ICT Entry V2 [TS_Indie]📌 Description – ICT Entry V2

The market structure, liquidity, FVG, and iFVG mechanisms remain the same as in Version 1.

However, the price action for order entries is different, with the positions of the FVG and iFVG swapped.

Pending orders and stop loss are placed at the iFVG.

⚙️ Core Logic & Working Mechanism

I won’t explain FVG in detail, as most traders are already familiar with it.

Let’s focus on the mechanism of iFVG instead.

The concept of iFVG is based on a supply-to-demand flip and a demand-to-supply flip within an FVG zone.

For an iFVG to be confirmed, the candle close must break through the FVG.

A wick alone does not count as a valid iFVG confirmation.

The confirmation of market structure swings uses a pivot length mechanism combined with price action.

It validates a swing by detecting a structure break formed by candles making new highs or new lows.

📈 Buy Setup

1.Liquidity sweep on the demand side, with price closing above the liquidity level.

2.A demand zone is formed as iFVG and FVG, where FVG is located above iFVG.

3.The gap between the upper box of iFVG and the lower box of FVG must be within the defined Min and Max range.

4.Market Structure must be in a Bullish trend.

5.Place a Pending Order at the upper box of iFVG and set Stop Loss at the lower box of iFVG (Entry and Stop Loss can be adjusted using Entry Zone and ATR-based Stop Loss).

📉 Sell Setup

1.Liquidity sweep on the supply side, with price closing below the liquidity level.

2.A supply zone is formed as iFVG and FVG, where FVG is located below iFVG.

3.The gap between the lower box of iFVG and the upper box of FVG must be within the defined Min and Max range.

4.Market Structure must be in a Bearish trend.

5.Place a Pending Order at the lower box of iFVG and set Stop Loss at the upper box of iFVG (Entry and Stop Loss can be adjusted using Entry Zone and ATR-based Stop Loss).

⚙️ Liquidity Sweep Conditions

➯ When a liquidity sweep occurs on the demand side, the system will start looking for Buy Setup conditions.

➯ When a liquidity sweep occurs on the supply side, the system will immediately switch to looking for Sell Setup conditions.

➯ The system will always prioritize the most recent liquidity sweep and search for setups based on that direction.

➯ The liquidity sweep condition will be invalidated when price closes back below (for demand sweep) or above (for supply sweep) the most recently swept liquidity level.

⭐ Pending Order Cancellation Conditions

A Pending Order will be canceled under the following conditions:

1.A new Price Action signal appears on either the Buy or Sell side.

2.When Time Session is enabled, the Pending Order is canceled once price exits the selected session.

🕹 Order Management Rule

When there is an active open position, the indicator restricts the creation of new Pending Orders to prevent overlapping positions.

⚠️ Disclaimer

This indicator is designed for educational and research purposes only. It does not guarantee profits and should not be considered financial advice. Trading in financial markets involves significant risk, including the potential loss of capital.

🥂 Community Sharing

If you find parameter settings that work well or produce strong statistical results, feel free to share them with the community so we can improve and develop this indicator together.

Strategytesting

Closed Source Strategy TesterAllows you to test an indicator that is closed source (you don't have access to the code). You will need to understand the exposed data elements of the indicator you are testing. This strategy is only looking for a buy, sell, exit long, or exit short to be signals that change from 0 to 1. The stop loss/take profit, if used, are expected to be price values.

I encourage you to copy this code and modify it to your needs for specific indicators.

ICT Entry V1 [TS_Indie]📌 Description – ICT Entry V1

This trading system is based on price action, combined with FVG, iFVG, and liquidity, and it uses the mechanism from the indicator “Smallest Swing ” to validate swings that become liquidity.

⚙️ Core Logic & Working Mechanism

I won’t explain FVG in detail, as most traders are already familiar with it.

Let’s focus on the mechanism of iFVG instead.

The concept of iFVG is based on a supply-to-demand flip and a demand-to-supply flip within an FVG zone.

For an iFVG to be confirmed, the candle close must break through the FVG.

A wick alone does not count as a valid iFVG confirmation.

The confirmation of market structure swings uses a pivot length mechanism combined with price action.

It validates a swing by detecting a structure break formed by candles making new highs or new lows.

📈 Buy Setup

1.Liquidity sweep on the demand side, with price closing above the liquidity level.

2.A demand zone is formed as FVG and iFVG, where iFVG is located above FVG.

3.The gap between the upper box of FVG and the lower box of iFVG must be within the defined Min and Max range.

4.Market Structure must be in a Bullish trend.

5.Place a Pending Order at the upper box of FVG and set Stop Loss at the lower box of FVG (Entry and Stop Loss can be adjusted using Entry Zone and ATR-based Stop Loss).

📉 Sell Setup

1.Liquidity sweep on the supply side, with price closing below the liquidity level.

2.A supply zone is formed as FVG and iFVG, where iFVG is located below FVG.

3.The gap between the lower box of FVG and the upper box of iFVG must be within the defined Min and Max range.

4.Market Structure must be in a Bearish trend.

5.Place a Pending Order at the lower box of FVG and set Stop Loss at the upper box of FVG (Entry and Stop Loss can be adjusted using Entry Zone and ATR-based Stop Loss).

⚙️ Liquidity Sweep Conditions

➯ When a liquidity sweep occurs on the demand side, the system will start looking for Buy Setup conditions.

➯ When a liquidity sweep occurs on the supply side, the system will immediately switch to looking for Sell Setup conditions.

➯ The system will always prioritize the most recent liquidity sweep and search for setups based on that direction.

➯ The liquidity sweep condition will be invalidated when price closes back below (for demand sweep) or above (for supply sweep) the most recently swept liquidity level.

⭐ Pending Order Cancellation Conditions

A Pending Order will be canceled under the following conditions:

1.A new Price Action signal appears on either the Buy or Sell side.

2.When Time Session is enabled, the Pending Order is canceled once price exits the selected session.

🕹 Order Management Rule

When there is an active open position, the indicator restricts the creation of new Pending Orders to prevent overlapping positions.

⚠️ Disclaimer

This indicator is designed for educational and research purposes only. It does not guarantee profits and should not be considered financial advice. Trading in financial markets involves significant risk, including the potential loss of capital.

🥂 Community Sharing

If you find parameter settings that work well or produce strong statistical results, feel free to share them with the community so we can improve and develop this indicator together.

StrategyMatrixLibLibrary "StrategyMatrixLib"

render_matrix(posStr, digits, bgCol, headBg, headTxt, valCol, valTxt)

Renders a strategy performance matrix (table) using strategy.* and strategy.closedtrades.*

Parameters:

posStr (string) : Table anchor position: "Top Left" | "Top Right" | "Bottom Left" | "Bottom Right"

digits (int) : Decimal places for numeric formatting

bgCol (color) : Background color for non-header cells

headBg (color) : Background for header rows

headTxt (color) : Text color for header rows

valCol (color) : Background for value cells

valTxt (color) : Text color for value cells

Returns: table id The created/updated table ID

ParabolicSAR+EMA[TS_Indie]🚀 EMA + Parabolic SAR Reversal Trading Strategy

This trading system effectively combines the use of Exponential Moving Averages (EMA) with the Parabolic SAR to identify both price trends and key reversal points. The EMA Fast is used to signal the primary short-term trend, while the EMA Slow acts as a filter for the long-term trend direction. The Parabolic SAR then helps to confirm the reversal signals.

🛠️ Tools Used

1. EMA Fast – Primary Short-Term Trend

2. EMA Slow – Long-Term Trend Filter

3. Parabolic SAR – Reversal Confirmation

🎯 Entry Rules

📈 Buy Setup

1. Trend Filter: EMA Fast > EMA Slow → Uptrend

2. Pullback: Price pulls back and closes below the EMA Fast line.

3. Reversal: Price reverses/pulls back up and closes above the EMA Fast line.

4. SAR Confirmation: The previous Parabolic SAR dot is above the high, and the dot in the current candle is below the low → Reversal signal confirmed.

5. Entry: Enter Buy immediately.

📉 Sell Setup

1. Trend Filter: EMA Fast < EMA Slow → Downtrend

2. Pullback: Price pulls back and closes above the EMA Fast line.

3. Reversal: Price reverses/pulls back down and closes below the EMA Fast line.

4. SAR Confirmation: The previous Parabolic SAR dot is below the low, and the dot in the current candle is above the high → Reversal signal confirmed.

5. Entry: Enter Sell immediately.

💰 Exit Management (Entry, Stop Loss, Take Profit)

1. Entry: Enter the order at the closing price of the signal candle.

2. Stop Loss (SL): Set the Stop Loss at the Parabolic SAR dot.

3. Take Profit (TP): Calculated from the Entry and Stop Loss points, multiplied by the Risk Reward Ratio.

⚙️ Optional Parameters

➭ Custom Risk/Reward Ratio for Take Profit.

➭ Option to add an ATR buffer to the Stop Loss.

➭ Adjustable EMA Fast period.

➭ Adjustable EMA Slow period.

➭ Adjustable Parabolic SAR parameters.

➭ Option to enable Long-only / Short-only positions.

➭ Customizable Backtest start and end date.

➭ Customizable trading session time.

🔔 Alert Function

Alerts display:

➭ Entry Price

➭ Stop Loss Price

➭ Take Profit Price

💡 This strategy allows for many parameter adjustments, such as the MA type, adding/subtracting from the Stop Loss using ATR, and selecting specific sessions for backtesting. If you find interesting or profitable results after adjusting the parameters, please share your comments with other traders!

⚠️ Disclaimer

This indicator is designed for educational and research purposes only. It does not guarantee profits and should not be considered financial advice. Trading in financial markets involves significant risk , including the potential loss of capital.

Quasimodo Pattern Strategy Back Test [TradingFinder] QM Trading🔵 Introduction

The QM pattern, also known as the Quasimodo pattern, is one of the popular patterns in price action, and it is often used by technical analysts. The QM pattern is used to identify trend reversals and provides a very good risk-to-reward ratio. One of the advantages of the QM pattern is its high frequency and visibility in charts.

Additionally, due to its strength, it is highly profitable, and as mentioned, its risk-to-reward ratio is very good. The QM pattern is highly popular among traders in supply and demand, and traders also use this pattern.

The Price Action QM pattern, like other Price Action patterns, has two types: Bullish QM and Bearish QM patterns. To identify this pattern, you need to be familiar with its types to recognize it.

🔵 Identifying the QM Pattern

🟣 Bullish QM

In the bullish QM pattern, as you can see in the image below, an LL and HH are formed. As you can see, the neckline is marked as a dashed line. When the price reaches this range, it will start its upward movement.

🟣 Bearish QM

The Price Action QM pattern also has a bearish pattern. As you can see in the image below, initially, an HH and LL are formed. The neckline in this image is the dashed line, and when the LL is formed, the price reaches this neckline. However, it cannot pass it, and the downward trend resumes.

🔵 How to Use

The Quasimodo pattern is one of the clearest structures used to identify market reversals. It is built around the concept of a structural break followed by a pullback into an area of trapped liquidity. Instead of relying on lagging indicators, this pattern focuses purely on price action and how the market reacts after exhausting one side of liquidity. When understood correctly, it provides traders with precise entry points at the transition between trend phases.

🟣 Bullish Quasimodo

A bullish Quasimodo forms after a clear downtrend when sellers start losing control. The market continues to make lower lows until a sudden higher high appears, signaling that buyers are entering with strength. Price then pulls back to retest the previous low, creating what is known as the Quasimodo low.

This area often becomes the final trap for sellers before the market shifts upward. A visible rejection or displacement from this zone confirms bullish momentum. Traders usually place entries near this level, stops below the low, and targets at previous highs or the next resistance zone. Combining the setup with demand zones or Fair Value Gaps increases its accuracy.

🟣 Bearish Quasimodo

A bearish Quasimodo forms near the top of an uptrend when buyers begin to lose strength. The market continues to make higher highs until a sudden lower low breaks the bullish structure, showing that selling pressure is entering the market. Price then retraces upward to retest the previous high, forming the Quasimodo high, where breakout buyers are often trapped.

Once rejection appears at this level, it indicates a likely reversal. Traders can enter short near this area, with stop-losses placed above the high and targets near the next support or previous lows. The setup gains more reliability when aligned with supply zones, SMT divergence, or bearish Fair Value Gaps.

🔵 Setting

Pivot Period : You can use this parameter to use your desired period to identify the QM pattern. By default, this parameter is set to the number 5.

Take Profit Mode : You can choose your desired Take Profit in three ways. Based on the logic of the QM strategy, you can select two Take Profit levels, TP1 and TP2. You can also choose your take profit based on the Reward to Risk ratio. You must enter your desired R/R in the Reward to Risk Ratio parameter.

Stop Loss Refine : The loss limit of the QM strategy is based on its logic on the Head pattern. You can refine it using the ATR Refine option to prevent Stop Hunt. You can enter your desired coefficient in the Stop Loss ATR Adjustment Coefficient parameter.

Reward to Risk Ratio : If you set Take Profit Mode to R/R, you must enter your desired R/R here. For example, if your loss limit is 10 pips and you set R/R to 2, your take profit will be reached when the price is 20 pips away from your entry point.

Stop Loss ATR Adjustment Coefficient : If you set Stop Loss Refine to ATR Refine, you must adjust your loss limit coefficient here. For example, if your buy position's loss limit is at the price of 1000, and your ATR is 10, if you set Stop Loss ATR Adjustment Coefficient to 2, your loss limit will be at the price of 980.

Entry Level Validity : Determines how long the Entry level remains valid. The higher the level, the longer the entry level will remain valid. By default it is 2 and it can be set between 2 and 15.

🔵 Results

The following examples show the backtest results of the Quasimodo (QM) strategy in action. Each image is based on specific settings for the symbol, timeframe, and input parameters, illustrating how the QM logic can generate signals under different market conditions. The detailed configuration for each backtest is also displayed on the image.

⚠ Important Note : Even with identical settings and the same symbol, results may vary slightly across different brokers due to data feed variations and pricing differences.

Default Properties of Backtests :

OANDA:XAUUSD | TimeFrame: 5min | Duration: 1 Year :

BINANCE:BTCUSD | TimeFrame: 5min | Duration: 1 Year :

CAPITALCOM:US30 | TimeFrame: 5min | Duration: 1 Year :

NASDAQ:QQQ | TimeFrame: 5min | Duration: 5 Year :

OANDA:EURUSD | TimeFrame: 5min | Duration: 5 Year :

PEPPERSTONE:US500 | TimeFrame: 5min | Duration: 5 Year :

W%R Pullback+EMA Trend [TS_Indie]🔰 Core Concept of the Strategy

The main idea is “Trend-Following with Momentum Pullback.”

This means trading in the direction of the main trend (defined by EMA) while using Williams %R to identify pullback entries (buying the dip or selling the rally) where momentum returns to the trend direction.

📊 Indicators Used

1. EMA Fast – Defines the short-term trend.

2. EMA Slow – Defines the long-term trend (used as a trend filter).

3. Williams %R

• Overbought zone: above -20

• Oversold zone: below -80

⚙️ Entry Rules

🔹 Buy Setup

1. EMA Fast > EMA Slow → Uptrend condition.

2. Williams %R on the previous candle dropped below -80, and on the current candle, it crosses back above -80 → indicates momentum returning to the upside.

3. Current close is above EMA Fast.

4. Entry Buy at the close of the candle where %R crosses above -80.

🎯 Entry, Stop Loss, and Take Profit

1. Entry : At the candle close where the signal occurs.

2. Stop Loss : At the lowest low between the current and previous candles.

3. Take Profit : Calculated based on entry price and stop loss distance multiplied by the Risk/Reward Ratio.

🔹 Sell Setup

1. EMA Fast < EMA Slow → Downtrend condition.

2. Williams %R on the previous candle went above -20, and on the current candle, it crosses back below -20 → indicates renewed selling momentum.

3. Current price is below EMA Fast.

4. Entry Sell at the close of the candle where %R crosses below -20.

🎯 Entry, Stop Loss, and Take Profit

1. Entry : At the candle close where the signal occurs.

2. Stop Loss : At the highest high between the current and previous candles.

3. Take Profit : Calculated based on entry price and stop loss distance multiplied by the Risk/Reward Ratio.

⚙️ Optional Parameters

• Custom Risk/Reward Ratio for Take Profit.

• Option to add ATR buffer to Stop Loss.

• Adjustable EMA Fast period.

• Adjustable EMA Slow period.

• Adjustable Williams %R period.

• Option to enable Long only / Short only positions.

• Customizable Backtest start and end date.

• Customizable trading session time.

⏰ Alert Function

Alerts display:

• Entry price

• Stop Loss price

• Take Profit price

Guys, try adjusting the parameters yourselves!

I’ve been tweaking the settings for several days and managed to get great results on XAU/USD in the 5-minute timeframe.

I think this strategy is quite interesting and could potentially deliver good results on other instruments as well.

⚠️ Disclaimer

This indicator is designed for educational and research purposes only.

It does not guarantee profits and should not be considered financial advice.

Trading in financial markets involves significant risk, including the potential loss of capital.

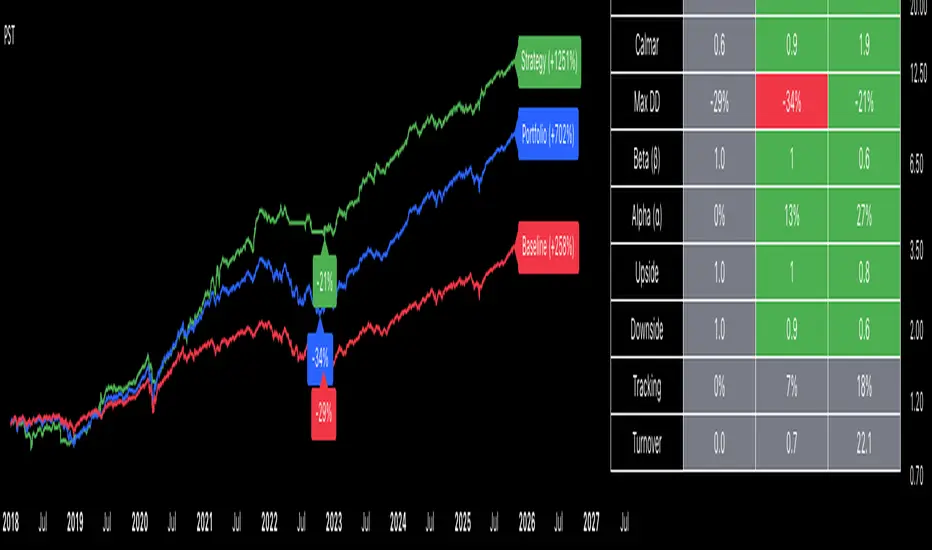

Portfolio Strategy TesterThe Portfolio Strategy Tester is an institutional-grade backtesting framework that evaluates the performance of trend-following strategies on multi-asset portfolios. It enables users to construct custom portfolios of up to 30 assets and apply moving average crossover strategies across individual holdings. The model features a clear, color-coded table that provides a side-by-side comparison between the buy-and-hold portfolio and the portfolio using the risk management strategy, offering a comprehensive assessment of both approaches relative to the benchmark.

Portfolios are constructed by entering each ticker symbol in the menu, assigning its respective weight, and reviewing the total sum of individual weights displayed at the top left of the table. For strategy selection, users can choose between Exponential Moving Average (EMA), Simple Moving Average (SMA), Wilder’s Moving Average (RMA), Weighted Moving Average (WMA), Moving Average Convergence Divergence (MACD), and Volume-Weighted Moving Average (VWMA). Moving average lengths are defined in the menu and apply only to strategy-enabled assets.

To accurately replicate real-world portfolio conditions, users can choose between daily, weekly, monthly, or quarterly rebalancing frequencies and decide whether cash is held or redistributed. Daily rebalancing maintains constant portfolio weights, while longer intervals allow natural drift. When cash positions are not allowed, capital from bearish assets is automatically redistributed proportionally among bullish assets, ensuring the portfolio remains fully invested at all times. The table displays a comprehensive set of widely used institutional-grade performance metrics:

CAGR = Compounded annual growth rate of returns.

Volatility = Annualized standard deviation of returns.

Sharpe = CAGR per unit of annualized standard deviation.

Sortino = CAGR per unit of annualized downside deviation.

Calmar = CAGR relative to maximum drawdown.

Max DD = Largest peak-to-trough decline in value.

Beta (β) = Sensitivity of returns relative to benchmark returns.

Alpha (α) = Excess annualized risk-adjusted returns relative to benchmark.

Upside = Ratio of average return to benchmark return on up days.

Downside = Ratio of average return to benchmark return on down days.

Tracking = Annualized standard deviation of returns versus benchmark.

Turnover = Average sum of absolute changes in weights per year.

Cumulative returns are displayed on each label as the total percentage gain from the selected start date, with green indicating positive returns and red indicating negative returns. In the table, baseline metrics serve as the benchmark reference and are always gray. For portfolio metrics, green indicates outperformance relative to the baseline, while red indicates underperformance relative to the baseline. For strategy metrics, green indicates outperformance relative to both the baseline and the portfolio, red indicates underperformance relative to both, and gray indicates underperformance relative to either the baseline or portfolio. Metrics such as Volatility, Tracking Error, and Turnover ratio are always displayed in gray as they serve as descriptive measures.

In summary, the Portfolio Strategy Tester is a comprehensive backtesting tool designed to help investors evaluate different trend-following strategies on custom portfolios. It enables real-world simulation of both active and passive investment approaches and provides a full set of standard institutional-grade performance metrics to support data-driven comparisons. While results are based on historical performance, the model serves as a powerful portfolio management and research framework for developing, validating, and refining systematic investment strategies.

The Best Strategy Template[LuciTech]Hello Traders,

This is a powerful and flexible strategy template designed to help you create, backtest, and deploy your own custom trading strategies. This template is not a ready-to-use strategy but a framework that simplifies the development process by providing a wide range of pre-built features and functionalities.

What It Does

The LuciTech Strategy Template provides a robust foundation for building your own automated trading strategies. It includes a comprehensive set of features that are essential for any serious trading strategy, allowing you to focus on your unique trading logic without having to code everything from scratch.

Key Features

The LuciTech Strategy Template integrates several powerful features to enhance your strategy development:

•

Advanced Risk Management: This includes robust controls for defining your Risk Percentage per Trade, setting a precise Risk-to-Reward Ratio, and implementing an intelligent Breakeven Stop-Loss mechanism that automatically adjusts your stop to the entry price once a specified profit threshold is reached. These elements are crucial for capital preservation and consistent profitability.

•

Flexible Stop-Loss Options: The template offers adaptable stop-loss calculation methods, allowing you to choose between ATR-Based Stop-Loss, which dynamically adjusts to market volatility, and Candle-Based Stop-Loss, which uses structural price points from previous candles. This flexibility ensures the stop-loss strategy aligns with diverse trading styles.

•

Time-Based Filtering: Optimize your strategy's performance by restricting trading activity to specific hours of the day. This feature allows you to avoid unfavorable market conditions or focus on periods of higher liquidity and volatility relevant to your strategy.

•

Customizable Webhook Alerts: Stay informed with advanced notification capabilities. The template supports sending detailed webhook alerts in various JSON formats (Standard, Telegram, Concise Telegram) to external platforms, facilitating real-time monitoring and potential integration with automated trading systems.

•

Comprehensive Visual Customization: Enhance your analytical clarity with extensive visual options. You can customize the colors of entry, stop-loss, and take-profit lines, and effectively visualize market inefficiencies by displaying and customizing Fair Value Gap (FVG) boxes directly on your chart.

How It Does It

The LuciTech Strategy Template is meticulously crafted using Pine Script, TradingView's powerful and expressive programming language. The underlying architecture is designed for clarity and modularity, allowing for straightforward integration of your unique trading signals. At its core, the template operates by taking user-defined entry and exit conditions and then applying a sophisticated layer of risk management, position sizing, and trade execution logic.

For instance, when a longCondition or shortCondition is met, the template dynamically calculates the appropriate position size. This calculation is based on your specified risk_percent of equity and the stop_distance (the distance between your entry price and the calculated stop-loss level). This ensures that each trade adheres to your predefined risk parameters, a critical component of disciplined trading.

The flexibility in stop-loss calculation is achieved through a switch statement that evaluates the sl_type input. Whether you choose an ATR-based stop, which adapts to market volatility, or a candle-based stop, which uses structural price points, the template seamlessly integrates these methods. The ATR calculation itself is further refined by allowing various smoothing methods (RMA, SMA, EMA, WMA), providing granular control over how volatility is measured.

Time-based filtering is implemented by comparing the current bar's time with user-defined start_hour, start_minute, end_hour, and end_minute inputs. This allows the strategy to activate or deactivate trading during specific market sessions or periods of the day, a valuable tool for optimizing performance and avoiding unfavorable conditions.

Furthermore, the template incorporates advanced webhook alert functionality. When a trade is executed, a customizable JSON message is formatted based on your webhook_format selection (Standard, Telegram, or Concise Telegram) and sent via alert function. This enables seamless integration with external services for real-time notifications or even automated trade execution through third-party platforms.

Visual feedback is paramount for understanding strategy behavior. The template utilizes plot and fill functions to clearly display entry prices, stop-loss levels, and take-profit targets directly on the chart. Customizable colors for these elements, along with dedicated options for Fair Value Gap (FVG) boxes, enhance the visual analysis during backtesting and live trading, making it easier to interpret the strategy's actions.

How It's Original

The LuciTech Strategy Template distinguishes itself in the crowded landscape of TradingView scripts through its unique combination of integrated, advanced risk management features, highly flexible stop-loss methodologies, and sophisticated alerting capabilities, all within a user-friendly and modular framework. While many templates offer basic entry/exit signal integration, LuciTech goes several steps further by providing a robust, ready-to-use infrastructure for managing the entire trade lifecycle once a signal is generated.

Unlike templates that might require users to piece together various risk management components or code complex stop-loss logic from scratch, LuciTech offers these critical functionalities out-of-the-box. The inclusion of dynamic position sizing based on a user-defined risk percentage, a configurable risk-to-reward ratio, and an intelligent breakeven mechanism significantly elevates its utility. This comprehensive approach to capital preservation and profit targeting is a cornerstone of professional trading and is often overlooked or simplified in generic templates.

Furthermore, the template's provision for multiple stop-loss calculation types—ATR-based for volatility adaptation, and candle-based for structural support/resistance—demonstrates a deep understanding of diverse trading strategies. The underlying code for these calculations is already implemented, saving developers considerable time and effort. The subtle yet powerful inclusion of FVG (Fair Value Gap) related inputs also hints at advanced price action concepts, offering a sophisticated layer of analysis and execution that is not commonly found in general-purpose templates.

The advanced webhook alerting system, with its support for various JSON formats tailored for platforms like Telegram, showcases an originality in catering to the needs of modern, automated trading setups. This moves beyond simple TradingView pop-up alerts, enabling seamless integration with external systems for real-time trade monitoring and execution. This level of external connectivity and customizable data output is a significant differentiator.

In essence, the LuciTech Strategy Template is original not just in its individual features, but in how these features are cohesively integrated to form a powerful, opinionated, yet highly adaptable system. It empowers traders to focus their creative energy on developing their core entry/exit signals, confident that the underlying framework will handle the complexities of risk management, trade execution, and external communication with precision and flexibility. It's a comprehensive solution designed to accelerate the development of robust and professional trading strategies.

How to Modify the Logic to Apply Your Strategy

The LuciTech Strategy Template is designed with modularity in mind, making it exceptionally straightforward to integrate your unique trading strategy logic. The template provides a clear separation between the core strategy management (risk, position sizing, exits) and the entry signal generation. This allows you to easily plug in your own buy and sell conditions without altering the robust underlying framework.

Here’s a step-by-step guide on how to adapt the template to your specific trading strategy:

1.

Locate the Strategy Logic Section:

Open the Pine Script editor in TradingView and navigate to the section clearly marked with the comment //Strategy Logic Example:. This is where the template’s placeholder entry conditions (a simple moving average crossover) are defined.

2.

Define Your Custom Entry Conditions:

Within this section, you will find variables such as longCondition and shortCondition. These are boolean variables that determine when a long or short trade should be initiated. Replace the existing example logic with your own custom buy and sell conditions. Your conditions can be based on any combination of indicators, price action patterns, candlestick formations, or other market analysis techniques. For example, if your strategy involves a combination of RSI and MACD, you would define longCondition as (rsi > 50 and macd_line > signal_line) and shortCondition as (rsi < 50 and macd_line < signal_line).

3.

Leverage the Template’s Built-in Features:

Once your longCondition and shortCondition are defined, the rest of the template automatically takes over. The integrated risk management module will calculate the appropriate position size based on your Risk % input and the chosen Stop Loss Type. The Risk:Reward ratio will determine your take-profit levels, and the Breakeven at R feature will manage your stop-loss dynamically. The time filter (Use Time Filter) will ensure your trades only occur within your specified hours, and the webhook alerts will notify you of trade executions.

is_strategyCorrection-Adaptive Trend Strategy (Open-Source)

Core Advantage: Designed specifically for the is_correction indicator, with full transparency and customization options.

Key Features:

Open-Source Code:

✅ Full access to the strategy logic – study how every trade signal is generated.

✅ Freedom to customize – modify entry/exit rules, risk parameters, or add new indicators.

✅ No black boxes – understand and trust every decision the strategy makes.

Built for is_correction:

Filters out false signals during market noise.

Works only in confirmed trends (is_correction = false).

Adaptable for Your Needs:

Change Take Profit/Stop Loss ratios directly in the code.

Add alerts, notifications, or integrate with other tools (e.g., Volume Profile).

For Developers/Traders:

Use the code as a template for your own strategies.

Test modifications risk-free on historical data.

How the Strategy Works:

Main Goal:

Automatically buys when the price starts rising and sells when it starts falling, but only during confirmed trends (ignoring temporary pullbacks).

What You See on the Chart:

📈 Up arrows ▼ (below the candle) = Buy signal.

📉 Down arrows ▲ (above the candle) = Sell signal.

Gray background = Market is in a correction (no trades).

Key Mechanics:

Buy Condition:

Price closes higher than the previous candle + is_correction confirms the main trend (not a pullback).

Example: Red candle → green candle → ▼ arrow → buy.

Sell Condition:

Price closes lower than the previous candle + is_correction confirms the trend (optional: turn off short-selling in settings).

Exit Rules:

Closes trades automatically at:

+0.5% profit (adjustable in settings).

-0.5% loss (adjustable).

Or if a reverse signal appears (e.g., sell signal after a buy).

User-Friendly Settings:

Sell – On (default: ON):

ON → Allows short-selling (selling when price falls).

OFF → Strategy only buys and closes positions.

Revers (default: OFF):

ON → Inverts signals (▼ = sell, ▲ = buy).

%Profit & %Loss:

Adjust these values (0-30%) to increase/decrease profit targets and risk.

Example Scenario:

Buy Signal:

Price rises for 3 days → green ▼ arrow → strategy buys.

Stop loss set 0.5% below entry price.

If price keeps rising → trade closes at +0.5% profit.

Correction Phase:

After a rally, price drops for 1 day → gray background → strategy ignores the drop (no action).

Stop Loss Trigger:

If price drops 0.5% from entry → trade closes automatically.

Key Features:

Correction Filter (is_correction):

Acts as a “noise filter” → avoids trades during temporary pullbacks.

Flexibility:

Disable short-selling, flip signals, or tweak profit/loss levels in seconds.

Transparency:

Open-source code → see exactly how every signal is generated (click “Source” in TradingView).

Tips for Beginners:

Test First:

Run the strategy on historical data (click the “Chart” icon in TradingView).

See how it performed in the past.

Customize It:

Increase %Profit to 2-3% for volatile assets like crypto.

Turn off Sell – On if short-selling confuses you.

Trust the Stop Loss:

Even if you think the price will rebound, the strategy will close at -0.5% to protect your capital.

Where to Find Settings:

Click the strategy name on the top-left of your chart → adjust sliders/toggles in the menu.

Русская Версия

Трендовая стратегия с открытым кодом

Главное преимущество: Полная прозрачность логики и адаптация под ваши нужды.

Особенности:

Открытый исходный код:

✅ Видите всю «кухню» стратегии – как формируются сигналы, когда открываются сделки.

✅ Меняйте правила – корректируйте тейк-профит, стоп-лосс или добавляйте новые условия.

✅ Никаких секретов – вы контролируете каждое правило.

Заточка под is_correction:

Игнорирует ложные сигналы в коррекциях.

Работает только в сильных трендах (is_correction = false).

Гибкая настройка:

Подстройте параметры под свой риск-менеджмент.

Добавьте свои индикаторы или условия для входа.

Для трейдеров и разработчиков:

Используйте код как основу для своих стратегий.

Тестируйте изменения на истории перед реальной торговлей.

Простыми словами:

Почему это удобно:

Открытый код = полный контроль. Вы можете:

Увидеть, как именно стратегия решает купить или продать.

Изменить правила закрытия сделок (например, поставить TP=2% вместо 1.5%).

Добавить новые условия (например, торговать только при высоком объёме).

Примеры кастомизации:

Новички: Меняйте только TP/SL в настройках (без кодинга).

Продвинутые: Добавьте RSI-фильтр, чтобы избегать перекупленности.

Разработчики: Встройте стратегию в свою торговую систему.

Как начать:

Скачайте код из TradingView.

Изучите логику в разделе strategy.entry/exit.

Меняйте параметры в блоке input.* (безопасно!).

Тестируйте изменения и оптимизируйте под свои цели.

Как работает стратегия:

Главная задача:

Автоматически покупает, когда цена начинает расти, и продаёт, когда падает. Но делает это «умно» — только когда рынок в основном тренде, а не во временном откате (коррекции).

Что видно на графике:

📈 Стрелки вверх ▼ (под свечой) — сигнал на покупку.

📉 Стрелки вниз ▲ (над свечой) — сигнал на продажу.

Серый фон — рынок в коррекции (не торгуем).

Как это работает:

Когда покупаем:

Если цена закрылась выше предыдущей и индикатор is_correction показывает «основной тренд» (не коррекция).

Пример: Была красная свеча → стала зелёная → появилась стрелка ▼ → покупаем.

Когда продаём:

Если цена закрылась ниже предыдущей и is_correction подтверждает тренд (опционально, можно отключить в настройках).

Когда закрываем сделку:

Автоматически при достижении:

+0.5% прибыли (можно изменить в настройках).

-0.5% убытка (можно изменить).

Или если появился противоположный сигнал (например, после покупки пришла стрелка продажи).

Настройки для чайников:

«Sell – On» (включено по умолчанию):

Если включено → стратегия будет продавать в шорт.

Если выключено → только покупки и закрытие позиций.

«Revers» (выключено по умолчанию):

Если включить → стратегия будет работать наоборот (стрелки ▼ = продажа, ▲ = покупка).

«%Profit» и «%Loss»:

Меняйте эти цифры (от 0 до 30), чтобы увеличить/уменьшить прибыль и риски.

Пример работы:

Сигнал на покупку:

Цена 3 дня растет → появляется зелёная стрелка ▼ → стратегия покупает.

Стоп-лосс ставится на 0.5% ниже цены входа.

Если цена продолжает расти → сделка закрывается при +0.5% прибыли.

Коррекция:

После роста цена падает на 1 день → фон становится серым → стратегия игнорирует это падение (не закрывает сделку).

Стоп-лосс:

Если цена упала на 0.5% от точки входа → сделка закрывается автоматически.

Важные особенности:

Фильтр коррекций (is_correction):

Это «защита от шума» — стратегия не реагирует на мелкие откаты, работая только в сильных трендах.

Гибкие настройки:

Можно запретить шорты, перевернуть сигналы или изменить уровни прибыли/убытка за 2 клика.

Прозрачность:

Весь код открыт → вы можете увидеть, как формируется каждый сигнал (меню «Исходник» в TradingView).

Советы для новичков:

Начните с теста:

Запустите стратегию на исторических данных (кнопка «Свеча» в окне TradingView).

Посмотрите, как она работала в прошлом.

Настройте под себя:

Увеличьте %Profit до 2-3%, если торгуете валюты.

Отключите «Sell – On», если не понимаете шорты.

Доверяйте стоп-лоссу:

Даже если кажется, что цена развернётся — стратегия закроет сделку при -0.5%, защитив ваш депозит.

Где найти настройки:

Кликните на название стратегии в верхнем левом углу графика → откроется меню с ползунками и переключателями.

Важно: Стратегия предоставляет «рыбу» – чтобы она стала «уловистой», адаптируйте её под свой стиль торговли!

Ensemble Alerts█ OVERVIEW

This indicator creates highly customizable alert conditions and messages by combining several technical conditions into groups , which users can specify directly from the "Settings/Inputs" tab. It offers a flexible framework for building and testing complex alert conditions without requiring code modifications for each adjustment.

█ CONCEPTS

Ensemble analysis

Ensemble analysis is a form of data analysis that combines several "weaker" models to produce a potentially more robust model. In a trading context, one of the most prevalent forms of ensemble analysis is the aggregation (grouping) of several indicators to derive market insights and reinforce trading decisions. With this analysis, traders typically inspect multiple indicators, signaling trade actions when specific conditions or groups of conditions align.

Simplifying ensemble creation

Combining indicators into one or more ensembles can be challenging, especially for users without programming knowledge. It usually involves writing custom scripts to aggregate the indicators and trigger trading alerts based on the confluence of specific conditions. Making such scripts customizable via inputs poses an additional challenge, as it often involves complicated input menus and conditional logic.

This indicator addresses these challenges by providing a simple, flexible input menu where users can easily define alert criteria by listing groups of conditions from various technical indicators in simple text boxes . With this script, you can create complex alert conditions intuitively from the "Settings/Inputs" tab without ever writing or modifying a single line of code. This framework makes advanced alert setups more accessible to non-coders. Additionally, it can help Pine programmers save time and effort when testing various condition combinations.

█ FEATURES

Configurable alert direction

The "Direction" dropdown at the top of the "Settings/Inputs" tab specifies the allowed direction for the alert conditions. There are four possible options:

• Up only : The indicator only evaluates upward conditions.

• Down only : The indicator only evaluates downward conditions.

• Up and down (default): The indicator evaluates upward and downward conditions, creating alert triggers for both.

• Alternating : The indicator prevents alert triggers for consecutive conditions in the same direction. An upward condition must be the first occurrence after a downward condition to trigger an alert, and vice versa for downward conditions.

Flexible condition groups

This script features six text inputs where users can define distinct condition groups (ensembles) for their alerts. An alert trigger occurs if all the conditions in at least one group occur.

Each input accepts a comma-separated list of numbers with optional spaces (e.g., "1, 4, 8"). Each listed number, from 1 to 35, corresponds to a specific individual condition. Below are the conditions that the numbers represent:

1 — RSI above/below threshold

2 — RSI below/above threshold

3 — Stoch above/below threshold

4 — Stoch below/above threshold

5 — Stoch K over/under D

6 — Stoch K under/over D

7 — AO above/below threshold

8 — AO below/above threshold

9 — AO rising/falling

10 — AO falling/rising

11 — Supertrend up/down

12 — Supertrend down/up

13 — Close above/below MA

14 — Close below/above MA

15 — Close above/below open

16 — Close below/above open

17 — Close increase/decrease

18 — Close decrease/increase

19 — Close near Donchian top/bottom (Close > (Mid + HH) / 2)

20 — Close near Donchian bottom/top (Close < (Mid + LL) / 2)

21 — New Donchian high/low

22 — New Donchian low/high

23 — Rising volume

24 — Falling volume

25 — Volume above average (Volume > SMA(Volume, 20))

26 — Volume below average (Volume < SMA(Volume, 20))

27 — High body to range ratio (Abs(Close - Open) / (High - Low) > 0.5)

28 — Low body to range ratio (Abs(Close - Open) / (High - Low) < 0.5)

29 — High relative volatility (ATR(7) > ATR(40))

30 — Low relative volatility (ATR(7) < ATR(40))

31 — External condition 1

32 — External condition 2

33 — External condition 3

34 — External condition 4

35 — External condition 5

These constituent conditions fall into three distinct categories:

• Directional pairs : The numbers 1-22 correspond to pairs of opposing upward and downward conditions. For example, if one of the inputs includes "1" in the comma-separated list, that group uses the "RSI above/below threshold" condition pair. In this case, the RSI must be above a high threshold for the group to trigger an upward alert, and the RSI must be below a defined low threshold to trigger a downward alert.

• Non-directional filters : The numbers 23-30 correspond to conditions that do not represent directional information. These conditions act as filters for both upward and downward alerts. Traders often use non-directional conditions to refine trending or mean reversion signals. For instance, if one of the input lists includes "30", that group uses the "Low relative volatility" condition. The group can trigger an upward or downward alert only if the 7-period Average True Range (ATR) is below the 40-period ATR.

• External conditions : The numbers 31-35 correspond to external conditions based on the plots from other indicators on the chart. To set these conditions, use the source inputs in the "External conditions" section near the bottom of the "Settings/Inputs" tab. The external value can represent an upward, downward, or non-directional condition based on the following logic:

▫ Any value above 0 represents an upward condition.

▫ Any value below 0 represents a downward condition.

▫ If the checkbox next to the source input is selected, the condition becomes non-directional . Any group that uses the condition can trigger upward or downward alerts only if the source value is not 0.

To learn more about using plotted values from other indicators, see this article in our Help Center and the Source input section of our Pine Script™ User Manual.

Group markers

Each comma-separated list represents a distinct group , where all the listed conditions must occur to trigger an alert. This script assigns preset markers (names) to each condition group to make the active ensembles easily identifiable in the generated alert messages and labels. The markers assigned to each group use the format "M", where "M" is short for "Marker" and "x" is the group number. The titles of the inputs at the top of the "Settings/Inputs" tab show these markers for convenience.

For upward conditions, the labels and alert messages show group markers with upward triangles (e.g., "M1▲"). For downward conditions, they show markers with downward triangles (e.g., "M1▼").

NOTE: By default, this script populates the "M1" field with a pre-configured list for a mean reversion group ("2,18,24,28"). The other fields are empty. If any "M*" input does not contain a value, the indicator ignores it in the alert calculations.

Custom alert messages

By default, the indicator's alert message text contains the activated markers and their direction as a comma-separated list. Users can override this message for upward or downward alerts with the two text fields at the bottom of the "Settings/Inputs" tab. When the fields are not empty , the alerts use that text instead of the default marker list.

NOTE: This script generates alert triggers, not the alerts themselves. To set up an alert based on this script's conditions, open the "Create Alert" dialog box, then select the "Ensemble Alerts" and "Any alert() function call" options in the "Condition" tabs. See the Alerts FAQ in our Pine Script™ User Manual for more information.

Condition visualization

This script offers organized visualizations of its conditions, allowing users to inspect the behaviors of each condition alongside the specified groups. The key visual features include:

1) Conditional plots

• The indicator plots the history of each individual condition, excluding the external conditions, as circles at different levels. Opposite conditions appear at positive and negative levels with the same absolute value. The plots for each condition show values only on the bars where they occur.

• Each condition's plot is color-coded based on its type. Aqua and orange plots represent opposing directional conditions, and purple plots represent non-directional conditions. The titles of the plots also contain the condition numbers to which they apply.

• The plots in the separate pane can be turned on or off with the "Show plots in pane" checkbox near the top of the "Settings/Inputs" tab. This input only toggles the color-coded circles, which reduces the graphical load. If you deactivate these visuals, you can still inspect each condition from the script's status line and the Data Window.

• As a bonus, the indicator includes "Up alert" and "Down alert" plots in the Data Window, representing the combined upward and downward ensemble alert conditions. These plots are also usable in additional indicator-on-indicator calculations.

2) Dynamic labels

• The indicator draws a label on the main chart pane displaying the activated group markers (e.g., "M1▲") each time an alert condition occurs.

• The labels for upward alerts appear below chart bars. The labels for downward alerts appear above the bars.

NOTE: This indicator can display up to 500 labels because that is the maximum allowed for a single Pine script.

3) Background highlighting

• The indicator can highlight the main chart's background on bars where upward or downward condition groups activate. Use the "Highlight background" inputs in the "Settings/Inputs" tab to enable these highlights and customize their colors.

• Unlike the dynamic labels, these background highlights are available for all chart bars, irrespective of the number of condition occurrences.

█ NOTES

• This script uses Pine Script™ v6, the latest version of TradingView's programming language. See the Release notes and Migration guide to learn what's new in v6 and how to convert your scripts to this version.

• This script imports our new Alerts library, which features functions that provide high-level simplicity for working with complex compound conditions and alerts. We used the library's `compoundAlertMessage()` function in this indicator. It evaluates items from "bool" arrays in groups specified by an array of strings containing comma-separated index lists , returning a tuple of "string" values containing the marker of each activated group.

• The script imports the latest version of the ta library to calculate several technical indicators not included in the built-in `ta.*` namespace, including Double Exponential Moving Average (DEMA), Triple Exponential Moving Average (TEMA), Fractal Adaptive Moving Average (FRAMA), Tilson T3, Awesome Oscillator (AO), Full Stochastic (%K and %D), SuperTrend, and Donchian Channels.

• The script uses the `force_overlay` parameter in the label.new() and bgcolor() calls to display the drawings and background colors in the main chart pane.

• The plots and hlines use the available `display.*` constants to determine whether the visuals appear in the separate pane.

Look first. Then leap.

Gold Friday Anomaly StrategyThis script implements the " Gold Friday Anomaly Strategy ," a well-known historical trading strategy that leverages the gold market's behavior from Thursday evening to Friday close. It is a backtesting-focused strategy designed to assess the historical performance of this pattern. Traders use this anomaly as it captures a recurring market tendency observed over the years.

What It Does:

Entry Condition: The strategy enters a long position at the beginning of the Friday trading session (Thursday evening close) within the defined backtesting period.

Exit Condition: Friday evening close.

Backtesting Controls: Allows users to set custom backtesting periods to evaluate strategy performance over specific date ranges.

Key Features:

Custom Backtest Periods: Easily configurable inputs to set the start and end date of the backtesting range.

Fixed Slippage and Commission Settings: Ensures realistic simulation of trading conditions.

Process Orders on Close: Backtesting is optimized by processing orders at the bar's close.

Important Notes:

Backtesting Only: This script is intended purely for backtesting purposes. Past performance is not indicative of future results.

Live Trading Recommendations: For live trading, it is highly recommended to use limit orders instead of market orders, especially during evening sessions, as market order slippage can be significant.

Default Settings:

Entry size: 10% of equity per trade.

Slippage: 1 tick.

Commission: 0.05% per trade.

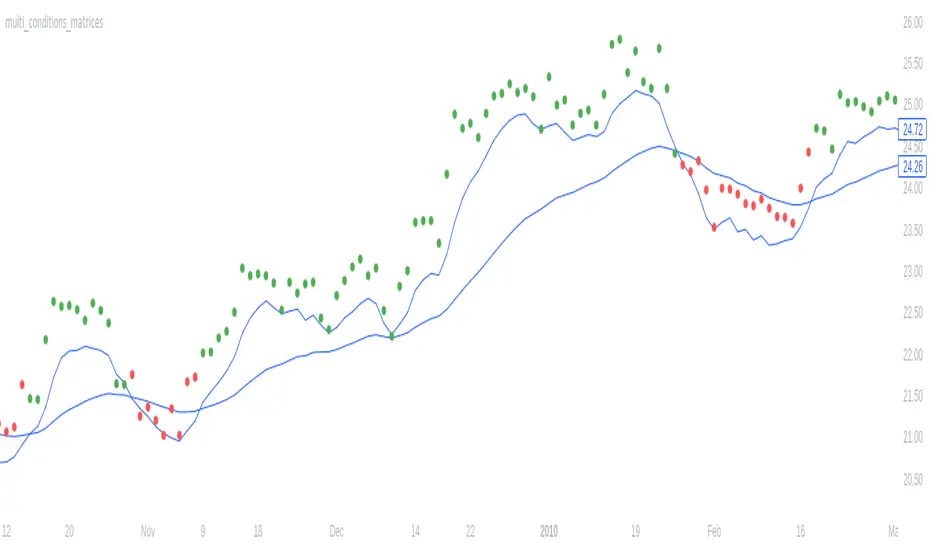

Multi conditions matricesLibrary "multi_conditions_matrices"

: facilitate including multiple AND / OR conditions to a script such as two entry / exit inputs groups.

method addConditions(conditions, conditionPair)

Helper to append conditions to a matrix condition array

Namespace types: matrix

Parameters:

conditions (matrix)

conditionPair (array) : array A condition pair , an input can be passed directly to enable

method check(conditions, operatorAnd)

check several condition within given operator

Namespace types: matrix

Parameters:

conditions (matrix)

operatorAnd (bool) : bool true if the operator between condition is AND (default OR)

Returns: bool Evaluates conditions

isWeekend()

isNightSignal(nightHour, morningHour, timezone)

Parameters:

nightHour (int)

morningHour (int)

timezone (string)

StrategyDashboardLibrary ”StrategyDashboard”

Hey, everybody!

I haven’t done anything here for a long time, I need to get better ^^.

In my strategies, so far private, but not about that, I constantly use dashboards, which clearly show how my strategy is working out.

Of course, you can also find a number of these parameters in the standard strategy window, but I prefer to display everything on the screen, rather than digging through a bunch of boxes and dropdowns.

At the moment I am using 2 dashboards, which I would like to share with you.

1. monthly(isShow)

this is a dashboard with the breakdown of profit by month in per cent. That is, it displays how much percentage you made or lost in a particular month, as well as for the year as a whole.

Parameters:

isShow (bool) - determine allowance to display or not.

2. total(isShow)

The second dashboard displays more of the standard strategy information, but in a table format. Information from the series “number of consecutive losers, number of consecutive wins, amount of earnings per day, etc.”.

Parameters:

isShow (bool) - determine allowance to display or not.

Since I prefer the dark theme of the interface, now they are adapted to it, but in the near future for general convenience I will add the ability to adapt to light.

The same goes for the colour scheme, now it is adapted to the one I use in my strategies (because the library with more is made by cutting these dashboards from my strategies), but will also make customisable part.

If you have any wishes, feel free to write in the comments, maybe I can implement and add them in the next versions.

Monte Carlo Simulation - Your Strategy [Kioseff Trading]Hello!

This script “Monte Carlo Simulation - Your Strategy” uses Monte Carlo simulations for your inputted strategy returns or the asset on your chart!

Features

Monte Carlo Simulation: Performs Monte Carlo simulation to generate multiple future paths.

Asset Price or Strategy: Can simulate either future asset prices based on historical log returns or a specific trading strategy's future performance.

User-Defined Input: Allows you to input your own historical returns for simulation.

Statistical Methods: Offers two simulation methods—Gaussian (Normal) distribution and Bootstrapping.

Graphical Display: Provides options for graphical representation, including line plots and histograms.

Cumulative Probability Target: Enables setting a user-defined cumulative probability target to quantify simulation results.

Adjustable Parameters: Offers numerous user-adjustable settings like number of simulations, forecast length, and more.

Historical Data Points: Option to specify the amount of historical data to be used in the simulation (price).

Custom Binning: Allows you to select the binning method for histograms, with options like Sturges, Rice, and Square Root.

Best/Worst Case: Allows you to show only the best case / worst case outcome (range) for all simulations!

Scatterplot: allows you to show up to 1000 potential outcomes for a specified trade number (or bars forward price endpoint) using a scatter plot.

The image above shows the primary components of the indicator!

The image above shows the best/worst case outcome feature in action!

The image above shows a "fun feature" where 1000 simulated end points for a 15-bar price trajectory are shown as a scatter plot!

How To Perform a Monte Carlo Simulation On Your Strategy

Really, you can input any data into the indicator it will perform a Monte Carlo Simulation on it :D

The following instructions show how to export your strategy results from TradingView to an Excel File, copy the data, and input it into the indicator.

However , you are not limited to following this method!

Wherever your strategy results are stored, simply copy and paste them into the indicator text area in the settings and simulations will begin.

Returns Should Follow This Format

1

3

-3

2

-5

The numbers are presented as a single column. No commas or separators used.

The numbers above are in sequential order. A return of "1" for the first trade and a return of "-5" for the last trade. Your strategy returns will likely be in sequential order already so don't worry too much about this (:

How To Perform a Monte Carlo Simulation On Your TradingView Strategy With Excel Data

Export your strategy returns to an excel file using TradingView

Navigate to your downloads folder to column G "Profit"

Click the column and press CTRL + SPACE to highlight the entire column

Press CTRL + C to copy the entire column

Open this indicator's settings and paste the returns into the text area

The image above illustrates the process!

Notes on Inputting Returns

*Must input your returns without a separate as a vertical list

*The initial text area can only hold so many return values. If your list of trades is large you can input additional returns into two additional text areas at the bottom of the indicator settings.

That should be it; thank you for checking this out!

Hobbiecode - Five Day Low RSI StrategyThis is a simple strategy that is working well on SPY but also well performing on Mini Futures SP500. The strategy is composed by the followin rules:

1. If today’s close is below yesterday’s five-day low, go long at the close.

2. Sell at the close when the two-day RSI closes above 50.

3. There is a time stop of five days if the sell criterium is not triggered.

If you backtest it on Mini Futures SP500 you will be able to track data from 1993. It is important to select D1 as timeframe.

Please share any comment or idea below.

Have a good trading,

Ramón.

Chandelier Exit ZLSMA StrategyIntroducing a Powerful Trading Indicator: Chandelier Exit with ZLSMA

If you're a trader, you know the importance of having the right tools and indicators to make informed decisions. That's why we're excited to introduce a powerful new trading indicator that combines the Chandelier Exit and ZLSMA: two widely-used and effective indicators for technical analysis.

The Chandelier Exit (CE) is a popular trailing stop-loss indicator developed by Chuck LeBeau. It's designed to follow the price trend of a security and provide an exit signal when the price crosses below the CE line. The CE line is based on the Average True Range (ATR), which is a measure of volatility. This means that the CE line adjusts to the volatility of the security, making it a reliable indicator for trailing stop-losses.

The ZLEMA (Zero Lag Exponential Moving Average) is a type of exponential moving average that's designed to reduce lag and improve signal accuracy. The ZLSMA takes into account not only the current price but also past prices, using a weighted formula to calculate the moving average. This makes it a smoother indicator than traditional moving averages, and less prone to giving false signals.

When combined, the CE and ZLSMA create a powerful indicator that can help traders identify trend changes and make more informed trading decisions. The CE provides the trailing stop-loss signal, while the ZLSMA provides a smoother trend line to help identify potential entry and exit points.

In our indicator, the CE and ZLSMA are plotted together on the chart, making it easy to see both the trailing stop-loss and the trend line at the same time. The CE line is displayed as a dotted line, while the ZLSMA line is displayed as a solid line.

Using this indicator, traders can set their stop-loss levels based on the CE line, while also using the ZLSMA line to identify potential entry and exit points. The combination of these two indicators can help traders reduce their risk and improve their trading performance.

In conclusion, the Chandelier Exit with ZLSMA is a powerful trading indicator that combines two effective technical analysis tools. By using this indicator, traders can identify trend changes, set stop-loss levels, and make more informed trading decisions. Try it out for yourself and see how it can improve your trading performance.

Warning: The results in the backtest are from a repainting strategy. Don't take them seriously. You need to do a dry live test in order to test it for its useability.

-

Here is a description of each input field in the provided source code:

length: An integer input used as the period for the ATR (Average True Range) calculation. Default value is 1.

mult: A float input used as a multiplier for the ATR value. Default value is 2.

showLabels: A boolean input that determines whether to display buy/sell labels on the chart. Default value is false.

isSignalLabelEnabled: A boolean input that determines whether to display signal labels on the chart. Default value is true.

useClose: A boolean input that determines whether to use the close price for extrema calculations. Default value is true.

zcolorchange: A boolean input that determines whether to enable rising/decreasing highlighting for the ZLSMA (Zero-Lag Exponential Moving Average) line. Default value is false.

zlsmaLength: An integer input used as the length for the ZLSMA calculation. Default value is 50.

offset: An integer input used as an offset for the ZLSMA calculation. Default value is 0.

-

Ty for checking this out and good luck on your trading journey! Likes and comments are appreciated. 👍

--

Credits to:

▪ @everget – Chandelier Exit (CE)

▪ @netweaver2022 – ZLSMA

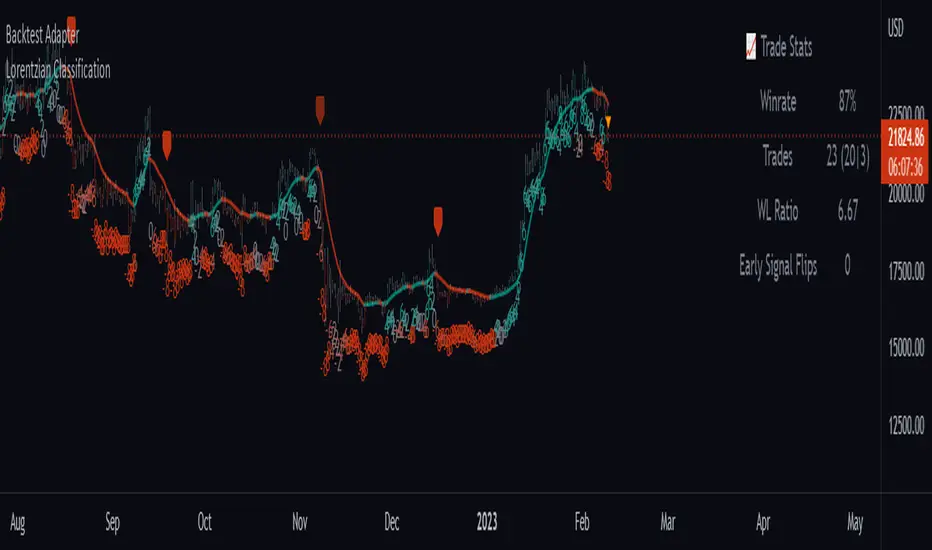

Backtest AdapterThis is a proof-of-concept Backtest Adapter that can be used with my recent publication "Machine Learning: Lorentzian Classification" located here:

This adapter is helpful because it enables interactive backtesting with TradingView's built-in "Strategy Tester" framework without the need to translate the logic from an "indicator" script to a "strategy" script.

To use this, one must have the "Machine Learning: Lorentzian Classification" script and this Backtest Adapter open simultaneously on the same chart. From there, simply change the "Source" setting of the Backtest Adapter to "Lorentzian Classification: Backtest Stream" to transfer the entry/exit signals stream to the Backtest Adapter.

For an example of how to implement your own backtest stream in your indicators, please refer to the "Backtesting" section in the source code of the "Machine Learning: Lorentzian Classification" script, which is shown below for convenience:

Reinforced RSI - The Quant Science This strategy was designed and written with the goal of showing and motivating the community how to integrate our 'Probabilities' module with their own script.

We have recreated one of the simplest strategies used by many traders. The strategy only trades long and uses the overbought and oversold levels on the RSI indicator.

We added stop losses and take profits to offer more dynamism to the strategy. Then the 'Probabilities' module was integrated to create a probabilistic reinforcement on each trade.

Specifically, each trade is executed, only if the past probabilities of making a profitable trade is greater than or equal to 51%. This greatly increased the performance of the strategy by avoiding possible bad trades.

The backtesting was calculated on the NASDAQ:TSLA , on 15 minutes timeframe.

The strategy works on Tesla using the following parameters:

1. Lenght: 13

2. Oversold: 40

3. Overbought: 70

4. Lookback: 50

5. Take profit: 3%

6. Stop loss: 3%

Time period: January 2021 to date.

Our Probabilities Module, used in the strategy example:

iMoku (Ichimoku Complete Tool) - The Quant Science iMoku™ is a professional all-in-one solution for the famous Ichimoku Kinko Hyo indicator.

The algorithm includes:

1. Backtesting spot

2. Visual tool

3. Auto-trading functions

With iMoku you can test four different strategies.

Strategy 1: Cross Tenkan Sen - Kijun Sen

A long position is opened with 100% of the invested capital ($1000) when "Tenkan Sen" crossover "Kijun Sen".

Closing the long position on the opposite condition.

There are 3 different strength signals for this strategy: weak, normal, strong.

Weak : the signal is weak when the condition is true and the price is above the 'Kumo'

Normal : the signal is normal when the condition is true and the price is within the 'Kumo'

Strong : the signal is strong when the condition is true and the price is below the 'Kumo'

Strategy 2: Cross Price - Kijun Sen

A long position is opened with 100% of the invested capital ($1000) when the price crossover the 'Kijun Sen'.

Closing the long position on the opposite condition.

There are 3 different strength signals for this strategy: weak, normal, strong.

Weak : the signal is weak when the condition is true and the price is above the 'Kumo'

Normal : the signal is normal when the condition is true and the price is inside the 'Kumo'

Strong : the signal is strong when the condition is true and the price is below the 'Kumo'

Strategy 3: Kumo Breakout

A long position is opened with 100% of the invested capital ($1000) when the price breakup the 'Kumo'.

Closing the long position with a percentage stop loss and take profit on the invested capital.

Strategy 4: Kumo Twist

A long position is opened with 100% of the invested capital ($1000) when the 'Kumo' goes from negative to positive (called "Twist").

Closing the long position on the opposite condition.

There are 2 different strength signals for this strategy: weak, and strong.

Weak : the signal is weak when the condition is true and the price is above the 'Kumo'

Strong : the signal is strong when the condition is true and the price is below the 'Kumo'

This script is compliant with algorithmic trading.

You can use this script with trading terminals such as 3Commas or CryptoHopper. Connecting this script is very easy.

1. Enter the user interface

2. Select and activate a strategy

3. Copy your bot's links into the dedicated fields

4. Create and activate alert

Disclaimer: algorithmic trading involves risk, the user should consider aspects such as slippage, liquidity and costs when evaluating an asset. The Quant Science is not responsible for any kind of damage resulting from use of this script. By using this script you take all the responsibilities and risks.

Channels Strategy [JoseMetal]============

ENGLISH

============

- Description:

This strategy is based on Bollinger Bands / Keltner Channel price "rebounds" (the idea of price bouncing from one band to another).

The strategy has several customizable options, which allows you to refine the strategy for your asset and timeframe.

You can customize settings for ALL indicators, Bollinger Bands (period and standard deviation), Keltner Channel (period and ATR multiplier) and ATR (period).

- AVAILABLE INDICATORS:

You can pick Bollinger Bands or Keltner Channels for the strategy, the chosen indicator will be plotted as well.

- CUSTOM CONDITIONS TO ENTER A POSITION:

1. Price breaks the band (low below lower band for LONG or high above higher band for SHORT).

2. Same as 1 but THEN (next candle) price closes INSIDE the bands.

3. Price breaks the band AND CLOSES OUT of the band (lower band for LONG and higher band for SHORT).

4. Same as 3 but THEN (next candle) price closes INSIDE the bands.

- STOP LOSS OPTIONS:

1. Previous wick (low of previous candle if LONG and high or previous candle if SHORT).

2. Extended band, you can customize settings for a second indicator with larger values to use it as STOP LOSS, for example, Bollinger Bands with 2 standard deviations to open positions and 3 for STOP LOSS.

3. ATR: you can pick average true ratio from a source (like closing price) with a multiplier to calculate STOP LOSS.

- TAKE PROFIT OPTIONS:

1. Opposite band (top band for LONGs, bottom band for SHORTs).

2. Moving average: Bollinger Bands simple moving average or Keltner Channel exponential moving average .

3. ATR: you can pick average true ratio from a source (like closing price) with a multiplier to calculate TAKE PROFIT.

- OTHER OPTIONS:

You can pick to trade only LONGs, only SHORTs, both or none (just indicator).

You can enable DYNAMIC TAKE PROFIT, which updates TAKE PROFIT on each candle, for example, if you pick "opposite band" as TAKE PROFIT, it'll update the TAKE PROFIT based on that, on every single new candle.

- Visual:

Bands shown will depend on the chosen indicator and it's settings.

ATR is only printed if used as STOP LOSS and/or TAKE PROFIT.

- Recommendations:

Recommended on DAILY timeframe , it works better with Keltner Channels rather than Bollinger Bands .

- Customization:

As you can see, almost everything is customizable, for colors and plotting styles check the "Style" tab.

Enjoy!

============

ESPAÑOL

============

- Descripción:

Esta estrategia se basa en los "rebotes" de precios en las Bandas de Bollinger / Canal de Keltner (la idea de que el precio rebote de una banda a otra).

La estrategia tiene varias opciones personalizables, lo que le permite refinar la estrategia para su activo y temporalidad favoritas.

Puedes personalizar la configuración de TODOS los indicadores, Bandas de Bollinger (periodo y desviación estándar), Canal de Keltner (periodo y multiplicador ATR) y ATR (periodo).

- INDICADORES DISPONIBLES:

Puedes elegir las Bandas de Bollinger o los Canales de Keltner para la estrategia, el indicador elegido será mostrado en pantalla.

- CONDICIONES PERSONALIZADAS PARA ENTRAR EN UNA POSICIÓN:

1. El precio rompe la banda (mínimo por debajo de la banda inferior para LONG o máximo por encima de la banda superior para SHORT).

2. Lo mismo que en el punto 1 pero ADEMÁS (en la siguiente vela) el precio cierra DENTRO de las bandas.

3. El precio rompe la banda Y CIERRA FUERA de la banda (banda inferior para LONG y banda superior para SHORT).

4. Igual que el 3 pero ADEMÁS (siguiente vela) el precio cierra DENTRO de las bandas.

- OPCIONES DE STOP LOSS:

1. Mecha anterior (mínimo de la vela anterior si es LONGy máximo de la vela anterior si es SHORT).

2. Banda extendida, puedes personalizar la configuración de un segundo indicador con valores más extensos para utilizarlo como STOP LOSS, por ejemplo, Bandas de Bollinger con 2 desviaciones estándar para abrir posiciones y 3 para STOP LOSS.

3. ATR: puedes elegir el average true ratio de una fuente (como el precio de cierre) con un multiplicador para calcular el STOP LOSS.

- OPCIONES DE TAKE PROFIT:

1. Banda opuesta (banda superior para LONGs, banda inferior para SHORTs).

2. Media móvil: media móvil simple de las Bandas de Bollinger o media móvil exponencial del Canal de Keltner .

3. ATR: se puede escoger el average true ratio de una fuente (como el precio de cierre) con un multiplicador para calcular el TAKE PROFIT.

- OTRAS OPCIONES:

Puedes elegir operar sólo con LONGs, sólo con SHORTs, ambos o ninguno (sólo el indicador).

Puedes activar el TAKE PROFIT DINÁMICO, que actualiza el TAKE PROFIT en cada vela, por ejemplo, si eliges "banda opuesta" como TAKE PROFIT, actualizará el TAKE PROFIT basado en eso, en cada nueva vela.

- Visual:

Las bandas mostradas dependerán del indicador elegido y de su configuración.

El ATR sólo se muestra si se utiliza como STOP LOSS y/o TAKE PROFIT.

- Recomendaciones:

Recomendada para temporalidad de DIARIO, funciona mejor con los Canales de Keltner que con las Bandas de Bollinger .

- Personalización:

Como puedes ver, casi todo es personalizable, para los colores y estilos de dibujo comprueba la pestaña "Estilo".

¡Que lo disfrutes!

[MT] Strategy Backtest Template| Initial Release | | EN |

An update of my old script, this script is designed so that it can be used as a template for all those traders who want to save time when programming their strategy and backtesting it, having functions already programmed that in normal development would take you more time to program, with this template you can simply add your favorite indicator and thus be able to take advantage of all the functions that this template has.

🔴Stop Loss and 🟢Take Profit:

No need to mention that it is a Stop Loss and a Take Profit, within these functions we find the options of: fixed percentage (%), fixed price ($), ATR, especially for Stop Loss we find the Pivot Points, in addition to this, the price range between the entry and the Stop Loss can be converted into a trailing stop loss, instead, especially for the Take Profit we have an option to choose a 1:X ratio that complements very well with the Pivot Points.

📈Heikin Ashi Based Entries:

Heikin Ashi entries are trades that are calculated based on Heikin Ashi candles but their price is executed to Japanese candles, thus avoiding false results that occur in Heikin candlestick charts, this making in certain cases better results in strategies that are executed with this option compared to Japanese candlesticks.

📊Dashboard:

A more visual and organized way to see the results and necessary data produced by our strategy, among them we can see the dates between which our operations are made regardless if you have activated some time filter, usual data such as Profit, Win Rate, Profit factor are also displayed in this panel, additionally data such as the total number of operations, how many were gains and how many losses, the average profit and loss for each operation and finally the maximum profits and losses followed, which are data that will be very useful to us when we elaborate our strategies.

Feel free to use this template to program your own strategies, if you find errors or want to request a new feature let me know in the comments or through my social networks found in my tradingview profile.

| Update 1.1 | | EN |

➕Additions: '

Time sessions filter and days of the week filter added to the time filter section.

Option to add leverage to the strategy.

5 Moving Averages, RSI, Stochastic RSI, ADX, and Parabolic Sar have been added as indicators for the strategy.

You can choose from the 6 available indicators the way to trade, entry alert or entry filter.

Added the option of ATR for Take Profit.

Ticker information and timeframe are now displayed on the dashboard.

Added display customization and color customization of indicator plots.

Added customization of display and color plots of trades displayed on chart.

📝Changes:

Now when activating the time filter it is optional to add a start or end date and time, being able to only add a start date or only an end date.

Operation plots have been changed from plot() to line creation with line.new().