Major Crypto Relative Strength Portfolio System Majors RSPS - Relative Strength Portfolio System for Major Cryptocurrencies

Overview

Majors RSPS (Relative Strength Portfolio System) is an advanced portfolio allocation indicator that combines relative strength analysis, trend consensus, and macro risk factors to dynamically allocate capital across major cryptocurrency assets. The system leverages the NormalizedIndicators Library to evaluate both absolute trends and relative performance, creating an adaptive portfolio that automatically adjusts exposure based on market conditions.

This indicator is designed for portfolio managers, asset allocators, and systematic traders who want a data-driven approach to cryptocurrency portfolio construction with automatic rebalancing signals.

🎯 Core Concept

What is RSPS?

RSPS (Relative Strength Portfolio System) evaluates each asset on two key dimensions:

Relative Strength: How is the asset performing compared to other major cryptocurrencies?

Absolute Trend: Is the asset itself in a bullish trend?

Assets that show both strong relative performance AND positive absolute trends receive higher allocations. Weak performers are automatically filtered out, with capital reallocated to cash or stronger assets.

Dual-Layer Architecture

Layer 1: Majors Portfolio (Orange Zone)

Evaluates 14 major cryptocurrency assets

Calculates relative strength against all other majors

Applies trend filters to ensure absolute momentum

Dynamically allocates capital based on comparative strength

Layer 2: Cash/Risk Position (Navy Zone)

Evaluates macro risk factors and market conditions

Determines optimal cash allocation

Acts as a risk-off mechanism during adverse conditions

Provides downside protection through dynamic cash holdings

📊 Tracked Assets

Major Cryptocurrencies (14 Assets)

BTC - Bitcoin (Benchmark L1)

ETH - Ethereum (Smart Contract L1)

SOL - Solana (High-Performance L1)

SUI - Sui (Move-Based L1)

TRX - Tron (Payment-Focused L1)

BNB - Binance Coin (Exchange L1)

XRP - Ripple (Payment Network)

FTM - Fantom (DeFi L1)

CELO - Celo (Mobile-First L1)

TAO - Bittensor (AI Network)

HYPE - Hyperliquid (DeFi Exchange)

HBAR - Hedera (Enterprise L1)

ADA - Cardano (Research-Driven L1)

THETA - Theta (Video Network)

🔧 How It Works

Step 1: Relative Strength Calculation

For each asset, the system calculates relative strength by:

RSPS Score = Average of:

- Asset/BTC trend consensus

- Asset/ETH trend consensus

- Asset/SOL trend consensus

- Asset/SUI trend consensus

- ... (all 14 pairs)

- Asset's absolute trend consensus

Key Logic:

Each pair is evaluated using the eth_4d_cal() calibration from NormalizedIndicators

If an asset's absolute trend is extremely weak (≤ 0.1), it receives a penalty score (-0.5)

Otherwise, it gets the average of all its relative strength comparisons

Step 2: Trend Filtering

Assets must pass a trend filter to receive allocation:

Trend Score = Average of:

- Asset/BTC trend (filtered for positivity)

- Asset/ETH trend (filtered for positivity)

- Asset's absolute trend (filtered for positivity)

Only positive values contribute to the trend score, ensuring bearish assets don't receive allocation.

Step 3: Portfolio Allocation

Capital is allocated proportionally based on filtered RSPS scores:

Asset Allocation % = (Asset's Filtered RSPS Score / Sum of All Filtered Scores) × Main Portfolio %

Example:

SOL filtered score: 0.6

BTC filtered score: 0.4

All others: 0

Total: 1.0

SOL receives: (0.6 / 1.0) × Main% = 60% of main portfolio

BTC receives: (0.4 / 1.0) × Main% = 40% of main portfolio

Step 4: Cash/Risk Allocation

The system evaluates macro conditions across 6 factors:

Inverse Major Crypto Trends (40% weight)

When BTC, ETH, SOL, SUI, DOGE, etc. trend down → Cash allocation increases

Evaluates total market cap trends (TOTAL, TOTAL2, OTHERS)

Stablecoin Dominance (10% weight)

USDC dominance vs. major crypto dominances

Higher stablecoin dominance → Higher cash allocation

MVRV Ratios (10% weight)

BTC and ETH Market Value to Realized Value

High MVRV (overvaluation) → Higher cash allocation

BTC/ETH Ratio (15% weight)

Relative performance between two market leaders

Indicates market phase (BTC dominance vs. alt season)

Active Address Ratios (5% weight)

USDC active addresses vs. BTC/ETH active addresses

Network activity comparison

Macro Indicators (15% weight)

Global currency circulation (USD, EUR, CNY, JPY)

Treasury yield curve (10Y-2Y)

High yield spreads

Central bank balance sheets and money supply

Cash Allocation Formula:

Cash % = (Sum of Risk Factors × 0.5) / (Risk Factors + Majors TPI)

When risk factors are elevated, cash allocation increases, reducing exposure to volatile assets.

📈 Visual Components

Orange Zone (Majors Portfolio)

Fill: Light orange area showing aggregate portfolio strength

Line: Average trend power index (TPI) of allocated assets

Baseline: 0 level (neutral)

Interpretation:

Above 0: Bullish allocation environment

Rising: Strengthening portfolio momentum

Falling: Weakening portfolio momentum

Below 0: No allocation (100% cash)

Navy Zone (Cash Position)

Fill: Navy blue area showing cash allocation strength

Line: Risk-adjusted cash allocation signal

Baseline: 0 level

Interpretation:

Higher navy zone: Elevated risk-off signal → More cash

Lower navy zone: Risk-on environment → Less cash

Zero: No cash allocation (100% invested)

Performance Line (Orange/Blue)

Orange: Main portfolio allocation dominant (risk-on mode)

Blue: Cash allocation dominant (risk-off mode)

Tracks: Cumulative portfolio returns with dynamic rebalancing

Allocation Table (Bottom Left)

Shows real-time portfolio composition:

ColumnDescriptionAssetCryptocurrency nameRSPS ValuePercentage allocation (of main portfolio)CashDollar amount (if enabled)

Color Coding:

Orange: Active allocation

Gray: Weak signal (borderline)

Blue: Cash position

Missing: No allocation (filtered out)

⚙️ Settings & Configuration

Required Setup

Chart Symbol

MUST USE: INDEX:BTCUSD or similar major crypto index

Recommended Timeframe: 1D (Daily) or 4D (4-Day)

Why: System needs price data for all 14 majors, BTC provides stable reference

Hide Chart Candles

For clean visualization:

Right-click on chart

Select "Hide Symbol" or set candle opacity to 0

This allows the indicator fills and table to be clearly visible

User Inputs

plot_table (Default: true)

Enable/disable the allocation table

Set to false if you only want the visual zones

use_cash (Default: false)

Enable portfolio dollar value calculations

Shows actual dollar allocations per asset

cash (Default: 100)

Total portfolio size in dollars/currency units

Used when use_cash is enabled

Example: Set to 10000 for a $10,000 portfolio

💡 Interpretation Guide

Entry Signals

Strong Allocation Signal:

✓ Orange zone elevated (> 0.3)

✓ Navy zone low (< 0.2)

✓ Performance line orange

✓ Multiple assets in allocation table

→ Action: Deploy capital to allocated assets per table percentages

Risk-Off Signal:

✓ Orange zone near zero

✓ Navy zone elevated (> 0.4)

✓ Performance line blue

✓ Few or no assets in table (high cash %)

→ Action: Reduce exposure, increase cash holdings

Rebalancing Triggers

Monitor the allocation table for changes:

New assets appearing: Add to portfolio

Assets disappearing: Remove from portfolio

Percentage changes: Rebalance existing positions

Cash % changes: Adjust overall exposure

Market Regime Detection

Risk-On (Bull Market):

Orange zone high and rising

Navy zone minimal

Many assets allocated (8-12)

High individual allocations (15-30% each)

Risk-Off (Bear Market):

Orange zone near zero or negative

Navy zone elevated

Few assets allocated (0-3)

Cash allocation dominant (70-100%)

Transition Phase:

Both zones moderate

Medium number of assets (4-7)

Balanced cash/asset allocation (40-60%)

🎯 Trading Strategies

Strategy 1: Pure RSPS Following

1. Check allocation table daily

2. Rebalance portfolio to match percentages

3. Follow cash allocation strictly

4. Review weekly, act on significant changes (>5%)

Best For: Systematic portfolio managers, passive allocators

Strategy 2: Threshold-Based

Entry Rules:

- Orange zone > 0.4 AND Navy zone < 0.3

- At least 5 assets in allocation table

- Total non-cash allocation > 60%

Exit Rules:

- Orange zone < 0.1 OR Navy zone > 0.5

- Fewer than 3 assets allocated

- Cash allocation > 70%

Best For: Active traders wanting clear rules

Strategy 3: Relative Strength Overlay

1. Use RSPS for broad allocation framework

2. Within allocated assets, overweight top 3 performers

3. Scale position sizes by RSPS score

4. Use individual asset charts for entry/exit timing

Best For: Discretionary traders with portfolio focus

Strategy 4: Risk-Adjusted Position Sizing

For each allocated asset:

Position Size = Base Position × (Asset's RSPS Score / Max RSPS Score) × (1 - Cash Allocation)

Example:

- $10,000 portfolio

- SOL RSPS: 0.6 (highest)

- BTC RSPS: 0.4

- Cash allocation: 30%

SOL Size = $10,000 × (0.6/0.6) × (1-0.30) = $7,000

BTC Size = $10,000 × (0.4/0.6) × (1-0.30) = $4,667

Cash = $10,000 × 0.30 = $3,000

Best For: Risk-conscious allocators

📊 Advanced Usage

Multi-Timeframe Confirmation

Use on multiple timeframes for robust signals:

1D Chart: Tactical allocation (daily rebalancing)

4D Chart: Strategic allocation (weekly review)

Strong Confirmation:

- Both timeframes show same top 3 assets

- Both show similar cash allocation levels

- Orange zones aligned on both

Weak/Conflicting:

- Different top performers

- Diverging cash allocations

→ Wait for alignment or use shorter timeframe

Sector Rotation Analysis

Group assets by type and watch rotation:

L1 Dominance: BTC, ETH, SOL, SUI, ADA high → Layer 1 season

Alt L1s: TRX, FTM, CELO rising → Alternative platform season

Specialized: TAO, THETA, HYPE strong → Niche narrative season

Payment/Stable: XRP, BNB allocation → Risk reduction phase

Divergence Trading

Bullish Divergence:

Navy zone declining (less risk-off)

Orange zone flat or slightly rising

Few assets still allocated but strengthening

→ Early accumulation signal

Bearish Divergence:

Orange zone declining

Navy zone rising

Asset count decreasing in table

→ Distribution/exit signal

Performance Tracking

The performance line (overlay) shows cumulative strategy returns:

Compare to BTC/ETH: Is RSPS outperforming?

Drawdown analysis: How deep are pullbacks?

Correlation: Does it track market or provide diversification?

🔬 Technical Details

Data Sources

Price Data:

COINEX: Primary exchange for alt data

CRYPTO: Alternative price feeds

INDEX: Aggregated index prices (recommended for BTC)

Macro Data:

Dominance metrics (SUI.D, BTC.D, etc.)

MVRV ratios (on-chain valuation)

Active addresses (network activity)

Global money supply and macro indicators

Calculation Methodology

RSPS Scoring:

For each asset, calculate 14 relative trends (vs. all others)

Calculate asset's absolute trend

Average all 15 values

Apply penalty filter for extremely weak trends (≤ 0.1)

Trend Consensus:

Uses eth_4d_cal() from NormalizedIndicators library

Combines 8 normalized indicators per measurement

Returns value from -1 (bearish) to +1 (bullish)

Performance Calculation:

Daily Return = Σ(Asset ROC × Asset Allocation)

Cumulative Performance = Previous Perf × (1 + Daily Return / 100)

Assumes perfect rebalancing and no slippage (theoretical performance).

Filtering Logic

filter() function:

pinescriptfilter(input) => input >= 0 ? input : 0

This zero-floor filter ensures:

Only positive trend values contribute to allocation

Bearish assets receive 0 weight

No short positions or inverse allocations

Anti-Manipulation Safeguards

Null Handling:

All values wrapped in nz() to handle missing data

Prevents calculation errors from data gaps

Normalization:

Allocations always sum to 100%

Prevents over/under-allocation

Conditional Logic:

Assets need positive values on multiple metrics

Single metric cannot drive allocation alone

⚠️ Important Considerations

Required Timeframes

1D (Daily): Recommended for most users

4D (4-Day): More stable, fewer rebalances

Other timeframes: Use at your own discretion, may require recalibration

Data Requirements

Needs INDEX:BTCUSD or equivalent major crypto symbol

All 14 tracked assets must have available data

Macro indicators require specific TradingView data feeds

Rebalancing Frequency

System provides daily allocation updates

Practical rebalancing: Weekly or on significant changes (>10%)

Consider transaction costs and tax implications

Performance Notes

Theoretical returns: No slippage, fees, or execution delays

Backtest carefully: Validate on your specific market conditions

Past performance: Does not guarantee future results

Risk Warnings

⚠️ High Concentration Risk: May allocate heavily to 1-3 assets

⚠️ Volatility: Crypto markets are inherently volatile

⚠️ Liquidity: Some allocated assets may have lower liquidity

⚠️ Correlation: All assets correlated to BTC/ETH to some degree

⚠️ System Risk: Relies on continued availability of data feeds

Not Financial Advice

This indicator is a tool for analysis and research. It does not constitute:

Investment advice

Portfolio management services

Trading recommendations

Guaranteed returns

Always perform your own due diligence and risk assessment.

🎓 Use Cases

For Portfolio Managers

Systematic allocation framework

Objective rebalancing signals

Risk-adjusted exposure management

Performance tracking vs. benchmarks

For Active Traders

Identify strongest assets to focus trading on

Gauge overall market regime (risk-on/off)

Time entry/exit for portfolio shifts

Complement technical analysis with allocation data

For Institutional Allocators

Quantitative portfolio construction

Multi-asset exposure optimization

Drawdown management through cash allocation

Compliance-friendly systematic approach

For Researchers

Study relative strength dynamics in crypto markets

Analyze correlation between majors

Test macro factor impact on crypto allocations

Develop derived strategies and signals

🔧 Setup Checklist

✅ Chart Configuration

Set chart to INDEX:BTCUSD

Set timeframe to 1D or 4D

Hide chart candles for clean visualization

Add indicator from library

✅ Indicator Settings

Enable plot_table (see allocation table)

Set use_cash if tracking dollar amounts

Input your portfolio size in cash parameter

✅ Monitoring Setup

Bookmark chart for daily review

Set alerts for major allocation changes (optional)

Create spreadsheet to track allocations (optional)

Establish rebalancing schedule (weekly recommended)

✅ Validation

Verify all 14 assets appear in table (when allocated)

Check that percentages sum to ~100%

Confirm performance line is tracking

Test cash allocation calculation if enabled

📋 Quick Reference

Signal Interpretation

ConditionOrange ZoneNavy ZoneActionStrong BullHigh (>0.4)Low (<0.2)Full allocationModerate BullMid (0.2-0.4)Low-MidStandard allocationNeutralLow (0.1-0.2)Mid (0.3-0.4)Balanced allocationModerate BearVery Low (<0.1)Mid-HighReduce exposureStrong BearZero/NegativeHigh (>0.5)High cash/exit

Rebalancing Thresholds

Change TypeThresholdActionIndividual asset±5%Consider rebalanceIndividual asset±10%Strongly rebalanceCash allocation±10%Adjust exposureAsset entry/exitAnyAdd/remove position

Color Legend

Orange: Main portfolio strength/allocation

Navy: Cash/risk-off allocation

Blue text: Cash position in table

Orange text: Active asset allocation

Gray text: Weak/borderline allocation

White: Headers and labels

🚀 Getting Started

Beginner Path

Add indicator to INDEX:BTCUSD daily chart

Hide candles for clarity

Enable plot_table to see allocations

Check table daily, note top 3-5 assets

Start with small allocation, observe behavior

Gradually increase allocation as you gain confidence

Intermediate Path

Set up on both 1D and 4D charts

Enable use_cash with your portfolio size

Create tracking spreadsheet

Implement weekly rebalancing schedule

Monitor divergences between timeframes

Compare performance to buy-and-hold BTC

Advanced Path

Modify code to add/remove tracked assets

Adjust relative strength calculation methodology

Customize cash allocation factors and weights

Integrate with portfolio management platform

Develop algorithmic rebalancing system

Create alerts for specific allocation conditions

📖 Additional Resources

Related Indicators

NormalizedIndicators Library: Core calculation engine

Individual asset trend indicators for deeper analysis

Macro indicator dashboards for cash allocation factors

Complementary Analysis

On-chain metrics (MVRV, active addresses, etc.)

Order book liquidity for execution planning

Correlation matrices for diversification analysis

Volatility indicators for position sizing

Learning Materials

Study relative strength portfolio theory

Research tactical asset allocation strategies

Understand crypto market cycles and phases

Learn about risk management in volatile assets

🎯 Key Takeaways

✅ Systematic allocation across 14 major cryptocurrencies

✅ Dual-layer approach: Asset selection + Cash management

✅ Relative strength focused: Invests in comparatively strong assets

✅ Trend filtering: Only allocates to assets in positive trends

✅ Dynamic rebalancing: Automatically adjusts to market conditions

✅ Risk-managed: Increases cash during adverse conditions

✅ Transparent methodology: Clear calculation logic

✅ Practical visualization: Easy-to-read table and zones

✅ Performance tracking: See cumulative strategy returns

✅ Highly customizable: Adjust assets, weights, and factors

📋 License

This code is subject to the Mozilla Public License 2.0 at mozilla.org

Majors RSPS transforms complex multi-asset portfolio management into a systematic, data-driven process. By combining relative strength analysis with trend consensus and macro risk factors, it provides traders and portfolio managers with a robust framework for navigating cryptocurrency markets with discipline and objectivity.WiederholenClaude kann Fehler machen. Bitte überprüfen Sie die Antworten. Sonnet 4.5

Manajemen portofolio

Price Drop CounterThe Price Drop Counter is a very basic statistical indicator.

See it as an analytical tool that tracks how many times an asset's price has dropped by a specified percentage from its recent peak within a defined date range.

The indicator monitors the highest price reached and counts each occurrence when the price falls by your chosen threshold, then resets its peak tracking point after each drop is registered.

Uses

Volatility Assessment: Measure how frequently significant price corrections occur during specific periods

Market Behavior Analysis: Compare drop frequency across different timeframes or market conditions

Risk Evaluation: Identify assets or periods with higher downside volatility

Historical Pattern Recognition: Study how often major pullbacks happened during bull or bear markets

Backtesting Support: Analyze how your strategy would perform based on the frequency of drawdowns

How to use it

Add the indicator to your TradingView chart

Configure the Percent Drop (%) to define your threshold (default: 10%). The indicator will count each time price falls by this percentage from the most recent high

IMPORTANT Set your Start Date and End Date to analyze a specific period of interest

The blue step-line plot shows the cumulative count of drops within your date range

Adjust the percentage threshold based on your analysis needs - use smaller values (2-5%) for more frequent signals or larger values (15-20%) for major corrections only

The counter resets its high-water mark after each qualifying drop, allowing it to track multiple sequential drops within the same period.

Rendement périodes (finary compass)Rendement sur une période donnée,

Outil de décision pour stratégie Momentum

Expsoure Guide by Tradewith_GaryDaily Guide for exposure building. Use this Indicator to improve your profitability by avoiding over-trading and picking the best days to initiate new trades. Valid only for swing trading format.

ATR Risk Display - Multi FuturesWhat This Does

I got tired of manually calculating my ATR stops and risk for different futures contracts, especially when switching between ES, NQ, and their micro versions. This indicator automatically detects what futures symbol you're trading and shows you the exact tick count and dollar risk for your stop loss.

The Problem It Solves

If you trade futures with ATR-based stops, you know the hassle:

Different contracts have different tick values

You need to calculate position risk in dollars

Switching between symbols means redoing all the math

Renko charts make it even more confusing since ATR needs to come from regular candles

This handles all of that automatically.

Key Features

Auto-detects futures symbols - ES, NQ, YM, RTY, GC, CL, and all the micros (MES, MNQ, etc.)

Shows everything you need in one line: ATR(timeframe) × multiplier = X ticks ($XXX)

Works on Renko charts - pulls ATR from regular timeframe charts (super important if you use Renko)

Adjustable position sizing - set your contract count and see total risk instantly

Clean, minimal display - just the info you need, no clutter

How to Use

Add it to any futures chart

Set your preferred ATR timeframe (I use 5-minute)

Set your ATR multiplier (I use 1.5x for my stops)

Set your contract size

That's it - the indicator handles the rest

The display will show something like: "ES ATR(5) × 1.5 = 12 ticks ($150)"

Settings Explained

ATR Timeframe: What timeframe to calculate ATR from (always uses regular candles, even on Renko)

ATR Multiplier: How many ATRs for your stop (1.5 is common, 2.0 for wider stops)

Number of Contracts: Your position size for risk calculation

Auto-Detect Symbol: Leave on unless you want to manually override

Supported Futures

Full size: ES, NQ, YM, RTY, GC, CL, ZB, ZN, 6E, 6J

Micros: MES, MNQ, MYM, M2K, MGC, MCL

Notes

Made this primarily for my own ES trading but figured others might find it useful

The tick values are based on standard CME specs

If you trade other futures, you can modify the code to add them

Works great alongside level indicators for risk management

Why This Exists

I use ATR trailing stops on all my trades and got tired of doing mental math every time I switched between charts or contracts. Especially useful if you trade both full-size and micro contracts - the risk difference is huge and easy to mess up.

Hope this helps your trading! Feel free to suggest improvements.

BEMFUNDING MAX LOT CALCULATION (Sakince)You can use this indicator to ensure you don't exceed the "Maximum Lot" limit. Because the required data varies from pair to pair, you should obtain the latest information from the BEM Funding platform.

Top 20 Screener📘 Indicator Description: I Top 20 Screener

Name:

Top 20 Screener

✅ 1. Features

This screener is designed to monitor and evaluate up to 20 selected IDX (Indonesia Stock Exchange) stocks using technical indicators. It offers a compact and visual table on your chart.

🔧 2. How to Use

Apply the Indicator

Add the indicator to your TradingView chart.

Make sure the timeframe and chart symbol are set correctly (usually apply it to any chart, as it requests data from the 20 symbols independently).

Choose Stocks to Screen

Under the “Symbols” section, check the stocks you want to include (default includes all 20).

Use the Filter Panel (Optional)

Turn on "Filter Enabled".

Choose a Filter Column (e.g., MACD > 0).

Set the "From" and "To" values to filter conditions (e.g., From = 1, To = 1 to show only MACD-positive stocks).

Interpret the Table

Each row shows one stock and its current technical status based on the selected indicators.

Green backgrounds mean bullish signals.

Red or gray indicate bearish or neutral.

📝 3. Remarks

This script uses request.security() to fetch external symbol data — it may lag slightly or be restricted in real-time depending on your plan.

Customizable Symbol List: You can edit the list to monitor any other stocks (IDX or non-IDX).

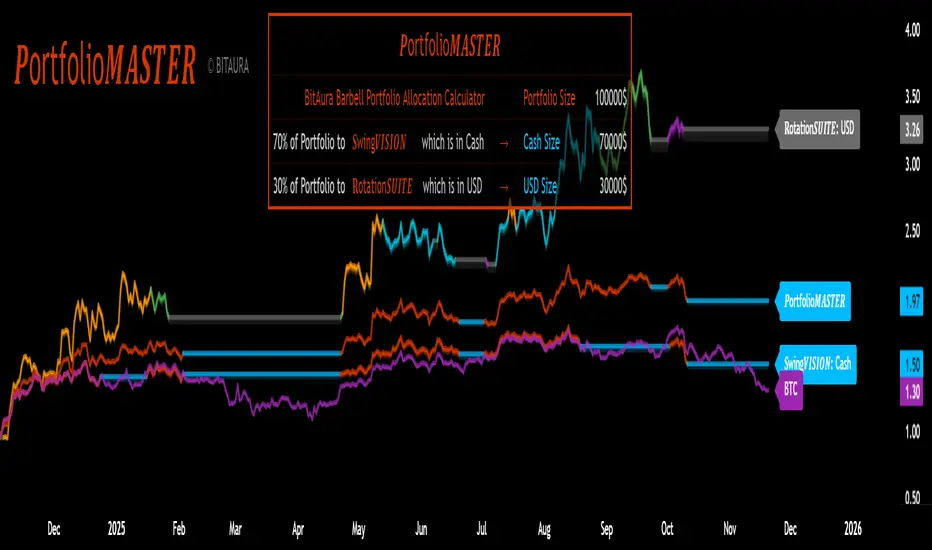

𝑷ortfolio𝑴𝑨𝑺𝑻𝑬𝑹 [BitAura]𝑷ortfolio𝑴𝑨𝑺𝑻𝑬𝑹

This Pine Script® indicator is meant to be used to manage a Barbell Portfolio composed of BitAura's various strategies in order to create a risk-reward balance for the investor's needs. The Portfolio is divided in two main parts, one being a lower-risk Bitcoin-only strategy while the other being the higher-risk, higher-reward 𝐑otation𝑺𝑼𝑰𝑻𝑬 V3 system. The user can choose the percentage splits between these two systems and then also configure them based on their risk profile.

Logic and Core Concepts

The 𝑷ortfolio𝑴𝑨𝑺𝑻𝑬𝑹 System uses the Barbell Portfolio theory to create a portfolio taylored for the final user and automatically calculates dollar allocation based on inputted settings.

Features

𝐑otation𝑺𝑼𝑰𝑻𝑬 : our advanced Strategy which allocates to the strongest asset amongst a pool of 4 Major Crypto Tokens, or de-risk to USD when these lack momentum.

BItcoin-only Strategy : This is theoretically a lower-risk system compared to 𝐑otation𝑺𝑼𝑰𝑻𝑬 and is made out of Universal Trend Following strategies. There are two variants, one being a Long-Term strategy (𝐂ycle𝑽𝑰𝑺𝑰𝑶𝑵) while the other one being of Medium-Term speed (𝐒wing𝑽𝑰𝑺𝑰𝑶𝑵).

Customizable Inputs : Allows users to adjust table settings, backtest date ranges, portfolio splits and portfolio dollar allocations.

Visual Outputs :

Allocation Table : Displays calculated allocation to each system based on user settings.

Equity Plots : Plots the Barbell Portfolio performance along with the two individual systems equities and allow comparisons between them and to Bitcoin Buy & Hold.

Color Presets : Offers five color themes (e.g., Arctic Blast, Fire vs. Ice) or custom color options for long/cash signals.

Pine Script v6 : Leverages matrices, tables, and gradient coloring for enhanced usability.

How to Use

Add to Chart : Apply the indicator to any chart on the 1D timeframe. The ticker doesn't matter as it doesn't affect the calculations, just make sure the ticker start date is earlier than the Backtest Start date applied in the script settings.

Input Portfolio size : Adjust the Dollar Portfolio size in the script settings in order to obtain accurate Portfolio Allocations in the respective table. Note that BitAura can't and won't be able to access your portfolio size.

Choose Barbell Split : Adjust based on your risk-profile how much to allocate to your preferred Bitcoin Strategy (default 70%) and how much to allocate to 𝐑otation𝑺𝑼𝑰𝑻𝑬 (default 30%).

Configure Systems : Select your preferred allocation type for 𝐑otation𝑺𝑼𝑰𝑻𝑬. Aggressive allocates 100% to the dominant asset, Moderate allocates 80% to the dominant asset and 20% to the second strongest one while Conservative does a 60/40 split between the first two assets.

Configure Settings : Adjust backtest start date (default: 31 Oct 2024) to properly track the Portfolio's performance.

Select Color Theme : Choose a preset color mode (e.g., Arctic Blast) or enable custom colors in the Colors group.

Monitor Outputs : Check the Table for Allocations and system signals, and view the equity curves to view the portfolio's performance.

Notes

The script is closed-source.

The script avoids lookahead bias by using barmerge.lookahead_off in request.security() calls.

The BitAura watermark can be toggled in the Script Settings .

Disclaimer : This script is for educational and analytical purposes only and does not constitute financial advice. Investing involves significant risk, and past performance is not indicative of future results. Always conduct your own research and apply proper risk management.

Kalkulator Pozycji — Auto Pip Point kalkulator wyznacza pozycje na podstawie ryzyka podanego w procentach

Checklist (D1 / H4 / M15/30 BoS / VP / Fibo / S/R) This is a simple, visual checklist indicator that allows you to quickly assess how many of your strategy conditions are met, without affecting the chart itself. It is ideal for multi-timeframe strategies and point-by-point setup monitoring.

Tactical Holding [SwissAlgo]Tactical Holding

A visual framework for managing long-term positions across market cycles

--------------------------------------------------------------

Purpose

Instead of holding a fixed position through all market conditions , you can use this framework to adjust your exposure tactically . By reducing positions during distribution phases and accumulating during favorable accumulation zones, you may end up holding more units of the asset over complete market cycles - even if you temporarily exit or reduce exposure during unfavorable periods. This approach aims to help you compound your holdings by taking advantage of market volatility rather than simply enduring it.

--------------------------------------------------------------

Recommended Settings

Timeframe : Weekly (1W) chart

Chart Type : Standard candlesticks (select 'Bar' type Candles)

This indicator is designed for higher timeframe analysis. While it can be applied to other timeframes, the logic and signal generation are optimized for weekly charts to filter out short-term noise and focus on major market cycles.

--------------------------------------------------------------

Key Features

♦ Market State Classification

The indicator aims to categorize potential market conditions into five color-coded states based on technical confluences:

* Bull (bright green): Multiple bullish indicators align

* Bull Retrace (teal): Bullish structure with temporary weakness

* Bull ⇆ Bear Reversal (yellow): Transitional phase between trends

* Bear (bright red): Multiple bearish indicators align

* Bear Retrace (Pale Red/Maroon): Bearish structure with temporary strength

♦ Visual Elements

* Candles change color based on the current market state

* A 50-period EMA tracks with the same color coding, providing visual trend context

* Small arrow markers appear when specific pattern conditions are met (zones for potential distribution or accumulation)

* A legend table (toggle on/off) explains the color system

* A label shows the current state name on the chart

♦ Pattern Recognition

The system monitors for two types of potential entry/exit zones:

1. State transition patterns after periods of market regime consistency

2. RSI divergence patterns (when price and momentum move in opposite directions)

♦ Customization

* Toggle the legend table visibility through settings

* All calculations are transparent and use standard technical analysis methods

--------------------------------------------------------------

How It Works

Think of this indicator as a traffic light system for your portfolio:

♦ Green zones suggest the asset might be in an environment where long-term holders historically have remained invested

Bright green (Bull) : Multiple technical indicators align in a potentially strong bullish phase

Pale green (Bull Retrace) : Bullish structure remains intact, but momentum shows temporary weakness - often a pullback within an uptrend

♦ Red zones suggest conditions where long-term holders might consider reducing exposure or waiting for better entry points

Dark red (Bear) : Multiple technical indicators align in a potentially strong bearish phase

Pale red (Bear Retrace) : Bearish structure remains intact but shows temporary strength - often a bounce within a downtrend

♦ Yellow zones indicate the market is in transition between bull and bear regimes - a time for increased attention as the trend direction becomes uncertain

The system doesn't predict future prices. Instead, it helps you understand the current technical environment by doing the heavy lifting of analyzing multiple indicators at once and presenting them in a simple visual format.

Example: During the 2022 crypto bear market, the indicator would have displayed extended red periods, signaling defensive conditions for holders. When accumulation arrows appeared in late 2022-early 2023, it highlighted potential re-entry zones as the technical regime transitioned back toward green, before the 2024 recovery.

--------------------------------------------------------------

Who This Is For

♦ Long-term investors who want to hold assets through cycles but prefer a systematic approach to position sizing and timing rather than buying and never selling .

♦ Portfolio managers looking for a visual tool to help determine when to increase or decrease exposure to specific assets based on technical regime changes.

♦ Swing traders on higher timeframes who want to align their positions with the broader market structure rather than fighting the trend.

This is not designed for:

* Day traders or scalpers

* Those seeking exact entry/exit prices

* Automated trading systems (this is a visual decision-support tool)

--------------------------------------------------------------

Understanding the Visuals

When you apply Tactical Holding to a chart, you'll see:

1. Colored candles - Instantly see what market regime the asset is in

2. Colored EMA line (thick line) - Provides a dynamic support/resistance reference that changes color with market conditions

3. Small arrows (↑ ↓) - Mark bars where specific technical patterns complete

4. State label - Shows current market classification

5. Legend table (top right) - Quick reference guide for the color system

6. Warning banner (top center) - Reminds you to use weekly charts

The visual design prioritizes clarity over complexity. You should be able to glance at a chart and immediately understand the current technical environment.

--------------------------------------------------------------

Important Limitations

This indicator cannot:

* Predict future price movements

* Guarantee profitable trades

* Work equally well on all assets or timeframes

* Replace your own research and risk management

Technical considerations:

* Divergence detection has a 3-bar confirmation lag (by design, to avoid false signals)

* State transitions require multiple technical confirmations, which may cause delayed reactions to rapid market changes

* The system is reactive, not predictive - it responds to price action after it occurs

* Performance varies significantly between trending assets (like Solana) and stable assets (like Apple)

--------------------------------------------------------------

Practical Application

Consider using this indicator as one component of a broader investment framework:

♦ Understanding Position Context:

The color-coded states can help frame your thinking about current holdings:

Bull: Technical conditions that have historically been associated with sustained uptrends

Bull Retrace: Pullbacks within an overall bullish structure- these periods may offer opportunities to evaluate entry points or reassess existing positions

Reversal (Yellow): Transitional phases where the trend direction is unclear - periods that may warrant closer monitoring

Bear Retrace: Temporary strength within an overall bearish structure - rallies that historically have often faded

Bear: Technical conditions that have historically been associated with sustained downtrends

♦ Interpreting Signal Arrows:

Arrow markers indicate when specific technical pattern conditions have been met. These are observation points, not instructions:

A signal appearing doesn't mean immediate action is required

Treat arrows as prompts for further analysis rather than automatic triggers

Consider the broader context: fundamentals, your investment timeline, risk tolerance, and overall market conditions

Signals show when historical technical patterns have formed - not whether those patterns will lead to the same outcomes as in the past

The framework is designed to organize information visually, not to tell you what to do. Your investment decisions should incorporate this technical perspective alongside other factors relevant to your situation.

--------------------------------------------------------------

Technical Methodology

For transparency, the indicator uses:

* RSI (14) with a 14-period SMA to assess momentum direction

* MACD (12,26,9) to confirm trend strength and histogram momentum

* Stochastic RSI with K and D line crossovers for additional confirmation

* 50-period EMA as the primary trend filter

* Linear regression-based slope analysis to detect flat/transitional periods

* Pivot-based divergence detection following standard technical analysis principles

All calculations use publicly available technical analysis formulas. Nothing is hidden or proprietary beyond the specific combination and weighting of these standard tools.

--------------------------------------------------------------

Disclaimer

This indicator is an educational and analytical tool only. It is not financial advice.

* Trading and investing involve substantial risk of loss

* Past performance of any technical system does not indicate future results

* No indicator can predict market movements with certainty

* Always conduct your own research and consult with qualified financial professionals

* Never invest more than you can afford to lose

* The creators of this indicator are not responsible for any trading losses

* This tool is not affiliated with, endorsed by, or connected to TradingView, 3Commas, or any other trading platform

* Use of this indicator is at your own risk

Risk Management: Regardless of what any indicator shows, always use proper position sizing, stop losses, and risk management appropriate to your personal financial situation.

This indicator provides a framework for analysis. Your decisions, research, and risk management determine your results.

Opening Range The OR indicator plots the Opening Range based on the choice of Start Time and End Time (Hour:Minute:Second).

BTC CME Gaps Detector [SwissAlgo]BTC CME Gaps Detector

Track Unfilled Gaps & Identify Price Magnets

------------------------------------------------------

Overview

The BTC CME Gap Detector identifies and tracks unfilled price gaps on any timeframe (1-minute recommended for scalping) to gauge potential trading bias.

Verify Gap Behavior Yourself : Use TradingView's Replay Mode on the 1-Minute chart to observe how the price interacts with gaps. Load the BTC1! ticker (Bitcoin CME Futures), enable Replay Mode, and play forward through time (for example: go back 15 days). You may observe patterns such as price frequently returning to fill gaps, nearest gaps acting as near-term targets, and gaps serving as potential support/resistance zones. Some gaps may fill quickly, while others may remain open for longer periods. This hands-on analysis lets you independently assess how gaps may influence price movement in real market conditions and whether you may use this indicator as a complement to your trading analysis.

------------------------------------------------------

Purpose

Price gaps occur when there is a discontinuity between consecutive candles - when the current candle's low is above the previous candle's high (gap up), or when the current candle's high is below the previous candle's low (gap down).

This indicator identifies and tracks these gaps on any timeframe to help traders:

Identify gap zones that may attract price (potential "price magnets")

Monitor gap fill progression

Assess potential directional bias based on nearest unfilled gaps (long, short)

Analyze market structure and liquidity imbalances

------------------------------------------------------

Why Use This Indicator?

Universal Gap Detection : Identifies all gaps on any timeframe (1-minute, hourly, daily, etc.)

Multi-Candle Mitigation Tracking : Detects gap fills that occur across multiple candles

Distance Analysis : Shows percentage distance to nearest bullish and bearish gaps

Visual Representation : Color-coded boxes indicate gap status (active vs. mitigated)

Age Filtering : Option to display only gaps within specified time periods (3/6/12/24 months), as older gaps may lose relevance

ATR-Based Sizing : Minimum gap size adjusts to instrument volatility to filter noise (i.e. small gaps)

------------------------------------------------------

Trading Concept

Gaps represent price zones where no trading occurred. Historical market behavior suggests that unfilled gaps may attract price action as markets tend to revisit areas of incomplete price discovery. This phenomenon creates potential trading opportunities:

Bullish gaps (above current price) may act as upside targets where the price could move to fill the gap

Bearish gaps (below current price) may act as downside targets where price could move to fill the gap

The nearest gap often provides directional bias, as closer gaps may have a higher probability of being filled in the near term

This indicator helps quantify gap proximity and provides a visual reference for these potential target zones.

EXAMPLE

Step 1: Bearish Gaps Appear Below Price

Step 2: Price Getting Close to Fill Gap

Step 3: Gap Mitigated Gap

------------------------------------------------------

Recommended Setup

Timeframe: 1-minute chart recommended for maximum gap detection frequency. Works on all timeframes (higher timeframes will show fewer, larger gaps).

Symbol: Any tradable instrument. Originally designed for BTC1! (CME Bitcoin Futures) but compatible with all symbols.

Settings:

ATR Length: 14 (default)

Min Gap Size: 0.5x ATR (adjust based on timeframe and noise level)

Gap Age Limit: 3 months (configurable)

Max Historical Gaps: 300 (adjustable 1-500)

------------------------------------------------------

How It Works

Gap Detection : Identifies price discontinuities on every candle where:

Gap up: current candle low > previous candle high

Gap down: current candle high < previous candle low

Minimum gap size filter (ATR-based) eliminates insignificant gaps

Mitigation Tracking : Monitors when price touches both gap boundaries. A gap is marked as filled when the price has touched both the top and bottom of the gap zone, even if this occurs across multiple candles.

Visual Elements :

Green boxes: Unfilled gaps above current price (potential bullish targets)

Red boxes: Unfilled gaps below current price (potential bearish targets)

Gray boxes: Filled gaps (historical reference)

Labels: Display gap type, price level, and distance percentage

Analysis Table: Shows :

Distance % to nearest bullish gap (above price)

Distance % to nearest bearish gap (below price)

Trade bias (LONG if nearest gap is above, SHORT if nearest gap is below)

------------------------------------------------------

Key Features

Detects gaps on any timeframe (1m, 5m, 1h, 1D, etc.)

Boxes extend 500 bars forward for active gaps, stop at the fill bar for mitigated gaps

Real-time distance calculations update on every candle

Configurable age filter removes outdated gaps

ATR multiplier ensures gap detection adapts to market volatility and timeframe

------------------------------------------------------

Disclaimer

This indicator is provided for informational and educational purposes only.

It does not constitute financial advice, investment recommendations, or trading signals. The concept that gaps attract price is based on historical observation and does not guarantee future results.

Gap fills are not certain - gaps may remain unfilled indefinitely, or the price may reverse before reaching a gap. This indicator should not be used as the sole basis for trading decisions.

All trading involves substantial risk, including the potential loss of principal. Users should conduct their own research, apply proper risk management, test strategies thoroughly, and consult with qualified financial professionals before making trading decisions.

The authors and publishers are not responsible for any losses incurred through the use of this indicator.

Volatility-Targeted Momentum Portfolio [BackQuant]Volatility-Targeted Momentum Portfolio

A complete momentum portfolio engine that ranks assets, targets a user-defined volatility, builds long, short, or delta-neutral books, and reports performance with metrics, attribution, Monte Carlo scenarios, allocation pie, and efficiency scatter plots. This description explains the theory and the mechanics so you can configure, validate, and deploy it with intent.

Table of contents

What the script does at a glance

Momentum, what it is, how to know if it is present

Volatility targeting, why and how it is done here

Portfolio construction modes: Long Only, Short Only, Delta Neutral

Regime filter and when the strategy goes to cash

Transaction cost modelling in this script

Backtest metrics and definitions

Performance attribution chart

Monte Carlo simulation

Scatter plot analysis modes

Asset allocation pie chart

Inputs, presets, and deployment checklist

Suggested workflow

1) What the script does at a glance

Pulls a list of up to 15 tickers, computes a simple momentum score on each over a configurable lookback, then volatility-scales their bar-to-bar return stream to a target annualized volatility.

Ranks assets by raw momentum, selects the top 3 and bottom 3, builds positions according to the chosen mode, and gates exposure with a fast regime filter.

Accumulates a portfolio equity curve with risk and performance metrics, optional benchmark buy-and-hold for comparison, and a full alert suite.

Adds visual diagnostics: performance attribution bars, Monte Carlo forward paths, an allocation pie, and scatter plots for risk-return and factor views.

2) Momentum: definition, detection, and validation

Momentum is the tendency of assets that have performed well to continue to perform well, and of underperformers to continue underperforming, over a specific horizon. You operationalize it by selecting a horizon, defining a signal, ranking assets, and trading the leaders versus laggards subject to risk constraints.

Signal choices . Common signals include cumulative return over a lookback window, regression slope on log-price, or normalized rate-of-change. This script uses cumulative return over lookback bars for ranking (variable cr = price/price - 1). It keeps the ranking simple and lets volatility targeting handle risk normalization.

How to know momentum is present .

Leaders and laggards persist across adjacent windows rather than flipping every bar.

Spread between average momentum of leaders and laggards is materially positive in sample.

Cross-sectional dispersion is non-trivial. If everything is flat or highly correlated with no separation, momentum selection will be weak.

Your validation should include a diagnostic that measures whether returns are explained by a momentum regression on the timeseries.

Recommended diagnostic tool . Before running any momentum portfolio, verify that a timeseries exhibits stable directional drift. Use this indicator as a pre-check: It fits a regression to price, exposes slope and goodness-of-fit style context, and helps confirm if there is usable momentum before you force a ranking into a flat regime.

3) Volatility targeting: purpose and implementation here

Purpose . Volatility targeting seeks a more stable risk footprint. High-vol assets get sized down, low-vol assets get sized up, so each contributes more evenly to total risk.

Computation in this script (per asset, rolling):

Return series ret = log(price/price ).

Annualized volatility estimate vol = stdev(ret, lookback) * sqrt(tradingdays).

Leverage multiplier volMult = clamp(targetVol / vol, 0.1, 5.0).

This caps sizing so extremely low-vol assets don’t explode weight and extremely high-vol assets don’t go to zero.

Scaled return stream sr = ret * volMult. This is the per-bar, risk-adjusted building block used in the portfolio combinations.

Interpretation . You are not levering your account on the exchange, you are rescaling the contribution each asset’s daily move has on the modeled equity. In live trading you would reflect this with position sizing or notional exposure.

4) Portfolio construction modes

Cross-sectional ranking . Assets are sorted by cr over the chosen lookback. Top and bottom indices are extracted without ties.

Long Only . Averages the volatility-scaled returns of the top 3 assets: avgRet = mean(sr_top1, sr_top2, sr_top3). Position table shows per-asset leverages and weights proportional to their current volMult.

Short Only . Averages the negative of the volatility-scaled returns of the bottom 3: avgRet = mean(-sr_bot1, -sr_bot2, -sr_bot3). Position table shows short legs.

Delta Neutral . Long the top 3 and short the bottom 3 in equal book sizes. Each side is sized to 50 percent notional internally, with weights within each side proportional to volMult. The return stream mixes the two sides: avgRet = mean(sr_top1,sr_top2,sr_top3, -sr_bot1,-sr_bot2,-sr_bot3).

Notes .

The selection metric is raw momentum, the execution stream is volatility-scaled returns. This separation is deliberate. It avoids letting volatility dominate ranking while still enforcing risk parity at the return contribution stage.

If everything rallies together and dispersion collapses, Long Only may behave like a single beta. Delta Neutral is designed to extract cross-sectional momentum with low net beta.

5) Regime filter

A fast EMA(12) vs EMA(21) filter gates exposure.

Long Only active when EMA12 > EMA21. Otherwise the book is set to cash.

Short Only active when EMA12 < EMA21. Otherwise cash.

Delta Neutral is always active.

This prevents taking long momentum entries during obvious local downtrends and vice versa for shorts. When the filter is false, equity is held flat for that bar.

6) Transaction cost modelling

There are two cost touchpoints in the script.

Per-bar drag . When the regime filter is active, the per-bar return is reduced by fee_rate * avgRet inside netRet = avgRet - (fee_rate * avgRet). This models proportional friction relative to traded impact on that bar.

Turnover-linked fee . The script tracks changes in membership of the top and bottom baskets (top1..top3, bot1..bot3). The intent is to charge fees when composition changes. The template counts changes and scales a fee by change count divided by 6 for the six slots.

Use case: increase fee_rate to reflect taker fees and slippage if you rebalance every bar or trade illiquid assets. Reduce it if you rebalance less often or use maker orders.

Practical advice .

If you rebalance daily, start with 5–20 bps round-trip per switch on liquid futures and adjust per venue.

For crypto perp microcaps, stress higher cost assumptions and add slippage buffers.

If you only rotate on lookback boundaries or at signals, use alert-driven rebalances and lower per-bar drag.

7) Backtest metrics and definitions

The script computes a standard set of portfolio statistics once the start date is reached.

Net Profit percent over the full test.

Max Drawdown percent, tracked from running peaks.

Annualized Mean and Stdev using the chosen trading day count.

Variance is the square of annualized stdev.

Sharpe uses daily mean adjusted by risk-free rate and annualized.

Sortino uses downside stdev only.

Omega ratio of sum of gains to sum of losses.

Gain-to-Pain total gains divided by total losses absolute.

CAGR compounded annual growth from start date to now.

Alpha, Beta versus a user-selected benchmark. Beta from covariance of daily returns, Alpha from CAPM.

Skewness of daily returns.

VaR 95 linear-interpolated 5th percentile of daily returns.

CVaR average of the worst 5 percent of daily returns.

Benchmark Buy-and-Hold equity path for comparison.

8) Performance attribution

Cumulative contribution per asset, adjusted for whether it was held long or short and for its volatility multiplier, aggregated across the backtest. You can filter to winners only or show both sides. The panel is sorted by contribution and includes percent labels.

9) Monte Carlo simulation

The panel draws forward equity paths from either a Normal model parameterized by recent mean and stdev, or non-parametric bootstrap of recent daily returns. You control the sample length, number of simulations, forecast horizon, visibility of individual paths, confidence bands, and a reproducible seed.

Normal uses Box-Muller with your seed. Good for quick, smooth envelopes.

Bootstrap resamples realized returns, preserving fat tails and volatility clustering better than a Gaussian assumption.

Bands show 10th, 25th, 75th, 90th percentiles and the path mean.

10) Scatter plot analysis

Four point-cloud modes, each plotting all assets and a star for the current portfolio position, with quadrant guides and labels.

Risk-Return Efficiency . X is risk proxy from leverage, Y is expected return from annualized momentum. The star shows the current book’s composite.

Momentum vs Volatility . Visualizes whether leaders are also high vol, a cue for turnover and cost expectations.

Beta vs Alpha . X is a beta proxy, Y is risk-adjusted excess return proxy. Useful to see if leaders are just beta.

Leverage vs Momentum . X is volMult, Y is momentum. Shows how volatility targeting is redistributing risk.

11) Asset allocation pie chart

Builds a wheel of current allocations.

Long Only, weights are proportional to each long asset’s current volMult and sum to 100 percent.

Short Only, weights show the short book as positive slices that sum to 100 percent.

Delta Neutral, 50 percent long and 50 percent short books, each side leverage-proportional.

Labels can show asset, percent, and current leverage.

12) Inputs and quick presets

Core

Portfolio Strategy . Long Only, Short Only, Delta Neutral.

Initial Capital . For equity scaling in the panel.

Trading Days/Year . 252 for stocks, 365 for crypto.

Target Volatility . Annualized, drives volMult.

Transaction Fees . Per-bar drag and composition change penalty, see the modelling notes above.

Momentum Lookback . Ranking horizon. Shorter is more reactive, longer is steadier.

Start Date . Ensure every symbol has data back to this date to avoid bias.

Benchmark . Used for alpha, beta, and B&H line.

Diagnostics

Metrics, Equity, B&H, Curve labels, Daily return line, Rolling drawdown fill.

Attribution panel. Toggle winners only to focus on what matters.

Monte Carlo mode with Normal or Bootstrap and confidence bands.

Scatter plot type and styling, labels, and portfolio star.

Pie chart and labels for current allocation.

Presets

Crypto Daily, Long Only . Lookback 25, Target Vol 50 percent, Fees 10 bps, Regime filter on, Metrics and Drawdown on. Monte Carlo Bootstrap with Recent 200 bars for bands.

Crypto Daily, Delta Neutral . Lookback 25, Target Vol 50 percent, Fees 15–25 bps, Regime filter always active for this mode. Use Scatter Risk-Return to monitor efficiency and keep the star near upper left quadrants without drifting rightward.

Equities Daily, Long Only . Lookback 60–120, Target Vol 15–20 percent, Fees 5–10 bps, Regime filter on. Use Benchmark SPX and watch Alpha and Beta to keep the book from becoming index beta.

13) Suggested workflow

Universe sanity check . Pick liquid tickers with stable data. Thin assets distort vol estimates and fees.

Check momentum existence . Run on your timeframe. If slope and fit are weak, widen lookback or avoid that asset or timeframe.

Set risk budget . Choose a target volatility that matches your drawdown tolerance. Higher target increases turnover and cost sensitivity.

Pick mode . Long Only for bull regimes, Short Only for sustained downtrends, Delta Neutral for cross-sectional harvesting when index direction is unclear.

Tune lookback . If leaders rotate too often, lengthen it. If entries lag, shorten it.

Validate cost assumptions . Increase fee_rate and stress Monte Carlo. If the edge vanishes with modest friction, refine selection or lengthen rebalance cadence.

Run attribution . Confirm the strategy’s winners align with intuition and not one unstable outlier.

Use alerts . Enable position change, drawdown, volatility breach, regime, momentum shift, and crash alerts to supervise live runs.

Important implementation details mapped to code

Momentum measure . cr = price / price - 1 per symbol for ranking. Simplicity helps avoid overfitting.

Volatility targeting . vol = stdev(log returns, lookback) * sqrt(tradingdays), volMult = clamp(targetVol / vol, 0.1, 5), sr = ret * volMult.

Selection . Extract indices for top1..top3 and bot1..bot3. The arrays rets, scRets, lev_vals, and ticks_arr track momentum, scaled returns, leverage multipliers, and display tickers respectively.

Regime filter . EMA12 vs EMA21 switch determines if the strategy takes risk for Long or Short modes. Delta Neutral ignores the gate.

Equity update . Equity multiplies by 1 + netRet only when the regime was active in the prior bar. Buy-and-hold benchmark is computed separately for comparison.

Tables . Position tables show current top or bottom assets with leverage and weights. Metric table prints all risk and performance figures.

Visualization panels . Attribution, Monte Carlo, scatter, and pie use the last bars to draw overlays that update as the backtest proceeds.

Final notes

Momentum is a portfolio effect. The edge comes from cross-sectional dispersion, adequate risk normalization, and disciplined turnover control, not from a single best asset call.

Volatility targeting stabilizes path but does not fix selection. Use the momentum regression link above to confirm structure exists before you size into it.

Always test higher lag costs and slippage, then recheck metrics, attribution, and Monte Carlo envelopes. If the edge persists under stress, you have something robust.

ICT Sessions Ranges [SwissAlgo]ICT Session Ranges - ICT Liquidity Zones & Market Structure

OVERVIEW

This indicator identifies and visualizes key intraday trading sessions and liquidity zones based on Inner Circle Trader (ICT) methodology (AM, NY Lunch Raid, PM Session, London Raid). It tracks 'higher high' and 'lower low' price levels during specific time periods that may represent areas where market participants have placed orders (liquidity).

PURPOSE

The indicator helps traders observe:

Session-based price ranges during different market hours

Opening range gaps between market close and next day's open

Potential areas where liquidity may be concentrated and trigger price action

SESSIONS TRACKED

1. London Session (02:00-05:00 ET): Tracks price range during early London trading hours

2. AM Session (09:30-12:00 ET): Tracks price range during the morning New York session

3. NY Lunch Session (12:00-13:30 ET): Tracks price range during typical low-volume lunch period

4. PM Session (13:30-16:00 ET): Tracks price range during the afternoon New York session

CALCULATIONS

Session High/Low: The highest high and lowest low recorded during each active session period

Opening Range Gap: Calculated as the difference between the previous day's 16:00 close and the current day's 09:30 open

Gap Mitigation: A gap is considered mitigated when the price reaches 50% of the gap range

All times are based on America/New_York timezone (ET)

BACKGROUND INDICATORS

NY Trading Hours (09:30-16:00 ET): Optional gray background overlay

Asian Session (20:00-23:59 ET): Optional purple background overlay

VISUAL ELEMENTS

Horizontal lines mark session highs and lows

Subtle background boxes highlight each session range

Labels identify each session type

Orange shaded boxes indicate unmitigated opening range gaps

Dotted line at 50% gap level shows mitigation threshold

FEATURES

Toggle visibility for each session independently

Customizable colors for each session type

Automatic removal of mitigated gaps

All drawing objects use transparent backgrounds for chart clarity

ICT CONCEPTS

This tool relates to concepts discussed by Inner Circle Trader regarding liquidity pools, session-based analysis, and gap theory. The indicator assumes that session highs and lows may represent areas where liquidity is concentrated, and that opening range gaps may attract price until mitigated.

USAGE NOTES

Best used on intraday timeframes (1-15 minute charts)

All sessions are calculated based on actual price movement during specified time periods

Historical session data is preserved as new sessions develop

Gap detection only triggers at 09:30 ET market open

DISCLAIMER

This indicator is for educational and informational purposes only. It displays historical price levels and time-based calculations. Past performance of price levels is not indicative of future results. The identification of "liquidity zones" is a theoretical concept and does not guarantee that orders exist at these levels or that prices will react to them. Trading involves substantial risk of loss. Users should conduct their own analysis and risk assessment before making any trading decisions.

TIME ZONE

Set your timezone to: America/New_York (UTC-5)

DTC - Profile W1: Watchlist Scanner🚀 DTC - Profile W1: 12-Symbol Watchlist Scanner

Stop flipping through dozens of charts!

This is a complete multi-symbol dashboard and scanner that runs the full, complex logic of the 'Alt Coin Dynamic Trend Core v2' (DTC) system on 12 different symbols at once.

It is designed to be your primary dashboard for monitoring an entire watchlist of altcoins, helping you spot new trends and confirmed trade signals at a single glance.

✨ Key Features

12 Configurable Tickers: Monitor your entire watchlist from one chart. All 12 ticker inputs can be changed in the settings.

Configurable Timeframe: Run your analysis on any timeframe. Simply change the "Analysis Timeframe" in the settings (e.g., "60" for 1H, "240" for 4H, "D" for Daily).

Advanced Trend Engine: Uses the SAMA-based 'Dynamic Trend Core' logic as its foundation.

Multi-Layer Filtering: Signals are not just simple crossovers. They are confirmed by a powerful suite of filters, including:

Market Cycle (Halving & Mayer Multiple)

Market Regime (TOTAL Market Cap filter)

Momentum (NMS & Cyclic RSI)

Trend Strength (ADX)

Volume & Volatility (Consolidation Filter)

Delta Pressure (Wick Analysis)

Automation-Ready Alerts: Fires JSON-formatted alerts perfect for 3Commas, webhooks, or any other trading bot.

100% Non-Repainting: All calculations are performed on confirmed, closed-bar data, so signals are stable and reliable.

📊 How to Read the Dynamic Table

The table is designed for quick, "at-a-glance" decisions.

1. TOKEN Column

Your chosen ticker.

2. TREND Column

Text: Shows the current trend state with an emoji:

🚀 BULL

💣 BEAR

🤷 CHOP

Background (Heatmap): This is the most important feature. The color is a gradient that shows the strength of the trend.

A weak, new bull trend will be dark green.

A strong, accelerating bull trend will be bright green.

A weak bear trend will be dark red.

A strong, collapsing bear trend will be bright red.

3. SIGNAL Column

This column only lights up when a new signal fires.

▲ LONG: A new long signal has just been confirmed on this bar.

▼ SHORT: A new short signal has just been confirmed on this bar.

—: The trend is established, and we are waiting for the next signal.

⚙️ How to Use

Add the script to your chart.

Open the Script Settings.

Under "Watchlist Configuration," change the 12 tickers to your favorite symbols. Make sure to include the exchange prefix (e.g., BYBIT:SOLUSDT, BINANCE:BTCUSDT).

Set your desired "Analysis Timeframe."

Monitor the dashboard for new signals.

For Automation:

Create a new alert.

Select the script (DTC-W1) as the condition.

Choose "Any alert() function call."

In the "Message" box, use the {{plot_0}} placeholder to capture the JSON alert message.

Disclaimer: This script is for informational and educational purposes only. All trading involves risk. Past performance is not indicative of future results.

Author: Andrew_S_1981 Framework & Refactoring by Gemini

Position Sizer (% of Acct & Shares Req)

This indicator calculates % position size and share quantity required based on total capital and user-defined risk percentages

This indicator differs from the Shares Qty indicator in that it is based on %'s rather than a user-defined, fixed dollar amount to risk (for those who prefer to calculate risk in this manner instead)

Tracks real-time Low of Day (LoD) during regular trading hours (RTH) for accurate stop placement

Current price as well as output rows 2 and 3 can be toggled on/off, per preference

Allows stop loss selection between LoD, Low of Week (LoW), and Prior Day Low (PDL)

Keeps data updating intraday to reflect changing LoD and price conditions

Provides a second “Stop Loss Compare” dropdown to compare two stop methods side by side

Displays all results in a dynamic on-chart table that updates with live prices

Shows capital amount, stop type, stop price, and share counts for three risk levels

=========

Risk rows displayed as: Risk of Cap Amt: ,

=========

Disclaimer:

This indicator is for educational and informational purposes only. It should not be used as the sole basis for trading decisions. Always combine with other forms of analysis, proper risk management techniques, and consider your individual trading plan and risk tolerance. All calculations and outputs are provided as-is, and it is your responsibility to verify their accuracy before making any trading decisions.

Aquantprice: Institutional Structure MatrixSETUP GUIDE

Open TradingView

Go to Indicators

Search: Aquantprice: Institutional Structure Matrix

Click Add to Chart

Customize:

Min Buy = 10, Min Sell = 7

Show only PP, R1, S1, TC, BC

Set Decimals = 5 (Forex) or 8 (Crypto)

USE CASES & TRADING STRATEGIES

1. CPR Confluence Trading (Most Popular)

Rule: Enter when ≥3 timeframes show Buy ≥10/15 or Sell ≥7/13

text Example:

Daily: 12/15 Buy

Weekly: 11/15 Buy

Monthly: 10/15 Buy

→ **STRONG LONG BIAS**

Enter on pullback to nearest **S1 or L3**

2. Hot Zone Scalping (Forex & Indices)

Rule: Trade only when price is in Hot Zone (closest 2 levels)

text Hot: S1-PP → Expect bounce or breakout

Action:

- Buy at S1 if Buy Count ↑

- Sell at PP if Sell Count ↑

3. Institutional Reversal Setup

Rule: Price at H3/L3 + Reversal Condition

text Scenario:

Price touches **Monthly L3**

L3 in **Hot Zone**

Buy Count = 13/15

→ **High-Probability Reversal Long**

4. CPR Width Filter (Avoid Choppy Markets)

Rule: Trade only if CPR Label = "Strong Trend"

text CPR Size < 0.25 → Trending

CPR Size > 0.75 → Sideways (Avoid)

5. Multi-Timeframe Bias Dashboard

Use "Buy" and "Sell" columns as a sentiment meter

TimeframeBuySellBiasDaily123BullishWeekly89BearishMonthly112Bullish

→ Wait for alignment before entering

HOW TO READ THE TABLE

Column Meaning Time frame D, W, M, 3M, 6M, 12MOpen Price Current session open PP, TC, BC, etc. Pivot levels (color-coded if in Hot Zone) Buy X/15 conditions met (≥10 = Strong Buy)Sell X/13 conditions met (≥7 = Strong Sell)CPR Size Histogram + Label (Trend vs Range)Zone Hot: PP-S1, Med: S2-L3, etc. + PP Distance

PRO TIPS

Best on 5M–1H charts for entries

Use with volume or order flow for confirmation

Set alerts on Buy ≥12/15 or Sell ≥10/13

Hide unused levels to reduce clutter

Combine with AQuantPrice Dashboard (Small TF) for full system

IDEAL MARKETS

Forex (EURUSD, GBPUSD, USDJPY)

Indices (NAS100, SPX500, DAX)

Crypto (BTC, ETH – use 6–8 decimals)

Commodities (Gold, Oil)

🚀 **NEW INDICATOR ALERT**

**Aquantprice: Institutional Structure Matrix**

The **ALL-IN-ONE CPR Dashboard** used by smart money traders.

✅ **6 Timeframes in 1 Table** (Daily → Yearly)

✅ **15 Buy + 13 Sell Conditions** (Institutional Logic)

✅ **Hot Zones, CPR Width, PP Distance**

✅ **Fully Customizable – Show/Hide Any Level**

✅ **Real-Time Zone Detection** (Hot, Med, Low)

✅ **Precision up to 8 Decimals**

**No more switching charts. No more confusion.**

See **where institutions are positioned** — instantly.

👉 **Add to Chart Now**: Search **"Aquantprice: Institutional Structure Matrix"**

🔥 **Free Access | Pro-Level Insights**

*By AQuant – Trusted by 10,000+ Traders*

#CPR #PivotTrading #SmartMoney #TradingView

FINAL TAGLINE

"See What Institutions See — Before They Move."

Aquantprice: Institutional Structure Matrix

Your Edge. One Dashboard.

AudenFX Futures Risk Management & CalculatorAudenFX Futures Risk Management (FRM) is a specialized utility indicator designed to help Futures traders calculate position size, risk exposure, and reward potential in a structured and consistent manner.

Unlike signal or entry indicators, this tool focuses entirely on capital protection and risk allocation, supporting traders in making more deliberate and well-planned decisions.

This indicator is particularly made for Micro and Mini Futures markets, where tick values vary across instruments, and miscalculation of position size can significantly affect overall account performance. FRM removes guesswork by using accurate, contract-specific tick values built directly into the calculation.

What Makes This Indicator Different

Most position sizing or risk calculators available publicly:

Are designed mainly for Forex / Pips, not Tick-valued Futures

Require manual tick value input, which can lead to calculation errors

Do not account for the difference between theoretical vs. executable contract sizing

Or only display formulas, instead of practical contract size output

AudenFX FRM addresses these limitations by:

Automatically applying correct tick value for each supported Futures contract

Using Stop Loss in ticks, matching actual Futures market structure

Providing rounded contract size that can be realistically executed (no decimals)

Showing both expected and actual risk after rounding, for transparency

Presenting data in a clear, on-chart table without cluttering price action

This helps minimize position size error and ensures risk is intentional, not accidental.

Key Features

Contract Support Works with Micro and Mini Futures contracts such as: MES, MNQ, MGC, SIL, MYM, ES, NQ, GC, SI, YM, RTY, M2K

Risk-Based Position Sizing Calculates trade size based on % of account equity or user-defined risk tolerance

Tick-Based SL Input Accepts Stop Loss in ticks, consistent with Futures charting and DOM placement

Accurate Tick Value Mapping Built-in tick value per contract — no manual lookup or conversion required

Contract Size Output Returns rounded number of contracts suitable for actual order execution

Actual Risk Transparency Displays the real dollar risk after rounding, preventing under/over exposure

Reward Estimation Calculates potential reward based on chosen Reward:Risk ratio (RR)

Customizable Table Display Adjustable position & size to match any chart layout preference

Intended Use

This indicator is suitable for:

Traders who prioritize risk management and capital preservation

Traders refining sizing consistency across volatile market environments

Manual, discretionary, price action, or system-based Futures traders

This tool does not generate buy/sell signals, define market direction, or promise trade outcomes.

It is meant to support a planned, methodical approach to risk, which can be applied in any strategy.

Important Disclaimer

This indicator is provided for educational and informational purposes only.

It does not guarantee profitability, prevent loss, or provide trading instructions or recommendations.

Users are fully responsible for their own trading decisions and financial outcomes.

OverBought & OverSold [SwissAlgo]OverBought & OverSold

Statistical analysis of momentum extremes

----------------------------------------------------------

Purpose

This indicator was built to answer three questions:

Is the current price move statistically extreme? - By comparing current momentum to historical distribution

What is the current market regime? - By combining trend position and momentum direction

Is momentum accelerating or decelerating? - By analyzing weekly momentum shifts

----------------------------------------------------------

What You Can Do With This Indicator

Identify Statistical Extremes

See when price momentum seems to have reached levels that historically preceded reversals

Compare the current Rate of Change to its historical mean and standard deviation

Spot when readings exceed ±1σ, ±2σ, or higher thresholds

Monitor Market Regime/State

Track whether the market seems to be in BULL, WEAK BULL, BEAR, or WEAK BEAR state

Observe potential transitions between regimes as they occur

Understand the relationship between price position and momentum

Assess Momentum Quality

Distinguish between potentially accelerating momentum (lime/red bars) and decelerating momentum (green/maroon bars)

Watch for possible momentum deterioration within established trends

Track weekly momentum patterns that filter out daily noise

Measure Distance from Trend

Monitor how far the price is from its long-term moving average (EMA 350)

Identify when price approaches trend support/resistance

Contextualize current position relative to historical distance patterns

----------------------------------------------------------

Overview

This indicator calculates a volume-weighted Rate of Change (ROC) and displays it with statistical Z-Score bands. It combines ROC analysis with market regime detection using weekly MACD and EMA positioning.

Key Features

Volume-weighted ROC calculation with 5-bar smoothing

Dynamic Z-Score bands (±0.5σ to ±6σ)

Four-state market regime classification

Weekly Stochastic RSI-based histogram coloring

Visual markers for extreme readings

Information table with current statistics

Calculations

Volume-Weighted ROC

The indicator compares two 5-bar volume-weighted average prices separated by the ROC

Length period:

Recent VWAP = Σ(Price × Volume) / Σ(Volume) for last 5 bars

Past VWAP = Σ(Price × Volume) / Σ(Volume) for 5 bars at lookback

ROC = ((Recent VWAP - Past VWAP) / Past VWAP) × 100

Default ROC Length: 30 periods

Why volume-weighted:

Single price points can be affected by temporary spikes

Volume weighting emphasizes legitimate price moves

5-bar averaging reduces single-bar noise

Z-Score Bands

The indicator maintains separate statistical distributions for positive and negative ROC values:

For positive ROC values: