[Stratégia] VWAP Mean Magnet v9 (Simple Alert)This strategy is specifically designed for a ranging (sideways-moving) Bitcoin market.

A trade is only opened and signaled on the chart if all three of the following conditions are met simultaneously at the close of a candle:

Zone Entry

The price must cross into the signal zone: the red band for a Short (sell) position, or the green band for a Long (buy) position.

RSI Confirmation

The RSI indicator must also confirm the signal. For a Short, it must go above 65 (overbought condition). For a Long, it must fall below 25 (oversold condition).

Volume Filter

The volume on the entry candle cannot be excessively high. This safety filter is designed to prevent trades during risky, high-momentum breakouts.

M-oscillator

Medico Action Zone self adjust TF version 2to create buy sell signal with adjusted EMA and timeframe

Fisher Crossover StrategyThe Fisher Crossover Strategy is a popular technical trading method that uses the Fisher Transform indicator developed by John Ehlers. This indicator mathematically converts price data into a normal Gaussian distribution, making market turning points sharper and easier to identify. The strategy is based on two lines: the Fisher line, which is the main transformed price value, and the Trigger line, which is a one-period lag of the Fisher line. Traders use the crossover of these lines to determine buy and sell opportunities.

A buy signal is generated when the Fisher line crosses above the Trigger line, indicating that bullish momentum may be starting, while a sell signal occurs when the Fisher line crosses below the Trigger line, suggesting a possible bearish reversal. Signals that occur relative to the zero line are often considered stronger; for example, a buy signal below the zero line may indicate a deeper market reversal. The strategy is simple to follow and can be applied to various markets including stocks, forex, commodities, and cryptocurrencies.

However, like all crossover strategies, it can produce false signals during sideways or ranging markets. To reduce whipsaws, traders often combine the Fisher Crossover Strategy with other tools such as support and resistance levels, volume analysis, or moving averages. Proper risk management with stop-loss and take-profit levels is also essential. Overall, the Fisher Crossover Strategy is valued for its clear entry and exit rules and its ability to highlight potential market reversals earlier than many other indicators.

Modular Range-Trading Strategy (V9.2)# 模块化震荡行情策略 (V9.2)

# Modular Range-Trading Strategy (V9.2)

## 策略简介 | Strategy Overview

该策略基于布林带 (Bollinger Bands)、RSI、MACD、ADX 等经典指标的组合,通过多逻辑模块化结构识别震荡区间的价格反转机会,支持多空双向操作,并在相同逻辑下允许智能加仓,适用于震荡市场的回测和研究。

This strategy combines classic indicators such as Bollinger Bands, RSI, MACD, and ADX to identify price reversal opportunities within ranging markets. It features a modular multi-logic structure, allowing both long and short trades with intelligent pyramiding under the same logic. It is designed for backtesting and research in range-bound conditions.

---

## 功能特点 | Key Features

- **多逻辑结构**:支持多套震荡逻辑(动能确认均值回归、布林带极限反转等)。

- **加仓与仓位互斥**:同逻辑下可智能加仓,不同逻辑间自动互斥,避免冲突。

- **回测可调时间范围**:可自定义回测起止时间,精准评估策略表现。

- **指标可视化**:布林带、RSI、MACD 及动态 ATR 止损线实时绘图。

- **K线收盘确认信号**:通过 `barstate.isconfirmed` 控制信号,避免未收盘的虚假信号。

- **Multi-logic structure**: Supports multiple range-trading logics (e.g., momentum-based mean reversion, Bollinger Band reversals).

- **Pyramiding with mutual exclusion**: Allows intelligent pyramiding within the same logic while preventing conflicts between different logics.

- **Adjustable backtesting range**: Customizable start and end dates for accurate performance evaluation.

- **Visual indicators**: Real-time plotting of Bollinger Bands, RSI, MACD, and dynamic ATR stop lines.

- **Close-bar confirmation**: Uses `barstate.isconfirmed` to avoid false signals before bar close.

---

## 使用说明 | Usage

1. 将该脚本添加到 TradingView 图表。

2. 在参数中设置回测时间段和指标参数。

3. 仅用于学习与策略研究,请勿直接用于实盘交易。

1. Add this script to your TradingView chart.

2. Configure backtesting dates and indicator parameters as needed.

3. For educational and research purposes only. **Not for live trading.**

---

## ⚠️ 免责声明 | Disclaimer

本策略仅供学习和研究使用,不构成任何形式的投资建议。

作者不参与任何实盘交易、资金管理或收益分成,也不保证策略盈利能力。

严禁将本脚本用于任何非法集资、私募募资或与虚拟货币相关的金融违法活动。

使用本策略即表示您自行承担所有风险与法律责任。

This strategy is for educational and research purposes only and does not constitute investment advice.

The author does not participate in live trading, asset management, or profit sharing, nor guarantee profitability.

The use of this script in illegal fundraising, private placements, or cryptocurrency-related financial activities is strictly prohibited.

By using this strategy, you accept all risks and legal responsibilities.

---

[Stratégia] VWAP Mean Magnet v2 (VolSzűrő)Ez a stratégia BTC- oldalazó időszakára van kifejlestve 1 perces chartra.

strategy15min bar, short-term and scalp strategy, eth, using stdev as trend line, long when price hits the lower line, short when price hits the upper line.

MACD Liquidity Tracker Strategy [Quant Trading]MACD Liquidity Tracker Strategy

Overview

The MACD Liquidity Tracker Strategy is an enhanced trading system that transforms the traditional MACD indicator into a comprehensive momentum-based strategy with advanced visual signals and risk management. This strategy builds upon the original MACD Liquidity Tracker System indicator by TheNeWSystemLqtyTrckr , converting it into a fully automated trading strategy with improved parameters and additional features.

What Makes This Strategy Original

This strategy significantly enhances the basic MACD approach by introducing:

Four distinct system types for different market conditions and trading styles

Advanced color-coded histogram visualization with four dynamic colors showing momentum strength and direction

Integrated trend filtering using 9 different moving average types

Comprehensive risk management with customizable stop-loss and take-profit levels

Multiple alert systems for entry signals, exits, and trend conditions

Flexible signal display options with customizable entry markers

How It Works

Core MACD Calculation

The strategy uses a fully customizable MACD configuration with traditional default parameters:

Fast MA : 12 periods (customizable, minimum 1, no maximum limit)

Slow MA : 26 periods (customizable, minimum 1, no maximum limit)

Signal Line : 9 periods (customizable, now properly implemented and used)

Cryptocurrency Optimization : The strategy's flexible parameter system allows for significant optimization across different crypto assets. Traditional MACD settings (12/26/9) often generate excessive noise and false signals in volatile crypto markets. By using slower, more smoothed parameters, traders can capture meaningful momentum shifts while filtering out market noise.

Example - DOGE Optimization (45/80/290 settings) :

• Performance : Optimized parameters yielding exceptional backtesting results with 29,800% PnL

• Why it works : DOGE's high volatility and social sentiment-driven price action benefits from heavily smoothed indicators

• Timeframes : Particularly effective on 30-minute and 4-hour charts for swing trading

• Logic : The very slow parameters filter out noise and capture only the most significant trend changes

Other Optimizable Cryptocurrencies : This parameter flexibility makes the strategy highly effective for major altcoins including SUI, SEI, LINK, Solana (SOL) , and many others. Each crypto asset can benefit from custom parameter tuning based on its unique volatility profile and trading characteristics.

Four Trading System Types

1. Normal System (Default)

Long signals : When MACD line is above the signal line

Short signals : When MACD line is below the signal line

Best for : Swing trading and capturing longer-term trends in stable markets

Logic : Traditional MACD crossover approach using the signal line

2. Fast System

Long signals : Bright Blue OR Dark Magenta (transparent) histogram colors

Short signals : Dark Blue (transparent) OR Bright Magenta histogram colors

Best for : Scalping and high-volatility markets (crypto, forex)

Logic : Leverages early momentum shifts based on histogram color changes

3. Safe System

Long signals : Only Bright Blue histogram color (strongest bullish momentum)

Short signals : All other colors (Dark Blue, Bright Magenta, Dark Magenta)

Best for : Risk-averse traders and choppy markets

Logic : Prioritizes only the strongest bullish signals while treating everything else as bearish

4. Crossover System

Long signals : MACD line crosses above signal line

Short signals : MACD line crosses below signal line

Best for : Precise timing entries with traditional MACD methodology

Logic : Pure crossover signals for more precise entry timing

Color-Coded Histogram Logic

The strategy uses four distinct colors to visualize momentum:

🔹 Bright Blue : MACD > 0 and rising (strong bullish momentum)

🔹 Dark Blue (Transparent) : MACD > 0 but falling (weakening bullish momentum)

🔹 Bright Magenta : MACD < 0 and falling (strong bearish momentum)

🔹 Dark Magenta (Transparent) : MACD < 0 but rising (weakening bearish momentum)

Trend Filter Integration

The strategy includes an advanced trend filter using 9 different moving average types:

SMA (Simple Moving Average)

EMA (Exponential Moving Average) - Default

WMA (Weighted Moving Average)

HMA (Hull Moving Average)

RMA (Running Moving Average)

LSMA (Least Squares Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

VIDYA (Variable Index Dynamic Average)

Default Settings : 50-period EMA for trend identification

Visual Signal System

Entry Markers : Blue triangles (▲) below candles for long entries, Magenta triangles (▼) above candles for short entries

Candle Coloring : Price candles change color based on active signals (Blue = Long, Magenta = Short)

Signal Text : Optional "Long" or "Short" text inside entry triangles (toggleable)

Trend MA : Gray line plotted on main chart for trend reference

Parameter Optimization Examples

DOGE Trading Success (Optimized Parameters) :

Using 45/80/290 MACD settings with 50-period EMA trend filter has shown exceptional results on DOGE:

Performance : Backtesting results showing 29,800% PnL demonstrate the power of proper parameter optimization

Reasoning : DOGE's meme-driven volatility and social sentiment spikes create significant noise with traditional MACD settings

Solution : Very slow parameters (45/80/290) filter out social media-driven price spikes while capturing only major momentum shifts

Optimal Timeframes : 30-minute and 4-hour charts for swing trading opportunities

Result : Exceptionally clean signals with minimal false entries during DOGE's characteristic pump-and-dump cycles

Multi-Crypto Adaptability :

The same optimization principles apply to other major cryptocurrencies:

SUI : Benefits from smoothed parameters due to newer coin volatility patterns

SEI : Requires adjustment for its unique DeFi-related price movements

LINK : Oracle news events create price spikes that benefit from noise filtering

Solana (SOL) : Network congestion events and ecosystem developments need smoothed detection

General Rule : Higher volatility coins typically benefit from very slow MACD parameters (40-50 / 70-90 / 250-300 ranges)

Key Input Parameters

System Type : Choose between Fast, Normal, Safe, or Crossover (Default: Normal)

MACD Fast MA : 12 periods default (no maximum limit, consider 40-50 for crypto optimization)

MACD Slow MA : 26 periods default (no maximum limit, consider 70-90 for crypto optimization)

MACD Signal MA : 9 periods default (now properly utilized, consider 250-300 for crypto optimization)

Trend MA Type : EMA default (9 options available)

Trend MA Length : 50 periods default (no maximum limit)

Signal Display : Both, Long Only, Short Only, or None

Show Signal Text : True/False toggle for entry marker text

Trading Applications

Recommended Use Cases

Momentum Trading : Capitalize on strong directional moves using the color-coded system

Trend Following : Combine MACD signals with trend MA filter for higher probability trades

Scalping : Use "Fast" system type for quick entries in volatile markets

Swing Trading : Use "Normal" or "Safe" system types for longer-term positions

Cryptocurrency Trading : Optimize parameters for individual crypto assets (e.g., 45/80/290 for DOGE, custom settings for SUI, SEI, LINK, SOL)

Market Suitability

Volatile Markets : Forex, crypto, indices (recommend "Fast" system or smoothed parameters)

Stable Markets : Stocks, ETFs (recommend "Normal" or "Safe" system)

All Timeframes : Effective from 1-minute charts to daily charts

Crypto Optimization : Each major cryptocurrency (DOGE, SUI, SEI, LINK, SOL, etc.) can benefit from custom parameter tuning. Consider slower MACD parameters for noise reduction in volatile crypto markets

Alert System

The strategy provides comprehensive alerts for:

Entry Signals : Long and short entry triangle appearances

Exit Signals : Position exit notifications

Color Changes : Individual histogram color alerts

Trend Conditions : Price above/below trend MA alerts

Strategy Parameters

Default Settings

Initial Capital : $1,000

Position Size : 100% of equity

Commission : 0.1%

Slippage : 3 points

Date Range : January 1, 2018 to December 31, 2069

Risk Management (Optional)

Stop Loss : Disabled by default (customizable percentage-based)

Take Profit : Disabled by default (customizable percentage-based)

Short Trades : Disabled by default (can be enabled)

Important Notes and Limitations

Backtesting Considerations

Uses realistic commission (0.1%) and slippage (3 points)

Default position sizing uses 100% equity - adjust based on risk tolerance

Stop-loss and take-profit are disabled by default to show raw strategy performance

Strategy does not use lookahead bias or future data

Risk Warnings

Past performance does not guarantee future results

MACD-based strategies may produce false signals in ranging markets

Consider combining with additional confluences like support/resistance levels

Test thoroughly on demo accounts before live trading

Adjust position sizing based on your risk management requirements

Technical Limitations

Strategy does not work on non-standard chart types (Heikin Ashi, Renko, etc.)

Signals are based on close prices and may not reflect intraday price action

Multiple rapid signals in volatile conditions may result in overtrading

Credits and Attribution

This strategy is based on the original "MACD Liquidity Tracker System" indicator created by TheNeWSystemLqtyTrckr . This strategy version includes significant enhancements:

Complete strategy implementation with entry/exit logic

Addition of the "Crossover" system type

Proper implementation and utilization of the MACD signal line

Enhanced risk management features

Improved parameter flexibility with no artificial maximum limits

Additional alert systems for comprehensive trade management

The original indicator's core color logic and visual system have been preserved while expanding functionality for automated trading applications.

OBV ATR Strategy (OBV Breakout Channel) bas20230503ผมแก้ไขจาก OBV+SMA อันเดิม ของเดิม ดูที่เส้น SMA สองเส้นตัดกันมั่นห่วยแตกสำหรับที่ผมลองเทรดจริง และหลักการเบรค ได้แรงบันดาลใจ ATR จาก เทพคอย ที่ใช้กับราคา แต่นี้ใช้กับ OBV แทน

และผมใช้เจมินี้ เพื่อแก้ ให้ เป็น strategy เพื่อเช็คย้อนหลังได้ง่ายกว่าเดิม

หลักการง่ายคือถ้ามันขึ้น มันจะขึ้นเรื่อยๆ

เขียน แบบสุภาพ (น่าจะอ่านได้ง่ายกว่าผมเขียน)

สคริปต์นี้ได้รับการพัฒนาต่อยอดจากแนวคิด OBV+SMA Crossover แบบดั้งเดิม ซึ่งจากการทดสอบส่วนตัวพบว่าประสิทธิภาพยังไม่น่าพอใจ กลยุทธ์ใหม่นี้จึงเปลี่ยนมาใช้หลักการ "Breakout" ซึ่งได้รับแรงบันดาลใจมาจากการใช้ ATR สร้างกรอบของราคา แต่เราได้นำมาประยุกต์ใช้กับ On-Balance Volume (OBV) แทน นอกจากนี้ สคริปต์ได้ถูกแปลงเป็น Strategy เต็มรูปแบบ (โดยความช่วยเหลือจาก Gemini AI) เพื่อให้สามารถทดสอบย้อนหลัง (Backtest) และประเมินประสิทธิภาพได้อย่างแม่นยำ

หลักการของกลยุทธ์: กลยุทธ์นี้ทำงานบนแนวคิดโมเมนตัมที่ว่า "เมื่อแนวโน้มได้เกิดขึ้นแล้ว มีโอกาสที่มันจะดำเนินต่อไป" โดยจะมองหาการทะลุของพลังซื้อ-ขาย (OBV) ที่แข็งแกร่งเป็นพิเศษเป็นสัญญาณเข้าเทร

----

สคริปต์นี้เป็นกลยุทธ์ (Strategy) ที่ใช้ On-Balance Volume (OBV) ซึ่งเป็นอินดิเคเตอร์ที่วัดแรงซื้อและแรงขายสะสม แทนที่จะใช้การตัดกันของเส้นค่าเฉลี่ย (SMA Crossover) ที่เป็นแบบพื้นฐาน กลยุทธ์นี้จะมองหาการ "ทะลุ" (Breakout) ของพลัง OBV ออกจากกรอบสูงสุด-ต่ำสุดของตัวเองในรอบที่ผ่านมา

สัญญาณกระทิง (Bull Signal): เกิดขึ้นเมื่อพลังการซื้อ (OBV) แข็งแกร่งจนสามารถทะลุจุดสูงสุดของตัวเองในอดีตได้ บ่งบอกถึงโอกาสที่แนวโน้มจะเปลี่ยนเป็นขาขึ้น

สัญญาณหมี (Bear Signal): เกิดขึ้นเมื่อพลังการขาย (OBV) รุนแรงจนสามารถกดดันให้ OBV ทะลุจุดต่ำสุดของตัวเองในอดีตได้ บ่งบอกถึงโอกาสที่แนวโน้มจะเปลี่ยนเป็นขาลง

ส่วนประกอบบนกราฟ (Indicator Components)

เส้น OBV

เส้นหลัก ที่เปลี่ยนเขียวเป็นแดง เป็นทั้งแนวรับและแนวต้าน และ จุด stop loss

เส้นนี้คือหัวใจของอินดิเคเตอร์ ที่แสดงถึงพลังสะสมของ Volume

เมื่อเส้นเป็นสีเขียว (แนวรับ): จะปรากฏขึ้นเมื่อกลยุทธ์เข้าสู่ "โหมดกระทิง" เส้นนี้คือระดับต่ำสุดของ OBV ในอดีต และทำหน้าที่เป็นแนวรับไดนามิก

เมื่อเส้นกลายเป็นสีแดงสีแดง (แนวต้าน): จะปรากฏขึ้นเมื่อกลยุทธ์เข้าสู่ "โหมดหมี" เส้นนี้คือระดับสูงสุดของ OBV ในอดีต และทำหน้าที่เป็นแนวต้านไดนามิก

สัญลักษณ์สัญญาณ (Signal Markers):

Bull 🔼 (สามเหลี่ยมขึ้นสีเขียว): คือสัญญาณ "เข้าซื้อ" (Long) จะปรากฏขึ้น ณ จุดที่ OBV ทะลุขึ้นไปเหนือกรอบด้านบนเป็นครั้งแรก

Bear 🔽 (สามเหลี่ยมลงสีแดง): คือสัญญาณ "เข้าขาย" (Short) จะปรากฏขึ้น ณ จุดที่ OBV ทะลุลงไปต่ำกว่ากรอบด้านล่างเป็นครั้งแรก

วิธีการใช้งาน (How to Use)

เพิ่มสคริปต์นี้ลงบนกราฟราคาที่คุณสนใจ

ไปที่แท็บ "Strategy Tester" ด้านล่างของ TradingView เพื่อดูผลการทดสอบย้อนหลัง (Backtest) ของกลยุทธ์บนสินทรัพย์และไทม์เฟรมต่างๆ

ใช้สัญลักษณ์ "Bull" และ "Bear" เป็นตัวช่วยในการตัดสินใจเข้าเทรด

ข้อควรจำ: ไม่มีกลยุทธ์ใดที่สมบูรณ์แบบ 100% ควรใช้สคริปต์นี้ร่วมกับการวิเคราะห์ปัจจัยอื่นๆ เช่น โครงสร้างราคา, แนวรับ-แนวต้านของราคา และการบริหารความเสี่ยง (Risk Management) ของตัวคุณเองเสมอ

การตั้งค่า (Inputs)

SMA Length 1 / SMA Length 2: ใช้สำหรับพล็อตเส้นค่าเฉลี่ยของ OBV เพื่อดูเป็นภาพอ้างอิง ไม่มีผลต่อตรรกะการเข้า-ออกของ Strategy อันใหม่ แต่มันเป็นของเก่า ถ้าชอบ ก็ใช้ได้ เมื่อ SMA สองเส้นตัดกัน หรือตัดกับเส้น OBV

High/Low Lookback Length: (ค่าพื้นฐาน30/แก้ตรงนี้ให้เหมาะสมกับ coin หรือหุ้น ตามความผันผวน ) คือระยะเวลาที่ใช้ในการคำนวณกรอบสูงสุด-ต่ำสุดของ OBV

ค่าน้อย: ทำให้กรอบแคบลง สัญญาณจะเกิดไวและบ่อยขึ้น แต่อาจมีสัญญาณหลอก (False Signal) เยอะขึ้น

ค่ามาก: ทำให้กรอบกว้างขึ้น สัญญาณจะเกิดช้าลงและน้อยลง แต่มีแนวโน้มที่จะเป็นสัญญาณที่แข็งแกร่งกว่า

แน่นอนครับ นี่คือคำแปลฉบับภาษาอังกฤษที่สรุปใจความสำคัญ กระชับ และสุภาพ เหมาะสำหรับนำไปใช้ในคำอธิบายสคริปต์ (Description) ของ TradingView ครับ

---Translate to English---

OBV Breakout Channel Strategy

This script is an evolution of a traditional OBV+SMA Crossover concept. Through personal testing, the original crossover method was found to have unsatisfactory performance. This new strategy, therefore, uses a "Breakout" principle. The inspiration comes from using ATR to create price channels, but this concept has been adapted and applied to On-Balance Volume (OBV) instead.

Furthermore, the script has been converted into a full Strategy (with assistance from Gemini AI) to enable precise backtesting and performance evaluation.

The strategy's core principle is momentum-based: "once a trend is established, it is likely to continue." It seeks to enter trades on exceptionally strong breakouts of buying or selling pressure as measured by OBV.

Core Concept

This is a Strategy that uses On-Balance Volume (OBV), an indicator that measures cumulative buying and selling pressure. Instead of relying on a basic Simple Moving Average (SMA) Crossover, this strategy identifies a "Breakout" of the OBV from its own highest-high and lowest-low channel over a recent period.

Bull Signal: Occurs when the buying pressure (OBV) is strong enough to break above its own recent highest high, indicating a potential shift to an upward trend.

Bear Signal: Occurs when the selling pressure (OBV) is intense enough to push the OBV below its own recent lowest low, indicating a potential shift to a downward trend.

On-Screen Components

1. OBV Line

This is the main indicator line, representing the cumulative volume. Its color changes to green when OBV is rising and red when it is falling.

2. Dynamic Support & Resistance Line

This is the thick Green or Red line that appears based on the strategy's current "mode." This line serves as a dynamic support/resistance level and can be used as a reference for stop-loss placement.

Green Line (Support): Appears when the strategy enters "Bull Mode." This line represents the lowest low of the OBV in the recent past and acts as dynamic support.

Red Line (Resistance): Appears when the strategy enters "Bear Mode." This line represents the highest high of the OBV in the recent past and acts as dynamic resistance.

3. Signal Markers

Bull 🔼 (Green Up Triangle): This is the "Long Entry" signal. It appears at the moment the OBV first breaks out above its high-low channel.

Bear 🔽 (Red Down Triangle): This is the "Short Entry" signal. It appears at the moment the OBV first breaks down below its high-low channel.

How to Use

Add this script to the price chart of your choice.

Navigate to the "Strategy Tester" panel at the bottom of TradingView to view the backtesting results for the strategy on different assets and timeframes.

Use the "Bull" and "Bear" signals as aids in your trading decisions.

Disclaimer: No strategy is 100% perfect. This script should always be used in conjunction with other forms of analysis, such as price structure, key price-based support/resistance levels, and your own personal risk management rules.

Inputs

SMA Length 1 / SMA Length 2: These are used to plot moving averages on the OBV for visual reference. They are part of the legacy logic and do not affect the new breakout strategy. However, they are kept for traders who may wish to observe their crossovers for additional confirmation.

High/Low Lookback Length: (Most Important Setting) This determines the period used to calculate the highest-high and lowest-low OBV channel. (Default is 30; adjust this to suit the asset's volatility).

A smaller value: Creates a narrower channel, leading to more frequent and faster signals, but potentially more false signals.

A larger value: Creates a wider channel, leading to fewer and slower signals, which are likely to be more significant.

TrendMaster Pro 2.3 with Alerts

Hello friends,

A member of the community approached me and asked me how to write an indicator that would achieve a particular set of goals involving comprehensive trend analysis, risk management, and session-based trading controls. Here is one example method of how to create such a system:

Core Strategy Components

Multi-Moving Average System - Uses configurable MA types (EMA, SMA, SMMA) with short-term (9) and long-term (21) periods for primary signal generation through crossovers

Higher Timeframe Trend Filter - Optional trend confirmation using a separate MA (default 50-period) to ensure trades align with broader market direction

Band Power Indicator - Dynamic high/low bands calculated using different MA types to identify price channels and volatility zones

Advanced Signal Filtering

Bollinger Bands Volatility Filter - Prevents trading during low-volatility ranging markets by requiring sufficient band width

RSI Momentum Filter - Uses customizable thresholds (55 for longs, 45 for shorts) to confirm momentum direction

MACD Trend Confirmation - Ensures MACD line position relative to signal line aligns with trade direction

Stochastic Oscillator - Adds momentum confirmation with overbought/oversold levels

ADX Strength Filter - Only allows trades when trend strength exceeds 25 threshold

Session-Based Trading Management

Four Trading Sessions - Asia (18:00-00:00), London (00:00-08:00), NY AM (08:00-13:00), NY PM (13:00-18:00)

Individual Session Limits - Separate maximum trade counts for each session (default 5 per session)

Automatic Session Closure - All positions close at specified market close time

Risk Management Features

Multiple Stop Loss Options - Percentage-based, MA cross, or band-based SL methods

Risk/Reward Ratio - Configurable TP levels based on SL distance (default 1:2)

Auto-Risk Calculation - Dynamic position sizing based on dollar risk limits ($150-$250 range)

Daily Limits - Stop trading after reaching specified TP or SL counts per day

Support & Resistance System

Multiple Pivot Types - Traditional, Fibonacci, Woodie, Classic, DM, and Camarilla calculations

Flexible Timeframes - Auto-adjusting or manual timeframe selection for S/R levels

Historical Levels - Configurable number of past S/R levels to display

Visual Customization - Individual color and display settings for each S/R level

Additional Features

Alert System - Customizable buy/sell alert messages with once-per-bar frequency

Visual Trade Management - Color-coded entry, SL, and TP levels with fill areas

Session Highlighting - Optional background colors for different trading sessions

Comprehensive Filtering - All signals must pass through multiple confirmation layers before execution

This approach demonstrates how to build a professional-grade trading system that combines multiple technical analysis methods with robust risk management and session-based controls, suitable for algorithmic trading across different market sessions.

Good luck and stay safe!

Strategy Builder With IndicatorsThis strategy script is designed for traders who enjoy building systems using multiple indicators.

Please note: This script does not include any built-in indicators. Instead, it works by referencing the plot outputs of the indicators you’ve already added to your chart.

For example, if you add a MACD and an ATR indicator to your chart, you can assign their plot values as inputs in the settings panel of this strategy.

• MACD as a trigger

• ATR as a filter

How Filters Work

Filters check whether certain conditions are met before a trade can be opened. For instance, if you set a filter like ATR > 30, then no trade will be executed unless that condition is true — even if the trigger fires.

All filters are linked, meaning every active filter must be satisfied for a trade to occur.

How Triggers Work

Triggers are what actually fire a trade signal — such as a moving average crossover or RSI breaking above a specific level. Unlike filters, triggers are independent. Only one active trigger needs to be true for the trade to execute.

Thanks to its modular structure, this strategy can be used with any indicator of your choice.

⸻

Risk Management Features

In the settings, you’ll find flexible options for:

• Stop Loss (SL)

• Trailing Stop Loss (TSL)

• Multi Take-Profit (TP)

These features enhance trade safety and let you tailor your risk management.

SL types available:

• Tick-based SL

• Percent-based SL

• ATR-based SL

Once you select your preferred SL type, you can fine-tune its distance using the offset field.

Trailing SL allows your stop to follow price as it moves in your favor — helping to lock in profits.

Multi-TP lets you take profits at two different levels, helping you secure gains while leaving room for extended moves.

Breakeven option is also available to automatically move your SL to entry after reaching a profit threshold.

⸻

How to Build a Solid Strategy

Let’s break down a good setup into three key components:

1. Trend Filter

Avoid trading against the trend — that’s like swimming against the current.

Use a filter like:

• Supertrend

• Momentum indicators

• Candlestick bias, etc.

Example: In this case, I used Supertrend and filtered for trades only if the price is above the uptrend line.

2. Trigger Condition

Once we confirm the trend is on our side, we need a trigger to execute at the right moment. This can be:

• RSI cross

• Candlestick patterns

• Trendline breaks

• Moving average crossovers, etc.

Example: I used RSI crossing above 50 as the entry trigger.

3. Risk Management

Even in the right trend at the right time — anything can happen. That’s why you should always define Stop Loss and Take Profit levels.

⸻

And there you have it! Your strategy is ready to backtest, refine, and deploy with alerts for live trading.

Questions or suggestions? Feel free to reach out

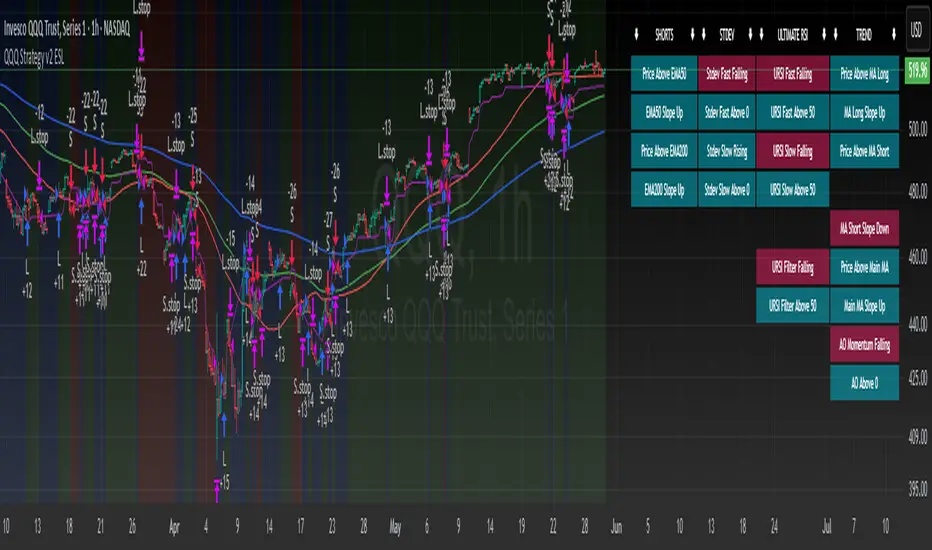

QQQ Strategy v2 ESL | easy-peasy-x This is a strategy optimized for QQQ (and SPY) for the 1H timeframe. It significantly outperforms passive buy-and-hold approach. With settings adjustments, it can be used on various assets like stocks and cryptos and various timeframes, although the default out of the box settings favor QQQ 1H.

The strategy uses various triggers to take both long and short trades. These can be adjusted in settings. If you try a different asset, see what combination of triggers works best for you.

Some of the triggers employ LuxAlgo's Ultimate RSI - shoutout to him for great script, check it out here .

Other triggers are based on custom signed standard deviation - basically the idea is to trade Bollinger Bands expansions (long to the upside, short to the downside) and fade or stay out of contractions.

There are three key moving averages in the strategy - LONG MA, SHORT MA, BASIC MA. Long and Short MAs are guides to eyes on the chart and also act as possible trend filters (adjustable in settings). Basic MA acts as guide to eye and a possible trade trigger (adjustable in settings).

There are a few trend filters the strategy can use - moving average, signed standard deviation, ultimate RSI or none. The filters act as an additional condition on triggers, making the strategy take trades only if both triggers and trend filter allows. That way one can filter out trades with unfavorable risk/reward (for instance, don't long if price is under the MA200). Different trade filters can be used for long and short trades.

The strategy employs various stop loss types, the default of which is a trailing %-based stop loss type. ATR-based stop loss is also available. The default 1.5% trailing stop loss is suitable for leveraged trading.

Lastly, the strategy can trigger take profit orders if certain conditions are met, adjustable in settings. Also, it can hold onto winning trades and exit only after stop out (in which case, consecutive triggers to take other positions will be ignored until stop out).

Let me know if you like it and if you use it, what kind of tweaks would you like to see.

With kind regards,

easy-peasy-x

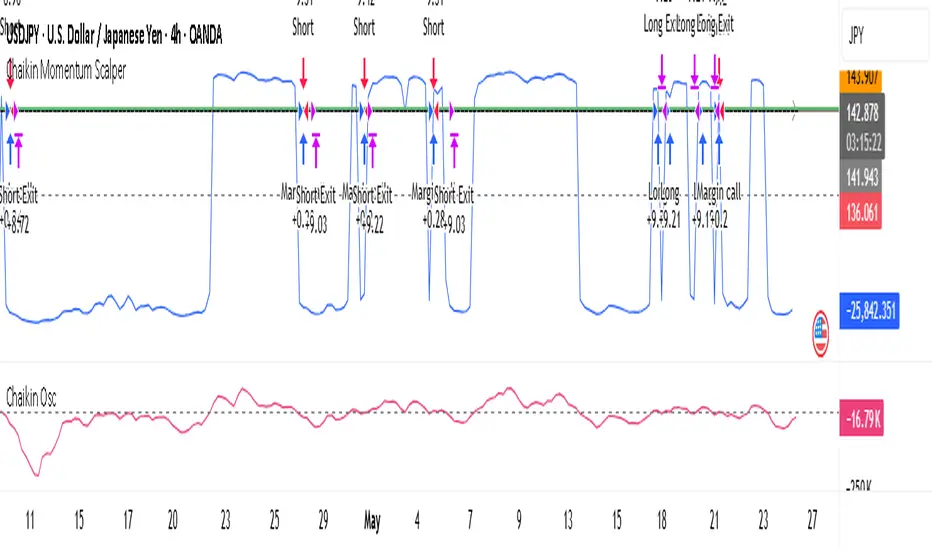

Chaikin Momentum Scalper🎯 Overview

The Chaikin Momentum Scalper is a powerful trading strategy designed to identify momentum shifts in the market and ride the trend for maximum profits. This strategy is ideal for trading the USD/JPY currency pair on a 15-minute chart, making it perfect for high-frequency trading (HFT). Whether you’re starting with a small account of $1,000 or managing a larger portfolio, this strategy can scale to suit your needs.

________________________________________

🔑 How the Strategy Works

Here’s how the Chaikin Momentum Scalper identifies trade opportunities:

1️⃣ Momentum Detection

The core of this strategy is the Chaikin Oscillator, a tool that measures the flow of money into or out of a market. It helps us understand whether buyers (bulls) or sellers (bears) are in control.

• When the indicator crosses above zero, it signals that buying momentum is picking up – a buying opportunity.

• When the indicator crosses below zero, it signals that selling momentum is increasing – a selling opportunity.

2️⃣ Trend Confirmation

We don’t just jump into trades based on momentum alone. We also use a 200-period simple moving average (SMA) to confirm the overall trend.

• If the price is above the SMA, it confirms an uptrend, so we look for buy trades.

• If the price is below the SMA, it confirms a downtrend, so we look for sell trades.

This way, we align our trades with the broader market direction for higher success rates.

3️⃣ Volatility & Risk Management

We use a tool called the Average True Range (ATR) to measure market volatility. This helps us:

• Set a stop-loss (where we’ll exit the trade if the market moves against us) at a safe distance from our entry point.

• Set a take-profit (where we’ll lock in profits) at a target that’s larger than the stop-loss, ensuring a good reward-to-risk ratio.

This approach adapts to the market’s behavior, tightening stops in calmer conditions and widening them when volatility increases.

________________________________________

📈 Why This Strategy Works

✅ It combines momentum and trend-following principles, increasing the chances of trading in the right direction.

✅ It dynamically adjusts risk levels based on market volatility, keeping losses small and profits big.

✅ It’s scalable – perfect for both small accounts (like $1,000) and larger, corporate-sized portfolios.

✅ It has been deep-backtested on USD/JPY 15-minute charts, proving its consistency across different market conditions.

________________________________________

📝 Important Notes

📌 This strategy is best used for USD/JPY on a 15-minute chart, making it great for high-frequency trading while you continue to build and refine your trading system.

📌 It’s designed to work on both small ($1,000+) and large accounts, so it can grow with you as your capital increases.

📌 While it has passed deep backtesting on this pair and timeframe, remember that no strategy is perfect. It’s crucial to test it yourself, start with a demo account, and apply proper risk management before trading real money.

🌟 Final Thoughts

The Chaikin Momentum Scalper is a solid, adaptable trading approach combining momentum, trend direction, and volatility awareness. If you’re looking for a strategy to kick-start your trading journey—or to add to your existing system—it offers a strong foundation.

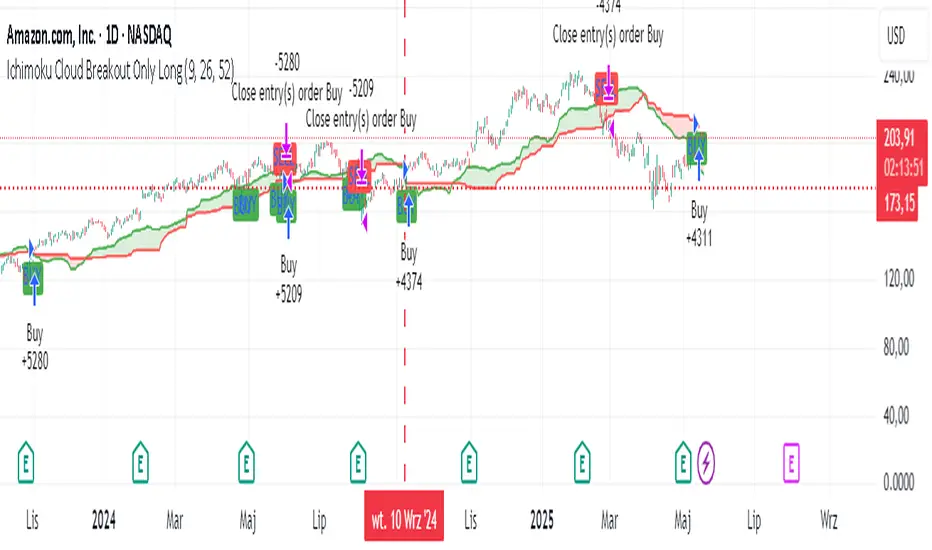

Ichimoku Cloud Breakout Only LongThis is a very simple trading strategy based exclusively on the Ichimoku Cloud. There are no additional indicators or complex rules involved. The key condition is that we only open long positions when the price is clearly above the cloud — indicating a bullish trend.

For optimal results, the recommended timeframes are 1D (daily) or 1W (weekly) charts. These higher timeframes help filter out market noise and provide more reliable trend signals.

We do not short the market under any circumstances. The focus is purely on riding upward momentum when the price breaks out or stays above the cloud.

This strategy works best when applied to growth stocks with strong upward trends and good fundamentals — such as Google (GOOGL), Tesla (TSLA), Apple (AAPL), or NVIDIA (NVDA).

EXODUS EXODUS by (DAFE) Trading Systems

EXODUS is a sophisticated trading algorithm built by Dskyz (DAFE) Trading Systems for competitive and competition purposes, designed to identify high-probability trades with robust risk management. this strategy leverages a multi-signal voting system, combining three core components—SPR, VWMO, and VEI—alongside ADX, choppiness filters, and ATR-based volatility gates to ensure trades are taken only in favorable market conditions. the algo uses a take-profit to stop-loss ratio, dynamic position sizing, and a strict voting mechanism requiring all signals to align before entering a trade.

EXODUS was not overfitted for any specific symbol. instead, it uses a generic tuned setting, making it versatile across various markets. while it can trade futures, it’s not currently set up for it but has the potential to do more with further development. visuals are intentionally minimal due to its competition focus, prioritizing performance over aesthetics. a more visually stunning version may be released in the future with enhanced graphics.

The Unique Core Components Developed for EXODUS

SPR (Session Price Recalibration)

SPR measures momentum during regular trading hours (RTH, 0930-1600, America/New_York) to catch session-specific trends.

spr_lookback = input.int(15, "SPR Lookback") this sets how many bars back SPR looks to calculate momentum (default 15 bars). it compares the current session’s price-volume score to the score 15 bars ago to gauge momentum strength.

how it works: a longer lookback smooths out the signal, focusing on bigger trends. a shorter one makes SPR more sensitive to recent moves.

how to adjust: on a 1-hour chart, 15 bars is 15 hours (about 2 trading days). if you’re on a shorter timeframe like 5 minutes, 15 bars is just 75 minutes, so you might want to increase it to 50 or 100 to capture more meaningful trends. if you’re trading a choppy stock, a shorter lookback (like 5) can help catch quick moves, but it might give more false signals.

spr_threshold = input.float (0.7, "SPR Threshold")

this is the cutoff for SPR to vote for a trade (default 0.7). if SPR’s normalized value is above 0.7, it votes for a long; below -0.7, it votes for a short.

how it works: SPR normalizes its momentum score by ATR, so this threshold ensures only strong moves count. a higher threshold means fewer trades but higher conviction.

how to adjust: if you’re getting too few trades, lower it to 0.5 to let more signals through. if you’re seeing too many false entries, raise it to 1.0 for stricter filtering. test on your chart to find a balance.

spr_atr_length = input.int(21, "SPR ATR Length") this sets the ATR period (default 21 bars) used to normalize SPR’s momentum score. ATR measures volatility, so this makes SPR’s signal relative to market conditions.

how it works: a longer ATR period (like 21) smooths out volatility, making SPR less jumpy. a shorter one makes it more reactive.

how to adjust: if you’re trading a volatile stock like TSLA, a longer period (30 or 50) can help avoid noise. for a calmer stock, try 10 to make SPR more responsive. match this to your timeframe—shorter timeframes might need a shorter ATR.

rth_session = input.session("0930-1600","SPR: RTH Sess.") rth_timezone = "America/New_York" this defines the session SPR uses (0930-1600, New York time). SPR only calculates momentum during these hours to focus on RTH activity.

how it works: it ignores pre-market or after-hours noise, ensuring SPR captures the main market action.

how to adjust: if you trade a different session (like London hours, 0300-1200 EST), change the session to match. you can also adjust the timezone if you’re in a different region, like "Europe/London". just make sure your chart’s timezone aligns with this setting.

VWMO (Volume-Weighted Momentum Oscillator)

VWMO measures momentum weighted by volume to spot sustained, high-conviction moves.

vwmo_momlen = input.int(21, "VWMO Momentum Length") this sets how many bars back VWMO looks to calculate price momentum (default 21 bars). it takes the price change (close minus close 21 bars ago).

how it works: a longer period captures bigger trends, while a shorter one reacts to recent swings.

how to adjust: on a daily chart, 21 bars is about a month—good for trend trading. on a 5-minute chart, it’s just 105 minutes, so you might bump it to 50 or 100 for more meaningful moves. if you want faster signals, drop it to 10, but expect more noise.

vwmo_volback = input.int(30, "VWMO Volume Lookback") this sets the period for calculating average volume (default 30 bars). VWMO weights momentum by volume divided by this average.

how it works: it compares current volume to the average to see if a move has strong participation. a longer lookback smooths the average, while a shorter one makes it more sensitive.

how to adjust: for stocks with spiky volume (like NVDA on earnings), a longer lookback (50 or 100) avoids overreacting to one-off spikes. for steady volume stocks, try 20. match this to your timeframe—shorter timeframes might need a shorter lookback.

vwmo_smooth = input.int(9, "VWMO Smoothing")

this sets the SMA period to smooth VWMO’s raw momentum (default 9 bars).

how it works: smoothing reduces noise in the signal, making VWMO more reliable for voting. a longer smoothing period cuts more noise but adds lag.

how to adjust: if VWMO is too jumpy (lots of false votes), increase to 15. if it’s too slow and missing trades, drop to 5. test on your chart to see what keeps the signal clean but responsive.

vwmo_threshold = input.float(10, "VWMO Threshold") this is the cutoff for VWMO to vote for a trade (default 10). above 10, it votes for a long; below -10, a short.

how it works: it ensures only strong momentum signals count. a higher threshold means fewer but stronger trades.

how to adjust: if you want more trades, lower it to 5. if you’re getting too many weak signals, raise it to 15. this depends on your market—volatile stocks might need a higher threshold to filter noise.

VEI (Velocity Efficiency Index)

VEI measures market efficiency and velocity to filter out choppy moves and focus on strong trends.

vei_eflen = input.int(14, "VEI Efficiency Smoothing") this sets the EMA period for smoothing VEI’s efficiency calc (bar range / volume, default 14 bars).

how it works: efficiency is how much price moves per unit of volume. smoothing it with an EMA reduces noise, focusing on consistent efficiency. a longer period smooths more but adds lag.

how to adjust: for choppy markets, increase to 20 to filter out noise. for faster markets, drop to 10 for quicker signals. this should match your timeframe—shorter timeframes might need a shorter period.

vei_momlen = input.int(8, "VEI Momentum Length") this sets how many bars back VEI looks to calculate momentum in efficiency (default 8 bars).

how it works: it measures the change in smoothed efficiency over 8 bars, then adjusts for inertia (volume-to-range). a longer period captures bigger shifts, while a shorter one reacts faster.

how to adjust: if VEI is missing quick reversals, drop to 5. if it’s too noisy, raise to 12. test on your chart to see what catches the right moves without too many false signals.

vei_threshold = input.float(4.5, "VEI Threshold") this is the cutoff for VEI to vote for a trade (default 4.5). above 4.5, it votes for a long; below -4.5, a short.

how it works: it ensures only strong, efficient moves count. a higher threshold means fewer trades but higher quality.

how to adjust: if you’re not getting enough trades, lower to 3. if you’re seeing too many false entries, raise to 6. this depends on your market—fast stocks like NQ1 might need a lower threshold.

Features

Multi-Signal Voting: requires all three signals (SPR, VWMO, VEI) to align for a trade, ensuring high-probability setups.

Risk Management: uses ATR-based stops (2.1x) and take-profits (4.1x), with dynamic position sizing based on a risk percentage (default 0.4%).

Market Filters: ADX (default 27) ensures trending conditions, choppiness index (default 54.5) avoids sideways markets, and ATR expansion (default 1.12) confirms volatility.

Dashboard: provides real-time stats like SPR, VWMO, VEI values, net P/L, win rate, and streak, with a clean, functional design.

Visuals

EXODUS prioritizes performance over visuals, as it was built for competitive and competition purposes. entry/exit signals are marked with simple labels and shapes, and a basic heatmap highlights market regimes. a more visually stunning update may be released later, with enhanced graphics and overlays.

Usage

EXODUS is designed for stocks and ETFs but can be adapted for futures with adjustments. it performs best in trending markets with sufficient volatility, as confirmed by its generic tuning across symbols like TSLA, AMD, NVDA, and NQ1. adjust inputs like SPR threshold, VWMO smoothing, or VEI momentum length to suit specific assets or timeframes.

Setting I used: (Again, these are a generic setting, each security needs to be fine tuned)

SPR LB = 19 SPR TH = 0.5 SPR ATR L= 21 SPR RTH Sess: 9:30 – 16:00

VWMO L = 21 VWMO LB = 18 VWMO S = 6 VWMO T = 8

VEI ES = 14 VEI ML = 21 VEI T = 4

R % = 0.4

ATR L = 21 ATR M (S) =1.1 TP Multi = 2.1 ATR min mult = 0.8 ATR Expansion = 1.02

ADX L = 21 Min ADX = 25

Choppiness Index = 14 Chop. Max T = 55.5

Backtesting: TSLA

Frame: Jan 02, 2018, 08:00 — May 01, 2025, 09:00

Slippage: 3

Commission .01

Disclaimer

this strategy is for educational purposes. past performance is not indicative of future results. trading involves significant risk, and you should only trade with capital you can afford to lose. always backtest and validate any strategy before using it in live markets.

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

About the Author

Dskyz (DAFE) Trading Systems is dedicated to building high-performance trading algorithms. EXODUS is a product of rigorous research and development, aimed at delivering consistent, and data-driven trading solutions.

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Moving Average Shift WaveTrend StrategyMoving Average Shift WaveTrend Strategy

🧭 Overview

The Moving Average Shift WaveTrend Strategy is a trend-following and momentum-based trading system designed to be overlayed on TradingView charts. It executes trades based on the confluence of multiple technical conditions—volatility, session timing, trend direction, and oscillator momentum—to deliver logical and systematic trade entries and exits.

🎯 Strategy Objectives

Enter trades aligned with the prevailing long-term trend

Exit trades on confirmed momentum reversals

Avoid false signals using session timing and volatility filters

Apply structured risk management with automatic TP, SL, and trailing stops

⚙️ Key Features

Selectable MA types: SMA, EMA, SMMA (RMA), WMA, VWMA

Dual-filter logic using a custom oscillator and moving averages

Session and volatility filters to eliminate low-quality setups

Trailing stop, configurable Take Profit / Stop Loss logic

“In-wave flag” prevents overtrading within the same trend wave

Visual clarity with color-shifting candles and entry/exit markers

📈 Trading Rules

✅ Long Entry Conditions:

Price is above the selected MA

Oscillator is positive and rising

200-period EMA indicates an uptrend

ATR exceeds its median value (sufficient volatility)

Entry occurs between 09:00–17:00 (exchange time)

Not currently in an active wave

🔻 Short Entry Conditions:

Price is below the selected MA

Oscillator is negative and falling

200-period EMA indicates a downtrend

All other long-entry conditions are inverted

❌ Exit Conditions:

Take Profit or Stop Loss is hit

Opposing signals from oscillator and MA

Trailing stop is triggered

🛡️ Risk Management Parameters

Pair: ETH/USD

Timeframe: 4H

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 2% of account equity (adjustable)

Total Trades: 224

Backtest Period: May 24, 2016 — April 7, 2025

Note: Risk parameters are fully customizable to suit your trading style and broker conditions.

🔧 Trading Parameters & Filters

Time Filter: Trades allowed only between 09:00–17:00 (exchange time)

Volatility Filter: ATR must be above its median value

Trend Filter: Long-term 200-period EMA

📊 Technical Settings

Moving Average

Type: SMA

Length: 40

Source: hl2

Oscillator

Length: 15

Threshold: 0.5

Risk Management

Take Profit: 1.5%

Stop Loss: 1.0%

Trailing Stop: 1.0%

👁️ Visual Support

MA and oscillator color changes indicate directional bias

Clear chart markers show entry and exit points

Trailing stops and risk controls are transparently managed

🚀 Strategy Improvements & Uniqueness

In-wave flag avoids repeated entries within the same trend phase

Filtering based on time, volatility, and trend ensures higher-quality trades

Dynamic high/low tracking allows precise trailing stop placement

Fully rule-based execution reduces emotional decision-making

💡 Inspirations & Attribution

This strategy is inspired by the excellent concept from:

ChartPrime – “Moving Average Shift”

It expands on the original idea with advanced trade filters and trailing logic.

Source reference:

📌 Summary

The Moving Average Shift WaveTrend Strategy offers a rule-based, reliable approach to trend trading. By combining trend and momentum filters with robust risk controls, it provides a consistent framework suitable for various market conditions and trading styles.

⚠️ Disclaimer

This script is for educational purposes only. Trading involves risk. Always use proper backtesting and risk evaluation before applying in live markets.

TrendTwisterV1.5 (Forex Ready + Indicators)A Precision Trend-Following TradingView Strategy for Forex**

HullShiftFX is a Pine Script strategy for TradingView that combines the power of the **Hull Moving Average (HMA)** and a **shifted Exponential Moving Average (EMA)** with multi-layered momentum filters including **RSI** and **dual Stochastic Oscillators**.

It’s designed for traders looking to catch high-probability breakouts with tight risk management and visual clarity.

Chart settings:

1. Select "Auto - Fits data to screen"

2. Please Select "Scale Price Chart Only" (To make the chart not squished)

### ✅ Entry Conditions

**Long Position:**

- Price closes above the 12-period Hull Moving Average.

- Price closes above the 5-period EMA shifted forward by 2 bars.

- RSI is above 50.

- Stochastic Oscillator (12,3,3) %K is above 50.

- Stochastic Oscillator (5,3,3) %K is above 50.

- Hull MA crosses above the shifted EMA.

**Short Position:**

- Price closes below the 12-period Hull Moving Average.

- Price closes below the 5-period EMA shifted forward by 2 bars.

- RSI is below 50.

- Stochastic Oscillator (12,3,3) %K is below 50.

- Stochastic Oscillator (5,3,3) %K is below 50.

- Hull MA crosses below the shifted EMA.

---

## 📉 Risk Management

- **Stop Loss:** Set at the low (for long) or high (for short) of the previous 2 candles.

- **Take Profit:** Calculated at a risk/reward ratio of **1.65x** the stop loss distance.

---

## 📊 Indicators Used

- **Hull Moving Average (12)**

- **Exponential Moving Average (5) **

- **Relative Strength Index (14)**

- **Stochastic Oscillators:**

- %K (12,3,3)

- %K (5,3,3)

RSI Pro+ (Bear market, financial crisis and so on EditionIn markets defined by volatility, fear, and uncertainty – the battlegrounds of bear markets and financial crises – you need tools forged in resilience. Introducing RSI Pro+, a strategy built upon a legendary indicator born in 1978, yet engineered with modern visual clarity to remain devastatingly effective even in the chaotic financial landscapes of 3078.

This isn't about complex algorithms predicting the unpredictable. It's about harnessing the raw, time-tested power of the Relative Strength Index (RSI) to identify potential exhaustion points and capitalize on oversold conditions. RSI Pro+ cuts through the noise, providing clear, actionable signals when markets might be poised for a relief bounce or reversal.

Core Technology (The 1978 Engine):

RSI Crossover Entry: The strategy initiates a LONG position when the RSI (default period 11) crosses above a user-defined low threshold (default 30). This classic technique aims to enter when selling pressure may be waning, offering potential entry points during sharp downturns or periods of consolidation after a fall.

Modern Enhancements (The 3078 Cockpit):

RSI Pro+ isn't just about the signal; it's about providing a professional-grade visual experience directly on your chart:

Entry Bar Highlight: A subtle background flash on the chart signals the exact bar where the RSI crossover condition is met, alerting you to potential entry opportunities.

Trade Bar Coloring: Once a trade is active, the price bars are subtly colored, giving you immediate visual confirmation that the strategy is live in the market.

Entry Price Line: A clear, persistent line marks your exact average entry price for the duration of the trade, serving as a crucial visual anchor.

Take Profit Line: Your calculated Take Profit target is plotted as a distinct line, keeping your objective clearly in sight.

Custom Entry Marker: A precise shape (▲) appears below the bar where the trade entry was actually executed, pinpointing the start of the position.

On-Chart Info Table (HUD): A clean, customizable Heads-Up Display appears when a trade is active, showing vital information at a glance:

Entry Price: Your position's average cost basis.

TP Target: The calculated price level for your Take Profit exit.

Current PnL%: Real-time Profit/Loss percentage for the open trade.

Full Customization: Nearly every aspect is configurable via the settings menu:

RSI Period & Crossover Level

Take Profit Percentage

Toggle ALL visual enhancements on/off individually

Position the Info Table wherever you prefer on the chart.

How to Use RSI Pro+:

Add to Chart: Apply the "RSI Pro+ (Bear market...)" strategy to your TradingView chart. Ensure any previous versions are removed.

Access Settings: Click the cogwheel icon (⚙️) next to the strategy name on your chart.

Configure Inputs (Crucial Step):

RSI Crossover Level: This is key. The default (30) targets standard oversold conditions. In severe downturns, you might experiment with lower levels (e.g., 25, 20) or higher ones (e.g., 40) depending on the asset and timeframe. Observe where RSI(11) typically bottoms out on your chart.

Take Profit Percentage (%): Define your desired profit target per trade (e.g., enter 0.5 for 0.5%, 1.0 for 1%). The default is a very small 0.11%.

RSI Period: While default is 11, you can adjust this (e.g., the standard 14).

Visual Enhancements: Enable or disable the visual features (background highlights, bar coloring, lines, markers, table) according to your preference using the checkboxes. Adjust table position.

Observe & Backtest: Watch how the strategy behaves on your chosen asset and timeframe. Use TradingView's Strategy Tester to analyze historical performance based on your settings. No strategy works perfectly everywhere; testing is essential.

Important Considerations:

Risk Management: This specific script version focuses on a Take Profit exit. It does not include an explicit Stop Loss. You MUST manage risk through appropriate position sizing, potentially adding a Stop Loss manually, or by modifying the script.

Oversold ≠ Reversal: An RSI crossover is an indicator of potential exhaustion, not a guarantee of a price reversal.

Fixed TP: A fixed percentage TP ensures small wins but may exit before larger potential moves.

Backtesting Limitations: Past performance does not guarantee future results.

RSI Pro+ strips away complexity to focus on a robust, time-honored principle, enhanced with modern visuals for the discerning trader navigating today's (and tomorrow's) challenging markets

Adaptive KDJ (MTF)Hey guys,

this is an adaptive MTF KDJ oscillator.

Pick up to 3 different timeframes, choose a weighting if you want and enjoy the beautiful signals it will show you.

The length of every timeframe is adaptive and based of the timeframe's ATR.

The plot shows the smoothed average of the 3 KDJ values.

Large triangles show KDJ crossings.

Small triangles show anticipations of possible crossings.

I found out it works best with 1m, 5m, 15m and weighting=1 for forex scalping in 1m.

Use other indicators for confluence.

TEMA OBOS Strategy PakunTEMA OBOS Strategy

Overview

This strategy combines a trend-following approach using the Triple Exponential Moving Average (TEMA) with Overbought/Oversold (OBOS) indicator filtering.

By utilizing TEMA crossovers to determine trend direction and OBOS as a filter, it aims to improve entry precision.

This strategy can be applied to markets such as Forex, Stocks, and Crypto, and is particularly designed for mid-term timeframes (5-minute to 1-hour charts).

Strategy Objectives

Identify trend direction using TEMA

Use OBOS to filter out overbought/oversold conditions

Implement ATR-based dynamic risk management

Key Features

1. Trend Analysis Using TEMA

Uses crossover of short-term EMA (ema3) and long-term EMA (ema4) to determine entries.

ema4 acts as the primary trend filter.

2. Overbought/Oversold (OBOS) Filtering

Long Entry Condition: up > down (bullish trend confirmed)

Short Entry Condition: up < down (bearish trend confirmed)

Reduces unnecessary trades by filtering extreme market conditions.

3. ATR-Based Take Profit (TP) & Stop Loss (SL)

Adjustable ATR multiplier for TP/SL

Default settings:

TP = ATR × 5

SL = ATR × 2

Fully customizable risk parameters.

4. Customizable Parameters

TEMA Length (for trend calculation)

OBOS Length (for overbought/oversold detection)

Take Profit Multiplier

Stop Loss Multiplier

EMA Display (Enable/Disable TEMA lines)

Bar Color Change (Enable/Disable candle coloring)

Trading Rules

Long Entry (Buy Entry)

ema3 crosses above ema4 (Golden Cross)

OBOS indicator confirms up > down (bullish trend)

Execute a buy position

Short Entry (Sell Entry)

ema3 crosses below ema4 (Death Cross)

OBOS indicator confirms up < down (bearish trend)

Execute a sell position

Take Profit (TP)

Entry Price + (ATR × TP Multiplier) (Default: 5)

Stop Loss (SL)

Entry Price - (ATR × SL Multiplier) (Default: 2)

TP/SL settings are fully customizable to fine-tune risk management.

Risk Management Parameters

This strategy emphasizes proper position sizing and risk control to balance risk and return.

Trading Parameters & Considerations

Initial Account Balance: $7,000 (adjustable)

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 128

Deep Test Results (2024/11/01 - 2025/02/24)BTCUSD-5M

Total P&L:+1638.20USD

Max equity drawdown:694.78USD

Total trades:128

Profitable trades:44.53

Profit factor:1.45

These settings aim to protect capital while maintaining a balanced risk-reward approach.

Visual Support

TEMA Lines (Three EMAs)

Trend direction is indicated by color changes (Blue/Orange)

ema3 (short-term) and ema4 (long-term) crossover signals potential entries

OBOS Histogram

Green → Strong buying pressure

Red → Strong selling pressure

Blue → Possible trend reversal

Entry & Exit Markers

Blue Arrow → Long Entry Signal

Red Arrow → Short Entry Signal

Take Profit / Stop Loss levels displayed

Strategy Improvements & Uniqueness

This strategy is based on indicators developed by "l_lonthoff" and "jdmonto0", but has been significantly optimized for better entry accuracy, visual clarity, and risk management.

Enhanced Trend Identification with TEMA

Detects early trend reversals using ema3 & ema4 crossover

Reduces market noise for a smoother trend-following approach

Improved OBOS Filtering

Prevents excessive trading

Reduces unnecessary risk exposure

Dynamic Risk Management with ATR-Based TP/SL

Not a fixed value → TP/SL adjusts to market volatility

Fully customizable ATR multiplier settings

(Default: TP = ATR × 5, SL = ATR × 2)

Summary

The TEMA + OBOS Strategy is a simple yet powerful trading method that integrates trend analysis and oscillators.

TEMA for trend identification

OBOS for noise reduction & overbought/oversold filtering

ATR-based TP/SL settings for dynamic risk management

Before using this strategy, ensure thorough backtesting and demo trading to fine-tune parameters according to your trading style.

Balance of Power for US30 4H [PineIndicators]The Balance of Power (BoP) Strategy is a momentum-based trading system for the US30 index on a 4-hour timeframe. It measures the strength of buyers versus sellers in each candle using the Balance of Power (BoP) indicator and executes trades based on predefined threshold crossovers. The strategy includes dynamic position sizing, adjustable leverage, and visual trade tracking.

⚙️ Core Strategy Mechanics

Positive values indicate buying strength.

Negative values indicate selling strength.

Values close to 1 suggest strong bullish momentum.

Values close to -1 indicate strong bearish pressure.

The strategy uses fixed threshold crossovers to determine trade entries and exits.

📌 Trade Logic

Entry Conditions

Long Entry: When BoP crosses above 0.8, signaling strong buying pressure.

Exit Conditions

Position Close: When BoP crosses below -0.8, indicating a shift to selling pressure.

This threshold-based system filters out low-confidence signals and focuses on high-momentum shifts.

📏 Position Sizing & Leverage

Leverage: Adjustable by the user (default = 5x).

Risk Management: Position size adapts dynamically based on equity fluctuations.

📊 Trade Visualization & History Tracking

Trade Markers:

"Buy" labels appear when a long position is opened.

"Close" labels appear when a position is exited.

Trade History Boxes:

Green for profitable trades.

Red for losing trades.

These elements provide clear visual tracking of past trade execution.

⚡ Usage & Customization

1️⃣ Apply the script to a US30 4H chart in TradingView.

2️⃣ Adjust leverage settings as needed.

3️⃣ Review trade signals and historical performance with visual markers.

4️⃣ Enable backtesting to evaluate past performance.

This strategy is designed for momentum-based trading and is best suited for volatile market conditions.

[SHORT ONLY] Internal Bar Strength (IBS) Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "Internal Bar Strength (IBS) Strategy" is a mean-reversion strategy designed to identify trading opportunities based on the closing price's position within the daily price range. It enters a short position when the IBS indicates overbought conditions and exits when the IBS reaches oversold levels. This strategy is Short-Only and was designed to be used on the Daily timeframe for Stocks and ETFs.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

- Low IBS (≤ 0.2) : Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8) : Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The IBS value rises to or above the Upper Threshold (default: 0.9).

The Closing price is greater than the previous bars High (close>high ).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

An exit Signal is generated when the IBS value drops to or below the Lower Threshold (default: 0.3). This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Upper Threshold: The IBS level at which the strategy enters trades. Default is 0.9.

Lower Threshold: The IBS level at which the strategy exits short positions. Default is 0.3.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for Stocks and ETFs markets and performs best when prices frequently revert to the mean.

The strategy can be optimized further using additional conditions such as using volume or volatility filters.

It is sensitive to extreme IBS values, which help identify potential reversals.

Backtesting results should be analyzed to optimize the Upper/Lower Thresholds for specific instruments and market conditions.

Iron Bot Statistical Trend Filter📌 Iron Bot Statistical Trend Filter

📌 Overview

Iron Bot Statistical Trend Filter is an advanced trend filtering strategy that combines statistical methods with technical analysis.

By leveraging Z-score and Fibonacci levels, this strategy quantitatively analyzes market trends to provide high-precision entry signals.

Additionally, it includes an optional EMA filter to enhance trend reliability.

Risk management is reinforced with Stop Loss (SL) and four Take Profit (TP) levels, ensuring a balanced approach to risk and reward.

📌 Key Features

🔹 1. Statistical Trend Filtering with Z-Score

This strategy calculates the Z-score to measure how much the price deviates from its historical mean.

Positive Z-score: Indicates a statistically high price, suggesting a strong uptrend.

Negative Z-score: Indicates a statistically low price, signaling a potential downtrend.

Z-score near zero: Suggests a ranging market with no strong trend.

By using the Z-score as a filter, market noise is reduced, leading to more reliable entry signals.

🔹 2. Fibonacci Levels for Trend Reversal Detection

The strategy integrates Fibonacci retracement levels to identify potential reversal points in the market.

High Trend Level (Fibo 23.6%): When the price surpasses this level, an uptrend is likely.

Low Trend Level (Fibo 78.6%): When the price falls below this level, a downtrend is expected.

Trend Line (Fibo 50%): Acts as a midpoint, helping to assess market balance.

This allows traders to visually confirm trend strength and turning points, improving entry accuracy.

🔹 3. EMA Filter for Trend Confirmation (Optional)

The strategy includes an optional 200 EMA (Exponential Moving Average) filter for trend validation.

Price above 200 EMA: Indicates a bullish trend (long entries preferred).

Price below 200 EMA: Indicates a bearish trend (short entries preferred).

Enabling this filter reduces false signals and improves trend-following accuracy.

🔹 4. Multi-Level Take Profit (TP) and Stop Loss (SL) Management

To ensure effective risk management, the strategy includes four Take Profit levels and a Stop Loss:

Stop Loss (SL): Automatically closes trades when the price moves against the position by a certain percentage.

TP1 (+0.75%): First profit-taking level.

TP2 (+1.1%): A higher probability profit target.

TP3 (+1.5%): Aiming for a stronger trend move.

TP4 (+2.0%): Maximum profit target.

This system secures profits at different stages and optimizes risk-reward balance.

🔹 5. Automated Long & Short Trading Logic

The strategy is built using Pine Script®’s strategy.entry() and strategy.exit(), allowing fully automated trading.

Long Entry:

Price is above the trend line & high trend level.

Z-score is positive (indicating an uptrend).

(Optional) Price is also above the EMA for stronger confirmation.

Short Entry:

Price is below the trend line & low trend level.

Z-score is negative (indicating a downtrend).

(Optional) Price is also below the EMA for stronger confirmation.

This logic helps filter out unnecessary trades and focus only on high-probability entries.

📌 Trading Parameters

This strategy is designed for flexible capital management and risk control.

💰 Account Size: $5000

📉 Commissions and Slippage: Assumes 94 pips commission per trade and 1 pip slippage.

⚖️ Risk per Trade: Adjustable, with a default setting of 1% of equity.

These parameters help preserve capital while optimizing the risk-reward balance.

📌 Visual Aids for Clarity

To enhance usability, the strategy includes clear visual elements for easy market analysis.

✅ Trend Line (Blue): Indicates market midpoint and helps with entry decisions.

✅ Fibonacci Levels (Yellow): Highlights high and low trend levels.

✅ EMA Line (Green, Optional): Confirms long-term trend direction.

✅ Entry Signals (Green for Long, Red for Short): Clearly marked buy and sell signals.

These features allow traders to quickly interpret market conditions, even without advanced technical analysis skills.

📌 Originality & Enhancements

This strategy is developed based on the IronXtreme and BigBeluga indicators,

combining a unique Z-score statistical method with Fibonacci trend analysis.

Compared to conventional trend-following strategies, it leverages statistical techniques

to provide higher-precision entry signals, reducing false trades and improving overall reliability.

📌 Summary

Iron Bot Statistical Trend Filter is a statistically-driven trend strategy that utilizes Z-score and Fibonacci levels.

High-precision trend analysis

Enhanced accuracy with an optional EMA filter

Optimized risk management with multiple TP & SL levels

Visually intuitive chart design

Fully customizable parameters & leverage support

This strategy reduces false signals and helps traders ride the trend with confidence.

Try it out and take your trading to the next level! 🚀

Statistical Arbitrage Pairs Trading - Long-Side OnlyThis strategy implements a simplified statistical arbitrage (" stat arb ") approach focused on mean reversion between two correlated instruments. It identifies opportunities where the spread between their normalized price series (Z-scores) deviates significantly from historical norms, then executes long-only trades anticipating reversion to the mean.

Key Mechanics:

1. Spread Calculation: The strategy computes Z-scores for both instruments to normalize price movements, then tracks the spread between these Z-scores.

2. Modified Z-Score: Uses a robust measure combining the median and Median Absolute Deviation (MAD) to reduce outlier sensitivity.

3. Entry Signal: A long position is triggered when the spread’s modified Z-score falls below a user-defined threshold (e.g., -1.0), indicating extreme undervaluation of the main instrument relative to its pair.

4. Exit Signal: The position closes automatically when the spread reverts to its historical mean (Z-score ≥ 0).

Risk management:

Trades are sized as a percentage of equity (default: 10%).

Includes commissions and slippage for realistic backtesting.