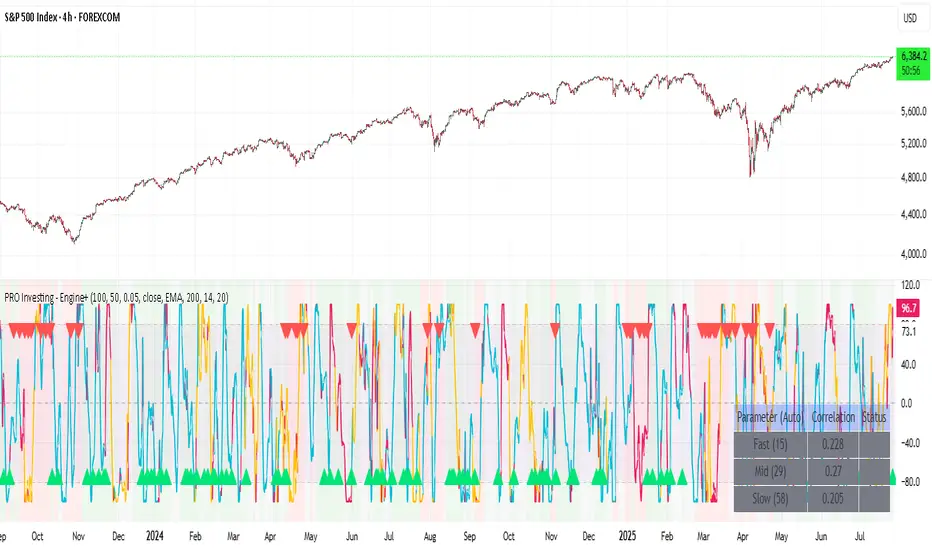

PRO Investing - Apex EnginePRO Investing - Apex Engine

1. Core Concept: Why Does This Indicator Exist?

Traditional momentum oscillators like RSI or Stochastic use a fixed "lookback period" (e.g., 14). This creates a fundamental problem: a 14-period setting that works well in a fast, trending market will generate constant false signals in a slow, choppy market, and vice-versa. The market's character is dynamic, but most tools are static.

The Apex Engine was built to solve this problem. Its primary innovation is a self-optimizing core that continuously adapts to changing market conditions. Instead of relying on one fixed setting, it actively tests three different momentum profiles (Fast, Mid, and Slow) in real-time and selects the one that is most synchronized with the current price action.

This is not just a random combination of indicators; it's a deliberate synthesis designed to create a more robust momentum tool. It combines:

Volatility analysis (ATR) to generate adaptive lookback periods.

Momentum measurement (ROC) to gauge the speed of price changes.

Statistical analysis (Correlation) to validate which momentum measurement is most effective right now.

Classic trend filters (Moving Average, ADX) to ensure signals are only taken in favorable market conditions.

The result is an oscillator that aims to be more responsive in volatile trends and more stable in quiet periods, providing a more intelligent and adaptive signal.

2. How It Works: The Engine's Three-Stage Process

To be transparent, it's important to understand the step-by-step logic the indicator follows on every bar. It's a process of Adapt -> Validate -> Signal.

Stage 1: Adapt (Dynamic Length Calculation)

The engine first measures market volatility using the Average True Range (ATR) relative to its own long-term average. This creates a volatility_factor. In high-volatility environments, this factor causes the base calculation lengths to shorten. In low-volatility, they lengthen. This produces three potential Rate of Change (ROC) lengths: dynamic_fast_len, dynamic_mid_len, and dynamic_slow_len.

Stage 2: Validate (Self-Optimizing Mode Selection)

This is the core of the engine. It calculates the ROC for all three dynamic lengths. To determine which is best, it uses the ta.correlation() function to measure how well each ROC's movement has correlated with the actual bar-to-bar price changes over the "Optimization Lookback" period. The ROC length with the highest correlation score is chosen as the most effective profile for the current moment. This "active" mode is reflected in the oscillator's color and the dashboard.

Stage 3: Signal (Normalized Velocity Oscillator)

The winning ROC series is then normalized into a consistent oscillator (the Velocity line) that ranges from -100 (extreme oversold) to +100 (extreme overbought). This ensures signals are comparable across any asset or timeframe. Signals are only generated when this Velocity line crosses its signal line and the trend filters (explained below) give a green light.

3. How to Use the Indicator: A Practical Guide

Reading the Visuals:

Velocity Line (Blue/Yellow/Pink): The main oscillator line. Its color indicates which mode is active (Fast, Mid, or Slow).

Signal Line (White): A moving average of the Velocity line. Crossovers generate potential signals.

Buy/Sell Triangles (▲ / ▼): These are your primary entry signals. They are intentionally strict and only appear when momentum, trend, and price action align.

Background Color (Green/Red/Gray): This is your trend context.

Green: Bullish trend confirmed (e.g., price above a rising 200 EMA and ADX > 20). Only Buy signals (▲) can appear.

Red: Bearish trend confirmed. Only Sell signals (▼) can appear.

Gray: No clear trend. The market is likely choppy or consolidating. No signals will appear; it is best to stay out.

Trading Strategy Example:

Wait for a colored background. A green or red background indicates the market is in a tradable trend.

Look for a signal. For a green background, wait for a lime Buy triangle (▲) to appear.

Confirm the trade. Before entering, confirm the signal aligns with your own analysis (e.g., support/resistance levels, chart patterns).

Manage the trade. Set a stop-loss according to your risk management rules. An exit can be considered on a fixed target, a trailing stop, or when an opposing signal appears.

4. Settings and Customization

This script is open-source, and its settings are transparent. You are encouraged to understand them.

Synaptic Engine Group:

Volatility Period: The master control for the adaptive engine. Higher values are slower and more stable.

Optimization Lookback: How many bars to use for the correlation check.

Switch Sensitivity: A buffer to prevent frantic switching between modes.

Advanced Configuration & Filters Group:

Price Source: The data source for momentum calculation (default close).

Trend Filter MA Type & Length: Define your long-term trend.

Filter by MA Slope: A key feature. If ON, allows for "buy the dip" entries below a rising MA. If OFF, it's stricter, requiring price to be above the MA.

ADX Length & Threshold: Filters out non-trending, choppy markets. Signals will not fire if the ADX is below this threshold.

5. Important Disclaimer

This indicator is a decision-support tool for discretionary traders, not an automated trading system or financial advice. Past performance is not indicative of future results. All trading involves substantial risk. You should always use proper risk management, including setting stop-losses, and never risk more than you are prepared to lose. The signals generated by this script should be used as one component of a broader trading plan.

Cari skrip untuk "马斯克+100万"

HSI1! First 30m Candle Strategy (15m Chart)## HSI1! First 30-Minute Candle Breakout Strategy (15m Chart) — Description

### Overview

This strategy is designed for trading **Hang Seng Index (HSI) Futures** on a 15-minute chart. It uses the price range established during the first 30 minutes of the Hong Kong main session (09:15–09:44:59) to define key breakout levels for a systematic trade entry each day.

### How the Strategy Works

#### 1. Reference Candle Period

- **Aggregation Window:** The strategy monitors the first two 15-minute bars of the session (09:15:00–09:44:59 HKT).

- **Range Capture:** It records the highest and lowest prices (the "reference high/low") during this window.

#### 2. Trade Setup

- After the 09:45 bar completes, the reference range is locked in.

- Throughout the rest of the trading day (within session hours), the strategy looks for breakouts beyond the reference range.

#### 3. Entry Rules

- **Long Entry (Buy):**

- Triggered if price rises to or above the reference high.

- Only entered if the user's settings permit "Buy Only" or "Both".

- **Short Entry (Sell):**

- Triggered if price falls to or below the reference low.

- Only entered if the user's settings permit "Sell Only" or "Both".

- **Single trade per day:**

- Once any trade executes, no additional trades are opened until the next session.

#### 4. Exit Rules

- **Take Profit (TP):**

- Target profit is set to a distance equal to the initial range added above the long entry (or subtracted below the short entry).

- Example: For a 100-point range, a long trade targets entry + 100 points.

- **Stop Loss (SL):**

- Longs are stopped out if price falls back to the session's reference low; shorts are stopped out if price rallies to the reference high.

#### 5. Session Control

- Active only within the regular day session (09:15–12:00 and 13:00–16:00 HKT).

- Trade tracking resets each new trading day.

#### 6. Trade Direction Manual Setting

- A user input allows restriction to "Buy Only", "Sell Only" or "Both" directions, providing discretion over daily bias.

### Example Workflow

| Step | Action |

|---------------------------|-------------------------------------------------------------------------|

| 09:15–09:44 | Aggregate first two 15m candles; record daily high/low |

| After 09:45 | Wait for a breakout (price crossing either the high or the low) |

| Long trade triggered | Enter at the reference high, target is "high + range", SL is at the low |

| Short trade triggered | Enter at the reference low, target is "low - range", SL at the high |

| Trade management | No more trades for the day, regardless of further breakouts |

| End of session (if open) | Trades may be closed per further logic or left to strategy to handle |

### Key Features and Benefits

- **Discipline:** Only one trade per day, minimizing overtrading.

- **Clarity:** Transparent entry/exit rules; no discretionary execution.

- **Flexibility:** User can bias system to buy-only, sell-only, or allow both, depending on trend or personal view.

- **Simple Risk Control:** Pre-defined stop loss and profit target for every trade.

- **Works best in:** Trending, breakout-prone markets with a history of impulsive moves early in the session.

This strategy is ideal for systematic traders looking to capture the Hang Seng's early session momentum, with robust rule-based management and minimal intervention.

SENTIMENTSENTIMENT Indicator – User Guide

Summary

The SENTIMENT indicator provides a quick visual reference for current and recent market sentiment. It compares the closing price to a custom sentiment value, which is the average of the 100-period (default) simple moving averages (SMA) of the high and low prices. The indicator displays this information in a color-coded table and plots the difference between price and sentiment as a line on your chart.

How to Use

1. Table Overview

The table appears on your chart in your chosen position.

It displays four rows: the current bar (“Now”) and the previous three bars (“Bar -1”, “Bar -2”, “Bar -3”).

Each row shows:

The bar label (The current bar is live and active, constantly changing)

The closing price for that bar

The difference between the closing price and the sentiment value for that bar

The sentiment difference is color-coded:

Green: Price is above sentiment (bullish)

Red: Price is below sentiment (bearish)

2. Chart Plot

The indicator plots a line showing the difference between the current price and the sentiment value.

When the line is above zero: price is above sentiment (bullish).

When the line is below zero: price is below sentiment (bearish).

3. Settings

Number of Lookback Bars: Adjusts the SMA period for sentiment calculation (default is 100).

Table Position: Choose where to display the table on your chart (e.g., Top Left, Bottom Right).

How to Interpret

Green values in the table or a plot above zero suggest bullish sentiment.

Red values in the table or a plot below zero suggest bearish sentiment.

Use this indicator to quickly assess if the market is trading above or below its recent average sentiment level.

Tips

You can combine the SENTIMENT indicator with other tools or signals for more robust trading decisions.

Adjust the lookback period to suit your trading timeframe and style.

MA Table [RanaAlgo]The "MA Table " indicator is a comprehensive and visually appealing tool for tracking moving average signals in TradingView. Here's a short summary of its usefulness:

Key Features:

Dual MA Support:

Tracks both EMA (Exponential Moving Average) and SMA (Simple Moving Average) signals (10, 20, 30, 50, 100 periods).

Users can toggle visibility for EMA/SMA separately.

Clear Signal Visualization:

Displays Buy (▲) or Sell (▼) signals based on price position relative to each MA.

Color-coded (green for buy, red for sell) for quick interpretation.

Customizable Table Design:

Adjustable position (9 placement options), colors, text size, and border styling.

Alternating row colors improve readability.

Optional MA Plots:

Can display the actual MA lines on the chart for visual confirmation (with distinct colors/styles).

Usefulness:

Quick Overview: The table consolidates multiple MA signals in one place, saving time compared to checking each MA individually.

Trend Confirmation: Helps confirm trend strength when multiple MAs align (e.g., price above all MAs → strong uptrend).

Flexible: Suitable for both short-term (10-20 period) and long-term (50-100 period) traders.

Aesthetic: Professional design enhances chart clarity without clutter.

Ideal For:

Traders who rely on moving average crossovers or price-MA relationships.

Multi-timeframe analysis when combined with other tools.

Beginners learning MA strategies (clear visual feedback).

TrendShift [MOT]📈 TrendShift – Multi-Factor Momentum & Trend Signal Suite

TrendShift is a precision-built momentum and confluence tool designed to highlight directional shifts in price action. It combines EMA slope structure, oscillator confirmation, volume behavior, and dynamic SL/TP logic into one cohesive system. Whether you're trading with the trend or catching reversals, TrendShift provides data-backed clarity and visual confidence — and it’s available free to the public.

🔍 Core Signal Logic

Buy (🟢 Long) and Sell (🔴 Short) signals are triggered when multiple conditions align within a set bar window (default: 5 bars):

Stochastic RSI K/D cross

RSI crosses above 20 (long) or below 80 (short)

Stochastic RSI breaks 20 (long) or 80 (short)

Volume exceeds 20-bar average

🧭 Visual Trend Dashboard – Signal Table

A real-time on-chart dashboard displays:

EMA Trend: Bullish / Bearish / Mixed (based on 4 EMA slopes)

Stoch RSI: Oversold / Overbought / Neutral

RSI: Exact value with zone label

Volume: Above or Below average

Dashboard theme and position are fully customizable.

📐 Trend Structure with EMA Slope Logic

Plots four EMAs (21, 50, 100, 200) color-coded by slope:

Green = Rising

Red = Falling

These feed into the dashboard's EMA Trend display.

🎯 Optional Take Profit / Stop Loss Zones

When enabled, SL/TP lines plot automatically on valid signals:

Fixed-distance targets (e.g., 10pt TP, 5pt SL)

Auto-remove on TP or SL hit

Separate lines for long vs. short trades

Fully customizable styling

🔁 Trailing Stop Filter (Internal Logic)

A custom ATR-based trailing stop helps validate directional strength:

ATR period

HHV window

ATR multiplier

Used internally — not plotted — to confirm trend progression before entry.

⚙️ Customizable Parameters

Every core component is user-configurable:

EMA periods: 21 / 50 / 100 / 200

ATR trailing logic: period, HHV, multiplier

Oscillator settings: Stoch RSI & RSI

Volume length

SL/TP toggles and point values

Bar clustering window

Dashboard theme and location

🔔 Alerts Included

BUY Signal Triggered

SELL Signal Triggered

Compatible with webhook automation or mobile push notifications.

⚠️ Disclaimer

This tool is for educational purposes only and is not financial advice. Trading involves risk — always do your own research and consult a licensed professional before making trading decisions.

% / ATR Buy, Target, Stop + Overlay & P/L% / ATR Buy, Target, Stop + Overlay & P/L

This tool combines volatility‑based and fixed‑percentage trade planning into a single, on‑chart overlay—with built‑in profit‑and‑loss estimates. Toggle between ATR or percentage modes, plot your Buy, Target and Stop levels, and see the dollar gain or loss for a specified position size—all in one interactive table and chart display.

NOTE: To activate plotted lines, price labels, P/L rows and table values, enter a Buy Price greater than zero.

What It Does

Mode Toggle: Choose between “ATR” (volatility‑based) or “%” (fixed‑percentage) calculations.

Buy Price Input: Manually enter your entry price.

ATR Mode:

Target = Buy + (ATR × Target Multiplier)

Stop = Buy − (ATR × Stop Multiplier)

Percentage Mode:

Target = Buy × (1 + Target % / 100)

Stop = Buy × (1 – Stop % / 100)

P/L Estimates: Specify a dollar amount to “invest” at your Buy price, and the script calculates:

Gain ($): Profit if Target is hit

Loss ($): Cost if Stop is hit

Visual Overlay: Draws horizontal lines for Buy, Target and Stop, with optional price labels on the chart scale.

Interactive Table: Displays Buy, Target, Stop, ATR/timeframe info (in ATR mode), percentages (in % mode), and P/L rows.

Customization Options

Line Settings:

Choose color, style (solid/dashed/dotted), and width for Buy, Target, Stop lines.

Extend lines rightward only or in both directions.

Table Settings:

Position the table (top/bottom × left/right).

Toggle individual rows: Buy Price; Target (multiplier or %); Stop (multiplier or %); Target ATR %; Stop ATR %; ATR Time Frame; ATR Value; Gain ($); Loss ($).

Customize text colors for each row and background transparency.

General Inputs:

ATR length and optional ATR timeframe override (e.g. use daily ATR on an intraday chart).

Target/Stop multipliers or percentages.

Dollar Amount for P/L calculations.

How to Use It for Trading

Plan Your Entry: Enter your intended Buy Price and position size (dollar amount).

Select Mode: Toggle between ATR or % mode depending on whether you prefer volatility‑based or fixed offsets.

Assess R:R and P/L: Instantly see your Target, Stop levels, and potential profit or loss in dollars.

Visual Reference: Lines and price labels update in real time as you tweak inputs—ideal for live trading, backtesting or trade journaling.

Ideal For

Traders who want both volatility‑based and percentage‑based exit options in one tool

Those who need on‑chart P/L estimates based on position size

Swing and intraday traders focused on objective, rule‑based trade management

Anyone who uses ATR for adaptive stops/targets or fixed percentages for simpler exits

Ultimate ATR Extreme DetectorUltimate ATR Extreme Detector

Professional Volatility Analysis Tool for Strategic Trading

Discover Market Turning Points with Precision

Key Features

Smart Extremum Detection: Identifies when ATR reaches its highest or lowest point in your specified lookback period

Quad Visual Alert System:

▲ Green bottom triangles for low volatility signals

▼ Red top triangles for high volatility signals

Background color highlighting for instant state recognition

Status panel showing current volatility extremes

Dual Alert Modes:

TradingView native alerts ("ATR Low/High Signal")

Visual chart alerts with period details (e.g., "Alert: ATR Low (50 bars)")

4 Calculation Methods: RMA (Wilder's), SMA, EMA, and WMA

Fully Customizable:

Adjustable ATR period (default: 14)

Variable lookback window (default: 50)

Toggle features on/off via intuitive input settings

How It Works

The indicator scans volatility extremes using proprietary logic:

Calculates True Range using selected method (RMA/SMA/EMA/WMA)

Compares current ATR value against historical data

Flags critical moments when:

Volatility contracts to N-period lows (prepare for breakouts)

Volatility expands to N-period highs (watch for trend exhaustion)

Strategic Applications

markdown

复制

| SIGNAL | MARKET CONDITION | TRADING IMPLICATION |

|------------------|-----------------------|--------------------------------|

| Low Volatility | Contraction/Consolidation | Anticipate breakout moves |

| High Volatility | Expansion/Climax | Prepare for reversals or pauses |

Position Sizing: Use ATR values to determine optimal stop distances

Entry Timing: Combine with price action at key support/resistance

Risk Management: Adjust stops dynamically based on volatility regime

Optimization Guide

Day Trading: Short lookback (20-30 periods)

Swing Trading: Medium lookback (50-100 periods)

Position Trading: Long lookback (100-200 periods)

Volatility Analysis: Compare multiple timeframes simultaneously

Professional Setup Recommendations

Combine with:

Breakout Confirmation: Volume spikes, chart patterns

Reversal Signals: RSI divergence, candlestick reversals

Volatility Filters: Bollinger Band contraction, Keltner Channel breakout

Compatibility: Works flawlessly across FX, stocks, crypto, and commodities on all timeframes.

Why Traders Choose This Indicator

"Transforms complex volatility analysis into clear, actionable visual cues – the essential tool for breakout traders and risk managers alike."

Install Now to:

Spot consolidation before big moves

Identify exhaustion at trend extremes

Automate volatility-based position sizing

Receive instant alerts at critical volatility turns

Master market rhythms with professional-grade volatility intelligence!

Info TableOverview

The Info Table V1 is a versatile TradingView indicator tailored for intraday futures traders, particularly those focusing on MESM2 (Micro E-mini S&P 500 futures) on 1-minute charts. It presents essential market insights through two customizable tables: the Main Table for predictive and macro metrics, and the New Metrics Table for momentum and volatility indicators. Designed for high-activity sessions like 9:30 AM–11:00 AM CDT, this tool helps traders assess price alignment, sentiment, and risk in real-time. Metrics update dynamically (except weekly COT data), with optional alerts for key conditions like volatility spikes or momentum shifts.

This indicator builds on foundational concepts like linear regression for predictions and adapts open-source elements for enhanced functionality. Gradient code is adapted from TradingView's Color Library. QQE logic is adapted from LuxAlgo's QQE Weighted Oscillator, licensed under CC BY-NC-SA 4.0. The script is released under the Mozilla Public License 2.0.

Key Features

Two Customizable Tables: Positioned independently (e.g., top-right for Main, bottom-right for New Metrics) with toggle options to show/hide for a clutter-free chart.

Gradient Coloring: User-defined high/low colors (default green/red) for quick visual interpretation of extremes, such as overbought/oversold or high volatility.

Arrows for Directional Bias: In the New Metrics Table, up (↑) or down (↓) arrows appear in value cells based on metric thresholds (top/bottom 25% of range), indicating bullish/high or bearish/low conditions.

Consensus Highlighting: The New Metrics Table's title cells ("Metric" and "Value") turn green if all arrows are ↑ (strong bullish consensus), red if all are ↓ (strong bearish consensus), or gray otherwise.

Predicted Price Plot: Optional line (default blue) overlaying the ML-predicted price for visual comparison with actual price action.

Alerts: Notifications for high/low Frahm Volatility (≥8 or ≤3) and QQE Bias crosses (bullish/bearish momentum shifts).

Main Table Metrics

This table focuses on predictive, positional, and macro insights:

ML-Predicted Price: A linear regression forecast using normalized price, volume, and RSI over a customizable lookback (default 500 bars). Gradient scales from low (red) to high (green) relative to the current price ± threshold (default 100 points).

Deviation %: Percentage difference between current price and predicted price. Gradient highlights extremes (±0.5% default threshold), signaling potential overextensions.

VWAP Deviation %: Percentage difference from Volume Weighted Average Price (VWAP). Gradient indicates if price is above (green) or below (red) fair value (±0.5% default).

FRED UNRATE % Change: Percentage change in U.S. unemployment rate (via FRED data). Cell turns red for increases (economic weakness), green for decreases (strength), gray if zero or disabled.

Open Interest: Total open MESM2 futures contracts. Gradient scales from low (red) to high (green) up to a hardcoded 300,000 threshold, reflecting market participation.

COT Commercial Long/Short: Weekly Commitment of Traders data for commercial positions. Long cell green if longs > shorts (bullish institutional sentiment); Short cell red if shorts > longs (bearish); gray otherwise.

New Metrics Table Metrics

This table emphasizes technical momentum and volatility, with arrows for quick bias assessment:

QQE Bias: Smoothed RSI vs. trailing stop (default length 14, factor 4.236, smooth 5). Green for bullish (RSI > stop, ↑ arrow), red for bearish (RSI < stop, ↓ arrow), gray for neutral.

RSI: Relative Strength Index (default period 14). Gradient from oversold (red, <30 + threshold offset, ↓ arrow if ≤40) to overbought (green, >70 - offset, ↑ arrow if ≥60).

ATR Volatility: Score (1–20) based on Average True Range (default period 14, lookback 50). High scores (green, ↑ if ≥15) signal swings; low (red, ↓ if ≤5) indicate calm.

ADX Trend: Average Directional Index (default period 14). Gradient from weak (red, ↓ if ≤0.25×25 threshold) to strong trends (green, ↑ if ≥0.75×25).

Volume Momentum: Score (1–20) comparing current to historical volume (lookback 50). High (green, ↑ if ≥15) suggests pressure; low (red, ↓ if ≤5) implies weakness.

Frahm Volatility: Score (1–20) from true range over a window (default 24 hours, multiplier 9). Dynamic gradient (green/red/yellow); ↑ if ≥7.5, ↓ if ≤2.5.

Frahm Avg Candle (Ticks): Average candle size in ticks over the window. Blue gradient (or dynamic green/red/yellow); ↑ if ≥0.75 percentile, ↓ if ≤0.25.

Arrows trigger on metric-specific logic (e.g., RSI ≥60 for ↑), providing directional cues without strict color ties.

Customization Options

Adapt the indicator to your strategy:

ML Inputs: Lookback (10–5000 bars) and RSI period (2+) for prediction sensitivity—shorter for volatility, longer for trends.

Timeframes: Individual per metric (e.g., 1H for QQE Bias to match higher frames; blank for chart timeframe).

Thresholds: Adjust gradients and arrows (e.g., Deviation 0.1–5%, ADX 0–100, RSI overbought/oversold).

QQE Settings: Length, factor, and smooth for fine-tuned momentum.

Data Toggles: Enable/disable FRED, Open Interest, COT for focus (e.g., disable macro for pure intraday).

Frahm Options: Window hours (1+), scale multiplier (1–10), dynamic colors for avg candle.

Plot/Table: Line color, positions, gradients, and visibility.

Ideal Use Case

Perfect for MESM2 scalpers and trend traders. Use the Main Table for entry confirmation via predicted deviations and institutional positioning. Leverage the New Metrics Table arrows for short-term signals—enter bullish on green consensus (all ↑), avoid chop on low volatility. Set alerts to catch shifts without constant monitoring.

Why It's Valuable

Info Table V1 consolidates diverse metrics into actionable visuals, answering critical questions: Is price mispriced? Is momentum aligning? Is volatility manageable? With real-time updates, consensus highlights, and extensive customization, it enhances precision in fast markets, reducing guesswork for confident trades.

Note: Optimized for futures; some metrics (OI, COT) unavailable on non-futures symbols. Test on demo accounts. No financial advice—use at your own risk.

The provided script reuses open-source elements from TradingView's Color Library and LuxAlgo's QQE Weighted Oscillator, as noted in the script comments and description. Credits are appropriately given in both the description and code comments, satisfying the requirement for attribution.

Regarding significant improvements and proportion:

The QQE logic comprises approximately 15 lines of code in a script exceeding 400 lines, representing a small proportion (<5%).

Adaptations include integration with multi-timeframe support via request.security, user-customizable inputs for length, factor, and smooth, and application within a broader table-based indicator for momentum bias display (with color gradients, arrows, and alerts). This extends the original QQE beyond standalone oscillator use, incorporating it as one of seven metrics in the New Metrics Table for confluence analysis (e.g., consensus highlighting when all metrics align). These are functional enhancements, not mere stylistic or variable changes.

The Color Library usage is via official import (import TradingView/Color/1 as Color), leveraging built-in gradient functions without copying code, and applied to enhance visual interpretation across multiple metrics.

The script complies with the rules: reused code is minimal, significantly improved through integration and expansion, and properly credited. It qualifies for open-source publication under the Mozilla Public License 2.0, as stated.

Multi-Crypto Principal Component AnalysisVersion 0.2

## 📌 Multi-Crypto Principal Component Analysis (PCA) — Indicator Summary

### 🎯 Purpose

This indicator identifies **cryptocurrency assets that are behaving differently** from the rest of the market, using a simplified approach inspired by Principal Component Analysis (PCA). It’s designed to help traders spot **cross-market divergences**, detect outliers, and improve asset selection and correlation-based strategies.

### ⚙️ How It Works

The indicator analyzes the **log returns** of up to 7 user-defined assets over a configurable lookback period (default: 100 bars). It computes the **z-score** (standardized deviation) for each asset’s return series and compares it against the average behavior of the group.

If an asset’s behavior deviates significantly (beyond a threshold of 1.5 standard deviations), it’s flagged as an **outlier**.

- Each outlier is plotted as a **colored dot horizontally spaced** above the price bar

- Up to **3 dots per bar** are shown for visual clarity

This PCA-style detection works in real time, directly on the chart, and gives you a quick overview of which assets are breaking correlation.

### 🔧 Inputs

- 🕒 **Lookback Period**: Number of bars to analyze (default: 100)

- 🔢 **Assets 1–7**: Choose any 7 crypto symbols from any exchange

- 🎨 **Colors**: Predefined per asset (e.g. BTCUSDT = red, ETHUSDT = yellow)

- 📈 **Threshold**: Internal (1.5 std dev); adjustable in code if needed

### 📊 Outputs

- 🟢 Dots above candles representing assets that are acting as outliers

- 🧠 Real-time clustering insight based on statistical deviation

- 🧭 Spatially spaced dots to avoid visual overlap when multiple outliers appear

### ⚠️ Limitations

- This is a **PCA-inspired approximation**, not true matrix-based PCA

- It does **not compute principal components or eigenvectors**

- Sensitivity may vary with asset volatility or sparse trading data

- Real PCA requires external tools like Python or R for full dimensional analysis

This tool is ideal for traders who want real-time crypto correlation insights without needing external data science platforms. It’s lightweight, fast, and highly visual — and gives you a powerful lens into market dislocations across multiple assets.

Contrarian Market Structure BreakMarket Structure Break application was inspired and adapted from Market Structure Oscillator indicator developed by Lux Algo. So much credit to their work.

This indicator pairs nicely with the Contrarian 100 MA and can be located here:

Indicator Description: Contrarian Market Structure BreakOverview

The "Contrarian Market Structure Break" indicator is a versatile tool tailored for traders seeking to identify potential reversal opportunities by analyzing market structure across multiple timeframes. Built on Institutional Concepts of Structure (ICT), this indicator detects Break of Structure (BOS) and Change of Character (CHoCH) patterns across short-term, intermediate-term, and long-term swings, plotting them with customizable lines and labels. It generates contrarian buy and sell signals when price breaks key swing levels, with a unique "Blue Dot Tracker" to monitor consecutive buy signals for trend confirmation. Optimized for the daily timeframe, this indicator is adaptable to other timeframes with proper testing, making it ideal for traders of forex, stocks, or cryptocurrencies.

How It Works

The indicator combines three key components to provide a comprehensive view of market dynamics: Multi-Timeframe Market Structure Analysis: It identifies swing highs and lows across short-term, intermediate-term, and long-term periods, plotting BOS (continuation) and CHoCH (reversal) events with customizable line styles and labels.

Contrarian Signal Generation: Buy and sell signals are triggered when the price crosses below swing lows (buy) or above swing highs (sell), indicating potential reversals in overextended markets.

Blue Dot Tracker: A unique feature that counts consecutive buy signals ("blue dots") and highlights a "Hold Investment" state with a yellow background when three or more buy signals occur, suggesting a potential trend continuation.

Signals are visualized as small circles below (buy) or above (sell) price bars, and a table in the bottom-right corner displays the blue dot count and recommended action (Hold or Flip Investment), enhancing decision-making clarity.

Mathematical Concepts Swing Detection: The indicator identifies swing highs and lows by comparing price patterns over three bars, ensuring robust detection of pivot points. A swing high occurs when the middle bar’s high is higher than the surrounding bars, and a swing low occurs when the middle bar’s low is lower.

Market Structure Logic: BOS is detected when the price breaks a prior swing high (bullish) or low (bearish) in the direction of the current trend, while CHoCH signals a potential reversal when the price breaks a swing level against the trend. These are calculated across three timeframes for a multi-dimensional perspective.

Blue Dot Tracker: This feature counts consecutive buy signals and tracks the entry price. If three or more buy signals occur without a sell signal, the indicator enters a "Hold Investment" state, marked by a yellow background, until the price exceeds the entry price or a sell signal occurs.

Entry and Exit Rules Buy Signal (Blue Dot Below Bar): Triggered when the closing price crosses below a swing low on either the intermediate-term or long-term timeframe, suggesting an oversold condition and potential reversal upward. Short-term signals can be enabled but are disabled by default to reduce noise.

Sell Signal (White Dot Above Bar): Triggered when the closing price crosses above a swing high on either the intermediate-term or long-term timeframe, indicating an overbought condition and potential reversal downward.

Blue Dot Tracker Logic: After a buy signal, the indicator increments a blue dot counter and records the entry price. If three or more consecutive buy signals occur (blueDotCount ≥ 3), the indicator enters a "Hold Investment" state, highlighted with a yellow background, suggesting a potential trend continuation. The "Hold Investment" state ends when the price exceeds the entry price or a sell signal occurs, resetting the counter.

Exit Rules: Traders can exit buy positions when a sell signal appears, the price exceeds the entry price during a "Hold Investment" state, or based on additional confirmation from BOS/CHoCH patterns or other technical analysis tools. Always use proper risk management.

Recommended Usage

The indicator is optimized for the daily timeframe, where it effectively captures significant reversal and continuation patterns in trending or ranging markets. It can be adapted to other timeframes (e.g., 1H, 4H, 15M) with careful testing of settings, particularly enabling/disabling short-term structure analysis to suit market conditions. Backtesting is recommended to optimize performance for your chosen asset and timeframe.

Customization Options Market Structure Display: Toggle short-term, intermediate-term, and long-term structures on or off, with customizable line styles (solid, dashed, dotted) and colors for bullish and bearish breaks.

Labels: Enable or disable BOS/CHoCH labels for each timeframe to reduce chart clutter.

Signal Visibility: Hide buy/sell signals if desired for a cleaner chart.

Blue Dot Tracker: Monitor the blue dot count and action (Hold or Flip Investment) via the table display, which is fully customizable in terms of position and appearance.

Why Use This Indicator?

The "Contrarian Market Structure Break" indicator offers a robust framework for identifying high-probability reversal and continuation setups using ICT principles. Its multi-timeframe analysis, clear signal visualization, and innovative Blue Dot Tracker provide traders with actionable insights into market dynamics. Whether you're a swing trader or a day trader, this indicator’s flexibility and intuitive design make it a valuable addition to your trading arsenal.

Note for TradingView Moderators

This script complies with TradingView's House Rules by providing an educational and transparent description without performance claims or guarantees. It is designed to assist traders in technical analysis and should be used alongside proper risk management and personal research. The code is original, well-documented, and includes customizable inputs and clear visual outputs to enhance the user experience.

Tips for Users:

Backtest thoroughly on your chosen asset and timeframe to validate signal reliability. Combine with other indicators or price action analysis for confirmation of entries and exits. Adjust timeframe settings and enable/disable short-term structures to match market volatility and your trading style.

Hope the "Contrarian Market Structure Break" indicator enhances your trading strategy and helps you navigate the markets with confidence! Happy trading!

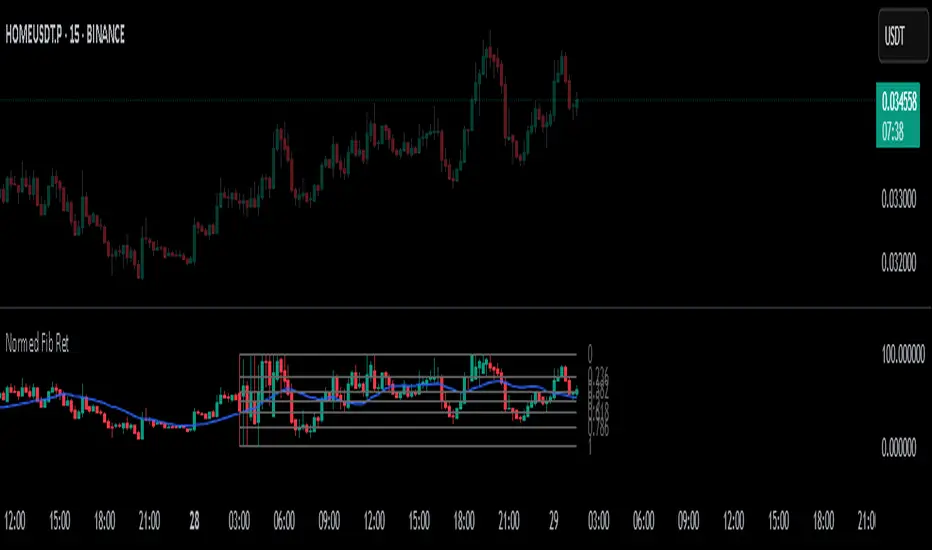

Normalized Fibonacci Retracement (MTF/LOG)A question: Instead of creating indicators that constantly plot Fibonacci Retracement levels in a visually overwhelming way, why don't we redefine them on a different scale? 🤨

Overview

The Normalized Fibonacci Retracement indicator converts price data to a 0-100 scale based on the selected timeframe's high-low range, displaying normalized candlesticks alongside standard Fibonacci levels (23.6%, 38.2%, 50%, 61.8%, 78.6%). This normalization reveals patterns that may be hidden in absolute price charts and allows consistent analysis across different instruments.

Originality

By normalizing prices to percentages, this indicator enables pattern recognition independent of absolute price levels. The same formation at $10-$20 and $1000-$2000 appears identical on the normalized scale, helping traders identify recurring structures across various assets and timeframes.

Concepts

The indicator uses a simple formula to transform price data into percentages. This creates a bounded scale where patterns become comparable regardless of the underlying asset's price range. The normalized view often reveals symmetries and relationships not visible in traditional price charts.

Mechanics

The system tracks highs and lows within the selected timeframe as anchor points. When a new period begins, fresh boundaries are established and prices recalculated. Trend direction is determined by timing of extremes. Linear scaling uses direct percentage calculation, while logarithmic scaling applies exponential interpolation for assets with large percentage moves.

Functions

Timeframe Selection: Higher timeframe analysis on any chart resolution

Normalized Display: OHLC data converted to 0-100 percentage scale

Fibonacci Levels: Standard retracement levels plotted automatically

Scaling Options: Linear or logarithmic calculation methods

Pattern Recognition: Reveals formations hidden in absolute price charts

Moving Average: Optional 20-period SMA overlay

Notes

Ensure chart data covers the full selected timeframe for accurate calculations. Use logarithmic scaling for volatile assets with large percentage moves. The normalized scale is effective at revealing patterns and structures that remain consistent across different price ranges, making it particularly useful for comparative analysis and pattern-based trading strategies.

I hope it helps everyone. Do not forget to manage your risk. And trade as safely as possible. Best of luck!

VoVix DEVMA🌌 VoVix DEVMA: A Deep Dive into Second-Order Volatility Dynamics

Welcome to VoVix+, a sophisticated trading framework that transcends traditional price analysis. This is not merely another indicator; it is a complete system designed to dissect and interpret the very fabric of market volatility. VoVix+ operates on the principle that the most powerful signals are not found in price alone, but in the behavior of volatility itself. It analyzes the rate of change, the momentum, and the structure of market volatility to identify periods of expansion and contraction, providing a unique edge in anticipating major market moves.

This document will serve as your comprehensive guide, breaking down every mathematical component, every user input, and every visual element to empower you with a profound understanding of how to harness its capabilities.

🔬 THEORETICAL FOUNDATION: THE MATHEMATICS OF MARKET DYNAMICS

VoVix+ is built upon a multi-layered mathematical engine designed to measure what we call "second-order volatility." While standard indicators analyze price, and first-order volatility indicators (like ATR) analyze the range of price, VoVix+ analyzes the dynamics of the volatility itself. This provides insight into the market's underlying state of stability or chaos.

1. The VoVix Score: Measuring Volatility Thrust

The core of the system begins with the VoVix Score. This is a normalized measure of volatility acceleration or deceleration.

Mathematical Formula:

VoVix Score = (ATR(fast) - ATR(slow)) / (StDev(ATR(fast)) + ε)

Where:

ATR(fast) is the Average True Range over a short period, representing current, immediate volatility.

ATR(slow) is the Average True Range over a longer period, representing the baseline or established volatility.

StDev(ATR(fast)) is the Standard Deviation of the fast ATR, which measures the "noisiness" or consistency of recent volatility.

ε (epsilon) is a very small number to prevent division by zero.

Market Implementation:

Positive Score (Expansion): When the fast ATR is significantly higher than the slow ATR, it indicates a rapid increase in volatility. The market is "stretching" or expanding.

Negative Score (Contraction): When the fast ATR falls below the slow ATR, it indicates a decrease in volatility. The market is "coiling" or contracting.

Normalization: By dividing by the standard deviation, we normalize the score. This turns it into a standardized measure, allowing us to compare volatility thrust across different market conditions and timeframes. A score of 2.0 in a quiet market means the same, relatively, as a score of 2.0 in a volatile market.

2. Deviation Analysis (DEV): Gauging Volatility's Own Volatility

The script then takes the analysis a step further. It calculates the standard deviation of the VoVix Score itself.

Mathematical Formula:

DEV = StDev(VoVix Score, lookback_period)

Market Implementation:

This DEV value represents the magnitude of chaos or stability in the market's volatility dynamics. A high DEV value means the volatility thrust is erratic and unpredictable. A low DEV value suggests the change in volatility is smooth and directional.

3. The DEVMA Crossover: Identifying Regime Shifts

This is the primary signal generator. We take two moving averages of the DEV value.

Mathematical Formula:

fastDEVMA = SMA(DEV, fast_period)

slowDEVMA = SMA(DEV, slow_period)

The Core Signal:

The strategy triggers on the crossover and crossunder of these two DEVMA lines. This is a profound concept: we are not looking at a moving average of price or even of volatility, but a moving average of the standard deviation of the normalized rate of change of volatility.

Bullish Crossover (fastDEVMA > slowDEVMA): This signals that the short-term measure of volatility's chaos is increasing relative to the long-term measure. This often precedes a significant market expansion and is interpreted as a bullish volatility regime.

Bearish Crossunder (fastDEVMA < slowDEVMA): This signals that the short-term measure of volatility's chaos is decreasing. The market is settling down or contracting, often leading to trending moves or range consolidation.

⚙️ INPUTS MENU: CONFIGURING YOUR ANALYSIS ENGINE

Every input has been meticulously designed to give you full control over the strategy's behavior. Understanding these settings is key to adapting VoVix+ to your specific instrument, timeframe, and trading style.

🌀 VoVix DEVMA Configuration

🧬 Deviation Lookback: This sets the lookback period for calculating the DEV value. It defines the window for measuring the stability of the VoVix Score. A shorter value makes the system highly reactive to recent changes in volatility's character, ideal for scalping. A longer value provides a smoother, more stable reading, better for identifying major, long-term regime shifts.

⚡ Fast VoVix Length: This is the lookback period for the fastDEVMA. It represents the short-term trend of volatility's chaos. A smaller number will result in a faster, more sensitive signal line that reacts quickly to market shifts.

🐌 Slow VoVix Length: This is the lookback period for the slowDEVMA. It represents the long-term, baseline trend of volatility's chaos. A larger number creates a more stable, slower-moving anchor against which the fast line is compared.

How to Optimize: The relationship between the Fast and Slow lengths is crucial. A wider gap (e.g., 20 and 60) will result in fewer, but potentially more significant, signals. A narrower gap (e.g., 25 and 40) will generate more frequent signals, suitable for more active trading styles.

🧠 Adaptive Intelligence

🧠 Enable Adaptive Features: When enabled, this activates the strategy's performance tracking module. The script will analyze the outcome of its last 50 trades to calculate a dynamic win rate.

⏰ Adaptive Time-Based Exit: If Enable Adaptive Features is on, this allows the strategy to adjust its Maximum Bars in Trade setting based on performance. It learns from the average duration of winning trades. If winning trades tend to be short, it may shorten the time exit to lock in profits. If winners tend to run, it will extend the time exit, allowing trades more room to develop. This helps prevent the strategy from cutting winning trades short or holding losing trades for too long.

⚡ Intelligent Execution

📊 Trade Quantity: A straightforward input that defines the number of contracts or shares for each trade. This is a fixed value for consistent position sizing.

🛡️ Smart Stop Loss: Enables the dynamic stop-loss mechanism.

🎯 Stop Loss ATR Multiplier: Determines the distance of the stop loss from the entry price, calculated as a multiple of the current 14-period ATR. A higher multiplier gives the trade more room to breathe but increases risk per trade. A lower multiplier creates a tighter stop, reducing risk but increasing the chance of being stopped out by normal market noise.

💰 Take Profit ATR Multiplier: Sets the take profit target, also as a multiple of the ATR. A common practice is to set this higher than the Stop Loss multiplier (e.g., a 2:1 or 3:1 reward-to-risk ratio).

🏃 Use Trailing Stop: This is a powerful feature for trend-following. When enabled, instead of a fixed stop loss, the stop will trail behind the price as the trade moves into profit, helping to lock in gains while letting winners run.

🎯 Trail Points & 📏 Trail Offset ATR Multipliers: These control the trailing stop's behavior. Trail Points defines how much profit is needed before the trail activates. Trail Offset defines how far the stop will trail behind the current price. Both are based on ATR, making them fully adaptive to market volatility.

⏰ Maximum Bars in Trade: This is a time-based stop. It forces an exit if a trade has been open for a specified number of bars, preventing positions from being held indefinitely in stagnant markets.

⏰ Session Management

These inputs allow you to confine the strategy's trading activity to specific market hours, which is crucial for day trading instruments that have defined high-volume sessions (e.g., stock market open).

🎨 Visual Effects & Dashboard

These toggles give you complete control over the on-chart visuals and the dashboard. You can disable any element to declutter your chart or focus only on the information that matters most to you.

📊 THE DASHBOARD: YOUR AT-A-GLANCE COMMAND CENTER

The dashboard centralizes all critical information into one compact, easy-to-read panel. It provides a real-time summary of the market state and strategy performance.

🎯 VOVIX ANALYSIS

Fast & Slow: Displays the current numerical values of the fastDEVMA and slowDEVMA. The color indicates their direction: green for rising, red for falling. This lets you see the underlying momentum of each line.

Regime: This is your most important environmental cue. It tells you the market's current state based on the DEVMA relationship. 🚀 EXPANSION (Green) signifies a bullish volatility regime where explosive moves are more likely. ⚛️ CONTRACTION (Purple) signifies a bearish volatility regime, where the market may be consolidating or entering a smoother trend.

Quality: Measures the strength of the last signal based on the magnitude of the DEVMA difference. An ELITE or STRONG signal indicates a high-conviction setup where the crossover had significant force.

PERFORMANCE

Win Rate & Trades: Displays the historical win rate of the strategy from the backtest, along with the total number of closed trades. This provides immediate feedback on the strategy's historical effectiveness on the current chart.

EXECUTION

Trade Qty: Shows your configured position size per trade.

Session: Indicates whether trading is currently OPEN (allowed) or CLOSED based on your session management settings.

POSITION

Position & PnL: Displays your current position (LONG, SHORT, or FLAT) and the real-time Profit or Loss of the open trade.

🧠 ADAPTIVE STATUS

Stop/Profit Mult: In this simplified version, these are placeholders. The primary adaptive feature currently modifies the time-based exit, which is reflected in how long trades are held on the chart.

🎨 THE VISUAL UNIVERSE: DECIPHERING MARKET GEOMETRY

The visuals are not mere decorations; they are geometric representations of the underlying mathematical concepts, designed to give you an intuitive feel for the market's state.

The Core Lines:

FastDEVMA (Green/Maroon Line): The primary signal line. Green when rising, indicating an increase in short-term volatility chaos. Maroon when falling.

SlowDEVMA (Aqua/Orange Line): The baseline. Aqua when rising, indicating a long-term increase in volatility chaos. Orange when falling.

🌊 Morphism Flow (Flowing Lines with Circles):

What it represents: This visualizes the momentum and strength of the fastDEVMA. The width and intensity of the "beam" are proportional to the signal strength.

Interpretation: A thick, steep, and vibrant flow indicates powerful, committed momentum in the current volatility regime. The floating '●' particles represent kinetic energy; more particles suggest stronger underlying force.

📐 Homotopy Paths (Layered Transparent Boxes):

What it represents: These layered boxes are centered between the two DEVMA lines. Their height is determined by the DEV value.

Interpretation: This visualizes the overall "volatility of volatility." Wider boxes indicate a chaotic, unpredictable market. Narrower boxes suggest a more stable, predictable environment.

🧠 Consciousness Field (The Grid):

What it represents: This grid provides a historical lookback at the DEV range.

Interpretation: It maps the recent "consciousness" or character of the market's volatility. A consistently wide grid suggests a prolonged period of chaos, while a narrowing grid can signal a transition to a more stable state.

📏 Functorial Levels (Projected Horizontal Lines):

What it represents: These lines extend from the current fastDEVMA and slowDEVMA values into the future.

Interpretation: Think of these as dynamic support and resistance levels for the volatility structure itself. A crossover becomes more significant if it breaks cleanly through a prior established level.

🌊 Flow Boxes (Spaced Out Boxes):

What it represents: These are compact visual footprints of the current regime, colored green for Expansion and red for Contraction.

Interpretation: They provide a quick, at-a-glance confirmation of the dominant volatility flow, reinforcing the background color.

Background Color:

This provides an immediate, unmistakable indication of the current volatility regime. Light Green for Expansion and Light Aqua/Blue for Contraction, allowing you to assess the market environment in a split second.

📊 BACKTESTING PERFORMANCE REVIEW & ANALYSIS

The following is a factual, transparent review of a backtest conducted using the strategy's default settings on a specific instrument and timeframe. This information is presented for educational purposes to demonstrate how the strategy's mechanics performed over a historical period. It is crucial to understand that these results are historical, apply only to the specific conditions of this test, and are not a guarantee or promise of future performance. Market conditions are dynamic and constantly change.

Test Parameters & Conditions

To ensure the backtest reflects a degree of real-world conditions, the following parameters were used. The goal is to provide a transparent baseline, not an over-optimized or unrealistic scenario.

Instrument: CME E-mini Nasdaq 100 Futures (NQ1!)

Timeframe: 5-Minute Chart

Backtesting Range: March 24, 2024, to July 09, 2024

Initial Capital: $100,000

Commission: $0.62 per contract (A realistic cost for futures trading).

Slippage: 3 ticks per trade (A conservative setting to account for potential price discrepancies between order placement and execution).

Trade Size: 1 contract per trade.

Performance Overview (Historical Data)

The test period generated 465 total trades , providing a statistically significant sample size for analysis, which is well above the recommended minimum of 100 trades for a strategy evaluation.

Profit Factor: The historical Profit Factor was 2.663 . This metric represents the gross profit divided by the gross loss. In this test, it indicates that for every dollar lost, $2.663 was gained.

Percent Profitable: Across all 465 trades, the strategy had a historical win rate of 84.09% . While a high figure, this is a historical artifact of this specific data set and settings, and should not be the sole basis for future expectations.

Risk & Trade Characteristics

Beyond the headline numbers, the following metrics provide deeper insight into the strategy's historical behavior.

Sortino Ratio (Downside Risk): The Sortino Ratio was 6.828 . Unlike the Sharpe Ratio, this metric only measures the volatility of negative returns. A higher value, such as this one, suggests that during this test period, the strategy was highly efficient at managing downside volatility and large losing trades relative to the profits it generated.

Average Trade Duration: A critical characteristic to understand is the strategy's holding period. With an average of only 2 bars per trade , this configuration operates as a very short-term, or scalping-style, system. Winning trades averaged 2 bars, while losing trades averaged 4 bars. This indicates the strategy's logic is designed to capture quick, high-probability moves and exit rapidly, either at a profit target or a stop loss.

Conclusion and Final Disclaimer

This backtest demonstrates one specific application of the VoVix+ framework. It highlights the strategy's behavior as a short-term system that, in this historical test on NQ1!, exhibited a high win rate and effective management of downside risk. Users are strongly encouraged to conduct their own backtests on different instruments, timeframes, and date ranges to understand how the strategy adapts to varying market structures. Past performance is not indicative of future results, and all trading involves significant risk.

🔧 THE DEVELOPMENT PHILOSOPHY: FROM VOLATILITY TO CLARITY

The journey to create VoVix+ began with a simple question: "What drives major market moves?" The answer is often not a change in price direction, but a fundamental shift in market volatility. Standard indicators are reactive to price. We wanted to create a system that was predictive of market state. VoVix+ was designed to go one level deeper—to analyze the behavior, character, and momentum of volatility itself.

The challenge was twofold. First, to create a robust mathematical model to quantify these abstract concepts. This led to the multi-layered analysis of ATR differentials and standard deviations. Second, to make this complex data intuitive and actionable. This drove the creation of the "Visual Universe," where abstract mathematical values are translated into geometric shapes, flows, and fields. The adaptive system was intentionally kept simple and transparent, focusing on a single, impactful parameter (time-based exits) to provide performance feedback without becoming an inscrutable "black box." The result is a tool that is both profoundly deep in its analysis and remarkably clear in its presentation.

⚠️ RISK DISCLAIMER AND BEST PRACTICES

VoVix+ is an advanced analytical tool, not a guarantee of future profits. All financial markets carry inherent risk. The backtesting results shown by the strategy are historical and do not guarantee future performance. This strategy incorporates realistic commission and slippage settings by default, but market conditions can vary. Always practice sound risk management, use position sizes appropriate for your account equity, and never risk more than you can afford to lose. It is recommended to use this strategy as part of a comprehensive trading plan. This was developed specifically for Futures

"The prevailing wisdom is that markets are always right. I take the opposite view. I assume that markets are always wrong. Even if my assumption is occasionally wrong, I use it as a working hypothesis."

— George Soros

— Dskyz, Trade with insight. Trade with anticipation.

Multy Dynamic POCThis script displays up to 4 independent Point of Control (POC) levels based on volume profile logic.

📌 Each POC can be configured individually:

Period options: Daily (D), Weekly (W), Monthly (M), or BARS (rolling bar window).

Dynamic recalculation when the period changes (e.g., new day/week/month or custom bar count).

Price-anchored lines for each POC level that scale correctly with the chart.

Customizable line color and thickness.

🔍 How it works:

For each active POC line, the script builds a simple volume distribution based on the candle’s average price (hl2) and volume.

The price range is split into 100 buckets. The one with the highest accumulated volume is selected as the Point of Control (POC).

In BARS mode, POC is recalculated every N bars. In D/W/M modes, it resets exactly at the beginning of a new period (according to TradingView’s time() function).

✅ Useful for:

Traders applying volume profile analysis without needing the full built-in volume profile tool.

Spotting dynamic high-volume zones in trends or ranges.

Strategy development or confirmation around high-interest price levels.

_______________________________________________________________________________

Данный индикатор отображает до 4 независимых уровней Point of Control (POC), рассчитанных по объёмам.

📌 Каждый POC можно настраивать отдельно:

Периоды: День (D), Неделя (W), Месяц (M) или BARS (скользящее окно по количеству баров).

Автоматический пересчёт при смене периода (например, новый день, неделя или месяц).

Линии POC привязаны к цене и масштабируются вместе с графиком.

Настраиваемый цвет и толщина линий.

🔍 Как работает:

Для каждой активной линии POC создаётся объёмное распределение: берется средняя цена свечи (hl2) и объем.

Диапазон цен делится на 100 уровней. Тот, где накоплено больше всего объёма, и есть POC.

В режиме BARS уровень пересчитывается каждые N баров. В режимах D/W/M — строго в начале нового периода.

✅ Подходит для:

Трейдеров, использующих объёмный анализ, но не имеющих платной подписки на Volume Profile.

Поиска уровней интереса и подтверждения сигналов.

Разработки стратегий с опорой на объём.

Position Size Calculator with Fees# Position Size Calculator with Portfolio Management - Manual

## Overview

The Position Size Calculator with Portfolio Management is an advanced Pine Script indicator designed to help traders calculate optimal position sizes based on their total portfolio value and risk management strategy. This tool automatically calculates your risk amount based on portfolio allocation percentages and determines the exact position size needed while accounting for trading fees.

## Key Features

- **Portfolio-Based Risk Management**: Calculates risk based on total portfolio value

- **Tiered Risk Allocation**: Separates trading allocation from total portfolio

- **Automatic Trade Direction Detection**: Determines long/short based on entry vs stop loss

- **Fee Integration**: Accounts for trading fees in position size calculations

- **Risk Factor Adjustment**: Allows scaling of position size up or down

- **Visual Display**: Shows all calculations in a clear, color-coded table

- **Automatic Risk Calculation**: No need to manually input risk amount

## Input Parameters

### Total Portfolio ($)

- **Purpose**: The total value of your investment portfolio

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If your total portfolio is worth $100,000, enter 100000

### Trading Portfolio Allocation (%)

- **Purpose**: The percentage of your total portfolio allocated to active trading

- **Default**: 20.0%

- **Range**: 0.0% to 100.0%

- **Step**: 0.01

- **Example**: If you allocate 20% of your portfolio to trading, enter 20

### Risk from Trading (%)

- **Purpose**: The percentage of your trading allocation you're willing to risk per trade

- **Default**: 0.1%

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If you risk 0.1% of your trading allocation per trade, enter 0.1

### Entry Price ($)

- **Purpose**: The price at which you plan to enter the trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Stop Loss ($)

- **Purpose**: The price at which you will exit if the trade goes against you

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk Factor

- **Purpose**: A multiplier to scale your position size up or down

- **Default**: 1.0 (no scaling)

- **Range**: 0.0 to 10.0

- **Step**: 0.1

- **Examples**:

- 1.0 = Normal position size

- 2.0 = Double the position size

- 0.5 = Half the position size

### Fee (%)

- **Purpose**: The percentage fee charged per transaction

- **Default**: 0.01% (0.01)

- **Range**: 0.0% to 1.0%

- **Step**: 0.001

## How Risk Amount is Calculated

The script automatically calculates your risk amount using this formula:

```

Risk Amount = Total Portfolio × Trading Allocation (%) × Risk % ÷ 10,000

```

### Example Calculation:

- Total Portfolio: $100,000

- Trading Allocation: 20%

- Risk per Trade: 0.1%

**Risk Amount = $100,000 × 20 × 0.1 ÷ 10,000 = $20**

This means you would risk $20 per trade, which is 0.1% of your $20,000 trading allocation.

## Portfolio Structure Example

Let's say you have a $100,000 portfolio:

### Allocation Structure:

- **Total Portfolio**: $100,000

- **Trading Allocation (20%)**: $20,000

- **Long-term Investments (80%)**: $80,000

### Risk Management:

- **Risk per Trade (0.1% of trading)**: $20

- **Maximum trades at risk**: Could theoretically have 1,000 trades before risking entire trading allocation

## How Position Size is Calculated

### Trade Direction Detection

- **Long Trade**: Entry price > Stop loss price

- **Short Trade**: Entry price < Stop loss price

### Position Size Formulas

#### For Long Trades:

```

Position Size = -Risk Factor × Risk Amount / (Stop Loss × (1 - Fee) - Entry Price × (1 + Fee))

```

#### For Short Trades:

```

Position Size = -Risk Factor × Risk Amount / (Entry Price × (1 - Fee) - Stop Loss × (1 + Fee))

```

## Output Display

The indicator displays a comprehensive table with color-coded sections:

### Portfolio Information (Light Blue Background)

- **Portfolio (USD)**: Your total portfolio value

- **Trading Portfolio Allocation (%)**: Percentage allocated to trading

- **Risk as % of Trading**: Risk percentage per trade

### Trade Setup (Gray Background)

- **Entry Price**: Your specified entry price

- **Stop Loss**: Your specified stop loss price

- **Fee (%)**: Trading fee percentage

- **Risk Factor**: Position size multiplier

### Risk Analysis (Red Background)

- **Risk Amount**: Automatically calculated dollar risk

- **Effective Entry**: Actual entry cost including fees

- **Effective Exit**: Actual exit value including fees

- **Expected Loss**: Calculated loss if stop loss is hit

- **Deviation from Risk %**: Accuracy of risk calculation

### Final Result (Blue Background)

- **Position Size**: Number of shares/units to trade

## Usage Examples

### Example 1: Conservative Long Trade

- **Total Portfolio**: $50,000

- **Trading Allocation**: 15%

- **Risk per Trade**: 0.05%

- **Entry Price**: $25.00

- **Stop Loss**: $24.00

- **Risk Factor**: 1.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $50,000 × 15% × 0.05% ÷ 100 = $3.75

### Example 2: Aggressive Short Trade

- **Total Portfolio**: $200,000

- **Trading Allocation**: 30%

- **Risk per Trade**: 0.2%

- **Entry Price**: $150.00

- **Stop Loss**: $155.00

- **Risk Factor**: 2.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $200,000 × 30% × 0.2% ÷ 100 = $120

**Actual Risk**: $120 × 2.0 = $240 (due to risk factor)

## Color Coding System

- **Green/Red Header**: Trade direction (Long/Short)

- **Light Blue**: Portfolio management parameters

- **Gray**: Trade setup parameters

- **Red**: Risk-related calculations and results

- **Blue**: Final position size result

## Best Practices

### Portfolio Management

1. **Keep trading allocation reasonable** (typically 10-30% of total portfolio)

2. **Use conservative risk percentages** (0.05-0.2% per trade)

3. **Don't risk more than you can afford to lose**

### Risk Management

1. **Start with small risk factors** (1.0 or less) until comfortable

2. **Monitor your total exposure** across all open positions

3. **Adjust risk based on market conditions**

### Trade Execution

1. **Always validate calculations** before placing trades

2. **Account for slippage** in volatile markets

3. **Consider position size relative to liquidity**

## Risk Management Guidelines

### Conservative Approach

- Trading Allocation: 10-20%

- Risk per Trade: 0.05-0.1%

- Risk Factor: 0.5-1.0

### Moderate Approach

- Trading Allocation: 20-30%

- Risk per Trade: 0.1-0.15%

- Risk Factor: 1.0-1.5

### Aggressive Approach

- Trading Allocation: 30-40%

- Risk per Trade: 0.15-0.25%

- Risk Factor: 1.5-2.0

## Troubleshooting

### Common Issues

1. **Position Size shows 0**

- Verify all portfolio inputs are greater than 0

- Check that entry price differs from stop loss

- Ensure calculated risk amount is positive

2. **Very small position sizes**

- Increase risk percentage or risk factor

- Check if your risk amount is too small for the price difference

3. **Large risk deviation**

- Normal for very small positions

- Consider adjusting entry/stop loss levels

### Validation Checklist

- Total portfolio value is realistic

- Trading allocation percentage makes sense

- Risk percentage is conservative

- Entry and stop loss prices are valid

- Trade direction matches your intention

## Advanced Features

### Risk Factor Usage

- **Scaling up**: Use risk factors > 1.0 for high-confidence trades

- **Scaling down**: Use risk factors < 1.0 for uncertain trades

- **Never exceed**: Risk factors that would risk more than your comfort level

### Multiple Timeframe Analysis

- Use different risk factors for different timeframes

- Consider correlation between positions

- Adjust trading allocation based on market conditions

## Disclaimer

This tool is for educational and planning purposes only. Always verify calculations manually and consider market conditions, liquidity, and correlation between positions. The automated risk calculation assumes you're comfortable with the mathematical relationship between portfolio allocation and individual trade risk. Past performance doesn't guarantee future results, and all trading involves risk of loss.

WRAMA Channel (Weighted RSI ATR MA)OVERVIEW

The WRAMA Channel (Weighted RSI ATR MA) is an advanced technical analysis tool designed to react more quickly to price movements compared to indicators using conventional moving averages. It combines the Relative Strength Index (RSI), Average True Range (ATR), and a weighted moving average, resulting in the WRAMA. This indicator forms a dynamic price channel based on a weighted average that incorporates both trend strength (via RSI) and market volatility (via ATR). It helps traders identify trends, potential reversals, and breakout signals, while offering broad customization options.

Key Features

WRAMA Price Channel:

Generates a dynamic channel around the weighted moving average (WRAMA), adapting to market volatility and momentum, similar to Bollinger Bands. Users are encouraged to adjust channel width and length according to their strategy.

The upper and lower channel bands are calculated based on a percentage deviation from the baseline line.

The channel fill color changes depending on the price's position relative to the baseline (green above, red below), with an optional gradient for better visualization.

Weighted Moving Average (WRAMA):

WRAMA is a custom weighted moving average (MA1), where closing prices are weighted based on RSI and ATR, allowing it to dynamically adapt to market conditions.

Baseline: The WRAMA line calculated over a user-defined period.

WRAMA Calculation:

RSI Weight: Based on RSI value. When RSI is in extreme zones (below the lower threshold or above the upper threshold), an extreme weight is applied. Otherwise, the weight is based on the squared RSI value divided by 100, raised to a power defined by the rsi_weight_factor.

ATR Weight: Based on the ATR-to-average-ATR ratio. If ATR exceeds a threshold (atr_threshold × avg_atr), an extreme weight is applied. Otherwise, the weight is based on the squared ratio of ATR to average ATR, raised to the power of the atr_weight_factor.

Combined Weight: RSI and ATR weights are combined using a rsi_atr_balance parameter. Final weight = RSI weight × balance + ATR weight × (1 - balance).

WRAMA Calculation: The closing price is multiplied by the combined weight. The result is averaged over the ma_length period and divided by the average of the weights, forming the WRAMA line. For current WRAMA (ma_length = 1), the calculation simplifies to a single weighted price.

Additional Moving Averages:

For additional confirmations, the indicator supports up to five moving averages (MA1–MA5) with various types (SMA, EMA, WMA, HMA, ALMA) and customizable periods.

All additional MAs are calculated based on WRAMA or its baseline, ensuring consistency and enabling deeper analysis within a unified methodology. MA trend directions can be tracked in a built-in signal table.

Trading Signals:

Breakout Signals: Breakouts above/below the channel are optionally marked with triangle shapes (green for bullish, red for bearish).

MA Signals: Price position relative to MAs or their slope generates bullish/bearish signals. These are optionally visualized with default triangles (green up, red down).

A signal table in the top-right corner summarizes the status of each moving average – bullish, bearish, or neutral.

Customization Options

Channel Settings:

MA Period: Length of the WRAMA baseline (default: 100).

Channel Deviation : Percentage offset from the baseline for upper/lower bands (default: 1.5%).

RSI Settings:

RSI Period: Length of the RSI calculation (default: 14).

RSI Upper/Lower Threshold: Overbought/oversold levels (default: 70/30).

RSI Weight Factor: Influence of RSI on weighting (default: 2.0).

ATR Settings:

ATR Period: ATR calculation length (default: 14).

ATR Threshold: Volatility threshold as a multiple of average ATR (default: 1.5).

ATR Weight Factor: Influence of ATR on weighting (default: 2.0).

RSI & ATR Combined:

Extreme Weight: Weight applied in extreme RSI/ATR conditions (default: 3.0).

RSI/ATR Balance: Balance between RSI and ATR influence (default: 0.5).

Signal Settings:

Show Breakout Signals: Enable/disable breakout triangles.

Show MA Signals: Enable/disable MA-based signals.

MA Signal Source: Choose between current WRAMA or baseline.

MA Signal Analysis: Based on price position or slope.

Neutral Threshold : Minimum distance from MA for signal neutrality (default: 0.5%).

Minimum MA Slope : Minimum slope for trend direction signals (default: 0.01%).

Moving Averages (MA1–MA5):

Options to enable/disable, select type (SMA, EMA, WMA, HMA, ALMA), set period length, and choose color.

Style Settings:

Gradient Fill: Enable/disable gradient coloring within the channel.

Show Baseline: Enable/disable WRAMA baseline visibility.

Colors: Customize line, fill, and signal colors.

Use Cases

Trend Identification: The WRAMA channel highlights trend direction and potential reversal zones when price contacts the channel edges.

Breakout Signals: Channel breakouts may indicate trend shifts or momentum surges.

MA Analysis: The signal table provides a clear summary of market direction (bullish, bearish, or neutral) based on selected moving averages.

Trading Strategies: Suitable for trend-following, mean-reversion, and scalping strategies, depending on user preferences and settings.

Notes

The indicator offers a high degree of flexibility, making it adaptable to various trading styles, instruments, and timeframes.

It is recommended to adjust channel length and width to fit your trading strategy.

Backtesting settings on historical data is advised to optimize parameters for a specific strategy and market.

Candle Emotion Oscillator [CEO]Candle Emotion Oscillator (CEO) - Revolutionary User Guide

🧠 World's First Market Psychology Oscillator

The Candle Emotion Oscillator (CEO) is a groundbreaking indicator that measures market emotions through pure candle price action analysis. This is the first oscillator ever created that translates candle patterns into psychological states, giving you unprecedented insight into market sentiment.

🚀 Revolutionary Concept

What Makes CEO Unique

100% Pure Price Action: No volume, no external data - just candle analysis

Market Psychology: Measures actual emotions: Fear, Greed, Panic, Euphoria

Never Been Done Before: First oscillator to analyze market emotions

Exhaustion Prediction: Detects emotional fatigue before reversals

Fast Response: Perfect for your 2-5 minute scalping setup

The Four Core Emotions

🟢 GREED (Positive Values)

What it measures: Market conviction and decisiveness

Candle Pattern: Large bodies, small wicks

Psychology: Traders are confident and decisive

Oscillator: Positive values (0 to +100)

Trading Implication: Trend continuation likely

🔴 FEAR (Negative Values)

What it measures: Market uncertainty and indecision

Candle Pattern: Small bodies, large wicks

Psychology: Traders are uncertain and hesitant

Oscillator: Negative values (0 to -100)

Trading Implication: Consolidation or reversal likely

🚀 EUPHORIA (Extreme Positive)

What it measures: Excessive optimism and buying pressure

Candle Pattern: Large green bodies with upper wicks

Psychology: Extreme bullish sentiment

Oscillator: Values above +60

Trading Implication: Overbought, reversal warning

💥 PANIC (Extreme Negative)

What it measures: Capitulation and selling pressure

Candle Pattern: Large red bodies with lower wicks

Psychology: Extreme bearish sentiment

Oscillator: Values below -60

Trading Implication: Oversold, reversal opportunity

📊 Visual Elements Explained

Main Components

Thick Colored Line: Primary emotion oscillator

Green: Greed (positive emotions)