G&S SMT### Description of the Pine Script

This Pine Script is designed to identify **Smart Money Technique (SMT)** setups between **Gold (GC1!)** and **Silver (SI1!) Futures** on a **15-minute timeframe**. It specifically looks for divergences between the price movements of Gold and Silver over the last 4 candles and compares it with the next candle's price movement. The script provides **Bullish** and **Bearish** signals for SMT during a specified time range of **8:45 AM EST to 10:30 AM EST**.

### Key Features of the Script:

1. **Futures Symbols**:

- The script uses **Gold Futures (GC1!)** and **Silver Futures (SI1!)** on a 15-minute timeframe to monitor their price movements.

2. **Time Range Filtering**:

- The signals are only active between **8:45 AM EST and 10:30 AM EST**, ensuring that the script only signals within the most relevant trading hours for your strategy.

3. **SMT Calculation (Last 4 Candles vs Next Candle)**:

- **Gold and Silver Price Change Calculation**: The script compares the price changes of **Gold** and **Silver** over the **last 4 candles** and then compares them with the price movement of the **next candle**:

- **Bullish SMT**: Occurs when Gold shows an increase in the last 4 candles while Silver shows a decrease, and both Gold and Silver show an increase in the next candle.

- **Bearish SMT**: Occurs when Gold shows a decrease in the last 4 candles while Silver shows an increase, and both Gold and Silver show a decrease in the next candle.

4. **Bullish and Bearish Signals**:

- **Bullish SMT Signal**: The script will plot a **green** arrow below the bar when a Bullish SMT setup is identified.

- **Bearish SMT Signal**: A **red** arrow above the bar is plotted when a Bearish SMT setup is identified.

5. **Gold and Silver Difference Plot**:

- The difference between the prices of **Gold** and **Silver** is plotted as a **blue line**, giving a visual representation of the relationship between the two assets. When the difference line moves significantly, it can indicate a potential divergence or convergence in the prices of Gold and Silver.

### Script Logic Breakdown:

1. **Price Change for Last 4 Candles**:

- The script calculates the price change for Gold and Silver from the 4th-to-last candle to the last candle.

- `gold_change_last4` and `silver_change_last4` calculate these price differences.

2. **Price Change for Next Candle**:

- It then calculates the price change from the last candle to the next candle.

- `gold_change_next` and `silver_change_next` calculate these price differences.

3. **Bullish SMT Condition**:

- If Gold increased while Silver decreased in the last 4 candles, and both Gold and Silver show an increase in the next candle, it indicates a **Bullish SMT**.

4. **Bearish SMT Condition**:

- If Gold decreased while Silver increased in the last 4 candles, and both Gold and Silver show a decrease in the next candle, it indicates a **Bearish SMT**.

5. **Time Filter**:

- Signals are only plotted when the current time is between **8:45 AM EST and 10:30 AM EST** to match your preferred trading hours.

### Visualization:

- **Bullish Signals**: Plotted as **green arrows** below the bars when a Bullish SMT setup is identified.

- **Bearish Signals**: Plotted as **red arrows** above the bars when a Bearish SMT setup is identified.

- **Gold - Silver Difference**: A **blue line** is plotted to show the price difference between Gold and Silver, helping visualize any divergence.

### How It Helps:

- **Divergence Identification**: This script highlights potential divergences between Gold and Silver Futures, which can provide insights into market sentiment and smart money movements.

- **Focus on Relevant Time Frame**: By filtering signals between 8:45 AM EST and 10:30 AM EST, you are focusing on a timeframe that can be more beneficial for trading.

- **Visual Clarity**: The arrows and the price difference line provide clear signals and a visual representation of the relationship between Gold and Silver, helping you make informed trading decisions.

This script is an automated approach to detecting **SMT setups** and helping traders recognize when Gold and Silver might be signaling a bullish or bearish move based on their divergence patterns.

Cari skrip untuk "机械革命无界15+时不时闪屏"

Options Series - Anchored VWAP Ribbon➤ AVWAP On different chart symbols:

⭐ Overview and Key Features:

Anchored VWAP Calculation:

The script implements the Anchored Volume Weighted Average Price (AVWAP), a tool used by professional traders to identify key price levels weighted by volume, starting from a specific timestamp (anchor point).

Bullish and Bearish Analysis:

It determines the dominance of bullish or bearish momentum based on the relationship between the close price and AVWAP levels across multiple time points.

Dynamic Visualization:

The background of the chart changes color based on overall bullish or bearish sentiment, making it easier to interpret market trends.

Multi-Time Anchors:

By defining multiple anchor points (e.g., 09:15, 09:20), the script calculates a series of AVWAP values for fine-grained intraday analysis.

Customizable Inputs:

Users can select the source price (e.g., hlc3), date, and time for AVWAP calculation.

⭐ How It Works and Functionality:

AVWAP Logic:

Uses the timestamp() function to establish a reference (anchor point).

Calculates the cumulative weighted price (price * volume) and cumulative volume from this anchor point.

The ratio of these sums gives the AVWAP, which updates dynamically with new bars.

Bullish and Bearish Signals:

Binary flags (1 or 0) are set for each time point depending on whether the closing price is above or below the AVWAP for that time.

Aggregates these flags into AVWAP_bull and AVWAP_bear to represent the overall market sentiment.

Decision Logic:

Determines final market conditions (bullish or bearish dominance) based on aggregated scores.

Visual feedback (background and bar colors) is applied accordingly.

⭐ Visualizations and User Experience:

Background Colors:

Green or red background highlights the overall sentiment (bullish or bearish), providing a quick market overview.

Bar Coloring:

Bars are color-coded based on bullish, bearish, or neutral conditions, making it easier to identify trends directly on the chart.

AVWAP Levels:

The calculated AVWAP values are plotted as colored lines for each anchor point, giving precise intraday levels of significance.

Bright colors (fluorescent green/red) are used for additional clarity when the close price is above or below these levels.

🎨 Settings and Customization:

Anchor Point:

Fully customizable anchor points allow users to set specific dates and times (e.g., 09:15 on December 13, 2024) for AVWAP calculations.

Source Price:

Users can choose from hlc3, close, or any other price source to calculate the AVWAP, tailoring the indicator to their strategy.

Visual Appearance:

The transparency, colors, and line styles are adjustable, enabling users to customize the chart to match their trading preferences.

Dynamic Signals:

The script accommodates numerous AVWAP levels, providing flexibility for scalpers and swing traders alike.

⭐ Uniqueness of the Concept:

Precise Intraday Analysis:

Unlike static VWAP, this script allows anchoring to specific times during the day, offering granular insights into market behavior.

Cumulative Sentiment Approach:

Aggregates signals across multiple time intervals, providing a comprehensive view of intraday momentum rather than a single-point reference.

Blending AVWAP with Visual Feedback:

Combines traditional AVWAP calculations with visually impactful features like background shading and bar coloring to enhance decision-making.

Scalability:

Supports adding multiple additional anchor points and customization for broader applicability in different market conditions.

🚀 Conclusion:

The Anchored VWAP Ribbon script is a powerful tool for traders seeking to analyze price behavior relative to volume-weighted levels anchored at specific times. It provides a visually intuitive way to assess intraday market sentiment, combining traditional technical indicators with customizable visualization features. The script’s flexibility makes it suitable for a variety of trading styles, from scalping to swing trading, while its unique cumulative sentiment logic sets it apart from conventional VWAP tools.

R-based Strategy Template [Daveatt]Have you ever wondered how to properly track your trading performance based on risk rather than just profits?

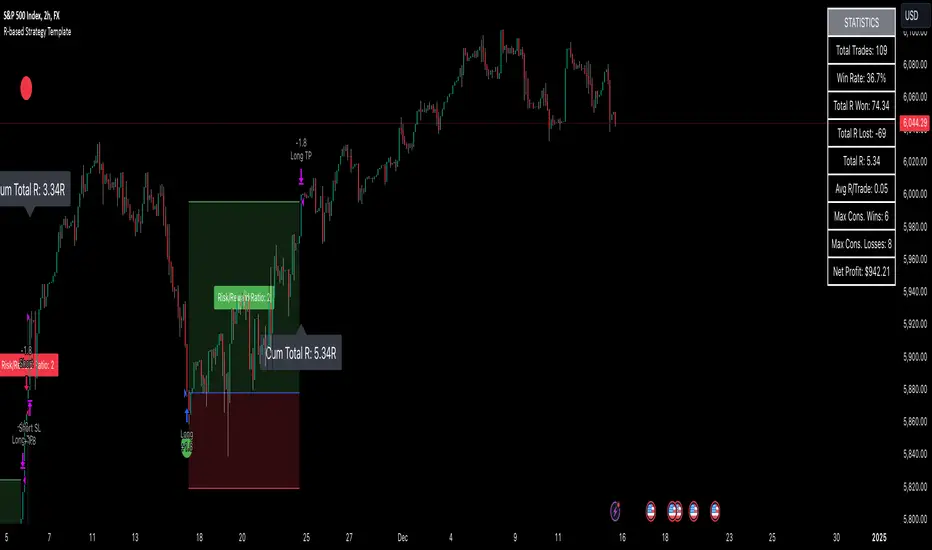

This template solves that problem by implementing R-multiple tracking directly in TradingView's strategy tester.

This script is a tool that you must update with your own trading entry logic.

Quick notes

Before we dive in, I want to be clear: this is a template focused on R-multiple calculation and visualization.

I'm using a basic RSI strategy with dummy values just to demonstrate how the R tracking works. The actual trading signals aren't important here - you should replace them with your own strategy logic.

R multiple logic

Let's talk about what R-multiple means in practice.

Think of R as your initial risk per trade.

For instance, if you have a $10,000 account and you're risking 1% per trade, your 1R would be $100.

A trade that makes twice your risk would be +2R ($200), while hitting your stop loss would be -1R (-$100).

This way of measuring makes it much easier to evaluate your strategy's performance regardless of account size.

Whenever the SL is hit, we lose -1R

Proof showing the strategy tester whenever the SL is hit: i.imgur.com

The magic happens in how we calculate position sizes.

The script automatically determines the right position size to risk exactly your specified percentage on each trade.

This is done through a simple but powerful calculation:

risk_amount = (strategy.equity * (risk_per_trade_percent / 100))

sl_distance = math.abs(entry_price - sl_price)

position_size = risk_amount / (sl_distance * syminfo.pointvalue)

Limitations with lower timeframe gaps

This ensures that if your stop loss gets hit, you'll lose exactly the amount you intended to risk. No more, no less.

Well, could be more or less actually ... let's assume you're trading futures on a 15-minute chart but in the 1-minute chart there is a gap ... then your 15 minute SL won't get filled and you'll likely to not lose exactly -1R

This is annoying but it can't be fixed - and that's how trading works anyway.

Features

The template gives you flexibility in how you set your stop losses. You can use fixed points, ATR-based stops, percentage-based stops, or even tick-based stops.

Regardless of which method you choose, the position sizing will automatically adjust to maintain your desired risk per trade.

To help you track performance, I've added a comprehensive statistics table in the top right corner of your chart.

It shows you everything you need to know about your strategy's performance in terms of R-multiples: how many R you've won or lost, your win rate, average R per trade, and even your longest winning and losing streaks.

Happy trading!

And remember, measuring your performance in R-multiples is one of the most classical ways to evaluate and improve your trading strategies.

Daveatt

Trend Stability Index (TSI)Overview

The Trend Stability Index (TSI) is a technical analysis tool designed to evaluate the stability of a market trend by analyzing both price movements and trading volume. By combining these two crucial elements, the TSI provides traders with insights into the strength and reliability of ongoing trends, assisting in making informed trading decisions.

Key Features

• Dual Analysis: Integrates price changes and volume fluctuations to assess trend stability.

• Customizable Periods: Allows users to set evaluation periods for both trend and volume based on their trading preferences.

• Visual Indicators: Displays the Trend Stability Index as a line chart, highlights neutral zones, and uses background colors to indicate trend stability or instability.

Configuration Settings

1. Trend Length (trendLength)

• Description: Determines the number of periods over which the price stability is evaluated.

• Default Value: 15

• Usage: A longer trend length smooths out short-term volatility, providing a clearer picture of the overarching trend.

2. Volume Length (volumeLength)

• Description: Sets the number of periods over which trading volume changes are assessed.

• Default Value: 15

• Usage: Adjusting the volume length helps in capturing significant volume movements that may influence trend strength.

Calculation Methodology

The Trend Stability Index is calculated through a series of steps that analyze both price and volume changes:

1. Price Change Rate (priceChange)

• Calculation: Utilizes the Rate of Change (ROC) function on the closing prices over the specified trendLength.

• Purpose: Measures the percentage change in price over the trend evaluation period, indicating the direction and momentum of the price movement.

2. Volume Change Rate (volumeChange)

• Calculation: Applies the Rate of Change (ROC) function to the trading volume over the specified volumeLength.

• Purpose: Assesses the percentage change in trading volume, providing insight into the conviction behind price movements.

3. Trend Stability (trendStability)

• Calculation: Multiplies priceChange by volumeChange.

• Purpose: Combines price and volume changes to gauge the overall stability of the trend. A higher positive value suggests a strong and stable trend, while negative values may indicate trend weakness or reversal.

4. Trend Stability Index (TSI)

• Calculation: Applies a Simple Moving Average (SMA) to the trendStability over the trendLength period.

• Purpose: Smooths the trend stability data to create a more consistent and interpretable index.

Trend/Ranging Determination

• Stable Trend (isStable)

• Condition: When the TSI value is greater than 0.

• Interpretation: Indicates that the current trend is stable and likely to continue in its direction.

• Unstable Trend / Range-bound Market

• Condition: When the TSI value is less than or equal to 0.

• Interpretation: Suggests that the trend may be weakening, reversing, or that the market is moving sideways without a clear direction.

Visualization

The TSI indicator employs several visual elements to convey information effectively:

1. TSI Line

• Representation: Plotted as a blue line.

• Purpose: Displays the Trend Stability Index values over time, allowing traders to observe trend stability dynamics.

2. Neutral Horizontal Line

• Representation: A gray horizontal line at the 0 level.

• Purpose: Serves as a reference point to distinguish between stable and unstable trends.

3. Background Color

• Stable Trend: Green background with 80% transparency when isStable is true.

• Unstable Trend: Red background with 80% transparency when isStable is false.

• Purpose: Provides an immediate visual cue about the current trend’s stability, enhancing the interpretability of the indicator.

Usage Guidelines

• Identifying Trend Strength: Utilize the TSI to confirm the strength of existing trends. A consistently positive TSI suggests strong trend momentum, while a negative TSI may signal caution or a potential reversal.

• Volume Confirmation: The integration of volume changes helps in validating price movements. Significant price changes accompanied by corresponding volume shifts can reinforce the reliability of the trend.

• Entry and Exit Signals: Traders can use crossovers of the TSI with the neutral line (0 level) as potential entry or exit points. For instance, a crossover from below to above 0 may indicate a bullish trend initiation, while a crossover from above to below 0 could suggest bearish momentum.

• Combining with Other Indicators: To enhance trading strategies, consider using the TSI in conjunction with other technical indicators such as Moving Averages, RSI, or MACD for comprehensive market analysis.

Example Scenario

Imagine analyzing a stock with the following observations using the TSI:

• The TSI has been consistently above 0 for the past 30 periods, accompanied by increasing trading volume. This scenario indicates a strong and stable uptrend, suggesting that buying opportunities may be favorable.

• Conversely, if the TSI drops below 0 while the price remains relatively flat and volume decreases, it may imply that the current trend is losing momentum, and the market could be entering a consolidation phase or preparing for a trend reversal.

Conclusion

The Trend Stability Index is a valuable tool for traders seeking to assess the reliability and strength of market trends by integrating price and volume dynamics. Its customizable settings and clear visual indicators make it adaptable to various trading styles and market conditions. By incorporating the TSI into your trading analysis, you can enhance your ability to identify and act upon stable and profitable trends.

Cabal Dev IndicatorThis is a TradingView Pine Script (version 6) that creates a technical analysis indicator called the "Cabal Dev Indicator." Here's what it does:

1. Core Functionality:

- It calculates a modified version of the Stochastic Momentum Index (SMI), which is a momentum indicator that shows where the current close is relative to the high/low range over a period

- The indicator combines elements of stochastic oscillator calculations with exponential moving averages (EMA)

2. Key Components:

- Uses configurable input parameters for:

- Percent K Length (default 15)

- Percent D Length (default 3)

- EMA Signal Length (default 15)

- Smoothing Period (default 5)

- Overbought level (default 40)

- Oversold level (default -40)

3. Calculation Method:

- Calculates the highest high and lowest low over the specified period

- Finds the difference between current close and the midpoint of the high-low range

- Applies EMA smoothing to both the range and relative differences

- Generates an SMI value and further smooths it using a simple moving average (SMA)

- Creates an EMA signal line based on the smoothed SMI

4. Visual Output:

- Plots the smoothed SMI line in green

- Plots an EMA signal line in red

- Shows overbought and oversold levels as gray horizontal lines

- Fills the areas above the overbought level with light red

- Fills the areas below the oversold level with light green

This indicator appears designed to help traders identify potential overbought and oversold conditions in the market, as well as momentum shifts, which could be used for trading decisions.

Would you like me to explain any specific part of the indicator in more detail?

Engulfing bar detectorHere’s the updated description with the added step about using Fibonacci levels across timeframes for confirmation:

Liquidity Engulfing Bar Detector

The **Liquidity Engulfing Bar Detector** is a powerful tool designed for traders who want to identify high-probability reversal patterns in the market based on liquidity grabbing and price action. This indicator highlights **Bullish Engulfing** and **Bearish Engulfing** bars that fulfill specific liquidity criteria, helping you spot potential trend reversals and trading opportunities.

**Features**:

1. **Bullish Engulfing Bars**:

- The current candle's low dips below the previous candle's low (grabs liquidity).

- The current candle closes above the previous candle's open.

- A green label is plotted above the engulfing bar for easy identification.

2. **Bearish Engulfing Bars**:

- The current candle's high exceeds the previous candle's high (grabs liquidity).

- The current candle closes below the previous candle's open.

- A red label is plotted below the engulfing bar for clear visibility.

3. **Customizable Alerts**:

- Receive instant notifications via TradingView alerts when a bullish or bearish engulfing pattern is detected.

- Alerts are fully customizable, allowing you to stay updated without actively monitoring the chart.

4. **Visual Markers**:

- Clear and intuitive labels make it easy to spot key patterns directly on your chart.

- Fully integrated with any timeframe and market, ensuring versatility for all trading styles.

---

### **How to Use**:

1. **Add the Indicator**:

- Apply the Liquidity Engulfing Bar Detector to your chart to automatically highlight bullish and bearish engulfing bars.

2. **Enable Alerts**:

- Set up TradingView alerts to get notified of potential setups in real-time.

3. **Analyze with Fibonacci Levels**:

- Draw a Fibonacci retracement tool over the identified engulfing bar, from its low to its high (for bullish patterns) or high to low (for bearish patterns).

- Use the following Fibonacci levels as key zones of interest:

- **0.0 (start)**, **0.25**, **0.5 (midpoint)**, **0.75**, and **1.0 (end)**.

- These levels often act as critical support or resistance zones for price action.

4. **Use Multi-Timeframe Confirmation**:

- Validate zones from higher timeframes using lower timeframe candles:

- **1-minute candles** for confirming zones on the **15-minute chart**.

- **5-minute candles** for confirming zones on the **1-hour chart**.

- **15-minute candles** for confirming zones on the **4-hour chart**.

- This approach ensures precision in your entry points and aligns intraday movements with higher timeframe setups.

5. **Integrate with Your Strategy**:

- Combine the indicator with other tools (e.g., trendlines, moving averages, or volume analysis) for confirmation.

- Use proper risk management to maximize your trading edge.

---

### **Why Use This Indicator?**

Liquidity grabs often signal the participation of major market players, which can lead to significant reversals or continuations. By combining liquidity concepts with engulfing bar patterns and Fibonacci analysis, this indicator helps you:

- Identify key market turning points.

- Improve your entries and exits with multi-timeframe precision.

- Enhance your trading strategy with an edge rooted in smart money concepts.

---

**Note**: This indicator is best used with proper risk management and alongside other technical or fundamental analyses.

---

Let me know if there's anything more you'd like to include!

ICT Macro Sessions by @zeusbottradingICT Macro Sessions Indicator

The ICT Macro Sessions Indicator is a powerful tool designed for traders who follow the ICT (Inner Circle Trader) methodology and want to optimize their trading during specific high-probability time intervals. This indicator highlights all the key macro sessions throughout the trading day in the GMT+8 (Hong Kong) time zone.

What Does the Indicator Do?

This indicator visually marks ICT Macro Sessions on your trading chart using background colors and optional labels. Each session corresponds to specific time intervals when institutional activity is most likely to drive price action. By focusing on these periods, traders can align their strategies with market volatility and liquidity, increasing their chances of success.

Highlighted Sessions

The indicator covers all major ICT Macro Sessions, each with a unique color for easy identification:

London Macro 1 (15:33–16:00 GMT+8):

- Marks the early London session, often characterized by strong directional moves.

London Macro 2 (17:03–17:30 GMT+8):

- Captures the mid-London session, where price frequently reacts to liquidity levels.

New York AM Macro 1 (22:50–23:10 GMT+8):

- Highlights the start of the New York session, a prime time for price reversals or continuations.

New York AM Macro 2 (23:50–00:10 GMT+8):

- Focuses on late-morning New York activity, often aligning with key news releases.

New York Lunch Macro (00:50–01:10 GMT+8):

- Covers the lunch period in New York, where price may consolidate or set up for afternoon moves.

New York PM Macro 1 (02:10–02:40 GMT+8):

- Tracks post-lunch activity in New York, often featuring renewed volatility.

New York PM Macro 2 (04:15–04:45 GMT+8):

- Captures late-session moves as institutional traders finalize their positions.

Features of the Indicator

Fixed Time: The indicator is pre-configured for GMT+8 but it will adapt automatically to your timezone. No need to change anything in the code.

Background Highlighting: Each session is visually marked with a unique background color for quick recognition.

Optional Labels: Traders can enable or disable labels for each session, providing flexibility in how information is displayed.

Session Toggles: You can choose which sessions to display based on your trading preferences and strategy.

Intraday Timeframes: The indicator is optimized for intraday charts with timeframes of 45 minutes or less. You can change it to anything you like.

Why Use This Indicator?

The ICT Macro Sessions Indicator helps traders focus on the most critical times of the trading day when institutional activity is at its peak. These periods often coincide with significant price movements, making them ideal for scalping, day trading, or even swing trading setups. By visually highlighting these sessions, the indicator eliminates guesswork and allows traders to plan their trades with precision.

4-Hour Moving AveragesTitle: 4-Hour Moving Averages Indicator

Description:

The "4-Hour Moving Averages" indicator is designed to help traders easily visualize key moving averages derived from the 4-hour timeframe, regardless of the chart interval they are using. This indicator plots four moving averages: a 15-period SMA (Short-Term), a 35-period SMA (Intermediate-Term), an 80-period SMA (Long-Term), and a 130-period SMA (Confirmation).

These moving averages provide a balanced approach for identifying short, medium, and long-term trends, as well as confirming significant market movements. Ideal for swing traders and those looking for clear trend signals, the indicator can be used for various markets, including stocks, forex, and cryptocurrencies.

The 4-hour moving averages overlay directly on the price chart, allowing for easy analysis of current price movements relative to important trend indicators. Use this script to enhance your trading decisions, identify opportunities, and avoid market traps by relying on consistent moving average trends.

Features:

- 15 SMA for Short-Term Trends (in red)

- 35 SMA for Intermediate-Term Trends (in orange)

- 80 SMA for Long-Term Trends (in green)

- 130 SMA for Confirmation (in blue)

Feel free to modify the settings to suit your specific strategy and market conditions.

Sessions ny vizScript Purpose

This indicator draws a colored background during the New York trading session. It's useful for traders who want to have a visual overview of when the American (NY) trading session is active.

Main Features

NY Session Visualization - draws a gray bar in the background of the chart during NY trading hours (15:00-19:00 CET)

Customization - allows users to:

Set custom session time range

Adjust background color and transparency

Limit display to only the last 24 hours

Input Parameters

sessionRange - session time range (default 15:00-19:00 CET)

sessionColour - background color (default gray with 90% transparency)

onlyLast24Hours - toggle for showing only the last 24 hours (default false)

Technical Details

Script is written in Pine Script version 5

Uses UNIX timestamp for time period calculations

Runs as an overlay indicator (overlay=true), meaning it displays directly on the price chart

Uses the bgcolor() function for background rendering

Contains logic to check if current time is within defined session

Usage

This indicator is useful for:

Monitoring active NY trading session hours

Planning trades during the most liquid hours of the US market

Visual orientation in the chart during different trading sessions

SMB MagicSMB Magic

Overview: SMB Magic is a powerful technical strategy designed to capture breakout opportunities based on price movements, volume spikes, and trend-following logic. This strategy works exclusively on the XAU/USD symbol and is optimized for the 15-minute time frame. By incorporating multiple factors, this strategy identifies high-probability trades with a focus on risk management.

Key Features:

Breakout Confirmation:

This strategy looks for price breakouts above the previous high or below the previous low, with a significant volume increase. A breakout is considered valid when it is supported by strong volume, confirming the strength of the price move.

Price Movement Filter:

The strategy ensures that only significant price movements are considered for trades, helping to avoid low-volatility noise. This filter targets larger price swings to maximize potential profits.

Exponential Moving Average (EMA):

A long-term trend filter is applied to ensure that buy trades occur only when the price is above the moving average, and sell trades only when the price is below it.

Fibonacci Levels:

Custom Fibonacci retracement levels are drawn based on recent price action. These levels act as dynamic support and resistance zones and help determine the exit points for trades.

Take Profit/Stop Loss:

The strategy incorporates predefined take profit and stop loss levels, designed to manage risk effectively. These levels are automatically applied to trades and are adjusted based on the market's volatility.

Volume Confirmation:

A volume multiplier confirms the strength of the breakout. A trade is only considered when the volume exceeds a certain threshold, ensuring that the breakout is supported by sufficient market participation.

How It Works:

Entry Signals:

Buy Signal: A breakout above the previous high, accompanied by significant volume and price movement, occurs when the price is above the trend-following filter (e.g., EMA).

Sell Signal: A breakout below the previous low, accompanied by significant volume and price movement, occurs when the price is below the trend-following filter.

Exit Strategy:

Each position (long or short) has predefined take-profit and stop-loss levels, which are designed to protect capital and lock in profits at key points in the market.

Fibonacci Levels:

Fibonacci levels are drawn to identify potential areas of support or resistance, which can be used to guide exits and stop-loss placements.

Important Notes:

Timeframe Restriction: This strategy is designed specifically for the 15-minute time frame.

Symbol Restriction: The strategy works exclusively on the XAU/USD (Gold) symbol and is not recommended for use with other instruments.

Best Performance in Trending Markets: It works best in trending conditions where breakouts occur frequently.

Disclaimer:

Risk Warning: Trading involves risk, and past performance is not indicative of future results. Always conduct your own research and make informed decisions before trading.

[Stuppieeeeeee] - Multiple vertical timeframes linesEnhance your trading experience with this intuitive indicator that displays vertical lines on your chart to mark the start of new bars in higher timeframes. Whether you're analyzing on a 5-minute chart or any other lower timeframe, this tool helps you visualize when significant periods begin on larger scales like hourly, daily, or even monthly charts.

Key Features:

Multiple Timeframes Supported: Choose from 5 minutes, 15 minutes, 1 hour, 4 hours, 12 hours, daily, weekly, and monthly timeframes to display vertical lines.

Customizable Appearance: Personalize each set of lines by adjusting their colors, including transparency levels, line styles (solid, dashed, dotted), and widths to suit your preferences and enhance visibility.

Automatic Visibility Management: The indicator intelligently hides lines for timeframes that are equal to or lower than your current chart timeframe, keeping your chart clean and focused.

Future Projection: Not only does it mark the start of current higher timeframe bars, but it also projects lines into the near future. This feature allows you to anticipate upcoming significant time intervals, aiding in better planning and decision-making.

Layer Control: You have the ability to control which lines appear above others. By adjusting the drawing order and using transparency settings, you ensure that all important lines are visible without cluttering your chart.

Benefits:

Enhanced Multi-Timeframe Analysis: Quickly identify when higher timeframe bars start while analyzing lower timeframe charts, helping you align your trades with significant market movements.

Improved Market Structure Understanding: Visual cues from the vertical lines aid in recognizing patterns and trends that span across different timeframes.

Strategic Planning: Anticipate key time intervals with future projection lines, allowing you to prepare for potential market shifts.

How to Use:

Apply the Indicator:

Add the indicator to your TradingView chart as you would with any other tool.

It's most effective when used on lower timeframe charts (like 5-minute or 15-minute charts) to display lines from higher timeframes.

Customize Settings:

Open the indicator's settings panel.

For each timeframe, adjust the line color, style, width, and transparency to your liking.

Set the transparency to allow underlying lines to show through if desired.

Interpret the Lines:

Vertical lines will appear at the start of new bars for the higher timeframes you've selected.

Use these visual markers to inform your entry and exit points, aligning them with larger market movements.

Pay attention to future lines to anticipate upcoming periods of interest.

Notes:

Performance Considerations: Displaying a large number of lines may impact chart performance. If you notice any lag, consider reducing the number of active timeframes or increasing line transparency.

TradingView Limitations: Be aware that TradingView limits the number of drawing objects on a chart. The indicator is designed to manage this, but extremely long timeframes or high bar counts might affect its operation.

Fibonacci Moving Average PlusFibonacci Moving Average Plus is a sophisticated technical indicator that employs the first 15 numbers of the Fibonacci sequence to create dynamic moving average channels. This indicator aims to capture both immediate and long-term price movements by calculating Exponential Moving Averages (EMAs) based on these Fibonacci values. By using Fibonacci-based moving averages for both high and low price points, the indicator generates a visual channel that reflects the ebb and flow of market trends, acting as potential zones of support and resistance. Additionally, the indicator provides midline, retracement, and extension levels rooted in Fibonacci ratios, which are frequently observed as key levels for reversals or trend continuation.

Ideology Behind Using Fibonacci Sequence-Based Moving Averages

The Fibonacci sequence, known for its mathematical harmony and prevalence in natural patterns, is widely utilized in technical analysis to identify potential turning points in markets. In this indicator, the first 15 Fibonacci numbers (5, 8, 13, 21, etc.) are used as the lookback periods for EMAs to capture different layers of market sentiment. These moving averages represent timeframes that are theoretically in alignment with the natural rhythms of market cycles, where key levels—often coinciding with Fibonacci numbers—can act as magnetic points for price.

The Fibonacci high and low channels aim to encapsulate price action, giving traders a sense of whether the market is trending, consolidating, or experiencing reversal pressure. These levels, grounded in both mathematics and market psychology, help traders spot areas where price might face resistance or find support.

Key Features

Fibonacci Moving Average High and Low: This indicator calculates the high and low EMAs based on Fibonacci sequence numbers (e.g., 5, 8, 13, etc.) for enhanced trend analysis.

Golden Pocket Retracement (GPR) and Extension (GPE) Bands: Displays common Fibonacci retracement and extension levels (0.618, 0.65 for retracement, and 1.618, 1.65 for extension).

Midline: Plots the average of the Fibonacci high and low to act as an additional reference level.

Stop-Loss Levels: Provides suggested stop-loss levels based on Fibonacci levels for both long and short positions.

Basic User Guide

Adjust Input Settings:

Input Timeframe: Set a specific timeframe for the Fibonacci moving average calculation, separate from the chart's primary timeframe.

Show Fibonacci MA High/Low: Toggle the visibility of the high and low Fibonacci moving averages.

Show Mid Line: Display a midline for added trend reference.

Show Golden Pocket Bands: Choose to display retracement or extension bands for potential support or resistance zones.

Show Stop-Loss Levels: Enable to visualize potential stop-loss levels for both long and short trades.

Interpretation:

Fibonacci MA High and Low: Use these lines to gauge the general trend. When the price is above both, it may indicate an uptrend; below both, a downtrend.

Golden Pocket Retracement: This zone (between 0.618 and 0.65) is often a key level for potential reversals or support/resistance.

Golden Pocket Extension: The 1.618 and 1.65 levels can indicate potential profit-taking or trend exhaustion points.

Stop-Loss Levels: The calculated stop-loss levels (long SL below and short SL above) can aid in risk management.

Customization:

You can customize the appearance and visibility of each component through the input settings to fit your specific strategy and visual preferences.

This indicator should be used alongside other technical analysis tools to provide a more comprehensive trading approach.

This Indicator would not exist without the original contributions and blessing from Sofien Kaabar

Screener MA CrossThe Screener MA Cross is an efficient tool designed to help traders quickly identify potential buy and sell signals across multiple currency pairs and timeframes. This script monitors the crossover behavior of two moving averages (MA8 and MA50) to determine possible entry points for trades.

Key Features:

Multi-Pair Monitoring: The indicator allows users to screen popular assets, including XAUUSD, US30, GBPUSD, EURUSD, USDJPY, USDCAD, and GBPJPY. You can add or remove symbols based on your preference.

Dual Timeframe Analysis: It tracks moving average crossovers on both 15-minute and 1-hour charts, giving users insights into short-term and medium-term trends without switching between timeframes.

Color-Coded Signals:

Green: Indicates a bullish "Buy" signal when the MA8 crosses above the MA50, suggesting upward momentum.

Red: Indicates a bearish "Sell" signal when the MA8 crosses below the MA50, signaling downward momentum.

Gray: Represents a neutral or no-cross state, indicating no clear trend.

Clean Table Format: Displays all relevant signals directly on your chart in a structured, easy-to-read table format, allowing you to quickly scan and assess trading opportunities.

How It Works: The script uses moving averages (MA8 and MA50) to analyze crossover patterns, a common method for identifying trend changes. A crossover occurs when a shorter moving average (MA8) crosses above or below a longer moving average (MA50). By requesting data from the 15-minute and 1-hour timeframes, the Screener MA Cross provides a clear overview of the market situation across various assets, helping you decide on potential trades.

This tool is particularly useful for trend-following strategies and can be used to spot momentum shifts on smaller timeframes, making it ideal for day traders and scalpers.

How to Use:

Add the indicator to your chart and customize the asset symbols to match your trading preferences.

Monitor the signals on the table. Green signals indicate potential buying opportunities, while red signals suggest possible selling points.

Use alongside other analysis: While the Screener MA Cross offers valuable insights, it's best used in combination with other indicators and analysis techniques to confirm trade setups.

[ETH] Optimized Trend Strategy - Lorenzo SuperScalpStrategy Title: Optimized Trend Strategy - Lorenzo SuperScalp

Description:

The Optimized Trend Strategy is a comprehensive trading system tailored for Ethereum (ETH) and optimized for the 15-minute timeframe but adaptable to various timeframes. This strategy utilizes a combination of technical indicators—RSI, Bollinger Bands, and MACD—to identify and act on price trends efficiently, providing traders with actionable buy and sell signals based on market conditions.

Key Features:

Multi-Indicator Approach:

RSI (Relative Strength Index): Identifies overbought and oversold conditions to time market entries and exits.

Bollinger Bands: Acts as a dynamic support and resistance level, helping to pinpoint precise entry and exit zones.

MACD (Moving Average Convergence Divergence): Detects momentum changes through bullish and bearish crossovers.

Signal Conditions:

Buy Signal:

RSI is below 45 (indicating an oversold condition).

Price is near or below the lower Bollinger Band.

MACD bullish crossover occurs.

Sell Signal:

RSI is above 55 (indicating an overbought condition).

Price is near or above the upper Bollinger Band.

MACD bearish crossunder occurs.

Trade Execution Logic:

Long Trades: Opened when a buy signal flashes. If there’s an open short position, it is closed before opening a long.

Short Trades: Opened when a sell signal flashes. If there’s an open long position, it is closed before opening a short.

The strategy also ensures a minimum number of bars between consecutive trades to avoid rapid trading in choppy conditions.

Pyramiding Support:

Up to 3 consecutive trades in the same direction are allowed, enabling traders to scale into positions based on strong signals.

Visual Indicators:

RSI Levels: Dotted lines at 45 and 55 for quick reference to oversold and overbought levels.

Buy and Sell Signals: Visual markers on the chart indicate where trades are executed, ensuring clarity on entry and exit points.

Best Used For:

Swing Trading & Scalping: While optimized for the 15-minute timeframe, this strategy works across various timeframes, making it suitable for both short-term scalping and swing trading.

Crypto Trading: Tailored for Ethereum but effective for other cryptocurrencies due to its dynamic indicator setup.

Range Tightening Indicator (RTI)The Range Tightening Indicator (RTI) quantifies price volatility relative to recent price action, helping traders identify low-volatility consolidations that often precede breakouts.

Range Tightening is calculated by measuring the range between each bar’s high and low prices over a chosen lookback period.

A 5-bar period is recommended for shorter-term momentum setups and a 15-bar period is recommended for swing trading. An option for a custom period is available to suit specific strategies. The default look back for custom is 50, ideal for longer term traders.

Other Key Features:

Dynamic Color Coding: The RTI line turns green when volatility doubles after a drop to or below 20, flagging significant volatility shifts commonly seen before breakouts.

Low-Volatility Dots: Orange dots appear on the RTI line when two or more consecutive bars show RTI values below 20, visually marking extended low-volatility periods.

Volatility Zones: Shaded zones provide quick context:

Zone 1 (0-5): Extremely tight volatility, shown in red.

Zone 2 (5-10): Low volatility, shown in light green.

Zone 3 (10-15): Moderate low volatility, shown in green.

The RTI indicator is ideal for traders looking to anticipate breakout conditions, with features that highlight consolidation phases, support momentum strategies, and help improve entry timing by focusing on shifts in volatility.

This indicator was inspired after Deepvue's RMV Indicator, but uses a different calculation. Results may vary.

Wave Anchor IndicatorThe Wave Anchor Indicator is designed to mark the crossing of overbought and oversold levels of higher time frame momentum waves, based on the VuManChu Cipher B+Divergences Wave Trend Indicator. This tool is inspired by the TP Mint trading strategy, which relies heavily on the momentum waves of Market Cipher B or VuManChu Cipher B for identifying optimal entry and exit points.

Key Concept: Anchored Waves

In the TP Mint strategy, momentum waves in overbought (above 60) or oversold (below -60) conditions on higher time frames are considered "anchored." These anchored waves provide strong signals for entries and take-profit points when viewed on lower time frames. The Wave Anchor Indicator focuses on these anchor conditions to help traders make informed decisions by seeing higher time frame anchor states directly on the entry time frame chart.

How It Works

Labeling Signals:

- On lower time frames, such as the 15-minute chart, the indicator shows labels when higher

time frame momentum waves (1-hour and 4-hour) cross the overbought or oversold levels.

- Labels above price indicate overbought conditions, with green labels when the wave crosses

upward and red labels when crossing downward.

- Labels below price signal oversold conditions, with red for a downward cross and green for an

upward cross.

- Each label displays the time frame of the crossing momentum wave, providing context for

traders at a glance.

Time Frame Pairings:

- On the 15-minute time frame, the indicator tracks anchor conditions from the 1-hour and 4-

hour time frames.

- On the 1-hour chart, it monitors 4-hour and daily time frame anchor conditions.

Customization and Alerts

Flexible Display Options : Users can choose to display none, one, or both of the grouped higher time frame labels, depending on their strategy and preferences.

Alerts : The indicator also allows for custom alerts when a label appears, helping traders stay on top of key market movements without constantly monitoring the chart.

Use Cases

This indicator is ideal for traders who use momentum-based strategies across multiple time frames. It simplifies the process of identifying key entry and exit points by focusing on the anchor conditions from higher time frames, making it easier to execute the TP Mint strategy or similar methods.

Thank you to VuManChu and LazyBear for mamking the momentum wave code open source and allowing it’s use in this indicator.

Japan Stock Market Indices Performance TableYou can display the performance of the Nikkei 225 Futures and major indices of the Japanese stock market for the day in a table format on your chart.

The 5-Minute Change Rate shows the change from the opening price of the most recent 5-minute candlestick.

The Daily Change Rate displays the change from the opening price at 09:00 GMT+9 on the current trading day.

Since the Japanese stock market opens at 09:00 GMT+9 , the values for Nikkei 225 Futures, USD/JPY, and EUR/JPY are also calculated based on their opening prices at that time. This script was created because, while brokerage apps allow you to see the comparison to the previous day's close for each index, they do not display the rate of change from the current day's opening price.

Notes:

All values are reset each trading day at 09:00 GMT+9.

If you have not purchased real-time market data from the Tokyo Stock Exchange and Osaka Exchange, data may be delayed by 20 minutes and may not display correctly.

The Tokyo Stock Exchange sector indices are distributed in real-time at 15-second intervals from the TSE, so this script aligns with that timing.

当日の日経225先物と日本株式市場の主要指数のパフォーマンスを表形式でチャート上に表示することができます。

5分変化率は直近の5分足の始値からの変化率、当日変化率は当日09:00の始値からの変化率を表示しています。

日本株式市場が開くのが GMT+9 09:00 のため、それに合わせて日経225先物、ドル円、ユーロ円も GMT+9 09:00 時点の始値を元に各値を算出しています。

各指数の前日比は証券会社のアプリで見れるものの、当日始値からの変化率が見れないため作成しました。

補足

各営業日の朝(GMT+9 09:00)に各値はリセットされます。

Tokyo Stock ExchangeとOsaka Exchangeのreal-time market dataを購入していない場合、データが20分遅れになるため正常に表示されない可能性があります。

東証業種別株価指数は東証から配信されるのが15秒間隔でのリアルタイムになるため、このスクリプトもそれに準ずる形となっています。

Financial Crisis Predictor - Doomsday ClockThe **Financial Crisis Predictor - Doomsday Clock** is a composite indicator that evaluates multiple market conditions to determine financial risk levels. It combines four key metrics: market volatility (via VIX), yield curve spread, stock market momentum, and credit risk (via high-yield spread). Each metric contributes to a weighted "risk score," scaled between 0 and 100, which helps gauge the probability of a financial crisis. Here's a breakdown of how it works:

### 1. **Market Volatility (VIX)**

- **How it's measured:**

- Uses the VIX index, which represents expected market volatility.

- Applies two exponential moving averages (EMAs) to smooth out the data—one fast and one slow.

- Triggers a signal if the fast EMA crosses above the slow EMA and VIX exceeds a defined threshold (default is 30).

- **Weighting:**

- Contributes up to 35% of the total risk score when active.

### 2. **Yield Curve Spread**

- **How it's measured:**

- Takes the difference between the yields of 10-year and 2-year U.S. Treasury bonds (inversion indicates recession risk).

- If the spread drops below a certain threshold (default is 0.2), it signals a potential recession.

- **Weighting:**

- Contributes up to 25% of the risk score.

### 3. **Stock Market Momentum**

- **How it's measured:**

- Analyzes the S&P 500 (SPY) using a 20-day EMA for price momentum.

- Checks for a cross under the 20-day EMA and if the 5-day rate of change (ROC) is less than -2.

- This combination signals bearish market momentum.

- **Weighting:**

- Contributes up to 20% of the risk score.

### 4. **Credit Risk (High Yield Spread)**

- **How it's measured:**

- Assesses high-yield corporate bond spreads using EMAs, similar to the VIX logic.

- A crossover of the fast EMA above the slow EMA combined with spreads exceeding a defined threshold (default is 5.0) indicates increased credit risk.

- **Weighting:**

- Contributes up to 20% of the total risk score.

### 5. **Risk Score Calculation**

- The final **risk score** ranges from 0 to 100 and is calculated using the weighted sum of the four indicators.

- The score is smoothed to minimize false signals and maintain stability.

### 6. **Risk Zones**

- **Extreme Risk:** If the risk score is ≥ 75, indicating a severe crisis warning.

- **High Risk:** If the risk score is between 15 and 75, signaling heightened risk.

- **Moderate Risk:** If the risk score is between 10 and 15, representing potential concerns.

- **Low Risk:** If the risk score is < 10, suggesting stable conditions.

### 7. **Visual & Alerts**

- The indicator plots the risk score on a chart with color-coded backgrounds to indicate risk levels: green (low), yellow (moderate), orange (high), and red (extreme).

- Alert conditions are set for each risk zone, notifying users when the risk level transitions into a higher zone.

This indicator aims to quickly detect potential financial crises by aggregating signals from key market factors, making it a versatile tool for traders, analysts, and risk managers.

RSI with Dynamic ColorsThe "RSI with Dynamic Colors" is a custom indicator built on top of the traditional Relative Strength Index (RSI), which helps traders identify overbought or oversold market conditions. This enhanced version includes added functionality like dynamic colors, highlighting specific conditions, and more customization options. Here's a breakdown of how this indicator works:

Indicator Components:

Relative Strength Index (RSI) Calculation:

The RSI is a momentum oscillator that measures the speed and change of price movements. It oscillates between 0 and 100, helping traders determine if an asset is overbought or oversold.

In this version, the RSI is calculated with a configurable lookback period (default is 14) and applies smoothing to both upward and downward price changes using the Relative Moving Average (RMA).

Dynamic Coloring:

The indicator dynamically changes the color of the RSI line based on its value. Specific thresholds include:

Blue: When the RSI is at or above an extreme overbought level (≥ 85).

Red: When the RSI is in the overbought zone (≥ 70 but < 85).

Yellow: When the RSI is at or below the extreme oversold level (≤ 15).

Green: When the RSI is in the oversold zone (≤ 30 but > 15).

White: When the RSI is between the oversold and overbought zones.

Moving Average Options (MA):

The indicator allows the user to plot an optional moving average of the RSI for additional trend confirmation. Users can select from various types of moving averages, including Simple Moving Average (SMA), Exponential Moving Average (EMA), and others.

Bollinger Bands can be optionally applied around the RSI to visualize volatility.

Overbought and Oversold Highlights:

It provides visual highlights (green for overbought and red for oversold) in the background of the RSI plot, making it easier to identify potential reversal zones.

Divergence Detection (Optional):

The indicator can optionally display regular bullish or bearish divergence, which can signal potential trend reversals. Divergence occurs when price moves in the opposite direction of the RSI.

Bullish divergence is indicated when the price makes lower lows while the RSI makes higher lows.

Bearish divergence is shown when the price makes higher highs while the RSI makes lower highs.

Alerts:

Users can set up alerts for bullish or bearish divergence, making it easier to get notified when key conditions occur in the market.

Use Case:

This custom RSI indicator is designed for traders who want to combine the classic RSI functionality with enhanced visual aids, such as color coding for different RSI zones, customizable moving averages, and Bollinger Bands. It is particularly useful for identifying potential market tops and bottoms by highlighting overbought/oversold conditions and divergence signals.

In summary, this indicator not only retains the traditional RSI's power but also adds new layers of insight through color, moving averages, and divergence detection, helping traders make better-informed decisions.

Judas Swing ICT 01 [TradingFinder] New York Midnight Opening M15🔵 Introduction

The Judas Swing (ICT Judas Swing) is a trading strategy developed by Michael Huddleston, also known as Inner Circle Trader (ICT). This strategy allows traders to identify fake market moves designed by smart money to deceive retail traders.

By concentrating on market structure, price action patterns, and liquidity flows, traders can align their trades with institutional movements and avoid common pitfalls. It is particularly useful in FOREX and stock markets, helping traders identify optimal entry and exit points while minimizing risks from false breakouts.

In today's volatile markets, understanding how smart money manipulates price action across sessions such as Asia, London, and New York is essential for success. The ICT Judas Swing strategy helps traders avoid common pitfalls by focusing on key movements during the opening time and range of each session, identifying breakouts and false breakouts.

By utilizing various time frames and improving risk management, this strategy enables traders to make more informed decisions and take advantage of significant market movements.

In the Judas Swing strategy, for a bullish setup, the price first touches the high of the 15-minute range of New York midnight and then the low. After that, the price returns upward, breaks the high, and if there’s a candlestick confirmation during the pullback, a buy signal is generated.

bearish setup, the price first touches the low of the range, then the high. With the price returning downward and breaking the low, if there’s a candlestick confirmation during the pullback to the low, a sell signal is generated.

🔵 How to Use

To effectively implement the Judas Swing strategy (ICT Judas Swing) in trading, traders must first identify the price range of the 15-minute window following New York midnight. This range, consisting of highs and lows, sets the stage for the upcoming movements in the London and New York sessions.

🟣 Bullish Setup

For a bullish setup, the price first moves to touch the high of the range, then the low, before returning upward to break the high. Following this, a pullback occurs, and if a valid candlestick confirmation (such as a reversal pattern) is observed, a buy signal is generated. This confirmation could indicate the presence of smart money supporting the bullish movement.

🟣 Bearish Setup

For a bearish setup, the process is the reverse. The price first touches the low of the range, then the high. Afterward, the price moves downward again and breaks the low. A pullback follows to the broken low, and if a bearish candlestick confirmation is seen, a sell signal is generated. This confirmation signals the continuation of the downward price movement.

Using the Judas Swing strategy enables traders to avoid fake breakouts and focus on strong market confirmations. The strategy is versatile, applying to FOREX, stocks, and other financial instruments, offering optimal trading opportunities through market structure analysis and time frame synchronization.

To execute this strategy successfully, traders must combine it with effective risk management techniques such as setting appropriate stop losses and employing optimal risk-to-reward ratios. While the Judas Swing is a powerful tool for predicting price movements, traders should remember that no strategy is entirely risk-free. Proper capital management remains a critical element of long-term success.

By mastering the ICT Judas Swing strategy, traders can better identify entry and exit points and avoid common traps from fake market movements, ultimately improving their trading performance.

🔵 Setting

Opening Range : High and Low identification time range.

Extend : The time span of the dashed line.

Permit : Signal emission time range.

🔵 Conclusion

The Judas Swing strategy (ICT Judas Swing) is a powerful tool in technical analysis that helps traders identify fake moves and align their trades with institutional actions, reducing risk and enhancing their ability to capitalize on market opportunities.

By leveraging key levels such as range highs and lows, fake breakouts, and candlestick confirmations, traders can enter trades with more precision. This strategy is applicable in forex, stocks, and other financial markets and, with proper risk management, can lead to consistent trading success.

Simple RSI stock Strategy [1D] The "Simple RSI Stock Strategy " is designed to long-term traders. Strategy uses a daily time frame to capitalize on signals generated by the Relative Strength Index (RSI) and the Simple Moving Average (SMA). This strategy is suitable for low-leverage trading environments and focuses on identifying potential buy opportunities when the market is oversold, while incorporating strong risk management with both dynamic and static Stop Loss mechanisms.

This strategy is recommended for use with a relatively small amount of capital and is best applied by diversifying across multiple stocks in a strong uptrend, particularly in the S&P 500 stock market. It is specifically designed for equities, and may not perform well in other markets such as commodities, forex, or cryptocurrencies, where different market dynamics and volatility patterns apply.

Indicators Used in the Strategy:

1. RSI (Relative Strength Index):

- The RSI is a momentum oscillator used to identify overbought and oversold conditions in the market.

- This strategy enters long positions when the RSI drops below the oversold level (default: 30), indicating a potential buying opportunity.

- It focuses on oversold conditions but uses a filter (SMA 200) to ensure trades are only made in the context of an overall uptrend.

2. SMA 200 (Simple Moving Average):

- The 200-period SMA serves as a trend filter, ensuring that trades are only executed when the price is above the SMA, signaling a bullish market.

- This filter helps to avoid entering trades in a downtrend, thereby reducing the risk of holding positions in a declining market.

3. ATR (Average True Range):

- The ATR is used to measure market volatility and is instrumental in setting the Stop Loss.

- By multiplying the ATR value by a custom multiplier (default: 1.5), the strategy dynamically adjusts the Stop Loss level based on market volatility, allowing for flexibility in risk management.

How the Strategy Works:

Entry Signals:

The strategy opens long positions when RSI indicates that the market is oversold (below 30), and the price is above the 200-period SMA. This ensures that the strategy buys into potential market bottoms within the context of a long-term uptrend.

Take Profit Levels:

The strategy defines three distinct Take Profit (TP) levels:

TP 1: A 5% from the entry price.

TP 2: A 10% from the entry price.

TP 3: A 15% from the entry price.

As each TP level is reached, the strategy closes portions of the position to secure profits: 33% of the position is closed at TP 1, 66% at TP 2, and 100% at TP 3.

Visualizing Target Points:

The strategy provides visual feedback by plotting plotshapes at each Take Profit level (TP 1, TP 2, TP 3). This allows traders to easily see the target profit levels on the chart, making it easier to monitor and manage positions as they approach key profit-taking areas.

Stop Loss Mechanism:

The strategy uses a dual Stop Loss system to effectively manage risk:

ATR Trailing Stop: This dynamic Stop Loss adjusts based on the ATR value and trails the price as the position moves in the trader’s favor. If a price reversal occurs and the market begins to trend downward, the trailing stop closes the position, locking in gains or minimizing losses.

Basic Stop Loss: Additionally, a fixed Stop Loss is set at 25%, limiting potential losses. This basic Stop Loss serves as a safeguard, automatically closing the position if the price drops 25% from the entry point. This higher Stop Loss is designed specifically for low-leverage trading, allowing more room for market fluctuations without prematurely closing positions.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

Together, these mechanisms ensure that the strategy dynamically manages risk while offering robust protection against significant losses in case of sharp market downturns.

The position size has been estimated by me at 75% of the total capital. For optimal capital allocation, a recommended value based on the Kelly Criterion, which is calculated to be 59.13% of the total capital per trade, can also be considered.

Enjoy !

Larry Williams Valuation Index [tradeviZion]Larry Williams Valuation Index

Welcome to the Larry Williams Valuation Index by tradeviZion! This script is an interpretation of Larry Williams' famous WillVal (Valuation) Index, originally developed in 1990 to help traders determine whether a market or asset is overvalued or undervalued. We've extended it to support multiple securities and offer alerts for different valuation levels, helping you make more informed trading decisions.

What is the Valuation Index?

The Valuation Index measures how a security's current price compares to its historical price action. It helps identify whether the security is overvalued (priced too high), undervalued (priced too low), or in a normal range.

This version supports multiple securities and uses valuation parameters to help you assess the relative valuation of three securities simultaneously. It can help you determine the best times to enter (buy) or exit (sell) the market.

Key Features

Multi-Security Analysis: Analyze up to three securities simultaneously to get a broader view of market conditions.

Valuation Levels: Automatically calculate overvaluation and undervaluation levels or set manual levels for consistent analysis.

Custom Alerts: Create custom alerts when securities move between overvalued, undervalued, or normal ranges.

Customizable Table Display: Display a table with valuation values and their status on the chart.

Getting Started

Step 1: Adding the Script to Your Chart

First, add the Larry Williams Valuation Index script to your chart on TradingView. The script is designed to work with any timeframe, but for best results, use weekly or daily timeframes for a longer-term perspective.

Step 2: Configuring Securities

The script allows you to analyze up to three different securities :

Security 1 (Default: DXY)

Security 2 (Default: GC1!)

Security 3 (Default: ZB1!)

You can enable or disable each security individually.

Custom Timeframe Option: You have the option to select a custom timeframe for analysis. This allows you to see whether the security is overvalued or undervalued in lower or higher timeframes. Note that this feature is experimental and has not been extensively tested. Larry Williams originally used the weekly timeframe to determine if a stock was overvalued or undervalued. By default, the indicator compares the current price with the security based on the selected timeframe, except if you choose to use a custom timeframe.

Pro Tip : New users can start with the default securities to understand the concept before using other assets.

Step 3: Valuation Index Settings

Short EMA Length : This is the short-term average used for calculations. A lower value makes it more responsive to recent price changes.

Long EMA Length : This is the long-term average, used to smooth the valuation over time.

Valuation Length (Default: 156) : Represents approximately three years of daily bars (as recommended by Larry Williams).

How is the Valuation Index Calculated?

The valuation calculation is done using a method called WVI (WillVal Index), which compares the current price of a security to the price of another correlated security. Here’s a step-by-step explanation:

1. Data Collection: The script takes the closing price of the security you are analyzing and the closing price of the correlated security.

2. Ratio Calculation : The ratio of the two prices is calculated:

Price Ratio = (Price of your security) / (Price of correlated security) * 100.

This ratio helps determine how expensive or cheap your security is compared to the correlated one.

3. Exponential Moving Averages (EMAs) : The price ratio is used to calculate short-term and long-term EMAs (Exponential Moving Averages). EMAs are used to create smooth lines that represent the average price of a security over a specific period of time, with more weight given to recent data. By calculating both short-term and long-term EMAs, we can identify the trend direction and how the security is performing compared to its historical averages.

4. Valuation Index Calculation:

The Valuation Index is calculated as the difference between the short-term EMA and the long-term EMA. This difference helps to determine if the security is currently overvalued or undervalued:

A positive value indicates that the price is above its longer-term trend, suggesting potential overvaluation.

A negative value indicates that the price is below its longer-term trend, suggesting potential undervaluation.

5. Normalization:

To make the valuation easier to interpret, the calculated valuation index is then normalized using the highest and lowest values over the selected valuation length (e.g., 156 bars).

This normalization process converts the index into a percentage between 0 and 100, where higher values indicate overvaluation and lower values indicate undervaluation.

Step 4: Understanding Valuation Levels

The valuation levels indicate whether a security is currently undervalued, overvalued, or in a normal range.

Manual Levels : You can manually set the overvaluation and undervaluation thresholds (default is 85 for overvalued and 15 for undervalued).

Auto Levels : The script can automatically calculate these levels based on recent price action, allowing you to adapt to changing market conditions.

Auto Levels Calculation Explained:

The Auto Levels are calculated by taking the average of the valuation indices for all three securities (e.g., index1, index2, and index3).

The script then looks at the highest and lowest values of this average over a selected number of recent bars (e.g., 50 bars).

The overvaluation level is determined by taking the highest value and multiplying it by a multiplier (e.g., 5). Similarly, the undervaluation level is calculated using the lowest value and the multiplier.

These dynamic levels adjust according to recent price action, providing an adaptive approach to identifying overvalued and undervalued conditions.

Step 5: How to Use the Script to Make Trading Decisions

For new users, here's a step-by-step trading strategy you can use with the Valuation Index:

1. Identify Undervalued Opportunities

When two or more securities are in the undervalued range (below 15 for manual or below automatically calculated undervalue levels), wait for at least two of these securities to turn from undervalued to normal .

This transition indicates a potential buy opportunity .

2. Buying Signal

When at least two securities transition from undervalued to normal, you can consider buying the asset.

This indicates that the market may be recovering from undervalued conditions and could be moving into a growth phase.

3. Selling Signal

Exit when the price high closes below the EMA 21 (21-day exponential moving average).

Alternatively, if the valuation index reaches overvalued levels (above 85 manually or auto-calculated), wait for it to drop back to normal . This can be another point to exit the trade .

You can also use any other sell condition based on your r isk management strategy .

Alerts for Valuation Levels

The script includes alerts to notify you of changing market conditions:

To activate these alerts, follow these steps, referring to the provided screenshot with detailed steps:

1. Enable Alerts : Click on the settings gear icon on the script title in your chart. In the settings menu, scroll to the section labeled Alerts Settings .

Enable Alerts by checking the Enable Alerts box.

Set the Required Securities for Alert (default is 2 securities).

Choose the Alert Frequency : Selecting Once Per Bar Close will trigger alerts only at the close of each bar, ensuring you receive confirmed signals rather than potentially noisy intermediate signals.

2. Select Alert Type : Choose the type of alert you want to activate, such as Alert on Overvalued, Alert on Undervalued, Alert on Over to Normal , or Alert on Under to Normal .

3. Save Settings : Click OK to save your alert settings.

4. Add Alert on Indicator : Click the "..." (More button) next to the indicator name on the chart and select " Add alert on tradeviZion - WillVal ".

5. Create Alert : In the Create Alert window:

Set Condition to tradeviZion - WillVal .

Ensure Any alert() function call is selected.

Set the Alert Name and select your Expiration preferences.

6. Set Notification Preferences : Go to the Notifications tab and select how you want to receive notifications, such as via app notification, toast notification, email , or sound alert . Adjust these preferences to best suit your needs.

7. Click Create : Finally, click Create to activate the alert.

These alerts will help you stay informed about key market conditions and take action accordingly, ensuring you do not miss critical trading opportunities.

Understanding the Table Display

The script includes an interactive table on the chart to show the valuation status of each security:

Security : The name of the security being analyzed.

Value : The current valuation index value.

Status : Indicates whether the security is overvalued, undervalued , or in a normal range.

Color: Displays a color code for easy identification of status:

Red for overvalued.

Green for undervalued.

Other colors represent normal valuation levels.

Empowering Messages : Motivational messages are displayed to encourage disciplined trading. These messages will change periodically, helping keep a positive trading mindset.

Acknowledgment

This tool builds upon the foundational work of Larry Williams, who developed the WillVal (Valuation) Index concept. It also incorporates enhancements to extend multi-security analysis, valuation normalization, and advanced alerting features, providing a more versatile and powerful indicator. The Larry Williams Valuation Index [ tradeviZion ] helps traders make informed decisions by assessing overvalued and undervalued conditions for multiple securities simultaneously.

Note : Always practice proper risk management and thoroughly test the indicator to ensure it aligns with your trading strategy. Past performance is not indicative of future results.

Trade smarter with TradeVizion—unlock your trading potential today!

BRT MACD CustomBRT MACD Custom — Adaptive and Flexible MACD for Multi-Timeframe Analysis

The BRT MACD Custom is an advanced version of the traditional MACD indicator, offering additional flexibility and adaptability for multi-timeframe trading. This custom script allows traders to adjust the calculation parameters for MACD to suit their specific trading strategy, timeframe, and market conditions.

Key Features

Multi-Timeframe Support

Unlike the standard MACD, this indicator lets you choose a specific timeframe (different from the chart timeframe) for calculating MACD values. This feature provides more flexibility in analyzing market trends on multiple timeframes without changing the main chart.

Example: You can analyze MACD on a 15-minute timeframe even when your chart is set to 1-minute, giving you broader market insights.

Customizable EMA and Signal Settings

Users can adjust the fast and slow EMA lengths as well as the signal smoothing to better align with their preferred trading strategies. The script allows switching between the two popular types of moving averages — SMA or EMA — for both the MACD and the signal line.

Volatility-Based Adaptive EMA

The script includes an adaptive mechanism for EMA calculation. When the selected timeframe closes, the indicator dynamically adjusts the calculation, ensuring the MACD values respond quickly to market volatility. This makes the indicator more reactive compared to static MACD implementations.

Shift Options for MACD, Signal, and Histogram

The indicator allows shifting the MACD, signal line, and histogram values by one or more bars. This can be useful for backtesting and simulating strategies where you anticipate future price movements.

Signal Alerts for Long and Short Trades

The script generates visual signals when certain conditions are met, indicating potential long or short trade opportunities. These signals are based on MACD and histogram crossovers:

Long Signal: Triggered when MACD is above the signal line and both are rising.

Short Signal: Triggered when MACD is below the signal line and both are falling.

Custom Plotting

The MACD line, signal line, and histogram are plotted on the chart for easy visualization. The histogram changes colors to reflect positive or negative momentum:

Green shades when MACD is above the signal line.

Red shades when MACD is below the signal line.

Applications in Trading

The BRT MACD Custom is ideal for traders who need flexibility in their technical analysis. Its multi-timeframe capabilities and customizable moving averages make it suitable for day trading, swing trading, and long-term investing across a variety of markets.

Scalping: Use the 1-minute or 5-minute timeframe to identify short-term trends while calculating MACD on a higher timeframe such as 15 or 30 minutes.

Swing Trading: Apply the indicator on 1-hour or 4-hour charts to detect mid-term trends.

Long-Term Investing: Analyze daily or weekly charts with longer EMA periods to confirm market direction before making large investments.