Monte Carlo Simulation - Your Strategy [Kioseff Trading]Hello!

This script “Monte Carlo Simulation - Your Strategy” uses Monte Carlo simulations for your inputted strategy returns or the asset on your chart!

Features

Monte Carlo Simulation: Performs Monte Carlo simulation to generate multiple future paths.

Asset Price or Strategy: Can simulate either future asset prices based on historical log returns or a specific trading strategy's future performance.

User-Defined Input: Allows you to input your own historical returns for simulation.

Statistical Methods: Offers two simulation methods—Gaussian (Normal) distribution and Bootstrapping.

Graphical Display: Provides options for graphical representation, including line plots and histograms.

Cumulative Probability Target: Enables setting a user-defined cumulative probability target to quantify simulation results.

Adjustable Parameters: Offers numerous user-adjustable settings like number of simulations, forecast length, and more.

Historical Data Points: Option to specify the amount of historical data to be used in the simulation (price).

Custom Binning: Allows you to select the binning method for histograms, with options like Sturges, Rice, and Square Root.

Best/Worst Case: Allows you to show only the best case / worst case outcome (range) for all simulations!

Scatterplot: allows you to show up to 1000 potential outcomes for a specified trade number (or bars forward price endpoint) using a scatter plot.

The image above shows the primary components of the indicator!

The image above shows the best/worst case outcome feature in action!

The image above shows a "fun feature" where 1000 simulated end points for a 15-bar price trajectory are shown as a scatter plot!

How To Perform a Monte Carlo Simulation On Your Strategy

Really, you can input any data into the indicator it will perform a Monte Carlo Simulation on it :D

The following instructions show how to export your strategy results from TradingView to an Excel File, copy the data, and input it into the indicator.

However , you are not limited to following this method!

Wherever your strategy results are stored, simply copy and paste them into the indicator text area in the settings and simulations will begin.

Returns Should Follow This Format

1

3

-3

2

-5

The numbers are presented as a single column. No commas or separators used.

The numbers above are in sequential order. A return of "1" for the first trade and a return of "-5" for the last trade. Your strategy returns will likely be in sequential order already so don't worry too much about this (:

How To Perform a Monte Carlo Simulation On Your TradingView Strategy With Excel Data

Export your strategy returns to an excel file using TradingView

Navigate to your downloads folder to column G "Profit"

Click the column and press CTRL + SPACE to highlight the entire column

Press CTRL + C to copy the entire column

Open this indicator's settings and paste the returns into the text area

The image above illustrates the process!

Notes on Inputting Returns

*Must input your returns without a separate as a vertical list

*The initial text area can only hold so many return values. If your list of trades is large you can input additional returns into two additional text areas at the bottom of the indicator settings.

That should be it; thank you for checking this out!

Indikator dan strategi

Statistical Package for the Trading Sciences [SS]

This is SPTS.

It stands for Statistical Package for the Trading Sciences.

Its a play on SPSS (Statistical Package for the Social Sciences) by IBM (software that, prior to Pinescript, I would use on a daily basis for trading).

Let's preface this indicator first:

This isn't so much an indicator as it is a project. A passion project really.

This has been in the works for months and I still feel like its incomplete. But the plan here is to continue to add functionality to it and actually have the Pinecoding and Tradingview community contribute to it.

As a math based trader, I relied on Excel, SPSS and R constantly to plan my trades. Since learning a functional amount of Pinescript and coding a lot of what I do and what I relied on SPSS, Excel and R for, I use it perhaps maybe a few times a week.

This indicator, or package, has some of the key things I used Excel and SPSS for on a daily and weekly basis. This also adds a lot of, I would say, fairly complex math functionality to Pinescript. Because this is adding functionality not necessarily native to Pinescript, I have placed most, if not all, of the functionality into actual exportable functions. I have also set it up as a kind of library, with explanations and tips on how other coders can take these functions and implement them into other scripts.

The hope here is that other coders will take it, build upon it, improve it and hopefully share additional functionality that can be added into this package. Hence why I call it a project. Okay, let's get into an overview:

Current Functions of SPTS:

SPTS currently has the following functionality (further explanations will be offered below):

Ability to Perform a One-Tailed, Two-Tailed and Paired Sample T-Test, with corresponding P value.

Standard Pearson Correlation (with functionality to be able to calculate the Pearson Correlation between 2 arrays).

Quadratic (or Curvlinear) correlation assessments.

R squared Assessments.

Standard Linear Regression.

Multiple Regression of 2 independent variables.

Tests of Normality (with Kurtosis and Skewness) and recognition of up to 7 Different Distributions.

ARIMA Modeller (Sort of, more details below)

Okay, so let's go over each of them!

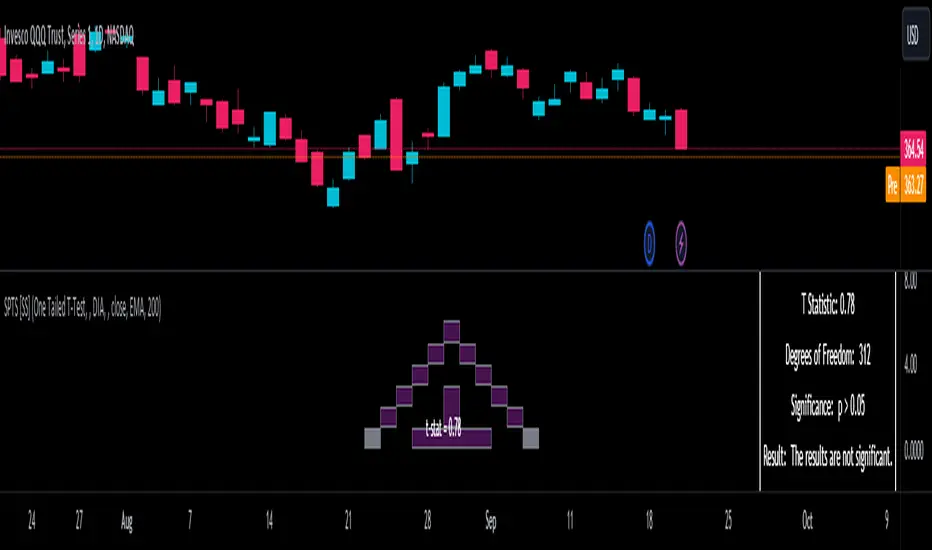

T-Tests

So traditionally, most correlation assessments on Pinescript are done with a generic Pearson Correlation using the "ta.correlation" argument. However, this is not always the best test to be used for correlations and determine effects. One approach to correlation assessments used frequently in economics is the T-Test assessment.

The t-test is a statistical hypothesis test used to determine if there is a significant difference between the means of two groups. It assesses whether the sample means are likely to have come from populations with the same mean. The test produces a t-statistic, which is then compared to a critical value from the t-distribution to determine statistical significance. Lower p-values indicate stronger evidence against the null hypothesis of equal means.

A significant t-test result, indicating the rejection of the null hypothesis, suggests that there is statistical evidence to support that there is a significant difference between the means of the two groups being compared. In practical terms, it means that the observed difference in sample means is unlikely to have occurred by random chance alone. Researchers typically interpret this as evidence that there is a real, meaningful difference between the groups being studied.

Some uses of the T-Test in finance include:

Risk Assessment: The t-test can be used to compare the risk profiles of different financial assets or portfolios. It helps investors assess whether the differences in returns or volatility are statistically significant.

Pairs Trading: Traders often apply the t-test when engaging in pairs trading, a strategy that involves trading two correlated securities. It helps determine when the price spread between the two assets is statistically significant and may revert to the mean.

Volatility Analysis: Traders and risk managers use t-tests to compare the volatility of different assets or portfolios, assessing whether one is significantly more or less volatile than another.

Market Efficiency Tests: Financial researchers use t-tests to test the Efficient Market Hypothesis by assessing whether stock price movements follow a random walk or if there are statistically significant deviations from it.

Value at Risk (VaR) Calculation: Risk managers use t-tests to calculate VaR, a measure of potential losses in a portfolio. It helps assess whether a portfolio's value is likely to fall below a certain threshold.

There are many other applications, but these are a few of the highlights. SPTS permits 3 different types of T-Test analyses, these being the One Tailed T-Test (if you want to test a single direction), two tailed T-Test (if you are unsure of which direction is significant) and a paired sample t-test.

Which T is the Right T?

Generally, a one-tailed t-test is used to determine if a sample mean is significantly greater than or less than a specified population mean, whereas a two-tailed t-test assesses if the sample mean is significantly different (either greater or less) from the population mean. In contrast, a paired sample t-test compares two sets of paired observations (e.g., before and after treatment) to assess if there's a significant difference in their means, typically used when the data points in each pair are related or dependent.

So which do you use? Well, it depends on what you want to know. As a general rule a one tailed t-test is sufficient and will help you pinpoint directionality of the relationship (that one ticker or economic indicator has a significant affect on another in a linear way).

A two tailed is more broad and looks for significance in either direction.

A paired sample t-test usually looks at identical groups to see if one group has a statistically different outcome. This is usually used in clinical trials to compare treatment interventions in identical groups. It's use in finance is somewhat limited, but it is invaluable when you want to compare equities that track the same thing (for example SPX vs SPY vs ES1!) or you want to test a hypothesis about an index and a leveraged share (for example, the relationship between FNGU and, say, MSFT or NVDA).

Statistical Significance

In general, with a t-test you would need to reference a T-Table to determine the statistical significance of the degree of Freedom and the T-Statistic.

However, because I wanted Pinescript to full fledge replace SPSS and Excel, I went ahead and threw the T-Table into an array, so that Pinescript can make the determination itself of the actual P value for a t-test, no cross referencing required :-).

Left tail (Significant):

Both tails (Significant):

Distributed throughout (insignificant):

As you can see in the images above, the t-test will also display a bell-curve analysis of where the significance falls (left tail, both tails or insignificant, distributed throughout).

That said, I have not included this function for the paired sample t-test because that is a bit more nuanced. But for the one and two tailed assessments, the indicator will provide you the P value.

Pearson Correlation Assessment

I don't think I need to go into too much detail on this one.

I have put in functionality to quickly calculate the Pearson Correlation of two array's, which is not currently possible with the "ta.correlation" function.

Quadratic (Curvlinear) Correlation

Not everything in life is linear, sometimes things are curved!

The Pearson Correlation is great for linear assessments, but tends to under-estimate the degree of the relationship in curved relationships. There currently is no native function to t-test for quadratic/curvlinear relationships, so I went ahead and created one.

You can see an example of how Quadratic and Pearson Correlations vary when you look at CME_MINI:ES1! against AMEX:DIA for the past 10 ish months:

Pearson Correlation:

Quadratic Correlation:

One or the other is not always the best, so it is important to check both!

R-Squared Assessments:

The R-squared value, or the square of the Pearson correlation coefficient (r), is used to measure the proportion of variance in one variable that can be explained by the linear relationship with another variable. It represents the goodness-of-fit of a linear regression model with a single predictor variable.

R-Squared is offered in 3 separate forms within this indicator. First, there is the generic R squared which is taking the square root of a Pearson Correlation assessment to assess the variance.

The next is the R-Squared which is calculated from an actual linear regression model done within the indicator.

The first is the R-Squared which is calculated from a multiple regression model done within the indicator.

Regardless of which R-Squared value you are using, the meaning is the same. R-Square assesses the variance between the variables under assessment and can offer an insight into the goodness of fit and the ability of the model to account for the degree of variance.

Here is the R Squared assessment of the SPX against the US Money Supply:

Standard Linear Regression

The indicator contains the ability to do a standard linear regression model. You can convert one ticker or economic indicator into a stock, ticker or other economic indicator. The indicator will provide you with all of the expected information from a linear regression model, including the coefficients, intercept, error assessments, correlation and R2 value.

Here is AAPL and MSFT as an example:

Multiple Regression

Oh man, this was something I really wanted in Pinescript, and now we have it!

I have created a function for multiple regression, which, if you export the function, will permit you to perform multiple regression on any variables available in Pinescript!

Using this functionality in the indicator, you will need to select 2, dependent variables and a single independent variable.

Here is an example of multiple regression for NASDAQ:AAPL using NASDAQ:MSFT and NASDAQ:NVDA :

And an example of SPX using the US Money Supply (M2) and AMEX:GLD :

Tests of Normality:

Many indicators perform a lot of functions on the assumption of normality, yet there are no indicators that actually test that assumption!

So, I have inputted a function to assess for normality. It uses the Kurtosis and Skewness to determine up to 7 different distribution types and it will explain the implication of the distribution. Here is an example of SP:SPX on the Monthly Perspective since 2010:

And NYSE:BA since the 60s:

And NVDA since 2015:

ARIMA Modeller

Okay, so let me disclose, this isn't a full fledge ARIMA modeller. I took some shortcuts.

True ARIMA modelling would involve decomposing the seasonality from the trend. I omitted this step for simplicity sake. Instead, you can select between using an EMA or SMA based approach, and it will perform an autogressive type analysis on the EMA or SMA.

I have tested it on lookback with results provided by SPSS and this actually works better than SPSS' ARIMA function. So I am actually kind of impressed.

You will need to input your parameters for the ARIMA model, I usually would do a 14, 21 and 50 day EMA of the close price, and it will forecast out that range over the length of the EMA.

So for example, if you select the EMA 50 on the daily, it will plot out the forecast for the next 50 days based on an autoregressive model created on the EMA 50. Here is how it looks on AMEX:SPY :

You can also elect to plot the upper and lower confidence bands:

Closing Remarks

So that is the indicator/package.

I do hope to continue expanding its functionality, but as of now, it does already have quite a lot of functionality.

I really hope you enjoy it and find it helpful. This. Has. Taken. AGES! No joke. Between referencing my old statistics textbooks, trying to remember how to calculate some of these things, and wanting to throw my computer against the wall because of errors in the code, this was a task, that's for sure. So I really hope you find some usefulness in it all and enjoy the ability to be able to do functions that previously could really only be done in external software.

As always, leave your comments, suggestions and feedback below!

Take care!

Position Cost DistributionThe Position Cost Distribution indicator (also known as the Market Position Overview, Chip Distribution, or CYQ Algorithm) provides an estimate of how shares are distributed across different price levels. Visually, it resembles the Volume Profile indicator, though they rely on distinct computational approaches.

🟠 Principle

The Position Cost Distribution algorithm is based on the principle that a security's total shares outstanding usually remains constant, except under conditions like stock splits, reverse splits, or new share issuance. It views all trading activity as simply exchanging share positions between holders at different price points.

By analyzing daily trade volume and the prior day's distribution, the algorithm infers the resulting share distribution after each day. By tracking these inferred transpositions over time, the indicator builds up an aggregate view of the estimated share concentration at each price level. This provides insights into potential buying and selling pressure zones that could form support or resistance areas.

Together with the Volume Profile, the Position Cost Distribution gives traders multiple lenses for examining market structure from both a volume and positional standpoint. Both can help identify meaningful technical price levels.

🟠 Algorithm

The algorithm initializes by allocating all shares to the price range encompassed by the first bar displayed on the chart. Preferably, the chart window should include the stock's IPO date, allowing the model to distribute shares specifically to the IPO price.

For subsequent trading sessions, the indicator performs the following calculations:

1. The daily turnover ratio is calculated by dividing the bar's trading volume by total outstanding shares.

2. For each price level (bucket), the number of shares is reduced by the turnover amount to represent shares transferring from existing holders.

3. The bar's total volume is then added to buckets corresponding to that period's price range.

Currently, the model assumes each share has an equal probability of being exchanged, regardless of how long ago it was acquired or at what price. Potential optimizations could incorporate factors like making shares held longer face a smaller chance of transfer compared to more recently purchased shares.

────────────────────────────────────────────

中文介绍:该指标为“筹码分布”的一个 TradingView 实现 :)

[Excalibur] Ehlers AutoCorrelation Periodogram ModifiedKeep your coins folks, I don't need them, don't want them. If you wish be generous, I do hope that charitable peoples worldwide with surplus food stocks may consider stocking local food banks before stuffing monetary bank vaults, for the crusade of remedying the needs of less than fortunate children, parents, elderly, homeless veterans, and everyone else who deserves nutritional sustenance for the soul.

DEDICATION:

This script is dedicated to the memory of Nikolai Dmitriyevich Kondratiev (Никола́й Дми́триевич Кондра́тьев) as tribute for being a pioneering economist and statistician, paving the way for modern econometrics by advocation of rigorous and empirical methodologies. One of his most substantial contributions to the study of business cycle theory include a revolutionary hypothesis recognizing the existence of dynamic cycle-like phenomenon inherent to economies that are characterized by distinct phases of expansion, stagnation, recession and recovery, what we now know as "Kondratiev Waves" (K-waves). Kondratiev was one of the first economists to recognize the vital significance of applying quantitative analysis on empirical data to evaluate economic dynamics by means of statistical methods. His understanding was that conceptual models alone were insufficient to adequately interpret real-world economic conditions, and that sophisticated analysis was necessary to better comprehend the nature of trending/cycling economic behaviors. Additionally, he recognized prosperous economic cycles were predominantly driven by a combination of technological innovations and infrastructure investments that resulted in profound implications for economic growth and development.

I will mention this... nation's economies MUST be supported and defended to continuously evolve incrementally in order to flourish in perpetuity OR suffer through eras with lasting ramifications of societal stagnation and implosion.

Analogous to the realm of economics, aperiodic cycles/frequencies, both enduring and ephemeral, do exist in all facets of life, every second of every day. To name a few that any blind man can naturally see are: heartbeat (cardiac cycles), respiration rates, circadian rhythms of sleep, powerful magnetic solar cycles, seasonal cycles, lunar cycles, weather patterns, vegetative growth cycles, and ocean waves. Do not pretend for one second that these basic aforementioned examples do not affect business cycle fluctuations in minuscule and monumental ways hour to hour, day to day, season to season, year to year, and decade to decade in every nation on the planet. Kondratiev's original seminal theories in macroeconomics from nearly a century ago have proven remarkably prescient with many of his antiquated elementary observations/notions/hypotheses in macroeconomics being scholastically studied and topically researched further. Therefore, I am compelled to honor and recognize his statistical insight and foresight.

If only.. Kondratiev could hold a pocket sized computer in the cup of both hands bearing the TradingView logo and platform services, I truly believe he would be amazed in marvelous delight with a GARGANTUAN smile on his face.

INTRODUCTION:

Firstly, this is NOT technically speaking an indicator like most others. I would describe it as an advanced cycle period detector to obtain market data spectral estimates with low latency and moderate frequency resolution. Developers can take advantage of this detector by creating scripts that utilize a "Dominant Cycle Source" input to adaptively govern algorithms. Be forewarned, I would only recommend this for advanced developers, not novice code dabbling. Although, there is some Pine wizardry introduced here for novice Pine enthusiasts to witness and learn from. AI did describe the code into one super-crunched sentence as, "a rare feat of exceptionally formatted code masterfully balancing visual clarity, precision, and complexity to provide immense educational value for both programming newcomers and expert Pine coders alike."

Understand all of the above aforementioned? Buckle up and proceed for a lengthy read of verbose complexity...

This is my enhanced and heavily modified version of autocorrelation periodogram (ACP) for Pine Script v5.0. It was originally devised by the mathemagician John Ehlers for detecting dominant cycles (frequencies) in an asset's price action. I have been sitting on code similar to this for a long time, but I decided to unleash the advanced code with my fashion. Originally Ehlers released this with multiple versions, one in a 2016 TASC article and the other in his last published 2013 book "Cycle Analytics for Traders", chapter 8. He wasn't joking about "concepts of advanced technical trading" and ACP is nowhere near to his most intimidating and ingenious calculations in code. I will say the book goes into many finer details about the original periodogram, so if you wish to delve into even more elaborate info regarding Ehlers' original ACP form AND how you may adapt algorithms, you'll have to obtain one. Note to reader, comparing Ehlers' original code to my chimeric code embracing the "Power of Pine", you will notice they have little resemblance.

What you see is a new species of autocorrelation periodogram combining Ehlers' innovation with my fascinations of what ACP could be in a Pine package. One other intention of this script's code is to pay homage to Ehlers' lifelong works. Like Kondratiev, Ehlers is also a hardcore cycle enthusiast. I intend to carry on the fire Ehlers envisioned and I believe that is literally displayed here as a pleasant "fiery" example endowed with Pine. With that said, I tried to make the code as computationally efficient as possible, without going into dozens of more crazy lines of code to speed things up even more. There's also a few creative modifications I made by making alterations to the originating formulas that I felt were improvements, one of them being lag reduction. By recently questioning every single thing I thought I knew about ACP, combined with the accumulation of my current knowledge base, this is the innovative revision I came up with. I could have improved it more but decided not to mind thrash too many TV members, maybe later...

I am now confident Pine should have adequate overhead left over to attach various indicators to the dominant cycle via input.source(). TV, I apologize in advance if in the future a server cluster combusts into a raging inferno... Coders, be fully prepared to build entire algorithms from pure raw code, because not all of the built-in Pine functions fully support dynamic periods (e.g. length=ANYTHING). Many of them do, as this was requested and granted a while ago, but some functions are just inherently finicky due to implementation combinations and MUST be emulated via raw code. I would imagine some comprehensive library or numerous authored scripts have portions of raw code for Pine built-ins some where on TV if you look diligently enough.

Notice: Unfortunately, I will not provide any integration support into member's projects at all. I have my own projects that require way too much of my day already. While I was refactoring my life (forgoing many other "important" endeavors) in the early half of 2023, I primarily focused on this code over and over in my surplus time. During that same time I was working on other innovations that are far above and beyond what this code is. I hope you understand.

The best way programmatically may be to incorporate this code into your private Pine project directly, after brutal testing of course, but that may be too challenging for many in early development. Being able to see the periodogram is also beneficial, so input sourcing may be the "better" avenue to tether portions of the dominant cycle to algorithms. Unique indication being able to utilize the dominantCycle may be advantageous when tethering this script to those algorithms. The easiest way is to manually set your indicators to what ACP recognizes as the dominant cycle, but that's actually not considered dynamic real time adaption of an indicator. Different indicators may need a proportion of the dominantCycle, say half it's value, while others may need the full value of it. That's up to you to figure that out in practice. Sourcing one or more custom indicators dynamically to one detector's dominantCycle may require code like this: `int sourceDC = int(math.max(6, math.min(49, input.source(close, "Dominant Cycle Source"))))`. Keep in mind, some algos can use a float, while algos with a for loop require an integer.

I have witnessed a few attempts by talented TV members for a Pine based autocorrelation periodogram, but not in this caliber. Trust me, coding ACP is no ordinary task to accomplish in Pine and modifying it blessed with applicable improvements is even more challenging. For over 4 years, I have been slowly improving this code here and there randomly. It is beautiful just like a real flame, but... this one can still burn you! My mind was fried to charcoal black a few times wrestling with it in the distant past. My very first attempt at translating ACP was a month long endeavor because PSv3 simply didn't have arrays back then. Anyways, this is ACP with a newer engine, I hope you enjoy it. Any TV subscriber can utilize this code as they please. If you are capable of sufficiently using it properly, please use it wisely with intended good will. That is all I beg of you.

Lastly, you now see how I have rasterized my Pine with Ehlers' swami-like tech. Yep, this whole time I have been using hline() since PSv3, not plot(). Evidently, plot() still has a deficiency limited to only 32 plots when it comes to creating intense eye candy indicators, the last I checked. The use of hline() is the optimal choice for rasterizing Ehlers styled heatmaps. This does only contain two color schemes of the many I have formerly created, but that's all that is essentially needed for this gizmo. Anything else is generally for a spectacle or seeing how brutal Pine can be color treated. The real hurdle is being able to manipulate colors dynamically with Merlin like capabilities from multiple algo results. That's the true challenging part of these heatmap contraptions to obtain multi-colored "predator vision" level indication. You now have basic hline() food for thought empowerment to wield as you can imaginatively dream in Pine projects.

PERIODOGRAM UTILITY IN REAL WORLD SCENARIOS:

This code is a testament to the abilities that have yet to be fully realized with indication advancements. Periodograms, spectrograms, and heatmaps are a powerful tool with real-world applications in various fields such as financial markets, electrical engineering, astronomy, seismology, and neuro/medical applications. For instance, among these diverse fields, it may help traders and investors identify market cycles/periodicities in financial markets, support engineers in optimizing electrical or acoustic systems, aid astronomers in understanding celestial object attributes, assist seismologists with predicting earthquake risks, help medical researchers with neurological disorder identification, and detection of asymptomatic cardiovascular clotting in the vaxxed via full body thermography. In either field of study, technologies in likeness to periodograms may very well provide us with a better sliver of analysis beyond what was ever formerly invented. Periodograms can identify dominant cycles and frequency components in data, which may provide valuable insights and possibly provide better-informed decisions. By utilizing periodograms within aspects of market analytics, individuals and organizations can potentially refrain from making blinded decisions and leverage data-driven insights instead.

PERIODOGRAM INTERPRETATION:

The periodogram renders the power spectrum of a signal, with the y-axis representing the periodicity (frequencies/wavelengths) and the x-axis representing time. The y-axis is divided into periods, with each elevation representing a period. In this periodogram, the y-axis ranges from 6 at the very bottom to 49 at the top, with intermediate values in between, all indicating the power of the corresponding frequency component by color. The higher the position occurs on the y-axis, the longer the period or lower the frequency. The x-axis of the periodogram represents time and is divided into equal intervals, with each vertical column on the axis corresponding to the time interval when the signal was measured. The most recent values/colors are on the right side.

The intensity of the colors on the periodogram indicate the power level of the corresponding frequency or period. The fire color scheme is distinctly like the heat intensity from any casual flame witnessed in a small fire from a lighter, match, or camp fire. The most intense power would be indicated by the brightest of yellow, while the lowest power would be indicated by the darkest shade of red or just black. By analyzing the pattern of colors across different periods, one may gain insights into the dominant frequency components of the signal and visually identify recurring cycles/patterns of periodicity.

SETTINGS CONFIGURATIONS BRIEFLY EXPLAINED:

Source Options: These settings allow you to choose the data source for the analysis. Using the `Source` selection, you may tether to additional data streams (e.g. close, hlcc4, hl2), which also may include samples from any other indicator. For example, this could be my "Chirped Sine Wave Generator" script found in my member profile. By using the `SineWave` selection, you may analyze a theoretical sinusoidal wave with a user-defined period, something already incorporated into the code. The `SineWave` will be displayed over top of the periodogram.

Roofing Filter Options: These inputs control the range of the passband for ACP to analyze. Ehlers had two versions of his highpass filters for his releases, so I included an option for you to see the obvious difference when performing a comparison of both. You may choose between 1st and 2nd order high-pass filters.

Spectral Controls: These settings control the core functionality of the spectral analysis results. You can adjust the autocorrelation lag, adjust the level of smoothing for Fourier coefficients, and control the contrast/behavior of the heatmap displaying the power spectra. I provided two color schemes by checking or unchecking a checkbox.

Dominant Cycle Options: These settings allow you to customize the various types of dominant cycle values. You can choose between floating-point and integer values, and select the rounding method used to derive the final dominantCycle values. Also, you may control the level of smoothing applied to the dominant cycle values.

DOMINANT CYCLE VALUE SELECTIONS:

External to the acs() function, the code takes a dominant cycle value returned from acs() and changes its numeric form based on a specified type and form chosen within the indicator settings. The dominant cycle value can be represented as an integer or a decimal number, depending on the attached algorithm's requirements. For example, FIR filters will require an integer while many IIR filters can use a float. The float forms can be either rounded, smoothed, or floored. If the resulting value is desired to be an integer, it can be rounded up/down or just be in an integer form, depending on how your algorithm may utilize it.

AUTOCORRELATION SPECTRUM FUNCTION BASICALLY EXPLAINED:

In the beginning of the acs() code, the population of caches for precalculated angular frequency factors and smoothing coefficients occur. By precalculating these factors/coefs only once and then storing them in an array, the indicator can save time and computational resources when performing subsequent calculations that require them later.

In the following code block, the "Calculate AutoCorrelations" is calculated for each period within the passband width. The calculation involves numerous summations of values extracted from the roofing filter. Finally, a correlation values array is populated with the resulting values, which are normalized correlation coefficients.

Moving on to the next block of code, labeled "Decompose Fourier Components", Fourier decomposition is performed on the autocorrelation coefficients. It iterates this time through the applicable period range of 6 to 49, calculating the real and imaginary parts of the Fourier components. Frequencies 6 to 49 are the primary focus of interest for this periodogram. Using the precalculated angular frequency factors, the resulting real and imaginary parts are then utilized to calculate the spectral Fourier components, which are stored in an array for later use.

The next section of code smooths the noise ridden Fourier components between the periods of 6 and 49 with a selected filter. This species also employs numerous SuperSmoothers to condition noisy Fourier components. One of the big differences is Ehlers' versions used basic EMAs in this section of code. I decided to add SuperSmoothers.

The final sections of the acs() code determines the peak power component for normalization and then computes the dominant cycle period from the smoothed Fourier components. It first identifies a single spectral component with the highest power value and then assigns it as the peak power. Next, it normalizes the spectral components using the peak power value as a denominator. It then calculates the average dominant cycle period from the normalized spectral components using Ehlers' "Center of Gravity" calculation. Finally, the function returns the dominant cycle period along with the normalized spectral components for later external use to plot the periodogram.

POST SCRIPT:

Concluding, I have to acknowledge a newly found analyst for assistance that I couldn't receive from anywhere else. For one, Claude doesn't know much about Pine, is unfortunately color blind, and can't even see the Pine reference, but it was able to intuitively shred my code with laser precise realizations. Not only that, formulating and reformulating my description needed crucial finesse applied to it, and I couldn't have provided what you have read here without that artificial insight. Finding the right order of words to convey the complexity of ACP and the elaborate accompanying content was a daunting task. No code in my life has ever absorbed so much time and hard fricking work, than what you witness here, an ACP gem cut pristinely. I'm unveiling my version of ACP for an empowering cause, in the hopes a future global army of code wielders will tether it to highly functional computational contraptions they might possess. Here is ACP fully blessed poetically with the "Power of Pine" in sublime code. ENJOY!

Support & Resistance AI (K means/median) [ThinkLogicAI]█ OVERVIEW

K-means is a clustering algorithm commonly used in machine learning to group data points into distinct clusters based on their similarities. While K-means is not typically used directly for identifying support and resistance levels in financial markets, it can serve as a tool in a broader analysis approach.

Support and resistance levels are price levels in financial markets where the price tends to react or reverse. Support is a level where the price tends to stop falling and might start to rise, while resistance is a level where the price tends to stop rising and might start to fall. Traders and analysts often look for these levels as they can provide insights into potential price movements and trading opportunities.

█ BACKGROUND

The K-means algorithm has been around since the late 1950s, making it more than six decades old. The algorithm was introduced by Stuart Lloyd in his 1957 research paper "Least squares quantization in PCM" for telecommunications applications. However, it wasn't widely known or recognized until James MacQueen's 1967 paper "Some Methods for Classification and Analysis of Multivariate Observations," where he formalized the algorithm and referred to it as the "K-means" clustering method.

So, while K-means has been around for a considerable amount of time, it continues to be a widely used and influential algorithm in the fields of machine learning, data analysis, and pattern recognition due to its simplicity and effectiveness in clustering tasks.

█ COMPARE AND CONTRAST SUPPORT AND RESISTANCE METHODS

1) K-means Approach:

Cluster Formation: After applying the K-means algorithm to historical price change data and visualizing the resulting clusters, traders can identify distinct regions on the price chart where clusters are formed. Each cluster represents a group of similar price change patterns.

Cluster Analysis: Analyze the clusters to identify areas where clusters tend to form. These areas might correspond to regions of price behavior that repeat over time and could be indicative of support and resistance levels.

Potential Support and Resistance Levels: Based on the identified areas of cluster formation, traders can consider these regions as potential support and resistance levels. A cluster forming at a specific price level could suggest that this level has been historically significant, causing similar price behavior in the past.

Cluster Standard Deviation: In addition to looking at the means (centroids) of the clusters, traders can also calculate the standard deviation of price changes within each cluster. Standard deviation is a measure of the dispersion or volatility of data points around the mean. A higher standard deviation indicates greater price volatility within a cluster.

Low Standard Deviation: If a cluster has a low standard deviation, it suggests that prices within that cluster are relatively stable and less likely to exhibit sudden and large price movements. Traders might consider placing tighter stop-loss orders for trades within these clusters.

High Standard Deviation: Conversely, if a cluster has a high standard deviation, it indicates greater price volatility within that cluster. Traders might opt for wider stop-loss orders to allow for potential price fluctuations without getting stopped out prematurely.

Cluster Density: Each data point is assigned to a cluster so a cluster that is more dense will act more like gravity and

2) Traditional Approach:

Trendlines: Draw trendlines connecting significant highs or lows on a price chart to identify potential support and resistance levels.

Chart Patterns: Identify chart patterns like double tops, double bottoms, head and shoulders, and triangles that often indicate potential reversal points.

Moving Averages: Use moving averages to identify levels where the price might find support or resistance based on the average price over a specific period.

Psychological Levels: Identify round numbers or levels that traders often pay attention to, which can act as support and resistance.

Previous Highs and Lows: Identify significant previous price highs and lows that might act as support or resistance.

The key difference lies in the approach and the foundation of these methods. Traditional methods are based on well-established principles of technical analysis and market psychology, while the K-means approach involves clustering price behavior without necessarily incorporating market sentiment or specific price patterns.

It's important to note that while the K-means approach might provide an interesting way to analyze price data, it should be used cautiously and in conjunction with other traditional methods. Financial markets are influenced by a wide range of factors beyond just price behavior, and the effectiveness of any method for identifying support and resistance levels should be thoroughly tested and validated. Additionally, developments in trading strategies and analysis techniques could have occurred since my last update.

█ K MEANS ALGORITHM

The algorithm for K means is as follows:

Initialize cluster centers

assign data to clusters based on minimum distance

calculate cluster center by taking the average or median of the clusters

repeat steps 1-3 until cluster centers stop moving

█ LIMITATIONS OF K MEANS

There are 3 main limitations of this algorithm:

Sensitive to Initializations: K-means is sensitive to the initial placement of centroids. Different initializations can lead to different cluster assignments and final results.

Assumption of Equal Sizes and Variances: K-means assumes that clusters have roughly equal sizes and spherical shapes. This may not hold true for all types of data. It can struggle with identifying clusters with uneven densities, sizes, or shapes.

Impact of Outliers: K-means is sensitive to outliers, as a single outlier can significantly affect the position of cluster centroids. Outliers can lead to the creation of spurious clusters or distortion of the true cluster structure.

█ LIMITATIONS IN APPLICATION OF K MEANS IN TRADING

Trading data often exhibits characteristics that can pose challenges when applying indicators and analysis techniques. Here's how the limitations of outliers, varying scales, and unequal variance can impact the use of indicators in trading:

Outliers are data points that significantly deviate from the rest of the dataset. In trading, outliers can represent extreme price movements caused by rare events, news, or market anomalies. Outliers can have a significant impact on trading indicators and analyses:

Indicator Distortion: Outliers can skew the calculations of indicators, leading to misleading signals. For instance, a single extreme price spike could cause indicators like moving averages or RSI (Relative Strength Index) to give false signals.

Risk Management: Outliers can lead to overly aggressive trading decisions if not properly accounted for. Ignoring outliers might result in unexpected losses or missed opportunities to adjust trading strategies.

Different Scales: Trading data often includes multiple indicators with varying units and scales. For example, prices are typically in dollars, volume in units traded, and oscillators have their own scale. Mixing indicators with different scales can complicate analysis:

Normalization: Indicators on different scales need to be normalized or standardized to ensure they contribute equally to the analysis. Failure to do so can lead to one indicator dominating the analysis due to its larger magnitude.

Comparability: Without normalization, it's challenging to directly compare the significance of indicators. Some indicators might have a larger numerical range and could overshadow others.

Unequal Variance: Unequal variance in trading data refers to the fact that some indicators might exhibit higher volatility than others. This can impact the interpretation of signals and the performance of trading strategies:

Volatility Adjustment: When combining indicators with varying volatility, it's essential to adjust for their relative volatilities. Failure to do so might lead to overemphasizing or underestimating the importance of certain indicators in the trading strategy.

Risk Assessment: Unequal variance can impact risk assessment. Indicators with higher volatility might lead to riskier trading decisions if not properly taken into account.

█ APPLICATION OF THIS INDICATOR

This indicator can be used in 2 ways:

1) Make a directional trade:

If a trader thinks price will go higher or lower and price is within a cluster zone, The trader can take a position and place a stop on the 1 sd band around the cluster. As one can see below, the trader can go long the green arrow and place a stop on the one standard deviation mark for that cluster below it at the red arrow. using this we can calculate a risk to reward ratio.

Calculating risk to reward: targeting a risk reward ratio of 2:1, the trader could clearly make that given that the next resistance area above that in the orange cluster exceeds this risk reward ratio.

2) Take a reversal Trade:

We can use cluster centers (support and resistance levels) to go in the opposite direction that price is currently moving in hopes of price forming a pivot and reversing off this level.

Similar to the directional trade, we can use the standard deviation of the cluster to place a stop just in case we are wrong.

In this example below we can see that shorting on the red arrow and placing a stop at the one standard deviation above this cluster would give us a profitable trade with minimal risk.

Using the cluster density table in the upper right informs the trader just how dense the cluster is. Higher density clusters will give a higher likelihood of a pivot forming at these levels and price being rejected and switching direction with a larger move.

█ FEATURES & SETTINGS

General Settings:

Number of clusters: The user can select from 3 to five clusters. A good rule of thumb is that if you are trading intraday, less is more (Think 3 rather than 5). For daily 4 to 5 clusters is good.

Cluster Method: To get around the outlier limitation of k means clustering, The median was added. This gives the user the ability to choose either k means or k median clustering. K means is the preferred method if the user things there are no large outliers, and if there appears to be large outliers or it is assumed there are then K medians is preferred.

Bars back To train on: This will be the amount of bars to include in the clustering. This number is important so that the user includes bars that are recent but not so far back that they are out of the scope of where price can be. For example the last 2 years we have been in a range on the sp500 so 505 days in this setting would be more relevant than say looking back 5 years ago because price would have to move far to get there.

Show SD Bands: Select this to show the 1 standard deviation bands around the support and resistance level or unselect this to just show the support and resistance level by itself.

Features:

Besides the support and resistance levels and standard deviation bands, this indicator gives a table in the upper right hand corner to show the density of each cluster (support and resistance level) and is color coded to the cluster line on the chart. Higher density clusters mean price has been there previously more than lower density clusters and could mean a higher likelihood of a reversal when price reaches these areas.

█ WORKS CITED

Victor Sim, "Using K-means Clustering to Create Support and Resistance", 2020, towardsdatascience.com

Chris Piech, "K means", stanford.edu

█ ACKNOLWEDGMENTS

@jdehorty- Thanks for the publish template. It made organizing my thoughts and work alot easier.

ABC on Recursive Zigzag [Trendoscope]There are several implementations of ABC pattern in tradingview and pine script. However, we have made this indicator to provide users additional quantifiable information along with flexibility to experiment and develop their own strategy based on the patterns.

🎲 Highlights of this indicator over other ABC implementations are:

Implementation is based on recursive multi level zigzag allows bigger as well as smaller patterns to be identified

Allows users to set their trading rules with respect to entry, target and stop ratios, experiment and build their own strategy based on the ABC pattern.

Back test summary including win ratio and risk reward will help users understand the profitability based on different settings being used.

🎲 Concept of ABC Pattern

The ABC pattern, also known as the "Corrective Wave" or "Zigzag Pattern," is a fundamental concept in Elliott Wave Theory, which is widely used in technical analysis to identify and predict price movements in financial markets.

The ABC pattern is a three-wave corrective pattern that typically occurs within the context of a larger impulse or trending wave. It consists of two smaller waves in the opposite direction (A and C) separated by a corrective wave (B). These waves are labeled alphabetically and represent price movements.

Wave A (Impulse Wave): Wave A is the first leg of the ABC pattern and is characterized by a strong price move in the opposite direction of the prevailing trend. It is often driven by a fundamental or sentiment-driven event that temporarily disrupts the trend.

Wave B (Corrective Wave): Wave B is the corrective wave that follows Wave A. It represents a partial retracement of Wave A's price movement. Wave B can take various forms, such as a simple correction or a complex correction (e.g., a triangle or a flat correction). It typically doesn't retrace the entire length of Wave A.

Wave C (Impulse Wave): Wave C is the final leg of the ABC pattern and is characterized by a strong price move in the same direction as the prevailing trend. It often surpasses the starting point of Wave A and confirms the resumption of the larger trend.

🎲 Indicator Components

Upon loading the indicator on the chart, we can observe the following components on the chart.

Pattern Drawings is the graphical representation of present patterns. Please note that it is not necessary for patterns to be there on the chart all the time. Patterns will appear on the chart when price makes the patterns.

Trade Box is the box representing trade signals of the pattern. These trade levels are generated based on the user settings.

Summary Table is the back test summary containing details of historical pattern performance including Win Ratio and Risk Reward.

🎲 Indicator Settings

Details of each user settings are provided in the tooltips. Below is the snapshot of it.

🎲 Alerts

Basic level of alerts are built in the script using alert function to highlight the following conditions:

New ABC Pattern

Updates to existing Pattern

Both conditions will alert simple text messages. There is not much customization provided as part of this indicator. We will consider providing more options in future versions based on the interest and demand shown by users.

Signal AdapterThis Signal Adapter script can compose a signal based on inputs from other simple (non-signal) indicators and can forwards it to the "Template Trailing Strategy".

It allows the user to combine up to eight external inputs and define the conditions that will trigger the start, end, cancel start and cancel end deals.

A signal will be composed from those user-defined conditions. The "indicator on indicator" feature is needed so you can forward the resulted signal to the "Template Trailing Strategy".

Thus you should be Plus or Premium user to get it's full potential. It is very convenient for those who want to create a strategy without coding their own signal indicator and for those

who want to fast prototype various ideas based on simple conditions.

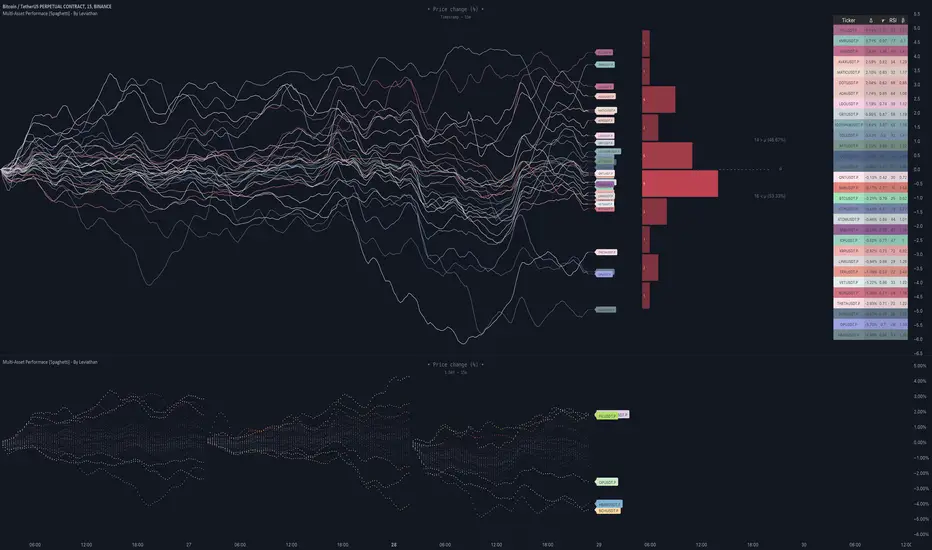

Multi-Asset Performance [Spaghetti] - By LeviathanThis indicator visualizes the cumulative percentage changes or returns of 30 symbols over a given period and offers a unique set of tools and data analytics for deeper insight into the performance of different assets.

Multi Asset Performance indicator (also called “Spaghetti”) makes it easy to monitor the changes in Price, Open Interest, and On Balance Volume across multiple assets simultaneously, distinguish assets that are overperforming or underperforming, observe the relative strength of different assets or currencies, use it as a tool for identifying mean reversion opportunities and even for constructing pairs trading strategies, detect "risk-on" or "risk-off" periods, evaluate statistical relationships between assets through metrics like correlation and beta, construct hedging strategies, trade rotations and much more.

Start by selecting a time period (e.g., 1 DAY) to set the interval for when data is reset. This will provide insight into how price, open interest, and on-balance volume change over your chosen period. In the settings, asset selection is fully customizable, allowing you to create three groups of up to 30 tickers each. These tickers can be displayed in a variety of styles and colors. Additional script settings offer a range of options, including smoothing values with a Simple Moving Average (SMA), highlighting the top or bottom performers, plotting the group mean, applying heatmap/gradient coloring, generating a table with calculations like beta, correlation, and RSI, creating a profile to show asset distribution around the mean, and much more.

One of the most important script tools is the screener table, which can display:

🔸 Percentage Change (Represents the return or the percentage increase or decrease in Price/OI/OBV over the current selected period)

🔸 Beta (Represents the sensitivity or responsiveness of asset's returns to the returns of a benchmark/mean. A beta of 1 means the asset moves in tandem with the market. A beta greater than 1 indicates the asset is more volatile than the market, while a beta less than 1 indicates the asset is less volatile. For example, a beta of 1.5 means the asset typically moves 150% as much as the benchmark. If the benchmark goes up 1%, the asset is expected to go up 1.5%, and vice versa.)

🔸 Correlation (Describes the strength and direction of a linear relationship between the asset and the mean. Correlation coefficients range from -1 to +1. A correlation of +1 means that two variables are perfectly positively correlated; as one goes up, the other will go up in exact proportion. A correlation of -1 means they are perfectly negatively correlated; as one goes up, the other will go down in exact proportion. A correlation of 0 means that there is no linear relationship between the variables. For example, a correlation of 0.5 between Asset A and Asset B would suggest that when Asset A moves, Asset B tends to move in the same direction, but not perfectly in tandem.)

🔸 RSI (Measures the speed and change of price movements and is used to identify overbought or oversold conditions of each asset. The RSI ranges from 0 to 100 and is typically used with a time period of 14. Generally, an RSI above 70 indicates that an asset may be overbought, while RSI below 30 signals that an asset may be oversold.)

⚙️ Settings Overview:

◽️ Period

Periodic inputs (e.g. daily, monthly, etc.) determine when the values are reset to zero and begin accumulating again until the period is over. This visualizes the net change in the data over each period. The input "Visible Range" is auto-adjustable as it starts the accumulation at the leftmost bar on your chart, displaying the net change in your chart's visible range. There's also the "Timestamp" option, which allows you to select a specific point in time from where the values are accumulated. The timestamp anchor can be dragged to a desired bar via Tradingview's interactive option. Timestamp is particularly useful when looking for outperformers/underperformers after a market-wide move. The input positioned next to the period selection determines the timeframe on which the data is based. It's best to leave it at default (Chart Timeframe) unless you want to check the higher timeframe structure of the data.

◽️ Data

The first input in this section determines the data that will be displayed. You can choose between Price, OI, and OBV. The second input lets you select which one out of the three asset groups should be displayed. The symbols in the asset group can be modified in the bottom section of the indicator settings.

◽️ Appearance

You can choose to plot the data in the form of lines, circles, areas, and columns. The colors can be selected by choosing one of the six pre-prepared color palettes.

◽️ Labeling

This input allows you to show/hide the labels and select their appearance and size. You can choose between Label (colored pointed label), Label and Line (colored pointed label with a line that connects it to the plot), or Text Label (colored text).

◽️ Smoothing

If selected, this option will smooth the values using a Simple Moving Average (SMA) with a custom length. This is used to reduce noise and improve the visibility of plotted data.

◽️ Highlight

If selected, this option will highlight the top and bottom N (custom number) plots, while shading the others. This makes the symbols with extreme values stand out from the rest.

◽️ Group Mean

This input allows you to select the data that will be considered as the group mean. You can choose between Group Average (the average value of all assets in the group) or First Ticker (the value of the ticker that is positioned first on the group's list). The mean is then used in calculations such as correlation (as the second variable) and beta (as a benchmark). You can also choose to plot the mean by clicking on the checkbox.

◽️ Profile

If selected, the script will generate a vertical volume profile-like display with 10 zones/nodes, visualizing the distribution of assets below and above the mean. This makes it easy to see how many or what percentage of assets are outperforming or underperforming the mean.

◽️ Gradient

If selected, this option will color the plots with a gradient based on the proximity of the value to the upper extreme, zero, and lower extreme.

◽️ Table

This section includes several settings for the table's appearance and the data displayed in it. The "Reference Length" input determines the number of bars back that are used for calculating correlation and beta, while "RSI Length" determines the length used for calculating the Relative Strength Index. You can choose the data that should be displayed in the table by using the checkboxes.

◽️ Asset Groups

This section allows you to modify the symbols that have been selected to be a part of the 3 asset groups. If you want to change a symbol, you can simply click on the field and type the ticker of another one. You can also show/hide a specific asset by using the checkbox next to the field.

SimilarityMeasuresLibrary "SimilarityMeasures"

Similarity measures are statistical methods used to quantify the distance between different data sets

or strings. There are various types of similarity measures, including those that compare:

- data points (SSD, Euclidean, Manhattan, Minkowski, Chebyshev, Correlation, Cosine, Camberra, MAE, MSE, Lorentzian, Intersection, Penrose Shape, Meehl),

- strings (Edit(Levenshtein), Lee, Hamming, Jaro),

- probability distributions (Mahalanobis, Fidelity, Bhattacharyya, Hellinger),

- sets (Kumar Hassebrook, Jaccard, Sorensen, Chi Square).

---

These measures are used in various fields such as data analysis, machine learning, and pattern recognition. They

help to compare and analyze similarities and differences between different data sets or strings, which

can be useful for making predictions, classifications, and decisions.

---

References:

en.wikipedia.org

cran.r-project.org

numerics.mathdotnet.com

github.com

github.com

github.com

Encyclopedia of Distances, doi.org

ssd(p, q)

Sum of squared difference for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of distance that calculates the squared euclidean distance.

euclidean(p, q)

Euclidean distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of distance that calculates the straight-line (or Euclidean).

manhattan(p, q)

Manhattan distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of absolute differences between both points.

minkowski(p, q, p_value)

Minkowsky Distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

p_value (float) : `float` P value, default=1.0(1: manhatan, 2: euclidean), does not support chebychev.

Returns: Measure of similarity in the normed vector space.

chebyshev(p, q)

Chebyshev distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of maximum absolute difference.

correlation(p, q)

Correlation distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of maximum absolute difference.

cosine(p, q)

Cosine distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Cosine distance between vectors `p` and `q`.

---

angiogenesis.dkfz.de

camberra(p, q)

Camberra distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Weighted measure of absolute differences between both points.

mae(p, q)

Mean absolute error is a normalized version of the sum of absolute difference (manhattan).

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Mean absolute error of vectors `p` and `q`.

mse(p, q)

Mean squared error is a normalized version of the sum of squared difference.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Mean squared error of vectors `p` and `q`.

lorentzian(p, q)

Lorentzian distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Lorentzian distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

intersection(p, q)

Intersection distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Intersection distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

penrose(p, q)

Penrose Shape distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Penrose shape distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

meehl(p, q)

Meehl distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Meehl distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

edit(x, y)

Edit (aka Levenshtein) distance for indexed strings.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

Returns: Number of deletions, insertions, or substitutions required to transform source string into target string.

---

generated description:

The Edit distance is a measure of similarity used to compare two strings. It is defined as the minimum number of

operations (insertions, deletions, or substitutions) required to transform one string into another. The operations

are performed on the characters of the strings, and the cost of each operation depends on the specific algorithm

used.

The Edit distance is widely used in various applications such as spell checking, text similarity, and machine

translation. It can also be used for other purposes like finding the closest match between two strings or

identifying the common prefixes or suffixes between them.

---

github.com

www.red-gate.com

planetcalc.com

lee(x, y, dsize)

Distance between two indexed strings of equal length.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

dsize (int) : `int` Dictionary size.

Returns: Distance between two strings by accounting for dictionary size.

---

www.johndcook.com

hamming(x, y)

Distance between two indexed strings of equal length.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

Returns: Length of different components on both sequences.

---

en.wikipedia.org

jaro(x, y)

Distance between two indexed strings.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

Returns: Measure of two strings' similarity: the higher the value, the more similar the strings are.

The score is normalized such that `0` equates to no similarities and `1` is an exact match.

---

rosettacode.org

mahalanobis(p, q, VI)

Mahalanobis distance between two vectors with population inverse covariance matrix.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

VI (matrix) : `matrix` Inverse of the covariance matrix.

Returns: The mahalanobis distance between vectors `p` and `q`.

---

people.revoledu.com

stat.ethz.ch

docs.scipy.org

fidelity(p, q)

Fidelity distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Bhattacharyya Coefficient between vectors `p` and `q`.

---

en.wikipedia.org

bhattacharyya(p, q)

Bhattacharyya distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Bhattacharyya distance between vectors `p` and `q`.

---

en.wikipedia.org

hellinger(p, q)

Hellinger distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The hellinger distance between vectors `p` and `q`.

---

en.wikipedia.org

jamesmccaffrey.wordpress.com

kumar_hassebrook(p, q)

Kumar Hassebrook distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Kumar Hassebrook distance between vectors `p` and `q`.

---

github.com

jaccard(p, q)

Jaccard distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Jaccard distance between vectors `p` and `q`.

---

github.com

sorensen(p, q)

Sorensen distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Sorensen distance between vectors `p` and `q`.

---

people.revoledu.com

chi_square(p, q, eps)

Chi Square distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

eps (float)

Returns: The Chi Square distance between vectors `p` and `q`.

---

uw.pressbooks.pub

stats.stackexchange.com

www.itl.nist.gov

kulczynsky(p, q, eps)

Kulczynsky distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

eps (float)

Returns: The Kulczynsky distance between vectors `p` and `q`.

---

github.com

All Candlestick Patterns on Backtest [By MUQWISHI]▋ INTRODUCTION :

The “All Candlestick Patterns on Backtest” indicator generates a table that offers a clear visualization of the historical return percentages for each candlestick pattern strategy over a specified time period. This table serves as an organized resource, serving as a launching point for in-depth research into candle formations. It may help to rectify any misconceptions surrounding candlestick patterns, refine trading approaches, and it could be foundation to make informed decisions in trading journey.

_______________________

▋ OVERVIEW:

_______________________

▋ CREDIT:

Credit to public technical “*All Candlestick Patterns*” indicator.

_______________________

▋ TABLE:

_______________________

▋ CHART:

_______________________

▋ INDICATOR SETTINGS:

#Section One: Table Setting

#Section Two: Backtest Setting

(1) Backtest Starting Period.

Note: If the datetime of the first candle on the chart is after the entreated datetime, the calculation will start from the first candle on the chart.

(2) Initial Equity ($).

(3) Leverage: Current Equity x Leverage Value.

(4) Entry Mode:

- “At Close”: Execute entry order as soon as the candle confirmed.

- “Breakout High (Low for Short)”: Stop limit buy order, entry order will be executed as soon as the next candle breakout the high of last pattern’s candle (low for short)

(5) Cancel Entry Within Bars: This option is applicable with {Entry Mode = Breakout High (Low for Short)}, to cancel the Entry Order if it's not executed within certain selected number of bars.

(6) Stoploss Range: the range refers to high of pattern - low of pattern.

(7) Risk:Reward: the calculation of risk:reward range start from entry price level. For example: A pattern triggered with range 10 points, and entry price is 100.

- For 1:1~risk:reward would the stoploss at 90 and takeprofit at 110.

- For 1:3~risk:reward would the stoploss at 90 and takeprofit at 130.

#Section Three: Technical & Candle Patterns

_______________________

▋ Comments:

This table was developed for research and educational purposes.

Candlestick patterns are almost similar as seen in “*All Candlestick Patterns*” indicator.

The table results should not be taken as a major concept to build a trading decision.

Personally, I see candlestick patterns as a means to comprehend the psychology of the market, and help to follow the price action.

Please let me know if you have any questions.

Thank you.

CE - 42MACRO Equity Factor Table This is Part 1 of 2 from the 42MACRO Recreation Series

The CE - 42MACRO Equity Factor Table is a whole toolbox packaged in a single indicator.

It aims to provide a probabilistic insight into the market realized GRID Macro Regime, use a multiplex of important Assets and Indices to form a high probability Implied Correlation expectation and allows to derive extra market insights by showing the most important aggregates and their performance over multiple timeframes... and what that might mean for the whole market direction, as well as the underlying asset.

WARNING

By the nature of the macro regimes, the outcomes are more accurate over longer Chart Timeframes (Week to Months).

However, it is also a valuable tool to form a proper,

market realized, short to medium term bias.

NOTE

This Indicator is intended to be used alongside the 2nd part "CE - 42MACRO Yield and Macro"

for a more wholistic approach and higher accuracy.

Due to coding limitations they can not be merged into one Indicator.

Methodology:

The Equity Factor Table tracks specifically chosen Assets to identify their performance and add the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below Assets, with more to come:

Dividend Compounders ( AMEX:SPHD )

Mid Caps ( AMEX:VO )

Emerging Markets ( AMEX:EEM )

Small Caps ( AMEX:IWM )

Mega Cap Growth ( NASDAQ:QQQ )

Brazil ( AMEX:EWZ )

United Kingdom ( AMEX:EWU )

Growth ( AMEX:IWF )

United States ( AMEX:SPY )

Japan ( AMEX:DXJ )

Momentum ( AMEX:MTUM )

China ( AMEX:FXI )

Low Beta ( AMEX:SPLV )

International ex-US ( NASDAQ:ACWX )

India ( AMEX:INDA )

Eurozone ( AMEX:EZU )

Quality ( AMEX:QUAL )

Size ( AMEX:OEF )

Functionalities:

1. Correlations

Takes a measure of Cross Market Correlations

2. Implied Trend

Calculates the trend for each Asset and uses the Correlation to obtain the Implied Trend for the underlying Asset

There are multiple functionalities to enhance Signal Speed and precision...

Reading a signal only over a certain threshold, otherwise being colored in gray to signal noise or unclear market behavior

Normalization of Signal

Double Normalization of Signal for more Speed... ideal for the Crypto Market

Using an additional Hull Moving Average to enhance Signal Speed

Additional simple Background coloring to get a Signal from the HMA

Barcoloring based on the Implied Correlation

3. Equity Factor Table

Shows market realized Asset performance

Provides the approximate realized GRID market regimes

Informs about "Risk ON" and "Risk OFF" market states

Now into the juicy stuff...

Visuals:

There is a variety of options to change visual settings of what is plotted and where

+ additional considerations.

Everything that is relevant in the underlying logic which can improve comprehension can be visualized with these options.

More to come

Market Correlation:

The Market Correlation Table takes the Correlation of all the Assets to the Asset on the Chart,

it furthermore uses the Normalized KAMA Oscillator by IkkeOmar to analyse the current trend of every single Asset.

(To enhance the Signal you can apply the mentioned Indicator on the relevant Assets to find your target Asset movements that you intend to capture...

and then change the length of the Indicator in here)

It then Implies a Correlation based on the Trend and the Correlation to give a probabilistically adjusted expectation for the future Chart Asset Movement.

This is strengthened by taking the average of all Implied Trends.

Thus the Correlation Table provides valuable insights about probabilistically likely Movement of the Asset over the defined time duration,

providing alpha for Traders and Investors alike.

Equity Factors:

The table provides valuable information about the current market environment (whether it's risk on or risk off),

the rough GRID models from 42MACRO and the actual market performance.

This allows you to obtain a deeper understanding of how the market works and makes it simple to identify the actual market direction,

makes it possible to derive overall market Health and shows market strength or weakness.

Utility:

The Equity Factor Table is divided in 4 Sections which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Equity Factors:

Are the values green for a specific Column?

If so then the market reflects the corresponding GRID behavior.

Bottom 5 Equity Factors:

Are the values red for a specific Column?

If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

This whole Indicator, as well as the second part, is based to a majority on 42MACRO's models.

I only brought them into TV and added things on top of it.