Adaptive Causal Wavelet Trend FilterThe Adaptive Causal Wavelet Trend Filter is a technical indicator implementing causal approximations of wavelet transform properties for better trend detection with adaptive volatility response.

The Adaptive Causal Wavelet Trend Filter (ACWTF) applies mathematical principles derived from wavelet analysis to financial time series, providing robust trend identification with minimal lag. Unlike conventional moving averages, it preserves significant price movements while filtering market noise through signal processing that i describe below.

I was inspired to build this indicator after reading " Wavelet-Based Trend Identification in Financial Time Series " by In, F., & Kim, S. 2013 and reading about Mexican Hat wavelet filters.

The ACWTF maintains optimal performance across varying market regimes without requiring parameter adjustments by adapting filter characteristics to current volatility conditions.

Mathematical Foundation

Inspired by the Mexican Hat wavelet (Ricker wavelet), this indicator implements causal approximations of wavelet filters optimized for real-time financial analysis. The multi-resolution approach identifies features at different scales and the adaptive component dynamically adjusts filtering characteristics based on local volatility measurements.

Key mathematical properties include:

Non-linear frequency response adaptation

Edge-preserving signal extraction

Scale-space analysis through dual filter implementation

Volatility-dependent coefficient adjustment, which I love

Filter Methods

Adaptive: Implements a volatility-weighted combination of multiple filter types to optimize the time-frequency resolution trade-off

Hull: Provides a causal approximation of wavelet edge detection properties with forward-projection characteristics

VWMA: Incorporates volume information into the filtering process for enhanced signal detection

EMA Cascade: Creates a multi-pole filter structure that approximates certain wavelet scaling properties

Suggestion: try all as they will provide slightly different signals. Try also different time-frames.

Practical Applications

Trend Direction Identification: Clear visual trend direction with reduced noise and lag

Regime Change Detection: Early identification of significant trend reversals

Market Condition Analysis: Integrated volatility metrics provide context for current market behavior

Multi-timeframe Confirmation: Alignment between primary and secondary filters offers additional confirmation

Entry/Exit Timing: Filter crossovers and trend changes provide potential trading signals

The comprehensive information panel provides:

Current filter method and trend state

Trend alignment between timeframes

Real-time volatility assessment

Price position relative to filter

Overall trading bias based on multiple factors

Implementation Notes

Log returns option provides improved statistical properties for financial time series

Primary and secondary filter lengths can be adjusted to optimize for specific instruments and timeframes

The indicator performs particularly well during trend transitions and regime changes

The indicator reduces the need for using additional indicators to check trend reversion

Wavelet

Wavelet-Trend ML Integration [Alpha Extract]Alpha-Extract Volatility Quality Indicator

The Alpha-Extract Volatility Quality (AVQ) Indicator provides traders with deep insights into market volatility by measuring the directional strength of price movements. This sophisticated momentum-based tool helps identify overbought and oversold conditions, offering actionable buy and sell signals based on volatility trends and standard deviation bands.

🔶 CALCULATION

The indicator processes volatility quality data through a series of analytical steps:

Bar Range Calculation: Measures true range (TR) to capture price volatility.

Directional Weighting: Applies directional bias (positive for bullish candles, negative for bearish) to the true range.

VQI Computation: Uses an exponential moving average (EMA) of weighted volatility to derive the Volatility Quality Index (VQI).

Smoothing: Applies an additional EMA to smooth the VQI for clearer signals.

Normalization: Optionally normalizes VQI to a -100/+100 scale based on historical highs and lows.

Standard Deviation Bands: Calculates three upper and lower bands using standard deviation multipliers for volatility thresholds.

Signal Generation: Produces overbought/oversold signals when VQI reaches extreme levels (±200 in normalized mode).

Formula:

Bar Range = True Range (TR)

Weighted Volatility = Bar Range × (Close > Open ? 1 : Close < Open ? -1 : 0)

VQI Raw = EMA(Weighted Volatility, VQI Length)

VQI Smoothed = EMA(VQI Raw, Smoothing Length)

VQI Normalized = ((VQI Smoothed - Lowest VQI) / (Highest VQI - Lowest VQI) - 0.5) × 200

Upper Band N = VQI Smoothed + (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

Lower Band N = VQI Smoothed - (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

🔶 DETAILS

Visual Features:

VQI Plot: Displays VQI as a line or histogram (lime for positive, red for negative).

Standard Deviation Bands: Plots three upper and lower bands (teal for upper, grayscale for lower) to indicate volatility thresholds.

Reference Levels: Horizontal lines at 0 (neutral), +100, and -100 (in normalized mode) for context.

Zone Highlighting: Overbought (⋎ above bars) and oversold (⋏ below bars) signals for extreme VQI levels (±200 in normalized mode).

Candle Coloring: Optional candle overlay colored by VQI direction (lime for positive, red for negative).

Interpretation:

VQI ≥ 200 (Normalized): Overbought condition, strong sell signal.

VQI 100–200: High volatility, potential selling opportunity.

VQI 0–100: Neutral bullish momentum.

VQI 0 to -100: Neutral bearish momentum.

VQI -100 to -200: High volatility, strong bearish momentum.

VQI ≤ -200 (Normalized): Oversold condition, strong buy signal.

🔶 EXAMPLES

Overbought Signal Detection: When VQI exceeds 200 (normalized), the indicator flags potential market tops with a red ⋎ symbol.

Example: During strong uptrends, VQI reaching 200 has historically preceded corrections, allowing traders to secure profits.

Oversold Signal Detection: When VQI falls below -200 (normalized), a lime ⋏ symbol highlights potential buying opportunities.

Example: In bearish markets, VQI dropping below -200 has marked reversal points for profitable long entries.

Volatility Trend Tracking: The VQI plot and bands help traders visualize shifts in market momentum.

Example: A rising VQI crossing above zero with widening bands indicates strengthening bullish momentum, guiding traders to hold or enter long positions.

Dynamic Support/Resistance: Standard deviation bands act as dynamic volatility thresholds during price movements.

Example: Price reversals often occur near the third standard deviation bands, providing reliable entry/exit points during volatile periods.

🔶 SETTINGS

Customization Options:

VQI Length: Adjust the EMA period for VQI calculation (default: 14, range: 1–50).

Smoothing Length: Set the EMA period for smoothing (default: 5, range: 1–50).

Standard Deviation Multipliers: Customize multipliers for bands (defaults: 1.0, 2.0, 3.0).

Normalization: Toggle normalization to -100/+100 scale and adjust lookback period (default: 200, min: 50).

Display Style: Switch between line or histogram plot for VQI.

Candle Overlay: Enable/disable VQI-colored candles (lime for positive, red for negative).

The Alpha-Extract Volatility Quality Indicator empowers traders with a robust tool to navigate market volatility. By combining directional price range analysis with smoothed volatility metrics, it identifies overbought and oversold conditions, offering clear buy and sell signals. The customizable standard deviation bands and optional normalization provide precise context for market conditions, enabling traders to make informed decisions across various market cycles.

Wavelet Filter with Adaptive Upsampling [BackQuant]Wavelet Filter with Adaptive Upsampling

The Wavelet Filter with Adaptive Upsampling is an advanced filtering and signal reconstruction tool designed to enhance the analysis of financial time series data. It combines wavelet transforms with adaptive upsampling techniques to filter and reconstruct price data, making it ideal for capturing subtle market movements and enhancing trend detection. This system uses high-pass and low-pass filters to decompose the price series into different frequency components, applying adaptive thresholding to eliminate noise and preserve relevant signal information.

Shout out to Loxx for the Least Squares fitting of trigonometric series and Quinn and Fernandes algorithm for finding frequency

www.tradingview.com

Key Features

1. Frequency Decomposition with High-Pass and Low-Pass Filters:

The indicator decomposes the input time series using high-pass and low-pass filters to separate the high-frequency (detail) and low-frequency (trend) components of the data. This decomposition allows for a more accurate analysis of underlying trends, while mitigating the impact of noise.

2. Soft Thresholding for Noise Reduction:

A soft thresholding function is applied to the high-frequency component, allowing for the reduction of noise while retaining significant market signals. This function adjusts the coefficients of the high-frequency data, removing small fluctuations and leaving only the essential price movements.

3. Adaptive Upsampling Process:

The upsampling process in this script can be customized using different methods: sinusoidal upsampling, advanced upsampling, and simple upsampling. Each method serves a unique purpose:

Sinusoidal Upsample uses a sine wave to interpolate between data points, providing a smooth transition.

Advanced Upsample utilizes a Quinn-Fernandes algorithm to estimate frequency and apply more sophisticated interpolation techniques, adapting to the market’s cyclical behavior.

Simple Upsample linearly interpolates between data points, providing a basic upsampling technique for less complex analysis.

4. Reconstruction of Filtered Signal:

The indicator reconstructs the filtered signal by summing the high and low-frequency components after upsampling. This allows for a detailed yet smooth representation of the original time series, which can be used for analyzing underlying trends in the market.

5. Visualization of Reconstructed Data:

The reconstructed series is plotted, showing how the upsampling and filtering process enhances the clarity of the price movements. Additionally, the script provides the option to visualize the log returns of the reconstructed series as a histogram, with positive returns shown in green and negative returns in red.

6. Cumulative Series and Trend Detection:

A cumulative series is plotted to visualize the compounded effect of the filtered and reconstructed data. This feature helps traders track the overall performance of the asset over time, identifying whether the asset is following a sustained upward or downward trend.

7. Adaptive Thresholding and Noise Estimation:

The system estimates the noise level in the high-frequency component and applies an adaptive thresholding process based on the standard deviation of the downsampled data. This ensures that only significant price movements are retained, further refining the trend analysis.

8. Customizable Parameters for Flexibility:

Users can customize the following parameters to adjust the behavior of the indicator:

Frequency and Phase Shift: Control the periodicity of the wavelet transformation and the phase of the upsampling function.

Upsample Factor: Adjust the level of interpolation applied during the upsampling process.

Smoothing Period: Determine the length of time used to smooth the signal, helping to filter out short-term fluctuations.

References

Enhancing Cross-Sectional Currency Strategies with Context-Aware Learning to Rank

arxiv.org

Daubechies Wavelet - Wikipedia

en.wikipedia.org

Quinn Fernandes Fourier Transform of Filtered Price by Loxx

Note on Usage for Mean-Reversion Strategy

This indicator is primarily designed for trend-following strategies. However, by taking the inverse of the signals, it can be adapted for mean-reversion strategies. This involves buying underperforming assets and selling outperforming ones. Caution: This method may not work effectively with highly correlated assets, as the price movements between correlated assets tend to mirror each other, limiting the effectiveness of mean-reversion strategies.

Final Thoughts

The Wavelet Filter with Adaptive Upsampling is a powerful tool for traders seeking to improve their understanding of market trends and noise. By using advanced wavelet decomposition and adaptive upsampling, this system offers a clearer, more refined picture of price movements, enhancing trend-following strategies. It’s particularly useful for detecting subtle shifts in market momentum and reconstructing price data in a way that removes noise, providing more accurate insights into market conditions.

PaddingThe Padding library is a comprehensive and flexible toolkit designed to extend time series data within TradingView, making it an indispensable resource for advanced signal processing tasks such as FFT, filtering, convolution, and wavelet analysis. At its core, the library addresses the common challenge of edge effects by "padding" your data—that is, by appending additional data points beyond the natural boundaries of your original dataset. This extension not only mitigates the distortions that can occur at the endpoints but also helps to maintain the integrity of various transformations and calculations performed on the series. The library accomplishes this while preserving the ordering of your data, ensuring that the most recent point always resides at index 0.

Central to the functionality of this library are two key enumerations: Direction and PaddingType. The Direction enum determines where the padding will be applied. You can choose to extend the data in the forward direction (ahead of the current values), in the backward direction (behind the current values), or in both directions simultaneously. The PaddingType enum defines the specific method used for extending the data. The library supports several methods—including symmetric, reflect, periodic, antisymmetric, antireflect, smooth, constant, and zero padding—each of which has been implemented to suit different analytical scenarios. For instance, symmetric padding mirrors the original data across its boundaries, while reflect padding continues the trend by reflecting around endpoint values. Periodic padding repeats the data, and antisymmetric padding mirrors the data with alternating signs to counterbalance it. The antireflect and smooth methods take into account the derivatives of your data, thereby extending the series in a way that preserves or smoothly continues these derivative values. Constant and zero padding simply extend the series using fixed endpoint values or zeros. Together, these enums allow you to fine-tune how your data is extended, ensuring that the padding method aligns with the specific requirements of your analysis.

The library is designed to work with both single variable inputs and array inputs. When using array-based methods—particularly with the antireflect and smooth padding types—please note that the implementation intentionally discards the last data point as a result of the delta computation process. This behavior is an important consideration when integrating the library into your TradingView studies, as it affects the overall data length of the padded series. Despite this, the library’s structure and documentation make it straightforward to incorporate into your existing scripts. You simply provide your data source, define the length of your data window, and select the desired padding type and direction, along with any optional parameters to control the extent of the padding (using both_period, forward_period, or backward_period).

In practical application, the Padding library enables you to extend historical data beyond its original range in a controlled and predictable manner. This is particularly useful when preparing datasets for further signal processing, as it helps to reduce artifacts that can otherwise compromise the results of your analytical routines. Whether you are an experienced Pine Script developer or a trader exploring advanced data analysis techniques, this library offers a robust solution that enhances the reliability and accuracy of your studies by ensuring your algorithms operate on a more complete and well-prepared dataset.

Library "Padding"

A comprehensive library for padding time series data with various methods. Supports both single variable and array inputs, with flexible padding directions and periods. Designed for signal processing applications including FFT, filtering, convolution, and wavelets. All methods maintain data ordering with most recent point at index 0.

symmetric(source, series_length, direction, both_period, forward_period, backward_period)

Applies symmetric padding by mirroring the input data across boundaries

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with symmetric padding applied

method symmetric(source, direction, both_period, forward_period, backward_period)

Applies symmetric padding to an array by mirroring the data across boundaries

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with symmetric padding applied

reflect(source, series_length, direction, both_period, forward_period, backward_period)

Applies reflect padding by continuing trends through reflection around endpoint values

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with reflect padding applied

method reflect(source, direction, both_period, forward_period, backward_period)

Applies reflect padding to an array by continuing trends through reflection around endpoint values

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with reflect padding applied

periodic(source, series_length, direction, both_period, forward_period, backward_period)

Applies periodic padding by repeating the input data

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with periodic padding applied

method periodic(source, direction, both_period, forward_period, backward_period)

Applies periodic padding to an array by repeating the data

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with periodic padding applied

antisymmetric(source, series_length, direction, both_period, forward_period, backward_period)

Applies antisymmetric padding by mirroring data and alternating signs

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antisymmetric padding applied

method antisymmetric(source, direction, both_period, forward_period, backward_period)

Applies antisymmetric padding to an array by mirroring data and alternating signs

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antisymmetric padding applied

antireflect(source, series_length, direction, both_period, forward_period, backward_period)

Applies antireflect padding by reflecting around endpoints while preserving derivatives

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antireflect padding applied

method antireflect(source, direction, both_period, forward_period, backward_period)

Applies antireflect padding to an array by reflecting around endpoints while preserving derivatives

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antireflect padding applied. Note: Last data point is lost when using array input

smooth(source, series_length, direction, both_period, forward_period, backward_period)

Applies smooth padding by extending with constant derivatives from endpoints

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with smooth padding applied

method smooth(source, direction, both_period, forward_period, backward_period)

Applies smooth padding to an array by extending with constant derivatives from endpoints

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with smooth padding applied. Note: Last data point is lost when using array input

constant(source, series_length, direction, both_period, forward_period, backward_period)

Applies constant padding by extending endpoint values

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with constant padding applied

method constant(source, direction, both_period, forward_period, backward_period)

Applies constant padding to an array by extending endpoint values

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with constant padding applied

zero(source, series_length, direction, both_period, forward_period, backward_period)

Applies zero padding by extending with zeros

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with zero padding applied

method zero(source, direction, both_period, forward_period, backward_period)

Applies zero padding to an array by extending with zeros

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with zero padding applied

pad_data(source, series_length, padding_type, direction, both_period, forward_period, backward_period)

Generic padding function that applies specified padding type to input data

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

padding_type (series PaddingType) : Type of padding to apply (see PaddingType enum)

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with specified padding applied

method pad_data(source, padding_type, direction, both_period, forward_period, backward_period)

Generic padding function that applies specified padding type to array input

Namespace types: array

Parameters:

source (array) : Array of values to pad

padding_type (series PaddingType) : Type of padding to apply (see PaddingType enum)

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with specified padding applied. Note: Last data point is lost when using antireflect or smooth padding types

make_padded_data(source, series_length, padding_type, direction, both_period, forward_period, backward_period)

Creates a window-based padded data series that updates with each new value. WARNING: Function must be called on every bar for consistency. Do not use in scopes where it may not execute on every bar.

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

padding_type (series PaddingType) : Type of padding to apply (see PaddingType enum)

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing windowed data with specified padding applied

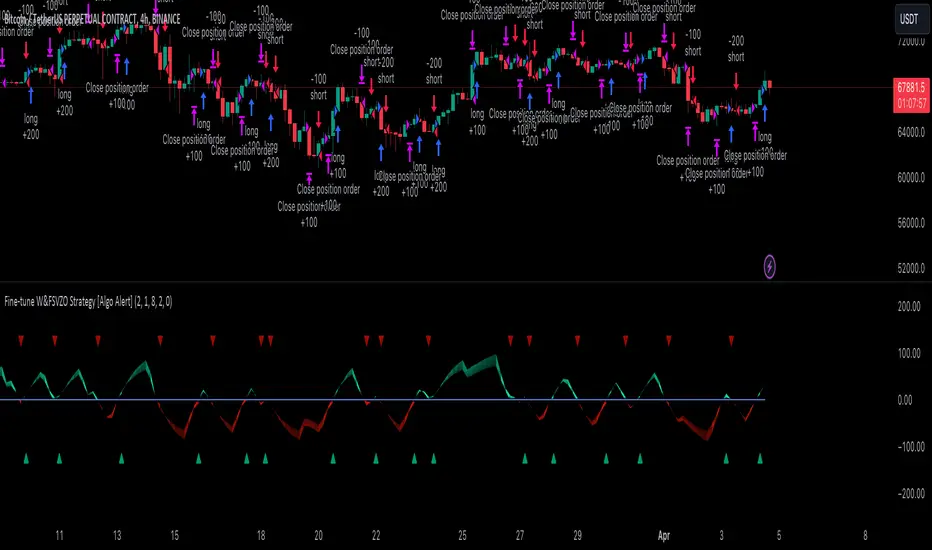

Fine-tune Inputs: Fourier Smoothed Volume zone oscillator WFSVZ0Use this Strategy to Fine-tune inputs for the (W&)FSVZ0 Indicator.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame.

MEANINGFUL DESCRIPTION:

The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Wavelet & Fourier Smoothed Volume Zone Oscillator (W&)FSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the Discrete Fourier Transform . Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Wavalet and Fourier aproximation with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

When I ndicator/Strategy returns 0 or natural trend , Strategy Closes All it's positions.

ORIGINALITY & USFULLNESS:

Personal combination of Fourier and Wavalet aproximation of a price which results in less noise Volume Zone Oscillator.

The Wavelet Transform is a powerful mathematical tool for signal analysis, particularly effective in analyzing signals with varying frequency or non-stationary characteristics. It dissects a signal into wavelets, small waves with varying frequency and limited duration, providing a multi-resolution analysis. This approach captures both frequency and location information, making it especially useful for detecting changes or anomalies in complex signals.

The Discrete Fourier Transform (DFT) is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 and Strategy closes all it's positions when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

In the next Image you can see that trend is negative on 4h, negative on 12h and positive on 1D. That means trend is negative.

I am sorry, the chart is a bit messy. The idea is to use the indicator over more than 1 Timeframe.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Fourier and Wavelet approximation of a close price are taken from aprox library.

Key Features:

You can tailor the Indicator/Strategy to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Fourier Transform (FFT) , the innovative Double Discrete Fourier Transform (DTF32) and Wavelet soothed Fourier soothed price series to suit your analytical needs.

Image of Wavelet transform with FAST settings, Double Fourier transform with FAST settings. Improved noice reduction with SLOW settings, and standard FSVZO with SLOW settings:

Fast setting are setting by default:

VZO length = 2

NoiceR max Length = 2

Slow settings are:

VZO length = 5 or 7

NoiceR max Length = 8

As you can see fast setting are more volatile. I suggest averaging fast setting on 4h 12h 1d 2d 3d 4d W and M Timeframe to get a clear view on market trend.

What if I want long only when VZO is rising and above 15 not 0?

You have set Setting VzoDifference to 15. That reduces the number of trend changes.

Example of W&FSVZO with VzoDifference 15 than 0:

VZO crossed 0 line but not 15 line and that's why Indicator returns 0 in one case an 1 in another.

What is Smooth length setting?

A way of calculating Bullish or Bearish (W&)FSVZO .

If smooth length is 2 the trend is rising if:

rising = VZO > ta.ema(VZO, 2)

Meaning that we check if VZO is higher that exponential average of the last 2 elements.

If smooth length is 1 the trend is rising if:

rising = VZO_ > VZO_

Use this Strategy to fine-tune inputs for the (W&)FSVZO Indicator.

(Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data)

I suggest using " Close all " input False when fine-tuning Inputs for 1 TimeFrame . When you export data to Excel/Numbers/GSheets I suggest using " Close all " input as True , except for the lowest TimeFrame . I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Wavelet & Fourier Smoothed Volume zone oscillator (W&)FSVZO Indicator id:

USER;e7a774913c1242c3b1354334a8ea0f3c

(only relevant to those that use API requests)

MEANINGFUL DESCRIPTION:

The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Wavelet & Fourier Smoothed Volume Zone Oscillator (W&)FSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the Discrete Fourier Transform. Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Wavalet and Fourier aproximation with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in natural trend.

ORIGINALITY & USFULLNESS:

Personal combination of Fourier and Wavalet aproximation of a price which results in less noise Volume Zone Oscillator.

The Wavelet Transform is a powerful mathematical tool for signal analysis, particularly effective in analyzing signals with varying frequency or non-stationary characteristics. It dissects a signal into wavelets, small waves with varying frequency and limited duration, providing a multi-resolution analysis. This approach captures both frequency and location information, making it especially useful for detecting changes or anomalies in complex signals.

The Discrete Fourier Transform (DFT) is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

In the next Image you can see that trend is positive on 4h, neutral on 12h and positive on 1D. That means trend is positive.

I am sorry, the chart is a bit messy. The idea is to use the indicator over more than 1 Timeframe.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Fourier and Wavelet approximation of a close price are taken from aprox library.

Key Features:

You can tailor the indicator to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Fourier Transform (FFT), the innovative Double Discrete Fourier Transform (DTF32) and Wavelet soothed Fourier soothed price series to suit your analytical needs.

Image of Wavelet transform with FAST settings, Double Fourier transform with FAST settings. Improved noice reduction with SLOW settings, and standard FSVZO with SLOW settings:

Fast setting are setting by default:

VZO length = 2

NoiceR max Length = 2

Slow settings are:

VZO length = 5 or 7

NoiceR max Length = 8

As you can see fast setting are more volatile. I suggest averaging fast setting on 4h 12h 1d 2d 3d 4d W and M Timeframe to get a clear view on market trend.

What if I want long only when VZO is rising and above 15 not 0?

You have set Setting VzoDifference to 15. That reduces the number of trend changes.

Example of W&FSVZO with VzoDifference 15 than 0:

VZO crossed 0 line but not 15 line and that's why Indicator returns 0 in one case an 1 in another.

What is Smooth length setting?

A way of calculating Bullish or Bearish FSVZO.

If smooth length is 2 the trend is rising if:

rising = VZO > ta.ema(VZO, 2)

Meaning that we check if VZO is higher that exponential average of the last 2 elements.

If smooth length is 1 the trend is rising if:

rising = VZO_ > VZO_

Rising is boolean value, meaning TRUE if rising and FALSE if falling.

Mathematical equations presented in Pinescript:

Fourier of the real (x axis) discrete:

x_0 = array.get(x, 0) + array.get(x, 1) + array.get(x, 2)

x_1 = array.get(x, 0) + array.get(x, 1) * math.cos( -2 * math.pi * _dir / 3 ) - array.get(y, 1) * math.sin( -2 * math.pi * _dir / 3 ) + array.get(x, 2) * math.cos( -4 * math.pi * _dir / 3 ) - array.get(y, 2) * math.sin( -4 * math.pi * _dir / 3 )

x_2 = array.get(x, 0) + array.get(x, 1) * math.cos( -4 * math.pi * _dir / 3 ) - array.get(y, 1) * math.sin( -4 * math.pi * _dir / 3 ) + array.get(x, 2) * math.cos( -8 * math.pi * _dir / 3 ) - array.get(y, 2) * math.sin( -8 * math.pi * _dir / 3 )

Euler's Noice reduction with both close and Discrete Furrier approximated price.

w = (dft1*src - dft1 *src ) / math.sqrt(math.pow(math.abs(src- src ),2) + math.pow(math.abs(dft1 - dft1 ),2))

filt := na(filt ) ? 0 : c1 * (w*dft1 + nz(w *dft1 )) / 2.0 /math.abs(dft1 -dft1 ) + c2 * nz(filt ) - c3 * nz(filt )

Usecase:

First option:

Select the preferred version of DFT and noise reduction settings based on your analysis requirements.

Leverage the script to identify Bullish and Bearish trends, shown with green and red triangle.

Combine Different Timeframes to accurately determine market trend.

Second option:

Pull the data with API sockets to automate your trading journey.

plot(close, title="ClosePrice", display=display.status_line)

plot(open, title="OpenPrice", display=display.status_line)

plot(greencon ? 1 : redcon ? -1 : 0, title="position", display=display.status_line)

Use ClosePrice, OpenPrice and "position" titles to easily read and backtest your strategy utilising more than 1 Time Frame.

Indicator id:

USER;e7a774913c1242c3b1354334a8ea0f3c

(only relevant to those that use API requests)