TwinPulse Q Lead SPY x QQQ Intermarket Pulse 1HTwinPulse Q Lead is a concise one hour indicator for SPY and QQQ that converts three sources of market information into a single pulse line, a mode readout with BUY SELL WAIT, and compact alerts. It blends intermarket leadership between QQQ and SPY, intraday flow from the slope of session VWAP, and where the current price sits inside the regular trading hours range. The three components are normalized, fused, compressed to a stable range, and smoothed for clear thresholds. The aim is a readable intraday regime signal that helps you decide when to participate and when to stand aside.

The script is built with Pine v6, uses request security with lookahead off, and does not repaint. It is an indicator, not a strategy. It does not contain any solicitation, links, or outside references. The description is self contained and explains both logic and use so that any trader can understand the design without reading code.

What makes this original and useful

Intermarket leadership is measured directly from QQQ and SPY on your working timeframe using a Z score of the return spread. When growth is leading value heavy large caps, leadership turns positive. When it lags, leadership turns negative. This gives a real time read of the Nasdaq versus S and P tug of war that most day traders watch informally.

Intraday flow is taken from the slope of the session VWAP. A linear regression of VWAP over a short window captures whether value is rising or falling inside the day. Dividing by ATR normalizes slope by typical movement so that the signal is comparable across weeks.

Session position places price inside the current regular hours high to low. It answers whether the day is trading in the top half, the bottom half, or the middle. This is a simple but powerful context filter for breakouts and fades.

The three components are fused into one pulse, compressed with either hyperbolic tangent or softsign to keep values bounded, and then smoothed by a short EMA. This yields a stable range with a zero line so the eye can read shifts quickly.

The panel shows a human readable mode with reasons and a strength score. Traders who do not want to read lines can rely on a simple state and a compact justification that explains why the state is set.

This is not a mashup that simply overlays unrelated indicators. Each component was chosen to answer a distinct question that is common to SPY and QQQ intraday decision making. Leadership answers who is in charge, flow answers whether value inside the session is building or leaking, and position answers if price is pressing the extremes or circling the middle. The pulse ties the three together and prevents any single component from dominating.

How the calculations work

Leadership. Compute a short rate of change for SPY and QQQ. Subtract SPY from QQQ to get spread returns, then compute a rolling Z score over a longer window. Positive values mean QQQ is leading. Negative values mean SPY is leading.

Flow. Compute session VWAP on the active symbol. Regress VWAP over a short window to obtain a slope estimate. Divide by ATR to scale slope by current volatility so that a small rise on a quiet day is not treated the same as a small rise on a wild day.

Position. Track the highest high and lowest low since the start of regular hours. Place the current close inside that range on a zero to one scale, then recenter to a minus one to plus one scale. Positive means the top half of the day, negative means the bottom half.

Fusion. Multiply each component by a weight so users can emphasize or de emphasize leadership, flow, or position. Sum to a raw pulse.

Compression. Pass the raw pulse through a bounded function. Hyperbolic tangent is smooth and has natural saturation near the extremes. Softsign is faster and behaves like a smoother version of sign near zero. Compression avoids unbounded excursions and makes thresholds meaningful across days.

Smoothing. Apply a short EMA to the compressed pulse to reduce noise. This creates the main line called TwinPulse in the plot.

Thresholds. You can use static symmetric levels or adaptive levels. The adaptive option computes a mean and a standard deviation of the smoothed pulse over a user window, then sets upper and lower thresholds as mean plus or minus sigma times standard deviation. This allows thresholds to adjust across regimes. Static levels are still available for traders who want repeatable levels.

Events and mode. A long event fires when the smoothed pulse crosses the upper threshold with positive flow and any optional filters agree. A short event fires on the symmetric condition. The mode reads the current state rather than fire and forget. It returns BUY when the smoothed pulse is above the upper threshold with positive flow, SELL when the smoothed pulse is below the lower threshold with negative flow, otherwise WAIT. A cooldown controls how often events can fire so alerts do not spam during choppy periods.

Inputs and default values

The script ships with defaults chosen for SPY and QQQ on one hour charts.

Symbols. SPY and QQQ by default. You can switch to any pair. Many users may test IWM versus SPY for small cap reads.

Regular hours selector. On by default. This restricts the position factor to New York regular hours. Turn it off if you prefer full session behavior.

ROC length is three bars. Z score length is fifty bars. VWAP slope window is ten bars. ATR length is fourteen bars. Pulse smoothing length is three bars.

Compression mode. Choose hyperbolic tangent or softsign. Hyperbolic tangent is default.

Weights. Leadership and flow are one by default. Position is set to zero point seven to give a modest influence to where price sits inside the day.

Thresholds. Adaptive thresholds are on by default with a lookback of one hundred bars and a sigma width of zero point eight. Static levels at plus or minus zero point six are ready if you disable adaptive mode.

Filters. ADX filter is off by default. If you enable it, the script requires ADX above a user minimum before it will signal. Higher time frame confirmation is off by default. When enabled it compares the smoothed pulse on the confirm timeframe to zero and requires alignment for longs or shorts.

Cooldown. Three bars by default so that alerts do not trigger too frequently.

UI. Bar coloring is on by default. The panel is on by default and sits at the top right.

All request security calls use lookahead off and will not request future data. All persistent state variables are assigned in a way that prevents repainting. The indicator does not use non standard chart types in its logic.

How to use the indicator

Load a one hour chart of SPY or QQQ. Keep a clean chart so that the script output is easy to read.

Turn on regular hours if you want the session position to reflect the cash session. This is recommended for SPY and QQQ.

Watch the panel. Mode reads BUY or SELL or WAIT. The strength value is a simple vote based score that ranges from zero to one hundred. It counts leadership, flow, ADX if enabled, and higher time frame confirmation if enabled. You can use strength to filter weak states.

Consider action only when mode is BUY or SELL and the signal has not just fired on the last bar. The triangles mark where an event fired. Alerts use the same logic as the events. WAIT means stand aside.

To slow the system, enable ADX and set a higher minimum or enable higher time frame confirmation. To speed it up, disable the filters, disable adaptive thresholds, or tighten the sigma width.

When publishing, use a clean chart with only this indicator. Show the symbol and timeframe clearly and make sure the plot legend is visible. If you add drawings on the chart, only include ones that help readers understand the output.

Publication notes and compliance

This description is written in English. The title uses ASCII and only uses capital letters for common abbreviations. The script is original and explains how and why the components work together. There are no links or promotional material. The script does not claim performance. It does not use lookahead. The panel and alerts exist to help a human read and act with discipline. The indicator can be published as open source or as protected. If you choose protected, the description still allows readers to understand how the logic works without access to the code.

If you later convert the logic into a strategy for publication, use realistic commission and slippage, risk no more than a small share of equity per trade, and choose a dataset that yields a large enough sample. Explain any deviations from these default recommendations in your strategy description. Do not publish results from non standard chart types since they can mislead readers on signal timing.

Limitations and risks

Intermarket leadership is a relative measure. There are hours when both SPY and QQQ fall while leadership remains positive. Treat leadership as a context, not a stand alone trigger.

VWAP slope is a path measure inside the session. It can flip several times on a choppy day. That is why the script uses a short smoothing and an optional cooldown. Use ADX or higher time frame confirmation to avoid the worst chop.

Session position assumes a meaningful regular hours range. On half days or around openings with gaps the position factor can be less informative. If this bothers you, reduce the weight of position or turn it off.

Compression and smoothing introduce lag by design. The goal is stability and clarity. If you want earlier but noisier signals, reduce smoothing and weights, and use static thresholds.

No indicator guarantees future results. TwinPulse Q Lead is a decision aid. It should be combined with your risk rules, position size policy, and a clear exit plan. Past behavior is not a promise for the future.

Frequently asked questions

What symbols are supported. Any symbol can be used as the chart symbol. Leadership uses the two user symbols which default to SPY and QQQ. Many traders may try IWM versus SPY or DIA versus SPY.

Can I change the timeframe. Yes, but the design target is one hour. On very short timeframes the VWAP slope becomes very sensitive and you should consider stronger filters.

Does the script repaint. No. It uses request security with lookahead off and the panel updates on the last bar only. Events are based on bar close conditions unless you attach alerts on any alert function call which will still respect the logic without looking into the future.

How are the strength numbers built. The strength score is the share of aligned votes across leadership, flow, ADX if enabled, and higher time frame confirmation if enabled. A value near one hundred means many filters agree. A value near fifty means partial alignment. It is not a probability or an accuracy number.

Can I use non standard chart types. You can view the indicator on them but do not publish signals from non standard chart types because that can mislead readers about timing. Use classic candles or bars when you publish and when you test.

Why do I sometimes see BUY but the price is not moving. A BUY mode requires pulse above the upper threshold and positive flow. It does not require higher highs immediately. Treat BUY as a permission to look for entries using your own execution rules.

Cari skrip untuk "gaps"

Session-Conditioned Regime ATRWhy this exists

Classic ATR is great—until the open. The first few bars often inherit overnight gaps and 24-hour noise that have nothing to do with the intraday regime you actually trade. That inflates early ATR, scrambles thresholds, and invites hyper-recency bias (“today is crazy!”) when it’s just the open being the open.

This tool was built to:

Separate session reality from 24h noise. Measure volatility only inside your defined session (e.g., NYSE 09:30–16:00 ET).

Judge candles against the current regime, not the last 2–3 bars. A rolling statistic from the last N completed sessions defines what “typical” means right now.

Label “large” and “small” objectively. Bars are colored only when True Range meaningfully departs from the session regime—no gut feel, no open-bar distortion (gap inclusion optional).

Overview

Purpose: objectively identify unusually big or small candles within the active trading session, compared to the recent session regime.

Use cases: volatility filters, entry/exit confirmation, session bias detection, adaptive sizing.

This indicator replaces generic ATR with a session-conditioned, regime-aware measure. It colors candles only when their True Range (TR) is abnormally large/small versus the last N completed sessions of the same session window.

How it works

Session gating: Only bars inside the selected session are evaluated (presets for NYSE, CME RTH, FX NY; custom supported).

Per-bar TR: TR = max(high, prevRef) − min(low, prevRef).

prevRef is the prior close for in-session bars.

First bar of the session can include the overnight gap (optional; default off).

Regime statistic: For any bar in session k, aggregate all in-session TRs from the previous N completed sessions (k−N … k−1), then compute Median (default) or Mean.

Today’s anchor: Running statistic from today’s session start → current bar (for context and the on-chart ratio).

Color logic:

Big if TR ≥ bigMult × RegimeStat

Small if TR ≤ smallMult × RegimeStat

Colored states: big bull, big bear, small bull, small bear.

Non-triggering bars retain the chart’s native colors.

Panel (top-right by default)

Regime ATR (Nd): session-conditioned statistic over the past N completed sessions.

Today ATR (anchored): running statistic for the current session.

Ratio (Today/Regime): intraday volatility vs regime.

Sample size n: number of bars used in the regime calculation.

Inputs

Session Preset: NYSE (09:30–16:00 ET), CME RTH (08:30–15:00 CT), FX NY (08:00–17:00 ET), Custom (session + IANA timezone).

Regime Window: number of completed sessions (default 5).

Statistic: Median (robust) or Mean.

Include Open Gap: include overnight gap in the first in-session bar’s TR (default off).

Big/Small thresholds: multipliers relative to RegimeStat (defaults: Big=1.5×, Small=0.67×).

Colors: four independent colors for big/small × bull/bear.

Panel position & text size.

Hidden outputs: expose RegimeStat, TodayStat, Ratio, and Z-score to other scripts.

Alerts

RegimeATR: BIG bar — triggers when a bar meets the “Big” condition.

RegimeATR: SMALL bar — triggers when a bar meets the “Small” condition.

Hidden outputs (for strategies/screeners)

RegimeATR_stat, TodayATR_stat, Today_vs_Regime_Ratio, BarTR_Zscore.

Notes & limitations

No look-ahead: calculations only use information available up to that bar. Historical colors reflect what would have been known then.

Warm-up: colors begin once there are at least N completed sessions; before that, regime is undefined by design.

Changing inputs (session window, multipliers, median/mean, gap toggle) recomputes the full series using the same rolling regime logic per bar.

Designed for standard candles. Styling respects existing chart colors when no condition triggers.

Practical tips

For a broader or tighter notion of “unusual,” adjust Big/Small multipliers.

Prefer Median in markets prone to outliers; use Mean if you want Z-score alignment with the panel’s regime mean/std.

Use the Ratio readout to spot compression/expansion days quickly (e.g., <0.7× = compressed session, >1.3× = expanded).

Roadmap

More session presets:

24h continuous (crypto, index CFDs).

23h/Globex futures (CME ETH with a 60-minute maintenance break).

Regional equities (LSE, Xetra, TSE), Asia/Europe/NY overlaps for FX.

Half-day/holiday templates and dynamic calendars.

Multi-regime comparison: track multiple overlapping regimes (e.g., RTH vs ETH for futures) and show separate stats/ratios.

Robust stats options: trimmed mean, MAD/Huber alternatives; optional percentile thresholds instead of fixed multipliers.

Subpanel visuals: rolling TodayATR and Ratio plots; optional Z-score ribbon.

Screener/strategy hooks: export boolean series for BIG/SMALL, plus a lightweight strategy template for backtesting entries/exits conditioned on regime volatility.

Performance/QOL: per-symbol presets, smarter warm-up, and finer control over sample caps for ultra-low TF charts.

Changelog

v0.9b (Beta)

Session presets (NYSE/CME RTH/FX NY/Custom) with timezone handling.

Panel enhancements: ratio + sample size n.

Four-state bar coloring (big/small × bull/bear).

Alerts for BIG/SMALL bars.

Hidden Z-score stream for downstream use.

Gap-in-TR toggle for the first in-session bar.

Disclaimer

For educational purposes only. Not investment advice. Validate thresholds and session settings across symbols/timeframes before live use.

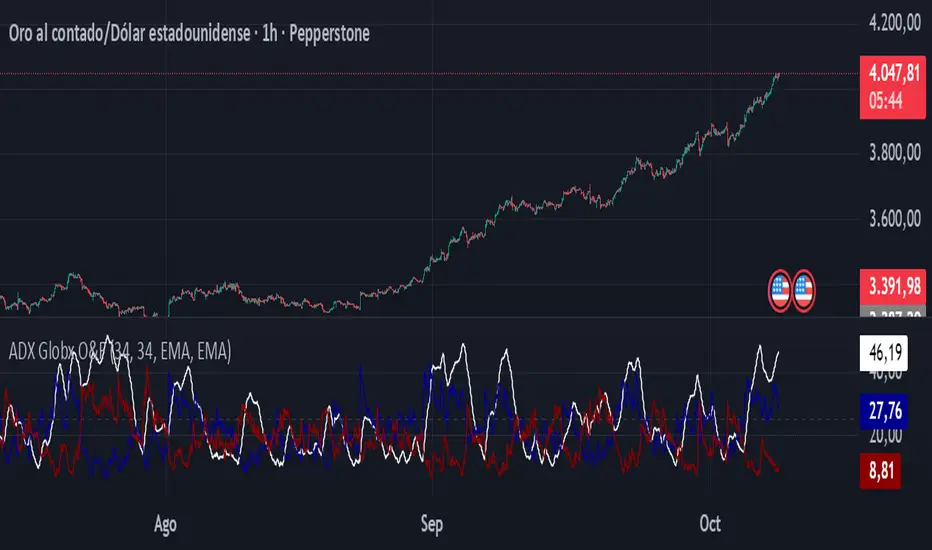

ADX - Globx Options & Futures 2.0The ADX Globx Options & Futures is a custom-built trend strength indicator designed to replicate and enhance the classic Average Directional Index (ADX) model, commonly used in professional trading platforms such as IQ Option.

This version is optimized for options and futures trading, providing precise directional strength readings through adaptive smoothing and configurable parameters.

Concept and Logic

This indicator measures the strength of the current trend, regardless of its direction (bullish or bearish), by comparing directional movement between price highs and lows over a defined period.

It uses three main components:

+DI (Positive Directional Indicator): represents bullish strength.

–DI (Negative Directional Indicator): represents bearish strength.

ADX (Average Directional Index): measures the intensity of the prevailing trend, independent of direction.

The script follows the original logic proposed by J. Welles Wilder Jr., but introduces enhanced smoothing flexibility.

Users can choose between EMA (Exponential Moving Average) and Wilder’s RMA (Running Moving Average) for both DI and ADX calculations, allowing closer alignment with various platform implementations (IQ Option, MetaTrader, etc.).

How It Works

Directional Movement Calculation

The script computes upward and downward movements (+DM and –DM) by comparing the differences in highs and lows between consecutive candles.

Only positive directional changes that exceed the opposite side are considered.

This ensures each bar contributes only one valid directional movement.

True Range and Smoothing

The True Range (TR) is calculated using ta.tr(true) to include price gaps—replicating how professional derivatives platforms account for volatility jumps.

Both TR and DM values are smoothed using the selected averaging method (EMA or Wilder).

Directional Index and ADX

The smoothed +DI and –DI values are normalized over the True Range to form the Directional Index (DX), which measures the percentage difference between the two.

The ADX is then derived by smoothing the DX values, providing a stable reading of overall market strength.

Visual Representation

The ADX (white line) indicates the overall trend strength.

The +DI (dark blue) and –DI (dark red) lines show which side (bullish or bearish) is currently dominant.

Reference levels at 20 and 25 serve as strength thresholds:

Below 20 → Weak or sideways market.

Above 25 → Strong and directional trend.

Usage and Interpretation

When ADX rises above 25, the market shows a strong trend — use +DI > –DI for bullish confirmation, or the opposite for bearish momentum.

A falling ADX suggests decreasing trend strength and potential consolidation.

The default parameters (ADX Length = 34, DI Length = 34, both smoothed by EMA) match IQ Option’s internal ADX configuration, ensuring consistency between platforms.

Works on any timeframe or asset class, but is especially tuned for futures and options volatility dynamics.

Originality and Improvements

Unlike many open-source ADX indicators, this version:

Recreates IQ Option’s 34-length EMA-based ADX calculation with exact parameter alignment.

Provides selectable smoothing algorithms (EMA or Wilder) to switch between modern and classic formulations.

Uses dark-theme-optimized visuals with fine line weight and subtle contrast for clean visibility.

Maintains constant guide levels (20/25) rendered globally for precision and style compliance in Pine Script v6.

Is fully rewritten for Pine Script v6, ensuring compatibility and optimized execution.

Recommended Use

Combine with trend-following systems or breakout strategies.

Ideal for identifying market strength before engaging in options directionals or futures entries.

Use the ADX to confirm breakout momentum or filter sideways markets.

Disclaimer

This script is for educational and analytical purposes. It does not constitute financial advice or a trading signal. Users are encouraged to validate the indicator within their own trading strategies and risk frameworks.

CVD Pro – Smart Overlay + Signals (with Persist Mode)What this Indicator Does

CVD Pro visualizes Cumulative Volume Delta (CVD) data directly on your main price chart — helping you detect real buying vs. selling pressure in real time.

Unlike most CVD scripts that run in a separate subwindow, this one overlays price-mapped CVD curves on the candles themselves for better confluence with market structure and FVG zones.

The script dynamically scales normalized CVD values to the price range and uses adaptive smoothing and deviation bands to highlight shifts in trader behavior.

It also includes automatic bullish/bearish crossover signals, displayed as on-chart labels.

⚙️ Main Features

✅ Price-mapped CVD Overlay

CVD is normalized (Z-score) and projected onto the price chart for easy visual correlation with price structure.

✅ Multi-Timeframe Presets

Three sensitivity presets optimized for different chart environments:

Strict (4H) → Best for macro trends and high-timeframe structure.

Balanced (1H / 30m) → Great for active swing setups.

Sensitive (15m) → Captures short-term intraday reversals.

✅ Dynamic Bands & Smoothing

Deviation bands visualize statistical extremes in delta pressure — helping to identify exhaustion and divergence points.

✅ Smart Buy/Sell Signal Logic

Automatic label triggers when the CVD Overlay crosses its smoothed baseline:

🟢 BULL LONG → Rising CVD above the mean (buyers in control).

🔴 BEAR SHORT → Falling CVD below the mean (sellers in control).

✅ Persist Mode

Toggle to keep the last signal visible until a new one forms — ideal for traders who prefer clean chart annotations without noise.

✅ Clean, Minimal Overlay

Everything happens directly on your chart — no extra windows, no clutter. Designed for use with Smart Money Concepts, Fair Value Gaps (FVGs), or volume imbalance setups.

🧩 Use Case

CVD Pro is designed for traders who:

Use Smart Money Concepts (SMC) or ICT-style trading

Watch for FVG reactions, breaker blocks, and liquidity sweeps

Need to confirm order flow direction or momentum strength

Trade intraday or swing setups with precision entries and clear bias confirmation

⚡ Recommended Settings

4H / 1H: Use Strict mode for major structure and confirmation.

1H / 30m: Balanced mode for clear mid-term trend alignment.

15m: Sensitive mode to catch scalps and lower-TF shifts.

🧠 Pro Tips

Combine with RSI or Market Structure Breaks (MSS) for additional confluence.

A strong CVD divergence near a key FVG or 0.5–0.705 Fibonacci zone often signals reversal.

Persistent CVD crossover + price structure break = high-probability entry.

🧩 Credits

Created by Patrick S. ("Nova Labs")

Concept inspired by professional order-flow analytics and adaptive Z-Score normalization.

Would you like me to write a shorter “public summary” paragraph (for the short description at the top of TradingView, the one-liner users see before expanding)?

It’s usually a 2–3 sentence hook like:

“Overlay-based CVD indicator that merges volume delta with price structure. Detect true buying/selling pressure using adaptive normalization, deviation bands, and clean bullish/bearish crossover signals.”

No Supply (Low-Volume Down Bars) — IdoThis indicator flags classic Wyckoff/VSA “No Supply (NS)” events—down bars that print on unusually low volume, suggesting a lack of sellers rather than strong selling pressure. NS often appears near support, LPS, or within re-accumulation ranges as a test before continuation higher.

Signal definition (configurable):

Down bar: choose Close < PrevClose or Close < Open.

Low volume: Volume < SMA(Volume, len) × threshold (e.g., 0.7).

Optional volume lower than the prior two bars (reduces noise).

Optional narrow spread: range (H–L) below its average.

Optional close position: close in the upper half of the bar.

Optional trend filter: only mark NS above or below an EMA (or any).

Optional wide-bar exclusion: skip unusually wide bars.

Visuals & outputs

Blue dot below each NS bar (optional bar tint).

Separate pane showing Relative Volume (vol / volSMA) to gauge effort.

Built-in alertcondition to trigger notifications when NS prints.

Inputs (high level)

lenVol: Volume SMA length.

ratioVol: Volume threshold vs. average (e.g., 0.7 = 70%).

usePrev2: Require volume below each of the prior two bars.

useNarrow + lenRange + ratioRange: Narrow-bar filter.

useClosePos + minClosePos: Close in upper portion of the bar.

downBarMode: Define “down bar” logic.

trendFiltOn, trendLen, trendSide: EMA trend filter.

useWideFilter, lenRangeWide, wideThreshold: Skip wide bars.

How to use (Wyckoff/VSA context)

Treat NS as a test of supply: price dips, but volume is light and close holds up.

Stronger when it prints near support/LPS within a re-accumulation structure.

Confirmation (recommended): within 1–3 bars, see demand—e.g., break above the NS high with expanding volume (above average or above the prior two bars). Many traders place a buy-stop just above the NS high; common stops are below the NS low or the most recent swing low.

Scanning tip

TradingView’s stock screener can’t consume Pine directly.

Use a Watchlist Custom Column that reports “bars since NS” to sort symbols (0 = NS on the latest bar). A companion column script is provided separately.

Notes & limitations

Works on any timeframe (intraday/daily/weekly), but context matters.

Expect false positives around news, gaps, or illiquid symbols—combine with structure (trend, S/R, phases) and risk management.

© moshel — Educational use only; not financial advice.

ORB 5 Minute w/FVG and Retracement Breakout strategy creates five minute breakout lines on the 1 minute chart. Highlights any fair value gaps created within ORB and creates an arrow showing when a candle retraces into the fvg.

3/4-Bar GRG / RGR Pattern (Conditional 4th Candle)This indicator can be used to identify the Green-Red-Green or Red-Green-Red pattern.

It is a price action indicator where a price action which identifies the defeat of buyers and sellers.

If the buyers comprehensively defeat the sellers then the price moves up and if the sellers defeat the buyers then the price moves down.

In my trading experience this is what defines the price movement.

It is a 3 or 4 candle pattern, beyond that i.e, 5 or more candles could mean a very sideways market and unnecessary signal generation.

How does it work?

Upside/Green signal

Say candle 1 is Green, which means buyers stepped in, then candle 2 is Red or a Doji, that means sellers brought the price down. Then if candle 3 is forming to be Green and breaks the closing of the 1st candle and opening of the 2nd candle, then a green arrow will appear and that is the place where you want to take your trade.

Here the buyers defeated the sellers.

Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

Important - We need to enter the trade as soon as the price moves above the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close. Ignore wicks.

I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

I call it the +-+ or GRG pattern.

Stop loss can be candle 2's mid for safe traders (that includes me) or candle 2's body low for risky traders.

Back testing suggests that body low will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Downside/Red signal

Say candle 1 is Red, which means sellers stepped in, then candle 2 is Green or a Doji, that means buyers took the price up. Then if candle 3 is forming to be Red and breaks the closing of the 1st candle and opening of the 2nd candle then a Red arrow will appear and that is the place where you want to take your trade.

Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

We need to enter the trade as soon as the price moves below the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close.

I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

I call it the -+- or RGR pattern.

Stop loss can be candle 2's mid for safe traders ( that includes me) or candle 2's body high for risky traders.

Back testing suggests that body high will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Important Settings

You can enable or disable the 4th candle signal to avoid the noise, but at times I have noticed that the 4th candle gives a very strong signal or I can say that the strong signal falls on the 4th candle. This is mostly a coincidence.

You can also configure how many previous bars should the signal be generated for. 10 to 30 is good enough. To backtest increase it to 2000 or 5000 for example.

Rest are self explanatory.

Pointers

If after taking the trade, the next candle moves in your direction and closes strong bullish or bearish, then move SL to break even and after that you can trail it.

If a upside trade hits SL and immediately a down side trade signal is generated on the next candle then take it. Vice versa is true.

Trades need to be taken on previous 2 candle's body high or low combined and not the wicks.

The most losses a trader takes is on a sideways day and because in our strategy the stop loss is so small that even on a sideways day we'll get out with a little profit or worst break even.

Hold targets for longer targets and don't panic.

If last 3-4 days have been sideways then there is a good probability that day will be trending so we can hold our trade for longer targets. Target to hold the trade for whole day and not exit till the day closes.

In general avoid trading in the middle of the day for index and stocks. Divide the day into 3 parts and avoid the middle.

Use Support/Resistance, 10, 20, 50, 200 EMA/SMA, Gaps, Whole/Round numbers(very imp) for identifying targets.

Trail your SL.

For indexes I would use 5 min and 15 min timeframe.

For commodities and crypto we can use higher timeframe as well. Look for signals during volatile time durations and avoid trading the whole day. Signal usually gives good targets on those times.

If a GRG or RGR pattern appears on a daily timeframe then this is our time to go big.

Minimum Risk to Reward should be 1:2 and for longer targets can be 1:4 to 1:10.

Trade with small lot size. Money management will happen automatically.

With small lot size and correct Risk-Re ward we can be very profitable. Don't trade with big lot size.

Stay in the market for longer and collect points not money.

Very imp - Watch market and learn to generate a market view.

Very imp - Only 4 candles are needed in trading - strong bullish, strong bearish, hammer, inverse hammer and doji.

Go big on bearish days for option traders. Puts are better bought and Calls are better sold.

Cluster of green signals can lead to bigger move on the upside and vice versa for red signals.

Most of this is what I learned from successful traders (from the top 2%) only the indicator is mine.

Opening Range Gaps [TakingProphets]What is an Opening Range Gap (ORG)?

In ICT, the Opening Range Gap is defined as the price difference between the previous session’s close (e.g., 4:00 PM EST in U.S. indices) and the current day’s open (9:30 AM EST).

That gap is a liquidity void—an area where no trading occurred during regular hours.

Why ICT Traders Care About ORG

Liquidity Void (Gap Fill Logic)

-Because the gap is an untraded area, it naturally acts as a draw on liquidity.

-Price often seeks to rebalance by retracing into or fully filling this void.

Premium/Discount Sensitivity

-Once the ORG is defined, ICT treats it as a mini dealing range.

-Above EQ (Consequent Encroachment) = algorithmic premium (sell-sensitive).

-Below EQ = algorithmic discount (buy-sensitive).

-Price reaction at these levels gives a precise read on institutional intent intraday.

Support/Resistance from ORG

-If the session opens above prior close, the gap often acts as support until violated.

-If the session opens below prior close, the gap often acts as resistance until reclaimed.

Key ICT Concepts Anchored to ORG

Consequent Encroachment (CE): The midpoint of the gap. The algo is highly sensitive to CE as a decision point: reject → continuation; reclaim → reversal.

Draw on Liquidity (DoL): Price is algorithmically “pulled” toward gap fills, CE, or the opposite side of the ORG.

Order Flow Confirmation: If price ignores the gap and runs away from it, this signals strong institutional order flow in that direction.

Confluence with Other Tools: FVGs, OBs, and HTF PD arrays often overlap with ORG levels, strengthening setups.

Practical Application for Traders

Bias Formation:

Use ORG EQ as a line in the sand for intraday bias.

If price trades below ORG EQ after the open → look for short setups into the prior day’s low or external liquidity.

If price trades above ORG EQ → favor longs into highs/liquidity pools.

Execution Framework:

Wait for liquidity raids or market structure shifts at ORG edges (.00, .25, .50, .75).

Target: EQ, opposite quarter, or full gap fill.

Precision Reads:

ORG lines let traders anticipate where algorithms are likely to respond, providing mechanical invalidation and clear targets without clutter.

Hour/Day/Month Optimizer [CHE] Hour/Day/Month Optimizer — Bucketed seasonality ranking for hours, weekdays, and months with additive or compounded returns, win rate, simple Sharpe proxy, and trade counts

Summary

This indicator profiles time-of-day, day-of-week, and month-of-year behavior by assigning every bar to a bucket and accumulating its return into that bucket. It reports per-bucket score (additive or compounded), win rate, a dispersion-aware return proxy, and trade counts, then ranks buckets and highlights the current one if it is best or worst. A compact on-chart table shows the top buckets or the full ranking; a last-bar label summarizes best and worst. Optional hour filtering and UTC shifting let you align buckets with your trading session rather than exchange time.

Motivation: Why this design?

Traders often see repetitive timing effects but struggle to separate genuine seasonality from noise. Static averages are easily distorted by sample size, compounding, or volatility spikes. The core idea here is simple, explicit bucket aggregation with user-controlled accumulation (sum or compound) and transparent quality metrics (win rate, a dispersion-aware proxy, and counts). The result is a practical, legible seasonality surface that can be used for scheduling and filtering rather than prediction.

What’s different vs. standard approaches?

Reference baseline: Simple heatmaps or average-return tables that ignore compounding, dispersion, or sample size.

Architecture differences:

Dual aggregation modes: additive sum of bar returns or compounded factor.

Per-bucket win rate and trade count to expose sample support.

A simple dispersion-aware return proxy to penalize unstable averages.

UTC offset and optional custom hour window.

Deterministic, closed-bar rendering via a lightweight on-chart table.

Practical effect: You see not only which buckets look strong but also whether the observation is supported by enough bars and whether stability is acceptable. The background tint and last-bar label give immediate context for the current bucket.

How it works (technical)

Each bar is assigned to a bucket based on the selected dimension (hour one to twenty-four, weekday one to seven, or month one to twelve) after applying the UTC shift. An optional hour filter can exclude bars outside a chosen window. For each bucket the script accumulates either the sum of simple returns or the compounded product of bar factors. It also counts bars and wins, where a win is any bar with a non-negative return. From these, it derives:

Score: additive total or compounded total minus the neutral baseline.

Win rate: wins as a percentage of bars in the bucket.

Dispersion-aware proxy (“Sharpe” column): a crude ratio that rises when average return improves and falls when variability increases.

Buckets are sorted by a user-selected key (score, win rate, dispersion proxy, or trade count). The current bar’s bucket is tinted if it matches the global best or worst. At the last bar, a table is drawn with headers, an optional info row, and either the top three or all rows, using zebra backgrounds and color-coding (lime for best, red for worst). Rendering is last-bar only; no higher-timeframe data is requested, and no future data is referenced.

Parameter Guide

UTC Offset (hours) — Shifts bucket assignment relative to exchange time. Default: zero. Tip: Align to your local or desk session.

Use Custom Hours — Enables a local session window. Default: off. Trade-off: Reduces noise outside your active hours but lowers sample size.

Start / End — Inclusive hour window one to twenty-four. Defaults: eight to seventeen. Tip: Widen if rankings look unstable.

Aggregation — “Additive” sums bar returns; “Multiplicative” compounds them. Default: Additive. Tip: Use compounded for long-horizon bias checks.

Dimension — Bucket by Hour, Day, or Month. Default: Hour. Tip: Start Hour for intraday planning; switch to Day or Month for scheduling.

Show — “Top Three” or “All”. Default: Top Three. Trade-off: Clarity vs. completeness.

Sort By — Score, Win Rate, Sharpe, or Trades. Default: Score. Tip: Use Trades to surface stable buckets; use Win Rate for skew awareness.

X / Y — Table anchor. Defaults: right / top. Tip: Move away from price clusters.

Text — Table text size. Default: normal.

Light Mode — Light palette for bright charts. Default: off.

Show Parameters Row — Info header with dimension and span. Default: on.

Highlight Current Bucket if Best/Worst — Background tint when current bucket matches extremes. Default: on.

Best/Worst Barcolor — Tint colors. Defaults: lime / red.

Mark Best/Worst on Last Bar — Summary label on the last bar. Default: on.

Reading & Interpretation

Score column: Higher suggests stronger cumulative behavior for the chosen aggregation. Compounded mode emphasizes persistence; additive mode treats all bars equally.

Win Rate: Stability signal; very high with very low trades is unreliable.

“Sharpe” column: A quick stability proxy; use it to down-rank buckets that look good on score but fluctuate heavily.

Trades: Sample size. Prefer buckets with adequate counts for your timeframe and asset.

Tinting: If the current bucket is globally best, expect a lime background; if worst, red. This is context, not a trade signal.

Practical Workflows & Combinations

Trend following: Use Hour or Day to avoid initiating trades during historically weak buckets; require structure confirmation such as higher highs and higher lows, plus a momentum or volatility filter.

Mean reversion: Prefer buckets with moderate scores but acceptable win rate and dispersion proxy; combine with deviation bands or volume normalization.

Exits/Stops: Tighten exits during historically weak buckets; relax slightly during strong ones, but keep absolute risk controls independent of the table.

Multi-asset/Multi-TF: Start with Hour on liquid intraday assets; for swing, use Day. On monthly seasonality, require larger lookbacks to avoid overfitting.

Behavior, Constraints & Performance

Repaint/confirmation: Calculations use completed bars only; table and label are drawn on the last bar and can update intrabar until close.

security()/HTF: None used; repaint risk limited to normal live-bar updates.

Resources: Arrays per dimension, light loops for metric building and sorting, `max_bars_back` two thousand, and capped label/table counts.

Known limits: Sensitive to sample size and regime shifts; ignores costs and slippage; bar-based wins can mislead on assets with frequent gaps; compounded mode can over-weight streaks.

Sensible Defaults & Quick Tuning

Start: Hour dimension, Additive, Top Three, Sort by Score, default session window off.

Too many flips: Switch to Sort by Trades or raise sample by widening hours or timeframe.

Too sluggish/over-smoothed: Switch to Additive (if on compounded) or shorten your chart timeframe while keeping the same dimension.

Overfit risk: Prefer “All” view to verify that top buckets are not isolated with tiny counts; use Day or Month only with long histories.

What this indicator is—and isn’t

This is a seasonality and scheduling layer that ranks time buckets using transparent arithmetic and simple stability checks. It is not a predictive model, not a complete trading system, and it does not manage risk. Use it to plan when to engage, then rely on structure, confirmation, and independent risk management for entries and exits.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

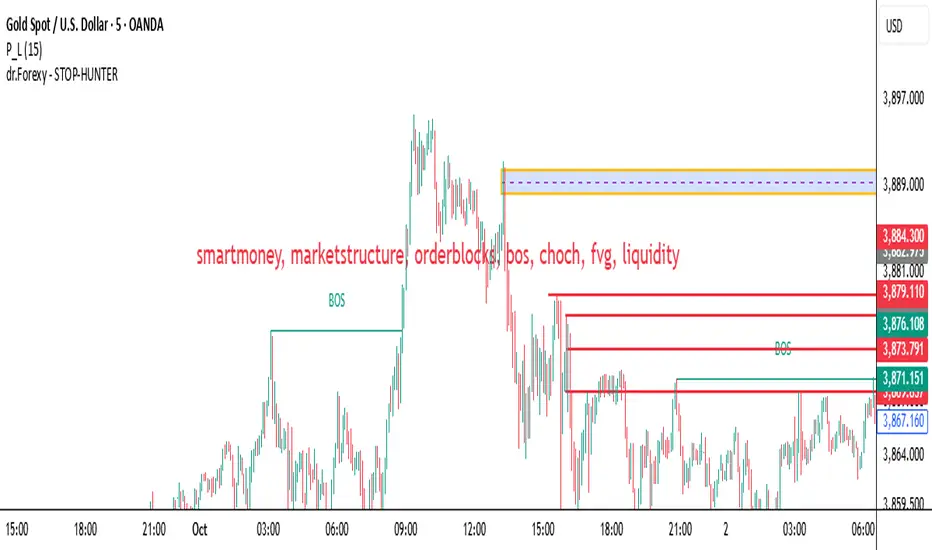

HUNT_line [Dr.Forexy]HUNT_line Indicator

📊 **Category:** Price Action & Market Structure

⏰ **Recommended Timeframe:** 5-minute and higher

🎯 **Purpose:** Advanced market structure visualization for professional traders

⸻

⚡ **Key Features:**

• Break of Structure (BOS) and Change of Character (CHOCH) detection

• Internal & Swing Market Structure analysis

• Order Blocks identification with smart filtering

• Fair Value Gaps (FVG) visualization

• Premium/Discount Zones

• Multi-timeframe support

• Real-time structure alerts

⸻

🛠 **How to Use:**

1. Apply on 5M or higher timeframes for best results

2. Monitor BOS/CHOCH for trend direction changes

3. Use Order Blocks as potential support/resistance areas

4. Watch for FVG fills as price inefficiency zones

5. Combine multiple confluences for higher probability setups

⸻

⚠️ **Risk Disclaimer:**

This indicator is for educational purposes only.

Not financial advice. Always conduct your own research.

⸻

🔹 **Credits:**

Inspired by LuxAlgo's "Smart Money Concepts" with custom improvements

Predicted Funding RatesOverview

The Predicted Funding Rates indicator calculates real-time funding rate estimates for perpetual futures contracts on Binance. It uses triangular weighting algorithms on multiple different timeframes to ensure an accurate prediction.

Funding rates are periodic payments between long and short position holders in perpetual futures markets

If positive, longs pay shorts (usually bullish)

If negative, shorts pay longs (usually bearish)

This is a prediction. Actual funding rates depend on the instantaneous premium index, derived from bid/ask impacts of futures. So whilst it may imitate it similarly, it won't be completely accurate.

This only applies currently to Binance funding rates, as HyperLiquid premium data isn't available. Other Exchanges may be added if their premium data is uploaded.

Methods

Method 1: Collects premium 1-minunute data using triangular weighing over 8 hours. This granular method fills in predicted funding for 4h and less recent data

Method 2: Multi-time frame approach. Daily uses 1 hour data in the calculation, 4h + timeframes use 15M data. This dynamic method fills in higher timeframes and parts where there's unavailable premium data on the 1min.

How it works

1) Premium data is collected across multiple timeframes (depending on the timeframe)

2) Triangular weighing is applied to emphasize recent data points linearly

Tri_Weighing = (data *1 + data *2 + data *3 + data *4) / (1+2+3+4)

3) Finally, the funding rate is calculated

FundingRate = Premium + clamp(interest rate - Premium, -0.05, 0.05)

where the interest rate is 0.01% as per Binance

Triangular weighting is calculated on collected premium data, where recent data receives progressively higher weight (1, 2, 3, 4...). This linear weighting scheme provides responsiveness to recent market conditions while maintaining stability, similar to an exponential moving average but with predictable, linear characteristics

A visual representation:

Data points: ──────────────>

Weights: 1 2 3 4 5

Importance: ▂ ▃ ▅ ▆ █

How to use it

For futures traders:

If funding is trending up, the market can be interpreted as being in a bull market

If trending down, the market can be interpreted as being in a bear market

Even used simply, it allows you to gauge roughly how well the market is performing per funding. It can basically be gauged as a sentiment indicator too

For funding rate traders:

If funding is up, it can indicate a long on implied APR values

If funding is down, it can indicate a short on implied APR values

It also includes an underlying APR, which is the annualized funding rate. For Binance, it is current funding * (24/8) * 365

For Position Traders: Monitor predicted funding rates before entering large positions. Extremely high positive rates (>0.05% for 8-hour periods) suggest overleveraged longs and potential reversal risk. Conversely, extreme negative rates indicate shorts dominance

Table:

Funding rate: Gives the predicted funding rate as a percentage

Current premium: Displays the current premium (difference between perpetual futures price and the underlying spot) as a percentage

Funding period: You can choose between 1 hour funding (HyperLiquid usually) and 8 hour funding (Binance)

APR: Underlying annualized funding rate

What makes it original

Whilst some predicted funding scripts exist, some aren't as accurate or have gaps in data. And seeing as funding values are generally missing from TV tickers, this gives traders accessibility to the script when they would have to use other platforms

Notes

Currently only compatible with symbols that have Binance USDT premium indices

Optimal accuracy is found on timeframes that are 4H or less. On higher timeframes, the accuracy drops off

Actual funding rates may differ

Inputs

Funding Period: Choose between "8 Hour" (standard Binance cycle) or "1 Hour" (divides the 8-hour rate by 8 for granular comparison)

Plot Type: Display as "Funding Rate" (percentage per interval) or "APR" (annualized rate calculated as 8-hour rate × 3 × 365)

Table: Toggle the information table showing current funding rate, premium, funding period, and APR in the top-right corner

Positive Colour: Sets the colour for positive funding rates where longs pay shorts (default: #00ffbb turquoise)

Negative Colour: Sets the colour for negative funding rates where shorts pay longs (default: red)

Table Background: Controls the background colour and transparency of the information table (default: transparent dark blue)

Table Text Colour: Sets the colour for all text labels in the information table (default: white)

Table Text Size: Controls font size with options from Tiny to Huge, with Small as the default balance of readability and space

Dynamic Volume Trace Profile [ChartPrime]⯁ OVERVIEW

Dynamic Volume Trace Profile is a reimagined take on volume profile analysis. Instead of plotting a static horizontal histogram on the side of your chart, this indicator projects dynamic volume trace lines directly onto the price action. Each bin is color-graded according to its relative strength, creating a living “volume skeleton” of the market. The orange trace highlights the current Point of Control (POC)—the price level with maximum historical traded volume within the lookback window. On the right side, the tool builds a mini profile, showing absolute volume per bin alongside its percentage share, where the POC always represents 100% strength .

⯁ KEY FEATURES

Dynamic On-Chart Bins:

The range between highest high and lowest low is split into 25 bins. Each bin is drawn as a horizontal trace line across the lookback chart period.

Gradient Color Encoding:

Trace lines fade from transparent to teal depending on relative volume size. The more intense the teal, the stronger the historical traded activity at that level.

Automatic POC Highlight:

The bin with the highest aggregated volume is flagged with an orange line . This POC adapts bar-by-bar as volume distribution shifts.

Right-Side Volume Profile:

At the chart’s right edge, the script prints a box-style profile. Each bin shows:

• Total volume (absolute units).

• Percentage of max volume, in parentheses (POC bin = 100%).

This gives both raw and normalized context at a glance.

Adjustable Lookback Window:

The lookback defines how many bars feed the profile. Increase for stable HTF zones or decrease for responsive intraday distributions.

POC Toggle & Styling:

Optionally toggle POC highlighting on/off, adjust colors, and set line thickness for better integration with your chart theme.

⯁ HOW IT WORKS (UNDER THE HOOD)

Step Sizing:

over last 100 bars is divided by to calculate bin height.

Volume Aggregation:

For each bar in the , the script checks which bin the close falls into, then adds that bar’s volume to the bin’s counter.

Gradient Mapping:

Bin volume is normalized against the max volume across all bins. That value is mapped onto a gradient from transparent → teal.

POC Logic:

The bin with highest volume is colored orange both on the dynamic trace and in the right-side profile.

Right-Hand Profile:

Boxes are drawn for each bin proportional to volume / maxVolume × 50 units, with text labels showing both absolute volume and normalized %.

⯁ USAGE

Use the orange trace as the dominant “magnet” level—price often gravitates to the POC.

Watch for clusters of strong teal traces as areas of high acceptance; thin or faint zones mark low-liquidity gaps prone to fast moves.

On intraday charts, tighten lookback to reveal session-based distributions . For swing or position trading, expand lookback to surface more durable volume shelves.

Compare the right-side profile % to judge how “top-heavy” or “bottom-heavy” the current distribution is.

Use bright, intense color traces as context for confluence with structure, OBs, or liquidity hunts.

⯁ CONCLUSION

Dynamic Volume Trace Profile takes the traditional volume profile and fuses it into the body of price itself. Instead of a fixed sidebar, you see gradient traces layered directly on the chart, giving real-time context of where volume concentrated and where price may be drawn. With built-in POC highlighting, normalized % readouts, and an adaptive right-side profile, it offers both precision levels and market structure awareness in a cleaner, more intuitive form.

Volume Profile 3D (Zeiierman)█ Overview

Volume Profile 3D (Zeiierman) is a next-generation volume profile that renders market participation as a 3D-style profile directly on your chart. Instead of flat histograms, you get a depth-aware profile with parallax, gradient transparency, and bull/bear separation, so you can see where liquidity stacked up and how it shifted during the move.

Highlights:

3D visual effect with perspective and depth shading for clarity.

Bull/Bear separation to see whether up bars or down bars created the volume.

Flexible colors and gradients that highlight where the most significant trading activity took place.

This is a state-of-the-art volume profile — visually powerful, highly flexible, and unlike anything else available.

█ How It Works

⚪ Profile Construction

The price range (from highest to lowest) is divided into a number of levels (buckets). Each bar’s volume is added to the correct level, based on its average price. This builds a map of where trading volume was concentrated.

You can choose to:

Aggregate all volume at each level, or

Split bullish vs. bearish volume , slightly offset for clarity.

This creates a clear view of which price zones matter most to the market.

⚪ 3D Effect Creation

The unique part of this indicator is how the 3D projection is built. Each volume block’s width is scaled to its relative size, then tilted with a slope factor to create a depth effect.

maxVol = bins.bu.max() + bins.be.max()

width = math.max(1, math.floor(bucketVol / maxVol * ((bar_index - start) * mult)))

slope = -(step * dev) / ((bar_index - start) * (mult/2))

factor = math.pow(math.min(1.0, math.abs(slope) / step), .5)

width → determines how far the volume extends, based on relative strength.

slope → creates the angled projection for the 3D look.

factor → adjusts perspective to make deeper areas shrink naturally.

The result is a 3D-style volume profile where large areas pop forward and smaller areas fade back, giving you immediate visual context.

█ How to Use

⚪ Support & Resistance Zones (HVNs and Value Area)

Regions where a lot of volume traded tend to act like walls:

If price approaches a high-volume area from above, it may act as support.

From below, it may act as resistance.

Traders often enter or exit near these zones because they represent strong agreement among market participants.

⚪ POC Rejections & Mean Reversions

The Point of Control (POC) is the single price level with the highest volume in the profile.

When price returns to the POC and rejects it, that’s often a signal for reversal trades.

In ranging markets, price may bounce between edges of the Value Area and revert to POC.

⚪ Breakouts via Low-Volume Zones (LVNs)

Low volume areas (gaps in the profile) offer path of least resistance:

Price often moves quickly through these thin zones when momentum builds.

Use them to spot breakouts or continuation trades.

⚪ Directional Insight

Use the bull/bear separation to see whether buyers or sellers dominated at key levels.

█ Settings

Use Active Chart – Profile updates with visible candles.

Custom Period – Fixed number of bars.

Up/Down – Adjust tilt for the 3D angle.

Left/Right – Scale width of the profile.

Aggregated – Merge bull/bear volume.

Bull/Bear Shift – Separate bullish and bearish volume.

Buckets – Number of price levels.

Choose from templates or set custom colors.

POC Gradient option makes high volume bolder, low volume lighter.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

RXTrend█ OVERVIEW

The "RXTrend" indicator is a technical analysis tool based on a unique approach to trend identification using RSI values from overbought and oversold zones. Designed for traders seeking a precise tool to identify key market levels and trend direction, the indicator offers flexible settings, dynamic trend lines, candlestick coloring, and buy/sell signals, supported by alerts for key events.

█ CONCEPTS

"RXTrend" leverages the Relative Strength Index (RSI) to identify overbought and oversold zones, which are often significant areas on the chart due to potentially higher volume, increased volatility, or acting as pivot points. To address this, I created an indicator that uses RSI values from these zones, mapping them to price levels to determine the trend. Additionally, for a clearer market picture, boxes are added to highlight overbought and oversold zones on the chart, and candlestick coloring is based on the direction of the RSI moving average. This provides further confirmation of the trend direction and identifies potential correction or reversal points. The indicator is universal and works across all markets (stocks, forex, cryptocurrencies) and timeframes.

█ FEATURES

- RSI Calculation: Calculates RSI based on the closing price over a specified period, with a default length of 14.

- Trend Line: A smoothed trend line based on mapping RSI values from overbought (for downtrends) or oversold (for uptrends) zones to price levels. RSI values are transformed into prices using the price range from a selected period (default: 50 bars) and then smoothed to form the trend line. The line changes color based on the trend direction (blue for uptrend, orange for downtrend).

- Candlestick Coloring: Option to color candles based on the direction of the RSI moving average (RSI MA). Candle colors align with the trend and box colors (blue for uptrend, orange for downtrend, gray for neutral).

- Overbought and Oversold Zones: Identifies overbought (RSI > OB) and oversold (RSI < OS) levels, drawing dynamic boxes on the price chart to reflect these zones. Boxes update in real-time, adjusting to new highs and lows.

- Buy and Sell Signals: Generates buy signals (blue "Buy" labels) when the price crosses above the smoothed oversold line and sell signals (orange "Sell" labels) when the price crosses below the smoothed overbought line.

- Shadow Fill: Option to fill the space between the trend line and price (HL2) with adjustable transparency, aiding visual trend assessment.

Alerts: Built-in alerts for:

- Buy and sell signals.

- Appearance of new overbought/oversold boxes.

- RSI MA direction change (candle color change to uptrend or downtrend).

Customization: Allows adjustment of RSI length, overbought/oversold levels, smoothing period, colors, box and label transparency, and the option to keep boxes after RSI returns to normal.

█ HOW TO USE

Add to Chart: Apply the indicator to your TradingView chart via the Pine Editor or Indicators menu.

Configure Settings:

RSI Settings:

- RSI Length: Sets the RSI calculation period (default: 14).

- Overbought Level (OB): Sets the overbought threshold (default: 70).

- Oversold Level (OS): Sets the oversold threshold (default: 30).

Price Settings:

- Price Range Lookback: Defines the period for calculating the price range (default: 50).

Candle Coloring:

- Color Candles: Enables/disables candle coloring based on RSI MA direction.

- RSI MA Length: Sets the RSI moving average period (default: 21).

Smoothing Settings:

- Smoothing Length: Degree of trend line smoothing (default: 5).

Colors:

- Trend Colors: Customize colors for uptrend (default: blue), downtrend (default: orange), and shadow fill.

Box Settings:

- Box Transparency: Adjusts box transparency (0-100).

- Box Colors: Sets colors for overbought (orange) and oversold (blue) zones.

- Keep Boxes: Determines if boxes remain after RSI returns to normal.

Signals:

- Show Buy/Sell Signals: Enables/disables signal label display.

- Label Transparency: Adjusts signal label transparency.

Interpreting Signals:

- Trend Line: Shows market direction (blue for uptrend, orange for downtrend).

- Buy Signals: Blue "Buy" label appears when the price crosses above the smoothed oversold line, signaling a potential uptrend.

- Sell Signals: Orange "Sell" label appears when the price crosses below the smoothed overbought line, signaling a potential downtrend.

- Overbought/Oversold Boxes: Orange boxes indicate overbought zones (RSI > OB), blue boxes indicate oversold zones (RSI < OS). Boxes expand dynamically in real-time.

- Candlestick Coloring: Candle colors align with the trend and box colors, reflecting RSI MA direction.

- Alerts: Set up alerts in TradingView for buy/sell signals, new overbought/oversold boxes, or RSI MA direction changes.

- Combining with Other Tools: Use the indicator alongside support/resistance levels, Fair Value Gaps (FVG), or other indicators to confirm signals.

█ APPLICATIONS

The "RXTrend" indicator is designed to identify key market zones and trend direction, making it useful for trend-following and reversal strategies. It enables:

- Trend Confirmation: Candlestick coloring and the trend line help assess the dominant market direction, supporting entry or exit decisions. The trend line can act as a significant support/resistance level, and a price bounce from it may provide a good entry point, especially when confirmed by Fibonacci levels. Additionally, the appearance of overbought/oversold boxes combined with a change in candle color (RSI MA direction) may indicate an impending correction. This allows analysis of potential market overextension and correction endings, enabling multiple entries within a trend.

- Overbought and Oversold Zone Identification: Boxes highlight potential reversal or correction points, especially when combined with support/resistance levels or FVG.

- Signal-Based Strategies: Buy and sell signals can be used as entry points in a trend or as warnings of potential reversals.

█ NOTES

- The indicator is universal and works across all markets and timeframes due to its RSI-based and price-mapping logic.

- Adjust settings (e.g., RSI length, OB/OS levels, smoothing) to suit your trading style and timeframe.

- Use in conjunction with other technical analysis tools to enhance signal accuracy.

MAMA [DCAUT]█ MAMA (MESA Adaptive Moving Average)

📊 OVERVIEW

The MESA Adaptive Moving Average (MAMA) represents an advanced implementation of John F. Ehlers' adaptive moving average system using the Hilbert Transform Discriminator. This indicator automatically adjusts to market cycles, providing superior responsiveness compared to traditional fixed-period moving averages while maintaining smoothness.

MAMA dynamically calculates two lines: the fast-adapting MAMA line and the following FAMA (Following Adaptive Moving Average) line. The system's core strength lies in its ability to automatically detect and adapt to the dominant market cycle, reducing lag during trending periods while providing stability during consolidation phases.

🎯 CORE CONCEPTS

Signal Interpretation:

• MAMA above FAMA: Indicates bullish trend momentum with the fast line leading upward movement

• MAMA below FAMA: Suggests bearish trend momentum with the fast line leading downward movement

• Golden Cross: MAMA crossing above FAMA signals potential upward momentum shift

• Death Cross: MAMA crossing below FAMA indicates potential downward momentum shift

• Line Convergence: MAMA and FAMA approaching each other suggests trend consolidation or potential reversal

Primary Applications:

• Trend Following: Enhanced responsiveness to trend changes compared to traditional moving averages

• Crossover Signals: MAMA/FAMA crossovers for identifying potential entry and exit points

• Cycle Analysis: Automatic adaptation to market's dominant cycle characteristics

• Reduced Lag: Minimized delay in trend detection while maintaining signal smoothness

📐 MATHEMATICAL FOUNDATION

Hilbert Transform Discriminator Technology:

The MAMA system employs John F. Ehlers' Hilbert Transform Discriminator, a sophisticated signal processing technique borrowed from telecommunications engineering. The Hilbert Transform creates a complex representation of the price series by generating a 90-degree phase-shifted version of the original signal, enabling precise cycle measurement.

The discriminator analyzes the instantaneous phase relationships between the original price series and its Hilbert Transform counterpart. This mathematical relationship reveals the dominant cycle period present in the market data at each point in time, forming the foundation for adaptive smoothing.

Instantaneous Period Calculation:

The algorithm computes the instantaneous period using the arctangent of the ratio between the Hilbert Transform and the original price series. This calculation produces a real-time measurement of the market's dominant cycle, typically ranging from short-term noise cycles to longer-term trend cycles.

The instantaneous period measurement undergoes additional smoothing to prevent erratic behavior from single-bar anomalies. This smoothed period value becomes the basis for calculating the adaptive alpha coefficient that controls the moving average's responsiveness.

Dynamic Alpha Coefficient System:

The adaptive alpha calculation represents the core mathematical innovation of MAMA. The alpha coefficient is derived from the instantaneous period measurement and constrained within the user-defined fast and slow limits.

The mathematical relationship converts the measured cycle period into an appropriate smoothing factor: shorter detected cycles result in higher alpha values (increased responsiveness), while longer cycles produce lower alpha values (increased stability). This creates an automatic adaptation mechanism that responds to changing market conditions.

MAMA/FAMA Calculation Process:

The MAMA line applies the dynamically calculated alpha coefficient to an exponential moving average formula: MAMA = alpha × Price + (1 - alpha) × MAMA . The FAMA line then applies a secondary smoothing operation to the MAMA line, creating a following average that provides confirmation signals.

This dual-line approach ensures that the fast-adapting MAMA line captures trend changes quickly, while the FAMA line offers a smoother confirmation signal, reducing the likelihood of acting on temporary price fluctuations.

Cycle Detection Mechanism:

The underlying cycle detection employs quadrature components derived from the Hilbert Transform to measure both amplitude and phase characteristics of price movements. This allows the system to distinguish between genuine trend changes and temporary price noise, automatically adjusting the smoothing intensity accordingly.

The mathematical framework ensures that during strong trending periods with clear directional movement, the algorithm reduces smoothing to minimize lag. Conversely, during consolidation phases with mixed signals, increased smoothing helps filter out false breakouts and whipsaws.

📋 PARAMETER CONFIGURATION

Source Selection Strategy:

• HL2 (High+Low)/2 (Default): Recommended for cycle analysis as it represents the midpoint of each period's trading range, reducing impact of opening gaps and closing spikes

• Close Price: Traditional choice reflecting final market sentiment, suitable for end-of-day analysis

• HLC3 (High+Low+Close)/3: Balanced approach incorporating range information with closing emphasis

• OHLC4 (Open+High+Low+Close)/4: Most comprehensive price representation for complete market view

Fast Limit Configuration (Default 0.5):

Controls the maximum responsiveness of the adaptive system. Higher values increase sensitivity to recent price changes but may introduce more noise. This parameter sets the upper bound for the dynamic alpha calculation.

Slow Limit Configuration (Default 0.05):

Determines the minimum responsiveness, providing stability during uncertain market conditions. Lower values increase smoothing but may cause delayed signals. This parameter sets the lower bound for the dynamic alpha calculation.

Parameter Relationship Considerations:

The fast and slow limits work together to define the adaptive range. The wider the range between these limits, the more dramatic the adaptation between trending and consolidating market conditions. Different market characteristics may benefit from different parameter configurations, requiring individual testing and validation.

📊 COLOR CODING SYSTEM

Line Visualization:

• Green Line (MAMA): The fast-adapting moving average that responds quickly to price changes

• Red Line (FAMA): The following adaptive moving average that provides confirmation signals

The fixed color scheme provides consistent visual identification of each line, enabling clear differentiation between the fast-adapting MAMA and the following FAMA throughout all market conditions.

💡 CORE VALUE PROPOSITION

Advantages Over Traditional Moving Averages:

• Cycle Adaptation: Automatically adjusts to market's dominant cycle rather than using fixed periods

• Reduced Lag: Faster response to genuine trend changes while filtering market noise

• Mathematical Foundation: Based on advanced signal processing techniques from telecommunications engineering

• Dual-Line System: Provides both fast adaptation (MAMA) and confirmation (FAMA) in one indicator

Comparative Performance Characteristics:

Unlike fixed-period moving averages that apply the same smoothing regardless of market conditions, MAMA adapts its behavior based on current market cycle characteristics. This may help reduce whipsaws during consolidation periods while maintaining responsiveness during trending phases.

Usage Considerations:

This indicator is designed for technical analysis purposes. The adaptive nature means that parameter optimization should consider the specific characteristics of the asset and timeframe being analyzed. Like all technical indicators, MAMA should be used as part of a comprehensive analysis approach rather than as a standalone signal generator.

Alert Functionality:

The indicator includes alert conditions for MAMA/FAMA crossovers, enabling automated notification of potential momentum shifts. These alerts can assist in timing analysis but should be combined with other forms of market analysis for decision-making purposes.

ICT SMC — OB & FVG (Enhanced v6)This indicator is a comprehensive implementation of ICT Smart Money Concepts (SMC), focusing on Order Blocks (OB) and Fair Value Gaps (FVG) with enhanced detection logic and session-based filtering.

🔍 Key Features

Impulse-Based OB Detection: Identifies bullish and bearish order blocks using configurable impulse bar logic and ATR-based movement thresholds.

Fair Value Gap Detection: Highlights FVGs based on price displacement logic, helping traders spot potential inefficiencies in price action.

Session Filtering: Allows users to filter signals based on major trading sessions (Sydney, Tokyo, London, New York).

Trend & Volume Confirmation: Integrates EMA slope, market structure breaks, and volume analysis to score trade signals.

Visual Zones: Displays OB and FVG zones using colored boxes with customizable transparency and color settings.

Signal Alerts: Generates long/short trade signals based on a scoring system and session validation, with built-in alert conditions.

⚙️ Customization

Adjustable EMA and ATR lengths

Configurable impulse bar count and movement thresholds

Toggleable session filters

Custom colors for OB and FVG zones

📈 Use Cases

This tool is ideal for traders who follow ICT concepts and want a visual, automated way to identify high-probability zones and trade setups based on smart money principles.

SCTI - D14SCTI - D14 Comprehensive Technical Analysis Suite

English Description

SCTI D14 is an advanced multi-component technical analysis indicator designed for professional traders and analysts. This comprehensive suite combines multiple analytical tools into a single, powerful indicator that provides deep market insights across various timeframes and methodologies.

Core Components:

1. EMA System (Exponential Moving Averages)

13 customizable EMA lines with periods ranging from 8 to 2584

Fibonacci-based periods (8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584)

Color-coded visualization for easy trend identification

Individual toggle controls for each EMA line

2. TFMA (Multi-Timeframe Moving Averages)

Cross-timeframe analysis with 3 independent EMA calculations

Real-time labels showing trend direction and price relationships

Customizable timeframes for each moving average

Percentage deviation display from current price

3. PMA (Precision Moving Average Cloud)

7-layer moving average system with customizable periods

Fill areas between moving averages for trend visualization

Support and resistance zone identification

Dynamic color-coded trend clouds

4. VWAP (Volume Weighted Average Price)

Multiple anchor points (Session, Week, Month, Quarter, Year, Earnings, Dividends, Splits)

Standard deviation bands for volatility analysis

Automatic session detection and anchoring

Statistical price level identification

5. Advanced Divergence Detector

12 technical indicators for divergence analysis (MACD, RSI, Stochastic, CCI, Williams %R, Bias, Momentum, OBV, VW-MACD, CMF, MFI, External)

Regular and hidden divergences detection

Bullish and bearish signals with visual confirmation

Customizable sensitivity and filtering options

Real-time alerts for divergence formations

6. Volume Profile & Node Analysis

Comprehensive volume distribution analysis

Point of Control (POC) identification

Value Area High/Low (VAH/VAL) calculations

Volume peaks and troughs detection

Support and resistance levels based on volume

7. Smart Money Concepts

Market structure analysis with Break of Structure (BOS) and Change of Character (CHoCH)

Internal and swing structure detection

Equal highs and lows identification

Fair Value Gaps (FVG) detection and visualization

Liquidity zones and institutional flow analysis

8. Trading Sessions

9 major trading sessions (Asia, Sydney, Tokyo, Shanghai, Hong Kong, Europe, London, New York, NYSE)

Real-time session status and countdown timers

Session volume and performance tracking

Customizable session boxes and labels

Statistical session analysis table

Key Features:

Modular Design: Enable/disable any component independently

Real-time Analysis: Live updates with market data

Multi-timeframe Support: Works across all chart timeframes

Customizable Alerts: Set alerts for any detected pattern or signal

Professional Visualization: Clean, organized display with customizable colors

Performance Optimized: Efficient code for smooth chart performance

Use Cases:

Trend Analysis: Identify market direction using multiple EMA systems

Entry/Exit Points: Use divergences and structure breaks for timing

Risk Management: Utilize volume profiles and session analysis for better positioning

Multi-timeframe Analysis: Confirm signals across different timeframes

Institutional Analysis: Track smart money flows and market structure

Perfect For:

Day traders seeking comprehensive market analysis

Swing traders needing multi-timeframe confirmation

Professional analysts requiring detailed market structure insights

Algorithmic traders looking for systematic signal generation

---