The Great Anchors: Dual AVWAP Powered by RSI

The Great Anchors

*Dual Anchored Volume Weighted Average Price Powered by RSI*

---

📌 Overview

The Great Anchors is a dual AVWAP-based indicator that resets dynamically using RSI extremes — either from the current asset or a master symbol (e.g., BTCUSDT). It identifies meaningful shifts in price structure and momentum using these "anchored" levels.

It’s designed to help traders spot trend continuations, momentum inflection points, and entry signals aligned with overbought/oversold conditions — but only when the market confirms through volume-weighted price direction.

---

🛠 Core Logic

• AVWAP 1 (favwap): Anchored when RSI reaches overbought levels (top anchor)

• AVWAP 2 (savwap): Anchored when RSI reaches oversold levels (bottom anchor)

• AVWAPs are recalculated each time a new OB/OS condition is triggered — acting like "fresh anchors" at key market turning points.

---

⚙️ Key Features

🔁 Auto or Manual RSI Thresholds

→ Automatically determines dynamic RSI OB/OS levels based on past peaks and troughs, or lets you set fixed levels.

🧠 Master Symbol Control

→ Use the RSI of a separate asset (like BTCUSDT, ETHUSDT, SOLUSDT, BNBUSDT, SUPRAUSDT) or indices (like TOTAL, TOTAL2, BFR) to control resets — ideal for tracking how BTC/major coins impacts altcoins/others.

🔍 Trend-Filtering Signal Logic

→ Signals are filtered for less noise and are triggered when:

- Both AVWAPs are rising (bullish) or falling (bearish)

- Price action confirms the structure

🎯 Visual Markers & Alerts

→ "💥" for bullish signals and "🔥" for bearish ones. Alerts included for automation or push notifications.

---

🎯 How to Use It

1. Add the indicator to your chart.

2. Choose whether to use RSI from the current symbol or a master symbol (e.g., BTC).

3. Select auto-adjusted or manual OB/OS levels.

4. Watch for:

- AVWAP(s) making a significant change (at this point it's one of the AVWAPs resetting)

- Check if price flip it upwards or downwards

- If price goes above both AVWAPs thats a likely bullish trend

- If price can't go above both AVWAPs up and fall bellow both that's a likely bearish trend

- Price retesting upper AVWAP and bounce

- likely bullish continuation

- Price retesting lower AVWAP and dip

- likely bearish continuation

- Signal icons on chart ("💥 - Bullish" or "🔥- Bearish")

Best suited for:

• Swing traders

• Momentum traders

• Traders timing altcoin entries using BTC/Major asset's RSI

---

🔔 Signal Explanation

💥 Bullish Signal =

• Both AVWAPs rising

• Higher lows in price structure

• Bullish candle close

• Triggered from overbought RSI reset

🔥 Bearish Signal =

• Both AVWAPs falling

• Lower highs in price structure

• Bearish candle close

• Triggered from oversold RSI reset

Signals reset by opposite signals to prevent noise or overfitting.

---

⚠️ Tips & Notes

• Use AVWAPs as dynamic support/resistance, even without signal triggers

• Pair with volume or divergence tools for stronger confirmation

---

🧩 Credits & Philosophy

This tool is built with a simple philosophy:

"Anchor your trades to meaningful moments in price — not arbitrary time."

The dual AVWAP concept helps you see how price reacts after momentum peaks, giving you a cleaner bias and more precise trade setups.

---

Cari skrip untuk "entry"

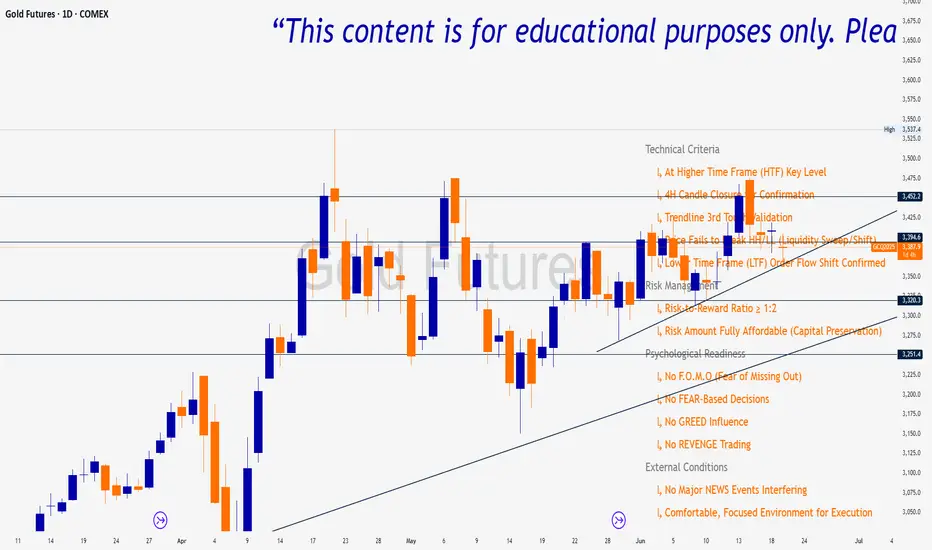

Trade Insight Entry Check List📌 Trade Insight™ Entry Checklist Indicator

This indicator is designed for Smart Money Concepts (SMC) and Price Action traders who prioritize precision, patience, and psychological discipline.

It helps you validate your trade setup across four essential categories before execution:

🔍 Technical Criteria

✅ Higher Time Frame (HTF) Key Level respected

✅ 4H Candle Closure Confirmation

✅ Trendline 3rd Touch Validation

✅ Liquidity Sweep or Shift (price fails to break HH/LL)

✅ Lower Time Frame (LTF) Order Flow Shift Confirmed

💰 Risk Management

✅ Risk-to-Reward Ratio ≥ 1:2

✅ Risk Amount Fully Affordable (Capital Preservation mindset)

🧠 Psychological Readiness

✅ No F.O.M.O (Fear of Missing Out)

✅ No FEAR-based decisions

✅ No GREED influence

✅ No REVENGE trading

NSE Index Strategy with Entry/Exit MarkersExplanation of the Code

Trend Filter (200 SMA):

The line trendSMA = ta.sma(close, smaPeriod) calculates the 200‑period simple moving average. By trading only when the current price is above this SMA (inUptrend = close > trendSMA), we aim to trade in the direction of the dominant trend.

RSI Entry Signal:

The RSI is calculated with rsiValue = ta.rsi(close, rsiPeriod). The script checks for an RSI crossover above the oversold threshold using ta.crossover(rsiValue, rsiOversold). This helps capture a potential reversal from a minor pullback in an uptrend.

ATR-Based Exits:

ATR is computed by atrValue = ta.atr(atrPeriod) and is used to set the stop loss and take profit levels:

Stop Loss: stopLossPrice = close - atrMultiplier * atrValue

Take Profit: takeProfitPrice = close + atrMultiplier * atrValue

This dynamic approach allows the exit levels to adjust according to the current market volatility.

Risk and Money Management:

The strategy uses a fixed percentage of equity (10% by default) for each trade. The built‑in commission parameter helps simulate real-world trading costs.

ZIP Entry Strategy( Using 50 SMA and 100 SMA)Description:

This strategy uses only two simple moving averages, specifically the 50 SMA and the 100 SMA.

Simple moving average : A simple moving average (SMA) calculates the average of a selected range of prices, usually closing prices, by the number of periods in that range.

Here's how it works:

Background color:

The chart background is colored green when the price is above the 100 SMA.

The chart background turns red when the price is below the 100 SMA.

The greenback ground suggest the bullish momentum and the red background suggests the bearish momentum.

We can use this long term trend to take the trades in alignment with the trend to increase our odds.

We will use the 50 SMA to identify the spots when a new trend is starting. When the price crosses above the 50 SMA while the background is green, the candle/bar color changes to white indicating a new trend beginning.

Conversely, when the price crosses below the 50 SMA while the background is red, the candle/bar color also changes to white indicating a new trend beginning.

The occurrence of white candles indicates the start of a potential new trend in alignment with the long term trend.

However, it's essential to remember that like any trading strategy, this one is not perfect. For more reliable results, it's advisable to combine it with a consideration of the overall price structure to minimize false entry signals.

Originality and usefulness

Even though it makes use of two moving averages, we don't use the moving average crossover. The moving average crossovers are either lagging or provide too many false signals. We have tried to address these issue with this strategy. While maintaining the long-term trend and ignoring false signals, it gives out signals early.

You can choose the moving average that best suits your needs by changing these moving averages to a different moving average . The 50 SMA and 100 SMA appeared to be giving the better signals in my experience.

I dont use any other indicators but i would like to check the price structure to make sure its moving along with the 50 SMA. Sometimes the choppy markets might give false signals.

Its okay to see multiple white candles as long as the price structure holds.

I have highlighted the white candles in the above chart. The color of the candle is always the same so the background decides whether its bearish or bullish cross

VWOP: Volume Weighted & Oscillated PriceWhile playing around with the standard "ta.vwap" I wondered why there was no length input, so I did some research on what the underlying calculation actually is, and did my best to augment it so as to allow for a variable length based on an oscillator value.

Normal VWAP = (Number of Shares Bought x Typical Price) / Total Volume

In my VWOP Calculation, typical price is replaced by selected moving average type or "matype" and then multiplied by the volume.

Then a total value is calculated using math.sum with a length value that changes according to a selected oscillator's value. The total is then divided by

the sum of just volume using the same oscillating length value. Result is then passed through the selected"matype" once more to give the final result.

Indicator designed for use as a entry/exit indicator in conjunction with more traditional moving averages and/or signal filters. Useful for taking volume + an oscillator into account along with price, instead of just the price as with a simple moving average.

OTE optimal trade entry (ICT); visible chart only: Dynamic-simple tool based on ICT free YouTube material of many years.

-Highlights a box showing Optimal Trade Entry (OTE): 61.8% - 78.6% retracement

-Auto shifts depending on Bull or Bear move on chart.

--If visible chart is Bullish (low then high): shows OTE box 61.8-78.6% retracement down from the high

--If visible chart is Bearish (high then low): shows OTE box 61.8-78.6% retracement up from the low

-Thanks the use of PineCoders Visible Chart Library, and some of the example code there

BB-RSI-ADX Entry PointsThis is a combination of indicators used to find oversold and overbought entry points for possible reversion.

A Green arrow will appear when all condition are met for an ENTER LONG position.

A Red arow will appear when all condition are met for an ENTER SHORT position.

You can modify all of these condition parameters from the indicator's settings.

How does the indicator work

The signals are using Bollinger Bands , BB %B , RSI and ADX indicators to try and find points of reversal

Enter LONG Conditions

Current candle low is below BB lower band.

The BB %B is more than 0.

RSI > 30

ADX > 25

Enter SHORT Conditions

Current candle high is above BB upper band.

The BB %B is less than 1.

RSI < 70

ADX > 25

Those are the default settings that seem to work for me but you can customize all of these from the indicator settings.

I find this strategy to best work on a 3 minute timeframe

Note: The bb %B is calculated for stDev - 1. This will help you see a change happening faster.

Stochastic RVIBased on the Stochastic RSI but uses RVI (Relative Volatility Index) as source. Another great tool for finding market lows and entry points. This oscillator is also good for finding accurate diversions.

Buy and Hold entry finder StrategyHello everyone!

I proudly present the backtest Strategy Script for my "Buy and Hold entry finder" Script.

It basically shows you the outcome, if you would use my indicator in the past.

The buy signals are limited to 1 order per month.

Order Size: Allows you to choose, how much money you want to invest per month. (Please consider, it will only invest an x amount per Order, but it will not stack the amount you did not invest in an previous month ) (Example in my indicator)

Pyramiding: Just regulates, how often you can open an position.

Commission: Here you can set how much it will cost to open an position at your broker.

I coded a feature that allows you to set a Start Date and an End Date for your backtest. In the end of the backtest the script closes all positions.

If you got any question, feel free to ask in the comments or send me a message.

Sincerely, RS Titan.

Reflex - A new Ehlers indicatorSource: Stocks and Commodities V38

Hooray! A new John Ehlers indicator!

John claims this indicator is lag-less and uses the SPY on the Daily as an example.

He states that drawing a line from peak to peak (or trough to trough) will correspond perfectly with the Asset.

I have to say I agree! There is typically one bar of lag or no lag at all!

I believe this indicator can be used for either entries or exits, but not both.

Entry

1. Entering Long positions at the pivot low points (Stocks and ETFs)

2. Entering Long when the Reflex crosses above the zero lines (Stocks, ETFs, Commodities)

Exit

1. Exiting Long positions at a new pivot high point (Stocks and ETFs)

2. Exiting Long when the Reflex crosses below the zero lines (Stocks, ETFs, Commodities)

In this example, I place a Long order on the SPY every time the Reflex crosses above the zero level and exit when it crosses below or pops my stop loss, set at 1.5 * Daily ATR.

4/6 Wins

+10.76%

For me, that's good enough to create a strategy and backtest on several Indices and ETFs, which is what I have a hunch this will work on.

I think there is a lot of promise from a single Indicator!

Let me know in the comment section if you're able to use this in a strategy.

FauxLife EFIModification to Elder's Force Index (EFI)

Ability to change calculation from standard EMA to your choice of SMA, EMA, WMA, or HMA. Very interesting results!

Adjust lookback from standard/suggested 13 candlesticks

Added a color indication to positive or negative force reading

Added background color tint for an easier read on dashboard setups

Suggested pair with my On Balance Volume with Cross to use as a filter & entry/exit setup. Enter or exit trades when the two indicators switch at the same time or within 1-2 candlesticks of each other.

Moving average system which waits for a better entryWait for a better entry:

A simple way to improve the relevant conditions is to wait for a better price than the system signal. One obvious problem is that when prices give a new signal and move on, you don't have a chance to enter the market at a better price. Statistically, a lot of small improvements may offset the chance that the deal was completely missed. In order to avoid missing the worst case of maximum profit, if there is no trading opportunity within 5 days, we can enter into the market at the closing and if there is no opportunity, the deal will end on day 5.

IMPULSE_2PSAR_ST_CMGEmasCurrently under Development.

Designed to easily get the trend using both SuperTrend and CM Guppy Emas, and using 2 PSARs for entry and trend change alert.

intended to trade scalping and options

CryptoJJ - SSL indicatorThe SSL indicator with colour change. Tool for spotting trends and finding good entry points. I recommend using it for higher timeframes, from 4h to 1D.

Play with the settings, you can change the moving avarage type, its length, if you prefer having the default

bar colours in your chart, disable the colouring function in the script.

Good luck crypto traders!

CryptoJJ

SOLARIZED PRICE ENTRY P/LYou can enter in a date, time and quantity of entry and track a P/L on the trade.

LINEdicator - Trendanalysis toolThis indicator creates an trend channel based on an EMA/SMA combo and a Parabolc SAR indicator.

Watch for the peaks and the size of the red/green channel for possible trend change.

Can also be used as an Entry/Exit/Stop-Loss setting tool.

Exit Strategy is important than Entry Strategy!Exit Strategy is important than Entry Strategy!

Simple strategy get large profit!

RSI-MTF-Histo-EntryThis indicator gives a histogram of RSI in relation to an ema of the RSI.

The histogram is then smoothed to reduce false signals.

The actualiteit RSI line with overbought/overvols signals can be added or omitted as preferred.

The background can be color coded if the RSI is above or below 50.

Version 2. Added support for MTF. Longer timesframes (1h-3h) tend to give better entry results.

As an example the indicator was added two times, one for the current timeframe and one for a longer timeframe.

T3 Entry and ExitI made this indicator to give clear entry and exit signals plus give signals when I should add onto my trades with no repainting!! The bottom indicator is set to 34 (the default settings). This gives me my entries and exits as shown by the green and red arrow. I use a 14 period setting for my signals to add onto my trade. If I am in a long trade as shown in the chart above and the 14 period T3EE has a fast line cross under the slow line and then a cross back over and I have not had my signal to close trade yet on the 34 period T3EE I will add to my long position. I cut the size of they order in half with each addition to my position. So if I entered with 2 lots I would add 1 lot with my first signal to add (shown by orange arrow) and then .5 lots with the second signal to add to my position and so on until it is time to close the position. If you day trade avoid entering positions between 4pm est and 9pm est. and the larger the ranges and the more trendy the market the better. Good Luck!!!

If you have any questions let me know :)

Price Action + Support/Resistance with LabelsEntry Conditions:

Long Entry (BUY): Based on the bullish engulfing pattern and price being above the resistance level.

Short Entry (SELL): For demonstration, the short entry condition is set as price being below the support level and a bullish candle in the previous bar. You can modify this logic for your own use case.

Stop Loss and Take Profit:

Stoploss is plotted at the calculated stop loss level.

Target is plotted at the calculated take profit level.

Labels:

For long trades, labels are added with "BUY", "STOPLOSS", and "TARGET".

For short trades (if enabled), labels are added with "SELL", "STOPLOSS", and "TARGET".

Labels are placed using label.new at specific locations on the chart (above or below bars).

Alert Conditions:

Alerts are created for both long and short entry signals so you can get notified when the entry conditions are met.

How it works:

BUY label will appear below the bar when a long entry condition is met.

SELL label will appear above the bar when a short entry condition is met.

STOPLOSS and TARGET labels will appear at their respective levels when an entry signal is triggered.

The labels will appear on the chart to give you a clear visual cue of the entry, stop loss, and take profit levels.

How to Use:

Copy the script into your Pine Editor on TradingView and apply it to your chart.

Observe the labels that show up on the chart:

"BUY" will appear below the bar when long conditions are met.

"SELL" will appear above the bar when short conditions are met (if using short logic).

"STOPLOSS" will be plotted at the stop loss level.

"TARGET" will be plotted at the take profit level.

Optional Customization:

You can modify the short entry condition based on your preferred method.

You can adjust the length for the support/resistance calculation, the stopLossRR, and other parameters to fine-tune the strategy for Nifty 50 or any other asset.

Let me know if you have any further questions or need additional modifications!

MACD + RSI + EMA + BB + ATR Day Trading StrategyEntry Conditions and Signals

The strategy implements a multi-layered filtering approach to entry conditions, requiring alignment across technical indicators, timeframes, and market conditions .

Long Entry Requirements

Trend Filter: Fast EMA (9) must be above Slow EMA (21), price must be above Fast EMA, and higher timeframe must confirm uptrend

MACD Signal: MACD line crosses above signal line, indicating increasing bullish momentum

RSI Condition: RSI below 70 (not overbought) but above 40 (showing momentum)

Volume & Volatility: Current volume exceeds 1.2x 20-period average and ATR shows sufficient market movement

Time Filter: Trading occurs during optimal hours (9:30-11:30 AM ET) when market volatility is typically highest

Exit Strategies

The strategy employs multiple exit mechanisms to adapt to changing market conditions and protect profits :

Stop Loss Management

Initial Stop: Placed at 2.0x ATR from entry price, adapting to current market volatility

Trailing Stop: 1.5x ATR trailing stop that moves up (for longs) or down (for shorts) as price moves favorably

Time-Based Exits: All positions closed by end of trading day (4:00 PM ET) to avoid overnight risk

Best Practices for Implementation

Settings

Chart Setup: 5-minute timeframe for execution with 15-minute chart for trend confirmation

Session Times: Focus on 9:30-11:30 AM ET trading for highest volatility and opportunity

Perfect OrderEntry Point

How to Entry

Perfect Order Entry

SMA5,13,21 & EMA75,90,200

Please enjoy your entry