Infinite Impulse Response (IIR) FilterInfinite Impulse Response (IIR) Filter indicator script.

This indicator was originally developed by John Ehlers (Stocks & Commodities V. 20:7 (26-31): Zero-Lag Data Smoothers).

Zerolag

Zero Lag Exponential Moving AverageZero Lag Exponential Moving Average indicator script based on the original version by John Ehlers and Ric Way

Zero Lag EMA v2 by KIVANÇ fr3762A different version of ZERO LAG EMA indicator by John Ehlers and Ric Way...

In this cover, Zero Lag EMA is calculated without using the PREV function.

The main purpose is that to provide BUY/SELL signals earlier than classical EMA's.

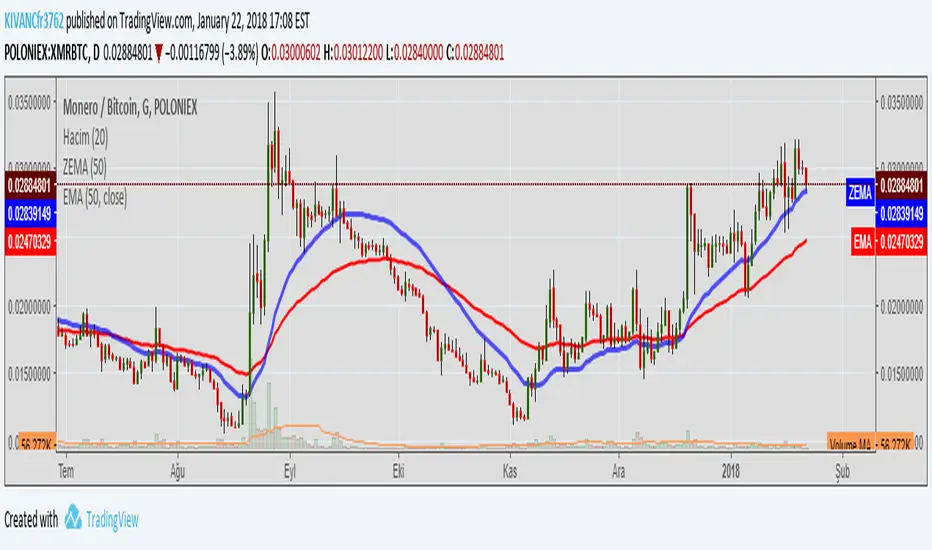

You can see the difference of conventional and Zero Lag EMA in the chart.

The red line is classical EMA and the blue colored line is ZEMA ( Zero Lag Ema ).

Turkish Explanation:

Ehlers ve Way'in ZERO LAG ,ndikatörünün Prev (previous value) kullanılmadan yorumlanarak hesaplanmış hali.

Amaç klasik Üssel Ortalamaya göre daha hızlı tepki verip, Al/Sat sinyallerini daha erken alabilmek.

Grafikte kırmızı renkle görülen normal Üssel HO ve mavi renkli olan Zero Lag (gecikmesiz) Üssel HO

Zero-Lag Average Directional Index with DI+ and DI-This average directional index follows the Nyquist Sampling Criterion making showing even better behaviour in high volatility environments than the Ehlers & Ric's "Zero Lag Moving Average".

Applies the same formulae as the moving average at Zero-lag Dürschner Moving Average

From the paper abstract: "The well-known Moving Averages (MA), namely the Simple Moving Average ( SMA ), the Exponential Moving Average ( EMA ) and the Weighted Moving Average ( WMA ), are modified in this paper with the help of the Nyquist Criterion. These modified Moving Averages 3.0 show good smoothing characteristics, illustrate relevant trends and trend reversals in price series without a time lag as far as calculated. With regard to smoothing, trend patterns and time lag bring about a significant improvement on conventional SMA (Moving Averages 1.0: SMA, EMA and WMA ). In addition to this, the efficiency of the Moving Averages 3.0 is demonstrated by applying several tests and a simple trading system."

The Dürschner Moving Average was published at the IFTA 2012 (International Federation of Technical Analysts) Journal, page 27.