Gabriel's Andean Oscillator📈 Gabriel's Andean Oscillator — Enhanced Trend-Momentum Hybrid

Gabriel's Andean Oscillator is a sophisticated trend-momentum indicator inspired by Alex Grover’s original Andean Oscillator concept. This enhanced version integrates multiple envelope types, smoothing options, and the ability to track volatility from both open/close and high/low dynamics—making it more responsive, adaptable, and visually intuitive.

🔍 What It Does

This oscillator measures bullish and bearish "energy" by calculating variance envelopes around price. Instead of traditional momentum formulas, it builds two exponential variance envelopes—one capturing the downside (bullish potential) and the other capturing the upside (bearish pressure). The result is a smoothed oscillator that reflects internal market tension and potential breakouts.

⚙️ Key Features

📐 Envelope Types:

Choose between:

"Regular" – Uses single EMA-based smoothing on open/close variance. Ideal for shorter timeframes.

"Double Smoothed" – Adds an extra layer of smoothing for noise reduction. Ideal for longer timeframes.

📊 Bullish & Bearish Components:

Bull = Measures potential upside using price lows (or open/close).

Bear = Measures downside pressure using highs (or open/close).

These can optionally be derived from high/low or open/close for flexible interpretation.

📏 Signal Line:

A customizable EMA of the dominant component to confirm momentum direction.

📉 Break Zone Area Plot:

An optional filled area showing when bull > bear or vice versa, useful for detecting expansion/contraction phases.

🟢 High/Low Overlay Option (Use Highs and Lows?):

Visualize secondary components derived from high/low prices to compare against the open/close dynamics and highlight volatility asymmetry.

🧠 How to Use It

Trend Confirmation:

When bull > bear and rising above signal → bullish bias.

When bear > bull and rising above signal → bearish bias.

Breakout Potential:

Watch the Break area plot (√(bull - bear)) for rapid expansion, signaling volatility bursts or directional moves.

High/Low Envelope Divergence:

Enabling the high/low comparison reveals hidden strength or weakness not visible in open/close alone.

🛠 Customizable Inputs

Envelope Type: Regular vs. Double Smoothed

EMA Envelope Lengths: For both regular and smoothed logic

Signal Length: Controls EMA smoothing for the signal

Use Highs and Lows?: Toggles second set of envelopes; the original doesn't include highs and lows.

Plot Breaks: Enables the filled “break” zone area, the squared difference between Open and Close.

🧪 Based On:

Andean Oscillator - Alpaca Markets

Licensed under CC BY-NC-SA 4.0

Developed by Gabriel, based on the work of Alex Grover

Cari skrip untuk "bias"

SMEMA Trend CoreSMEMA Trend Core is a multi-timeframe trend analysis tool designed to provide a clean, adaptive and structured view of the market’s directional bias. It can be used in short term, swing or long term contexts. The internal calculation adjusts automatically based on the selected trading style, while always combining data from six timeframes.

At its core, the indicator uses a SMEMA, which is a Simple Moving Average applied to an EMA. This combination improves smoothness without losing reactivity. The SMEMA is calculated separately on 1H, 4H, 1D, 3D, 1W and 1M timeframes. These six values are then combined using dynamic weights that depend on the trading mode:

Short Term mode gives more influence to 1H and 4H

Swing Trading mode gives more influence to 1D, 3D and 1W

Long Term mode gives more influence to 1W and 1M

However, all six timeframes are always included in the final result. This avoids the tunnel vision of relying on a single resolution and ensures that the indicator captures both local and structural movements.

The result is a synthetic trend line, called Global SMEMA, that adapts to market conditions and offers a realistic view of the ongoing trend. To enhance the reading, the indicator calculates a Trend Score. This score reflects the position of price relative to the Global SMEMA, scaled by a long-term ATR, and adjusted by the slope of the trend line. A hyperbolic tangent function is used to normalize values and reduce distortion from outliers.

The final score is capped between -10 and +10, and used to define the trend state:

Green when the trend is bullish (score > +1.5)

Red when the trend is bearish (score < -1.5)

Brown when the trend is neutral (score between -1.5 and +1.5)

Optional Deviation Bands can be displayed at ±1, ±2 and ±3 ATR distances around the central line. These dynamic zones help identify extended price movements or potential support and resistance areas, depending on the current trend bias.

Main features:

A single, stable trend line based on six timeframes

Automatic rebalancing depending on trading mode

Quantified score integrating distance and slope

No overreaction to short-term noise

Deviation zones for advanced market context

No repainting, no lookahead, 100% real-time

SMEMA Trend Core is not a signal tool. It is a directional framework that helps you stay aligned with the real structure of the market. Use it to confirm setups, filter trades or simply understand where the market stands in its trend cycle.

VWAP Supply & Demand Zones PRO**Overview:**

This script represents a major evolution of the original "VWAP Supply and Demand Zones" indicator. Initially created to explore price interaction with VWAP, it has now matured into a robust and feature-rich tool for identifying high-probability zones of institutional buying and selling pressure. The update introduces volume and momentum validation, dynamic zone management, alert logic, and a visual dashboard (HUD) — all designed for improved precision and clarity. The structural improvements, anti-repainting logic, and significant added utility warranted releasing this as a new script rather than a minor update.

---

### What It Does:

This indicator dynamically detects **supply and demand zones** using VWAP-based logic combined with **volume** and **momentum confirmation**. When price crosses VWAP with strength, it identifies the potential zone of excess demand (below VWAP) or supply (above VWAP), marking it visually with colored regions on the chart.

Each zone is extended for a user-defined duration, monitored for touch interactions (tests), and tracked for possible breaks. The script helps traders interpret price behavior around these institutional zones as either **reversal** opportunities or **continuation** confirmation depending on context and strategy preference.

---

### How It Works:

* **VWAP Basis**: Zones are anchored at VWAP at the time of a significant cross.

* **Volume & Momentum Filters**: Crosses are only considered valid if backed by above-average volume and notable price momentum.

* **Zone Drawing**: Validated supply and demand zones are drawn as boxes on the chart. Each is extended forward for a customizable number of bars.

* **Touch Counting**: Zones track the number of price touches. Alerts are issued after a user-defined number of tests.

* **Break Detection**: If price closes significantly beyond a zone boundary, the zone is marked as broken and visually dimmed.

* **Visual Dashboard (HUD)**: A compact real-time HUD displays VWAP value, active zone counts, and current market bias.

---

### How to Use It:

**Reversal Trading:**

* Look for price **rejecting** a zone after touching it.

* Use rejection candles or secondary indicators (e.g., RSI divergence) to confirm.

* These setups may offer low-risk entries when price respects the zone.

**Continuation Trading:**

* A **break of a zone** suggests strong directional bias.

* Use confirmed zone breaks to enter in the direction of momentum.

* Ideal in trending environments, especially with high volume and ATR movement.

---

### Key Inputs:

* **VWAP Length**: Moving VWAP period (default: 20)

* **Zone Width %**: Percentage size of zone buffer (default: 0.5%)

* **Min Touches**: How many times price must test a zone before alerts trigger

* **Zone Extension**: How far into the future zones are projected

* **Volume & ATR Filters**: Ensure only strong, valid crossovers create zones

---

### Alerts:

You can enable alerts for:

* **New zone creation**

* **Zone tests (after minimum touch count)**

* **Zone breaks**

* **VWAP crosses**

* **Active presence inside a zone (entry conditions)**

These alerts help automate market monitoring, making it suitable for discretionary or systematic workflows.

---

### Why It's a New Script:

This is not a cosmetic update. The internal logic, signal generation, filtering methodology, visual engine, and UX framework have been entirely rebuilt from the ground up. The result is a highly adaptive, precision-oriented tool — appropriate for intraday scalpers and swing traders alike. It goes far beyond the original in terms of functionality and reliability, justifying a fresh release.

---

### Suitable Markets and Timeframes:

* Works across all liquid markets (crypto, equities, futures, forex)

* Best used on timeframes where volume data is stable (5m and above recommended)

* Recalibrate inputs for optimal detection across instruments

Combined ATPC & MACD DivergenceTrend Optimizer + Divergence Finder in One Unified Tool

🔍 Overview:

This powerful dual-system indicator merges two proven analytical engines:

✅ The Algorganic Typical Price Channel (ATPC) — a custom trend oscillator that highlights mean-reversion and directional bias.

✅ A refined MACD system with divergence detection, enhanced with an adjusted Donchian midline for real-time trend strength filtering.

Together, they provide a high-confidence, multi-signal system ideal for swing trading, scalping, or confirming reversals with context.

⚙️ Core Components & Logic

🧠 1. ATPC Engine (Trend Commodity Index)

A momentum and volatility-normalized oscillator based on the typical price (H+L+C)/3:

TrendCI Line (Blue) – Main trend signal based on smoothed CCI logic.

TrendLine2 (Orange) – A slower smoothing of TrendCI for crossovers.

Key Zones (customizable):

🔴 Ultra Overbought: +73

🟣 Overbought: +58

🟣 Oversold: -58

🔴 Ultra Oversold: -73

Trade Logic:

✅ Buy Signal: TrendCI crosses above TrendLine2 while in oversold zone

❌ Sell Signal: TrendCI crosses below TrendLine2 while in overbought zone

Additional visual feedback:

Histogram Bars show strength and direction of momentum shift

Green/Red Circles highlight potential long/short setups

📉 2. MACD System + Divergence Finder

Classic MACD enhanced with a Donchian Midline overlay to filter trend bias.

🔷 MACD Line and 🟠 Signal Line show crossover momentum

🟩/🟥 Histogram shows distance from the signal line

🟪 Adjusted Donchian Midline dynamically adapts to range-bound vs trending environments

Background Color provides real-time trend state:

✅ Green = Bullish Trend

❌ Red = Bearish Trend

No color = Neutral / Choppy

MACD Boundaries (user-defined):

Overbought: +1.0

Oversold: -1.0

🔀 3. Divergence Detection

Spot hidden power shifts before price reacts:

🔼 Positive Divergence – Price makes lower lows, but MACD histogram rises

🔽 Negative Divergence – Price makes higher highs, but MACD histogram weakens

These are visually marked with:

Green “+Div” label (bullish reversal cue)

Red “–Div” label (bearish exhaustion signal)

🎯 How to Use It

For Trend Traders:

Stay in sync with macro trend using MACD histogram + background

Use ATPC crossovers for precision entries

Avoid signals during neutral background (chop filter)

For Reversal Traders:

Look for bullish +Div with ATPC buy signal in oversold zone

Look for bearish –Div with ATPC sell signal in overbought zone

Mid-Donchian line can act as confluence or breakout trigger

For Scalpers & Intraday Traders:

Combine with VWAP, liquidity zones, or order flow levels

ATPC crossovers + MACD histogram zero-line flip = potential scalp entry

Use histogram slope and divergence to avoid false momentum traps

🧩 Customizable Inputs

🎛️ ATPC: Channel & Smoothing lengths, overbought/oversold thresholds

🎛️ MACD: Fast/slow EMAs, signal smoothing, Donchian period, bounds

🎨 Fully theme-compatible with adjustable colors and line styles

🔔 Alerts (Add Your Own)

While this version doesn’t contain built-in alerts, you can easily add alerts based on:

buySignal or sellSignal from ATPC logic

Histogram cross zero or trend flip

MACD Divergence event

📜 “This indicator doesn't just show signals—it tells a story about who’s in control of the market, and when that control might be slipping.”

Last Week's APM FX pairs only📖 Description:

This script is designed for precision-focused forex traders who understand the power of volatility measurement. It calculates the Average Price Movement (APM) from the previous week by measuring the full wick-to-wick range (high to low) of each daily candle from Monday to Friday, then averaging them across the five sessions.

🔍 Core Features:

✅ Accurate APM Calculation:

Pulls daily high-low ranges from last week using locked daily timeframe data, ensuring stable and reliable pip range measurements across all chart timeframes.

✅ Auto-Adjusts for Pip Precision:

Detects whether the pair is JPY-based or not, and automatically adjusts the pip multiplier (100 for JPY pairs, 10,000 for all others) to give true pip values.

✅ Visual Display in Clean UI:

The calculated APM is displayed in a non-intrusive, fixed-position table in the top-right corner of the chart — making it ideal for traders who want continuous awareness of recent market behavior without visual clutter.

✅ Timeless on Any Timeframe:

Whether you’re on the 1-minute chart or the daily, the script remains anchored and accurate because it sources raw data from the daily chart internally.

📈 How It Helps Your Trading:

🧠 Volatility Awareness: Know how much a pair typically moves per day based on recent historical behavior — great for range analysis, target setting, or session biasing.

📊 Week-to-Week Comparison: Use it as a benchmark to compare current volatility to last week’s. Great for identifying if the market is expanding, contracting, or stabilizing.

🔗 Perfect for Confluence: APM can serve as a supporting metric when combined with order blocks, liquidity zones, news catalysts, or other volatility-based tools like ATR.

🛠️ Ideal For:

Professional and prop firm traders

Institutional model traders (ICT-style or SMC)

Volatility scalpers and range-based intraday traders

Anyone building a rules-based trading system with data-driven logic

🔐 Clean. Reliable. Focused.

If you value structure, volatility awareness, and pip precision — this tool belongs in your chart workspace.

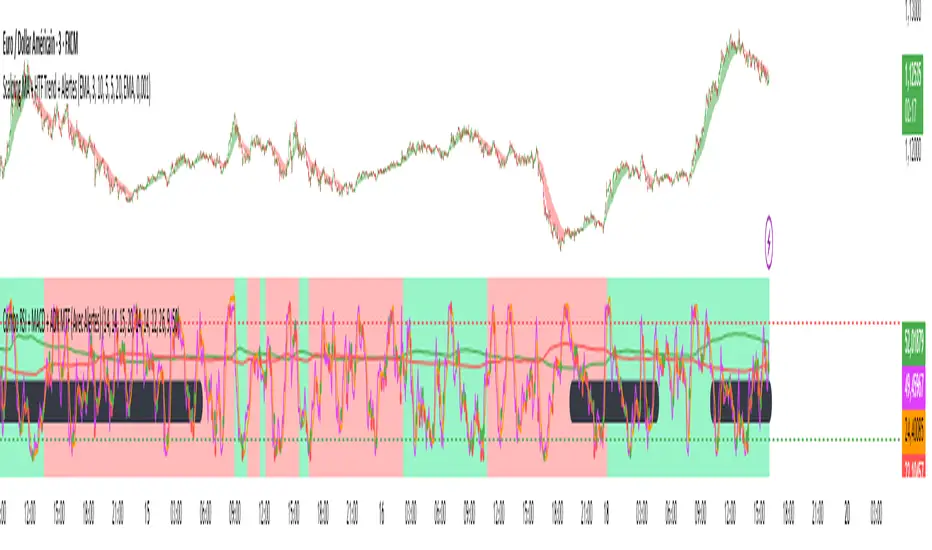

Combo RSI + MACD + ADX MTF (Avec Alertes)✅ Recommended Title:

Multi-Signal Oscillator: ADX Trend + DI + RSI + MACD (MTF, Cross Alerts)

✅ Detailed Description

📝 Overview

This indicator combines advanced technical analysis tools to identify trend direction, capture reversals, and filter false signals.

It includes:

ADX (Multi-TimeFrame) for trend and trend strength detection.

DI+ / DI- for directional bias.

RSI + ZLSMA for oscillation analysis and divergence detection.

Zero-Lag Normalized MACD for momentum and entry timing.

⚙️ Visual Components

✅ Green/Red Background: Displays overall trend based on Multi-TimeFrame ADX.

✅ DI+ / DI- Lines: Green and red curves showing directional bias.

✅ Normalized RSI: Blue oscillator with orange ZLSMA smoothing.

✅ Zero-Lag MACD: Violet or fuchsia/orange oscillator depending on the version.

✅ Crossover Points: Colored circles marking buy and sell signals.

✅ ADX Strength Dots: Small black dots when ADX exceeds the strength threshold.

🚨 Included Alert System

✅ RSI / ZLSMA Crossovers (Buy / Sell).

✅ MACD / Signal Line Crossovers (Buy / Sell).

✅ DI+ / DI- Crossovers (Buy / Sell).

✅ Double Confirmation DI+ / RSI or DI+ / MACD.

✅ Double Confirmation DI- / RSI or DI- / MACD.

✅ Trend Change Alerts via Background Color.

✅ ADX Strength Alerts (Above Threshold).

🛠️ Suggested Configuration Examples

1. Short-Term Reversal Detection:

RSI Length: 7 to 14

ZLSMA Length: 7 to 14

MACD Fast/Slow: 5 / 13

ADX MTF Period: 5 to 15

ADX Threshold: 15 to 20

2. Long-Term Trend Following:

RSI Length: 21 to 30

ZLSMA Length: 21 to 30

MACD Fast/Slow: 12 / 26

ADX MTF Period: 30 to 50

ADX Threshold: 20 to 25

3. Scalping / Day Trading:

RSI Length: 5 to 9

ZLSMA Length: 5 to 9

MACD Fast/Slow: 3 / 7

ADX MTF Period: 5 to 10

ADX Threshold: 10 to 15

🎯 Why Use This Tool?

Filters false signals using ADX-based background coloring.

Provides multi-source alerting (RSI, MACD, ADX).

Helps identify true market strength zones.

Works on all markets: Forex, Crypto, Stocks, Indices.

A.K Dynamic EMA/SMA / MTF S&R Zones Toolkit with AlertsThe A.K Dynamic EMA/SMA / MTF Support & Resistance Zones Toolkit is a powerful all-in-one technical analysis tool designed for traders who want a clean yet comprehensive market view. Whether you're scalping lower timeframes or swing trading higher timeframes, this indicator gives you both the structure and signals to take action with confidence.

Key Features:

✅ Customizable EMA/SMA Suite

Display key Exponential and Simple Moving Averages including 5, 9, 20, 50, 100, and 200 EMAs, plus optional 50 SMA for trend filtering. Each line can be toggled individually and color-customized.

✅ Multi-Timeframe Support & Resistance Zones

Automatically detects dynamic S/R zones on key timeframes (5min, 15min, 30min, 1H, 4H, 1D) using swing highs/lows. Zones are color-coded by strength and whether they're broken or active, providing a clear visual roadmap for price reaction levels.

✅ Zone Strength & Break Detection

Distinguishes between strong and weak zones based on price proximity and reaction depth, with visual shading and automatic label updates when a level is broken.

✅ Price Action-Based Buy/Sell Signals

Generates BUY signals when bullish candles react to strong support (supply) zones, and SELL signals when bearish candles react to strong resistance (demand) zones. All logic is adjustable — including candle body vs wick detection, tolerance range, and strength thresholds.

✅ Alerts Engine

Built-in TradingView alerts for price touching support/resistance or triggering buy/sell signals. Perfect for automation or hands-free monitoring.

✅ Optional Candle & Trend Filters

Highlight bullish/bearish candles visually for additional confirmation.

Optional RSI display and 50-period SMA trend filter to guide directional bias.

🧠 Use Case Scenarios:

Identify dynamic supply & demand zones across multiple timeframes.

Confirm trend direction with EMAs and SMA filters.

React quickly to clean BUY/SELL signals based on actual price interaction with strong zones.

Customize it fully to suit scalping, day trading, or swing trading strategies.

📌 Recommended Settings:

Use default zone transparency (65%) and offset (250 bars) for optimal visual clarity.

Enable alerts to get notified when price enters key S/R levels or when a trade signal occurs.

Combine this tool with your entry/exit plan for better decision-making under pressure.

💡 Pro Tip: Add this indicator to a clean chart and let the zones + EMAs guide your directional bias. Use alerts to avoid screen-watching and improve discipline.

Created by:

Version: Pine Script v6

Platform: TradingView

Anchored Bollinger Band Range [SS]This is the anchored Bollinger band indicator.

What it does?

The anchored BB indicator:

Takes a user defined range and calculates the Standard Deviation of the entire selected range for the high and low values.

Computes a moving average of the high and low during the selected period (which later becomes the breakout range average)

Anchors to the last high and last low of the period range to add up to 4 standard deviations to the upside and downside, giving you 4 high and low targets.

How can you use it?

The anchored BB indicator has many applicable uses, including

Identifying daily ranges based on premarket trading activity ( see below ):

Finding breakout ranges for intraday pattern setups ( see below ):

Identified pattern of interest:

Applying Anchored BB:

Identifying daily or pattern biases based on the position to the opening breakout range average (blue line). See the examples with explanations:

ex#1:

ex#2:

The Opening Breakout Average

As you saw in the examples above, the blue line represents the opening breakout range average.

This is the average high of the period of interest and the average low of the period of interest.

Price action above this line would be considered Bullish, and Bearish if below.

This also acts as a retracement zone in non-trending markets. For example:

Best Use Cases

Identify breakout ranges for patterns on larger timeframes. For example

This pattern on SPY, if we overlay the Anchored BB:

You want to see it actually breakout from this range and hold to confirm a breakout. Failure to exceed the BB range, means that it is just ranging with no real breakout momentum.

Identify conservative ranges for a specific period in time, for example QQQ:

Worst Use Cases

Using it as a hard and fast support and resistance indicator. This is not what it is for and ranges can be exceeded with momentum. The key is looking for whether ranges are exceeded (i.e. high momentum, thus breakout play) or they are not (thus low volume, rangy).

Using it for longer term outlooks. This is not ideal for long term ranges, as with any Bollinger/standard deviation based approach, it is only responsive to CURRENT PA and cannot forecast FUTURE PA.

User Inputs

The indicator is really straight forward. There are 2 optional inputs and 1 required input.

Period Selection: Required. Selects the period for the indicator to perform the analysis on. You just select it with your mouse on the chart.

Visible MA: Optional. You can choose to have the breakout range moving average visible or not.

Fills: Optional. You can choose to have the fills plotted or not.

And that is the indicator! Very easy to use and hope you enjoy and find it helpful!

As always, safe trades everyone! 🚀

Multi-Factor Reversal AnalyzerMulti-Factor Reversal Analyzer – Quantitative Reversal Signal System

OVERVIEW

Multi-Factor Reversal Analyzer is a comprehensive technical analysis toolkit designed to detect market tops and bottoms with high precision. It combines trend momentum analysis, price action behavior, wave oscillation structure, and volatility breakout potential into one unified indicator.

This indicator is not a random mix of tools — each module is carefully selected for a specific purpose. When combined, they form a multi-dimensional view of the market, merging trend analysis, momentum divergence, and volatility compression to produce high-confidence signals.

Why Combine These Modules?

Module Combination Ideas & How to Use Them

Factor A: Trend Detector + Gold Zone

Concept:

• The Trend Detector (light yellow histogram) evaluates market strength:

• Histogram trending downward or staying below 50 → bearish conditions;

• Trending upward or staying above 50 → bullish conditions.

• The Gold Zone identifies areas of volatility compression — typically a prelude to explosive market moves.

Practical Application:

• When the Gold Zone appears and the Trend Detector is bearish → likely downside move;

• When the Gold Zone appears and the Trend Detector is bullish → likely upside breakout.

• Note: The Gold Zone does not mean the bottom is in. It is not a buy signal on its own — always combine it with other modules for directional bias.

Factor B: PAI + Wave Trend

Concept:

• PAI (Price Action Index) is a custom oscillator that combines price momentum with volatility dispersion, displaying strength zones:

• Green area → bullish dominance;

• Red area → bearish pressure.

• Wave Trend offers smoothed crossover signals via the main and signal lines.

Practical Application:

• When PAI is in the green zone and Wave Trend makes a bullish crossover → potential reversal to the upside;

• When PAI is in the red zone and Wave Trend shows a bearish crossover → potential start of a downtrend.

Factor C: Trend Detector + PAI

Concept:

• Combines directional trend strength with price action strength to confirm setups via confluence.

Practical Application:

• Trend Detector histogram bottoms out + PAI enters the green zone → high chance of upward reversal;

• Histogram tops out + PAI in the red zone → increased likelihood of downside continuation.

Multi-Factor Confluence (Advanced Use)

• When Trend Detector, PAI, and Wave Trend all align in the same direction (bullish or bearish), the directional signal becomes significantly more reliable.

• This setup is especially useful for trend-following or swing trade entries.

KEY FEATURES

1. Multi-Layer Reversal Logic

• Combines trend scoring, oscillator divergence, and volatility squeezes for triangulated reversal detection.

• Helps traders distinguish between trend pullbacks and true reversals.

2. Advanced Divergence Detection

• Detects both regular and hidden divergences using pivot-based confirmation logic.

• Customizable lookback ranges and pivot sensitivity provide flexible tuning for different market styles.

3. Gold Zone Volatility Compression

• Highlights pre-breakout zones using custom oscillation models (RSI, harmonic, Karobein, etc.).

• Improves anticipation of breakout opportunities following low-volatility compressions.

4. Trend Direction Context

• PAI and Trend Score components provide top-down insight into prevailing bias.

• Built-in “Straddle Area” highlights consolidation zones; breakouts from this area often signal new trend phases.

5. Flexible Visualization

• Color-coded trend bars, reversal markers, normalized oscillator plots, and trend strength labels.

• Designed for both visual discretionary traders and data-driven system developers.

USAGE GUIDELINES

1. Applicable Markets

• Suitable for stocks, crypto, futures, and forex

• Supports reversal, mean-reversion, and breakout trading styles

2. Recommended Timeframes

• Short-term traders: 5m / 15m / 1H — use Wave Trend divergence + Gold Zone

• Swing traders: 4H / Daily — rely on Price Action Index and Trend Detector

• Macro trend context: use PAI HTF mode for higher timeframe overlays

3. Reversal Strategy Flow

• Watch for divergence (WT/PAI) + Gold Zone compression

• Confirm with Trend Score weakening or flipping

• Use Straddle Area breakout for final trigger

• Optional: enable bar coloring or labels for visual reinforcement

• The indicator performs optimally when used in conjunction with a harmonic pattern recognition tool

4. Additional Note on the Gold Zone

The “Gold Zone” does not directly indicate a market bottom. Since it is displayed at the bottom of the chart, it may be misunderstood as a bullish signal. In reality, the Gold Zone represents a compression of price momentum and volatility, suggesting that a significant directional move is about to occur. The direction of that move—upward or downward—should be determined by analyzing the histogram:

• If histogram momentum is weakening, the Gold Zone may precede a downward move.

• If histogram momentum is strengthening, it may signal an upcoming rebound or rally.

Treat the Gold Zone as a warning of impending volatility, and always combine it with trend indicators for accurate directional judgment.

RISK DISCLAIMER

• This indicator calculates trend direction based on historical data and cannot guarantee future market performance. When using this indicator for trading, always combine it with other technical analysis tools, fundamental analysis, and personal trading experience for comprehensive decision-making.

• Market conditions are uncertain, and trend signals may result in false positives or lag. Traders should avoid over-reliance on indicator signals and implement stop-loss strategies and risk management techniques to reduce potential losses.

• Leverage trading carries high risks and may result in rapid capital loss. If using this indicator in leveraged markets (such as futures, forex, or cryptocurrency derivatives), exercise caution, manage risks properly, and set reasonable stop-loss/take-profit levels to protect funds.

• All trading decisions are the sole responsibility of the trader. The developer is not liable for any trading losses. This indicator is for technical analysis reference only and does not constitute investment advice.

• Before live trading, it is recommended to use a demo account for testing to fully understand how to use the indicator and apply proper risk management strategies.

CHANGELOG

v1.0: Initial release featuring integrated Price Action Index, Trend Strength Scoring, Wave Trend Oscillator, Gold Zone Compression Detection, and dual-type divergence recognition. Supports higher timeframe (HTF) synchronization, visual signal markers, and diversified parameter configurations.

[COG]S&P 500 Weekly Seasonality ProjectionS&P 500 Weekly Seasonality Projection

This indicator visualizes S&P 500 seasonality patterns based on historical weekly performance data. It projects price movements for up to 26 weeks ahead, highlighting key seasonal periods that have historically affected market performance.

Key Features:

Projects price movements based on historical S&P 500 weekly seasonality patterns (2005-2024)

Highlights six key seasonal periods: Jan-Feb Momentum, March Lows, April-May Strength, Summer Strength, September Dip, and Year-End Rally

Customizable forecast length from 1-26 weeks with quick timeframe selection buttons

Optional moving average smoothing for more gradual projections

Detailed statistics table showing projected price and percentage change

Seasonality mini-map showing the full annual pattern with current position

Customizable colors and visual elements

How to Use:

Apply to S&P 500 index or related instruments (daily timeframe or higher recommended)

Set your desired forecast length (1-26 weeks)

Monitor highlighted seasonal zones that have historically shown consistent patterns

Use the projection line as a general guideline for potential price movement

Settings:

Forecast length: Configure from 1-26 weeks or use quick select buttons (1M, 3M, 6M, 1Y)

Visual options: Customize colors, backgrounds, label sizes, and table position

Display options: Toggle statistics table, period highlights, labels, and mini-map

This indicator is designed as a visual guide to help identify potential seasonal tendencies in the S&P 500. Historical patterns are not guarantees of future performance, but understanding these seasonal biases can provide valuable context for your trading decisions.

Note: For optimal visualization, use on Daily timeframe or higher. Intraday timeframes will display a warning message.

[COG]Nasdaq Weekly Seasonality ProjectionNasdaq Weekly Seasonality Projection

This indicator provides a visualization of Nasdaq seasonality patterns based on historical weekly performance data. It projects price movements for up to 26 weeks ahead, highlighting key seasonal periods that have historically affected tech stocks.

Key Features:

Projects price movements based on historical Nasdaq weekly seasonality patterns

Highlights six key seasonal periods: January Effect, March Lows, April-May Strength, Tech Summer Rally, September Dip, and Q4 Tech Rally

Customizable forecast length from 1-26 weeks with quick timeframe selection buttons

Optional moving average smoothing for more gradual projections

Detailed statistics table showing projected price and percentage change

Seasonality mini-map showing the full annual pattern with current position

Customizable colors and visual elements

How to Use:

Apply to Nasdaq indices or tech-focused instruments (daily timeframe or higher recommended)

Set your desired forecast length (1-26 weeks)

Monitor highlighted seasonal zones that have historically shown consistent patterns

Use the projection line as a general guideline for potential price movement

Settings:

Forecast length: Configure from 1-26 weeks or use quick select buttons (1M, 3M, 6M, 1Y)

Visual options: Customize colors, backgrounds, label sizes, and table position

Display options: Toggle statistics table, period highlights, labels, and mini-map

This indicator is designed as a visual guide to help identify potential seasonal tendencies in Nasdaq and tech stocks. Historical patterns are not guarantees of future performance, but understanding these seasonal biases can provide valuable context for your trading decisions.

Note: For optimal visualization, use on Daily timeframe or higher. Intraday timeframes will display a warning message.

Implied and Historical VolatilityAbstract

This TradingView indicator visualizes implied volatility (IV) derived from the VIX index and historical volatility (HV) computed from past price data of the S&P 500 (or any selected asset). It enables users to compare market participants' forward-looking volatility expectations (via VIX) with realized past volatility (via historical returns). Such comparisons are pivotal in identifying risk sentiment, volatility regimes, and potential mispricing in derivatives.

Functionality

Implied Volatility (IV):

The implied volatility is extracted from the VIX index, often referred to as the "fear gauge." The VIX represents the market's expectation of 30-day forward volatility, derived from options pricing on the S&P 500. Higher values of VIX indicate increased uncertainty and risk aversion (Whaley, 2000).

Historical Volatility (HV):

The historical volatility is calculated using the standard deviation of logarithmic returns over a user-defined period (default: 20 trading days). The result is annualized using a scaling factor (default: 252 trading days). Historical volatility represents the asset's past price fluctuation intensity, often used as a benchmark for realized risk (Hull, 2018).

Dynamic Background Visualization:

A dynamic background is used to highlight the relationship between IV and HV:

Yellow background: Implied volatility exceeds historical volatility, signaling elevated market expectations relative to past realized risk.

Blue background: Historical volatility exceeds implied volatility, suggesting the market might be underestimating future uncertainty.

Use Cases

Options Pricing and Trading:

The disparity between IV and HV provides insights into whether options are over- or underpriced. For example, when IV is significantly higher than HV, options traders might consider selling volatility-based derivatives to capitalize on elevated premiums (Natenberg, 1994).

Market Sentiment Analysis:

Implied volatility is often used as a proxy for market sentiment. Comparing IV to HV can help identify whether the market is overly optimistic or pessimistic about future risks.

Risk Management:

Institutional and retail investors alike use volatility measures to adjust portfolio risk exposure. Periods of high implied or historical volatility might necessitate rebalancing strategies to mitigate potential drawdowns (Campbell et al., 2001).

Volatility Trading Strategies:

Traders employing volatility arbitrage can benefit from understanding the IV/HV relationship. Strategies such as "long gamma" positions (buying options when IV < HV) or "short gamma" (selling options when IV > HV) are directly informed by these metrics.

Scientific Basis

The indicator leverages established financial principles:

Implied Volatility: Derived from the Black-Scholes-Merton model, implied volatility reflects the market's aggregate expectation of future price fluctuations (Black & Scholes, 1973).

Historical Volatility: Computed as the realized standard deviation of asset returns, historical volatility measures the intensity of past price movements, forming the basis for risk quantification (Jorion, 2007).

Behavioral Implications: IV often deviates from HV due to behavioral biases such as risk aversion and herding, creating opportunities for arbitrage (Baker & Wurgler, 2007).

Practical Considerations

Input Flexibility: Users can modify the length of the HV calculation and the annualization factor to suit specific markets or instruments.

Market Selection: The default ticker for implied volatility is the VIX (CBOE:VIX), but other volatility indices can be substituted for assets outside the S&P 500.

Data Frequency: This indicator is most effective on daily charts, as VIX data typically updates at a daily frequency.

Limitations

Implied volatility reflects the market's consensus but does not guarantee future accuracy, as it is subject to rapid adjustments based on news or events.

Historical volatility assumes a stationary distribution of returns, which might not hold during structural breaks or crises (Engle, 1982).

References

Black, F., & Scholes, M. (1973). "The Pricing of Options and Corporate Liabilities." Journal of Political Economy, 81(3), 637-654.

Whaley, R. E. (2000). "The Investor Fear Gauge." The Journal of Portfolio Management, 26(3), 12-17.

Hull, J. C. (2018). Options, Futures, and Other Derivatives. Pearson Education.

Natenberg, S. (1994). Option Volatility and Pricing: Advanced Trading Strategies and Techniques. McGraw-Hill.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (2001). The Econometrics of Financial Markets. Princeton University Press.

Jorion, P. (2007). Value at Risk: The New Benchmark for Managing Financial Risk. McGraw-Hill.

Baker, M., & Wurgler, J. (2007). "Investor Sentiment in the Stock Market." Journal of Economic Perspectives, 21(2), 129-151.

BTC Seasonality Strategy (Weekly)This strategy identifies potential weekend opportunities in Bitcoin (BTC) markets by leveraging the concept of seasonality, entering a position at a predefined time and day, and exiting at a specified time and day.

Key Features

Customizable Time and Day Selection:

Users can select the entry and exit days and corresponding times (in EST).

Directional Flexibility:

The strategy allows traders to choose between long or short positions.

TradingView Compliance:

The script adheres to TradingView's house rules, avoids overly complex conditions, and provides clear user-configurable inputs.

How It Works

The script determines the current weekday and hour in EST, converting TradingView's UTC time for accurate comparisons.

If the current day and hour match the selected entry conditions, a trade (long or short) is opened.

The position is closed when the current day and hour match the specified exit conditions.

Theoretical Basis

Market Seasonality:

The concept of seasonality in financial markets refers to predictable patterns based on time, such as weekends or specific days of the week. Studies have shown that cryptocurrency markets exhibit unique trading behaviors during weekends due to reduced institutional activity and higher retail participation behavioral Biases**:

Retail traders often dominate weekend markets, potentially causing predictable inefficiencies .

Reverences**

Baur, D. G., Hong, K., & Lee, A. D. (2018). Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money, 54, 177–189.

Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letters, 148, 80–82.

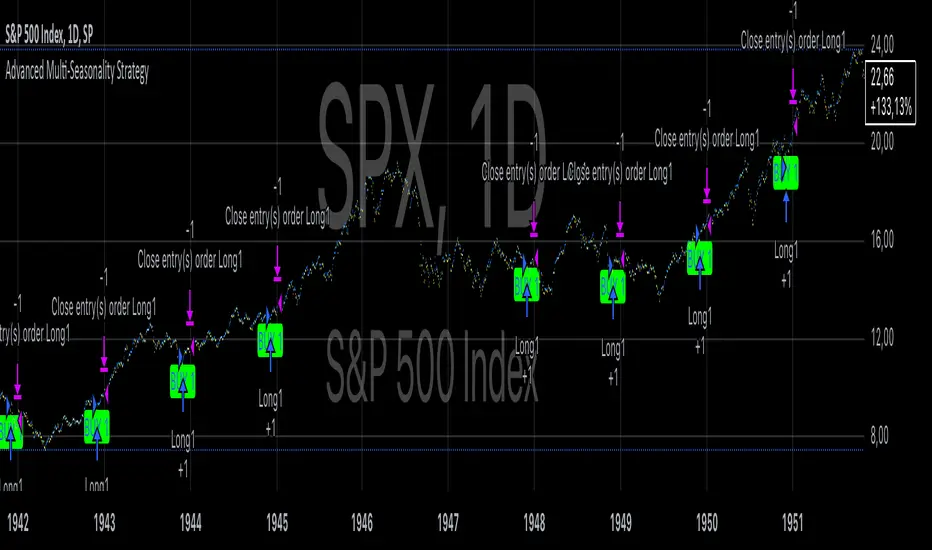

Advanced Multi-Seasonality StrategyThe Multi-Seasonality Strategy is a trading system based on seasonal market patterns. Seasonality refers to recurring market trends driven by predictable calendar-based events. These patterns emerge due to economic cycles, corporate activities (e.g., earnings reports), and investor behavior around specific times of the year. Studies have shown that such effects can influence asset prices over defined periods, leading to opportunities for traders who exploit these patterns (Hirshleifer, 2001; Bouman & Jacobsen, 2002).

How the Strategy Works:

The strategy allows the user to define four distinct periods within a calendar year. For each period, the trader selects:

Entry Date (Month and Day): The date to enter the trade.

Holding Period: The number of trading days to remain in the trade after the entry.

Trade Direction: Whether to take a long or short position during that period.

The system is designed with flexibility, enabling the user to activate or deactivate each of the four periods. The idea is to take advantage of seasonal patterns, such as buying during historically strong periods and selling during weaker ones. A well-known example is the "Sell in May and Go Away" phenomenon, which suggests that stock returns are higher from November to April and weaker from May to October (Bouman & Jacobsen, 2002).

Seasonality in Financial Markets:

Seasonal effects have been documented across different asset classes and markets:

Equities: Stock markets tend to exhibit higher returns during certain months, such as the "January effect," where prices rise after year-end tax-loss selling (Haugen & Lakonishok, 1987).

Commodities: Agricultural commodities often follow seasonal planting and harvesting cycles, which impact supply and demand patterns (Fama & French, 1987).

Forex: Currency pairs may show strength or weakness during specific quarters based on macroeconomic factors, such as fiscal year-end flows or central bank policy decisions.

Scientific Basis:

Research shows that market anomalies like seasonality are linked to behavioral biases and institutional practices. For example, investors may respond to tax incentives at the end of the year, and companies may engage in window dressing (Haugen & Lakonishok, 1987). Additionally, macroeconomic factors, such as monetary policy shifts and holiday trading volumes, can also contribute to predictable seasonal trends (Bouman & Jacobsen, 2002).

Risks of Seasonal Trading:

While the strategy seeks to exploit predictable patterns, there are inherent risks:

Market Changes: Seasonal effects observed in the past may weaken or disappear as market conditions evolve. Increased algorithmic trading, globalization, and policy changes can reduce the reliability of historical patterns (Lo, 2004).

Overfitting: One of the risks in seasonal trading is overfitting the strategy to historical data. A pattern that worked in the past may not necessarily work in the future, especially if it was based on random chance or external factors that no longer apply (Sullivan, Timmermann, & White, 1999).

Liquidity and Volatility: Trading during specific periods may expose the trader to low liquidity, especially around holidays or earnings seasons, leading to slippage and larger-than-expected price swings.

Economic and Geopolitical Shocks: External events such as pandemics, wars, or political instability can disrupt seasonal patterns, leading to unexpected market behavior.

Conclusion:

The Multi-Seasonality Strategy capitalizes on the predictable nature of certain calendar-based patterns in financial markets. By entering and exiting trades based on well-established seasonal effects, traders can potentially capture short-term profits. However, caution is necessary, as market dynamics can change, and seasonal patterns are not guaranteed to persist. Rigorous backtesting, combined with risk management practices, is essential to successfully implementing this strategy.

References:

Bouman, S., & Jacobsen, B. (2002). The Halloween Indicator, "Sell in May and Go Away": Another Puzzle. American Economic Review, 92(5), 1618-1635.

Fama, E. F., & French, K. R. (1987). Commodity Futures Prices: Some Evidence on Forecast Power, Premiums, and the Theory of Storage. Journal of Business, 60(1), 55-73.

Haugen, R. A., & Lakonishok, J. (1987). The Incredible January Effect: The Stock Market's Unsolved Mystery. Dow Jones-Irwin.

Hirshleifer, D. (2001). Investor Psychology and Asset Pricing. Journal of Finance, 56(4), 1533-1597.

Lo, A. W. (2004). The Adaptive Markets Hypothesis: Market Efficiency from an Evolutionary Perspective. Journal of Portfolio Management, 30(5), 15-29.

Sullivan, R., Timmermann, A., & White, H. (1999). Data-Snooping, Technical Trading Rule Performance, and the Bootstrap. Journal of Finance, 54(5), 1647-1691.

This strategy harnesses the power of seasonality but requires careful consideration of the risks and potential changes in market behavior over time.

Ultimate Oscillator Trading StrategyThe Ultimate Oscillator Trading Strategy implemented in Pine Script™ is based on the Ultimate Oscillator (UO), a momentum indicator developed by Larry Williams in 1976. The UO is designed to measure price momentum over multiple timeframes, providing a more comprehensive view of market conditions by considering short-term, medium-term, and long-term trends simultaneously. This strategy applies the UO as a mean-reversion tool, seeking to capitalize on temporary deviations from the mean price level in the asset’s movement (Williams, 1976).

Strategy Overview:

Calculation of the Ultimate Oscillator (UO):

The UO combines price action over three different periods (short-term, medium-term, and long-term) to generate a weighted momentum measure. The default settings used in this strategy are:

Short-term: 6 periods (adjustable between 2 and 10).

Medium-term: 14 periods (adjustable between 6 and 14).

Long-term: 20 periods (adjustable between 10 and 20).

The UO is calculated as a weighted average of buying pressure and true range across these periods. The weights are designed to give more emphasis to short-term momentum, reflecting the short-term mean-reversion behavior observed in financial markets (Murphy, 1999).

Entry Conditions:

A long position is opened when the UO value falls below 30, indicating that the asset is potentially oversold. The value of 30 is a common threshold that suggests the price may have deviated significantly from its mean and could be due for a reversal, consistent with mean-reversion theory (Jegadeesh & Titman, 1993).

Exit Conditions:

The long position is closed when the current close price exceeds the previous day’s high. This rule captures the reversal and price recovery, providing a defined point to take profits.

The use of previous highs as exit points aligns with breakout and momentum strategies, as it indicates sufficient strength for a price recovery (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages two well-established phenomena in financial markets: momentum and mean-reversion. Momentum, identified in earlier studies like those by Jegadeesh and Titman (1993), describes the tendency of assets to continue in their direction of movement over short periods. Mean-reversion, as discussed by Poterba and Summers (1988), indicates that asset prices tend to revert to their mean over time after short-term deviations. This dual approach aims to buy assets when they are temporarily oversold and capitalize on their return to the mean.

Multi-timeframe Analysis:

The UO’s incorporation of multiple timeframes (short, medium, and long) provides a holistic view of momentum, unlike single-period oscillators such as the RSI. By combining data across different timeframes, the UO offers a more robust signal and reduces the risk of false entries often associated with single-period momentum indicators (Murphy, 1999).

Trading and Market Efficiency:

Studies in behavioral finance, such as those by Shiller (2003), show that short-term inefficiencies and behavioral biases can lead to overreactions in the market, resulting in price deviations. This strategy seeks to exploit these temporary inefficiencies, using the UO as a signal to identify potential entry points when the market sentiment may have overly pushed the price away from its average.

Strategy Performance:

Backtests of this strategy show promising results, with profit factors exceeding 2.5 when the default settings are optimized. These results are consistent with other studies on short-term trading strategies that capitalize on mean-reversion patterns (Jegadeesh & Titman, 1993). The use of a dynamic, multi-period indicator like the UO enhances the strategy’s adaptability, making it effective across different market conditions and timeframes.

Conclusion:

The Ultimate Oscillator Trading Strategy effectively combines momentum and mean-reversion principles to trade on temporary market inefficiencies. By utilizing multiple periods in its calculation, the UO provides a more reliable and comprehensive measure of momentum, reducing the likelihood of false signals and increasing the profitability of trades. This aligns with modern financial research, showing that strategies based on mean-reversion and multi-timeframe analysis can be effective in capturing short-term price movements.

References:

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Williams, L. (1976). Ultimate Oscillator. Market research and technical trading analysis.

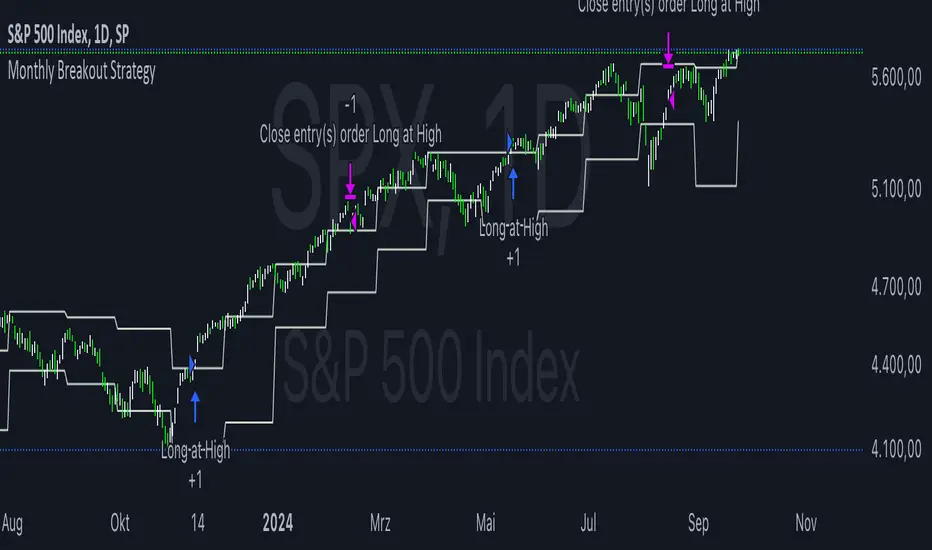

Monthly Breakout StrategyThis Monthly High/Low Breakout Strategy is designed to take long or short positions based on breakouts from the high or low of the previous month. Users can select whether they want to go long at a breakout above the previous month’s high, short at a breakdown below the previous month’s low, or use the reverse logic. Additionally, it includes a month filter, allowing trades to be executed only during user-specified months.

Breakout strategies, particularly those based on monthly highs and lows, aim to capitalize on price momentum. These systems rely on the assumption that once a significant price level is breached (such as the previous month's high or low), the market is likely to continue moving in the same direction due to increased volatility and trend-following behaviors by traders. Studies have demonstrated the potential effectiveness of breakout strategies in financial markets.

Scientific Evidence Supporting Breakout Strategies:

Momentum in Financial Markets:

Research on momentum-based strategies, which include breakout trading, shows that securities breaking key levels of support or resistance tend to continue their price movement in the direction of the breakout. Jegadeesh and Titman (1993) found that stocks with strong performance over a given period tend to continue performing well in subsequent periods, a principle also applied to breakout strategies.

Behavioral Finance:

The psychological factor of herd behavior is one of the driving forces behind breakout strategies. When prices break out of a key level (such as a monthly high), it triggers increased buying or selling pressure as traders join the trend. Barberis, Shleifer, and Vishny (1998) explained how cognitive biases, such as overconfidence and sentiment, can amplify price trends, which breakout strategies attempt to exploit.

Market Efficiency:

While markets are generally efficient, periods of inefficiency can occur, particularly around the breakouts of significant price levels. These inefficiencies often result in temporary price trends, which breakout strategies can exploit before the market corrects itself (Fama, 1970).

Risk Considerations:

Despite the potential for profit, the Monthly Breakout Strategy comes with several risks:

False Breakouts:

One of the most common risks in breakout strategies is the occurrence of false breakouts. These happen when the price temporarily moves above (or below) a key level but quickly reverses direction, causing losses for traders who entered positions too early. This is particularly risky in low-volatility environments.

Market Volatility:

Monthly breakout strategies rely on momentum, which may not be consistent across different market conditions. During periods of low volatility, price breakouts might lack the follow-through required for the strategy to succeed, leading to poor performance.

Whipsaw Risk:

The strategy is vulnerable to whipsaw markets, where prices oscillate around key levels without establishing a clear direction. This can result in frequent entry and exit signals that lead to losses, especially if trading costs are not managed properly.

Overfitting to Past Data:

If the month-selection filter is overly optimized based on historical data, the strategy may suffer from overfitting—performing well in backtests but poorly in real-time trading. This happens when strategies are tailored to past market conditions that may not repeat.

Conclusion:

While monthly breakout strategies can be effective in markets with strong momentum, they are subject to several risks, including false breakouts, volatility dependency, and whipsaw behavior. It is crucial to backtest this strategy thoroughly and ensure it aligns with your risk tolerance before implementing it in live trading.

References:

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Barberis, N., Shleifer, A., & Vishny, R. (1998). A Model of Investor Sentiment. Journal of Financial Economics, 49(3), 307-343.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, 25(2), 383-417.

Tomorrow Floor Pivots with CPR By Nifty ZThe colors for resistance and support levels have been updated to gradient reds and greens for clearer distinction.

The CPR band uses light blue and purple to stand out more effectively.

Here's a detailed explanation of the user inputs and the typical use of **Floor Pivots for Tomorrow’s Market Range** in a trading context, focusing on support, resistance, and breakout scenarios:

The script allows traders to customize key parameters for their analysis:

1. Pivot Timeframe:

- Users can select different timeframes for calculating floor pivots, such as 1 hour, 4 hours, daily, weekly, monthly, etc.

- This is crucial because the timeframe selection influences the granularity of the support and resistance levels for the next trading day.

- For instance, selecting a **Daily** timeframe will calculate floor pivots for the next trading day, while selecting **Weekly** will give levels for the upcoming week.

2. Show Floor Pivots:

- Users can toggle the visibility of the calculated **Floor Pivots**, which include resistance levels (R1, R2, R3, R4) and support levels (S1, S2, S3, S4).

3. Show CPR (Central Pivot Range):

- CPR (Central Pivot Range) is a key area where the price tends to consolidate.

- The script allows users to enable or disable the visibility of CPR, which consists of the BC (Bottom Central Pivot) and TC (Top Central Pivot).

4. Show Labels:

- Users can choose whether or not to display labels indicating the **Pivot**, **Support**, and Resistance levels on the chart. This can be helpful for visual analysis when day trading.

Understanding Floor Pivots

The Floor Pivots (Pivot, Resistance, and Support levels) for tomorrow's market range are calculated based on today’s high, low, and close. These levels help traders anticipate how the market may behave in the upcoming session.

1. Pivot:

- The Pivot Point is a central level, calculated as the average of the high, low, and close. It’s considered a reference point that determines the market’s overall bias.

- If the price is trading **above the pivot**, it generally suggests a **bullish** sentiment for the day.

- If the price is trading **below the pivot**, it suggests a **bearish** sentiment.

2. Resistance Levels (R1, R2, R3, R4):

- R1 is often the first area where price may stall in an uptrend. It represents the first major resistance level.

- **R2**, **R3**, and **R4** mark additional levels of resistance, progressively further away from the current price. These are used to project potential upward targets.

- These resistance levels are areas where the price might encounter selling pressure, especially during day trading.

3. **Support Levels (S1, S2, S3, S4):**

- Similarly, **S1** is the first area where the price might find support in a downtrend.

- **S2**, **S3**, and **S4** provide deeper support levels where the price may bounce from.

- These support zones are used by day traders to anticipate where the price might reverse upward.

### **Role of Resistance and Support in Day Trading**

- **Resistance Levels (R1, R2, R3, R4)** indicate potential areas where price could **stall** during an uptrend. These levels are useful for **short-term traders** looking to set exit points or identify reversal zones.

- **Support Levels (S1, S2, S3, S4)** highlight areas where the price could **find support** and potentially **bounce** higher. These levels are particularly helpful for identifying buy zones in a downtrend.

- If a price **breaks out** above the resistance levels or **breaks down** below the support levels, it often signals a strong trend continuation.

### **Understanding the Central Pivot Range (CPR)**

The **CPR** is formed by two key levels:

- **BC (Bottom Central Pivot):** The midpoint of the day’s high and low.

- **TC (Top Central Pivot):** The difference between the pivot and BC.

The CPR acts as a region of **consolidation** or **indecision** where the market is likely to stay within a narrow range. The width of the CPR gives traders a sense of volatility:

- A **narrow CPR** often signals that a **breakout** is imminent.

- A **wider CPR** suggests that the market could remain range-bound.

### **Market Sentiment Based on Floor Pivots**

The relationship between **today’s** and **tomorrow’s pivots** is crucial in determining the market sentiment for the next day.

1. **Bullish Case (Higher Highs):**

- If **tomorrow's pivot** is higher than **today's pivot**, it indicates a **bullish sentiment**. This suggests that the market is likely to trend upward in the next session.

- In a **bullish overlapping pivot range**, if **Day 1 (today)** is higher than **Day 2 (tomorrow)**, traders expect continued upward momentum.

2. **Bearish Case (Lower Lows):**

- Conversely, if **tomorrow's pivot** is lower than **today's pivot**, it suggests a **bearish sentiment** and that the market could trend downward in the next session.

- In a **bearish overlapping pivot range**, if **Day 1 (today)** is lower than **Day 2 (tomorrow)**, traders expect continued downward pressure.

### **Breakout Scenarios**

A breakout occurs when the price **violates either the support or resistance levels** significantly, indicating that the price is moving in the direction of the breakout.

1. **Bullish Breakout:**

- If the price consistently stays **above the CPR** and **resistance levels (R1, R2)**, it indicates a strong **bullish breakout**.

- This is especially true when the **CPR is narrow** for both days, signaling a buildup in price action and a potential breakout to the upside.

2. **Bearish Breakout:**

- If the price breaks **below the CPR** and **support levels (S1, S2)**, it indicates a **bearish breakout**.

- A narrow CPR on **both days** suggests that a breakout to the downside could be imminent.

3. **Neutral or Ranging Days:**

- Sometimes, the CPR stays **unchanged** for 4-5 days, indicating a period of **consolidation** where the price is moving within a tight range. This often leads to a significant breakout once the consolidation ends.

Strategic Application of Floor Pivots for Tomorrow

Traders use floor pivots to plan their next-day trades by:

- **Aligning with Market Sentiment:** Based on whether tomorrow’s pivot is higher or lower than today’s, traders can align their trades in the direction of the market’s overall bias.

- **Identifying Entry and Exit Points:** Resistance and support levels provide well-defined areas to enter or exit trades, making pivots essential for day trading strategies.

- **Anticipating Breakouts:** Monitoring the width of the CPR and the relation between pivots helps traders anticipate potential breakouts, allowing them to react quickly to sudden price movements.

By effectively using these pivots and understanding their significance, traders can improve their decision-making for short-term trades in the stock or futures markets.

Monthly Purchase Strategy with Dynamic Contract Size This trading strategy is designed to automate monthly purchases of a security, adjusting the size of each purchase based on the percentage of the portfolio's equity. The key features of this strategy include:

Monthly Purchases: The strategy buys the security on a specified day of each month, based on the user's input.

Dynamic Position Sizing: The size of each purchase is calculated as a percentage of the current equity. This allows the position size to adjust dynamically with the portfolio's performance.

Slippage and Commission Considerations: Slippage is simulated by adjusting the entry price by a set number of ticks, while commissions are factored in as fixed costs per trade.

Drawdown Calculation: The strategy tracks the highest equity value and calculates the drawdown, which is the percentage decrease from this peak equity. This helps in assessing the performance and risk of the strategy.

Benefits of the Strategy

Automated Investment: The strategy automates the investment process, reducing the need for manual trading decisions and ensuring consistent execution.

Dynamic Position Sizing: By adjusting the purchase size based on the portfolio’s equity, the strategy helps in managing risk and capitalizing on market movements proportionally to the portfolio’s performance.

Regular Investments: Investing on a regular schedule helps in averaging the purchase price of the security, which can reduce the impact of short-term volatility.

Risk Management: Monitoring drawdown helps in assessing the risk and performance of the strategy, providing insights into potential losses relative to the highest equity value.

Scientific Documentation on ETF Savings Plans

1. Dollar-Cost Averaging and Investment Behavior:

Title: "The Benefits of Dollar-Cost Averaging: A Study of Investment Behavior"

Authors: William F. Sharpe

Journal: Financial Analysts Journal, 1994

Summary: This study discusses the concept of dollar-cost averaging (DCA), which involves investing a fixed amount of money at regular intervals regardless of market conditions. The study highlights that DCA can reduce the impact of market volatility and lower the average cost of investments over time.

Reference: Sharpe, W. F. (1994). The Benefits of Dollar-Cost Averaging: A Study of Investment Behavior. Financial Analysts Journal, 50(4), 27-36.

2. ETFs and Long-Term Investment Strategies:

Title: "Exchange-Traded Funds and Their Role in Long-Term Investment Strategies"

Authors: John C. Bogle

Journal: The Journal of Portfolio Management, 2007

Summary: This paper explores the advantages of using ETFs for long-term investment strategies, emphasizing their low costs, tax efficiency, and diversification benefits. It also discusses how ETFs can be used effectively in automated investment plans like ETF savings plans.

Reference: Bogle, J. C. (2007). Exchange-Traded Funds and Their Role in Long-Term Investment Strategies. The Journal of Portfolio Management, 33(4), 14-25.

3. Risk and Return in ETF Investments:

Title: "Risk and Return Characteristics of Exchange-Traded Funds"

Authors: Eugene F. Fama and Kenneth R. French

Journal: Journal of Financial Economics, 2010

Summary: Fama and French analyze the risk and return characteristics of ETFs compared to traditional mutual funds. The study provides insights into how ETFs can be a viable option for investors seeking diversified exposure while managing risk and optimizing returns.

Reference: Fama, E. F., & French, K. R. (2010). Risk and Return Characteristics of Exchange-Traded Funds. Journal of Financial Economics, 96(2), 257-278.

4. The Impact of Automated Investment Plans:

Title: "The Impact of Automated Investment Plans on Portfolio Performance"

Authors: David G. Blanchflower and Andrew J. Oswald

Journal: Journal of Behavioral Finance, 2012

Summary: This research examines how automated investment plans, including ETF savings plans, affect portfolio performance. It highlights the benefits of automation in reducing behavioral biases and ensuring consistent investment practices.

Reference: Blanchflower, D. G., & Oswald, A. J. (2012). The Impact of Automated Investment Plans on Portfolio Performance. Journal of Behavioral Finance, 13(2), 77-89.

Summary

The "Monthly Purchase Strategy with Dynamic Contract Size and Drawdown" provides a disciplined approach to investing by automating purchases and adjusting position sizes based on portfolio equity. It leverages the benefits of dollar-cost averaging and regular investment, with risk management through drawdown monitoring. Scientific literature supports the effectiveness of ETF savings plans and automated investment strategies in optimizing returns and managing investment risk.

CNN Fear and Greed Index JD modified from minusminusCNN Fear and Greed Index - www.cnn.com

Modified from minusminus -

See Documentation from CNN's website

CNN's Fear and Greed index is an attempt to quantitatively score the Fear and Greed in the SPX using 7 factors:

Market Momentum- S&P 500 (SPX) and its 125-day moving average

Stock Price Strength -Net new 52-week highs and lows on the NYSE

Stock Price Breadth - McClellan Volume Summation Index

Put and Call options - 5-day average put/call ratio

Market Volatility - VIX and its 50-day moving average

Safe Haven Demand - Difference in 20-day stock and bond returns

Junk Bond Demand - Yield spread: junk bonds vs. investment grade

Each Factor has a weight input for the final calculation initially set to a weight of 1. The final calculation of the index is a weighted average of each factor.

3 Factors have separate functions for calculation : See Code for Clarity

SPX Momentum : difference between the Daily CBOE:SPX index value and it's 125 Day Simple moving average.

Stock Price Strength : Net New 52-week highs and lows on the NYSE.

Function calculates a measure of Net New 52-week highs by:

NYSE 52-week highs (INDEX:MAHN) - all new NYSE Highs (INDEX:HIGH)

measure of Net New 52-week lows by:

NYSE 52-week lows (INDEX:MALN) - all new NYSE Lows (INDEX:LOWN)

Then calculate a ratio of Net New 52-week Highs and Lows over Total Highs and Lows then takes a 5-day moving average of that ratio-See Code

Stock Price Breadth is the McClellan Volume Summation Index :

First Calculate the McClellan Oscillator

Second Calculate the Summation Index

4 Factors are Straight data requests

5 Day Simple Moving Average of the Put-Call Ratio on SPY

50 Day Simple Moving Average of the SPX VIX

Difference between 20 Day Simple Moving Average of SPX Daily Close and 20 Day Simple Moving Average of 10Y Constant Maturity US Treasury Note

Yield Spread between ICE BofA US High Yield Index and ICE BofA US Investment Grade Corporate Yield Index

The Fear and Greed Index is a weighted average of these factors - which is then normalized to scale from 0 to 100 using the past 25 values - length parameter.

3 Zones are Shaded: Red for Extreme Fear, Grey for normal jitters, Green for Extreme Greed.

Disclaimer: This is not financial advice. These are just my ideas, and I am not an investment advisor or investment professional. This code is for informational purposes only and do your own analysis before making any investment decisions. This is an attempt to replicate in spirt an index CNN publishes on their website and in no way shape or form infringes on their content, calculations or proprietary information.

From CNN: www.cnn.com

FEAR & GREED INDEX FAQs

What is the CNN Business Fear & Greed Index?

The Fear & Greed Index is a way to gauge stock market movements and whether stocks are fairly priced. The theory is based on the logic that excessive fear tends to drive down share prices, and too much greed tends to have the opposite effect.

How is Fear & Greed Calculated?

The Fear & Greed Index is a compilation of seven different indicators that measure some aspect of stock market behavior. They are market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand. The index tracks how much these individual indicators deviate from their averages compared to how much they normally diverge. The index gives each indicator equal weighting in calculating a score from 0 to 100, with 100 representing maximum greediness and 0 signaling maximum fear.

How often is the Fear & Greed Index calculated?

Every component and the Index are calculated as soon as new data becomes available.

How to use Fear & Greed Index?

The Fear & Greed Index is used to gauge the mood of the market. Many investors are emotional and reactionary, and fear and greed sentiment indicators can alert investors to their own emotions and biases that can influence their decisions. When combined with fundamentals and other analytical tools, the Index can be a helpful way to assess market sentiment.

Prospect Theory IndicatorProspect Theory Indicator

This indicator is designed based on Prospect Theory, which was developed by Nobel laureates Daniel Kahneman and Amos Tversky. Prospect Theory explains how people make decisions involving risk and uncertainty, highlighting their tendency to value potential losses more than equivalent gains and their focus on relative gains and losses rather than absolute outcomes.

Features:

1. Reference Points: The indicator calculates and displays the highest and lowest prices over a specified period (default is 14 periods). These are the reference points used to evaluate current price movements.

2. Risk/Reward Ratio: It calculates the risk/reward ratio by comparing the current price to the reference points. The risk is defined as the distance to the lowest point, and the reward as the distance to the highest point.

3. Visual Indicators:

• Green Line: Indicates the highest reference point (High Reference Point).

• Red Line: Indicates the lowest reference point (Low Reference Point).

• Green Triangle: Displays when the reward outweighs the risk, suggesting a favorable condition for entering a trade.

• Red Triangle: Displays when the risk outweighs the reward, suggesting a cautious approach.

4. Labels: Provides real-time labels showing the risk/reward ratio, and marks the current conditions as “High Risk” or “High Reward” based on the calculated ratio.

Usage:

• Entry Signals: Use green triangles for potential buy entries when the reward is higher than the risk.

• Exit Signals: Use red triangles as a signal to review your positions, as the risk has become higher than the reward.

• Risk Management: Continuously monitor the risk/reward ratio to maintain optimal risk management in your trading strategy.

This indicator helps traders make more informed and objective decisions, mitigating the emotional biases described by Prospect Theory.

($ROSE Trader) Mean Multiple OscillatorThe ROSE Trader Mean Multiple Oscillator is an adaptation of The Mayer Multiple, using the 99-Day Simple Moving Average rather than the 200-Day (adjusted for ROSE's higher delta), setting distinct preset levels for ROSE overbought and oversold conditions.

Who is this indicator for?

While this indicator will function on any chart, it is setup for trading Oasis BINANCE:ROSEUSDT token specifically — the presets used are tailored to the ROSE chart.

While it is an open source public script, it has been released primarily for the ROSE community

What does this indicator offer?

This indicator follows the same concepts as the Mayer Multiple, popular with BTC. What makes it unique is that it the presets are setup specifically for the BINANCE:ROSEUSDT , based upon my trading experience.

About the Mayer Multiple:

The Mayer Multiple is a derivative of the 200-day MA, calculated by dividing the BTC market price by the 200-day MA. The 200-day MA is a widely recognised indicator for BTC in establishing macro bull or bear bias. The Mayer Multiple therefore represents a measure of distance away from this long-term average or mean price as a tool to gauge overbought and oversold conditions.

For BTC overbought, and oversold conditions, have historically coincided with Mayer Multiple values of 2.4, and 0.8 respectively.

Adapting this concept to the ROSE token:

The adaption of the Mayer Multiple offered here adjusts the 200-day MA to suit the higher delta or volatility of the BINANCE:ROSEUSDT token specifically. For ROSE I use the 99-day MA to establish macro bull or bear bias. The derived 'Mean Multiple', based on the 99-day MA therefore represents a measure of distance away from this long-term average or mean price as a tool to gauge overbought and oversold conditions.

For ROSE overbought, and oversold conditions, tend to coincide with values of 1.618, and 0.618 respectively. Further offsets have been preprogrammed to add nuance to the way this indicator may be used in different market conditions

The ROSE Trader Mean Multiple Oscillator:

The Oscillator version of this script is useful to determine possible levels that price is likely to reach overbought and over sold conditions by plotting the offsets and values directly on the price chart

Calculations:

99-Day Simple Moving Average (99D SMA) * by offset

This script is partnered with the "ROSE Trade Mean Multiple”: an adaptation of The Mayer Multiple, using the 99-Day Simple Moving Average rather than the 200-Day (adjusted for ROSE's higher delta), setting distinct preset levels for ROSE overbought and oversold conditions.

Note: this script is setup to work with any instrument, but the presets are built to provide actionable data on the Oasis BINANCE:ROSEUSDT token specifically. It is not a predicative model, it rather shows how price has behaved historically / statistically at these levels given past data.

($ROSE Trader) Mean MultipleThe ROSE Trader Mean Multiple is an adaptation of The Mayer Multiple, using the 99-Day Simple Moving Average rather than the 200-Day (adjusted for ROSE's higher delta), setting distinct preset levels for ROSE overbought and oversold conditions.

Who is this indicator for?

While this indicator will function on any chart, it is setup for trading Oasis BINANCE:ROSEUSDT token specifically — the presets used are tailored to the ROSE chart.

While it is an open source public script, it has been released primarily for the ROSE community

What does this indicator offer?

This indicator follows the same concepts as the Mayer Multiple, popular with BTC. What makes it unique is that it the presets are setup specifically for the BINANCE:ROSEUSDT , based upon my trading experience.

About the Mayer Multiple:

The Mayer Multiple is a derivative of the 200-day MA, calculated by dividing the BTC market price by the 200-day MA. The 200-day MA is a widely recognised indicator for BTC in establishing macro bull or bear bias. The Mayer Multiple therefore represents a measure of distance away from this long-term average or mean price as a tool to gauge overbought and oversold conditions.

For BTC overbought, and oversold conditions, have historically coincided with Mayer Multiple values of 2.4, and 0.8 respectively.

Adapting this concept to the ROSE token:

The adaption of the Mayer Multiple offered here adjusts the 200-day MA to suit the higher delta or volatility of the BINANCE:ROSEUSDT token specifically. For ROSE I use the 99-day MA to establish macro bull or bear bias. The derived 'Mean Multiple', based on the 99-day MA therefore represents a measure of distance away from this long-term average or mean price as a tool to gauge overbought and oversold conditions.