Live Mini Terminal 1 : Relative General Data ChangeThis script displays relative data changes occurring in the adjustable period and/or adaptive automatic period in various markets.

It was inspired by the data terminals used by commercial traders.

Period selection can be set in the menu.

This script uses the adaptive period algorithm used by Autonomous LSTM and Relativity scripts.

Or you can set the period manually from the menu.

For more information about adaptive period this script uses:

This script works only for 1 day (1D) and 1 week (1W) time frames.

Since COT data is used, the most efficient time frame is 1 week (1W) .

Features

Value changes on a percentage basis (%)

Commitment of Traders position changes on a percentage basis :

Net position percentage is calculated as Short - Long and there is no inverse relationship.

Direct relationship is provided.

Due to the advantage of movement, future data were drawn instead of spot values on the required instruments.

INSTRUMENTS

US10Y : U.S Government Bonds 10 Year Yields

VIX : CBOE Volatility Index (S&P 500 VIX )

GOLD : XAUUSD : Gold

WTI : West Texas Intermediate : USOIL , Crude Oil

BCO : Brent Crude Oil : UKOIL , Light Crude Oil

SP500 : S&P 500 Index

DXY : US Dollar Index

TIO : Iron Ore : Iron Ore %62 Fe CFR China Futures

XAG : SI : Silver

NG : Natural Gas

JPYUSD : Japanese Yen

EURUSD : Euro/Dollar

Position Change InfoPanel

10 US T-Bond positions are used because there is no position equivalent in US10Y.

In other instruments, the corresponding position provisions are written and their changes are calculated.

USAGE

The script can be used as an indicator by putting it under the chart as shown above.

It is necessary to enlarge to see clearly.

Since it is not often looked at,

such use is the best method for healthy interpretation.

Cari skrip untuk "vix"

ANN Forecast Dependent Variable Odd GeneratorHello , this script is the ANN Forecast version of my "Dependent Variable Odd Generator " script.

I went to simplify a bit because the deep learning calculations are too much for this command.

The latest instruments included:

WTI : West Texas Intermediate (WTICOUSD , USOIL , CL1! ) Average error : 0.007593

BRENT : Brent Crude Oil ( BCOUSD , UKOIL , BB1! ) Average error : 0.006591

GOLD : XAUUSD , GOLD , GC1! Average error : 0.012767

SP500 : S&P 500 Index ( SPX500USD , SP1! ) Average error : 0.011650

EURUSD : Eurodollar ( EURUSD , 6E1! , FCEU1!) Average error : 0.005500

ETHUSD : Ethereum ( ETHUSD , ETHUSDT ) Average error : 0.009378

BTCUSD : Bitcoin ( BTCUSD , BTCUSDT , XBTUSD , BTC1! ) Average error : 0.01050

GBPUSD : British Pound ( GBPUSD , 6B1! , GBP1!) Average error : 0.009999

USDJPY : US Dollar / Japanese Yen ( USDJPY , FCUY1!) Average error : 0.009198

USDCHF : US Dollar / Swiss Franc ( USDCHF , FCUF1! ) Average error : 0.009999

USDCAD : Us Dollar / Canadian Dollar ( USDCAD ) Average error : 0.012162

VIX : S & P 500 Volatility Index (VX1! , VIX ) Average error : 0.009999

ES : S&P 500 E-Mini Futures ( ES1! ) Average error : 0.010709

SSE : Shangai Stock Exchange Composite (Index ) ( 000001 ) Average error : 0.011287

XRPUSD : Ripple (XRPUSD , XRPUSDT ) Average error : 0.009803

Simply select the required instrument from the tradingview analysis screen, then add this command and select the same instrument from the settings section.

The codes are not open-source because they contain forecast algorithm codes a little that I will use commercially in the future.

However, I will never remove this script, and you can use it for free unlimitedly.

For more information about my artificial neural network forecast series:

For more information about my dependent variable odd generator :

For more information about simple artificial neural networks :

(detailed information about ANN )

(25 in 1 version )

I hope it helps in your analysis. Regards , Noldo .

NOTE : In the first pass bar of the definite positive and negative zone, alerts are added for both conditions.

ANN Forecast Stochastic Oscillator [Noldo] In this script, I tried to integrate ANN Forecast Algorithm on Stochastic Oscillator.

It took me quite a while, but i guess it worth.

After selecting the ticker, select the instrument from the menu and the system will automatically turn on the appropriate Forecast Stoch system.

The system is trained with ANN values of ANN MACD 25 in 1.

The Forecast algorithm is not open-source.

But I'm never remove this script.

You can use it forever for free.

As you can see in the presentation, although it is in the same period, it is more accurate and agile than standard Stochastic Oscillator .

I think even a bar is important in trade.

For those who don't see that command,listed instruments with alternative tickers and error rates:

WTI : West Texas Intermediate (WTICOUSD , USOIL , CL1! ) Average error : 0.007593

BRENT : Brent Crude Oil ( BCOUSD , UKOIL , BB1! ) Average error : 0.006591

GOLD : XAUUSD , GOLD , GC1! Average error : 0.012767

SP500 : S&P 500 Index ( SPX500USD , SP1! ) Average error : 0.011650

EURUSD : Eurodollar ( EURUSD , 6E1! , FCEU1!) Average error : 0.005500

ETHUSD : Ethereum ( ETHUSD , ETHUSDT ) Average error : 0.009378

BTCUSD : Bitcoin ( BTCUSD , BTCUSDT , XBTUSD , BTC1! ) Average error : 0.01050

GBPUSD : British Pound ( GBPUSD , 6B1! , GBP1!) Average error : 0.009999

USDJPY : US Dollar / Japanese Yen ( USDJPY , FCUY1!) Average error : 0.009198

USDCHF : US Dollar / Swiss Franc ( USDCHF , FCUF1! ) Average error : 0.009999

USDCAD : Us Dollar / Canadian Dollar ( USDCAD ) Average error : 0.012162

SOYBNUSD : Soybean ( SOYBNUSD , ZS1! ) Average error : 0.010000

CORNUSD : Corn ( ZC1! ) Average error : 0.007574

NATGASUSD : Natural Gas ( NATGASUSD , NG1! ) Average error : 0.010000

SUGARUSD : Sugar ( SUGARUSD , SB1! ) Average error : 0.011081

WHEATUSD : Wheat ( WHEATUSD , ZW1! ) Average error : 0.009980

XPTUSD : Platinum ( XPTUSD , PL1! ) Average error : 0.009964

XU030 : Borsa Istanbul 30 Futures ( XU030 , XU030D1! ) Average error : 0.010727

VIX : S & P 500 Volatility Index (VX1! , VIX ) Average error : 0.009999

ES : S&P 500 E-Mini Futures ( ES1! ) Average error : 0.010709

SSE : Shangai Stock Exchange Composite (Index ) ( 000001 ) Average error : 0.011287

XRPUSD : Ripple (XRPUSD , XRPUSDT ) Average error : 0.009803

Extras :

- Crossover and crossunder alerts

- Switchable barcolor

NOTE :

Australian Dollar / US Dollar ( AUDUSD ) removed due to high average error. (Average error > 0.013 )

Timeframe advice :

I suggest you to use that system TF >= 1D

My favorite is 1 week bars. (1W)

More info about forecast series (My last forecast example ) :

Special thanks :

Special thanks to dear wroclai for his great effort .

NOTE : I decided to build Autonomous LSTM on Stochastic Oscillator , i think Stochastic Oscillator one of the best and it contains naturally high-lows.

ANN Forecast MACD [Noldo] In this script, I tried to convert ANN MACD to MACD Forecast.

It took me quite a while, but it was fun.

After selecting the ticker, select the instrument from the menu and the system will automatically turn on the appropriate Forecast MACD system.

The system is trained with ANN values of ANN MACD 25 in 1.

But because the system is overloaded, only the most popular instruments are left.

The others were unfortunately eliminated.

The only difference is that it was built on the forecast algorithm of my own creation.

The Forecast algorithm is not open-source.

The codes are a nice framework for some of my most valuable systems about ANN . (Working on them. )

But I'm never remove this script.

You can use it forever for free.

As you can see in the presentation, although it is in the same period, it is more accurate and agile than normal MACD.

I think even a bar is important in trade.

For those who don't see that command,listed instruments with alternative tickers and error rates:

WTI : West Texas Intermediate (WTICOUSD , USOIL , CL1! ) Average error : 0.007593

BRENT : Brent Crude Oil ( BCOUSD , UKOIL , BB1! ) Average error : 0.006591

GOLD : XAUUSD , GOLD , GC1! Average error : 0.012767

SP500 : S&P 500 Index ( SPX500USD , SP1! ) Average error : 0.011650

EURUSD : Eurodollar ( EURUSD , 6E1! , FCEU1!) Average error : 0.005500

ETHUSD : Ethereum ( ETHUSD , ETHUSDT ) Average error : 0.009378

BTCUSD : Bitcoin ( BTCUSD , BTCUSDT , XBTUSD , BTC1! ) Average error : 0.01050

GBPUSD : British Pound ( GBPUSD , 6B1! , GBP1!) Average error : 0.009999

USDJPY : US Dollar / Japanese Yen ( USDJPY , FCUY1!) Average error : 0.009198

USDCHF : US Dollar / Swiss Franc ( USDCHF , FCUF1! ) Average error : 0.009999

USDCAD : Us Dollar / Canadian Dollar ( USDCAD ) Average error : 0.012162

SOYBNUSD : Soybean ( SOYBNUSD , ZS1! ) Average error : 0.010000

CORNUSD : Corn ( ZC1! ) Average error : 0.007574

NATGASUSD : Natural Gas ( NATGASUSD , NG1! ) Average error : 0.010000

SUGARUSD : Sugar ( SUGARUSD , SB1! ) Average error : 0.011081

WHEATUSD : Wheat ( WHEATUSD , ZW1! ) Average error : 0.009980

XPTUSD : Platinum ( XPTUSD , PL1! ) Average error : 0.009964

XU030 : Borsa Istanbul 30 Futures ( XU030 , XU030D1! ) Average error : 0.010727

VIX : S & P 500 Volatility Index (VX1! , VIX ) Average error : 0.009999

ES : S&P 500 E-Mini Futures ( ES1! ) Average error : 0.010709

SSE : Shangai Stock Exchange Composite (Index ) ( 000001 ) Average error : 0.011287

XRPUSD : Ripple (XRPUSD , XRPUSDT ) Average error : 0.009803

Extras :

- Crossover and crossunder alerts

- Switchable barcolor

NOTE :

Australian Dollar / US Dollar (AUDUSD ) removed due to high average error. (Average error > 0.013 )

Timeframe advice :

I suggest you to use that system TF >= 1D

My favorite is 1 week bars. (1W)

Info about forecast series :

www.sciencedirect.com

Special thanks :

Special thanks to dear wroclai for his great effort .

ANN MACD : 25 IN 1 SCRIPTIn this script, I tried to fit deep learning series to 1 command system up to the maximum point.

After selecting the ticker, select the instrument from the menu and the system will automatically turn on the appropriate ann system.

Listed instruments with alternative tickers and error rates:

WTI : West Texas Intermediate (WTICOUSD , USOIL , CL1! ) Average error : 0.007593

BRENT : Brent Crude Oil (BCOUSD , UKOIL , BB1! ) Average error : 0.006591

GOLD : XAUUSD , GOLD , GC1! Average error : 0.012767

SP500 : S&P 500 Index (SPX500USD , SP1!) Average error : 0.011650

EURUSD : Eurodollar (EURUSD , 6E1! , FCEU1!) Average error : 0.005500

ETHUSD : Ethereum (ETHUSD , ETHUSDT ) Average error : 0.009378

BTCUSD : Bitcoin (BTCUSD , BTCUSDT , XBTUSD , BTC1!) Average error : 0.01050

GBPUSD : British Pound (GBPUSD,6B1! , GBP1!) Average error : 0.009999

USDJPY : US Dollar / Japanese Yen (USDJPY , FCUY1!) Average error : 0.009198

USDCHF : US Dollar / Swiss Franc (USDCHF , FCUF1! ) Average error : 0.009999

USDCAD : Us Dollar / Canadian Dollar (USDCAD) Average error : 0.012162

SOYBNUSD : Soybean (SOYBNUSD , ZS1!) Average error : 0.010000

CORNUSD : Corn (ZC1! ) Average error : 0.007574

NATGASUSD : Natural Gas (NATGASUSD , NG1!) Average error : 0.010000

SUGARUSD : Sugar (SUGARUSD , SB1! ) Average error : 0.011081

WHEATUSD : Wheat (WHEATUSD , ZW1!) Average error : 0.009980

XPTUSD : Platinum (XPTUSD , PL1! ) Average error : 0.009964

XU030 : Borsa Istanbul 30 Futures ( XU030 , XU030D1! ) Average error : 0.010727

VIX : S & P 500 Volatility Index (VX1! , VIX ) Average error : 0.009999

YM : E - Mini Dow Futures (YM1! ) Average error : 0.010819

ES : S&P 500 E-Mini Futures (ES1! ) Average error : 0.010709

GAZP : Gazprom Futures (GAZP , GZ1! ) Average error : 0.008442

SSE : Shangai Stock Exchange Composite (Index ) ( 000001 ) Average error : 0.011287

XRPUSD : Ripple (XRPUSD , XRPUSDT ) Average error : 0.009803

Note 1 : Australian Dollar (AUDUSD , AUD1! , FCAU1! ) : Instrument has been removed because it has an average error rate of over 0.13.

The average error rate is 0.1850.

I didn't delete it from the menu just because there was so much request,

You can use.

Note 2 : Friends have too many requests, it took me a week in total and 1 other script that I'll share in 2 days.

Reaching these error rates is a very difficult task, and when I keep at a low learning rate, they are trained for a very long time.

If I don't see the error rate at an average low, I increase the layers and go back into a longer process.

It takes me 45 minutes per instrument to command artificial neural networks, so I'll release one more open source, and then we'll be laying 70-80 percent of the world trade volume with artificial neural networks.

Note 3 :

I would like to thank wroclai for helping me with this script.

This script is subject to MIT License on behalf of both of us.

You can review my original idea scripts from my Github page.

You can use it free but if you are going to modify it, just quote this script .

I hope it will help everyone, after 1-2 days I will share another ann script that I think is of the same importance as this, stay tuned.

Regards , Noldo .

TheStocksDoctor_WVF + ADX + CCIThis script is a modified version of CM Williams Vix Fix for which I have added an indicator that shows when ADX and CCI are both indicating positive momentum - highlighted by green bars. This is part of TheStocksDoctor Trading System.

Inputs are as follows:

Lookback period Standard Deviation High ---> 22

Bolinger Band Length ---> 20

Bollinger Band Standard Dev.. ---> 2

Lookback period percentile high ---> 50

Highest Percentile ---> 0.85

----Highlight bars Below... --->

Show Highlight bar if WVF WAS true is now False --->

Show highlight bar if WVF IS True --->

----Highlight bars Below Use Filtered... --->

Show highlight bar for filtered entry --->

Show highlight bar for AGGRESSIVE Filtered Entry? --->

Check below to Turn all Bars Gray --->

Check box to Turn Bars gray? --->

Long-term look back current bar has to close Below... ---> 40

Medium-term look back current bar has to close below... ---> 14

Entry price action strength --close... ---> 3

--------Turn On/Off Alerts below... --->

---To activate alerts you HAVE To Check... --->

---You can un Check the box BELOW... --->

Show Williams Vix Fix Histogram... --->

Show Alert WVF = True? --->

Show Alert WVF wa true now False? --->

Show Alert WVF Filtered? --->

Show Alert WVF AGGRESSIVE Filter? --->

ADX Smoothing ---> 17

DI Length ---> 17

CryptoPeek_VixFixAbout: Modified version of the Vix Fix algorithm, which can be used to identify volatility

Features:

Black line = Vix Fix

Blue line = Bollinger bands

(JS) S&P 500 Volatility Oscillator For OptionsThe idea for this started here: www.tradingview.com with the user @dime

This should only be used on SPX or SPY (though you could use it on other things for correlation I suppose) given that the instrument used to create this calculation is derived from the S&P 500 (thank you VIX). There's a lot of moving parts here though, so allow me to explain...

First: The main signal is when Implied Volatility (from VIX) drops beneath Historical Volatility - which is what you want to see so you aren't purchasing a ton of premium on long options. Green and above 0 means that IV% has dropped lower than Historical Volatility. (this signal, for example, would suggest using a Long Call or Put depending on your sentiment)

Second: The green line running underneath zero is the bottom portion of the "Average True Range" derived from the values used to create the oscillator. the closer the bottom histogram is to the green line, the more "normal" IV% is. Obviously, if this gets far away from the line then it could be setting up nicely to short options and sell the IV premium to someone else. (this signal, for example, would suggest using something like a Bull Put Spread)

Third: The red background along with the white line that drops down below zero signals when (and how far) the IV% from 3 months out (from VIX3M) is less than the current IV%. This would signal the current environment has IV way too high, a signal to short options once again (and don't take any long option positions!).

Tried to make this simple, yet effective. If you trade options on SPX, SPY, even ES1! futures - this is a tool tailored specifically for you! As I said before, if you want you can use it for correlation on other securities. Any other ideas or suggestions surrounding this, please let me know! Enjoy!

Correlative Move IndicatorEDIT: When loading this indicator it uses a default symbol for comparison of SPX. On Tradingview SPX is a Daily price (unless you buy real time) so you will see "Loading ..." and never see data. Move out to a daily time frame -or- switch the symbol to something available intraday. /EDIT

Correlates the movement of the price you are graphing to the price of someting else that you pick (default is SPX, see EDIT above)

Comments in code explain what I did. If correlations are too tight for CC to show anything but a flat line try this.

Please comment / improve.

=====================

// A simple indicator that looks complex (impress your friends)

// Provides rate of change in the propensity of something

// to move in correlation with whatever you are graphing.

// Inputs are:

// "Compared symbol" - standard Trading View symbol input. You can input ratios & formulas if you like; Defaults to SPX

// "Invert?" - by default the indicator shows the item you have charted as numerator and the "Compared symbol"

// the denominator. So if you graphed "UVXY" and open this indicator with default compared symbol "SPX" then

// the base relationship is UVXY/SPX. Click the box if you want SPX/UVXY (for example) instead.

// "Fast EMA Period" - the period for the fast EMA (white line). default = 7

// "Slow EMA Period" - the period for the slow EMA (black line). default = 27. Important: the bakground color of the indicator

// changes based on this EMA hitting threshold values below.

// "+ threshold" - > threshold for green background. default = 1.0

// "- threshold" - < threshold for red background. default = 0.99

// "BBand Period" - number of periods back for BBand (1 std deviation) calculation. default = 15

// Does not measure correlation per se - it measures change in that correlation.

// If two things do not correlate well in the first place then you will see a lot of noise

// and I wish you much luck in interpreting it.

// However, if two things do correlate well (like VXX and VIX) then this will help you detect

// circumstances where that correlation is unstable. Such instability can signal change in direction.

// I developed it to track real time changes in contango / backwardation in various VIX futures instruments which I trade.

// Tip - always try invert - sometimes the correlation changes become clearer. That can be because the threshold bias

// towards "+" with the defaults here, so think about what the "logical" relationship is and adjust the thresholds, or invert,

// or do both. Just remember - the indicator is below the item you are charting, so the default "source"/"compared"

// relationship is intuitive as you look at the screen. Volatility traders, however, will find "invert" useful with default

// thresholds signalling "green" for contango and "red" for backwardation.

// Short and long ema trends added for smoothing and trend change indications.

// Background color changes to green when correlation changing "positively" and red when "negatively" and white when near 1.

// Think of the value "1" as representing the base "1 to 1" correlation between two things. That doesn't mean same price -

// it means same rate and direction in change in price.

// 1 std deviation is used to build a basic Bollinger Band in blue. The number of periods for calculating that is an input.

// You may find a change in correlation signal outside a Bollinger Band signals a direction change. TV alerts can be

// set for such events.

CM ATR PercentileRankCM ATR PercentileRank - Great For Showing Market Bottoms.

When Increased Volatility to the Downside Reaches Extreme Levels it’s Usually a Sign of a Market Bottom.

This Indicator Takes the ATR and uses a different LookBack Period to calculate the Percentile Rank of ATR Which is a Great Way To Calculate Volatility

Be Careful Of Using w/ Market Tops. Not As Reliable.

***Ability to Control ATR Period and set PercentileRank to Different Lookback Period

***Ability to Plot Histogram Just Showing Percentiles or Histogram Based on Up/Down Close

Fuchsia Lines = Greater Than 90th Percentile of Volatility based on ATR and LookBack Period.

Red Lines = Warning — 80-90th Percentile

Orange Lines = 70-80th Percentile

Other Useful Indicators

Williams Vix Fix

CM_RSI EMA Is a Great Filter for Williams Vix Fix

Intelligent Fear Indicator Pro+ v1.0 [EN] Intelligent Fear Pro+ — Make Your Decisions with Confidence

Turn candlesticks into clear, professionally filtered signals. The indicator combines pattern recognition with trend, volume, and volatility filters to deliver market signals that cut through the noise and highlight high-probability opportunities. It provides stronger confidence in every decision and shows only what matters on the chart for more accurate entries and exits, helping you pick the best trades across different timeframes.

Why You’ll Love It

High-quality signals: Confirms patterns with trend, volume, VWAP, ADX, and ATR.

Multi-timeframe confirmation: Smart filtering using higher-timeframe signals to reduce false alerts.

Instant alerts: Ready-to-use notifications so you never miss a move.

Practical design: Clean chart markers and a strong trend box to clarify current direction.

Flexible for any market: Works on forex, stocks, futures, and crypto — from scalping to swing trading.

What It Detects

Powerful patterns: Three White Soldiers / Three Black Crows, Five Soldiers / Five Crows, Cup & Handle, Engulfing, Morning Star, and Evening Star.

Professional filters: EMA trend, volume, VWAP, ADX (trend strength), ATR (true body momentum).

Optional VIX filter: Avoid trades during peak fear/volatility cycles.

How to Use It Quickly

Add it to your chart and adjust to your trading style.

Watch for pattern signals + confirmation from filters (trend/volume/VWAP).

Plan entries and exits with clear risk management.

⚠️ Important Note: This indicator is a decision-support tool, not investment advice. Always apply strict risk management.

Download Intelligent Fear Pro+ now and start seeing the market with greater clarity and speed.

BTC Macro Composite Global liquidity Index -OffsetThis indicator is based on the thesis that Bitcoin price movements are heavily influenced by macro liquidity trends. It calculates a weighted composite index based on the following components:

• Global Liquidity (41%): Sum of central bank balance sheets (Fed , ECB , BoJ , and PBoC ), adjusted to USD.

• Investor Risk Appetite (22%): Derived from the Copper/Gold ratio, inverse VIX (as a risk-on signal), and the spread between High Yield and Investment Grade bonds (HY vs IG OAS).

• Gold Sensitivity (15–20%): Combines the XAUUSD price with BTC/Gold ratio to reflect the historical influence of gold on Bitcoin pricing.

Each component is normalized and then offset forward by 90 days to attempt predictive alignment with Bitcoin’s price.

The goal is to identify macro inflection points with high predictive value for BTC. It is not a trading signal generator but rather a macro trend context indicator.

❗ Important: This script should be used with caution. It does not account for geopolitical shocks, regulatory events, or internal BTC market structure (e.g., miner behavior, on-chain metrics).

💡 How to use:

• Use on the 1D timeframe.

• Look for divergences between BTC price and the macro index.

• Apply in confluence with other technical or fundamental frameworks.

🔍 Originality:

While similar components exist in macro dashboards, this script combines them uniquely using time-forward offsets and custom weighting specifically tailored for BTC behavior.

Macro Pulse Dashboard [SwissAlgo]Macro Pulse Dashboard

What is it?

The Macro Pulse Dashboard is a multi-asset performance dashboard designed to give traders and investors a quick snapshot of global market conditions. The indicator tracks price and momentum across crypto, equities, sectors, commodities, bonds, and macro indicators—considering multiple timeframes—in one color-coded table with a trend indication for each asset.

Purpose

Give you a fast, single-glance read of global markets so you can gauge whether conditions are broadly risk-on or risk-off and where strength/weakness clusters across markets.

Who it’s for

Traders and investors who want a clear, beginner-friendly macro overview to frame ideas and risk, without digging through multiple charts.

Why this may help you

Gives context fast : before focusing on one chart, you see the broader environment. This can help avoid trades that fight the macro tide.

Reduces noise : instead of jumping between watchlists and windows, you get a single, consistent view each day.

Improves decision quality : aligning ideas with the table’s short-term and medium-term bias can assist with timing and position sizing.

Builds routine : spend 30 seconds at the open scanning for agreement or conflict across crypto, equities, sectors, commodities, bonds, and macro gauges. If signals are mixed, consider waiting or sizing down; if they align, proceed with your plan.

Beginner-friendly : clear green/red percentages and a simple Trend icon make it easy to interpret without advanced indicators. The trend is determined using a simplified rule in this version.

What’s included

Crypto (BTC/ETH, dominance, total/alt caps), equity indices (US futures, Europe 50, FTSE, HSI, Nikkei, Nifty), US sectors (XLK, SOXX, ARKK, XLY, XLV), commodities (Gold, Silver, WTI, Nat Gas), bonds/credit ETFs (SHY, IEF, TLT, LQD, HYG, AGG, EMB), and macro gauges (US10Y, DXY, EURUSD, VIX).

Columns

Price/Value, % change over 1D, 1W, 2W, 1M, YTD, plus a simple trend glyph (▲ up, ▼ down, ◆ mixed).

Trend logic

The Trend icon is a simple overview (not a signal): ▲ if both short-term (1W) and 1M changes are positive, ▼ if both are negative, ◆ otherwise.

How numbers are computed

All changes use the last completed daily close.

1D = change since the prior daily close.

1W/2W/1M: crypto uses 7/14/30 calendar days; other assets use 5/10/21 trading sessions.

YTD compares to the first daily close of the year.

Prices show a $ prefix where applicable and are compacted (M/B/T).

Repainting

The table uses daily data with lookahead_off and updates only after the daily bar completes. It does not repaint intrabar.

Settings

Anchor (top-left) and Table Size (Small/Normal/Large).

Notes

Informational/educational tool only. Not trading advice. No buy/sell signals or alerts are generated.

Symbols depend on TradingView data availability; if a symbol isn’t accessible on your plan, that row will show “—”.

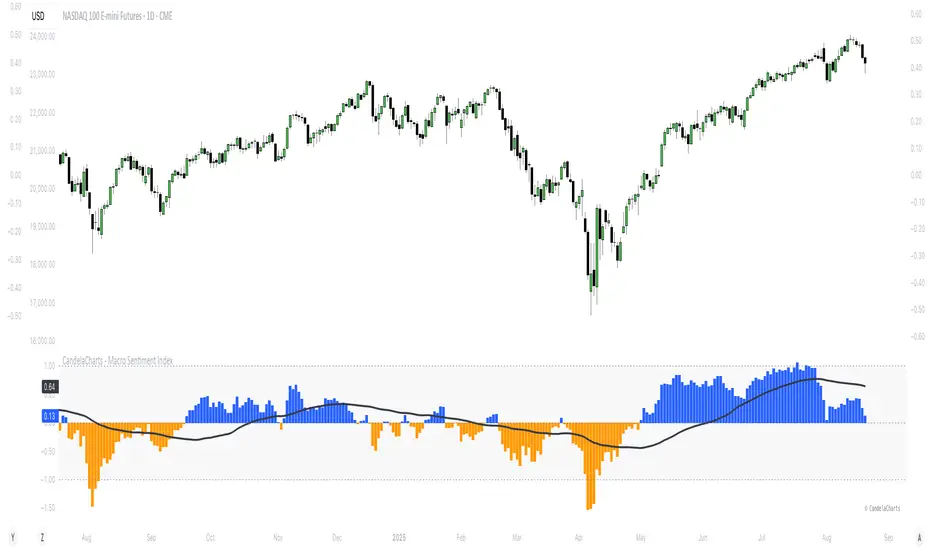

CandelaCharts - Macro Sentiment Index 📝 Overview

The Macro Sentiment Index (MSI) is a multi-asset, rules-based indicator designed to quantify global market risk appetite by aggregating signals from a diversified basket of financial instruments across equities, fixed income, commodities, currencies, volatility, and macroeconomic data.

Developed under the CandelaCharts framework, MSI transforms complex intermarket dynamics into a single, interpretable sentiment score. It reflects the collective behavior of institutional and retail investors, central bank policies, liquidity conditions, and macroeconomic trends.

Rather than relying on a single data source, the index combines over 30 components grouped into five core categories:

Risk-On Assets

Risk-Off / Defensive Assets

Macro & Interest Rate Indicators

Central Bank & Policy Proxies

Sentiment Ratios & Cross-Asset Signals

Each component is standardized using z-score normalization over a user-defined lookback period, weighted based on empirical significance, and aggregated into a composite sentiment score.

The final output oscillates around a neutral baseline (0), with positive values indicating risk-on conditions and negative values signaling risk-off sentiment.

📦 Features

Multi-Dimensional Inputs: Integrates equities, bonds, commodities, volatility, FX, yield curves, policy, macro, sector rotations, and sentiment ratios for holistic market breadth.

Adaptive Scoring System: Converts inputs into z-scores over a lookback window, normalizes directionality, and highlights relative strength/weakness in real time.

Weighted Aggregation: Users assign custom weights (0.1–3.0) to inputs, enabling fine-tuning for regimes or strategies. The index is a weighted average of component scores.

Smoothing & Visualization Modes: Apply SMA, EMA, RMA, or VWMA with custom length. Display as line, histogram, area, or columns with neutral, overbought, and oversold zones.

Correlation Monitoring: On-chart table tracks rolling correlations (default 20 periods) between asset prices and MSI, detecting divergences and regime changes.

Customizable UI: Personalize fonts, text size, branding, and color schemes for bullish/bearish phases and MA line visualization.

⚙️ Settings

Lookback: Define how far back the indicator evaluates data

MA (Moving Average): When enabled, overlays a moving default disabled

MA Smoothing: Applies a secondary smoothing layer

Correlation: Defines the period over which correlation is measured

Mode: Determines the visual layout style

Equity Benchmarks: SPY, QQQ, IWM, EEM

Fixed Income: TLT, HYG, LQD, SHY

Commodities: Gold (GC), Copper (HG), Oil (CL), BCOM

Volatility: VIX, VVIX, MOVE, SKEW

FX Pairs: USD/JPY, USD/CHF, AUD/JPY, DXY

Yield Curves: 10Y-2Y Spread (TYX), 10Y-5Y (TNX-FEDFUNDS)

Monetary Policy: SOFR, ED, FF futures

Global Macro: BDIY, M2, TED Spread, Put/Call Ratio

Sector Rotation: XLU/XLY, XLY/XLP

Sentiment Ratios: SPY/TLT, HYG/LQD, BTC/Gold, Copper/Gold, etc

⚡️ Showcase

Default Mode

Area Mode

Smoothing Moving Average

📒 Usage

Interpreting the Index

Above 0: Net risk-on sentiment - (Markets favor growth, liquidity, and speculative assets)

Below 0: Net risk-off sentiment - (Flight to safety, rising volatility, defensive positioning)

Above +1: Extreme risk-on / complacency - (Potential overheating or topping pattern)

Below −1: Extreme risk-off / fear - (Stress, capitulation, or strong defensive rotation)

🚨 Alerts

The indicator does not provide any alerts!

⚠️ Disclaimer

These tools are exclusively available on the TradingView platform.

Our charting tools are intended solely for informational and educational purposes and should not be regarded as financial, investment, or trading advice. They are not designed to predict market movements or offer specific recommendations. Users should be aware that past performance is not indicative of future results and should not rely on these tools for financial decisions. By using these charting tools, the purchaser agrees that the seller and creator hold no responsibility for any decisions made based on information provided by the tools. The purchaser assumes full responsibility and liability for any actions taken and their consequences, including potential financial losses or investment outcomes that may result from the use of these products.

By purchasing, the customer acknowledges and accepts that neither the seller nor the creator is liable for any undesired outcomes stemming from the development, sale, or use of these products. Additionally, the purchaser agrees to indemnify the seller from any liability. If invited through the Friends and Family Program, the purchaser understands that any provided discount code applies only to the initial purchase of Candela's subscription. The purchaser is responsible for canceling or requesting cancellation of their subscription if they choose not to continue at the full retail price. In the event the purchaser no longer wishes to use the products, they must unsubscribe from the membership service, if applicable.

We do not offer reimbursements, refunds, or chargebacks. Once these Terms are accepted at the time of purchase, no reimbursements, refunds, or chargebacks will be issued under any circumstances.

By continuing to use these charting tools, the user confirms their understanding and acceptance of these Terms as outlined in this disclaimer.

Overnight Gap Dominance Indicator (OGDI)The Overnight Gap Dominance Indicator (OGDI) measures the relative volatility of overnight price gaps versus intraday price movements for a given security, such as SPY or SPX. It uses a rolling standard deviation of absolute overnight percentage changes divided by the standard deviation of absolute intraday percentage changes over a customizable window. This helps traders identify periods where overnight gaps predominate, suggesting potential opportunities for strategies leveraging extended market moves.

Instructions

A

pply the indicator to your TradingView chart for the desired security (e.g., SPY or SPX).

Adjust the "Rolling Window" input to set the lookback period (default: 60 bars).

Modify the "1DTE Threshold" and "2DTE+ Threshold" inputs to tailor the levels at which you switch from 0DTE to 1DTE or multi-DTE strategies (default: 0.5 and 0.6).

Observe the OGDI line: values above the 1DTE threshold suggest favoring 1DTE strategies, while values above the 2DTE+ threshold indicate multi-DTE strategies may be more effective.

Use in conjunction with low VIX environments and uptrend legs for optimal results.

Information-Geometric Market DynamicsInformation-Geometric Market Dynamics

The Information Field: A Geometric Approach to Market Dynamics

By: DskyzInvestments

Foreword: Beyond the Shadows on the Wall

If you have traded for any length of time, you know " the feeling ." It is the frustration of a perfect setup that fails, the whipsaw that stops you out just before the real move, the nagging sense that the chart is telling you only half the story. For decades, technical analysis has relied on interpreting the shadows—the patterns left behind by price. We draw lines on these shadows, apply indicators to them, and hope they reveal the future.

But what if we could stop looking at the shadows and, instead, analyze the object casting them?

This script introduces a new paradigm for market analysis: Information-Geometric Market Dynamics (IGMD) . The core premise of IGMD is that the price chart is merely a one-dimensional projection of a much richer, higher-dimensional reality—an " information field " generated by the collective actions and beliefs of all market participants.

This is not just another collection of indicators. It is a unified framework for measuring the geometry of the market's information field—its memory, its complexity, its uncertainty, its causal flows—and making high-probability decisions based on that deeper reality. By fusing advanced mathematical and informational concepts, IGMD provides a multi-faceted lens through which to view market behavior, moving beyond simple price action into the very structure of market information itself.

Prepare to move beyond the flatland of the price chart. Welcome to the information field.

The IGMD Framework: A Multi-Kernel Approach

What is a Kernel? The Heart of Transformation

In mathematics and data science, a kernel is a powerful and elegant concept. At its core, a kernel is a function that takes complex, often inscrutable data and transforms it into a more useful format. Think of it as a specialized lens or a mathematical "probe." You cannot directly measure abstract concepts like "market memory" or "trend quality" by looking at a price number. First, you must process the raw price data through a specific mathematical machine—a kernel—that is designed to output a measurement of that specific property. Kernels operate by performing a sort of "similarity test," projecting data into a higher-dimensional space where hidden patterns and relationships become visible and measurable.

Why do creators use them? We use kernels to extract features —meaningful pieces of information—that are not explicitly present in the raw data. They are the essential tools for moving beyond surface-level analysis into the very DNA of market behavior. A simple moving average can tell you the average price; a suite of well-chosen kernels can tell you about the character of the price action itself.

The Alchemist's Challenge: The Art of Fusion

Using a single kernel is a challenge. Using five distinct, computationally demanding mathematical engines in unison is an immense undertaking. The true difficulty—and artistry—lies not just in using one kernel, but in fusing the outputs of many . Each kernel provides a different perspective, and they can often give conflicting signals. One kernel might detect a strong trend, while another signals rising chaos and uncertainty. The IGMD script's greatest strength is its ability to act as this alchemist, synthesizing these disparate viewpoints through a weighted fusion process to produce a single, coherent picture of the market's state. It required countless hours of testing and calibration to balance the influence of these five distinct analytical engines so they work in harmony rather than cacophony.

The Five Kernels of Market Dynamics

The IGMD script is built upon a foundation of five distinct kernels, each chosen to probe a unique and critical dimension of the market's information field.

1. The Wavelet Kernel (The "Microscope")

What it is: The Wavelet Kernel is a signal processing function designed to decompose a signal into different frequency scales. Unlike a Fourier Transform that analyzes the entire signal at once, the wavelet slides across the data, providing information about both what frequencies are present and when they occurred.

The Kernels I Use:

Haar Kernel: The simplest wavelet, a square-wave shape defined by the coefficients . It excels at detecting sharp, sudden changes.

Daubechies 2 (db2) Kernel: A more complex and smoother wavelet shape that provides a better balance for analyzing the nuanced ebb and flow of typical market trends.

How it Works in the Script: This kernel is applied iteratively. It first separates the finest "noise" (detail d1) from the first level of trend (approximation a1). It then takes the trend a1 and repeats the process, extracting the next level of cycle (d2) and trend (a2), and so on. This hierarchical decomposition allows us to separate short-term noise from the long-term market "thesis."

2. The Hurst Exponent Kernel (The "Memory Gauge")

What it is: The Hurst Exponent is derived from a statistical analysis kernel that measures the "long-term memory" or persistence of a time series. It is the definitive measure of whether a series is trending (H > 0.5), mean-reverting (H < 0.5), or random (H = 0.5).

How it Works in the Script: The script employs a method based on Rescaled Range (R/S) analysis. It calculates the average range of price movements over increasingly larger time lags (m1, m2, m4, m8...). The slope of the line plotting log(range) vs. log(lag) is the Hurst Exponent. Applying this complex statistical analysis not to the raw price, but to the clean, wavelet-decomposed trend lines, is a key innovation of IGMD.

3. The Fractal Dimension Kernel (The "Complexity Compass")

What it is: This kernel measures the geometric complexity or "jaggedness" of a price path, based on the principles of fractal geometry. A straight line has a dimension of 1; a chaotic, space-filling line approaches a dimension of 2.

How it Works in the Script: We use a version based on Ehlers' Fractal Dimension Index (FDI). It calculates the rate of price change over a full lookback period (N3) and compares it to the sum of the rates of change over the two halves of that period (N1 + N2). The formula d = (log(N1 + N2) - log(N3)) / log(2) quantifies how much "longer" and more convoluted the price path was than a simple straight line. This kernel is our primary filter for tradeable (low complexity) vs. untradeable (high complexity) conditions.

4. The Shannon Entropy Kernel (The "Uncertainty Meter")

What it is: This kernel comes from Information Theory and provides the purest mathematical measure of information, surprise, or uncertainty within a system. It is not a measure of volatility; a market moving predictably up by 10 points every bar has high volatility but zero entropy .

How it Works in the Script: The script normalizes price returns by the ATR, categorizes them into a discrete number of "bins" over a lookback window, and forms a probability distribution. The Shannon Entropy H = -Σ(p_i * log(p_i)) is calculated from this distribution. A low H means returns are predictable. A high H means returns are chaotic. This kernel is our ultimate gauge of market conviction.

5. The Transfer Entropy Kernel (The "Causality Probe")

What it is: This is by far the most advanced and computationally intensive kernel in the script. Transfer Entropy is a non-parametric measure of directed information flow between two time series. It moves beyond correlation to ask: "Does knowing the past of Volume genuinely reduce our uncertainty about the future of Price?"

How it Works in the Script: To make this work, the script discretizes both price returns and the chosen "driver" (e.g., OBV) into three states: "up," "down," or "neutral." It then builds complex conditional probability tables to measure the flow of information in both directions. The Net Transfer Entropy (TE Driver→Price minus TE Price→Driver) gives us a direct measure of causality . A positive score means the driver is leading price, confirming the validity of the move. This is a profound leap beyond traditional indicator analysis.

Chapter 3: Fusion & Interpretation - The Field Score & Dashboard

Each kernel is a specialist providing a piece of the puzzle. The Field Score is where they are fused into a single, comprehensive reading. It's a weighted sum of the normalized scores from all five kernels, producing a single number from -1 (maximum bearish information field) to +1 (maximum bullish information field). This is the ultimate "at-a-glance" metric for the market's net state, and it is interpreted through the dashboard.

The Dashboard: Your Mission Control

Field Score & Regime: The master metric and its plain-English interpretation ("Uptrend Field", "Downtrend Field", "Transitional").

Kernel Readouts (Wave Align, H(w), FDI, etc.): The live scores of each individual kernel. This allows you to see why the Field Score is what it is. A high Field Score with all components in agreement (all green or red) is a state of High Coherence and represents a high-quality setup.

Market Context: Standard metrics like RSI and Volume for additional confluence.

Signals: The raw and adjusted confluence counts and the final, calculated probability scores for potential long and short entries.

Pattern: Shows the dominant candlestick pattern detected within the currently forming APEX range box and its calculated confidence percentage.

Chapter 4: Mastering the Controls - The Inputs Menu

Every parameter is a lever to fine-tune the IGMD engine.

📊 Wavelet Transform: Kernel ( Haar for sharp moves, db2 for smooth trends) and Scales (depth of analysis) let you tune the script's core microscope to your asset's personality.

📈 Hurst Exponent: The Window determines if you're assessing short-term or long-term market memory.

🔍 Fractal Dimension & ⚡ Entropy Volatility: Adjust the lookback windows to make these kernels more or less sensitive to recent price action. Always keep "Normalize by ATR" enabled for Entropy for consistent results.

🔄 Transfer Entropy: Driver lets you choose what causal force to measure (e.g., OBV, Volume, or even an external symbol like VIX). The throttle setting is a crucial performance tool, allowing you to balance precision with script speed.

⚡ Field Fusion • Weights: This is where you can customize the model's "brain." Increase the weights for the kernels that best align with your trading philosophy (e.g., w_hurst for trend followers, w_fdi for chop avoiders).

📊 Signal Engine: Mode offers presets from Conservative to Aggressive . Min Confluence sets your evidence threshold. Dynamic Confluence is a powerful feature that automatically adapts this threshold to the market regime.

🎨 Visuals & 📏 Support/Resistance: These inputs give you full control over the chart's appearance, allowing you to toggle every visual element for a setup that is as clean or as data-rich as you desire.

Chapter 5: Reading the Battlefield - On-Chart Visuals

Pattern Boxes (The Large Rectangles): These are not simple range boxes. They appear when the Field Score crosses a significance threshold, signaling a potential ignition point.

Color: The color reflects the dominant candlestick pattern that has occurred within that box's duration (e.g., green for Bull Engulf).

Label: Displays the dominant pattern, its duration in bars, and a calculated Confidence % based on field strength and pattern clarity.

Bar Pattern Boxes (The Small Boxes): If enabled, these highlight individual, significant candlestick patterns ( BE for Bull Engulf, H for Hammer) on a bar-by-bar basis.

Signal Markers (▲ and ▼): These appear only when the Signal Engine's criteria are all met. The number is the calculated Probability Score .

RR Rails (Dashed Lines): When a signal appears, these lines automatically plot the Entry, Stop Loss (based on ATR), and two Take Profit targets (based on Risk/Reward ratios). They dynamically break and disappear as price touches each level.

Support & Resistance Lines: Plots of the highest high ( Resistance ) and lowest low ( Support ) over a lookback, providing key structural levels.

Chapter 6: Development Philosophy & A Final Word

One single question: " What is the market really doing? " It represents a triumph of complexity, blending concepts from signal processing, chaos theory, and information theory into a cohesive framework. It is offered for educational and analytical purposes and does not constitute financial advice. Its goal is to elevate your analysis from interpreting flat shadows to measuring the rich, geometric reality of the market's information field.

As the great mathematician Benoit Mandelbrot , father of fractal geometry, noted:

"Clouds are not spheres, mountains are not cones, coastlines are not circles, and bark is not smooth, nor does lightning travel in a straight line."

Neither does the market. IGMD is a tool designed to navigate that beautiful, complex, and fractal reality.

— Dskyz, Trade with insight. Trade with anticipation.

US Macro Cycle (Z-Score Model)US Macro Cycle (Z-Score Model)

This indicator tracks the US economic cycle in real time using a weighted composite of seven macro and market-based indicators, each converted into a rolling Z-score for comparability. The model identifies the current phase of the cycle — Expansion, Peak, Contraction, or Recovery — and suggests sector tilts based on historical performance in each phase.

Core Components:

Yield Curve (10y–2y): Positive & steepening = growth; inverted = slowdown risk.

Credit Spreads (HYG/LQD): Tightening = risk-on; widening = risk-off.

Sector Leadership (Cyclicals vs. Defensives): Measures market leadership regime.

Copper/Gold Ratio: Higher copper = growth signal; higher gold = defensive.

SPY vs. 200-day MA: Equity trend strength.

SPY/IEF Ratio: Stocks vs. bonds relative strength.

VIX (Inverted): Low/falling volatility = supportive; high/rising = risk-off.

Methodology:

Each series is transformed into a rolling Z-score over the selected lookback period (optionally using median/MAD for robustness and winsorization to clip outliers).

Z-scores are combined using user-defined weights and normalized.

The smoothed composite is compared against phase thresholds to classify the macro environment.

Features:

Customizable Weights: Emphasize the indicators most relevant to your strategy.

Adjustable Thresholds: Fine-tune cycle phase definitions.

Background Coloring: Visual cue for the current phase.

Summary Table: Displays composite Z, confidence %, and individual Z-scores.

Alerts: Trigger when the phase changes, with details on the composite score and recommended tilt.

Use Cases:

Align sector rotation or relative strength strategies with the macro backdrop.

Identify favorable or defensive phases for tactical allocation.

Monitor macro turning points to manage portfolio risk.

It's doesn't fill nan gaps so there is quite a bit of zeroes, non-repainting.

Kelly Position Size CalculatorThis position sizing calculator implements the Kelly Criterion, developed by John L. Kelly Jr. at Bell Laboratories in 1956, to determine mathematically optimal position sizes for maximizing long-term wealth growth. Unlike arbitrary position sizing methods, this tool provides a scientifically solution based on your strategy's actual performance statistics and incorporates modern refinements from over six decades of academic research.

The Kelly Criterion addresses a fundamental question in capital allocation: "What fraction of capital should be allocated to each opportunity to maximize growth while avoiding ruin?" This question has profound implications for financial markets, where traders and investors constantly face decisions about optimal capital allocation (Van Tharp, 2007).

Theoretical Foundation

The Kelly Criterion for binary outcomes is expressed as f* = (bp - q) / b, where f* represents the optimal fraction of capital to allocate, b denotes the risk-reward ratio, p indicates the probability of success, and q represents the probability of loss (Kelly, 1956). This formula maximizes the expected logarithm of wealth, ensuring maximum long-term growth rate while avoiding the risk of ruin.

The mathematical elegance of Kelly's approach lies in its derivation from information theory. Kelly's original work was motivated by Claude Shannon's information theory (Shannon, 1948), recognizing that maximizing the logarithm of wealth is equivalent to maximizing the rate of information transmission. This connection between information theory and wealth accumulation provides a deep theoretical foundation for optimal position sizing.

The logarithmic utility function underlying the Kelly Criterion naturally embodies several desirable properties for capital management. It exhibits decreasing marginal utility, penalizes large losses more severely than it rewards equivalent gains, and focuses on geometric rather than arithmetic mean returns, which is appropriate for compounding scenarios (Thorp, 2006).

Scientific Implementation

This calculator extends beyond basic Kelly implementation by incorporating state of the art refinements from academic research:

Parameter Uncertainty Adjustment: Following Michaud (1989), the implementation applies Bayesian shrinkage to account for parameter estimation error inherent in small sample sizes. The adjustment formula f_adjusted = f_kelly × confidence_factor + f_conservative × (1 - confidence_factor) addresses the overconfidence bias documented by Baker and McHale (2012), where the confidence factor increases with sample size and the conservative estimate equals 0.25 (quarter Kelly).

Sample Size Confidence: The reliability of Kelly calculations depends critically on sample size. Research by Browne and Whitt (1996) provides theoretical guidance on minimum sample requirements, suggesting that at least 30 independent observations are necessary for meaningful parameter estimates, with 100 or more trades providing reliable estimates for most trading strategies.

Universal Asset Compatibility: The calculator employs intelligent asset detection using TradingView's built-in symbol information, automatically adapting calculations for different asset classes without manual configuration.

ASSET SPECIFIC IMPLEMENTATION

Equity Markets: For stocks and ETFs, position sizing follows the calculation Shares = floor(Kelly Fraction × Account Size / Share Price). This straightforward approach reflects whole share constraints while accommodating fractional share trading capabilities.

Foreign Exchange Markets: Forex markets require lot-based calculations following Lot Size = Kelly Fraction × Account Size / (100,000 × Base Currency Value). The calculator automatically handles major currency pairs with appropriate pip value calculations, following industry standards described by Archer (2010).

Futures Markets: Futures position sizing accounts for leverage and margin requirements through Contracts = floor(Kelly Fraction × Account Size / Margin Requirement). The calculator estimates margin requirements as a percentage of contract notional value, with specific adjustments for micro-futures contracts that have smaller sizes and reduced margin requirements (Kaufman, 2013).

Index and Commodity Markets: These markets combine characteristics of both equity and futures markets. The calculator automatically detects whether instruments are cash-settled or futures-based, applying appropriate sizing methodologies with correct point value calculations.

Risk Management Integration

The calculator integrates sophisticated risk assessment through two primary modes:

Stop Loss Integration: When fixed stop-loss levels are defined, risk calculation follows Risk per Trade = Position Size × Stop Loss Distance. This ensures that the Kelly fraction accounts for actual risk exposure rather than theoretical maximum loss, with stop-loss distance measured in appropriate units for each asset class.

Strategy Drawdown Assessment: For discretionary exit strategies, risk estimation uses maximum historical drawdown through Risk per Trade = Position Value × (Maximum Drawdown / 100). This approach assumes that individual trade losses will not exceed the strategy's historical maximum drawdown, providing a reasonable estimate for strategies with well-defined risk characteristics.

Fractional Kelly Approaches

Pure Kelly sizing can produce substantial volatility, leading many practitioners to adopt fractional Kelly approaches. MacLean, Sanegre, Zhao, and Ziemba (2004) analyze the trade-offs between growth rate and volatility, demonstrating that half-Kelly typically reduces volatility by approximately 75% while sacrificing only 25% of the growth rate.

The calculator provides three primary Kelly modes to accommodate different risk preferences and experience levels. Full Kelly maximizes growth rate while accepting higher volatility, making it suitable for experienced practitioners with strong risk tolerance and robust capital bases. Half Kelly offers a balanced approach popular among professional traders, providing optimal risk-return balance by reducing volatility significantly while maintaining substantial growth potential. Quarter Kelly implements a conservative approach with low volatility, recommended for risk-averse traders or those new to Kelly methodology who prefer gradual introduction to optimal position sizing principles.

Empirical Validation and Performance

Extensive academic research supports the theoretical advantages of Kelly sizing. Hakansson and Ziemba (1995) provide a comprehensive review of Kelly applications in finance, documenting superior long-term performance across various market conditions and asset classes. Estrada (2008) analyzes Kelly performance in international equity markets, finding that Kelly-based strategies consistently outperform fixed position sizing approaches over extended periods across 19 developed markets over a 30-year period.

Several prominent investment firms have successfully implemented Kelly-based position sizing. Pabrai (2007) documents the application of Kelly principles at Berkshire Hathaway, noting Warren Buffett's concentrated portfolio approach aligns closely with Kelly optimal sizing for high-conviction investments. Quantitative hedge funds, including Renaissance Technologies and AQR, have incorporated Kelly-based risk management into their systematic trading strategies.

Practical Implementation Guidelines

Successful Kelly implementation requires systematic application with attention to several critical factors:

Parameter Estimation: Accurate parameter estimation represents the greatest challenge in practical Kelly implementation. Brown (1976) notes that small errors in probability estimates can lead to significant deviations from optimal performance. The calculator addresses this through Bayesian adjustments and confidence measures.

Sample Size Requirements: Users should begin with conservative fractional Kelly approaches until achieving sufficient historical data. Strategies with fewer than 30 trades may produce unreliable Kelly estimates, regardless of adjustments. Full confidence typically requires 100 or more independent trade observations.

Market Regime Considerations: Parameters that accurately describe historical performance may not reflect future market conditions. Ziemba (2003) recommends regular parameter updates and conservative adjustments when market conditions change significantly.

Professional Features and Customization

The calculator provides comprehensive customization options for professional applications:

Multiple Color Schemes: Eight professional color themes (Gold, EdgeTools, Behavioral, Quant, Ocean, Fire, Matrix, Arctic) with dark and light theme compatibility ensure optimal visibility across different trading environments.

Flexible Display Options: Adjustable table size and position accommodate various chart layouts and user preferences, while maintaining analytical depth and clarity.

Comprehensive Results: The results table presents essential information including asset specifications, strategy statistics, Kelly calculations, sample confidence measures, position values, risk assessments, and final position sizes in appropriate units for each asset class.

Limitations and Considerations

Like any analytical tool, the Kelly Criterion has important limitations that users must understand:

Stationarity Assumption: The Kelly Criterion assumes that historical strategy statistics represent future performance characteristics. Non-stationary market conditions may invalidate this assumption, as noted by Lo and MacKinlay (1999).

Independence Requirement: Each trade should be independent to avoid correlation effects. Many trading strategies exhibit serial correlation in returns, which can affect optimal position sizing and may require adjustments for portfolio applications.

Parameter Sensitivity: Kelly calculations are sensitive to parameter accuracy. Regular calibration and conservative approaches are essential when parameter uncertainty is high.

Transaction Costs: The implementation incorporates user-defined transaction costs but assumes these remain constant across different position sizes and market conditions, following Ziemba (2003).

Advanced Applications and Extensions

Multi-Asset Portfolio Considerations: While this calculator optimizes individual position sizes, portfolio-level applications require additional considerations for correlation effects and aggregate risk management. Simplified portfolio approaches include treating positions independently with correlation adjustments.

Behavioral Factors: Behavioral finance research reveals systematic biases that can interfere with Kelly implementation. Kahneman and Tversky (1979) document loss aversion, overconfidence, and other cognitive biases that lead traders to deviate from optimal strategies. Successful implementation requires disciplined adherence to calculated recommendations.

Time-Varying Parameters: Advanced implementations may incorporate time-varying parameter models that adjust Kelly recommendations based on changing market conditions, though these require sophisticated econometric techniques and substantial computational resources.

Comprehensive Usage Instructions and Practical Examples

Implementation begins with loading the calculator on your desired trading instrument's chart. The system automatically detects asset type across stocks, forex, futures, and cryptocurrency markets while extracting current price information. Navigation to the indicator settings allows input of your specific strategy parameters.

Strategy statistics configuration requires careful attention to several key metrics. The win rate should be calculated from your backtest results using the formula of winning trades divided by total trades multiplied by 100. Average win represents the sum of all profitable trades divided by the number of winning trades, while average loss calculates the sum of all losing trades divided by the number of losing trades, entered as a positive number. The total historical trades parameter requires the complete number of trades in your backtest, with a minimum of 30 trades recommended for basic functionality and 100 or more trades optimal for statistical reliability. Account size should reflect your available trading capital, specifically the risk capital allocated for trading rather than total net worth.

Risk management configuration adapts to your specific trading approach. The stop loss setting should be enabled if you employ fixed stop-loss exits, with the stop loss distance specified in appropriate units depending on the asset class. For stocks, this distance is measured in dollars, for forex in pips, and for futures in ticks. When stop losses are not used, the maximum strategy drawdown percentage from your backtest provides the risk assessment baseline. Kelly mode selection offers three primary approaches: Full Kelly for aggressive growth with higher volatility suitable for experienced practitioners, Half Kelly for balanced risk-return optimization popular among professional traders, and Quarter Kelly for conservative approaches with reduced volatility.

Display customization ensures optimal integration with your trading environment. Eight professional color themes provide optimization for different chart backgrounds and personal preferences. Table position selection allows optimal placement within your chart layout, while table size adjustment ensures readability across different screen resolutions and viewing preferences.

Detailed Practical Examples

Example 1: SPY Swing Trading Strategy

Consider a professionally developed swing trading strategy for SPY (S&P 500 ETF) with backtesting results spanning 166 total trades. The strategy achieved 110 winning trades, representing a 66.3% win rate, with an average winning trade of $2,200 and average losing trade of $862. The maximum drawdown reached 31.4% during the testing period, and the available trading capital amounts to $25,000. This strategy employs discretionary exits without fixed stop losses.

Implementation requires loading the calculator on the SPY daily chart and configuring the parameters accordingly. The win rate input receives 66.3, while average win and loss inputs receive 2200 and 862 respectively. Total historical trades input requires 166, with account size set to 25000. The stop loss function remains disabled due to the discretionary exit approach, with maximum strategy drawdown set to 31.4%. Half Kelly mode provides the optimal balance between growth and risk management for this application.

The calculator generates several key outputs for this scenario. The risk-reward ratio calculates automatically to 2.55, while the Kelly fraction reaches approximately 53% before scientific adjustments. Sample confidence achieves 100% given the 166 trades providing high statistical confidence. The recommended position settles at approximately 27% after Half Kelly and Bayesian adjustment factors. Position value reaches approximately $6,750, translating to 16 shares at a $420 SPY price. Risk per trade amounts to approximately $2,110, representing 31.4% of position value, with expected value per trade reaching approximately $1,466. This recommendation represents the mathematically optimal balance between growth potential and risk management for this specific strategy profile.

Example 2: EURUSD Day Trading with Stop Losses

A high-frequency EURUSD day trading strategy demonstrates different parameter requirements compared to swing trading approaches. This strategy encompasses 89 total trades with a 58% win rate, generating an average winning trade of $180 and average losing trade of $95. The maximum drawdown reached 12% during testing, with available capital of $10,000. The strategy employs fixed stop losses at 25 pips and take profit targets at 45 pips, providing clear risk-reward parameters.

Implementation begins with loading the calculator on the EURUSD 1-hour chart for appropriate timeframe alignment. Parameter configuration includes win rate at 58, average win at 180, and average loss at 95. Total historical trades input receives 89, with account size set to 10000. The stop loss function is enabled with distance set to 25 pips, reflecting the fixed exit strategy. Quarter Kelly mode provides conservative positioning due to the smaller sample size compared to the previous example.

Results demonstrate the impact of smaller sample sizes on Kelly calculations. The risk-reward ratio calculates to 1.89, while the Kelly fraction reaches approximately 32% before adjustments. Sample confidence achieves 89%, providing moderate statistical confidence given the 89 trades. The recommended position settles at approximately 7% after Quarter Kelly application and Bayesian shrinkage adjustment for the smaller sample. Position value amounts to approximately $700, translating to 0.07 standard lots. Risk per trade reaches approximately $175, calculated as 25 pips multiplied by lot size and pip value, with expected value per trade at approximately $49. This conservative position sizing reflects the smaller sample size, with position sizes expected to increase as trade count surpasses 100 and statistical confidence improves.

Example 3: ES1! Futures Systematic Strategy

Systematic futures trading presents unique considerations for Kelly criterion application, as demonstrated by an E-mini S&P 500 futures strategy encompassing 234 total trades. This systematic approach achieved a 45% win rate with an average winning trade of $1,850 and average losing trade of $720. The maximum drawdown reached 18% during the testing period, with available capital of $50,000. The strategy employs 15-tick stop losses with contract specifications of $50 per tick, providing precise risk control mechanisms.

Implementation involves loading the calculator on the ES1! 15-minute chart to align with the systematic trading timeframe. Parameter configuration includes win rate at 45, average win at 1850, and average loss at 720. Total historical trades receives 234, providing robust statistical foundation, with account size set to 50000. The stop loss function is enabled with distance set to 15 ticks, reflecting the systematic exit methodology. Half Kelly mode balances growth potential with appropriate risk management for futures trading.

Results illustrate how favorable risk-reward ratios can support meaningful position sizing despite lower win rates. The risk-reward ratio calculates to 2.57, while the Kelly fraction reaches approximately 16%, lower than previous examples due to the sub-50% win rate. Sample confidence achieves 100% given the 234 trades providing high statistical confidence. The recommended position settles at approximately 8% after Half Kelly adjustment. Estimated margin per contract amounts to approximately $2,500, resulting in a single contract allocation. Position value reaches approximately $2,500, with risk per trade at $750, calculated as 15 ticks multiplied by $50 per tick. Expected value per trade amounts to approximately $508. Despite the lower win rate, the favorable risk-reward ratio supports meaningful position sizing, with single contract allocation reflecting appropriate leverage management for futures trading.

Example 4: MES1! Micro-Futures for Smaller Accounts

Micro-futures contracts provide enhanced accessibility for smaller trading accounts while maintaining identical strategy characteristics. Using the same systematic strategy statistics from the previous example but with available capital of $15,000 and micro-futures specifications of $5 per tick with reduced margin requirements, the implementation demonstrates improved position sizing granularity.

Kelly calculations remain identical to the full-sized contract example, maintaining the same risk-reward dynamics and statistical foundations. However, estimated margin per contract reduces to approximately $250 for micro-contracts, enabling allocation of 4-5 micro-contracts. Position value reaches approximately $1,200, while risk per trade calculates to $75, derived from 15 ticks multiplied by $5 per tick. This granularity advantage provides better position size precision for smaller accounts, enabling more accurate Kelly implementation without requiring large capital commitments.

Example 5: Bitcoin Swing Trading

Cryptocurrency markets present unique challenges requiring modified Kelly application approaches. A Bitcoin swing trading strategy on BTCUSD encompasses 67 total trades with a 71% win rate, generating average winning trades of $3,200 and average losing trades of $1,400. Maximum drawdown reached 28% during testing, with available capital of $30,000. The strategy employs technical analysis for exits without fixed stop losses, relying on price action and momentum indicators.

Implementation requires conservative approaches due to cryptocurrency volatility characteristics. Quarter Kelly mode is recommended despite the high win rate to account for crypto market unpredictability. Expected position sizing remains reduced due to the limited sample size of 67 trades, requiring additional caution until statistical confidence improves. Regular parameter updates are strongly recommended due to cryptocurrency market evolution and changing volatility patterns that can significantly impact strategy performance characteristics.

Advanced Usage Scenarios

Portfolio position sizing requires sophisticated consideration when running multiple strategies simultaneously. Each strategy should have its Kelly fraction calculated independently to maintain mathematical integrity. However, correlation adjustments become necessary when strategies exhibit related performance patterns. Moderately correlated strategies should receive individual position size reductions of 10-20% to account for overlapping risk exposure. Aggregate portfolio risk monitoring ensures total exposure remains within acceptable limits across all active strategies. Professional practitioners often consider using lower fractional Kelly approaches, such as Quarter Kelly, when running multiple strategies simultaneously to provide additional safety margins.

Parameter sensitivity analysis forms a critical component of professional Kelly implementation. Regular validation procedures should include monthly parameter updates using rolling 100-trade windows to capture evolving market conditions while maintaining statistical relevance. Sensitivity testing involves varying win rates by ±5% and average win/loss ratios by ±10% to assess recommendation stability under different parameter assumptions. Out-of-sample validation reserves 20% of historical data for parameter verification, ensuring that optimization doesn't create curve-fitted results. Regime change detection monitors actual performance against expected metrics, triggering parameter reassessment when significant deviations occur.

Risk management integration requires professional overlay considerations beyond pure Kelly calculations. Daily loss limits should cease trading when daily losses exceed twice the calculated risk per trade, preventing emotional decision-making during adverse periods. Maximum position limits should never exceed 25% of account value in any single position regardless of Kelly recommendations, maintaining diversification principles. Correlation monitoring reduces position sizes when holding multiple correlated positions that move together during market stress. Volatility adjustments consider reducing position sizes during periods of elevated VIX above 25 for equity strategies, adapting to changing market conditions.

Troubleshooting and Optimization

Professional implementation often encounters specific challenges requiring systematic troubleshooting approaches. Zero position size displays typically result from insufficient capital for minimum position sizes, negative expected values, or extremely conservative Kelly calculations. Solutions include increasing account size, verifying strategy statistics for accuracy, considering Quarter Kelly mode for conservative approaches, or reassessing overall strategy viability when fundamental issues exist.

Extremely high Kelly fractions exceeding 50% usually indicate underlying problems with parameter estimation. Common causes include unrealistic win rates, inflated risk-reward ratios, or curve-fitted backtest results that don't reflect genuine trading conditions. Solutions require verifying backtest methodology, including all transaction costs in calculations, testing strategies on out-of-sample data, and using conservative fractional Kelly approaches until parameter reliability improves.

Low sample confidence below 50% reflects insufficient historical trades for reliable parameter estimation. This situation demands gathering additional trading data, using Quarter Kelly approaches until reaching 100 or more trades, applying extra conservatism in position sizing, and considering paper trading to build statistical foundations without capital risk.

Inconsistent results across similar strategies often stem from parameter estimation differences, market regime changes, or strategy degradation over time. Professional solutions include standardizing backtest methodology across all strategies, updating parameters regularly to reflect current conditions, and monitoring live performance against expectations to identify deteriorating strategies.

Position sizes that appear inappropriately large or small require careful validation against traditional risk management principles. Professional standards recommend never risking more than 2-3% per trade regardless of Kelly calculations. Calibration should begin with Quarter Kelly approaches, gradually increasing as comfort and confidence develop. Most institutional traders utilize 25-50% of full Kelly recommendations to balance growth with prudent risk management.

Market condition adjustments require dynamic approaches to Kelly implementation. Trending markets may support full Kelly recommendations when directional momentum provides favorable conditions. Ranging or volatile markets typically warrant reducing to Half or Quarter Kelly to account for increased uncertainty. High correlation periods demand reducing individual position sizes when multiple positions move together, concentrating risk exposure. News and event periods often justify temporary position size reductions during high-impact releases that can create unpredictable market movements.

Performance monitoring requires systematic protocols to ensure Kelly implementation remains effective over time. Weekly reviews should compare actual versus expected win rates and average win/loss ratios to identify parameter drift or strategy degradation. Position size efficiency and execution quality monitoring ensures that calculated recommendations translate effectively into actual trading results. Tracking correlation between calculated and realized risk helps identify discrepancies between theoretical and practical risk exposure.

Monthly calibration provides more comprehensive parameter assessment using the most recent 100 trades to maintain statistical relevance while capturing current market conditions. Kelly mode appropriateness requires reassessment based on recent market volatility and performance characteristics, potentially shifting between Full, Half, and Quarter Kelly approaches as conditions change. Transaction cost evaluation ensures that commission structures, spreads, and slippage estimates remain accurate and current.

Quarterly strategic reviews encompass comprehensive strategy performance analysis comparing long-term results against expectations and identifying trends in effectiveness. Market regime assessment evaluates parameter stability across different market conditions, determining whether strategy characteristics remain consistent or require fundamental adjustments. Strategic modifications to position sizing methodology may become necessary as markets evolve or trading approaches mature, ensuring that Kelly implementation continues supporting optimal capital allocation objectives.

Professional Applications