically rigorous bandit algorithms, deploys a complete RL stack (Q-Learning, TD(λ), Policy Gradient), integrates institutional microstructure metrics (VPIN, Kyle's Lambda), adapts continuously through dual-layer memory and meta-learning, and provides full transparency on approximations and limitations.

The system is designed for serious algorithmic traders who understand that no indicator is perfect, but through proper machine learning, we can build systems that improve over time and adapt to changing markets without manual intervention.

Use responsibly. Risk disclosure applies. Past performance ≠ future results.

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

Algorithm Predator - ML-liteAlgorithm Predator - ML-lite

This indicator combines four specialized trading agents with an adaptive multi-armed bandit selection system to identify high-probability trade setups. It is designed for swing and intraday traders who want systematic signal generation based on institutional order flow patterns , momentum exhaustion , liquidity dynamics , and statistical mean reversion .

Core Architecture

Why These Components Are Combined:

The script addresses a fundamental challenge in algorithmic trading: no single detection method works consistently across all market conditions. By deploying four independent agents and using reinforcement learning algorithms to select or blend their outputs, the system adapts to changing market regimes without manual intervention.

The Four Trading Agents

1. Spoofing Detector Agent 🎭

Detects iceberg orders through persistent volume at similar price levels over 5 bars

Identifies spoofing patterns via asymmetric wick analysis (wicks exceeding 60% of bar range with volume >1.8× average)

Monitors order clustering using simplified Hawkes process intensity tracking (exponential decay model)

Signal Logic: Contrarian—fades false breakouts caused by institutional manipulation

Best Markets: Consolidations, institutional trading windows, low-liquidity hours

2. Exhaustion Detector Agent ⚡

Calculates RSI divergence between price movement and momentum indicator over 5-bar window

Detects VWAP exhaustion (price at 2σ bands with declining volume)

Uses VPIN reversals (volume-based toxic flow dissipation) to identify momentum failure

Signal Logic: Counter-trend—enters when momentum extreme shows weakness

Best Markets: Trending markets reaching climax points, over-extended moves

3. Liquidity Void Detector Agent 💧

Measures Bollinger Band squeeze (width <60% of 50-period average)

Identifies stop hunts via 20-bar high/low penetration with immediate reversal and volume spike

Detects hidden liquidity absorption (volume >2× average with range <0.3× ATR)

Signal Logic: Breakout anticipation—enters after liquidity grab but before main move

Best Markets: Range-bound pre-breakout, volatility compression zones

4. Mean Reversion Agent 📊

Calculates price z-scores relative to 50-period SMA and standard deviation (triggers at ±2σ)

Implements Ornstein-Uhlenbeck process scoring (mean-reverting stochastic model)

Uses entropy analysis to detect algorithmic trading patterns (low entropy <0.25 = high predictability)

Signal Logic: Statistical reversion—enters when price deviates significantly from statistical equilibrium

Best Markets: Range-bound, low-volatility, algorithmically-dominated instruments

Adaptive Selection: Multi-Armed Bandit System

The script implements four reinforcement learning algorithms to dynamically select or blend agents based on performance:

Thompson Sampling (Default - Recommended):

Uses Bayesian inference with beta distributions (tracks alpha/beta parameters per agent)

Balances exploration (trying underused agents) vs. exploitation (using proven winners)

Each agent's win/loss history informs its selection probability

Lite Approximation: Uses pseudo-random sampling from price/volume noise instead of true random number generation

UCB1 (Upper Confidence Bound):

Calculates confidence intervals using: average_reward + sqrt(2 × ln(total_pulls) / agent_pulls)

Deterministic algorithm favoring agents with high uncertainty (potential upside)

More conservative than Thompson Sampling

Epsilon-Greedy:

Exploits best-performing agent (1-ε)% of the time

Explores randomly ε% of the time (default 10%, configurable 1-50%)

Simple, transparent, easily tuned via epsilon parameter

Gradient Bandit:

Uses softmax probability distribution over agent preference weights

Updates weights via gradient ascent based on rewards

Best for Blend mode where all agents contribute

Selection Modes:

Switch Mode: Uses only the selected agent's signal (clean, decisive)

Blend Mode: Combines all agents using exponentially weighted confidence scores controlled by temperature parameter (smooth, diversified)

Lock Agent Feature:

Optional manual override to force one specific agent

Useful after identifying which agent dominates your specific instrument

Only applies in Switch mode

Four choices: Spoofing Detector, Exhaustion Detector, Liquidity Void, Mean Reversion

Memory System

Dual-Layer Architecture:

Short-Term Memory: Stores last 20 trade outcomes per agent (configurable 10-50)

Long-Term Memory: Stores episode averages when short-term reaches transfer threshold (configurable 5-20 bars)

Memory Boost Mechanism: Recent performance modulates agent scores by up to ±20%

Episode Transfer: When an agent accumulates sufficient results, averages are condensed into long-term storage

Persistence: Manual restoration of learned parameters via input fields (alpha, beta, weights, microstructure thresholds)

How Memory Works:

Agent generates signal → outcome tracked after 8 bars (performance horizon)

Result stored in short-term memory (win = 1.0, loss = 0.0)

Short-term average influences agent's future scores (positive feedback loop)

After threshold met (default 10 results), episode averaged into long-term storage

Long-term patterns (weighted 30%) + short-term patterns (weighted 70%) = total memory boost

Market Microstructure Analysis

These advanced metrics quantify institutional order flow dynamics:

Order Flow Toxicity (Simplified VPIN):

Measures buy/sell volume imbalance over 20 bars: |buy_vol - sell_vol| / (buy_vol + sell_vol)

Detects informed trading activity (institutional players with non-public information)

Values >0.4 indicate "toxic flow" (informed traders active)

Lite Approximation: Uses simple open/close heuristic instead of tick-by-tick trade classification

Price Impact Analysis (Simplified Kyle's Lambda):

Measures market impact efficiency: |price_change_10| / sqrt(volume_sum_10)

Low values = large orders with minimal price impact ( stealth accumulation )

High values = retail-dominated moves with high slippage

Lite Approximation: Uses simplified denominator instead of regression-based signed order flow

Market Randomness (Entropy Analysis):

Counts unique price changes over 20 bars / 20

Measures market predictability

High entropy (>0.6) = human-driven, chaotic price action

Low entropy (<0.25) = algorithmic trading dominance (predictable patterns)

Lite Approximation: Simple ratio instead of true Shannon entropy H(X) = -Σ p(x)·log₂(p(x))

Order Clustering (Simplified Hawkes Process):

Tracks self-exciting event intensity (coordinated order activity)

Decays at 0.9× per bar, spikes +1.0 when volume >1.5× average

High intensity (>0.7) indicates clustering (potential spoofing/accumulation)

Lite Approximation: Simple exponential decay instead of full λ(t) = μ + Σ α·exp(-β(t-tᵢ)) with MLE

Signal Generation Process

Multi-Stage Validation:

Stage 1: Agent Scoring

Each agent calculates internal score based on its detection criteria

Scores must exceed agent-specific threshold (adjusted by sensitivity multiplier)

Agent outputs: Signal direction (+1/-1/0) and Confidence level (0.0-1.0)

Stage 2: Memory Boost

Agent scores multiplied by memory boost factor (0.8-1.2 based on recent performance)

Successful agents get amplified, failing agents get dampened

Stage 3: Bandit Selection/Blending

If Adaptive Mode ON:

Switch: Bandit selects single best agent, uses only its signal

Blend: All agents combined using softmax-weighted confidence scores

If Adaptive Mode OFF:

Traditional consensus voting with confidence-squared weighting

Signal fires when consensus exceeds threshold (default 70%)

Stage 4: Confirmation Filter

Raw signal must repeat for consecutive bars (default 3, configurable 2-4)

Minimum confidence threshold: 0.25 (25%) enforced regardless of mode

Trend alignment check: Long signals require trend_score ≥ -2, Short signals require trend_score ≤ 2

Stage 5: Cooldown Enforcement

Minimum bars between signals (default 10, configurable 5-15)

Prevents over-trading during choppy conditions

Stage 6: Performance Tracking

After 8 bars (performance horizon), signal outcome evaluated

Win = price moved in signal direction, Loss = price moved against

Results fed back into memory and bandit statistics

Trading Modes (Presets)

Pre-configured parameter sets:

Conservative: 85% consensus, 4 confirmations, 15-bar cooldown

Expected: 60-70% win rate, 3-8 signals/week

Best for: Swing trading, capital preservation, beginners

Balanced: 70% consensus, 3 confirmations, 10-bar cooldown

Expected: 55-65% win rate, 8-15 signals/week

Best for: Day trading, most traders, general use

Aggressive: 60% consensus, 2 confirmations, 5-bar cooldown

Expected: 50-58% win rate, 15-30 signals/week

Best for: Scalping, high-frequency trading, active management

Elite: 75% consensus, 3 confirmations, 12-bar cooldown

Expected: 58-68% win rate, 5-12 signals/week

Best for: Selective trading, high-conviction setups

Adaptive: 65% consensus, 2 confirmations, 8-bar cooldown

Expected: Varies based on learning

Best for: Experienced users leveraging bandit system

How to Use

1. Initial Setup (5 Minutes):

Select Trading Mode matching your style (start with Balanced)

Enable Adaptive Learning (recommended for automatic agent selection)

Choose Thompson Sampling algorithm (best all-around performance)

Keep Microstructure Metrics enabled for liquid instruments (>100k daily volume)

2. Agent Tuning (Optional):

Adjust Agent Sensitivity multipliers (0.5-2.0):

<0.8 = Highly selective (fewer signals, higher quality)

0.9-1.2 = Balanced (recommended starting point)

1.3 = Aggressive (more signals, lower individual quality)

Monitor dashboard for 20-30 signals to identify dominant agent

If one agent consistently outperforms, consider using Lock Agent feature

3. Bandit Configuration (Advanced):

Blend Temperature (0.1-2.0):

0.3 = Sharp decisions (best agent dominates)

0.5 = Balanced (default)

1.0+ = Smooth (equal weighting, democratic)

Memory Decay (0.8-0.99):

0.90 = Fast adaptation (volatile markets)

0.95 = Balanced (most instruments)

0.97+ = Long memory (stable trends)

4. Signal Interpretation:

Green triangle (▲): Long signal confirmed

Red triangle (▼): Short signal confirmed

Dashboard shows:

Active agent (highlighted row with ► marker)

Win rate per agent (green >60%, yellow 40-60%, red <40%)

Confidence bars (█████ = maximum confidence)

Memory size (short-term buffer count)

Colored zones display:

Entry level (current close)

Stop-loss (1.5× ATR)

Take-profit 1 (2.0× ATR)

Take-profit 2 (3.5× ATR)

5. Risk Management:

Never risk >1-2% per signal (use ATR-based stops)

Signals are entry triggers, not complete strategies

Combine with your own market context analysis

Consider fundamental catalysts and news events

Use "Confirming" status to prepare entries (not to enter early)

6. Memory Persistence (Optional):

After 50-100 trades, check Memory Export Panel

Record displayed alpha/beta/weight values for each agent

Record VPIN and Kyle threshold values

Enable "Restore From Memory" and input saved values to continue learning

Useful when switching timeframes or restarting indicator

Visual Components

On-Chart Elements:

Spectral Layers: EMA8 ± 0.5 ATR bands (dynamic support/resistance, colored by trend)

Energy Radiance: Multi-layer glow boxes at signal points (intensity scales with confidence, configurable 1-5 layers)

Probability Cones: Projected price paths with uncertainty wedges (15-bar projection, width = confidence × ATR)

Connection Lines: Links sequential signals (solid = same direction continuation, dotted = reversal)

Kill Zones: Risk/reward boxes showing entry, stop-loss, and dual take-profit targets

Signal Markers: Triangle up/down at validated entry points

Dashboard (Configurable Position & Size):

Regime Indicator: 4-level trend classification (Strong Bull/Bear, Weak Bull/Bear)

Mode Status: Shows active system (Adaptive Blend, Locked Agent, or Consensus)

Agent Performance Table: Real-time win%, confidence, and memory stats

Order Flow Metrics: Toxicity and impact indicators (when microstructure enabled)

Signal Status: Current state (Long/Short/Confirming/Waiting) with confirmation progress

Memory Panel (Configurable Position & Size):

Live Parameter Export: Alpha, beta, and weight values per agent

Adaptive Thresholds: Current VPIN sensitivity and Kyle threshold

Save Reminder: Visual indicator if parameters should be recorded

What Makes This Original

This script's originality lies in three key innovations:

1. Genuine Meta-Learning Framework:

Unlike traditional indicator mashups that simply display multiple signals, this implements authentic reinforcement learning (multi-armed bandits) to learn which detection method works best in current conditions. The Thompson Sampling implementation with beta distribution tracking (alpha for successes, beta for failures) is statistically rigorous and adapts continuously. This is not post-hoc optimization—it's real-time learning.

2. Episodic Memory Architecture with Transfer Learning:

The dual-layer memory system mimics human learning patterns:

Short-term memory captures recent performance (recency bias)

Long-term memory preserves historical patterns (experience)

Automatic transfer mechanism consolidates knowledge

Memory boost creates positive feedback loops (successful strategies become stronger)

This architecture allows the system to adapt without retraining , unlike static ML models that require batch updates.

3. Institutional Microstructure Integration:

Combines retail-focused technical analysis (RSI, Bollinger Bands, VWAP) with institutional-grade microstructure metrics (VPIN, Kyle's Lambda, Hawkes processes) typically found in academic finance literature and professional trading systems, not standard retail platforms. While simplified for Pine Script constraints, these metrics provide insight into informed vs. uninformed trading , a dimension entirely absent from traditional technical analysis.

Mashup Justification:

The four agents are combined specifically for risk diversification across failure modes:

Spoofing Detector: Prevents false breakout losses from manipulation

Exhaustion Detector: Prevents chasing extended trends into reversals

Liquidity Void: Exploits volatility compression (different regime than trending)

Mean Reversion: Provides mathematical anchoring when patterns fail

The bandit system ensures the optimal tool is automatically selected for each market situation, rather than requiring manual interpretation of conflicting signals.

Why "ML-lite"? Simplifications and Approximations

This is the "lite" version due to necessary simplifications for Pine Script execution:

1. Simplified VPIN Calculation:

Academic Implementation: True VPIN uses volume bucketing (fixed-volume bars) and tick-by-tick buy/sell classification via Lee-Ready algorithm or exchange-provided trade direction flags

This Implementation: 20-bar rolling window with simple open/close heuristic (close > open = buy volume)

Impact: May misclassify volume during ranging/choppy markets; works best in directional moves

2. Pseudo-Random Sampling:

Academic Implementation: Thompson Sampling requires true random number generation from beta distributions using inverse transform sampling or acceptance-rejection methods

This Implementation: Deterministic pseudo-randomness derived from price and volume decimal digits: (close × 100 - floor(close × 100)) + (volume % 100) / 100

Impact: Not cryptographically random; may have subtle biases in specific price ranges; provides sufficient variation for agent selection

3. Hawkes Process Approximation:

Academic Implementation: Full Hawkes process uses maximum likelihood estimation with exponential kernels: λ(t) = μ + Σ α·exp(-β(t-tᵢ)) fitted via iterative optimization

This Implementation: Simple exponential decay (0.9 multiplier) with binary event triggers (volume spike = event)

Impact: Captures self-exciting property but lacks parameter optimization; fixed decay rate may not suit all instruments

4. Kyle's Lambda Simplification:

Academic Implementation: Estimated via regression of price impact on signed order flow over multiple time intervals: Δp = λ × Δv + ε

This Implementation: Simplified ratio: price_change / sqrt(volume_sum) without proper signed order flow or regression

Impact: Provides directional indicator of impact but not true market depth measurement; no statistical confidence intervals

5. Entropy Calculation:

Academic Implementation: True Shannon entropy requires probability distribution: H(X) = -Σ p(x)·log₂(p(x)) where p(x) is probability of each price change magnitude

This Implementation: Simple ratio of unique price changes to total observations (variety measure)

Impact: Measures diversity but not true information entropy with probability weighting; less sensitive to distribution shape

6. Memory System Constraints:

Full ML Implementation: Neural networks with backpropagation, experience replay buffers (storing state-action-reward tuples), gradient descent optimization, and eligibility traces

This Implementation: Fixed-size array queues with simple averaging; no gradient-based learning, no state representation beyond raw scores

Impact: Cannot learn complex non-linear patterns; limited to linear performance tracking

7. Limited Feature Engineering:

Advanced Implementation: Dozens of engineered features, polynomial interactions (x², x³), dimensionality reduction (PCA, autoencoders), feature selection algorithms

This Implementation: Raw agent scores and basic market metrics (RSI, ATR, volume ratio); minimal transformation

Impact: May miss subtle cross-feature interactions; relies on agent-level intelligence rather than feature combinations

8. Single-Instrument Data:

Full Implementation: Multi-asset correlation analysis (sector ETFs, currency pairs, volatility indices like VIX), lead-lag relationships, risk-on/risk-off regimes

This Implementation: Only OHLCV data from displayed instrument

Impact: Cannot incorporate broader market context; vulnerable to correlated moves across assets

9. Fixed Performance Horizon:

Full Implementation: Adaptive horizon based on trade duration, volatility regime, or profit target achievement

This Implementation: Fixed 8-bar evaluation window

Impact: May evaluate too early in slow markets or too late in fast markets; one-size-fits-all approach

Performance Impact Summary:

These simplifications make the script:

✅ Faster: Executes in milliseconds vs. seconds (or minutes) for full academic implementations

✅ More Accessible: Runs on any TradingView plan without external data feeds, APIs, or compute servers

✅ More Transparent: All calculations visible in Pine Script (no black-box compiled models)

✅ Lower Resource Usage: <500 bars lookback, minimal memory footprint

⚠️ Less Precise: Approximations may reduce statistical edge by 5-15% vs. academic implementations

⚠️ Limited Scope: Cannot capture tick-level dynamics, multi-order-book interactions, or cross-asset flows

⚠️ Fixed Parameters: Some thresholds hardcoded rather than dynamically optimized

When to Upgrade to Full Implementation: