Risk Distribution HistogramStatistical risk visualization and analysis tool for any ticker 📊

The Risk Distribution Histogram visualizes the statistical distribution of different risk metrics for any financial instrument. It converts risk data into histograms with quartile-based color coding, so that traders can understand their risk, tail-risks, exposure patterns and make data-driven decisions based on empirical evidence rather than assumptions.

The indicator supports multiple risk calculation methods, each designed for different aspects of market analysis, from general volatility assessment to tail risk analysis.

Risk Measurement Methods

Standard Deviation

Captures raw daily price volatility by measuring the dispersion of price movements. Ideal for understanding overall market conditions and timing volatility-based strategies.

Use case: Options trading and volatility analysis.

Average True Range (ATR)

Measures true range as a percentage of price, accounting for gaps and limit moves. Valuable for position sizing across different price levels.

Use case: Position sizing and stop-loss placement.

The chart above illustrates how ATR statistical distribution can be used by looking at the ATR % of price distribution. For example, 90% of the movements are below 5%.

Downside Deviation

Only considers negative price movements, making it ideal for checking downside risk and capital protection rather than capturing upside volatility.

Use case: Downside protection strategies and stop losses.

Drawdown Analysis

Tracks peak-to-trough declines, providing insight into maximum loss potential during different market conditions.

Use case: Risk management and capital preservation.

The chart above illustrates tale risk for the asset (TQQQ), showing that it is possible to have drawdowns higher than 20%.

Entropy-Based Risk (EVaR)

Uses information theory to quantify market uncertainty. Higher entropy values indicate more unpredictable price action, valuable for detecting regime changes.

Use case: Advanced risk modeling and tail-risk.

VIX Histogram

Incorporates the market's fear index directly into analysis, showing how current volatility expectations compare to historical patterns. The CAPITALCOM:VIX histogram is independent from the ticker on the chart.

Use case: Volatility trading and market timing.

Visual Features

The histogram uses quartile-based color coding that immediately shows where current risk levels stand relative to historical patterns:

Green (Q1): Low Risk (0-25th percentile)

Yellow (Q2): Medium-Low Risk (25-50th percentile)

Orange (Q3): Medium-High Risk (50-75th percentile)

Red (Q4): High Risk (75-100th percentile)

The data table provides detailed statistics, including:

Count Distribution: Historical observations in each bin

PMF: Percentage probability for each risk level

CDF: Cumulative probability up to each level

Current Risk Marker: Shows your current position in the distribution

Trading Applications

When current risk falls into upper quartiles (Q3 or Q4), it signals conditions are riskier than 50-75% of historical observations. This guides position sizing and portfolio adjustments.

Key applications:

Position sizing based on empirical risk distributions

Monitoring risk regime changes over time

Comparing risk patterns across timeframes

Risk distribution analysis improves trade timing by identifying when market conditions favor specific strategies.

Enter positions during low-risk periods (Q1)

Reduce exposure in high-risk periods (Q4)

Use percentile rankings for dynamic stop-loss placement

Time volatility strategies using distribution patterns

Detect regime shifts through distribution changes

Compare current conditions to historical benchmarks

Identify outlier events in tail regions

Validate quantitative models with empirical data

Configuration Options

Data Collection

Lookback Period: Control amount of historical data analyzed

Date Range Filtering: Focus on specific market periods

Sample Size Validation: Automatic reliability warnings

Histogram Customization

Bin Count: 10-50 bins for different detail levels

Auto/Manual Bin Width: Optimize for your data range

Visual Preferences: Custom colors and font sizes

Implementation Guide

Start with Standard Deviation on daily charts for the most intuitive introduction to distribution-based risk analysis.

Method Selection: Begin with Standard Deviation

Setup: Use daily charts with 20-30 bins

Interpretation: Focus on quartile transitions as signals

Monitoring: Track distribution changes for regime detection

The tool provides comprehensive statistics including mean, standard deviation, quartiles, and current position metrics like Z-score and percentile ranking.

Enjoy, and please let me know your feedback! 😊🥂

Drawdown

3 Red / 3 Green Strategy with Volatility CheckStrategy Name: 3 Red / 3 Green Strategy with Volatility Check by AlgoTradeKit

Overview

This long-only strategy is designed for daily bars on NASDAQ (or similar instruments) and combines simple price action with a volatility filter. It “tells it like it is” – enter when the market shows weakness, but only in sufficiently volatile conditions, and exit either on signs of a reversal or after a set number of days.

Entry Conditions

- Price Action :

Enter a long position when there are 3 consecutive red days (each day's close is below its open).

- Volatility Filter :

The entry is allowed only if the current ATR (Average True Range) calculated over the specified ATR Period (default 12) is greater than its 30-day simple moving average. This ensures the market has enough volatility to justify the trade.

Exit Conditions

- Reversal Signal :

Exit the long position when 3 consecutive green days occur (each day's close is above its open), signaling a potential reversal.

- Time Limit :

Regardless of market conditions, any open trade is closed if it reaches the Maximum Trade Duration (default 22 days). This helps limit exposure during stagnant or unfavorable market conditions.

- You can toggle the three-green-day exit if you want to isolate the time-based exit.

Input Parameters

- Maximum Trade Duration (days): Default is 22 days.

- ATR Period: Default is 12.

- Use 3 Green Days Exit: Toggle to enable or disable the three-green-day exit condition.

How It Works

1. Entry: The strategy monitors daily price action for 3 consecutive down days. When this occurs and if the market is volatile enough (current ATR > 30-day ATR average), it opens a long position.

2. Exit: The position is closed if the price action reverses with 3 consecutive up days or if the trade has been open for the maximum allowed duration - i.e. use it on daily chart.

Risk Management

- The built-in maximum trade duration prevents trades from lingering too long in a non-trending or consolidating market.

- The volatility filter helps ensure that trades are only taken when there is sufficient price movement, potentially increasing the odds of a meaningful move.

Disclaimer

This strategy is provided “as is” without any warranties. It is essential to backtest and validate the performance on your specific instrument and market conditions before deploying live capital. Trading involves significant risk, and you should adjust parameters to match your risk tolerance.

Test and tweak this strategy to see if it fits your trading style and market conditions. Happy trading!

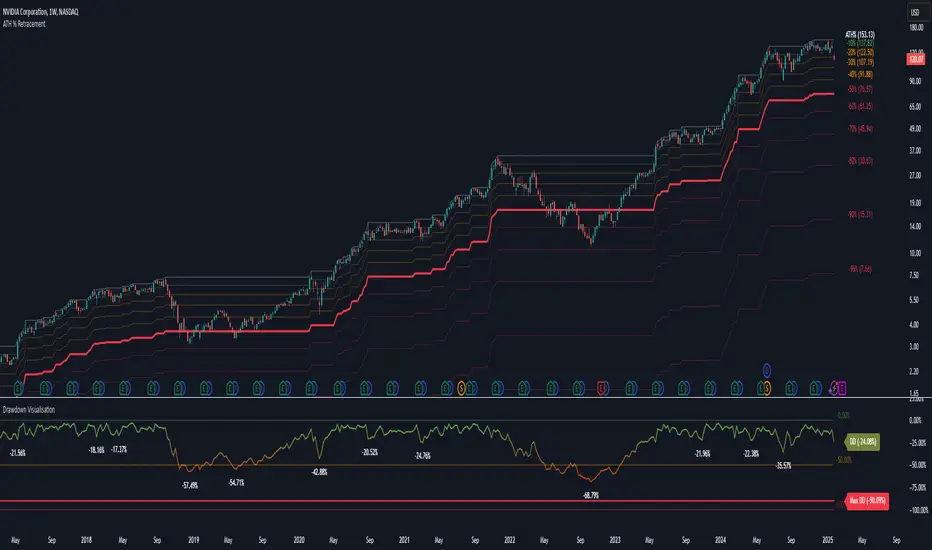

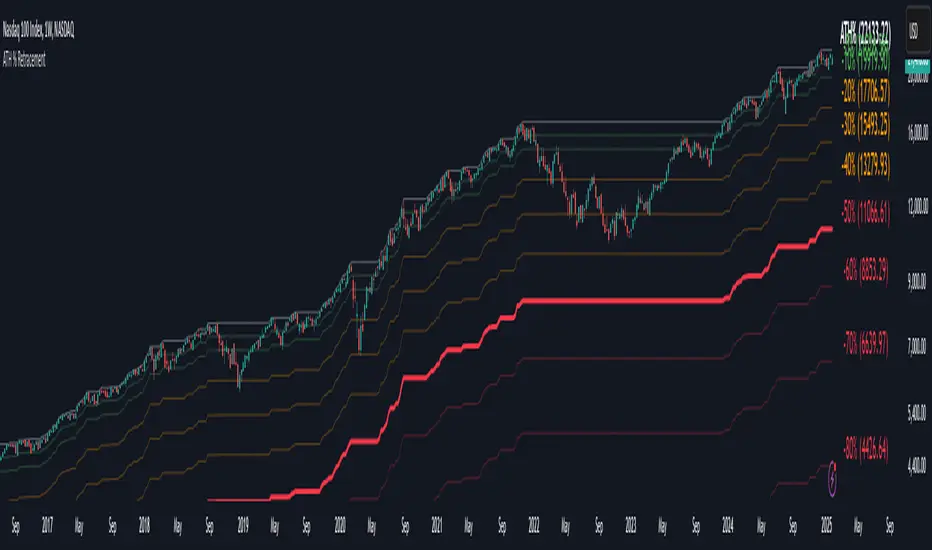

Drawdown Visualisation█ OVERVIEW

The Drawdown Visualisation indicator calculates and displays the instrument’s drawdown (in percent) relative to its all‐time high (ATH) from a user‐defined start date. It provides customisable options for label appearance, threshold lines (0%, –50%, –100%), and can plot historic drawdown levels via pivot detection.

█ USAGE

This indicator should be used with the Percentage Retracement from ATH indicator.

█ KEY FEATURES

Custom Date Settings — Use a custom start date so that only specified price action is considered.

Retracement Level Calculation — Determines ATH and computes multiple retracement levels using percentages from 0% to –100%.

Visual Signals and Customisation — Plots configurable horizontal lines and labels that display retracement percentages and prices.

Time Filtering — Bases calculations on data from the desired time period.

Historic Drawdowns — Display historical drawdowns

█ PURPOSE

Assist traders in visualising the depth of price retracements from recent or historical peaks.

Identify critical zones where the market may find support or resistance after reaching an ATH.

Facilitate more informed entry and exit decisions by clearly demarcating retracement levels on the chart.

█ IDEAL USERS

Swing Traders — Looking to exploit pullbacks following strong upward moves.

Technical Analysts — Interested in pinpointing key retracement levels as potential reversal or continuation points.

Price Action Traders — Focused on the nuances of market peaks and subsequent corrections.

Strategy Developers — Keen to backtest and refine approaches centred on retracement dynamics.

Percentage Retracement from ATH█ OVERVIEW

The Percentage Retracement from ATH indicator is a dynamic trading utility designed to help traders gauge market pullbacks from the peak price. By calculating key retracement levels based on the All-Time High (ATH) and user‑defined percentage inputs, it offers clear visual cues to assist in identifying potential support and resistance zones.

█ KEY FEATURES

Custom Date — Use a custom start date so the indicator only considers specified price action.

Retracement Calculation — Determines ATH and calculates levels based on user‑defined percentages (0% to –100%).

Visual Customisation — Plots configurable horizontal lines and labels showing retracement percentages and prices.

Time Filtering — Uses time filtering to base levels on the desired data period.

█ PURPOSE

Assist traders in visualising the depth of price retracements from recent or historical peaks.

Identify critical zones where the market may find support or resistance after reaching an ATH.

Facilitate more informed entry and exit decisions by clearly demarcating retracement levels on the chart.

█ IDEAL USERS

Swing Traders — Looking to exploit pullbacks following strong upward moves.

Technical Analysts — Interested in pinpointing key retracement levels as potential reversal or continuation points.

Price Action Traders — Focused on the nuances of market peaks and subsequent corrections.

Strategy Developers — Keen to backtest and refine approaches centred on retracement dynamics.

Bearish Wick Reversal█ STRATEGY OVERVIEW

The "Bearish Wick Reversal Strategy" identifies potential bullish reversals following significant bearish price rejection (long lower wicks). This counter-trend approach enters long positions when bearish candles show exaggerated downside wicks relative to closing prices, then exits on bullish confirmation signals. Includes optional EMA trend filtering for improved reliability.

█ What is a Bearish Wick?

A price rejection pattern where:

Bearish candle (close < open) forms with extended lower wick

Wick represents failed selloff: Low drops significantly below close

Measured as: (Low - Close)/Close × 100 (Negative percentage indicates downward extension)

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

Bearish candle forms with close < open

Lower wick exceeds user-defined threshold (Default: -1% of close price)

The signal occurs within the specified time window

If enabled, the close price must also be above the 200-period EMA (Exponential Moving Average)

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ PERFORMANCE OVERVIEW

Ideal Market: Volatile instruments with frequent price rejections

Key Risk: False signals in sustained bearish trends

Optimization Tip: Test various thresholds

Filter Impact: EMA reduces trades but improves win rate and reduces drawdown

Drawdown Tracker [SpokoStocks]Drawdown Tracker

The Drawdown Tracker is a powerful tool designed to help traders monitor and visualize the drawdown of symbol. By tracking both current and maximum drawdown levels, this indicator provides valuable insights into risk and potential capital preservation.

Features:

> Current Drawdown:

The current drawdown is calculated as the percentage drop from the record high to the current low, providing a real-time view of the loss from the peak.

> Maximum Drawdown:

The maximum drawdown represents the deepest drop observed from any peak in the historical data, giving an understanding of the worst-case scenario for losses.

> You can choose between two modes:

Full History: Tracks the maximum drawdown from the entire available data.

Rolling Period: Tracks the maximum drawdown within a defined rolling period (default 50 bars), allowing for a shorter-term risk assessment.

> Customizable Rolling Period:

You can adjust the rolling period length through the Rolling Period Length input to reflect different time frames for drawdown calculations.

> Warning Level:

A customizable warning level (default -65%) is plotted on the chart. This acts as a threshold to alert users when the drawdown crosses into a potentially concerning territory.

> Gradient Color Visualization:

The current drawdown is visualized using a gradient color, transitioning from red to yellow as the drawdown increases from -100% to 0%, providing an easy-to-interpret view of the severity of the drawdown.

> New Max Drawdown Marker:

Whenever a new maximum drawdown is recorded, a triangle marker is displayed at the bottom of the chart, along with a label showing the drawdown percentage. This provides clear visual confirmation when a new historical low is reached.

> Alerts:

Warning Level Breach Alert: Alerts you when the drawdown breaches the warning level you’ve set, helping you stay aware of significant risk events.

New Max Drawdown Alert: Triggers when a new maximum drawdown is recorded, allowing you to act quickly if necessary.

Use Cases:

Risk Management: Keep track of how much an asset is down from the peak, helping you make informed decisions about risk and drawdown tolerances.

Risk Disclaimer:

The information provided by this script is for educational and informational purposes only. It is not intended as financial advice and should not be construed as such. All trading and investment activities involve a high level of risk and may result in the loss of capital. The user is solely responsible for any decisions made based on the content provided by this script.

By using this script, you acknowledge and agree that you use it at your own risk. The creator of this script makes no warranties regarding the accuracy, completeness, or reliability of the information, and disclaims any responsibility for any losses or damages arising from its use.

Always conduct your own research and consult with a qualified financial advisor before making any investment decisions.

Monthly Drawdowns and Moves UP This script allows users to analyze the performance of a specific month across multiple years, focusing on maximum drawdowns and maximum upward moves within the selected month. The script offers the following features:

Dynamic Month Selection : Choose any month to analyze using an intuitive dropdown menu.

Maximum Drawdown and Upward Move Calculations :

Calculate the largest percentage drop (drawdown) and rise (move up) for the selected month each year.

Visual Highlights :

The selected month is visually highlighted on the chart with a semi-transparent overlay.

Dynamic Labels:

Labels display the maximum drawdown and upward move directly on the chart for better visualization.

Comprehensive Table Summary:

A table provides a year-by-year summary of the maximum drawdowns and upward moves for the selected month, making it easy to spot trends over time.

Customizable Display Options:

Toggle the visibility of drawdown labels, move-up labels, and the summary table for a clutter-free experience.

This tool is perfect for traders and analysts looking to identify seasonal patterns, assess risk and opportunity, and gain deeper insights into monthly performance metrics across years. Customize, explore, and make informed decisions with this powerful Pine Script indicator.

The Adaptive Pairwise Momentum System [QuantraSystems]The Adaptive Pairwise Momentum System

QuantraSystems guarantees that the information created and published within this document and on the Tradingview platform is fully compliant with applicable regulations, does not constitute investment advice, and is not exclusively intended for qualified investors.

Important Note!

The system equity curve presented here has been generated as part of the process of testing and verifying the methodology behind this script.

Crucially, it was developed after the system was conceptualized, designed, and created, which helps to mitigate the risk of overfitting to historical data. In other words, the system was built for robustness, not for simply optimizing past performance.

This ensures that the system is less likely to degrade in performance over time, compared to hyper-optimized systems that are tailored to past data. No tweaks or optimizations were made to this system post-backtest.

Even More Important Note!!

The nature of markets is that they change quickly and unpredictably. Past performance does not guarantee future results - this is a fundamental rule in trading and investing.

While this system is designed with broad, flexible conditions to adapt quickly to a range of market environments, it is essential to understand that no assumptions should be made about future returns based on historical data. Markets are inherently uncertain, and this system - like all trading systems - cannot predict future outcomes.

Introduction

The Adaptive Pairwise Momentum System is not just an indicator but a comprehensive asset rotation and trend-following system. In short, it aims to find the highest performing asset from the provided range.

The system dynamically optimizes capital allocation across up to four high-performing assets, ensuring that the portfolio adapts swiftly to changing market conditions. The system logic consists of sophisticated quantitative methods, rapid momentum analysis, and robust trend filtering. The overarching goal is to ensure that the portfolio is always invested in the highest-performing asset based on dynamic market conditions, while at the same time managing risk through broader market filters and internal mechanisms like volatility and beta analysis.

Legend

System Equity Curve:

The equity curve displayed in the chart is dynamically colored based on the asset allocation at any given time. This color-coded approach allows traders to immediately identify transitions between assets and the corresponding impact on portfolio performance.

Highlighting of Current Highest Performer:

The current bar in the chart is highlighted based on the confirmed highest performing asset. This is designed to give traders advanced notice of potential shifts in allocation even before a formal position change occurs. The highlighting enables traders to prepare in real time, making it easier to manage positions without lag, particularly in fast-moving markets.

Highlighted Symbols in the Asset Table:

In the table displayed on the right hand side of the screen, the current top-performing symbol is highlighted. This clear signal at a glance provides immediate insight into which asset is currently being favored by the system. This feature enhances clarity and helps traders make informed decisions quickly, without needing to analyze the underlying data manually.

Performance Overview in Tables:

The left table provides insight into both daily and overall system performance from inception, offering traders a detailed view of short-term fluctuations and long-term growth. The right-hand table breaks down essential metrics such as Sharpe ratio, Sortino ratio, Omega ratio, and maximum drawdown for each asset, as well as for the overall system and HODL strategy.

Asset-Specific Signals:

The signals column in the table indicates whether an asset is currently held or being considered for holding based on the system's dynamic rankings. This is a critical visual aid for asset reallocation decisions, signaling when it may be appropriate to either maintain or change the asset of the portfolio.

Core Features and Methodologies

Flexibility in Asset Selection

One of the major advantages of this system is its flexibility. Users can easily modify the number and type of assets included for comparison. You can quickly input different assets and backtest their performance, allowing you to verify how well this system might fit different tokens or market conditions. This flexibility empowers users to adapt the system to a wide range of market environments and tailor it to their unique preferences.

Whole System Risk Mitigation - Macro Trend Filter

One of the features of this script is its integration of a Macro-level Trend Filter for the entire portfolio. The purpose of this filter is to ensure no capital is allocated to any token in the rotation system unless Bitcoin itself is in a positive trend. The logic here is that Bitcoin, as the cryptocurrency market leader, often sets the tone for the entire cryptocurrency market. By using Bitcoins trend direction as a barometer for overall market conditions, we create a system where capital is not allocated during unfavorable or bearish market conditions - significantly reducing exposure to downside risk.

Users have the ability to toggle this filter on and off in the input menu, with five customizable options for the trend filter, including the option to use no filter. These options are:

Nova QSM - a trend aggregate combining the Rolling VWAP, Wave Pendulum Trend, KRO Overlay, and the Pulse Profiler provides the market trend signal confirmation.

Kilonova QSM - a versatile aggregate combining the Rolling VWAP, KRO Overlay, the KRO Base, RSI Volatility Bands, NNTRSI, Regression Smoothed RSI and the RoC Suite.

Quasar QSM - an enhanced version of the original RSI Pulsar. The Quasar QSM refines the trend following approach by utilizing an aggregated methodology.

Pairwise Momentum and Strength Ranking

The backbone of this system is its ability to identify the strongest-performing asset in the selected pool, ensuring that the portfolio is always exposed to the asset showing the highest relative momentum. The system continually ranks these assets against each other and determines the highest performer by measure of past and coincident outperformance. This process occurs rapidly, allowing for swift responses to shifts in market momentum, which ensures capital is always working in the most efficient manner. The speed and precision of this reallocation strategy make the script particularly well-suited for active, momentum-driven portfolios.

Beta-Adjusted Asset Selection as a Tiebreaker

In the circumstance where two (or more) assets exhibit the same relative momentum score, the system introduces another layer of analysis. In the event of a strength ‘tie’ the system will preference maintaining the current position - that is, if the previously strongest asset is now tied, the system will still allocate to the same asset. If this is not the case, the asset with the higher beta is selected. Beta is a measure of an asset’s volatility relative to Bitcoin (BTC).

This ensures that in bullish conditions, the system favors assets with a higher potential for outsized gains due to their inherent volatility. Beta is calculated based on the Average Daily Return of each asset compared to BTC. By doing this, the system ensures that it is dynamically adjusting to risk and reward, allocating to assets with higher risk in favorable conditions and lower risk in less favorable conditions.

Dynamic Asset Reallocation - Opposed to Multi-Asset Fixed Intervals

One of the standout features of this system is its ability to dynamically reallocate capital. Unlike traditional portfolio allocation strategies that may rebalance between a basket of assets monthly or quarterly, this system recalculates and reallocates capital on the next bar close (if required). As soon as a new asset exhibits superior performance relative to others, the system immediately adjusts, closing the previous position and reallocating funds to the top-ranked asset.

This approach is particularly powerful in volatile markets like cryptocurrencies, where trends can shift quickly. By reallocating swiftly, the system maximizes exposure to high-performing assets while minimizing time spent in underperforming ones. Moreover, this process is entirely automated, freeing the trader from manually tracking and measuring individual token strength.

Our research has demonstrated that, from a risk-adjusted return perspective, concentration into the top-performing asset consistently outperforms broad diversification across longer time horizons. By focusing capital on the highest-performing asset, the system captures outsized returns that are not achievable through traditional diversification. However, a more risk-averse investor, or one seeking to reduce drawdowns, may prefer to move the portfolio further left along the theoretical Capital Allocation Line by incorporating a blend of cash, treasury bonds, or other yield-generating assets or even include market neutral strategies alongside the rotation system. This hybrid approach would effectively lower the overall volatility of the portfolio while still maintaining exposure to the system’s outsized returns. In theory, such an investor can reduce risk without sacrificing too much potential upside, creating a more balanced risk-return profile.

Position Changes and Fees/Slippage

Another critical and often overlooked element of this system is its ability to account for fees and slippage. Given the increased speed and frequency of allocation logic compared to the buy-and-hold strategy, it is of vital importance that the system recognises that switching between assets may incur slippage, especially in highly volatile markets. To account for this, the system integrates realistic slippage and fee estimates directly into the equity curve, simulating expected execution costs under typical market conditions and gives users a more realistic view of expected performance.

Number of Position Changes

Understanding the number of position changes in a strategy is critical to assessing its feasibility in real world trading. Frequent position changes can lead to increased costs due to slippage and fees. Monitoring the number of position changes provides insight into the system’s behavior - helping to evaluate how active the strategy is and whether it aligns with the trader's desired time input for position management.

Equity Curve and Performance Calculations

To provide a benchmark, the script also generates a Buy-and-Hold (or "HODL") equity curve that represents an equal split across the four selected assets. This allows users to easily compare the performance of the dynamic rotation system with that of a more traditional investment strategy.

The script tracks key performance metrics for both the dynamic portfolio and the HODL strategy, including:

Sharpe Ratio

The Sharpe Ratio is a key metric that evaluates a portfolio’s risk-adjusted return by comparing its ‘excess’ return to its volatility. Traditionally, the Sharpe Ratio measures returns relative to a risk-free rate. However, in our system’s calculation, we omit the risk-free rate and instead measure returns above a benchmark of 0%. This adjustment provides a more universal comparison, especially in the context of highly volatile assets like cryptocurrencies, where a traditional risk-free benchmark, such as the usual 3-month T-bills, is often irrelevant or too distant from the realities of the crypto market.

By using 0% as the baseline, we focus purely on the strategy's ability to generate raw returns in the face of market risk, which makes it easier to compare performance across different strategies or asset classes. In an environment like cryptocurrency, where volatility can be extreme, the importance of relative return against a highly volatile backdrop outweighs comparisons to a risk-free rate that bears little resemblance to the risk profile of digital assets.

Sortino Ratio

The Sortino Ratio improves upon the Sharpe Ratio by specifically targeting downside risk and leaves the upside potential untouched. In contrast to the Sharpe Ratio (which penalizes both upside and downside volatility), the Sortino Ratio focuses only on negative return deviations. This makes it a more suitable metric for evaluating strategies like the Adaptive Pairwise Momentum Strategy - that aim to minimize drawdowns without restricting upside capture. By measuring returns relative to a 0% baseline, the Sortino ratio provides a clearer assessment of how well the system generates gains while avoiding substantial losses in highly volatile markets like crypto.

Omega Ratio

The Omega Ratio is calculated as the ratio of gains to losses across all return thresholds, providing a more complete view of how the system balances upside and downside risk even compared to the Sortino Ratio. While it achieves a similar outcome to the Sortino Ratio by emphasizing the system's ability to capture gains while limiting losses, it is technically a mathematically superior method. However, we include both the Omega and Sortino ratios in our metric table, as the Sortino Ratio remains more widely recognized and commonly understood by traders and investors of all levels.

Case Study

Notes

For the sake of brevity, the Important Notes section found in the header of this text will not be rewritten. Instead, it will be highlighted that now is the perfect time to reread these notes. Reading this case study in the context of what has been mentioned above is of key importance.

As a second note, it is worth mentioning that certain market periods are referred to as either “Bull” or “Bear” markets - terms I personally find to be vague and undefinable - and therefore unfavorable. They will be used nevertheless, due to their familiarity and ease of understanding in this context. Substitute phrases could be “Macro Uptrend” or “Macro Downtrend.”

Overview

This case study provides an in-depth performance analysis of the Adaptive Pairwise Momentum System , a long-only system that dynamically allocates to outperforming assets and moves into cash during unfavorable conditions.

This backtest includes realistic assumptions for slippage and fees, applying a 0.5% cost for every position change, which includes both asset reallocation and moving to a cash position. Additionally, the system was tested using the top four cryptocurrencies by market capitalization as of the test start date of 01/01/2022 in order to minimize selection bias.

The top tokens on this date (excluding Stablecoins) were:

Bitcoin

Ethereum

Solana

BNB

This decision was made in order to avoid cherry picking assets that might have exhibited exceptional historical performance - minimizing skew in the back test. Furthermore, although this backtest focuses on these specific assets, the system is built to be flexible and adaptable, capable of being applied to a wide range of assets beyond those initially tested.

Any potential lookahead bias or repainting in the calculations has been addressed by implementing the lookback modifier for all repainting sensitive data, including asset ratios, asset scoring, and beta values. This ensures that no future information is inadvertently used in the asset allocation process.

Additionally, a fixed lookback period of one bar is used for the trend filter during allocations - meaning that the trend filter from the prior bar must be positive for an allocation to occur on the current bar. It is also important to note that all the data displayed by the indicator is based on the last confirmed (closed) bar, ensuring that the entire system is repaint-proof.

The study spans the 2022 cryptocurrency bear market through the subsequent bull market of 2023 and 2024. The stress test highlights how the system reacted to one of the most challenging market downturns in crypto history - which includes events such as:

Luna and TerraUSD crash

Three Arrows Capital liquidation

Celsius bankruptcy

Voyager Digital bankruptcy

FTX collapse

Silicon Valley + Signature + Silvergate banking collapses

Subsequent USDC deppegging

And arguably more important, 2022 was characterized by a tightening of monetary policy after the unprecedented monetary easing in response to the Covid pandemic of 2020/2021. This shift undeniably puts downward pressure on asset prices, most probably to the extent that this had a causal role to many of the above events.

By incorporating these real-world challenges, the backtest provides a more accurate and robust performance evaluation that avoids overfitting or excessive optimization for one specific market condition.

The Bear Market of 2022: Stress Test and System Resilience

During the 2022 bear market, where the overall crypto market experienced deep and consistent corrections, the Adaptive Pairwise Momentum System demonstrated its ability to mitigate downside risk effectively.

Dynamic Allocation and Cash Exposure:

The system rotated in and out of cash, as indicated by the gray period on the system equity curve. This allocation to cash during downtrending periods, specifically in late 2022, acted as the systems ‘risk-off’ exposure - the purest form of such an exposure. This prevented the system from experiencing the magnitude of drawdown suffered by the ‘Buy-and-Hold (HODL) investors.

In contrast, a passive HODL strategy would have suffered a staggering 75.32% drawdown, as it remained fully allocated to chosen assets during the market's decline. The active Pairwise Momentum system’s smaller drawdown of 54.35% demonstrates its more effective capital preservation mechanisms.

The Bull Market of 2023 and 2024: Capturing Market Upside

Following the crypto bear market, the system effectively capitalized on the recovery and subsequent bull market of 2023 and 2024.

Maximizing Market Gains:

As trends began turning bullish in early 2023, the system caught the momentum and promptly allocated capital to only the quantified highest performing asset of the time - resulting in a parabolic rise in the system's equity curve. Notably, the curve transitions from gray to purple during this period, indicating that Solana (SOL) was the top-performing asset selected by the system.

This allocation to Solana is particularly striking because, at the time, it was an asset many in the market shunned due to its association with the FTX collapse just months prior. However, this highlights a key advantage of quantitative systems like the one presented here: decisions are driven purely from objective data - free from emotional or subjective biases. Unlike human traders, who are inclined (whether consciously or subconsciously) to avoid assets that are ‘out of favor,’ this system focuses purely on price performance, often uncovering opportunities that are overlooked by discretionary based investors. This ability to make data-driven decisions ensures that the strategy is always positioned to capture the best risk-adjusted returns, even in scenarios where judgment might fail.

Minimizing Volatility and Drawdown in Uptrends

While the system captured substantial returns during the bull market it also did so with lower volatility compared to HODL. The sharpe ratio of 4.05 (versus HODL’s 3.31) reflects the system's superior risk-adjusted performance. The allocation shifts, combined with tactical periods of cash holding during minor corrections, ensured a smoother equity curve growth compared to the buy-and-hold approach.

Final Summary

The percentage returns are mentioned last for a reason - it is important to emphasize that risk-adjusted performance is paramount. In this backtest, the Pairwise Momentum system consistently outperforms due to its ability to dynamically manage risk (as seen in the superior Sharpe, Sortino and Omega ratios). With a smaller drawdown of 54.35% compared to HODL’s 75.32%, the system demonstrates its resilience during market downturns, while also capturing the highest beta on the upside during bullish phases.

The system delivered 266.26% return since the backtest start date of January 1st 2022, compared to HODL’s 10.24%, resulting in a performance delta of 256.02%

While this backtest goes some of the way to verifying the system’s feasibility, it’s important to note that past performance is not indicative of future results - especially in volatile and evolving markets like cryptocurrencies. Market behavior can shift, and in particular, if the market experiences prolonged sideways action, trend following systems such as the Adaptive Pairwise Momentum Strategy WILL face significant challenges.

Risk Radar ProThe "Risk Radar Pro" indicator is a sophisticated tool designed to help investors and traders assess the risk and performance of their investments over a specified period. This presentation will explain each component of the indicator, how to interpret the results, and the advantages compared to traditional metrics.

The "Risk Radar Pro" indicator includes several key metrics:

● Beta

● Maximum Drawdown

● Compound Annual Growth Rate (CAGR)

● Annualized Volatility

● Dynamic Sharpe Ratio

● Dynamic Sortino Ratio

Each of these metrics is dynamically calculated using data from the entire selected period, providing a more adaptive and accurate measure of performance and risk.

1. Start Date

● Description: The date from which the calculations begin.

● Interpretation: This allows the user to set a specific period for analysis, ensuring that all metrics reflect the performance from this point onward.

2. Beta

● Description: Beta measures the volatility or systematic risk of the instrument relative to a reference index (e.g., SPY).

● Interpretation: A beta of 1 indicates that the instrument moves with the market. A beta greater than 1 indicates more volatility than the market, while a beta less than 1 indicates less volatility.

● Advantages: Unlike classic beta, which typically uses fixed historical intervals, this dynamic beta adjusts to market changes over the entire selected period, providing a more responsive measure.

3. Maximum Drawdown

● Description: The maximum observed loss from a peak to a trough before a new peak is achieved.

● Interpretation: This shows the largest single drop in value during the specified period. It is a critical measure of downside risk.

● Advantages: By tracking the maximum drawdown dynamically, the indicator can provide timely alerts when significant losses occur, allowing for better risk management.

4. Annualized Performance

● Description: The mean annual growth rate of the investment over the specified period.

● Interpretation: The Annualized Performance represents the smoothed annual rate at which the investment would have grown if it had grown at a steady rate.

● Advantages: This dynamic calculation reflects the actual long-term growth trend of the investment rather than relying on a fixed time frame.

5. Annualized Volatility

● Description: Measures the degree of variation in the instrument's returns over time, expressed as a percentage.

● Interpretation: Higher volatility indicates greater risk, as the investment's returns fluctuate more.

● Advantages: Annualized volatility calculated over the entire selected period provides a more accurate measure of risk, as it includes all market conditions encountered during that time.

6. Dynamic Sharpe Ratio

● Description: Measures the risk-adjusted return of an investment relative to its volatility.

● Choice of Risk-Free Rate Ticker: Users can select a ticker symbol to represent the risk-free rate in Sharpe ratio calculations. The default option is US03M, representing the 3-month US Treasury bill.

● Interpretation: A higher Sharpe ratio indicates better risk-adjusted returns. This ratio accounts for the risk-free rate to provide a comparison with risk-free investments.

● Advantages: By using returns and volatility over the entire period, the dynamic Sharpe ratio adjusts to changes in market conditions, offering a more accurate measure than traditional static calculations.

7. Dynamic Sortino Ratio

● Description: Similar to the Sharpe ratio, but focuses only on downside risk.

Interpretation: A higher Sortino ratio indicates better risk-adjusted returns, focusing solely on negative returns, which are more relevant to risk-averse investors.

● Choice of Risk-Free Rate Ticker: Similarly, users can choose a ticker symbol for the risk-free rate in Sortino ratio calculations. By default, this is also set to US03M.

● Advantages: This ratio's dynamic calculation considering the downside deviation over the entire period provides a more accurate measure of risk-adjusted returns in volatile markets.

Comparison with Basic Metrics

● Static vs. Dynamic Calculations: Traditional metrics often use fixed historical intervals, which may not reflect current market conditions. The dynamic calculations in "Risk Radar Pro" adjust to market changes, providing more relevant and timely information.

● Comprehensive Risk Assessment: By including metrics like maximum drawdown, Sharpe ratio, and Sortino ratio, the indicator provides a holistic view of both upside potential and downside risk.

● User Customization: Users can customize the start date, reference index, risk-free rate, and table position, tailoring the indicator to their specific needs and preferences.

Conclusion

The "Risk Radar Pro" indicator is a powerful tool for investors and traders looking to assess and manage risk more effectively. By providing dynamic, comprehensive metrics, it offers a significant advantage over traditional static calculations, ensuring that users have the most accurate and relevant information to make informed decisions.

The "Risk Radar Pro" indicator provides analytical tools and metrics for informational purposes only. It is not intended as financial advice. Users should conduct their own research and consider their individual risk tolerance and investment objectives before making any investment decisions based on the indicator's outputs. Trading and investing involve risks, including the risk of loss. Past performance is not indicative of future results.

Drawdown % (with SMA)This script, titled "Drawdown % (with SMA)" and designed for Pine Script version 5

offers a sophisticated tool for traders to monitor drawdown percentages, a crucial metric in assessing investment risks. The script calculates the drawdown as the percentage decrease from the all-time high value of the selected financial instrument.

Blockunity Drawdown Visualizer (BDV)Monitor the drawdown (value of the drop between the highest and lowest points) of assets and act accordingly to reduce your risk.

Introducing BDV, the incredibly intuitive metric that visualizes asset drawdowns in the most visually appealing manner. With its color gradient display, BDV allows you to instantly grasp the state of retracement from the asset’s highest price level. But that’s not all – you have the option to display the oscillator’s colorization directly on your chart, enhancing your analysis even further.

The Idea

The goal is to provide the community with the best and most complete tool for visualizing the Drawdown of any asset.

How to Use

Very simple to use, the indicator takes the form of an oscillator, with colors ranging from red to green depending on the Drawdown level. A table summarizes several key data points.

Elements

On the oscillator, you'll find a line with a color gradient showing the asset's Drawdown. The flatter line represents the Max Drawdown (the lowest value reached).

In addition, the table summarizes several data:

The asset's All Time High (ATH).

Current Drawdown.

The Max Drawdown that has been reached.

Settings

First of all, you can activate a "Bar Color" in the settings (You must also uncheck "Borders" and "Wick" in your Chart Settings):

You can display Fibonacci levels on the oscillator. You'll see that levels can be relevant to drawdown. The color of the levels is also configurable.

In the calculation parameters, you can first choose between taking the High of the candles or the Close. By default this is Close, but if you change the parameter to High, the indication next to ATH in the table will change, and you'll see that the values in the table will be affected.

The second calculation parameter (Start Date) lets you modify the effective start date of the ATH, which will affect the drawdown level. Here's an example:

How it Works

First, we calculate the ATH:

var bdv_top = bdv_source

bdv_top := na(bdv_top ) ? bdv_source : math.max(bdv_source, bdv_top )

Then the drawdown is calculated as follows:

bdv = ((bdv_source / bdv_top) * 100) - 100

Then the max drawdown :

bdv_max = bdv

bdv_max := na(bdv_max ) ? bdv : math.min(bdv, bdv_max )

ATH Drawdown Indicator by Atilla YurtsevenThe ATH (All-Time High) Drawdown Indicator, developed by Atilla Yurtseven, is an essential tool for traders and investors who seek to understand the current price position in relation to historical peaks. This indicator is especially useful in volatile markets like cryptocurrencies and stocks, offering insights into potential buy or sell opportunities based on historical price action.

This indicator is suitable for long-term investors. It shows the average value loss of a price. However, it's important to remember that this indicator only displays statistics based on past price movements. The price of a stock can remain cheap for many years.

1. Utility of the Indicator:

The ATH Drawdown Indicator provides a clear view of how far the current price is from its all-time high. This is particularly beneficial in assessing the magnitude of a pullback or retracement from peak levels. By understanding these levels, traders can gauge market sentiment and make informed decisions about entry and exit points.

2. Risk Management:

This indicator aids in risk management by highlighting significant drawdowns from the ATH. Traders can use this information to adjust their position sizes or set stop-loss orders more effectively. For instance, entering trades when the price is significantly below the ATH could indicate a higher potential for recovery, while a minimal drawdown from the ATH may suggest caution due to potential overvaluation.

3. Indicator Functionality:

The indicator calculates the percentage drawdown from the ATH for each trading period. It can display this data either as a line graph or overlaid on candles, based on user preference. Horizontal lines at -25%, -50%, -75%, and -100% drawdown levels offer quick visual cues for significant price levels. The color-coding of candles further aids in visualizing bullish or bearish trends in the context of ATH drawdowns.

4. ATH Level Indicator (0 Level):

A unique feature of this indicator is the 0 level, which signifies that the price is currently at its all-time high. This level is a critical reference point for understanding the market's peak performance.

5. Mean Line Indicator:

Additionally, this indicator includes a 'Mean Line', representing the average percentage drawdown from the ATH. This average is calculated over more than a thousand past bars, leveraging the law of large numbers to provide a reliable mean value. This mean line is instrumental in understanding the typical market behavior in relation to the ATH.

Disclaimer:

Please note that this ATH Drawdown Indicator by Atilla Yurtseven is provided as an open-source tool for educational purposes only. It should not be construed as investment advice. Users should conduct their own research and consult a financial advisor before making any investment decisions. The creator of this indicator bears no responsibility for any trading losses incurred using this tool.

Please remember to follow and comment!

Trade smart, stay safe

Atilla Yurtseven

Drawdown Dynamics IndicatorDescription :

The Drawdown Dynamics Indicator is a straightforward tool that offers insights into three critical aspects of an asset’s financial performance: Total Max Drawdown, Rolling Period Max Drawdown, and Current Max Drawdown. Inside of the indicator, you can select to view either the rolling period max drawdown or the all-time max drawdown. This is represented by the gray line. The blue line represents the asset's current drawdown.

Rolling Period Max Drawdown is more about a snapshot view, highlighting the maximum loss from a peak to a trough for an adjustable rolling time frame. This is a feature not available with other indicators that exist on TradingView.

Total Max Drawdown gives a broad view, showcasing the all-time deepest decline in an asset’s value.

Current Max Drawdown offers a live update, focusing on the asset's present phase and how it's performing in real-time.

Practical Uses :

The utility of this indicator becomes evident when you start exploring the risks and performance metrics of assets. A notable use of this indicator is in comparing the drawdowns of a trading strategy against the inherent drawdowns of an asset. It helps in painting a clearer picture of risk and performance of both the asset and the strategy.

Risk Understanding : By comparing the strategy drawdown to the asset drawdown, traders get to understand if the risk they’re taking aligns with the asset’s natural risk behavior.

Evaluating Strategy’s Strength : If a strategy can weather the storms of the asset's natural drawdown phases and come out relatively unscathed, it can speak to its strength.

Performance Comparison : It also acts as a benchmark tool. Traders can pit different strategies against each other, using the asset’s drawdown as a baseline, to see which one manages risks better.

Disclaimer : This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

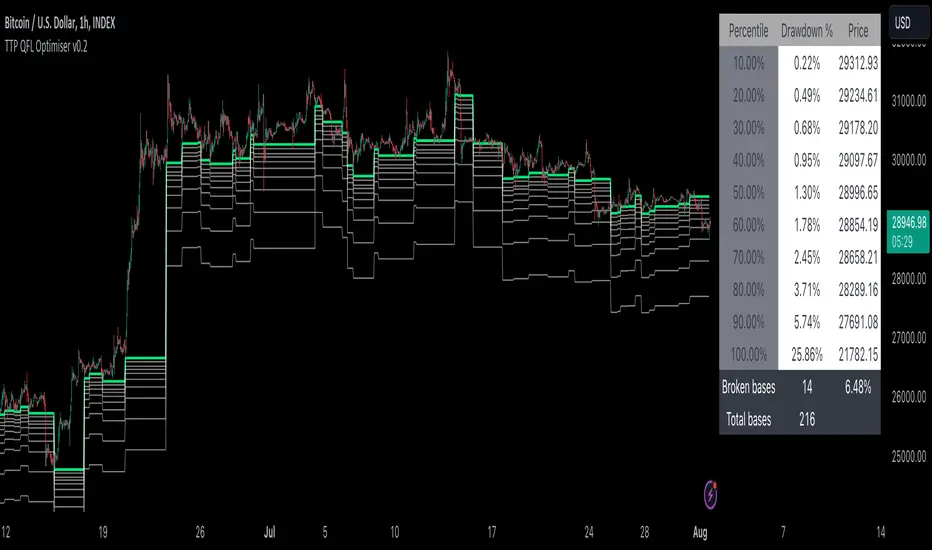

TTP QFL OptimiserThis tool is designed to help finding the best take profit and stop loss levels when trading with QFL bases (Quick Fingers Luc).

You can use it to see the average drawdown among all historic bases broken for an asset and then find the drawdowns that are more frequent using the percentile parameters provided.

For example, by knowing that 98% of the bases got broken with a drawdown of up to 5% can become extremely useful for deciding where to place your take profit or stop loss levels.

It supports QFL 1H, 2H and 4H but make sure to set the chart timeframe to a lower timeframe than QFL to obtain valid results.

Two percentiles are provided to be able to evaluate potential TP and SL at the same time.

Steps:

- Load an asset in the 15min TF

- Select the QFL version: 1H more deals / lower quality vs 4H less deals/ better quality

- Find a percentile that triggers enough deals (example: 70) and then another percentile that doesn't get hit too much (example: 98)

- Confirm the values p1 and p2 provided in the table and the white and grey lines for the results of which drawdown percentages correspond to such selection of percentiles

Once having p1 and p2 use your backtesting and forward testing tools to confirm and adjust accordingly.

TTP RSI drawdownThis indicator offers a way to trade the RSI drawdown combined together with its value.

Parameters

- Lookback. How many candles in the past are used to calculate the drawdown of the RSI

- RSI strength and timeframe

- Lower and Upper RSI limits. These are used to colour the drawdown chart, the greener the closed to your specified lower limit and the more red the closer to the upper limit. These limits are also used to confirm that the signal occurs with an RSI value within the given limits.

- Signal threshold. Buy signals will only be triggered when the drawdown of the RSI is higher than the provided value.

Buy signals

The signal will trigger in white color and will plot a 1 to allow backtesting.

TradingView alerts can be set for buy signals.

Buy signals will be trigger only when:

- RSI value is within the provided lower and upper limit values

- RSI drawdown is higher than the provided threshold.

Features

- Back-testable (plots 1 for buy)

- TV alerts

Chart modes

- show RSI

- show highest RSI

- show RSI drawdown

In the short time I've been playing with this new idea I noticed it can be used both for swing trading and for long term analysis like for example finding market bottoms.

Here's an example setup to find BTC past market cycle bottoms:

- load a chart with INDEX:BTCUSD

- set the chart timeframe to daily

- set the chart to logarithmic scale

- zoom out to see the full chart

- add the RSI drawdown indicator

- use the following parameters in the indicator: timeframe: week, gaps: off, show RSI drawdown: on, lookback:30, length:14, lower: 20, upper: 30: threshold: 40

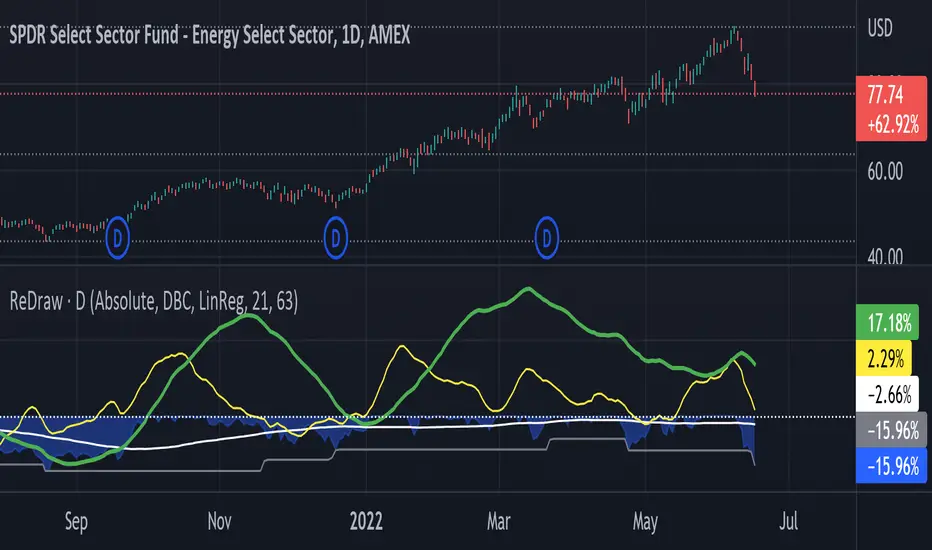

Return & Drawdown

ReDraw script calculates the historical returns and drawdown for the given periods.

By default, the return of the linear regression trends is displayed (can be turned off in settings). In this mode, two linear regression trends are being computed for both long and short periods, and the percent value indicates the "return of the trend" for the corresponding period. Observing the dynamic of the linear regression trends can give a great hint if the trend is slowing down.

When the smoothing method is set to "none" or WMA3/5, the real asset return is shown for both periods, using the formula (LastPrice-FirstPrice)/FirstPrice

The script calculates the maximum drawdown for the long period using the formula (max(Price) - LastPrice) / max(Price).

The white line under the zero is the average maximum drawdown over the long period.

When the mode is set to Compare, ReDraw will display the difference in metrics between the current and selected symbol (SPY by default).

Sig30MALICEHello everyone

Bot is optimalized BINANCE:ALICEUSDTPERP BOT, which select leverage betwen 2x and 4x

TimeFrame : 30min

TP : 80 point

SL : 120 point

the bot works as follows:

the way he opens a position consists of two conditions

1) Moving average (crossovers)

2) RSI

Backtesting is set for counting as 13 contrat, this bot can get more with 50% of equity.

I think this is really solid 30min bot, which is already really important to make something solid on 30min

However keep in mind this is scalper and optimalization scalpers are really hard and have to be set from time to time

This bot is also great for other optimalizations .

.

.

.

.

.

.

Enjoy

trailing_drawdown

Description:

Drawdown was a tool to measure historical risk, derived from measuring current wealth from its previous peak, casually from portfolio construction (weights allocation), will consider to having a minimum drawdown. In this indicator, the drawdown for individual assets is utilized to measure its value or percentage from its trailing peak (default to 1-yr period).

Drawdown:

drawdown = (price/peaks)-1

Feature:

Static: display drawdown as percentage

Dynamic: display drawdown as value

Yearly Percentage ReturnsAn indicator that lets you visualize the historical Yearly Percentage returns of any symbol .

Key Features:

Displays the yearly returns from start to end of each year

Displays a table showing all yearly returns for current symbol

Displays start of each year as a vertical line

Displays up to 5 custom horizontal levels

Table Settings:

Enable table - Show/Hide the table

Size - Sets the size of the table

Position - Sets the position of the table on the screen

Direction - Sets the direction of the table to display the data (Vertically or Horizontally)

Percent Off All-time High (% Off High)Percent Off All-time High tracks the percentage difference between the previous day’s closing price and the All-Time high price of the security’s entire price history.

This metric tells you how far the price has deviated from/converged on the all-time high price.

Simple/Compounded Returns & Drawdowns TableVery excited to bring this script to the public. This is a very useful table that displays the performance of any strategy you give it in a more detailed view. It runs on all timeframes and at any position on the chart with the replay function. It also updates on tick changes. The table consists of three modes: Simple Equity, Compound Equity and Drawdown.

Simple Equity – shows the change in equity for every month and year. It is calculated by finding the difference in initial equity at the beginning of the month/year and the end of the month/year. The table will thus display strategy performance in blocks of time that are not correlated. It is an excellent way to see individual month/year performance from start to finish but it may not represent true change in equity over time. For example, let's assume that 100% of equity is used on every trade for simplicity. If a loss of 50% is made in the first month and a profit of 100% is made in the next month, the strategy will show 50% profit for the year. This aggregate value might be helpful to know for testing purposes, but in reality, the account is actually at break-even for the year (Initial Equity * 0.5 * 2 = Initial Equity).

Compound Equity – shows compounded change in equity for every month and year. It is calculated by finding the difference in starting equity when the strategy is run and equity at the end of the month/year. The table will thus display the true strategy performance – compounded equity at the end of each month/year.

Drawdown – shows max drawdown for every month and year. It is calculated by finding the difference between the highest equity achieved for the month/year and the trough in equity for the same month/year. Notice: strategy tester might have a max drawdown value higher than any of the drawdown values in the table. This is because the strategy tester calculates the difference between the highest and lowest equity for the entire strategy, whereas the table displays drawdowns for months and years only. Sometimes, the max drawdown for the year will also be the max drawdown for the entire strategy; hence the two values will be the same.

To use this table with your own strategy, simply find " PLACE YOUR STRATEGY CODE HERE " at the bottom of the script and place your strategy code there. Special thanks to QuantNomad for the inspiration. As always, please let me know if there are any bugs or if you need some help. Leave a like if you wish!

BCT Buy And Hold w/ Advanced StatisticsThis is a script designed to simulate a buy and hold strategy in the chart that its applied to.

Tradingview backtester is really limited in the statistics it gives you based on equity and information of open trades. For that reason many of the buy and hold scripts suffer from the same problem, a lack of useful statistics about your buy and hold strategy.

This script allows you to filter a specific buy and hold period (or use the whole data available in the tradingivew chart) and get useful statistics based on equity on a bar by bar basis.

Date Range Filtering

This allows you to chose a specific period to test the buy and hold strategy and to visualize the statistics.

We include 3 main tables which offer useful information so you can compare your strategy vs buy and hold strategy.

This 3 tables are:

Draw Downs Table

This table shows the Current P/L, Current Draw Down, Average and Maximum Draw Downs based on the equity of the buy and hold strategy calculated by candle. This can show you how much average and maximum loss or pain you would have to go through in order to stick to the buy and hold strategy.

Custom Statistics Table

This table shows useful advanced statistics to compare the buy and hold strategy to other strategies.

CAGR: Compounded annual growth rate is the industry standard in terms of showing annualized returns for any strategy or investment.

Annualized Return ($)

Trade Duration (Days): Self explanatory, displays how long the buy and hold trade was open or is open counted in days.

Max Stagnation Period (Days): Measures the Maximum time taken between new equity highs.

Average Draw Down : Average value of all draw downs from equity highs over the period (sampled 1 time per candle).

Maximum Draw Down : Largest draw down from equity highs in the whole period.

Return / Avg DrawDown: Advanced Proprietary statistic in which the annualized (non compounding) return is divided by the Average Draw Down (displayed in the Draw Downs Table)

Return / Maximum DrawDown: Advanced statistic in which the annualized (non compounding) return is divided by the Maximum Draw Down (displayed in the Draw Downs Table)

CAGR / Avg DrawDown: Advanced Proprietary statistic in which the CAGR (compounding) is divided by the Average Draw Down (displayed in the Draw Downs Table)

CAGR / Maximum DrawDown: Advanced Proprietary statistic in which the CAGR (compounding) is divided by the Maximum Draw Down (displayed in the Draw Downs Table)

Note: All the advanced statistics show, in slightly different ways, how much a strategy compensates you in relation to the risk taken. In other words you can see this as a way to quantify risk adjusted returns between multiple strategies. We prefer using the CAGR based advanced Statistics as they give a more universal value to compare across multiple strategies and asset classes.

In Sample / Out Of Sample Custom Stats (IS/OOS) Table

This table shows similar statistics as the Custom Statistics Table but is able to break down the backtest period into segments, this is useful when testing strategies as it can be used to test optimization quality. In this Buy and Hold strategy this can be used to visualize the stats of 2 periods at the same time and compare them without need to change settings or use another instance of the script.

All the Stats are the same as in the Custom Statistics Table with the difference of some being removed and the table being constructed in a way that facilitates the comparison of stats between In Sample, Out Of Sample and Full periods

Drawdown strategy indicatorThis indicator uses drawdown and max drawdown to determine good areas to enter or exit the market.

It uses the ratio between those values and two thresholds provided by the user: top and bottom.

These two values will be used to highlight the areas that match the users strategy criteria.

I normally use this indicator on the 4h or higher timeframes.

On BTC using the default parameters it predicts the tops pretty nicely. The areas of accumulation or buy zones are consistent with the ones that follow each halving.

The chart shows:

- Drawdown

- max drawdown

- drawdown average

- drawdown ratio

- buy and sell zones

The study includes alerts for both buy and sell zones.