Cari skrip untuk "bar"

Average Daily Range - without open barBasic ADR-indicator that is showing the daily range on lower timeframes as well, without using the current open daily bar for calculation.

Also plots as line in a separate indicator window. Updates displayed value when hovering over the candles on the chart to see historical Numbers.

Leledc Exhaustion BarAn mt4 indicator converted to pine,its not always accurate but combined with S/R ,pivots, fibs etc will give an edge.

Dots are the major swings holow circles are the minor swings

more here

www.abundancetradinggroup.com

3-Bar-Reversal-Pattern Strategy Backtest This startegy based on 3-day pattern reversal described in "Are Three-Bar

Patterns Reliable For Stocks" article by Thomas Bulkowski, presented in

January, 2000 issue of Stocks&Commodities magazine.

That pattern conforms to the following rules:

- It uses daily prices, not intraday or weekly prices;

- The middle day of the three-day pattern has the lowest low of the three days, with no ties allowed;

- The last day must have a close above the prior day's high, with no ties allowed;

- Each day must have a nonzero trading range.

Please, use it only for learning or paper trading. Do not for real trading.

HEIKIN ASHI COLOUR CHANGE ALERTThis can be used to trigger an alert if Heikin Ashi bar changes color :)

Franklin ATR Bar highlight by els (robotfarm.ru)Script highlights signal bars for tfc3.ru school trading strategy. Working timeframe D.

Colored Volume Bars with Standard Deviation from the MeanI have updated the indicator to help visualize volume . The percentage scale is based on a 21 period look back average . The colored volume bars represent volumes that exceed specified standard deviation of this 21 period average as indicated in the figure. The deviation bands are based on a the 55sma of the 21 period average (brown line). A 8 period sma of the 21 moving average (red line) is also indicated.

Alpha/Bars converterSimple tool to convert alpha in Bars length period. Often MA period's are express in alpha ratio, and become difficult to visualize the MA length's . Now you can convert alpha in to periods, and periods in alpha

Internal Bar Strength IndicatorThe internal bar strength or (IBS) is an oscillating indicator which measures the relative position of the close price with respect to the low to high range for the same period.

YK Fuller BarsThe script highlights "Fuller's pins" and generates alerts when these bars are appearing

Higher Resolution Bars on Intraday ChartHi everybody!

With new plotbar and plotcandle functions you may plot somewhat "stretched" daily bars over intraday chart. Enjoy!

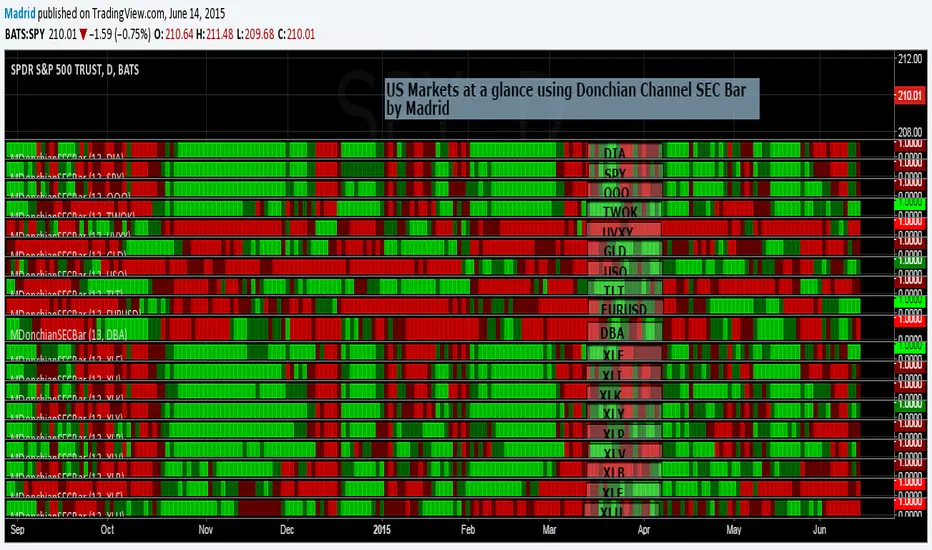

Madrid Donchian SEC barThis study is based on the Donchain Channel Bar indicator but this adds security as a parameter. This allows several instances of this indicator to be used in the same page to create a heat map to take look at a glance at several securities, just like the example where this was implemented.

The only two parameters it requires are the security symbol and the length of the analysis.

Madrid MA Ribbon BarThis study is the companion of the MMAR, displayed here in this publication. This displays the same information as MMAR, but in a linear format. This measures the possibilities of a trend reversal. If the bar fills over 50% of the opposite color from bottom to top then chances are there will be a trend reversal. Otherwise it is just a reentry point.

This study doesn't require but one parameter, and the default is very good. Define if you want to use the standard or the exponential moving average. It is simple, easy to interpret and doesn't require much space on the screen.

It uses only four standard colors

1. Red : A downtrend in progress

2. Green: A short reentry or a trend reversal warning

3. Lime : An uptrend in progress

4. Maroon: A long reentry or a trend reversal warning