PSAR with ATR Trailing Stop + SMA Filter📈 Strategy Overview: PSAR + 6×ATR Trailing Stop with SMA Filter

This strategy is built around the principle of “Cut the losers, let the winners run” — a disciplined, trend-following approach that combines the Parabolic SAR indicator with dynamic risk management and a Simple Moving Average (SMA) trend filter.

🔍 Strategy Logic

Trend Filter Trades are only taken in the direction of the prevailing trend, defined by a user-selected SMA (default: 100).

✅ Long trades only when price is above the SMA

✅ Short trades only when price is below the SMA

Entry Signal: A trade is triggered when the Parabolic SAR flips to the opposite side of the price bars, signaling a potential trend reversal.

Stop Loss: The stop loss is dynamically set at 6×ATR from the entry price. This adapts to market volatility and is recalculated every bar — effectively acting as a trailing stop.

Exit Logic: There is no fixed take profit. The trade remains open until the trailing stop is hit — allowing winners to run and losers to be cut quickly.

Risk Management: Each trade risks 0.5% of total equity, ensuring consistent position sizing and capital preservation.

📊 Visual Elements

PSAR dots mark trend direction changes

SMA line shows the broader trend filter

Trailing stop crosses (with 50% opacity) indicate the current stop level without cluttering the chart

⚙️ Customizable Inputs

PSAR parameters: Start, Increment, Maximum

ATR length and multiplier

SMA length

Risk percentage per trade

This strategy is ideal for traders who want to stay aligned with the trend, automate disciplined exits, and avoid emotional decision-making. Clean, simple, and powerful.

Wishing you calm and successful trades!

Simplertrading

3 Red / 3 Green Strategy with Volatility CheckStrategy Name: 3 Red / 3 Green Strategy with Volatility Check by AlgoTradeKit

Overview

This long-only strategy is designed for daily bars on NASDAQ (or similar instruments) and combines simple price action with a volatility filter. It “tells it like it is” – enter when the market shows weakness, but only in sufficiently volatile conditions, and exit either on signs of a reversal or after a set number of days.

Entry Conditions

- Price Action :

Enter a long position when there are 3 consecutive red days (each day's close is below its open).

- Volatility Filter :

The entry is allowed only if the current ATR (Average True Range) calculated over the specified ATR Period (default 12) is greater than its 30-day simple moving average. This ensures the market has enough volatility to justify the trade.

Exit Conditions

- Reversal Signal :

Exit the long position when 3 consecutive green days occur (each day's close is above its open), signaling a potential reversal.

- Time Limit :

Regardless of market conditions, any open trade is closed if it reaches the Maximum Trade Duration (default 22 days). This helps limit exposure during stagnant or unfavorable market conditions.

- You can toggle the three-green-day exit if you want to isolate the time-based exit.

Input Parameters

- Maximum Trade Duration (days): Default is 22 days.

- ATR Period: Default is 12.

- Use 3 Green Days Exit: Toggle to enable or disable the three-green-day exit condition.

How It Works

1. Entry: The strategy monitors daily price action for 3 consecutive down days. When this occurs and if the market is volatile enough (current ATR > 30-day ATR average), it opens a long position.

2. Exit: The position is closed if the price action reverses with 3 consecutive up days or if the trade has been open for the maximum allowed duration - i.e. use it on daily chart.

Risk Management

- The built-in maximum trade duration prevents trades from lingering too long in a non-trending or consolidating market.

- The volatility filter helps ensure that trades are only taken when there is sufficient price movement, potentially increasing the odds of a meaningful move.

Disclaimer

This strategy is provided “as is” without any warranties. It is essential to backtest and validate the performance on your specific instrument and market conditions before deploying live capital. Trading involves significant risk, and you should adjust parameters to match your risk tolerance.

Test and tweak this strategy to see if it fits your trading style and market conditions. Happy trading!

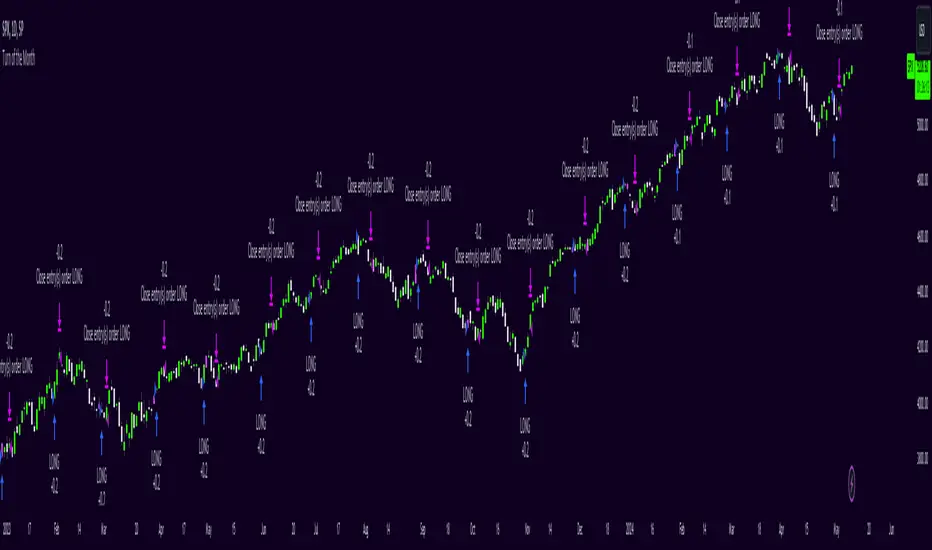

Turn of the Month Strategy [Honestcowboy]The end of month effect is a well known trading strategy in the stock market. Quite simply, most stocks go up at the end of the month. What's even better is that this effect spills over to the next phew days of the next month.

In this script we backtest this theory which should work especially well on SP500 pair.

By default the strategy buys 2 days before the end of each month and exits the position 3 days into the next month.

The strategy is a long only strategy and is extremely simple. The SP500 is one of the #1 assets people use for long term investing due to it's "9.8%" annualised return. However as a trader you want the best deal possible. This strategy is only inside the market for about 25% of the time while delivering a similar return per exposure with a lower drawdown.

Here are some hypothesis why turn of the month effect happens in the stock markets:

Increased inflow from savings accounts to stocks at end of month

Rebalancing of portfolios by fund managers at end of month

The timing of monthly cash flows received by pension funds, which are reinvested in the stock market.

The script also has some inputs to define how many days before end of the month you want to buy the asset and how long you want to hold it into the next month.

It is not possible to buy the asset exactly on this day every month as the market closes on the weekend. I've added some logic where it will check if that day is a friday, saturdady or sunday. If that is the case it will send the buy signal on the end of thursday, this way we enter on the friday and don't lose that months trading opportunity.

The backtest below uses 4% exposure per trade as to show the equity curve more clearly and because of publishing rules. However, most fund managers and investors use 100% exposure. This way you actually risk money to earn money. Feel free to adjust the settings to your risk profile to get a clearer picture of risks and rewards before implementing in your portfolio.

2 Moving Averages | Trend FollowingThe trading system is a trend-following strategy based on two moving averages (MA) and Parabolic SAR (PSAR) indicators.

How it works:

The strategy uses two moving averages: a fast MA and a slow MA.

It checks for a bullish trend when the fast MA is above the slow MA and the current price is above the fast MA.

It checks for a bearish trend when the fast MA is below the slow MA and the current price is below the fast MA.

The Parabolic SAR (PSAR) indicator is used for additional trend confirmation.

Long and short positions can be turned on or off based on user input.

The strategy incorporates risk management with stop-loss orders based on the Average True Range (ATR).

Users can filter the backtest date range and display various indicators.

The strategy is designed to work with the date range filter, risk management, and user-defined positions.

Features:

Trend-following strategy.

Two customizable moving averages.

Parabolic SAR for trend confirmation.

User-defined risk management with stop-loss based on ATR.

Backtest date range filter.

Flexibility to enable or disable long and short positions.

This trading system provides a comprehensive approach to trend-following and risk management, making it suitable for traders looking to capture trends with controlled risk.