SenxseAiSenxseiAI is a fully modular, multi-framework trading system designed for precision, clarity, and ease of use.

This tool blends market structure, dynamic S/R mapping, trend-logic, and session-based liquidity levels into a unified visual workflow. It highlights real-time entry signals with clean rays and labeled flags, while optional session, daily, and weekly highs/lows anchor traders to key liquidity points. A comprehensive theme engine—with multiple color packs and custom overrides—allows the interface to adapt to any chart style or user preference.

The UI is intentionally minimal, using toggle-based controls instead of overwhelming parameter lists, making the script beginner-friendly while maintaining professional depth.

Cari skrip untuk "session"

Absorption PROOF - Absorption PRO (Clean & Smart)Ultra-clean, high-precision absorption reversal strategy.Detects institutional buying/selling pressure using volume-weighted delta proxy and VWAP deviation zones.Smart RSI + early-session range filter automatically separates valid range-bound reversals from trend exhaustion.Green/Red circles → High-probability entries (fully tradable)

Small crosses + colored zones → Rejected signals (avoid)

Blue dotted lines → Session range ±100% deviation levels (optional)

By default: only signals and rejection zones displayed — zero clutter.Minimalist, professional, and deadly accurate on futures & forex (1m–15m).Less noise. Better trades.

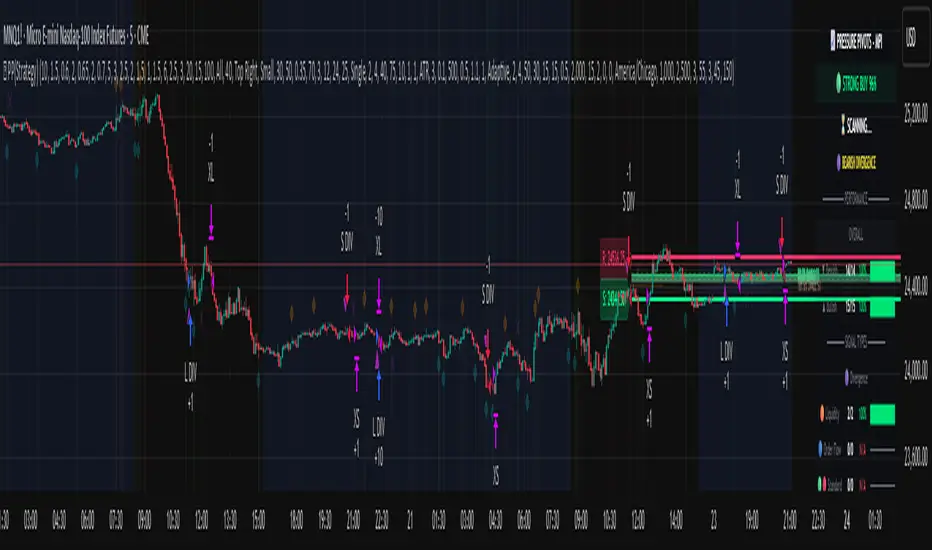

Pressure Pivots - MPI (Strategy)⇋ PRESSURE PIVOTS — MARKET PRESSURE INDEX STRATEGY

A comprehensive reversal trading system that combines order flow pressure analysis, multi-factor confluence detection, and adaptive machine learning to identify high-probability turning points in liquid markets.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

CORE INNOVATION: MARKET PRESSURE INDEX (MPI)

Traditional indicators measure price movement. The Market Pressure Index measures the force behind the movement.

How MPI Works:

Every bar tells two stories through volume distribution:

• Buy Pressure: Volume × (Close - Low) / (High - Low)

• Sell Pressure: Volume × (High - Close) / (High - Low)

• Net Pressure: Buy Pressure - Sell Pressure

This raw pressure is then normalized against baseline activity to create the bounded MPI (-1.0 to +1.0):

• Smooth Pressure: EMA(Net Pressure, period)

• Baseline Activity: SMA(|Net Pressure|, period × 2)

• MPI: (Smooth Pressure / Baseline) × Sensitivity

What MPI Reveals:

MPI > +0.7: Extreme buy pressure → Exhaustion potential

MPI = +0.2 to +0.7: Healthy bullish momentum

MPI = -0.2 to +0.2: Neutral/balanced pressure

MPI = -0.7 to -0.2: Healthy bearish momentum

MPI < -0.7: Extreme sell pressure → Exhaustion potential

Why It Works:

Two bars can both move 10 points, but if one closes at the high on high volume (aggressive buying) and the other closes mid-range on average volume (weak buying), only MPI distinguishes between sustainable momentum and exhaustion. This volume-weighted pressure analysis reveals conviction behind price moves—the key to timing reversals.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SEVEN-FACTOR CONFLUENCE SYSTEM

MPI extremes alone aren't enough. The system requires multiple independent confirmations through weighted scoring:

1. DIVERGENCE (Weight: 3.0) — Premium Signal Type: DIV

Price makes new high but MPI makes lower high (or inverse for bullish)

• Detection: Tracks pivots with 5-bar lookback, compares price vs MPI at pivot points

• Signal: Purple triangles, highest weight (pressure weakening while price extends)

2. LIQUIDITY SWEEP (Weight: 2.5) — Premium Signal Type: LIQ

Price breaks swing high/low within 0.3 ATR then reverses

• Detection: Break within tolerance + close back through level

• Signal: Orange triangles, second-highest weight (stop hunt reversal)

3. ORDER FLOW IMBALANCE (Weight: 2.0) — Premium Signal Type: OF

Aggressive buying/selling 50% above normal

• Detection: EMA(aggressive volume) vs SMA(imbalance) threshold

• Signal: Aqua triangles, institutional positioning

4. VELOCITY EXHAUSTION (Weight: 1.5)

Parabolic move (2+ ATRs in 3 bars) + extreme MPI

• Detection: |3-bar price change / ATR| > threshold + MPI > ±0.5

• Indicates: Momentum deceleration, blow-off top/bottom

5. WICK REJECTION (Weight: 1.5)

Single bar: wick > 60% of range, or sequence: 2 bars with 40% + 30% wicks

• Detection: Shooting stars (bearish) or hammers (bullish)

• Indicates: Intrabar rejection, battle won by opposing side

6. VOLUME SPIKE (Weight: 1.0)

Volume > 20-bar average × multiplier (default: 2.0x)

• Detection: Participation surge confirmation

• Lowest weight: Can be manipulated, better as confirmation

7. POSITION FACTOR (Weight: 1.0)

At 10-bar highest (bearish) or lowest (bullish)

• Detection: Structural positioning for reversal

• Base requirement: Must be at extreme to score

Scoring Logic:

Premium Signals (DIV/LIQ/OF): Must score ≥6.0 (default premiumThreshold)

Standard Signals (STD): Must score ≥4.0 (default standardThreshold)

Example Scoring:

Divergence (3.0) + Liquidity Sweep (2.5) + Volume (1.0) = 6.5 → FIRES (DIV signal)

Recent High (1.0) + Wick (1.5) + Volume (1.0) + Velocity (1.5) = 5.0 → FIRES (STD signal)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ADAPTIVE LEARNING ENGINE

Unlike static strategies, this system learns from every trade and optimizes itself.

Performance Tracking:

Every trade records:

• Entry Score: Confluence level at entry

• Signal Type: DIV / LIQ / OF / STD

• Win/Loss: Boolean outcome

• R-Multiple: (Exit - Entry) / (Entry - Stop)

• MAE: Maximum Adverse Excursion (worst drawdown)

• MFE: Maximum Favorable Excursion (best profit reached)

Three Adaptive Parameters:

1. Signal Threshold Adaptation

If Win Rate < Target (45%): RAISE threshold → fewer signals, better quality

If Win Rate > Target + 10% AND good R: LOWER threshold → more signals, profitable

2. Stop Distance Adaptation

If Avg MAE > 0.85 AND WR < 50%: WIDEN stops → reduce premature exits

If Avg MAE < 0.4 AND WR > 55%: TIGHTEN stops → reduce risk

3. Target Distance Adaptation

If Avg MFE > Target × 1.5: EXTEND targets → capture more of runners

If Avg MFE < Target × 0.7: SHORTEN targets → take profits faster

Signal Type Filtering:

The system tracks performance by type (DIV/LIQ/OF/STD):

• If Type WR < 40% AND Avg R < 0.8: Type DISABLED

• If Type WR ≥ 40% OR Avg R ≥ 0.8: Type RE-ENABLED

Example: If OF signals consistently lose while DIV signals win, system automatically stops taking OF signals and focuses on DIV.

Warmup Period:

First 30 trades (default) gather baseline data with relaxed thresholds. After warmup, full adaptation activates.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPLETE POSITION MANAGEMENT

Dynamic Position Sizing:

Base Contracts = (Equity × Risk%) / (Stop Distance × Point Value)

Then multiplied by:

• Score Bonus: Up to +50% for highest-scoring signals

• Signal Type Bonus: DIV signals +50%, LIQ signals +30%

• Streak Multiplier: After 3 losses: 50% reduction, After 3 wins: 25% increase

Example: High-scoring DIV signal on winning streak = 3-4× larger position than weak STD signal on losing streak

Entry Modes:

Single Entry: Full size at once, exit at TP2 (or partial at TP1)

Tiered Entry: 40% at TP1 (2R), 60% at TP2 (4R adaptive)

Stop Management (3 Modes):

Structural: Beyond recent 20-bar swing high/low + buffer

ATR: Fixed ATR multiplier (default: 2.0 ATR, then adapts)

Hybrid: Attempt structural, fallback to ATR if invalid

Plus:

• Breakeven: Move stop to entry ± 1 tick when 1R reached

• Trailing: Activate when 1.5R reached, trail 0.8R behind price

• Max Loss Override: Cap dollar risk regardless of calculation

Target Management:

Fixed Mode: TP1 = 2R, TP2 = 4R

Adaptive Mode: TP1 = 2R fixed, TP2 adapts based on MFE analysis

Partial Exits: Default 50% at TP1, remainder at TP2 or trailing stop

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPREHENSIVE RISK CONTROLS

Daily Limits:

• Max Daily Loss: $2,000 default → HALT trading

• Max Daily Trades: 15 default → prevent overtrading

• Max Concurrent: 2 positions → limit correlation risk

Session Controls:

• Trading Hours: Specify start/end times + timezone

• Weekend Block: Optional (avoid crypto weekend volatility)

Prop Firm Protection (Live Trading Only):

• Daily Loss Limit: Stricter of general or prop limit ($1,000 default)

• Trailing Drawdown: Tracks high water mark, HALTS if breach ($2,500 default)

• Reset on Reload: Optional high water mark reset

Liquidity Filter (Optional):

• Time-Based: Avoid first/last X minutes of session

• Volume-Based: Require minimum volume ratio (0.5× average default)

Market Regime Filter (Optional):

• ADX-Based: Only trade when ADX > threshold (trending)

• Block: Consolidation (ADX < 20) or Transitional regimes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

REAL-TIME DASHBOARD

MPI Gauge Section:

Shows current pressure: 🟢 STRONG BUY (+0.5 to +1.0), 🟩 BUY PRESSURE (+0.2 to +0.5), ⚪ NEUTRAL (-0.2 to +0.2), 🟥 SELL PRESSURE (-0.5 to -0.2), 🔴 STRONG SELL (-1.0 to -0.5)

Signal Status Section:

• Active Signals: "🔴 DIV SELL" (purple background), "🟢 LIQ BUY" (orange), "🔵 OF SELL" (aqua), "🟢 STD BUY" (green)

• Warnings: "⚠️ BEAR WARNING" / "⚠️ BULL WARNING" (yellow) — setup forming, not full signal

• Scanning: "⏳ SCANNING..." (gray) — no signal active

• Confidence Bar: Visual score display "██████░░░░" showing confluence strength

Divergence Indicator:

"🟣 BEARISH DIVERGENCE" or "🟡 BULLISH DIVERGENCE" when detected

Performance Statistics:

• Overall Win Rate: Wins/Total with visual bar (lime ≥70%, yellow 50-70%, red <50%)

• Directional: Bearish vs Bullish win rates separately

• By Signal Type: DIV / LIQ / OF / STD individual performance tracking

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

KEY PARAMETERS EXPLAINED

🎯 Pressure Engine:

• MPI Period (5-50, default: 14): Smoothing period — lower for scalping, higher for position trading

• MPI Sensitivity (0.5-5.0, default: 1.5): Amplification — lower compresses range, higher more extremes

🔍 Detection:

• Wick Threshold (0.3-0.9, default: 0.6): Minimum wick-to-range ratio for rejection

• Volume Spike (1.2-3.0x, default: 2.0): Multiplier above average for spike

• Aggressive Ratio (0.5-0.9, default: 0.65): Close position in range for aggressive orders

• Velocity Threshold (1.0-5.0 ATR, default: 2.0): ATR-normalized move for exhaustion

• MPI Extreme (0.5-0.95, default: 0.7): Level considered overbought/oversold

⚖️ Weights:

• Divergence: 3.0 (highest — pressure weakening)

• Liquidity: 2.5 (second — stop hunts)

• Order Flow: 2.0 (institutional positioning)

• Velocity: 1.5 (momentum exhaustion)

• Wick: 1.5 (rejection patterns)

• Volume: 1.0 (lowest — can be manipulated)

🎚️ Thresholds:

• Premium (4.0-15.0, default: 6.0): Score for DIV/LIQ/OF signals

• Standard (2.0-8.0, default: 4.0): Score for STD signals

• Warning Confluence (1-4, default: 2): Factors for yellow diamond warnings

🧬 Adaptive:

• Enable (true/false, default: true): Master learning switch

• Warmup Trades (5-100, default: 30): Data collection before adaptation

• Lookback (20-200, default: 50): Recent trades for performance calculation

• Adapt Speed (0.05-0.50, default: 0.15): Parameter adjustment rate

• Target Win Rate (30-70%, default: 45%): Optimization goal

• Target R-Multiple (0.5-5.0, default: 1.5): Risk/reward goal

💼 Position:

• Base Risk (0.1-10.0%, default: 1.5%): Equity risked per trade

• Max Contracts (1-100, default: 10): Hard position limit

• DIV Bonus (1.0-3.0x, default: 1.5): Size multiplier for divergence signals

• LIQ Bonus (1.0-3.0x, default: 1.3): Size multiplier for liquidity signals

🛡️ Stops:

• Mode (Structural/ATR/Hybrid, default: ATR): Stop placement method

• ATR Multiplier (0.5-5.0, default: 2.0): Stop distance in ATRs (adapts)

• Breakeven at (0.3-3.0R, default: 1.0R): When to move stop to entry

• Trail Trigger (0.5-5.0R, default: 1.5R): When to activate trailing

• Trail Offset (0.3-3.0R, default: 0.8R): Distance behind price

🎯 Targets:

• Mode (Fixed/Adaptive, default: Fixed): Target placement method

• TP1 (0.5-10.0R, default: 2.0R): First target for partial exit

• TP2 (1.0-15.0R, default: 4.0R): Final target (adapts in adaptive mode)

• Partial % (0-100%, default: 50%): Position percentage to exit at TP1

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

PROFESSIONAL USAGE PROTOCOL

Phase 1: Paper Trading (Weeks 1-4)

• Setup: Default settings, all adaptive features ON, 0.5% base risk

• Goal: 30+ trades for warmup, observe MPI behavior and signal frequency

• Adjust: MPI sensitivity if stuck near neutral or always at extremes

• Threshold: Raise/lower if too many/few signals

Phase 2: Micro Live (Weeks 5-8)

• Requirements: WR >43%, at least one type >55%, Avg R >0.8

• Setup: 10-25% intended size, 0.5-1.0% risk, 1 position max

• Focus: Execution quality, match dashboard performance

• Journal: Screenshot every signal, track outcomes

Phase 3: Full Scale (Month 3+)

• Requirements: WR >45% over 50+ trades, Avg R >1.2, drawdown <15%

• Progression: Months 3-4 (1.0-1.5% risk), 5-6 (1.5-2.0%), 7+ (1.5-2.5%)

• Maintenance: Weekly dashboard review, monthly deep analysis

• Warnings: Reduce size if WR drops >10%, consecutive losses >7, or drawdown >20%

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DEVELOPMENT INSIGHTS

The Pressure Insight: Emerged from analyzing intrabar volume distribution. Within every candlestick, volume accumulates at different price levels. MPI deconstructs this to reveal conviction behind moves.

The Confluence Challenge: Early versions using MPI extremes alone achieved only 42% win rate. The seven-factor confluence system emerged from testing which combinations produced reliable reversals. Divergence + liquidity sweep became the strongest setup (68% win rate in isolation).

The Adaptive Breakthrough: Per-signal-type performance tracking revealed DIV signals winning at 71% while OF signals languished at 38%. Adaptive filtering disabled weak types automatically, recovering win rate from 39% to 54% during the 2022 volatility spike.

The Position Sizing Revelation: Dynamic sizing based on signal quality and recent performance increased Sharpe ratio from 1.2 to 1.9 while decreasing max drawdown from 18% to 12% over 500 trades. Bigger positions on better signals = geometric edge amplification.

The Risk Control Lesson: Testing with $50K accounts revealed catastrophic failure modes: daily loss cascades, overtrading commission bleed, weekend gap blowouts. Multi-layer controls (daily limits, concurrent caps, prop firm protection) became essential.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

LIMITATIONS & ASSUMPTIONS

What This Is NOT:

• NOT a Holy Grail: Typical performance 52-58% WR, 1.3-1.8 avg R, probabilistic edge

• NOT Predictive: Identifies high-probability conditions, doesn't forecast prices

• NOT Market-Agnostic: Best on liquid auction-driven markets (futures, forex, major crypto)

• NOT Hands-Off: Requires oversight for news events, gaps, system anomalies

• NOT Immune to Regime Changes: Adaptive engine helps but cannot predict black swans

Critical Assumptions:

1. Volume reflects intent (valid for regulated markets, violated by wash trading)

2. Pressure extremes mean-revert (true in ranging/exhaustion, fails in paradigm shifts)

3. Stop hunts exist (valid in liquid markets, less in thin/random walk periods)

4. Past patterns persist (valid in stable regimes, fails when structure fundamentally changes)

Works Best On: Major futures (ES, NQ, CL), liquid forex pairs (EUR/USD, GBP/USD), large-cap stocks, BTC

Performs Poorly On: Low-volume stocks, illiquid crypto pairs, news-driven headline events

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

RISK DISCLOSURE

Trading futures, forex, and leveraged instruments involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. This strategy is provided for educational purposes only and should not be construed as financial advice.

The adaptive engine learns from historical data—there is no guarantee that past relationships will persist. Market conditions change, volatility regimes shift, and black swan events occur. No strategy can eliminate the risk of loss.

Users must validate performance on their specific instruments and timeframes before risking capital. The developer makes no warranties regarding profitability or suitability. Users assume all responsibility for trading decisions and outcomes.

"The market doesn't care about your indicators. It only cares about pressure—who's willing to pay more, who's desperate to sell. Find the exhaustion. Trade the reversal. Let the system learn the rest."

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

AutoTrader v3.0[by Irum]1. 스크립트 목적 / 정의

1-1. 한글 설명

이 스크립트의 목적

15분봉 BTC/USDT 같은 레버리지/선물 환경에서,

“EMA 재돌파 + BB 스퀴즈 국면”에서만 진입하고,

상위 추세(레짐 필터) + ATR 기반 리스크/수량 + ATR 트레일링 + 부분청산을 한 번에 관리하는 “올인원 자동 전략”입니다.

핵심 특징:

진입 로직

EMA(기본 9) 를 기준으로

종가가 EMA를 위로 돌파(골든크로스) & BB 폭이 좁을 때 → Long 진입 후보

종가가 EMA를 아래로 돌파(데드크로스) & BB 폭이 좁을 때 → Short 진입 후보

이걸 “Re-break + Squeeze” 구조로 설계해서,

변동성이 줄었다가 방향이 다시 나오려는 시점만 노립니다.

레짐 필터(Regime Filter)

상위 타임프레임(기본 1시간봉 HTF EMA 200)의 기울기와

ATR 빠른 선/느린 선으로

상승 추세 + 변동성 살아있는 구간만 Long 허용

하락 추세 + 변동성 살아있는 구간만 Short 허용

즉, 역추세 매매를 최대한 차단하고, 추세 방향만 따라갑니다.

Pivot 기반 손절 + ATR 리스크 기반 수량(ATR Sizing v2.1)

최근 swing low/high(피벗) 또는 일정 구간 fallback low/high를 기준으로 기술적 손절선을 잡고,

그 손절까지의 거리를 이용해,

“한 번의 손절 시 계좌의 riskPct%만 잃도록” 수량을 자동 계산합니다.

ATR 스파이크(갑작스러운 변동성 폭발) 구간은 진입 자체를 피하려고 합니다.

R-multiple 기반 TP + 부분 청산 + ATR Ladder 트레일링

진입 시점의 위험(R = Entry - SL) 을 기준으로

R 배수 기준 부분청산(예: 1R에서 50% 청산)

R 배수 기준 최종 TP(예: 2R)

포지션이 잘 가면 ATR 기반 트레일링 스탑(ATR Ladder) 을 적용해서,

이익 구간에서 손절선을 점점 끌어올려 BE(본전 이상) → 수익 보호 모드로 전환합니다.

세션 필터 / 뉴욕 뉴스피크 회피용 세션 회피

사용자가 정한 세션 안에서만 매매하거나,

특정 뉴스 타임(예: CPI, FOMC 근처 시간대)을 회피하도록 시간대를 차단할 수 있습니다.

1-2. English Description

Purpose

This strategy is an all-in-one auto-trading system designed mainly for leveraged/futures markets (e.g., BTC/USDT 15m) that:

Enters only on EMA re-break + Bollinger Band squeeze

Uses higher timeframe regime filter for trend direction

Sizes positions with ATR-based risk (v2.1)

Manages exits with R-multiple partial TP + final TP + ATR ladder trailing stop

Key points:

Entry Logic

Uses a fast EMA (default 9).

When price crosses above EMA and BB width is below threshold (squeeze) → Long signal.

When price crosses below EMA and BB width is below threshold → Short signal.

So it focuses on volatility contraction → re-expansion setups.

Regime Filter

Uses HTF EMA (default 200 EMA on 60m) slope + fast vs slow ATR:

Only allow long trades in uptrend + active volatility

Only allow short trades in downtrend + active volatility

This is to avoid counter-trend trading and align with macro trend.

Pivot-based SL + ATR Sizing v2.1

Sets SL using recent pivot highs/lows with a minimum buffer.

Computes risk per unit and chooses quantity so that riskPct % of equity is lost at SL.

Filters out trades during ATR spikes (abnormally large volatility).

R-multiple TP + Partial + ATR Ladder Trailing

Uses the initial risk (R) to:

Take partial profit at partialRR R (e.g., 1R at 50% size).

Set final TP at finalRR R or a fixed % TP.

Uses ATR ladder trailing to progressively tighten stops as price moves in favor.

Session / News Avoidance

Optionally trade only inside a custom session,

Or avoid specific time windows (e.g., high-impact news).

CongTrader Strategy V1📈 CongTrader Strategy V1 — Official Overview

CongTrader Strategy V1 is a precision-built algorithm designed for intraday and swing traders who want a structured, rules-driven approach to capturing directional momentum while avoiding low-quality market conditions.

This strategy combines volatility-based logic, trend confirmation filters, and a market-conditioning engine to produce high-probability long and short signals with strictly candle-close confirmed entries (no intrabar repainting).

🔍 Core Philosophy

Modern markets move in bursts of volatility that are often preceded by subtle shifts in momentum and structure.

CongTrader V1 is engineered to:

identify emerging directional pressure early

filter out noise, consolidation, and choppy environments

only execute when multiple conditions align

maintain consistent, disciplined trade management

The result is a strategy that aims to trade quality over quantity, focusing on clear, structured setups rather than impulsive, intrabar signals.

🧠 Key Components (High-Level Explanation)

1️⃣ Directional Signal Engine (Trigger System)

The strategy uses a custom momentum-oscillation model to detect potential turning points and trend continuations.

This engine smooths price action, measures pressure extremes, and generates trigger crossovers that signal potential long or short opportunities.

(The exact formula and coefficients are proprietary and not displayed.)

2️⃣ ATR-Based Risk Management

Each trade is automatically paired with:

a volatility-adaptive stop loss, and

a volatility-adaptive profit target

This allows the strategy to adjust position management dynamically based on current market movement rather than fixed pip or dollar distances.

3️⃣ Trend Confirmation Filter (EMA)

A long-term EMA trend filter prevents counter-trend entries by ensuring:

Long positions trade only above trend

Short positions trade only below trend

This keeps signals aligned with higher-timeframe momentum.

4️⃣ VWAP Institutional Bias Filter

VWAP is used as a dynamic market fair-value reference.

The strategy only trades when price action shows favorable positioning relative to VWAP—helping avoid false moves and mean-reversion traps.

5️⃣ Range & Volatility Filter

A volatility/range filter avoids entering during tight consolidations.

If the market is not moving or lacks range expansion, the strategy waits patiently.

This significantly reduces chop and whipsaw trades.

6️⃣ RTH (Regular Trading Hours) Protection

Optionally limits trades to regular exchange hours for traders who avoid low-liquidity overnight sessions.

⏳ Candle-Close Entry Confirmation (No Repainting)

All entries are strictly confirmed after the bar closes, which means:

No intrabar fakeouts

No signal disappearance

No repainting

Cleaner, more realistic backtesting

This ensures the strategy behaves the same in backtests and in live charts.

🎯 Trade Logic Summary

A trade is only taken when:

✔ A directional trigger signal occurs

✔ Price meets VWAP bias conditions

✔ Price aligns with the long-term trend

✔ Sufficient volatility/range is present

✔ (Optional) Within regular trading hours

✔ The candle has fully confirmed

Every trade is managed automatically with ATR-based stop loss and take profit placement.

📊 Who This Strategy Is For

CongTrader V1 works well for:

Intraday traders (1–15m)

Swing traders (30m–4h)

Momentum and trend-followers

Algorithmic traders looking for disciplined, rules-based entries

Traders who want cleaner signals and less noise

Anyone who wants to avoid low-quality, choppy markets

🔔 Alerts Included

Built-in alerts notify you instantly when conditions for long or short entries are met, making it suitable for:

Manual execution

Automated trading systems

Signal services

🧩 Important Note

This strategy is designed for educational purposes and is not financial advice. Performance may vary depending on market conditions, broker feed, and instrument volatility. Always backtest thoroughly and use risk management.

Futures Fighter MO: Multi-Confluence Day Trading System ADX/SMI👋 Strategy Overview: The Multi-Confluence Mashup

The Futures Fighter MO is a comprehensive, multi-layered day trading strategy designed for experienced traders focusing on high-liquidity futures contracts (e.g., NQ, ES, R2K).

This strategy is a sophisticated mashup that uses the 1-minute chart for surgical entries while enforcing strict environmental filtering through higher-timeframe data. We aim to capture high-conviction moves only when multiple, uncorrelated signals align.

🧠 How the Logic Works (Concepts & Confluence)

Our logic is built on four pillars, which must align for a trade to be executed:

Primary Trend Filter

Indicators :

ADX/DMI (15-Minute Lookback)

Role :

Price action is filtered to ensure the ADX (17/14) is above 25, confirming a strong, prevailing market trend (Bullish or Bearish). Trades are strictly rejected during "Flat" (sideways) market regimes.

Entry Signal Types

The system uses multiple entry types:

- 🟢 Trend Long/Short: A breakout/rejection near the 200-Period EMA is confirmed by the primary ADX trend.

- 🔴 Engulfing Rejection: A strong signal when a Bullish/Bearish Engulfing or Doji prints near the long-term 500-Period EMA (emaGOD) while the Stochastic Momentum Index (SMI on 30M) is in an extreme overbought/oversold state (below $-40$ or above $40$).

Volatility & Volume Confirmation

Indicators: Average True Range (ATR) and 20-Period SMA of Volume

Role: Every entry requires a volume spike (Current Volume $> 1.5 \times$ SMA Volume) to confirm that the move is supported by significant liquidity. Volatility is tracked via ATR to define bar range and stop boundaries.

Structural Guardrails

Indicators: Daily Pivot Points (PP, S1-S3, R1-R3)

Role: Trades are disabled if the current bar's price range intersects with a Daily Pivot Point. This is a critical filter to avoid high-chop consolidation zones near key structural levels.

📊 Strategy Results & Required Disclosures

I strive to publish backtesting results that are transparent and realistic for the retail futures trader.

- Initial Capital: $50,000 - A realistic base for Mini/Micro futures contracts.

- Order Size: 1 Contract (Pyramiding up to 3) - Conservative risk relative to the account size.

- Commission: $0.11 USD per order - Represents realistic costs for low-cost brokers.

- Slippage: 2 Ticks - Accounts for expected market friction.

⚠️ Risk Management & Deviations

Stop-Loss: The strategy uses a dynamic stop-loss system where positions are closed upon a reversal (e.g., breaking the 50-Period EMA or failure to hold a Pivot Point), rather than a fixed tick-based stop. This is suited for experienced traders using a low relative risk (single Micro-contract entry) on a larger account. Users must confirm that the first entry's maximum potential loss remains below $10\%$ of their capital for compliance.

Trade Sample Size: Due to data limitations of the TradingView Essential plan (showing $\approx 50$ trades over 2 weeks), the sample size is under the ideal $100+$ target. Justification: This system is designed to generate signals across a portfolio of correlated futures markets (NQ, ES, R2K, Gold, Crude), meaning the real sample size for a user tracking the portfolio is significantly higher.

Drawdown Control: This strategy is designed for manual management. It requires the user to turn the script/alerts OFF after a significant drawdown and only reactivate it once a recovery trend is established externally.

The strategy uses a combination of dynamic trailing stops, structural support/resistance zones, and a fixed profit target to manage open positions.

🛑 Strategy Exit Logic

1. General Stop-Loss (Dynamic Trailing Stop)

These conditions act as the primary dynamic stop, closing the position if the market reverses past a key Moving Average (MA):

- Long Positions Closed When: The current bar's close crosses under the 50-Period EMA (emaLong).

- Short Positions Closed When: The current bar's close crosses above the 50-Period EMA (emaLong).

2. Profit Target (Fixed Percentage)

The script includes a general exit based on a user-defined profit percentage:

Take Profit Trigger: The position is closed when the currentProfitPercent meets or exceeds the input Profit Target (%) (default is 1.0% of the entry price).

3. Structural Exits (Daily Pivot Points)

These exits are high-priority, "close all" orders that trigger when the price fails to hold or reclaims a recent Daily Pivot Point, suggesting a failure of the current move.

- VR Close All - Long ($\sym{size} > 0$) - Price crosses under a Daily Resistance Level (R1, R2, or R3) minus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Resistance as support.

- VS Close All - Short ($\sym{size} < 0$) - Price crosses above a Daily Support Level (S1, S2, or S3) plus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Support as resistance.

4. Trend Failure Exit (Trend-Following Signals Only)

This exit protects against holding a position when the primary high-timeframe trend used for the entry has failed:

- Long Positions Closed When: The primary trend is no longer "bullish" for more than 2 consecutive bars (i.e., it turned "bearish" or "flat").

- Short Positions Closed When: The primary trend is no longer "bearish" for more than 2 consecutive bars (i.e., it turned "bullish" or "flat").

5. End of Day (EOD) Session Control

The final hard exits based on time:

- End of Session (EoS): At 11:30 AM, new trades are disabled (TradingDay := false). Open positions are kept.

- End of Day (EoD): At 1:30 PM, all remaining open positions are closed (strategy.close_all).

🤝 Development & Disclaimer

This script and description were created with assistance from Gemini and GitHub Copilot. My focus is on helping fellow real estate investors and day traders develop mechanically sound systems.

Disclaimer: This is for educational purposes only and does not constitute financial advice. Always abide by the Realtor Code and manage your own risk.

High Accuracy Engulfing Strategy [PIPNEXUS]Title: EMA Engulfing Setup

Description:

This indicator focuses on identifying strong engulfing patterns that form around the EMA line, helping traders catch high-probability moves in line with market direction.

Concept Overview:

The idea is simple — when both the engulfing candle and the candle being engulfed have their bodies touching the EMA line, it often represents a key point of rejection or continuation. These areas can produce clean entries with strong momentum.

How to Use:

1. Wait for a valid engulfing formation near the EMA line.

Both the engulfing and the engulfed candles should have their bodies touching the EMA.

2. Enter in the direction of the engulfing candle once the pattern is confirmed.

3. For pinpoint entries, observe the market during session changes (especially in the first 3–5 minutes after a session opens).

4. For longer and more stable trades, look for the same pattern on 15-minute or 1-hour charts.

5. Always align your trades with the prevailing market structure and avoid counter-trend setups.

Note:

This indicator is designed for technical and educational use. It does not generate buy or sell signals automatically, nor does it guarantee performance. Use it alongside your own market analysis and proper risk management.

TriAnchor Elastic Reversion US Market SPY and QQQ adaptedSummary in one paragraph

Mean-reversion strategy for liquid ETFs, index futures, large-cap equities, and major crypto on intraday to daily timeframes. It waits for three anchored VWAP stretches to become statistically extreme, aligns with bar-shape and breadth, and fades the move. Originality comes from fusing daily, weekly, and monthly AVWAP distances into a single ATR-normalized energy percentile, then gating with a robust Z-score and a session-safe gap filter.

Scope and intent

• Markets: SPY QQQ IWM NDX large caps liquid futures liquid crypto

• Timeframes: 5 min to 1 day

• Default demo: SPY on 60 min

• Purpose: fade stretched moves only when multi-anchor context and breadth agree

• Limits: strategy uses standard candles for signals and orders only

Originality and usefulness

• Unique fusion: tri-anchor AVWAP energy percentile plus robust Z of close plus shape-in-range gate plus breadth Z of SPY QQQ IWM

• Failure mode addressed: chasing extended moves and fading during index-wide thrusts

• Testability: each component is an input and visible in orders list via L and S tags

• Portable yardstick: distances are ATR-normalized so thresholds transfer across symbols

• Open source: method and implementation are disclosed for community review

Method overview in plain language

Base measures

• Range basis: ATR(length = atr_len) as the normalization unit

• Return basis: not used directly; we use rank statistics for stability

Components

• Tri-Anchor Energy: squared distances of price from daily, weekly, monthly AVWAPs, each divided by ATR, then summed and ranked to a percentile over base_len

• Robust Z of Close: median and MAD based Z to avoid outliers

• Shape Gate: position of close inside bar range to require capitulation for longs and exhaustion for shorts

• Breadth Gate: average robust Z of SPY QQQ IWM to avoid fading when the tape is one-sided

• Gap Shock: skip signals after large session gaps

Fusion rule

• All required gates must be true: Energy ≥ energy_trig_prc, |Robust Z| ≥ z_trig, Shape satisfied, Breadth confirmed, Gap filter clear

Signal rule

• Long: energy extreme, Z negative beyond threshold, close near bar low, breadth Z ≤ −breadth_z_ok

• Short: energy extreme, Z positive beyond threshold, close near bar high, breadth Z ≥ +breadth_z_ok

What you will see on the chart

• Standard strategy arrows for entries and exits

• Optional short-side brackets: ATR stop and ATR take profit if enabled

Inputs with guidance

Setup

• Base length: window for percentile ranks and medians. Typical 40 to 80. Longer smooths, shorter reacts.

• ATR length: normalization unit. Typical 10 to 20. Higher reduces noise.

• VWAP band stdev: volatility bands for anchors. Typical 2.0 to 4.0.

• Robust Z window: 40 to 100. Larger for stability.

• Robust Z entry magnitude: 1.2 to 2.2. Higher means stronger extremes only.

• Energy percentile trigger: 90 to 99.5. Higher limits signals to rare stretches.

• Bar close in range gate long: 0.05 to 0.25. Larger requires deeper capitulation for longs.

Regime and Breadth

• Use breadth gate: on when trading indices or broad ETFs.

• Breadth Z confirm magnitude: 0.8 to 1.8. Higher avoids fighting thrusts.

• Gap shock percent: 1.0 to 5.0. Larger allows more gaps to trade.

Risk — Short only

• Enable short SL TP: on to bracket shorts.

• Short ATR stop mult: 1.0 to 3.0.

• Short ATR take profit mult: 1.0 to 6.0.

Properties visible in this publication

• Initial capital: 25000USD

• Default order size: Percent of total equity 3%

• Pyramiding: 0

• Commission: 0.03 percent

• Slippage: 5 ticks

• Process orders on close: OFF

• Bar magnifier: OFF

• Recalculate after order is filled: OFF

• Calc on every tick: OFF

• request.security lookahead off where used

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Fills and slippage vary by venue

• Shapes can move during bar formation and settle on close

• Standard candles only for strategies

Honest limitations and failure modes

• Economic releases or very thin liquidity can overwhelm mean-reversion logic

• Heavy gap regimes may require larger gap filter or TR-based tuning

• Very quiet regimes reduce signal contrast; extend windows or raise thresholds

Open source reuse and credits

• None

Strategy notice

Orders are simulated by TradingView on standard candles. request.security uses lookahead off where applicable. Non-standard charts are not supported for execution.

Entries and exits

• Entry logic: as in Signal rule above

• Exit logic: short side optional ATR stop and ATR take profit via brackets; long side closes on opposite setup

• Risk model: ATR-based brackets on shorts when enabled

• Tie handling: stop first when both could be touched inside one bar

Dataset and sample size

• Test across your visible history. For robust inference prefer 100 plus trades.

FluxGate Daily Swing StrategySummary in one paragraph

FluxGate treats long and short as different ecosystems. It runs two independent engines so the long side can be bold when the tape rewards upside persistence while the short side can stay selective when downside is messy. The core reads three directional drivers from price geometry then removes overlap before gating with clean path checks. The complementary risk module anchors stop distance to a higher timeframe ATR so a unit means the same thing on SPY and BTC. It can add take profit breakeven and an ATR trail that only activates after the trade earns it. If a stop is hit the strategy can re enter in the same direction on the next bar with a daily retry cap that you control. Add it to a clean chart. Use defaults to see the intended behavior. For conservative workflows evaluate on bar close.

Scope and intent

• Markets. Large cap equities and liquid ETFs major FX pairs US index futures and liquid crypto pairs

• Timeframes. From one minute to daily

• Default demo in this publication. SPY on one day timeframe

• Purpose. Reduce false starts without missing sustained trends by fusing independent drivers and suppressing activity when the path is noisy

• Limits. This is a strategy. Orders are simulated on standard candles. Non standard chart types are not supported for execution

Originality and usefulness

• Unique fusion. FluxGate extracts three drivers that look at price from different angles. Direction measures slope of a smoothed guide and scales by realized volatility so a point of slope does not mean a different thing on different symbols. Persistence looks at short sign agreement to reward series of closes that keep direction. Curvature measures the second difference of a local fit to wake up during convex pushes. These three are then orthonormalized so a strong reading in one does not double count through another.

• Gates that matter. Efficiency ratio prefers direct paths over treadmills. Entropy turns up versus down frequency into an information read. Light fractal cohesion punishes wrinkly paths. Together they slow the system in chop and allow it to open up when the path is clean.

• Separate long and short engines. Threshold tilts adapt to the skew of score excursions. That lets long engage earlier when upside distribution supports it and keeps short cautious where downside surprise and venue frictions are common.

• Practical risk behavior. Stops are ATR anchored on a higher timeframe so the unit is portable. Take profit is expressed in R so two R means the same concept across symbols. Breakeven and trailing only activate after a chosen R so early noise does not squeeze a good entry. Re entry after stop lets the system try again without you babysitting the chart.

• Testability. Every major window and the aggression controls live in Inputs. There is no hidden magic number.

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close for stability and easy aggregation through time. Realized volatility is the standard deviation of returns over a moving window.

• Range basis for risk. ATR computed on a higher timeframe anchor such as day week or month. That anchor is steady across venues and avoids chasing chart specific quirks.

Components

• Directional intensity. Use an EMA of typical price as a guide. Take the day to day slope as raw direction. Divide by realized volatility to get a unit free measure. Soft clip to keep outliers from dominating.

• Persistence. Encode whether each bar closed up or down. Measure short sign agreement so a string of higher closes scores better than a jittery sequence. This favors push continuity without guessing tops or bottoms.

• Curvature. Fit a short linear regression and compute the second difference of the fitted series. Strong curvature flags acceleration that slope alone may miss.

• Efficiency gate. Compare net move to path length over a gate window. Values near one indicate direct paths. Values near zero indicate treadmill behavior.

• Entropy gate. Convert up versus down frequency into a probability of direction. High entropy means coin toss. The gate narrows there.

• Fractal cohesion. A light read of path wrinkliness relative to span. Lower cohesion reduces the urge to act.

• Phase assist. Map price inside a recent channel to a small signed bias that grows with confidence. This helps entries lean toward the right half of the channel without becoming a breakout rule.

• Shock control. Compare short volatility to long volatility. When short term volatility spikes the shock gate temporarily damps activity so the system waits for pressure to normalize.

Fusion rule

• Normalize the three drivers after removing overlap

• Blend with weights that adapt to your aggression input

• Multiply by the gates to respect path quality

• Smooth just enough to avoid jitter while keeping timing responsive

• Compute an adaptive mean and deviation of the score and set separate long and short thresholds with a small tilt informed by skew sign

• The result is one long score and one short score that can cross their thresholds at different times for the same tape which is a feature not a bug

Signal rule

• A long suggestion appears when the long score crosses above its long threshold while all gates are active

• A short suggestion appears when the short score crosses below its short threshold while all gates are active

• If any required gate is missing the state is wait

• When a position is open the status is in long or in short until the complementary risk engine exits or your entry mode closes and flips

Inputs with guidance

Setup Long

• Base length Long. Master window for the long engine. Typical range twenty four to eighty. Raising it improves selectivity and reduces trade count. Lowering it reacts faster but can increase noise

• Aggression Long. Zero to one. Higher values make thresholds more permissive and shorten smoothing

Setup Short

• Base length Short. Master window for the short engine. Typical range twenty eight to ninety six

• Aggression Short. Zero to one. Lower values keep shorts conservative which is often useful on upward drifting symbols

Entries and UI

• Entry mode. Both or Long only or Short only

Complementary risk engine

• Enable risk engine. Turns on bracket exits while keeping your signal logic untouched

• ATR anchor timeframe. Day Week or Month. This sets the structural unit of stop distance

• ATR length. Default fourteen

• Stop multiple. Default one point five times the anchor ATR

• Use take profit. On by default

• Take profit in R. Default two R

• Breakeven trigger in R. Default one R

Usage recipes

Intraday trend focus

• Entry mode Both

• ATR anchor Week

• Aggression Long zero point five Aggression Short zero point three

• Stop multiple one point five Take profit two R

• Expect fewer trades that stick to directional pushes and skip treadmill noise

Intraday mean reversion focus

• Session windows optional if you add them in your copy

• ATR anchor Day

• Lower aggression both sides

• Breakeven later and trailing later so the first bounce has room

• This favors fade entries that still convert into trends when the path stays clean

Swing continuation

• Signal timeframe four hours or one day

• Confirm timeframe one day if you choose to include bias

• ATR anchor Week or Month

• Larger base windows and a steady two R target

• This accepts fewer entries and aims for larger holds

Properties visible in this publication

• Initial capital 25.000

• Base currency USD

• Default order size percent of equity value three - 3% of the total capital

• Pyramiding zero

• Commission zero point zero three percent - 0.03% of total capital

• Slippage five ticks

• Process orders on close off

• Recalculate after order is filled off

• Calc on every tick off

• Bar magnifier off

• Any request security calls use lookahead off everywhere

Realism and responsible publication

• No performance promises. Past results never guarantee future outcomes

• Fills and slippage vary by venue and feed

• Strategies run on standard candles only

• Shapes can update while a bar is forming and settle on close

• Keep risk per trade sensible. Around one percent is typical for study. Above five to ten percent is rarely sustainable

Honest limitations and failure modes

• Sudden news and thin liquidity can break assumptions behind entropy and cohesion reads

• Gap heavy symbols often behave better with a True Range basis for risk than a simple range

• Very quiet regimes can reduce score contrast. Consider longer windows or higher thresholds when markets sleep

• Session windows follow the exchange time of the chart if you add them

• If stop and target can both be inside a single bar this strategy prefers stop first to keep accounting conservative

Open source reuse and credits

• No reused open source beyond public domain building blocks such as ATR EMA and linear regression concepts

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on history and in simulation with realistic costs

Supertrend Strategy With Multi Tp & TslHello Traders,

This strategy is based on the popular Supertrend indicator, which many traders use as a simple trend-following tool. The core entry logic is straightforward:

Buy (Long) when the price closes above the Supertrend line.

Sell (Short) when the price closes below the Supertrend line.

However, trading success isn’t only about entries — proper risk management makes all the difference. That’s why this strategy includes four stop-loss methods, two take-profit types, and a trailing stop-loss system. You can customize all of these settings to create your own personalized version.

🛑 Stop-Loss Methods

Tick – Uses the instrument’s smallest price increment. Ideal for tick-based markets such as Futures or Forex.

Percent – Defines the stop-loss as a percentage of entry price. Commonly used in Crypto trading.

ATR – Uses the Average True Range value to determine stop-loss distance. Perfect for adapting to changing market volatility.

Supertrend – The stop-loss level is set at the Supertrend line value at the time of entry.

🔁 Trailing Stop-Loss & Reverse Signals

Trailing SL: If enabled, the chosen stop-loss method will trail the price dynamically from the moment the position opens.

Close with Reverse Signals: When activated, the current position closes and reverses on an opposite signal. If disabled, the strategy waits until the current position is closed before opening a new one.

🎯 Take-Profit Options

Tick – Set a fixed take-profit level based on tick distance.

Percent – Set take-profit based on a percentage change from entry.

Ratio – Sets take-profit based on the entry-to-stop-loss distance × ratio value.

Each take-profit method allows you to define the percentage of position to close at that level.

⚖️ Breakeven Option

When Breakeven is enabled, after the first take-profit is triggered, the stop-loss automatically moves to the entry level, protecting your capital.

⚙️ Additional Settings

Position Type: Choose between Long only, Short only, or Both directions.

Session Filter: Trade only during specific time ranges. Activate this option and set your desired session hours (make sure to select your correct timezone).

📈 Visuals

The strategy plots entry, stop-loss, and take-profit levels directly on the chart, allowing you to clearly visualize your trades and manage them effectively.

Feel free to ask any questions or suggest improvements — this strategy is built for flexibility and experimentation!

Larry Williams Oops StrategyThis strategy is a modern take on Larry Williams’ classic Oops setup. It trades intraday while referencing daily bars to detect opening gaps and align entries with the prior day’s direction. Risk is managed with day-based stops, and—unlike the original—all positions are closed at the end of the session (or at the last bar’s close), not at a fixed profit target or the first profitable open.

Entry Rules

Long setup (bullish reversion): Today opens below yesterday’s low (down gap) and yesterday’s candle was bearish. Place a buy stop at yesterday’s low + Filter (ticks).

Short setup (bearish reversion): Today opens above yesterday’s high (up gap) and yesterday’s candle was bullish. Place a sell stop at yesterday’s high − Filter (ticks).

Longs are only taken on down-gap days; shorts only on up-gap days.

Protective Stop

If long, stop loss trails the current day’s low.

If short, stop loss trails the current day’s high.

Exit Logic

Positions are force-closed at the end of the session (in the last bar), ensuring no overnight exposure. There is no take-profit; only stop loss or end-of-day flat.

Notes

This strategy is designed for intraday charts (minutes/seconds) using daily data for gaps and prior-day direction.

Longs/shorts can be enabled or disabled independently.

Rebound Sigma Pro - StrategyOverview

Rebound Sigma Pro is a mean-reversion indicator that detects statistically oversold conditions in trending markets.

It helps traders identify potential short-term rebounds based on momentum exhaustion and volatility-adjusted entry zones.

Concept

The indicator combines two quantitative components:

Short-term momentum to detect short-term exhaustion

Trend filter to ensure setups align with the long-term direction

When a stock in an uptrend becomes temporarily oversold, a limit-entry signal is plotted.

The trade is then tracked until short-term conditions normalize or a time-based exit occurs.

Visual Signals

Green Triangle: Suggests placing a limit order for the next session

Green Circle: Confirms entry was filled

Red Triangle: Signals an exit for the next session’s open

Orange Background: Pending order

Green Background: Position active

Red Background: Exit phase

Yellow Line: Entry reference price

User Inputs

Limit Entry (% below previous close) – Default 1 %

Use Limit Entry – Switch between limit or market entries

Enable Time Exit – Optional holding-period constraint

Maximum Holding Days

All other internal parameters (momentum length, filters) are pre-configured.

Alerts

Limit Order Signal: New setup detected

Entry Confirmed: Order filled

Exit Signal: Exit expected next day

Usage

Designed for liquid equities and ETFs

Works best in confirmed uptrends

Backtesting encouraged to adapt parameters per symbol and timeframe

Notes

Not an automated strategy; manual order execution required

Past behavior does not imply future performance

Always apply sound position sizing and risk management

Disclaimer

This indicator is provided for educational and analytical purposes only.

It does not constitute financial advice or performance assurance.

AR Alerts Basic 🤖A non-repainting, ATR-based trailing stop strategy and session-based trading filters.

Features:

Dynamic buy/sell trailing stops using ATR for stable exits.

EMA exit for remaining positions to lock in profits.

Time session filters: trade only during defined market hours.

Trend detection using EMA50/EMA100 coloring.

Backtest dashboard Table showing total trades, win rate, P&L, growth, profit factor, and max drawdown. can be uncheck from Style Tab.

Fully non-repainting signals for reliable historical testing.

Perfect for traders who want stable signals, trailing stops, and a clean backtest summary in one indicator.

@infonatics

IB BreakoutIt marks the IB range (high, low, midpoint) from a chosen session window (default 9:30–10:30).

It plots the IB lines, midpoint (colored based on close), and extension levels (+/–25% and 50%).

After the IB session ends, it looks for breakouts:

Long if price closes above IB high.

Short if price closes below IB low.

Each trade targets the 25% extension in the breakout direction, with an optional stop at the opposite IB level.

It limits the number of trades per day and displays info (trades, position, IB range, next target) in a table.

Signalgo Strategy ISignalgo Strategy I: Technical Overview

Signalgo Strategy I is a systematically engineered TradingView strategy script designed to automate, test, and manage trend-following trades using multi-timeframe price/volume logic, volatility-based targets, and multi-layered exit management. This summary covers its operational structure, user inputs, entry and exit methodology, unique technical features, and practical application.

Core Logic and Workflow

Multi-Timeframe Data Synthesis

User-Defined Timeframe: The user chooses a timeframe (e.g., 1H, 4H, 1D, etc.), on which all strategy signals are based.

Cross-Timeframe Inputs: The strategy imports closing price, volume, and Average True Range (ATR) for the selected interval, independently from the chart’s native timeframe, enabling robust multi-timeframe analysis.

Price Change & Volume Ratio: It calculates the percent change of price per bar and computes a volume ratio by comparing current volume to its 20-bar moving average—enabling detection of true “event” moves vs. normal market noise.

Hype Filtering

Anti-Hype Mechanism: An entry is automatically filtered out if abnormal high volume occurs without corresponding price movement, commonly observed during manipulation or announcement periods. This helps isolate genuine market-driven momentum.

User Inputs

Select Timeframe: Choose which interval drives signal generation.

Backtest Start Date: Specify from which date historical signals are included in the strategy (for precise backtests).

Take-Profit/Stop-Loss Configuration: Internally, risk levels are set as multiples of ATR and allow for three discrete profit targets.

Entry Logic

Trade Signal Criteria:

Price change magnitude in the current bar must exceed a fixed sensitivity threshold.

Volume for the bar must be significantly elevated compared to average, indicating meaningful participation.

Anti-hype check must not be triggered.

Bullish/Bearish Determination: If all conditions are met and price change direction is positive, a long signal triggers. If negative, a short signal triggers.

Signal Debouncing: Ensures a signal triggers only when a new condition emerges, avoiding duplicate entries on flat or choppy bars.

State Management: The script tracks whether an active long or short is open to avoid overlapping entries and to facilitate clean reversals.

Exit Strategy

Take-Profits: Three distinct profit targets (TP1, TP2, TP3) are calculated as fixed multiples of the ATR-based stop loss, adapting dynamically to volatility.

Reversals: If a buy signal appears while a short is open (or vice versa), the existing trade is closed and reversed in a single step.

Time-Based Exit: If, 49 bars after entry, the trade is in-profit but hasn’t reached TP1, it exits to avoid stagnation risk.

Adverse Move Exit: The position is force-closed if it suffers a 10% reversal from entry, acting as a catastrophic stop.

Visual Feedback: Each TP/SL/exit is plotted as a clear, color-coded line on the chart; no hidden logic is used.

Alerts: Built-in TradingView alert conditions allow automated notification for both entries and strategic exits.

Distinguishing Features vs. Traditional MA Strategies

Event-Based, Not Just Slope-Based: While classic moving average strategies enter trades on MA crossovers or slope changes, Signalgo Strategy I demands high-magnitude price and volume confirmation on the chosen timeframe.

Volume Filtering: Very few MA strategies independently filter for meaningful volume spikes.

Real Market Event Focus: The anti-hype filter differentiates organic market trends from manipulated “high-volume, no-move” sessions.

Three-Layer Exit Logic: Instead of a single trailing stop or fixed RR, this script manages three profit targets, time-based closures, and hard adverse thresholds.

Multi-Timeframe, Not Chart-Dependent: The “main” analytical interval can be set independently from the current chart, allowing for in-depth cross-timeframe backtests and system runs.

Reversal Handling: Automatic handling of signal reversals closes and flips positions precisely, reducing slippage and manual error.

Persistent State Tracking: Maintains variables tracking entry price, trade status, and target/stop levels independently of chart context.

Trading Application

Strategy Sandbox: Designed for robust backtesting, allowing users to simulate performance across historical data for any major asset or interval.

Active Risk Management: Trades are consistently managed for both fixed interval “stall” and significant loss, not just via trailing stops or fixed-day closes.

Alert Driven: Can power algorithmic trading bots or notify discretionary traders the moment a qualifying market event occurs.

VWAP Executor — v6 (VWAP fix)tarek helishPractical scalping plan with high-rate (sometimes reaching 70–85% in a quiet market)

Concept: “VWAP bounce with a clear trend.”

Tools: 1–3-minute chart for entry, 5-minute trend filter, VWAP, EMA(50) on 5M, ATR(14) on 1M, volume.

When to trade: London session or early New York session; avoid 10–15 minutes before/after high-impact news.

Entry rules (buy for example):

Trend: Price is above the EMA(50) on 5M and has an upward trend.

Entry zone: First bounce to VWAP (or a ±1 standard deviation channel around it).

Signal: Bullish rejection/engulfing candle on 1M with increasing volume, and RSI(2) has exited oversold territory (optional).

Order: Entry after the confirmation candle closes or a limit close to VWAP.

Trade Management:

Stop: Below the bounce low or 0.6xATR(1M) (strongest).

Target: 0.4–0.7xATR(1M) or the previous micro-high (small return to increase success rate).

Trigger: Move the stop to breakeven after +0.25R; close manually if the 1M candle closes strongly against you.

Filter: Do not trade if the spread widens, or the price "saws" around VWAP without a trend.

Sell against the rules in a downtrend.

Why this plan raises the heat-rate? You buy a "small discount" within an existing trend and near the institutional average price (VWAP), with a small target price.

مواقعي شركة الماسة للخدمات المنزلية

شركة تنظيف بالرياض

نقل عفش بالرياض

Market Open Impulse [LuciTech]Market Open Impulse Strategy

The Market Open Impulse Strategy is designed to capture significant price movements that occur at market open (2:30 PM UK time). This strategy identifies impulsive candles with high volatility and enters trades based on the direction and strength of the initial market reaction.

How It Works:

The strategy activates exclusively at 2:30 PM UK time during market open sessions. It uses ATR-based volatility filtering to identify impulsive candles that exceed a configurable multiplier (default 1.5x ATR). Long entries are triggered when an impulsive candle closes above its midpoint and above the opening price, while short entries occur when an impulsive candle closes below its midpoint and below the opening price.

Risk management is handled through precise stop loss placement at the opposite extreme of the impulse candle (high for short positions, low for long positions). Take profit levels are calculated using a configurable risk-reward ratio with a default setting of 3:1. Position sizing is automatically calculated based on the percentage risk per trade, and an optional breakeven feature can move the stop loss to the entry price at specified profit levels.

The strategy incorporates time-based filtering to ensure trades only occur during the specified market open window. Visual indicators highlight qualifying impulsive candles and plot all entry and exit levels for clear trade management. The system offers flexible risk management with customizable risk percentage, risk-reward ratios, and breakeven settings, along with multiple stop loss calculation methods including both ATR-based and candle-based options.

Key Parameters:

Market open timing is fully configurable through hour and minute settings for strategy activation. The impulse ATR multiple sets the minimum volatility threshold required for trade qualification, with visual highlighting available for qualifying setups. Risk management parameters include the percentage of account equity to risk per trade, target profit multiples relative to initial risk, and the profit level threshold for breakeven stop loss adjustment. Users can choose between ATR-based or candle-based stop loss calculation methods and adjust technical parameters for volatility calculation including ATR length and smoothing methods.

Applications:

This strategy is particularly effective for trading market open volatility and momentum, capturing institutional order flow during key timing windows, executing short-term swing trades on significant price impulses, and trading markets with predictable opening patterns and consistent volatility characteristics.

Combo 2/20 EMA & Bandpass Filter by TamarokDescription:

This strategy combines a 2/20 exponential moving average (EMA) crossover with a custom bandpass filter to generate buy and sell signals.

Use the Fast EMA and Slow EMA inputs to adjust trend sensitivity, and the Bandpass Filter Length, Delta, and Zones to fine-tune momentum turns.

Signals occur when both EMA and BPF agree in direction, with optional reversal and time filters.

How to use:

1. Add the script to your chart in TradingView.

2. Adjust the EMA and BP Filter parameters to match your asset’s volatility.

3. Enable ‘Reverse Signals’ to trade counter-trend, or use the time filter to limit sessions.

4. Set alerts on Long Alert and Short Alert for automated notifications.

Inspiration:

Based on HPotter’s original combo strategy (Stocks & Commodities Mar 2010).

Updated to Pine Script v6 with streamlined code and alerts.

WARNING:

For purpose educate only

Breakouts With DXY Filter Strategy [LuciTech]This advanced breakout strategy combines pivot-based breakout detection with an innovative DXY (US Dollar Index) inverse correlation filter to enhance trade selection quality. The strategy identifies breakouts from recent pivot highs and lows while using DXY movements as a confirmation filter, based on the principle that USD strength/weakness often inversely correlates with other asset movements.

Key Features

Core Breakout Logic

- Pivot-Based Detection: Identifies breakouts above recent pivot highs (bullish) and below recent pivot lows (bearish)

- Customizable Lookback: Adjustable pivot length for different market conditions

- Visual Breakout Lines: Optional display of breakout levels with customizable colors

DXY Inverse Correlation Filter

- Smart USD Filter: Uses DXY movements to confirm breakout signals

- Inverse Logic: Long signals require DXY bearishness, short signals require DXY bullishness

- Threshold Control: Minimum DXY movement percentage required for signal confirmation

- Real-time DXY Data: Pulls live DXY data for accurate correlation analysis

Moving Average Filter

- Multiple MA Types: Support for SMA, EMA, WMA, VWMA, and HMA

- Trend Confirmation: Only takes trades in the direction of the selected moving average

- Customizable Parameters: Adjustable length and source for the moving average

Advanced Risk Management

- Multiple Stop Loss Types:

- ATR-based stops with customizable multiplier

- Candle-based stops using previous candle levels

- Fixed point-based stops

- Risk-Reward Optimization: Configurable risk-reward ratios (1:1 to 1:10)

- Breakeven Function: Automatic stop loss adjustment to breakeven after specified R-multiple

- Position Sizing: Percentage-based risk management with automatic position calculation

Time-Based Trading

- Session Filter: Trade only during specified time windows

- London Time Zone: Uses Europe/London timezone for consistency

- Visual Session Highlighting: Optional background fill for active trading hours

Alert System

- Webhook Integration: JSON-formatted alerts for automated trading

- Telegram Support: Pre-formatted messages for Telegram bot integration

- Multiple Formats: Standard, Telegram, and Concise Telegram alert options

- Real-time Notifications: Instant alerts on breakout signals

How It Works

1. Breakout Detection: The script continuously monitors for closes above recent pivot highs or below recent pivot lows

2. DXY Confirmation: When a breakout occurs, the script checks if DXY is moving in the opposite direction with sufficient momentum

3. MA Filter: If enabled, ensures the breakout aligns with the overall trend direction

4. Time Filter: Validates that the signal occurs within the specified trading hours

5. Risk Calculation: Automatically calculates position size based on the defined risk percentage and stop loss distance

6. Trade Execution: Places trades with predetermined stop loss and take profit levels

Unique Advantages

- Multi-Timeframe Approach: Combines asset-specific breakouts with broader USD market sentiment

- False Breakout Reduction: DXY filter helps eliminate breakouts that lack fundamental backing

- Comprehensive Risk Management: Multiple stop loss methods and automatic position sizing

- High Customization: Extensive parameters for different trading styles and market conditions

- Professional Alert System: Ready for automated trading integration

WaverVanir Alpha Reversal Scalper [ETF Eval Bot]🧠 Strategy Overview:

The WaverVanir Alpha Reversal Scalper is a precision-engineered futures trading bot designed to pass prop firm evaluations, specifically Elite Trader Funding (ETF) via Tradovate integration.

This scalping engine was developed after analyzing over 100+ evaluation trades, and is powered by institutional logic, volume behavior, and adaptive VWAP-based confluence.

🔍 Core Logic:

Directional Bias: Trades long only based on VWAP slope confirmation (to avoid funding-damaging shorts)

Entry Conditions:

Price deviates below VWAP standard deviation

Volume spike exceeds 1.5× 20-period average

Bullish reversal wick detected (smart money pattern)

Exit Management:

Stop Loss: 10-tick precision SL below local low

Take Profit: 2.5R static or dynamic trailing stop

Session Filter: Trades only between 9:00–14:00 ET, avoiding lunch and close traps

📊 Backtest Summary (ESU2025)

Metric Result

Net Profit $9,487.50

Profit Factor 1.66 (longs)

Sharpe Ratio 0.03

Sortino Ratio 0.042

Winning Bias Long-Only

Max Drawdown Under $3,000

Commissions $0 (sim tested)

🧪 Tested across March–July 2025 on CME Mini ES (ESU2025)

🔒 Short trades disabled after review: Net −$7,312.50 loss on shorts alone

✅ Profit factor improves > 60% post-optimization

🔄 Recent Optimizations

❌ Disabled unprofitable short setups

✅ VWAP slope filter added for institutional alignment

✅ Trailing stop logic added (activates after 1.5R)

⏱️ Session filter to reduce market noise

🧠 Designed For:

Passing ETF funding challenges quickly

Avoiding drawdown breaches with controlled risk

Running on TradingView with direct Tradovate integration

🚀 Execution-Ready

This bot runs natively on TradingView. Simply:

Add the Pine Script to your chart

Use a tradable symbol (e.g., ESU2025)

Create an alert using “Order fills”

✅ Enable auto-trading to Tradovate

📡 Learn More

🔗 Powered by VolanX Protocol, the AI-driven infrastructure layer of

🌐 WaverVanir International LLC – where institutional logic meets retail precision.

—

🧠 Want to upgrade this bot to include macros, adaptive entries, or launch in NQ/CL?

💬 Drop a comment or message — let’s build your funding empire.

#ES #Futures #ETF #Funding #PropFirm #TradingBot #VWAP #VolumeProfile #AlphaScalper #WaverVanir #VolanX

US Index First Candle Breakout with FVGStrategy Description: US Index First Candle Breakout with FVG

Works on NG1! and YM1! for maximised profit.

Overview:

The "US Index First Candle Breakout with FVG" strategy is designed to capitalize on the volatility present during the first minutes of the U.S. stock market opening. By focusing on the initial 5-minute candle, this strategy identifies key price levels that can serve as breakout points for potential trading opportunities.

Key Features:

1. Breakout Strategy:

The strategy tracks the high and low of the first 5-minute candle after the market opens at 9:30 AM (New York time). These levels are critical indicators for potential price movements.

A long position is triggered when the price breaks above the high of the first candle, while a short position is initiated when the price drops below the low.

2. Manual Trade Direction Filter: (developing)

Users can select their preferred trading direction through a customizable input:

Buy only: Execute long trades only.

Sell only: Execute short trades only.

Both: Allow trades in both directions.

This feature enables traders to align the strategy with their market outlook and risk tolerance.

3. Fair Value Gap (FVG) Analysis:

The strategy incorporates an FVG filter to enhance trade precision. It assesses market gaps to identify whether a breakout is supported by underlying market dynamics.

The algorithm checks for conditions that indicate a valid breakout based on previous price action, ensuring that trades are made on strong signals.

4. Risk Management:

A customizable risk per trade setting allows users to define their risk tolerance in ticks.

The strategy includes a reward-to-risk ratio input, enabling traders to set their take-profit levels based on their risk preferences.

Stop-loss levels are automatically calculated based on the breakout direction, helping to safeguard against unexpected price movements.

5. Automatic Trade Execution:

Trades are executed automatically based on the defined conditions, reducing the need for manual intervention and allowing traders to capitalize on market movements in real-time.

Session End Closure:

The strategy automatically closes all open positions at 4:00 PM (New York time), ensuring that trades do not carry overnight risk.

How to Use the Strategy:

Simply add the script to your TradingView chart, set your desired parameters, and select your preferred trade direction.

Monitor for breakout signals during the first trading session, and let the automated system handle trade entries and exits based on your specifications.

Conclusion:

The "US Index First Candle Breakout with FVG" strategy is ideal for traders seeking to leverage early market volatility with a structured approach. By combining breakout techniques with FVG analysis and customizable trade direction, this strategy offers a robust framework for navigating the complexities of the U.S. stock market's opening dynamics.

LANZ Strategy 6.0 [Backtest]🔷 LANZ Strategy 6.0 — Precision Backtesting Based on 09:00 NY Candle, Dynamic SL/TP, and Lot Size per Trade

LANZ Strategy 6.0 is the simulation version of the original LANZ 6.0 indicator. It executes a single LIMIT BUY order per day based on the 09:00 a.m. New York candle, using dynamic Stop Loss and Take Profit levels derived from the candle range. Position sizing is calculated automatically using capital, risk percentage, and pip value — allowing accurate trade simulation and performance tracking.

📌 This is a strategy script — It simulates real trades using strategy.entry() and strategy.exit() with full money management for risk-based backtesting.

🧠 Core Logic & Trade Conditions

🔹 BUY Signal Trigger:

At 09:00 a.m. NY (New York time), if:

The current candle is bullish (close > open)

→ A BUY order is placed at the candle’s close price (EP)

Only one signal is evaluated per day.

⚙️ Stop Loss / Take Profit Logic

SL can be:

Wick low (0%)

Or dynamically calculated using a % of the full candle range

TP is calculated using the user-defined Risk/Reward ratio (e.g., 1:4)

The TP and SL levels are passed to strategy.exit() for each trade simulation.

💰 Risk Management & Lot Size Calculation

Before placing the trade:

The system calculates pip distance from EP to SL

Computes the lot size based on:

Account capital

Risk % per trade

Pip value (auto or manual)

This ensures every trade uses consistent, scalable risk regardless of instrument.

🕒 Manual Close at 3:00 p.m. NY

If the trade is still open by 15:00 NY time, it will be closed using strategy.close().

The final result is the actual % gain/loss based on how far price moved relative to SL.

📊 Backtest Accuracy

One trade per day

LIMIT order at the candle close

SL and TP pre-defined at execution

No repainting

Session-restricted (only runs on 1H timeframe)

✅ Ideal For:

Traders who want to backtest a clean and simple daily entry system

Strategy developers seeking reproducible, high-conviction trades

Users who prefer non-repainting, session-based simulations

👨💻 Credits:

💡 Developed by: LANZ

🧠 Logic & Money Management Engine: LANZ

📈 Designed for: 1H charts

🧪 Purpose: Accurate simulation of LANZ 6.0's NY Candle Entry system

Warrior Trading Momentum Strategy

# 🚀 Warrior Trading Momentum Strategy - Day Trading Excellence

## Strategy Overview

This comprehensive Pine Script strategy replicates the proven methodologies taught by Ross Cameron and the Warrior Trading community. Designed for active day traders, it identifies high-probability momentum setups with strict risk management protocols.

## 📈 Core Trading Setups

### 1. Gap and Go Trading

- **Primary Focus**: Stocks gapping up 2%+ with volume confirmation

- **Entry Logic**: Breakout above gap open with momentum validation

- **Volume Filter**: 2x average volume requirement for quality setups

### 2. ABCD Pattern Recognition

- **Pattern Detection**: Automated identification of classic ABCD reversal patterns

- **Validation**: A-B and C-D move relationship analysis

- **Entry Trigger**: D-point breakout with volume confirmation

### 3. VWAP Momentum Plays

- **Strategy**: Entries near VWAP with bounce confirmation

- **Distance Filter**: Configurable percentage distance for optimal entries

- **Direction Bias**: Above VWAP bullish momentum validation

### 4. Red to Green Reversals

- **Setup**: Reversal patterns after consecutive red candles

- **Confirmation**: Volume spike with bullish close required

- **Momentum**: Trend change validation with RSI support

### 5. Breakout Momentum

- **Logic**: Breakouts above recent highs with volume

- **Filters**: EMA20 and RSI confirmation for quality

- **Trend**: Established momentum direction validation

## ⚡ Key Features

### Smart Risk Management

- **Position Sizing**: Automatic calculation based on account risk percentage

- **Stop Loss**: 2 ATR-based stops for volatility adjustment

- **Take Profit**: Configurable risk-reward ratios (default 1:2)

- **Trailing Stops**: Profit protection with adjustable triggers

### Advanced Filtering System

- **Time Filters**: Market hours trading with lunch hour avoidance

- **Volume Confirmation**: Multi-timeframe volume analysis

- **Momentum Indicators**: RSI and moving average trend validation

- **Quality Control**: Multiple confirmation layers for signal accuracy

### PDT-Friendly Design

- **Trade Limiting**: Built-in daily trade counter for accounts under $25K

- **Selective Trading**: Priority scoring system for A+ setups only