COIN/BTC Volume-Weighted DivergenceThe COIN/BTC Volume-Weighted Divergence indicator identifies buy and sell signals by analyzing deviations between Coinbase and Bitcoin prices relative to their respective VWAPs (Volume-Weighted Average Price). This method isolates points of potential trend reversals, overextensions, or relative mispricing based on volume-adjusted price benchmarks.

The indicator leverages Coinbase’s high beta relative to Bitcoin in bull markets. A buy signal occurs when Coinbase is below VWAP (indicating undervaluation) while Bitcoin is above VWAP (signaling strong broader momentum). A sell signal is generated when Coinbase trades above VWAP (indicating overvaluation) while Bitcoin moves below VWAP (indicating weakening momentum).

This divergence logic enables traders to identify misalignment between Bitcoin-driven market trends and Coinbase’s price behavior. The indicator effectively identifies undervalued entry points and signals exits before speculative extensions are correct. It provides a systematic approach to trading during trending conditions, aligning decisions with volume-weighted price dynamics and inter-asset relationships.

How It Works

1. VWAP:

“fair value” benchmark combining price and volume.

• Above VWAP: Bullish momentum.

• Below VWAP: Bearish momentum.

2. Divergence:

• Coinbase Divergence: close - coin_vwap (distance from COIN’s VWAP).

• Bitcoin Divergence: btc_price - btc_vwap (distance from BTC’s VWAP).

3. Signals:

• Buy: Coinbase is below VWAP (potentially oversold), and Bitcoin is above VWAP (broader bullish trend).

• Sell: Coinbase is above VWAP (potentially overbought), and Bitcoin is below VWAP (broader bearish trend).

4. Visualization:

• Green triangle: Buy signal.

• Red triangle: Sell signal.

Strengths

• Combines price and volume for reliable insights.

• Highlights potential trend reversals or overextensions.

• Exploits correlations between Coinbase and Bitcoin.

Limitations

• Struggles in sideways markets.

• Sensitive to volume spikes, which may distort VWAP.

• Ineffective in strong trends where divergence persists.

Improvements

1. Z-Scores: Use statistical thresholds (e.g., ±2 std dev) for stronger signals.

2. Volume Filter: Generate signals only during high-volume periods.

3. Momentum Confirmation: Combine with RSI or MACD for better reliability.

4. Multi-Timeframe VWAP: Use intraday, daily, and weekly VWAPs for deeper analysis.

Complementary Tools

• Momentum Indicators: RSI, MACD for trend validation.

• Volume-Based Metrics: OBV, cumulative delta volume.

• Support/Resistance Levels: Enhance reversal accuracy.

Cari skrip untuk "deep股票代码"

Salience Theory Crypto Returns (AiBitcoinTrend)The Salience Theory Crypto Returns Indicator is a sophisticated tool rooted in behavioral finance, designed to identify trading opportunities in the cryptocurrency market. Based on research by Bordalo et al. (2012) and extended by Cai and Zhao (2022), it leverages salience theory—the tendency of investors, particularly retail traders, to overemphasize standout returns.

In the crypto market, dominated by sentiment-driven retail investors, salience effects are amplified. Attention disproportionately focused on certain cryptocurrencies often leads to temporary price surges, followed by reversals as the market stabilizes. This indicator quantifies these effects using a relative return salience measure, enabling traders to capitalize on price reversals and trends, offering a clear edge in navigating the volatile crypto landscape.

👽 How the Indicator Works

Salience Measure Calculation :

👾 The indicator calculates how much each cryptocurrency's return deviates from the average return of all cryptos over the selected ranking period (e.g., 21 days).

👾 This deviation is the salience measure.

👾 The more a return stands out (salient outcome), the higher the salience measure.

Ranking:

👾 Cryptos are ranked in ascending order based on their salience measures.

👾 Rank 1 (lowest salience) means the crypto is closer to the average return and is more predictable.

👾 Higher ranks indicate greater deviation and unpredictability.

Color Interpretation:

👾 Green: Low salience (closer to average) – Trending or Predictable.

👾 Red/Orange: High salience (far from average) – Overpriced/Unpredictable.

👾 Text Gradient (Teal to Light Blue): Helps visualize potential opportunities for mean reversion trades (i.e., cryptos that may return to equilibrium).

👽 Core Features

Salience Measure Calculation

The indicator calculates the salience measure for each cryptocurrency by evaluating how much its return deviates from the average market return over a user-defined ranking period. This measure helps identify which assets are trending predictably and which are likely to experience a reversal.

Dynamic Ranking System

Cryptocurrencies are dynamically ranked based on their salience measures. The ranking helps differentiate between:

Low Salience Cryptos (Green): These are trending or predictable assets.

High Salience Cryptos (Red): These are overpriced or deviating significantly from the average, signaling potential reversals.

👽 Deep Dive into the Core Mathematics

Salience Theory in Action

Salience theory explains how investors, particularly in the crypto market, tend to prefer assets with standout returns (salient outcomes). This behavior often leads to overpricing of assets with high positive returns and underpricing of those with standout negative returns. The indicator captures these deviations to anticipate mean reversions or trend continuations.

Salience Measure Calculation

// Calculate the average return

avgReturn = array.avg(returns)

// Calculate salience measure for each symbol

salienceMeasures = array.new_float()

for i = 0 to array.size(returns) - 1

ret = array.get(returns, i)

salienceMeasure = math.abs(ret - avgReturn) / (math.abs(ret) + math.abs(avgReturn) + 0.1)

array.push(salienceMeasures, salienceMeasure)

Dynamic Ranking

Cryptos are ranked in ascending order based on their salience measures:

Low Ranks: Cryptos with low salience (predictable, trending).

High Ranks: Cryptos with high salience (unpredictable, likely to revert).

👽 Applications

👾 Trend Identification

Identify cryptocurrencies that are currently trending with low salience measures (green). These assets are likely to continue their current direction, making them good candidates for trend-following strategies.

👾 Mean Reversion Trading

Cryptos with high salience measures (red to light blue) may be poised for a mean reversion. These assets are likely to correct back towards the market average.

👾 Reversal Signals

Anticipate potential reversals by focusing on high-ranked cryptos (red). These assets exhibit significant deviation and are prone to price corrections.

👽 Why It Works in Crypto

The cryptocurrency market is dominated by retail investors prone to sentiment-driven behavior. This leads to exaggerated price movements, making the salience effect a powerful predictor of reversals.

👽 Indicator Settings

👾 Ranking Period : Number of bars used to calculate the average return and salience measure.

Higher Values: Smooth out short-term volatility.

Lower Values: Make the ranking more sensitive to recent price movements.

👾 Number of Quantiles : Divide ranked assets into quantile groups (e.g., quintiles).

Higher Values: More detailed segmentation (deciles, percentiles).

Lower Values: Broader grouping (quintiles, quartiles).

👾 Portfolio Percentage : Percentage of the portfolio allocated to each selected asset.

Enter a percentage (e.g., 20 for 20%), automatically converted to a decimal (e.g., 0.20).

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Dollar Volume DivergenceOverview

The Dollar Volume Profile and Divergence Indicator is a comprehensive tool designed to analyze both standard volume and dollar volume activity in the market. It visualizes dollar volume (calculated as close * volume) and highlights divergences between dollar volume and standard volume, providing insights into underlying market dynamics that aren't immediately visible with traditional volume analysis.

Key Features

Dollar Volume Profile:

Plots dollar volume as a histogram.

Highlights high-dollar volume bars in green (indicating significant trading activity).

Includes an optional average dollar volume line to show trends over time.

Volume-Divergence Analysis:

Calculates the difference (divergence) between dollar volume and standard volume.

Displays positive divergence (dollar volume > standard volume) in green and negative divergence (dollar volume < standard volume) in red.

Supports both histogram and boolean point visualization for divergence, offering flexibility in how the data is displayed.

Customizable Visualization:

Users can toggle between a Histogram or Boolean Points for divergence visualization.

Option to enable or disable the dollar volume profile and its average line.

Adjustable length parameter to fine-tune sensitivity for averages and divergences.

Use Cases

Volume Confirmation: Analyze whether dollar volume aligns with standard volume to confirm strong price movements.

Divergence Detection: Identify areas where dollar volume and standard volume deviate, which may signal potential reversals or exhaustion in a trend.

Market Strength Analysis: Assess the intensity of trading activity at specific price levels to determine key areas of interest.

How It Works

Dollar Volume Calculation:

Dollar volume is derived by multiplying the close price by the volume for each bar.

A moving average of dollar volume is used to determine relative activity levels.

Divergence Calculation:

The script calculates the difference between dollar volume and standard volume.

Positive values indicate that dollar volume exceeds standard volume, suggesting institutional or larger-scale trades.

Negative values highlight areas of lower dollar volume compared to standard volume.

Visualization:

The Dollar Volume Profile is displayed as a histogram, with high-dollar volume bars highlighted.

Divergences are overlaid as either a histogram or triangle markers, depending on user preference.

Average lines (optional) provide smoother trends for both dollar volume and divergence.

Customization Options

Length: Adjusts the period for moving average calculations.

Plot Style: Choose between Histogram or Boolean Points for divergence visualization.

Toggle Visibility: Enable or disable the Dollar Volume Profile and its average line for a cleaner chart.

Why Use This Indicator?

This indicator bridges the gap between traditional volume analysis and dollar volume analysis, offering deeper insights into market behavior. By combining these metrics, traders can detect nuanced patterns, validate trends, and identify divergences that may signal market turning points or continuation.

Best Practices

Use this indicator in conjunction with price action and other technical indicators for confirmation.

Look for divergences in high-dollar volume areas to detect potential trend reversals.

Analyze the interaction between the dollar volume profile and divergence histogram for a comprehensive view of market activity.

Important Notice:

Trading financial markets involves significant risk and may not be suitable for all investors. The use of technical indicators like this one does not guarantee profitable results. This indicator should not be used as a standalone analysis tool. It is essential to combine it with other forms of analysis, such as fundamental analysis, risk management strategies, and awareness of current market conditions. Always conduct thorough research or consult with a qualified financial advisor before making trading decisions. Past performance is not indicative of future results.

Disclaimer:

Trading financial instruments involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. This indicator is provided for informational and educational purposes only and should not be considered investment advice. Always conduct your own research and consult with a licensed financial professional before making any trading decisions.

Note: The effectiveness of any technical indicator can vary based on market conditions and individual trading styles. It's crucial to test indicators thoroughly using historical data and possibly paper trading before applying them in live trading scenarios.

Rolling VWAP with Optional Kalman FilterThis script provides an advanced and customizable Rolling VWAP (Volume-Weighted Average Price) indicator, designed for traders who want to refine their trend analysis and improve decision-making. With a unique option to apply a Kalman Filter, you can smooth out VWAP values to reduce noise in volatile markets, making it easier to identify actionable trends.

Key Features:

Dynamic Rolling VWAP:

Choose the rolling window size (number of bars) to match your trading style, whether you’re an intraday scalper or a swing trader.

Kalman Filter Toggle:

Enable the Kalman filter to smooth VWAP values and eliminate market noise.

Adjustable Kalman Gain to control the level of smoothing, making it suitable for both fast and slow markets.

Price Source Flexibility:

Use the Typical Price ((H+L+C)/3) or the Close Price as the basis for VWAP calculation.

Visual Enhancements:

Background shading highlights whether the price is above (bullish) or below (bearish) the VWAP, helping traders make quick visual assessments.

A legend dynamically updates the current VWAP value.

Dual View Option:

Compare the raw Rolling VWAP and the Kalman-filtered VWAP when the filter is enabled, giving you deeper insight into market trends.

Use Cases:

Intraday Traders: Identify key price levels for re-entry or exits using a short rolling window and responsive filtering.

Swing Traders: Analyze broader trends with a longer rolling window and smoother VWAP output.

Volatile Markets: Use the Kalman filter to reduce noise and avoid false signals during high market volatility.

How to Use:

Adjust the Rolling Window to set the number of bars for VWAP calculation.

Toggle Kalman Filter on/off depending on your preference for raw or smoothed VWAP values.

Fine-tune the Kalman Gain for the desired level of smoothing.

Use the shading to quickly assess whether the price is trading above or below the VWAP for potential entry/exit signals.

MA Multi-Timeframe [ChartPrime]The MA Multi-Timeframe indicator is designed to provide multi-timeframe moving averages (MAs) for better trend analysis across different periods. This tool allows traders to monitor up to four different MAs on a single chart, each coming from a selectable timeframe and type (SMA, EMA, SMMA, WMA, VWMA). The indicator helps traders gauge both short-term and long-term price trends, allowing for a clearer understanding of market dynamics.

⯁ KEY FEATURES AND HOW TO USE

⯌ Multi-Timeframe Moving Averages :

The indicator allows traders to select up to four MAs, each from different timeframes. These timeframes can be set in the input settings (e.g., Daily, Weekly, Monthly), and each moving average can be displayed with its corresponding timeframe label directly on the chart.

Example of different timeframes for MAs:

⯌ Moving Average Types :

Users can choose from several types of moving averages, including SMA, EMA, SMMA, WMA, and VWMA, making the indicator adaptable to different strategies and market conditions. This flexibility allows traders to tailor the MAs to their preference.

Example of different types of MAs:

⯌ Dashboard Display :

The indicator includes a built-in dashboard that shows each MA, its timeframe, and whether the price is currently above or below that MA. This dashboard provides a quick overview of the trend across different timeframes, allowing traders to determine whether the overall trend is up or down.

Example of trend overview via the dashboard:

⯌ Polyline Representation :

Each MA is plotted using polylines to avoid plot functions and create a curves across up to 4000 bars back, ensuring that historical data is visualized clearly for a deeper analysis of how the price interacts with these levels over time.

if barstate.islast

for i = 0 to 4000

cp.push(chart.point.from_index(bar_index , ma ))

polyline.delete(polyline.new(cp, curved = false, line_color = color, line_style = style) )

Example of polylines for moving averages:

⯌ Customization Options :

Traders can customize the length of the MAs for all timeframes using a single input. The color, style (solid, dashed, dotted) of each moving average are also customizable, giving users full control over the visual appearance of the indicator on their chart.

Example of custom MA styles:

⯁ USER INPUTS

MA Type : Select the type of moving average for each timeframe (SMA, EMA, SMMA, WMA, VWMA).

Timeframe : Choose the timeframe for each moving average (e.g., Daily, Weekly, Monthly).

MA Length : Set the length for the moving averages, which will be applied to all four MAs.

Line Style : Customize the style of each MA line (solid, dashed, or dotted).

Colors : Set the color for each MA for better visual distinction.

⯁ CONCLUSION

The MA Multi-Timeframe indicator is a versatile and powerful tool for traders looking to monitor price trends across multiple timeframes with different types of moving averages. The dashboard simplifies trend identification, while the customizable options make it easy to adapt to individual trading strategies. Whether you're analyzing short-term price movements or long-term trends, this indicator offers a comprehensive solution for tracking market direction.

Advanced MA and MACD PercentageIntroduction

The "Advanced MA and MACD Percentage" indicator is a powerful and innovative tool designed to help traders analyze financial markets with ease and precision. This indicator combines Moving Averages (MA) with the MACD indicator to assess the market’s overall trend and calculate the percentage of buy and sell signals based on current data.

Features

Multi-Timeframe Analysis:

Allows selecting your preferred timeframe for trend analysis, such as minute, hourly, daily, or weekly charts.

Support for Multiple Moving Average Types:

Offers the option to use either Simple Moving Average (SMA) or Exponential Moving Average (EMA), based on user preference.

Comprehensive MACD Analysis:

Analyzes the relationship between multiple moving averages (e.g., 20/50, 50/100) using MACD to provide deeper insights into market dynamics.

Calculation of Buy and Sell Percentages:

Computes the percentage of indicators signaling buy or sell conditions, providing a clear summary to assist trading decisions.

Intuitive Visual Interface:

Displays buy and sell percentages as two visible lines (green and red) on the chart.

Includes reference lines to clarify the range of percentages (100% to 0%).

How It Works

Moving Averages Calculation:

Calculates moving averages (20, 50, 100, 150, and 200) for the selected timeframe.

MACD Pair Analysis:

Computes the MACD to compare the performance between various moving average pairs, such as (20/50) and (50/100).

Identifying Buy and Sell Signals:

Counts the number of indicators signaling buy (price above MAs or positive MACD histogram).

Converts the count into percentages for both buy and sell signals.

Visual Representation:

Plots buy and sell percentages as clear lines (green for buy, red for sell).

Adds reference lines (100% and 0%) for easier interpretation.

How to Use the Indicator?

Settings:

Choose the type of moving average (SMA or EMA).

Select the timeframe that suits your strategy (e.g., 15 minutes, 1 hour, or daily).

Reading the Results:

If the buy percentage (green line) is above 50%, the overall trend is bullish (buy).

If the sell percentage (red line) is above 50%, the overall trend is bearish (sell).

Integrating Into Your Strategy:

Combine it with other indicators to confirm entry and exit signals.

Use it to quickly understand the market’s overall trend without needing complex manual analysis.

Benefits of the Indicator

Simplified Analysis: Provides a straightforward summary of the market's overall trend.

Adaptable to All Timeframes: Works perfectly on all timeframes.

Customizable: Allows users to adjust settings according to their needs.

Important Notes

This indicator does not provide direct buy or sell signals. Instead, it offers a summary of the market’s condition based on a combination of indicators.

It is recommended to use it alongside other technical analysis tools for precise trading signals.

Conclusion

The "Advanced MA and MACD Percentage" indicator is an ideal tool for traders who want to analyze the market using a combination of Moving Averages and MACD. It gives you a comprehensive overview of the overall trend, helping you make informed and quick trading decisions. Try it now and see the difference!

Alternative Price [OmegaTools]The Alternative Price script is a sophisticated and flexible indicator designed to redefine how traders visualize and interpret price data. By offering multiple unique charting modes, robust customization options, and advanced features, this tool provides a comprehensive alternative to traditional price charts. It is particularly useful for identifying market trends, detecting patterns, and simplifying complex data into actionable insights.

This script is highly versatile, allowing users to choose from five distinct charting modes: Candles, Line, Channel, Renko, and Bubbles. Each mode serves a unique purpose and presents price information in an innovative way. When using this script, it is strongly recommended to hide the platform’s default price candles or chart data. Doing so will eliminate redundancy and provide a clearer and more focused view of the alternative price visualization.

The Candles mode offers a traditional candlestick charting style but with added flexibility. Users can choose to enable smoothed opens or smoothed closes, which adjust the way the open and close prices are calculated. When smoothed opens are enabled, the opening price is computed as the average of the actual open price and the closing prices of the previous two bars. This creates a more gradual representation of price transitions, particularly useful in markets prone to sudden spikes or irregularities. Similarly, smoothed closes modify the closing price by averaging it with the previous close, the high-low midpoint, and an exponential moving average of the high-low-close mean. This technique filters out noise, making trends and price momentum easier to identify.

In the Line mode, the script displays a simple line chart that connects the smoothed closing prices. This mode is ideal for traders who prefer minimalism or need to focus on the overall trend without the distraction of individual bar details. The Channel mode builds upon this by plotting additional lines representing the highs and lows of each bar. The resulting visualization resembles a price corridor that helps identify support and resistance zones or price compression areas.

The Renko mode introduces a more advanced and noise-filtering method of visualizing price movements. Renko charts, constructed using the ATR (Average True Range) as a baseline, display blocks that represent a specific price range. The script dynamically calculates the size of these blocks based on ATR, with separate thresholds for upward and downward movements. This makes Renko mode particularly effective for identifying sustained trends while ignoring minor price fluctuations. Additionally, the open and close values of Renko blocks can be smoothed to further refine the visualization.

The Bubbles mode represents price activity using circles or bubbles whose size corresponds to relative volume. This mode provides a quick and intuitive way to assess market participation at different price levels. Larger bubbles indicate higher trading volumes, while smaller bubbles highlight periods of lower activity. This visualization is particularly valuable in understanding the relationship between price movements and market liquidity.

The coloring of candles and other chart elements is a core feature of this script. Users can select between two color modes: Normal and Volume. In Normal mode, bullish candles are displayed in the user-defined bullish color, while bearish candles use the bearish color. Neutral elements, such as midpoints or undecided price movements, are shaded with a neutral color. In Volume mode, the candle colors are dynamically adjusted based on trading volume. A gradient color scale is applied, where the intensity of the bullish or bearish colors reflects the volume for that particular bar. This feature allows traders to visually identify periods of heightened activity and associate them with specific price movements.

Engulfing patterns, a popular technical analysis tool, are automatically detected and marked on the chart when the corresponding setting is enabled. The script identifies long engulfing patterns, where the current bar's range completely encompasses the previous bar’s range and indicates a potential bullish reversal. Similarly, short engulfing patterns are identified where the current bar fully engulfs the previous bar in the opposite direction, suggesting a bearish reversal. These patterns are visually highlighted with circular markers to draw the trader’s attention.

Each feature and mode is highly customizable. The colors for bullish, bearish, and neutral movements can be personalized, and the thresholds for patterns or smoothing can be fine-tuned to match specific trading strategies. The script's ability to toggle between various modes makes it adaptable to different market conditions and analysis preferences.

In summary, the Alternative Price script is a comprehensive tool that redefines the way traders view price charts. By offering multiple visualization modes, customizable features, and advanced detection algorithms, it provides a powerful way to uncover market trends, volume relationships, and significant patterns. The recommendation to hide default chart elements ensures that the focus remains on this innovative tool, enhancing its usability and clarity. This script empowers traders to gain deeper insights into market behavior and make informed trading decisions, all while maintaining a clean and visually appealing chart layout.

Keep in mind that some of the modes of this indicator might not reflect the actual closing price of the underlying asset, before opening a trade, check carefully the actual price!

Hybrid Adaptive Double Exponential Smoothing🙏🏻 This is HADES (Hybrid Adaptive Double Exponential Smoothing) : fully data-driven & adaptive exponential smoothing method, that gains all the necessary info directly from data in the most natural way and needs no subjective parameters & no optimizations. It gets applied to data itself -> to fit residuals & one-point forecast errors, all at O(1) algo complexity. I designed it for streaming high-frequency univariate time series data, such as medical sensor readings, orderbook data, tick charts, requests generated by a backend, etc.

The HADES method is:

fit & forecast = a + b * (1 / alpha + T - 1)

T = 0 provides in-sample fit for the current datum, and T + n provides forecast for n datapoints.

y = input time series

a = y, if no previous data exists

b = 0, if no previous data exists

otherwise:

a = alpha * y + (1 - alpha) * a

b = alpha * (a - a ) + (1 - alpha) * b

alpha = 1 / sqrt(len * 4)

len = min(ceil(exp(1 / sig)), available data)

sig = sqrt(Absolute net change in y / Sum of absolute changes in y)

For the start datapoint when both numerator and denominator are zeros, we define 0 / 0 = 1

...

The same set of operations gets applied to the data first, then to resulting fit absolute residuals to build prediction interval, and finally to absolute forecasting errors (from one-point ahead forecast) to build forecasting interval:

prediction interval = data fit +- resoduals fit * k

forecasting interval = data opf +- errors fit * k

where k = multiplier regulating intervals width, and opf = one-point forecasts calculated at each time t

...

How-to:

0) Apply to your data where it makes sense, eg. tick data;

1) Use power transform to compensate for multiplicative behavior in case it's there;

2) If you have complete data or only the data you need, like the full history of adjusted close prices: go to the next step; otherwise, guided by your goal & analysis, adjust the 'start index' setting so the calculations will start from this point;

3) Use prediction interval to detect significant deviations from the process core & make decisions according to your strategy;

4) Use one-point forecast for nowcasting;

5) Use forecasting intervals to ~ understand where the next datapoints will emerge, given the data-generating process will stay the same & lack structural breaks.

I advise k = 1 or 1.5 or 4 depending on your goal, but 1 is the most natural one.

...

Why exponential smoothing at all? Why the double one? Why adaptive? Why not Holt's method?

1) It's O(1) algo complexity & recursive nature allows it to be applied in an online fashion to high-frequency streaming data; otherwise, it makes more sense to use other methods;

2) Double exponential smoothing ensures we are taking trends into account; also, in order to model more complex time series patterns such as seasonality, we need detrended data, and this method can be used to do it;

3) The goal of adaptivity is to eliminate the window size question, in cases where it doesn't make sense to use cumulative moving typical value;

4) Holt's method creates a certain interaction between level and trend components, so its results lack symmetry and similarity with other non-recursive methods such as quantile regression or linear regression. Instead, I decided to base my work on the original double exponential smoothing method published by Rob Brown in 1956, here's the original source , it's really hard to find it online. This cool dude is considered the one who've dropped exponential smoothing to open access for the first time🤘🏻

R&D; log & explanations

If you wanna read this, you gotta know, you're taking a great responsability for this long journey, and it gonna be one hell of a trip hehe

Machine learning, apprentissage automatique, машинное обучение, digital signal processing, statistical learning, data mining, deep learning, etc., etc., etc.: all these are just artificial categories created by the local population of this wonderful world, but what really separates entities globally in the Universe is solution complexity / algorithmic complexity.

In order to get the game a lil better, it's gonna be useful to read the HTES script description first. Secondly, let me guide you through the whole R&D; process.

To discover (not to invent) the fundamental universal principle of what exponential smoothing really IS, it required the review of the whole concept, understanding that many things don't add up and don't make much sense in currently available mainstream info, and building it all from the beginning while avoiding these very basic logical & implementation flaws.

Given a complete time t, and yet, always growing time series population that can't be logically separated into subpopulations, the very first question is, 'What amount of data do we need to utilize at time t?'. Two answers: 1 and all. You can't really gain much info from 1 datum, so go for the second answer: we need the whole dataset.

So, given the sequential & incremental nature of time series, the very first and basic thing we can do on the whole dataset is to calculate a cumulative , such as cumulative moving mean or cumulative moving median.

Now we need to extend this logic to exponential smoothing, which doesn't use dataset length info directly, but all cool it can be done via a formula that quantifies the relationship between alpha (smoothing parameter) and length. The popular formulas used in mainstream are:

alpha = 1 / length

alpha = 2 / (length + 1)

The funny part starts when you realize that Cumulative Exponential Moving Averages with these 2 alpha formulas Exactly match Cumulative Moving Average and Cumulative (Linearly) Weighted Moving Average, and the same logic goes on:

alpha = 3 / (length + 1.5) , matches Cumulative Weighted Moving Average with quadratic weights, and

alpha = 4 / (length + 2) , matches Cumulative Weighted Moving Average with cubic weghts, and so on...

It all just cries in your shoulder that we need to discover another, native length->alpha formula that leverages the recursive nature of exponential smoothing, because otherwise, it doesn't make sense to use it at all, since the usual CMA and CMWA can be computed incrementally at O(1) algo complexity just as exponential smoothing.

From now on I will not mention 'cumulative' or 'linearly weighted / weighted' anymore, it's gonna be implied all the time unless stated otherwise.

What we can do is to approach the thing logically and model the response with a little help from synthetic data, a sine wave would suffice. Then we can think of relationships: Based on algo complexity from lower to higher, we have this sequence: exponential smoothing @ O(1) -> parametric statistics (mean) @ O(n) -> non-parametric statistics (50th percentile / median) @ O(n log n). Based on Initial response from slow to fast: mean -> median Based on convergence with the real expected value from slow to fast: mean (infinitely approaches it) -> median (gets it quite fast).

Based on these inputs, we need to discover such a length->alpha formula so the resulting fit will have the slowest initial response out of all 3, and have the slowest convergence with expected value out of all 3. In order to do it, we need to have some non-linear transformer in our formula (like a square root) and a couple of factors to modify the response the way we need. I ended up with this formula to meet all our requirements:

alpha = sqrt(1 / length * 2) / 2

which simplifies to:

alpha = 1 / sqrt(len * 8)

^^ as you can see on the screenshot; where the red line is median, the blue line is the mean, and the purple line is exponential smoothing with the formulas you've just seen, we've met all the requirements.

Now we just have to do the same procedure to discover the length->alpha formula but for double exponential smoothing, which models trends as well, not just level as in single exponential smoothing. For this comparison, we need to use linear regression and quantile regression instead of the mean and median.

Quantile regression requires a non-closed form solution to be solved that you can't really implement in Pine Script, but that's ok, so I made the tests using Python & sklearn:

paste.pics

^^ on this screenshot, you can see the same relationship as on the previous screenshot, but now between the responses of quantile regression & linear regression.

I followed the same logic as before for designing alpha for double exponential smoothing (also considered the initial overshoots, but that's a little detail), and ended up with this formula:

alpha = sqrt(1 / length) / 2

which simplifies to:

alpha = 1 / sqrt(len * 4)

Btw, given the pattern you see in the resulting formulas for single and double exponential smoothing, if you ever want to do triple (not Holt & Winters) exponential smoothing, you'll need len * 2 , and just len * 1 for quadruple exponential smoothing. I hope that based on this sequence, you see the hint that Maybe 4 rounds is enough.

Now since we've dealt with the length->alpha formula, we can deal with the adaptivity part.

Logically, it doesn't make sense to use a slower-than-O(1) method to generate input for an O(1) method, so it must be something universal and minimalistic: something that will help us measure consistency in our data, yet something far away from statistics and close enough to topology.

There's one perfect entity that can help us, this is fractal efficiency. The way I define fractal efficiency can be checked at the very beginning of the post, what matters is that I add a square root to the formula that is not typically added.

As explained in the description of my metric QSFS , one of the reasons for SQRT-transformed values of fractal efficiency applied in moving window mode is because they start to closely resemble normal distribution, yet with support of (0, 1). Data with this interesting property (normally distributed yet with finite support) can be modeled with the beta distribution.

Another reason is, in infinitely expanding window mode, fractal efficiency of every time series that exhibits randomness tends to infinitely approach zero, sqrt-transform kind of partially neutralizes this effect.

Yet another reason is, the square root might better reflect the dimensional inefficiency or degree of fractal complexity, since it could balance the influence of extreme deviations from the net paths.

And finally, fractals exhibit power-law scaling -> measures like length, area, or volume scale in a non-linear way. Adding a square root acknowledges this intrinsic property, while connecting our metric with the nature of fractals.

---

I suspect that, given analogies and connections with other topics in geometry, topology, fractals and most importantly positive test results of the metric, it might be that the sqrt transform is the fundamental part of fractal efficiency that should be applied by default.

Now the last part of the ballet is to convert our fractal efficiency to length value. The part about inverse proportionality is obvious: high fractal efficiency aka high consistency -> lower window size, to utilize only the last data that contain brand new information that seems to be highly reliable since we have consistency in the first place.

The non-obvious part is now we need to neutralize the side effect created by previous sqrt transform: our length values are too low, and exponentiation is the perfect candidate to fix it since translating fractal efficiency into window sizes requires something non-linear to reflect the fractal dynamics. More importantly, using exp() was the last piece that let the metric shine, any other transformations & formulas alike I've tried always had some weird results on certain data.

That exp() in the len formula was the last piece that made it all work both on synthetic and on real data.

^^ a standalone script calculating optimal dynamic window size

Omg, THAT took time to write. Comment and/or text me if you need

...

"Versace Pip-Boy, I'm a young gun coming up with no bankroll" 👻

∞

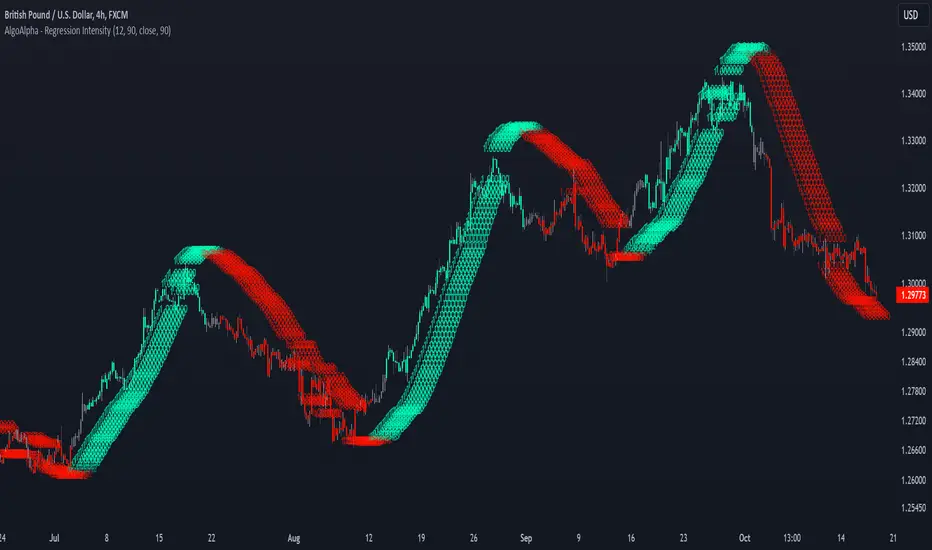

Linear Regression Intensity [AlgoAlpha]Introducing the Linear Regression Intensity indicator by AlgoAlpha, a sophisticated tool designed to measure and visualize the strength of market trends using linear regression analysis. This indicator not only identifies bullish and bearish trends with precision but also quantifies their intensity, providing traders with deeper insights into market dynamics. Whether you’re a novice trader seeking clearer trend signals or an experienced analyst looking for nuanced trend strength indicators, Linear Regression Intensity offers the clarity and detail you need to make informed trading decisions.

Key Features:

📊 Comprehensive Trend Analysis: Utilizes linear regression over customizable periods to assess and quantify trend strength.

🎨 Customizable Appearance: Choose your preferred colors for bullish and bearish trends to align with your trading style.

🔧 Flexible Parameters: Adjust the lookback period, range tolerance, and regression length to tailor the indicator to your specific strategy.

📉 Dynamic Bar Coloring: Instantly visualize trend states with color-coded bars—green for bullish, red for bearish, and gray for neutral.

🏷️ Intensity Labels: Displays dynamic labels that represent the intensity of the current trend, helping you gauge market momentum at a glance.

🔔 Alert Conditions: Set up alerts for strong bullish or bearish trends and trend neutrality to stay ahead of market movements without constant monitoring.

Quick Guide to Using Linear Regression Intensity:

🛠 Add the Indicator: Simply add Linear Regression Intensity to your TradingView chart from your favorites. Customize the settings such as lookback period, range tolerance, and regression length to fit your trading approach.

📈 Market Analysis: Observe the color-coded bars to quickly identify the current trend state. Use the intensity labels to understand the strength behind each trend, allowing for more strategic entry and exit points.

🔔 Set Up Alerts: Enable alerts for when strong bullish or bearish trends are detected or when the trend reaches a neutral zone. This ensures you never miss critical market movements, even when you’re away from the chart.

How It Works:

The Linear Regression Intensity indicator leverages linear regression to calculate the underlying trend of a selected price source over a specified length. By analyzing the consistency of the regression values within a defined lookback period, it determines the trend’s intensity based on a percentage tolerance. The indicator aggregates pairwise comparisons of regression values to assess whether the trend is predominantly upward or downward, assigning a state of bullish, bearish, or neutral accordingly. This state is then visually represented through dynamic bar colors and intensity labels, offering a clear and immediate understanding of market conditions. Additionally, the inclusion of Average True Range (ATR) ensures that the intensity visualization accounts for market volatility, providing a more robust and reliable trend assessment. With customizable settings and alert conditions, Linear Regression Intensity empowers traders to fine-tune their strategies and respond swiftly to evolving market trends.

Elevate your trading strategy with Linear Regression Intensity and gain unparalleled insights into market trends! 🌟📊

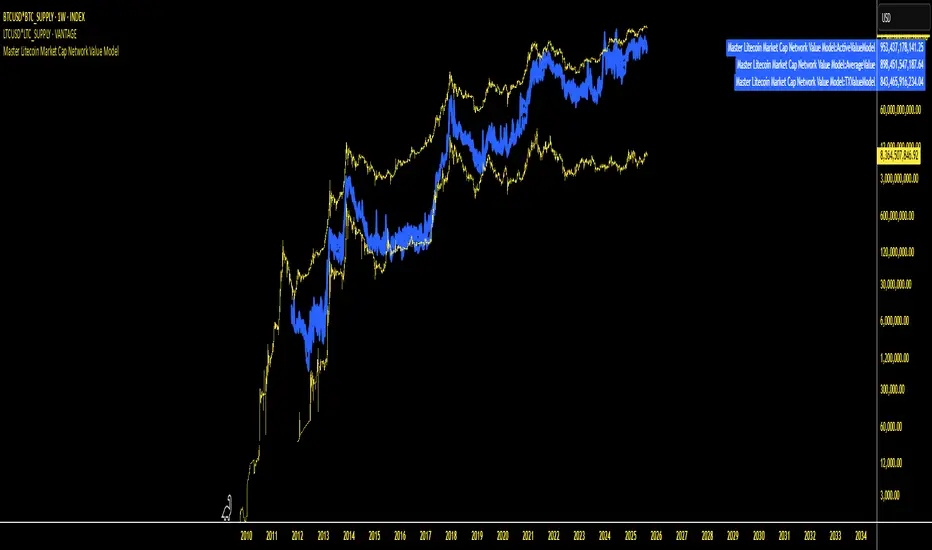

Master Litecoin Market Cap Network Value ModelMaster Litecoin Market Cap Network Value Model

This indicator visualizes Litecoin's network fundamentals compared to Bitcoin, developed by @masterbtcltc. By analyzing various on-chain metrics and market data, this script helps users evaluate Litecoin’s intrinsic value relative to Bitcoin.

Key Features:

Network Metrics:

NewAddressValueModel: Tracks the ratio of new addresses in Litecoin compared to Bitcoin.

TotalAddressValueModel: Compares total addresses across the two networks.

Transaction & Volume Metrics:

TXValueModel: Compares transaction activity.

VolumeValueModel and VolumeUSDValueModel: Analyzes transaction volumes in native units and USD.

Usage & Adoption:

ActiveValueModel: Tracks the ratio of active addresses between Litecoin and Bitcoin.

RetailValueModel: Measures retail adoption strength in the Litecoin network.

Blockchain & Holder Data:

BlockValueModel: Compares block sizes.

NonZeroModel: Evaluates addresses with non-zero balances.

HodlerModel: Compares long-term holders between Litecoin and Bitcoin.

Averaged Insights:

AverageValueModel: Aggregates all metrics for a complete view of network valuation.

Visual Design:

Blue Themed Metrics: Network value models are displayed in a uniform blue color with a line thickness of 4 and 25% transparency for clarity.

Distinct Price Plot: Litecoin’s price is plotted in yellow, with a thin line (width 2) and no transparency, keeping it visually separate.

Use Cases:

Ideal for traders, investors, and enthusiasts aiming to:

Identify Litecoin’s market trends.

Detect periods of undervaluation or overvaluation.

Gain deeper insights into Litecoin’s network fundamentals.

Important Instruction: To ensure accurate results, plot this indicator on VANTAGE:LTCUSD * GLASSNODE:LTC_SUPPLY. This ensures alignment with the data sources and guarantees the script performs as intended.

Feel free to explore, use, and share this open-source script to better understand Litecoin’s value potential!

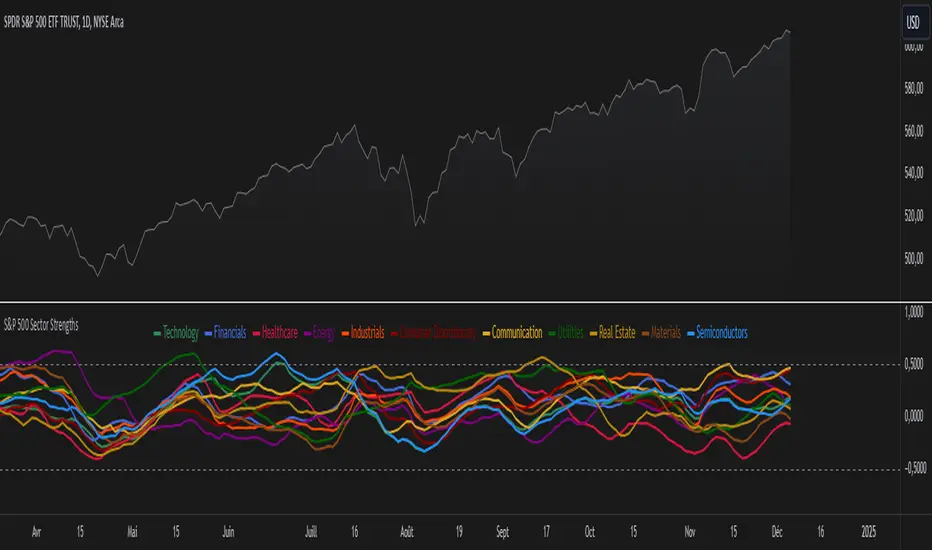

S&P 500 Sector StrengthsThe "S&P 500 Sector Strengths" indicator is a sophisticated tool designed to provide traders and investors with a comprehensive view of the relative performance of various sectors within the S&P 500 index. This indicator utilizes the True Strength Index (TSI) to measure and compare the strength of different sectors, offering valuable insights into market trends and sector rotations.

At its core, the indicator calculates the TSI for each sector using price data obtained through the request.security() function. The TSI, a momentum oscillator, is computed using a user-defined smoothing period, allowing for customization based on individual preferences and trading styles. The resulting TSI values for each sector are then plotted on the chart, creating a visual representation of sector strengths.

To use this indicator effectively, traders should focus on comparing the movements of different sector lines. Sectors with lines moving higher are showing increasing strength, while those with descending lines are exhibiting weakness. This comparative analysis can help identify potential investment opportunities and sector rotations. Additionally, when multiple sector lines move in tandem, it may signal a broader market trend.

The indicator includes dashed lines at 0.5 and -0.5, serving as reference points for overbought and oversold conditions. Sectors with TSI values above 0.5 might be considered overbought, suggesting caution, while those below -0.5 could be viewed as oversold, potentially indicating buying opportunities.

One of the key advantages of this indicator is its flexibility. Users can toggle the visibility of individual sectors and customize their colors, allowing for a tailored analysis experience. This feature is particularly useful when focusing on specific sectors or reducing chart clutter for clearer visualization.

The indicator's ability to provide a comprehensive overview of all major S&P 500 sectors in a single chart is a significant benefit. This consolidated view enables quick comparisons and helps in identifying relative strengths and weaknesses across sectors. Such insights can be invaluable for portfolio allocation decisions and in spotting emerging market trends.

Moreover, the dynamic legend feature enhances the indicator's usability. It automatically updates to display only the visible sectors, improving chart readability and interpretation.

By leveraging this indicator, market participants can gain a deeper understanding of sector dynamics within the S&P 500. This enhanced perspective can lead to more informed decision-making in sector allocation strategies and individual stock selection. The indicator's ability to potentially detect early trends by comparing sector strengths adds another layer of value, allowing users to position themselves ahead of broader market movements.

In conclusion, the "S&P 500 Sector Strengths" indicator is a powerful tool that combines technical analysis with sector comparison. Its user-friendly interface, customizable features, and comprehensive sector coverage make it an valuable asset for traders and investors seeking to navigate the complexities of the S&P 500 market with greater confidence and insight.

BTC Price Percentage Difference( Bitfinex - Coinbase)Introduction:

The BTC Price Percentage Difference Histogram Indicator is a powerful tool designed to help traders visualize and capitalize on the price discrepancies of Bitcoin (BTC) between two major exchanges: Bitfinex and Coinbase. By calculating the real-time percentage difference of BTC-USD prices and displaying it as a color-coded histogram, this indicator enables you to quickly spot potential arbitrage opportunities and gain deeper insights into market dynamics.

Features:

• Real-Time Percentage Difference Calculation:

• Computes the percentage difference between BTC-USD prices on Bitfinex and Coinbase.

• Color-Coded Histogram Visualization:

• Green Bars: Indicate that the BTC price on Bitfinex is higher than on Coinbase.

• Red Bars: Indicate that the BTC price on Bitfinex is lower than on Coinbase.

• User-Friendly and Intuitive:

• Simple setup with no additional inputs required.

• Automatically adapts to the chart’s timeframe for seamless integration.

Why Bitfinex Whales Matter:

Bitfinex is renowned for hosting some of the largest Bitcoin traders, often referred to as “whales.” These influential players have the capacity to move the market, and historically, they’ve demonstrated a high success rate in buying at market bottoms and selling at market tops. By tracking the price discrepancies between Bitfinex and other exchanges like Coinbase, you can gain valuable insights into the sentiment and actions of these key market participants.

Fourier Extrapolation of PriceThis advanced algorithm leverages Fourier analysis to predict price trends by decomposing historical price data into its frequency components. Unlike traditional algorithms that often operate in lower-dimensional spaces, this method harnesses a multidimensional approach to capture intricate market behaviors. By utilizing additional dimensions, the algorithm identifies and extrapolates subtle patterns and oscillations that are typically overlooked, providing a more robust and nuanced forecast.

Ideal for traders seeking a deeper understanding of market dynamics, this tool offers an enhanced predictive capability by aligning its calculations with the complexity of real-world financial systems.

Fibonacci Snap Tool [TradersPro]

OVERVIEW

The Fibonacci Snap tool automatically snaps to the swing high and swing low of the price data shown on the chart display. Fibonacci retracement levels can be used for entry, exit, or as a confirmation of trend continuation.

If the swing high on the chart comes before the swing low, the price is in a downtrend.If the swing high comes after the swing low, the price is in an uptrend.

We call the 23.60% Fibonacci level the momentum zone of the trend. Price in a solid trend, either up or down, will typically hold the 23.60% Fibonacci level as support (demand) in an uptrend or resistance (supply) in a downtrend.

Deeper Fibonacci levels of 38.20%, 50.00%, and 61.80% are corrective supply/demand zones. As price moves against the found trend, it can move into this range block we call the corrective zone.

Fibonacci retracement levels are used to identify potential supply/demand areas where price could reverse or consolidate. These levels are based on key ratios derived from the Fibonacci sequence, and we only use the core 23.60%, 38.20%, 50.00%, and 61.80% ratios.

CONCEPTS

Price action moves in trend cycles, these retracement levels help traders measure proportional relationships between the high/low swings in the price trend.

When a price trend is moving against the trend, traders can find opportunities to trade with the current trend at key Fibonacci levels. Fibonacci levels can be used to anticipate where price might find supply/demand imbalance and continue moving in the trend direction.

Traders apply the indicator by selecting a window of price they want to analyze in the chart display, and the Fibonacci Snap tool will snap to the high and low of the visible price display.

The Intent and Use of This Tool

The 23.60% level acts as a momentum or continuation of trend. The 38.20% to 61.80% range are corrective zones of the trend.

The 61.80% level, also known as the golden ratio (Google the term “Golden Ratio”; it's fun), can often represent the location of supply/demand imbalance.

In an uptrend, it can represent the area of no more selling supply, and the balance can shift to buying demand. In a downtrend, it can represent the area of no more buying demand and the balance can shift to selling supply.

When used with the Momentum Zones indicator, these two tools create a powerful combination for traders to find, implement, and manage trades.

Normalized True Range - Grouped by WeekdaysThis indicator helps traders analyze daily volatility patterns across different days of the week by calculating normalized price ranges.

Unlike traditional volatility measures, it uses a normalized approach by dividing the daily range (high-low) by the midpoint price and multiplying by 100, providing a percentage-based measure that's comparable across different price levels. This normalization makes it particularly useful for comparing volatility patterns across different assets or time periods.

The indicator also includes a statistical overlay that highlights extreme volatility events. By calculating the 5th and 95th percentiles of the normalized ranges within your specified date range, it creates upper and lower bounds that help identify outlier days where volatility was exceptionally high or low.

These bounds appear as horizontal lines on the chart, making it easy to spot when current volatility breaks out of its historical norms.

The data is presented in both visual and tabular formats, with a comprehensive table showing the maximum, minimum, average, and 25th percentile ranges for each day of the week. This dual presentation allows traders to both quickly spot patterns visually and access detailed statistics for deeper analysis.

The user can customize the analysis period through simple date range inputs, making it flexible for different analytical timeframes.

COT Report Indicator with Selectable Data TypeOverview

The COT Report Indicator with Selectable Data Types is a powerful tool for traders who want to gain deeper insights into market sentiment using the Commitment of Traders (COT) data. This indicator allows you to visualize the net positions of different participant categories—Commercial, Noncommercial, and Nonreportable—directly on your chart.

The indicator is fully customizable, allowing you to select the type of data to display, sync with your chart's timeframe, or choose a custom timeframe. Whether you're analyzing gold, crude oil, indices, or forex pairs, this indicator adapts seamlessly to your trading needs.

Features

Dynamic Data Selection:

Choose between Commercial, Noncommercial, or Nonreportable data types.

Analyze the net positions of market participants for more informed decision-making.

Flexible Timeframes:

Sync with the chart's timeframe for quick analysis.

Select a custom timeframe to view COT data at your preferred granularity.

Wide Asset Coverage:

Supports various assets, including gold, silver, crude oil, indices, and forex pairs.

Automatically adjusts to the ticker you're analyzing.

Clear Visual Representation:

Displays Net Long, Net Short, and Net Difference (Long - Short) positions with distinct colors for easy interpretation.

Error Handling:

Alerts you if the symbol is unsupported, ensuring you know when COT data isn't available for a specific asset.

How to Use

Add the Indicator:

Click "Indicators" in TradingView and search for "COT Report Indicator with Selectable Data Types."

Add it to your chart.

Customize the Settings:

Data Type: Choose between Commercial, Noncommercial, or Nonreportable positions.

Data Source: Select "Futures Only" or "Futures and Options."

Timeframe: Sync with the chart's timeframe or specify a custom one (e.g., weekly, monthly).

Interpret the Data:

Green Line: Net Long Positions.

Red Line: Net Short Positions.

Black Line: Net Difference (Long - Short).

Supported Symbols:

Gold, Silver, Crude Oil, Natural Gas, Forex Pairs, S&P 500, US30, NAS100, and more.

Who Can Benefit

Trend Followers: Identify the buying/selling trends of Commercial and Noncommercial participants.

Sentiment Analysts: Understand shifts in sentiment among major market players.

Long-Term Traders: Use COT data to confirm or contradict your fundamental analysis.

Example Use Case

For example, if you're trading gold (XAUUSD) and select Noncommercial Positions, you’ll see the long and short positions of speculators. An increase in net long positions may signal bullish sentiment, while an increase in net short positions may indicate bearish sentiment.

If you switch to Commercial Positions, you'll get insights into how hedgers and institutions are positioning themselves, helping you confirm or counterbalance your current trading strategy.

Limitations

The indicator only works with supported symbols (COT data availability is limited to specific assets).

The COT data is updated weekly, so it is not suitable for short-term intraday trading.

Risk Indicator# Risk Indicator

A dynamic risk analysis tool that helps traders identify optimal entry and exit points using a normalized risk scale from 0 to 1. The indicator combines price action, moving averages, and logarithmic scaling to provide clear visual signals for different risk zones.

### Key Features

• Displays risk levels on a scale of 0-1 with intuitive color gradients (blue → cyan → green → yellow → orange → red)

• Shows predicted price levels for different risk values

• Divides the chart into 5 DCA (Dollar Cost Average) zones

• Includes customizable alerts for rapid risk changes and zone transitions

• Automatically adjusts to market conditions using dynamic ATH/ATL calculations

### Customizable Parameters

• SMA Period: Adjust the smoothing period for the baseline moving average

• Power Factor: Fine-tune the sensitivity of risk calculations

• Initial ATL Value: Set the starting point for ATL calculations

• Label Offset: Adjust the position of price level labels

• Visual Options: Toggle price levels and zone labels

• Alert Settings: Customize alert thresholds and enable/disable notifications

### Risk Zones Explained

The indicator divides the chart into five distinct zones:

- 0.0-0.2: DCA 5x (Deep Blue) - Strongest buy zone

- 0.2-0.4: DCA 4x (Cyan) - Strong buy zone

- 0.4-0.6: DCA 3x (Green) - Neutral zone

- 0.6-0.8: DCA 2x (Yellow/Orange) - Take profit zone

- 0.8-1.0: DCA 1x (Red) - Strong take profit / potential sell zone

### Alerts

Built-in alerts for:

• Rapid increases in risk level

• Rapid decreases in risk level

• Entry into buy zones

• Entry into sell zones

### How to Use

1. Add the indicator to your chart

2. Adjust the SMA period and power factor to match your trading timeframe

3. Monitor the risk level and corresponding price predictions

4. Use the DCA zones to guide your position sizing

5. Set up alerts for your preferred risk thresholds

### Tips

- Lower risk values (blue/cyan) suggest potentially good entry points

- Higher risk values (orange/red) suggest taking profits or reducing position size

- Use in conjunction with other technical analysis tools for best results

- Adjust the power factor to fine-tune sensitivity to price movements

### Notes

- Past performance is not indicative of future results

- This indicator is meant to be used as part of a complete trading strategy

- Always manage your risk and position size according to your trading plan

Version 1.0

Asset MaxGain MinLoss Tracker [CHE]Asset MaxGain MinLoss Tracker – Your Tool to Discover the Best Trading Opportunities

Introduction

Hello dear traders,

Today, I'd like to introduce you to a fantastic tool: the Asset MaxGain MinLoss Tracker . This indicator is designed to help you identify the best trading opportunities in the market by analyzing the maximum gain and adjusted maximum loss potentials of various assets.

Why Use This Indicator?

1. Time-Saving Analysis

Instead of spending hours sifting through different charts, this indicator provides you with key metrics for up to 10 assets at a glance.

2. Compare Multiple Assets Simultaneously

Monitor and compare multiple assets to discover which ones offer the highest profit potential and the lowest risk of loss.

3. Customizable Settings

Adjust the observation period and select the assets you want to analyze according to your trading strategy.

4. Clear Visual Representation

Data is presented in an easy-to-read table directly on your chart, highlighting assets with the highest maximum gain and the lowest adjusted maximum loss.

How to Use It in Everyday Trading

Step 1: Setting Up the Indicator

Select Your Assets: Choose up to 10 assets you wish to track. These can be cryptocurrencies, stocks, forex pairs, etc.

Configure the Trading Period Length: Set the number of bars (candles) over which you want to calculate the maximum gain and adjusted maximum loss. This allows you to tailor the analysis to your preferred time frame, whether it's short-term trading or long-term investing.

Step 2: Interpreting the Results

Maximum Gain (%): This value shows the potential upside of each asset over the selected period. A higher percentage indicates a greater potential for profit if the asset's price moves upward.

Adjusted Maximum Loss (%): This figure represents the potential downside risk, adjusted to give a more accurate reflection of loss potential. A lower percentage means less risk of significant loss.

Category Highlighting: Assets are categorized based on their performance:

High Gain & Low Loss: Assets that have both the highest max gain and the lowest adjusted max loss.

High Gain: Assets with the highest max gain.

Low Loss: Assets with the lowest adjusted max loss.

Step 3: Making Trading Decisions

Identify Opportunities: Focus on assets categorized as High Gain & Low Loss for the most favorable risk-to-reward scenarios.

Risk Management: Use the adjusted maximum loss to assess and mitigate potential risks associated with each asset.

Portfolio Diversification: Allocate your investments across assets with varying levels of gain and loss potentials to diversify your portfolio effectively.

Practical Example

Imagine you're monitoring the following assets:

Asset 1: BTCUSD

Asset 2: ETHUSD

Asset 3: ADAUSD

Asset 4: XRPUSD

After applying the indicator:

BTCUSD shows a high maximum gain but also a high adjusted maximum loss.

ETHUSD has both a high maximum gain and a low adjusted maximum loss, categorizing it as High Gain & Low Loss.

ADAUSD indicates a low maximum gain but the lowest adjusted maximum loss.

XRPUSD reflects moderate values in both categories.

Decision Making:

Primary Focus: ETHUSD may be your top choice due to its high reward and lower risk.

Risk-Averse Option: ADAUSD could be considered if you prioritize minimizing losses.

Balanced Approach: Diversify by investing in both ETHUSD and ADAUSD.

Understanding the Core Functionality

While you don't need to delve deep into the code to use the indicator effectively, understanding its core function can enhance your confidence in the tool.

The Main Function: Calculating Max Gain and Adjusted Max Loss

The heart of the indicator is a function that calculates two critical metrics for each asset:

Maximum Gain (sym_MaxGain):

Purpose: Measures the highest potential profit over the selected period.

How It Works: It finds the lowest price (sym_minlow) within the period and calculates the percentage increase to the current high price. This shows how much you could have gained if you bought at the lowest point.

Adjusted Maximum Loss (sym_AdjustedMaxLoss):

Purpose: Provides an adjusted measure of the potential loss, giving a more realistic risk assessment.

How It Works: It identifies the highest price (sym_maxhigh) within the period and calculates the percentage decrease to the current low price. This value is adjusted to account for the diminishing impact as losses approach 100%.

Simplified Explanation of the Function

Data Retrieval: For each asset (sym), the function retrieves the high and low prices over the specified timeframe.

Calculations:

Find Highest and Lowest Prices: Determines sym_maxhigh and sym_minlow within the tracking period.

Compute Max Gain: Calculates the potential gain from sym_minlow to the current high.

Compute Max Loss: Calculates the potential loss from sym_maxhigh to the current low.

Adjust Max Loss: Adjusts the max loss calculation to prevent distortion as losses near 100%.

Output: Returns both sym_MaxGain and sym_AdjustedMaxLoss for further analysis.

Benefits of Understanding the Function

Transparency: Knowing how these values are calculated can increase your trust in the indicator's outputs.

Customization: If you're familiar with coding, you might tailor the function to suit specific trading strategies.

Enhanced Analysis: Understanding the underlying calculations allows you to interpret the results more effectively, aiding in better decision-making.

Conclusion

The Asset MaxGain MinLoss Tracker is a powerful tool that can significantly enhance your trading efficiency and effectiveness by:

Providing Quick Insights: Save time by getting immediate access to essential performance metrics of multiple assets.

Assisting in Risk Management: Use the adjusted maximum loss to understand and mitigate potential risks.

Supporting Strategic Decisions: Identify assets with the best risk-to-reward ratios to optimize your trading strategy.

Take advantage of this indicator to elevate your trading game and make more informed decisions with confidence.

Thank you for your time, and happy trading!

Disclaimer:

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

This indicator is inspired by the "Max Gain" indicator. A special thanks to Skipper86 for his relentless effort, creativity, and contributions to the TradingView community, which served as a foundation for this work.

Quick scan for signal🙏🏻 Hey TV, this is QSFS, following:

^^ Quick scan for drift (QSFD)

^^ Quick scan for cycles (QSFC)

As mentioned before, ML trading is all about spotting any kind of non-randomness, and this metric (along with 2 previously posted) gonna help ya'll do it fast. This one will show you whether your time series possibly exhibits mean-reverting / consistent / noisy behavior, that can be later confirmed or denied by more sophisticated tools. This metric is O(n) in windowed mode and O(1) if calculated incrementally on each data update, so you can scan Ks of datasets w/o worrying about melting da ice.

^^ windowed mode

Now the post will be divided into several sections, and a couple of things I guess you’ve never seen or thought about in your life:

1) About Efficiency Ratios posted there on TV;

Some of you might say this is the Efficiency Ratio you’ve seen in Perry's book. Firstly, I can assure you that neither me nor Perry, just as X amount of quants all over the world and who knows who else, would say smth like, "I invented it," lol. This is just a thing you R&D when you need it. Secondly, I invite you (and mods & admin as well) to take a lil glimpse at the following screenshot:

^^ not cool...

So basically, all the Efficiency Ratios that were copypasted to our platform suffer the same bug: dudes don’t know how indexing works in Pine Script. I mean, it’s ok, I been doing the same mistakes as well, but loxx, cmon bro, you... If you guys ever read it, the lines 20 and 22 in da code are dedicated to you xD

2) About the metric;

This supports both moving window mode when Length > 0 and all-data expanding window mode when Length < 1, calculating incrementally from the very first data point in the series: O(n) on history, O(1) on live updates.

Now, why do I SQRT transform the result? This is a natural action since the metric (being a ratio in essence) is bounded between 0 and 1, so it can be modeled with a beta distribution. When you SQRT transform it, it still stays beta (think what happens when you apply a square root to 0.01 or 0.99), but it becomes symmetric around its typical value and starts to follow a bell-shaped curve. This can be easily checked with a normality test or by applying a set of percentiles and seeing the distances between them are almost equal.

Then I noticed that on different moving window sizes, the typical value of the metric seems to slide: higher window sizes lead to lower typical values across the moving windows. Turned out this can be modeled the same way confidence intervals are made. Lines 34 and 35 explain it all, I guess. You can see smth alike on an autocorrelogram. These two match the mean & mean + 1 stdev applied to the metric. This way, we’ve just magically received data to estimate alpha and beta parameters of the beta distribution using the method of moments. Having alpha and beta, we can now estimate everything further. Btw, there’s an alternative parameterization for beta distributions based on data length.

Now what you’ll see next is... u guys actually have no idea how deep and unrealistically minimalistic the underlying math principles are here.

I’m sure I’m not the only one in the universe who figured it out, but the thing is, it’s nowhere online or offline. By calculating higher-order moments & combining them, you can find natural adaptive thresholds that can later be used for anomaly detection/control applications for any data. No hardcoded thresholds, purely data-driven. Imma come back to this in one of the next drops, but the truest ones can already see it in this code. This way we get dem thresholds.

Your main thresholds are: basis, upper, and lower deviations. You can follow the common logic I’ve described in my previous scripts on how to use them. You just register an event when the metric goes higher/lower than a certain threshold based on what you’re looking for. Then you take the time series and confirm a certain behavior you were looking for by using an appropriate stat test. Or just run a certain strategy.

To avoid numerous triggers when the metric jitters around a threshold, you can follow this logic: forget about one threshold if touched, until another threshold is touched.

In general, when the metric gets higher than certain thresholds, like upper deviation, it means the signal is stronger than noise. You confirm it with a more sophisticated tool & run momentum strategies if drift is in place, or volatility strategies if there’s no drift in place. Otherwise, you confirm & run ~ mean-reverting strategies, regardless of whether there’s drift or not. Just don’t operate against the trend—hedge otherwise.

3) Flex;

Extension and limit thresholds based on distribution moments gonna be discussed properly later, but now you can see this:

^^ magic

Look at the thresholds—adaptive and dynamic. Do you see any optimizations? No ML, no DL, closed-form solution, but how? Just a formula based on a couple of variables? Maybe it’s just how the Universe works, but how can you know if you don’t understand how fundamentally numbers 3 and 15 are related to the normal distribution? Hm, why do they always say 3 sigmas but can’t say why? Maybe you can be different and say why?

This is the primordial power of statistical modeling.

4) Thanks;

I really wanna dedicate this to Charlotte de Witte & Marion Di Napoli, and their new track "Sanctum." It really gets you connected to the Source—I had it in my soul when I was doing all this ∞

RS Cycles [QuantVue]The RS Cycles indicator is a technical analysis tool that expands upon traditional relative strength (RS) by incorporating Beta-based adjustments to provide deeper insights into a stock's performance relative to a benchmark index. It identifies and visualizes positive and negative performance cycles, helping traders analyze trends and make informed decisions.

Key Concepts:

Traditional Relative Strength (RS):

Definition: A popular method to compare the performance of a stock against a benchmark index (e.g., S&P 500).

Calculation: The traditional RS line is derived as the ratio of the stock's closing price to the benchmark's closing price.

RS=Stock Price/Benchmark Price

Usage: This straightforward comparison helps traders spot periods of outperformance or underperformance relative to the market or a specific sector.

Beta-Adjusted Relative Strength (Beta RS):

Concept: Traditional RS assumes equal volatility between the stock and benchmark, but Beta RS accounts for the stock's sensitivity to market movements.

Calculation:

Beta measures the stock's return relative to the benchmark's return, adjusted by their respective volatilities.

Alpha is then computed to reflect the stock's performance above or below what Beta predicts:

Alpha=Stock Return−(Benchmark Return×β)

Significance: Beta RS highlights whether a stock outperforms the benchmark beyond what its Beta would suggest, providing a more nuanced view of relative strength.

RS Cycles:

The indicator identifies positive cycles when conditions suggest sustained outperformance:

Short-term EMA (3) > Mid-term EMA (10) > Long-term EMA (50).

The EMAs are rising, indicating positive momentum.

RS line shows upward movement over a 3-period window.

EMA(21) > 0 confirms a broader uptrend.

Negative cycles are marked when the opposite conditions are met:

Short-term EMA (3) < Mid-term EMA (10) < Long-term EMA (50).

The EMAs are falling, indicating negative momentum.

RS line shows downward movement over a 3-period window.

EMA(21) < 0 confirms a broader downtrend.

This indicator combines the simplicity of traditional RS with the analytical depth of Beta RS, making highlighting true relative strength and weakness cycles.

Relative Momentum StrengthThe Relative Momentum Strength (RMS) indicator is designed to help traders and investors identify tokens with the strongest momentum over two customizable timeframes. It calculates and plots the percentage price change over 30-day and 90-day periods (or user-defined periods) to evaluate a token's relative performance.

30-Day Momentum (Green Line): Short-term price momentum, highlighting recent trends and movements.

90-Day Momentum (Blue Line): Medium-term price momentum, providing insights into broader trends.

This tool is ideal for comparing multiple tokens or assets to identify those showing consistent strength or weakness. Use it to spot outperformers and potential reversals in a competitive universe of assets.

How to Use:

Apply this indicator to your TradingView chart for any token or asset.

Look for tokens with consistently high positive momentum for potential strength.

Use the plotted values to compare relative performance across your watchlist.

Customization:

Adjust the momentum periods to suit your trading strategy.

Overlay it with other indicators like RSI or volume for deeper analysis.

Universal Estimated Funding RateDescription:

This indicator calculates an estimated funding rate for perpetual futures contracts on Binance. The funding rate is derived from the premium index, reflecting the difference between the perpetual futures price and the spot market price, with an assumed constant interest rate.

Key Features:

Dynamic Symbol Detection: Automatically adapts to the base and quote currencies of the current chart, making it compatible with most Binance trading pairs that support both spot and perpetual markets.

Customizable Timeframes: Supports multiple timeframes, with a default recommendation of 4 hours to align with Binance's funding intervals.

Real-Time Data: Fetches live spot and perpetual prices to calculate the premium index and estimate funding rates in real time.

Error Handling: Displays alerts and highlights invalid data if the pair lacks spot or perpetual market information, ensuring clarity for the user.

Use Case:

This indicator is designed to help traders:

Track market sentiment through funding rates.

Identify opportunities for arbitrage or hedging between spot and perpetual markets.

Monitor trends in funding rates to complement technical analysis and refine entry/exit decisions.

How It Works:

The script dynamically identifies the spot and perpetual futures symbols for the selected chart.