Cari skrip untuk "Volatility"

JustNifty: VnF Levels (Volatility and Fibbonacci Levels)Volatility and Fibonacci Levels based on JustNifty Blog and Twitter

Volatility Direction DetectorThis script helps trader identify volatility direction in order to classify each market move. It also provides good entry points.

Volatility RatioVolatility Ratio indicator script. This indicator was originally developed by Jack Schwager.

Volatility Finite Volume Elements Strategy This version has an important enhancement to the previous one that`s

especially useful with intraday minute charts.

Due to the volatility had not been taken into account to avoid the extra

complication in the formula, the previous formula has some drawbacks:

The main drawback is that the constant cutoff coefficient will overestimate

price changes in minute charts and underestimate corresponding changes in

weekly or monthly charts.

And now the indicator uses adaptive cutoff coefficient which will adjust to

all time frames automatically.

WARNING:

This script to change bars colors.

Implied Volatility TestThought for 42sOverview of the "Implied Volatility Suite" Indicator

The "Implied Volatility Suite" is a custom TradingView indicator written in Pine Script (version 6) designed to estimate and visualize implied volatility (IV) for any stock or asset charted on TradingView. Unlike true implied volatility derived from options pricing (e.g., via Black-Scholes), this script provides a synthetic approximation based on historical price data. It offers flexibility by allowing users to choose between two calculation methods: "Model Implied Volatility" (a statistical projection based on log-normal assumptions) or "VixFix" (a historical volatility proxy inspired by Larry Williams' VIX Fix indicator). The output is plotted as an oscillating line, similar to the Relative Strength Index (RSI), making it easy to interpret overbought/oversold conditions or trends in volatility. Users can select what to plot: raw Implied Volatility, IV Rank, IV Percentile, or Volatility Skew Index, with color-coded visuals for quick analysis (e.g., red/green thresholds for ranks/percentiles).

This indicator is particularly useful for stocks without listed options, where real IV data isn't available, or for traders seeking a quick volatility gauge integrated into their charts.

What the Code Does

At its core, the script computes a volatility metric and transforms it into one of four plottable formats, then displays it as a line chart in a separate pane below the main price chart. Here's a breakdown:

User Inputs and Configuration:

Volatility Calculation Method: Choose "Model Implied Volatility" (default) or "VixFix".

Expiry Parameters (for Model method): Minutes, Hours, and Days until expiry (default 45 days). These are combined into Days (as a float for fractional days) and converted to years (Expiry = Days / 365).

Length Parameters: For Model IV rank/percentile (default 365), VixFix length (default 252, with recommendations like 9, 22, etc.), and VixFix rank/percentile length (default 252).

Output Choice: Select "Implied Volatility", "IV Rank", "IV Percentile" (default "IV Rank"), or "Volatility Skew Index".

The script uses spot = close as the reference price.

Core Calculations:

Model Implied Volatility:

Computes log returns: LogReturn = math.log(spot / spot ) (percentage change between prior bars).

Calculates the simple moving average (Average) and standard deviation (STDEV) of log returns over an integer-rounded Days period.

Projects a time-adjusted mean (Time_Average = Days * Average) and standard deviation (Time_STDEV = STDEV * math.sqrt(Days)), assuming a random walk scaled by time.

Derives upper and lower bounds for the price at expiry: upper = spot * math.exp(Time_Average + 1 * Time_STDEV) and lower = spot * math.exp(Time_Average - 1 * Time_STDEV), representing a 1-standard-deviation range under log-normal distribution.

Computes the width of this range (width = upper - lower), halves it to get standard_dev, and annualizes it to sigma: sigma = standard_dev / (spot * math.sqrt(Expiry)).

Applies an "optimizer": If sigma > 1, halve it (to prevent unrealistically high values).

Result: IV (a decimal, e.g., 0.25 for 25% IV).

VixFix (Synthetic VIX Proxy):

Based on Larry Williams' VIX Fix formula, which estimates fear/volatility without options data: (ta.highest(spot, VIXFixLength) - low) / ta.highest(spot, VIXFixLength) * 100.

The script extends this for "upside" and "downside" by shifting the spot and low prices by multiples of standard deviation (0 for base VixFix).

VixFix is the average of upside(0) and downside(0), which are identical, yielding the standard VIX Fix value.

Volatility Skew Index:

Measures asymmetry in volatility (e.g., higher downside vol indicating fear).

For Model: Averages "upside IV" (calculated on spot shifted up by 1,2,3 * stdev) minus "downside IV" (shifted down).

For VixFix: Similar, but using shifted VIX Fix formulas for upside/downside.

Positive skew might indicate upside bias; negative indicates downside.

Rank and Percentile:

IV Rank: Normalizes the current volatility: (Volatility - ta.lowest(Volatility, Len)) / (ta.highest(Volatility, Len) - ta.lowest(Volatility, Len)) * 100.

IV Percentile: Uses ta.percentrank(Volatility, Len) to show what percentage of past values are below the current.

Len depends on the chosen method (e.g., 365 for Model).

Plotting and Visualization:

Selects VolatilityData based on user choice (e.g., IV * 100 for percentage display).

Applies colors: Red (<50) or green (>=50) for rank/percentile; aqua for skew; yellow for raw IV.

Plots as a line: plot(VolatilityData, color=col, title="Volatility Data").

The script switches logic seamlessly via conditionals (e.g., Volatility = VolCalc == "VixFix" ? VixFix : IV), ensuring the chosen method and output are used.

How It Works (Step-by-Step Execution Flow)

Initialization: Reads user inputs and sets spot = close. Computes Days (float) and DaysInt = math.round(Days) for integer lengths in TA functions.

Log Returns and Base Stats: For Model, calculates log returns, then SMA and STDEV over DaysInt.

Projection and IV Derivation: Scales stats to expiry time, computes bounds, derives sigma/IV.

Skew Functions: Defines reusable functions Model_Upside(i) and Model_Downside(i) (or VIX equivalents) to shift prices and recompute IV/VIX on shifted series.

Aggregation: Computes skew as average difference; sets Volatility to IV or VixFix.

Rank/Percentile/Skew: Applies over user-defined lengths.

Output Logic: Determines what to plot and its color based on VolatilityChoice.

Rendering: Plots the line in TradingView's indicator pane, updating bar-by-bar.

This leverages Pine Script's built-in functions like ta.sma, ta.stdev, ta.highest/lowest, and math.exp/log for efficiency.

Pros

Accessibility: Provides IV estimates for non-optionable assets (e.g., individual stocks, ETFs without options), filling a gap in TradingView's native tools.

Customization: Multiple methods (Model for forward-looking, VixFix for historical) and outputs (raw, ranked, percentile, skew) allow tailored analysis. Expiry adjustments make it suitable for options-like thinking.

Visual Simplicity: Oscillates like RSI (0-100 for ranks/percentiles), with intuitive colors, aiding quick decisions (e.g., high IV Rank might signal options selling opportunities).

No External Data Needed: Relies solely on chart data (close, low), making it lightweight and real-time.

Educational Value: Exposes users to volatility concepts like skew and log-normal projections, potentially improving trading strategies.

Flexibility in Timeframes: Works on any chart interval, with adjustable lengths for short-term (e.g., 9-bar VixFix) or long-term (365-day ranks).

Limitations

Not True Implied Volatility: This is a historical or model-based proxy, not derived from actual options prices. It may overestimate/underestimate real market-implied vol, especially during events (e.g., earnings) where options premium spikes unpredictably.

Assumptions in Model Method: Relies on log-normal distribution and constant volatility, ignoring fat tails, jumps, or mean reversion in real markets. The "optimizer" (halving sigma >1) is arbitrary and may distort results.

VixFix Variant Limitations: While based on a proven indicator, the upside/downside shifts (by stdev of prices, not returns) could be inaccurate for skew, as stdev(prices) doesn't scale properly with returns. It's backward-looking, not predictive like true IV.

Data Requirements: Needs sufficient historical bars (e.g., 365 for ranks), failing on new listings or short charts. Rounding Days to integer may introduce minor inaccuracies for fractional expiries.

Computational Intensity: Functions like repeated ta.stdev and shifts for skew (called multiple times per bar) could slow performance on long histories or low-power devices.

No Real-Time Options Integration: Doesn't pull live options data; users must manually compare to actual IV (e.g., via CBOE VIX for indices).

Potential for Misinterpretation: Oscillating line might mislead (e.g., high IV Rank doesn't always mean "sell vol"), and skew calculation is non-standard, requiring user expertise.

Version Dependency: Built for Pine v6 (as of 2025); future TradingView updates could break it, though it's straightforward to migrate.

Overall, this script is a valuable tool for volatility-aware trading but should be used alongside other indicators (e.g., ATR, Bollinger Bands) and validated against real options data when available. For improvements, consider backtesting its signals or integrating alerts for thresholds.1.9sHow can Grok help?

Shannon Entropy Volatility AnalyzerThis algorithm aims to measure market uncertainty or volatility using a Shannon entropy-based approach. 🔄📊

Entropy is a measure of disorder or unpredictability, and here we use it to evaluate the structure of price returns within a defined range of periods (window length). 🧩⏳ Thus, the goal is to detect changes to identify conditions of high or low volatility. 🔍⚡

What we seek with Shannon's formula in this algorithm is to measure market uncertainty or volatility through dynamic entropy. This measure helps us understand how unpredictable price behavior is over a given period, which is key to making informed decisions. 📈🧠

Through this formula, we calculate the level of disorder or dispersion in price returns based on their probability of occurrence, enabling us to identify moments of high or low volatility. 💡💥

Shannon Entropy Calculation 📏

• Uses probabilities to measure uncertainty in returns. 🎲

• Entropy is normalized on a scale of 0 to 100, where:

o High Entropy: Unpredictable movements (high uncertainty). ⚠️💥

•

o Low Entropy: Structured movements (low uncertainty). 📉🔒

•

• With probabilities, we measure the level of dispersion or unpredictability of returns using Shannon's entropy formula. 📊🔍

________________________________________

Indicator Usefulness 🛠️

• Identify High Volatility: When the market is unpredictable, the indicator signals "High Uncertainty." ⚡🔮

• Detect Market Stability: When the market is more predictable and structured, the indicator highlights "Low Uncertainty." 🔒🧘♂️

• Neutral Zones: Helps monitor markets without extreme conditions, enabling safer entry or exit opportunities. ⚖️🚶♂️

________________________________________

Uncertainty Zones 🌀

1. High Uncertainty: When entropy exceeds the upper threshold. 🚨🔺

2. Low Uncertainty: When entropy is below the lower threshold. 🔻💡

3. Neutral: When entropy lies between both thresholds. ⚖️🔄

________________________________________

What We Aim to Achieve with the Formula in Practice 🎯

1. Detection of Volatile Moments: Shannon’s formula helps us identify when the market is unpredictable. This is a good moment to take additional precautions, such as reducing position size or avoiding trading during high volatility phases. ⚠️📉

2. Trading Opportunities in Stable Markets: With low entropy, we can identify when the market is more predictable, favoring trend or momentum strategies with a higher chance of success. 🚀📈

3. Optimization of Risk Management: By measuring market volatility in real-time, we can adjust entry and exit strategies, tailoring risk based on the level of uncertainty detected. 🔄⚖️

________________________________________

We hope this makes it easy to interpret and use. If you have any questions or comments, please feel free to reach out to us! 📬😊

Logarithmic VolatilityIntroducing the Logarithmic Volatility Indicator , an innovative trading indicator designed especially for trading in low volatility markets. This powerful indicator is aimed at traders of all levels, from beginners to experts, and is based on fundamental concepts of mathematics and statistics applied to the financial market. Its main objective is to provide you with a better understanding of price movements and help you make more accurate investment decisions, especially in low volatility environments.

The purpose of this indicator is to find a volatility estimator that depends on the difference between High and Low, taking into account that this measure is directly proportional to volatility. A first result was obtained by Parkinson (1980) which was later improved by Garman and Klass (1980), who improved the estimator by obtaining one of minimum variance. It is the simplified version (and recommended by them) of the Garman and Klass estimator that is used to calculate the daily volatility of the asset.

The Logarithmic Volatility Indicator is a unique smoothing indicator that uses logarithms and volatility calculation of the opening, high, low and closing prices. It combines these elements to obtain an accurate representation of market volatility in situations where volatility is low.

Features

This indicator has several outstanding features designed to enhance your trading analysis in low volatility environments:

• Intraday Volatility Calculation: This innovative feature allows you to view market volatility levels in real time, providing a clear view of market fluctuations even when volatility is low.

• EMA (Exponential Moving Average) Multi Length: The indicator incorporates three different EMA lengths (Fast, Medium and Slow). This gives you a deeper and more detailed analysis of market volatility, allowing you to detect subtle changes in volatility and make more accurate predictions.

• Visual color change: The indicator uses a color change between green and red to facilitate quick interpretation of the market. Green indicates a decrease in volatility, while red indicates an increase in volatility. This feature helps you quickly identify changes in market dynamics even in periods of low volatility.

• Histogram display: In addition to the colors, the indicator can also be displayed as a histogram. This intuitive representation allows you to visually observe changes in volatility over time and detect emerging patterns or trends in markets with low volatility.

Settings

The Logarithmic Volatility Indicator allows you to customize various settings to suit your specific trading needs:

• Slow EMA length: you can select the length of the slow exponential moving average according to your preferences and trading strategies.

• Fast EMA length: Similarly, you can choose the length of the fast exponential moving average to suit your trading style.

• Average EMA length: In addition to the two EMA lengths above, this indicator offers a third EMA length for even more detailed analysis. This additional feature is especially useful when trading in markets with low volatility, as it allows you to capture subtle changes in market dynamics.

Trading

The Logarithmic Volatility Indicator is designed not only to provide you with essential information about market volatility, but also to give you clear indications on when to trade. Here's how you can use the indicator's colors to guide your trading decisions:

- Long Trading: When the fast EMA has a smaller value than the slow EMA, the indicator will change to green. This is a signal to enter a long trade. That is, you can consider buying at this point, as an increase in price is anticipated due to decreasing volatility. With volatility declining, there is a greater likelihood that the price will continue in the current direction rather than fluctuate erratically.

- b]Short Trading: On the other hand, when the fast EMA has a higher value than the slow EMA, the indicator will turn red. This is a signal to enter a short trade. In other words, you may consider selling at this point, as a decline in price is anticipated due to rising volatility. With volatility on the rise, there is a greater risk of steeper price fluctuations.

It is important to remember that, as with any indicator, the Logarithmic Volatility Indicator does not guarantee 100% success. You should always use this indicator in combination with other analytical tools and good risk management. This tool provides you with an overview of market volatility and can help you identify trading opportunities in low volatility markets, but the final decision on when and how to trade should always be based on your own analysis and judgment.

In conclusion, the Logarithmic Volatility Indicator is an essential trading tool that every trader should have in their arsenal, especially when facing low volatility markets. With its accurate volatility calculation and easy-to-understand visualization, it will help you improve your trading decisions and maximize your profits even in situations where price movements are less pronounced. Try it today and take advantage of its efficiency in low volatility environments!

---------------------------------------------------------------------------------------------------

Presentamos el Indicador de Volatilidad Logarítmica , un innovador indicador de trading diseñado especialmente para operar en mercados con baja volatilidad. Este poderoso indicador está dirigido a traders de todos los niveles, desde principiantes hasta expertos, y se basa en conceptos fundamentales de matemáticas y estadísticas aplicadas al mercado financiero. Su objetivo principal es proporcionarte una mejor comprensión de los movimientos de precios y ayudarte a tomar decisiones de inversión más precisas, especialmente en entornos de baja volatilidad.

Con este indicador se pretende encontrar un estimador de la volatilidad que dependa de la diferencia entre el High y el Low, teniendo en cuenta que esta medida es directamente proporcional a la volatilidad. Un primer resultado fue obtenido por Parkinson (1980) que posteriormente fue mejorado por Garman y Klass (1980), que mejoraron el estimador obteniendo uno de varianza mínima. Es la versión simplificada (y recomendada por ellos mismos) del estimador de Garman y Klass la que se utiliza para calcular la volatilidad diaria del activo.

El Indicador de Volatilidad Logarítmica es un indicador de suavizado único que utiliza logaritmos y el cálculo de la volatilidad de los precios de apertura, máximo, mínimo y cierre. Combina estos elementos para obtener una representación precisa de la volatilidad del mercado en situaciones donde la volatilidad es baja.

Características

Este indicador cuenta con varias características sobresalientes diseñadas para mejorar tu análisis de trading en entornos de baja volatilidad:

• Cálculo de la volatilidad intradía: Esta función innovadora te permite ver los niveles de volatilidad del mercado en tiempo real, lo que brinda una visión clara de las fluctuaciones del mercado incluso cuando la volatilidad es baja.

• EMA (Exponential Moving Average) Multi Longitud: El indicador incorpora tres longitudes diferentes de EMA (Rápida, Media y Lenta). Esto te proporciona un análisis más profundo y detallado de la volatilidad del mercado, permitiéndote detectar cambios sutiles en la volatilidad y realizar predicciones más precisas.

• Cambio de color visual: El indicador utiliza un cambio de color entre verde y rojo para facilitar la interpretación rápida del mercado. El verde indica una disminución de la volatilidad, mientras que el rojo indica un aumento de la volatilidad. Esta característica te ayuda a identificar rápidamente cambios en la dinámica del mercado incluso en períodos de baja volatilidad.

• Visualización Histograma: Además de los colores, el indicador también se puede visualizar como un histograma. Esta representación intuitiva te permite observar de manera visual los cambios en la volatilidad a lo largo del tiempo y detectar patrones o tendencias emergentes en mercados con baja volatilidad.

Ajustes

El Indicador de Volatilidad Logarítmica te permite personalizar varios ajustes para adaptarlos a tus necesidades de trading específicas:

• Longitud de EMA lenta: Puedes seleccionar la longitud de la media móvil exponencial lenta según tus preferencias y estrategias de trading.

• Longitud de EMA rápida: De manera similar, puedes elegir la longitud de la media móvil exponencial rápida para ajustarla a tu estilo de trading.

• Longitud de EMA media: Además de las dos longitudes de EMA anteriores, este indicador ofrece una tercera longitud de EMA para un análisis aún más detallado. Esta característica adicional es especialmente útil cuando operas en mercados con baja volatilidad, ya que te permite capturar cambios sutiles en la dinámica del mercado.

Operativa

El Indicador de Volatilidad Logarítmica está diseñado no solo para brindarte información esencial sobre la volatilidad del mercado, sino también para ofrecerte indicaciones claras sobre cuándo operar. Aquí te explicamos cómo puedes utilizar los colores del indicador para guiar tus decisiones de trading:

• Operativa en Largo: Cuando la EMA rápida tiene un valor más pequeño que la EMA lenta, el indicador cambiará a color verde. Esta es una señal para entrar en una operación en largo. Es decir, puedes considerar comprar en este punto, ya que se anticipa un aumento en el precio debido a la disminución de la volatilidad. Con la volatilidad en descenso, existe una mayor probabilidad de que el precio continúe en la dirección actual en lugar de fluctuar erráticamente.

• Operativa en Corto: Por otro lado, cuando la EMA rápida tiene un valor mayor que la EMA lenta, el indicador se tornará rojo. Esta es una señal para entrar en una operación en corto. En otras palabras, puedes considerar vender en este punto, ya que se anticipa una disminución en el precio debido al aumento de la volatilidad. Con la volatilidad en ascenso, existe un mayor riesgo de fluctuaciones de precio más pronunciadas.

Es importante recordar que, como con cualquier indicador, el Indicador de Volatilidad Logarítmica no garantiza un éxito del 100%. Siempre debes usar este indicador en combinación con otras herramientas de análisis y una buena gestión de riesgos. Esta herramienta te proporciona una visión general de la volatilidad del mercado y puede ayudarte a identificar oportunidades de trading en mercados con baja volatilidad, pero la decisión final de cuándo y cómo operar siempre deberá basarse en tu propio análisis y juicio.

En conclusión, el Indicador de Volatilidad Logarítmica es una herramienta de trading esencial que todo trader debe tener en su arsenal, especialmente cuando se enfrenta a mercados con baja volatilidad. Con su cálculo preciso de la volatilidad y su visualización fácil de entender, te ayudará a mejorar tus decisiones de trading y a maximizar tus ganancias incluso en situaciones donde los movimientos de precios son menos pronunciados. ¡Pruébalo hoy mismo y aprovecha su eficiencia en entornos de baja volatilidad!

SV Volatility Indicator BasicThe SV Volatility Indicator Basic in TradingView calculates and visualizes daily and average volatility over specified periods using three lines. Here’s what it does:

1. Daily Volatility Calculation. The indicator computes daily volatility as the percentage difference between the high and low prices relative to the closing price:

2. 30-day Moving Average of Volatility. A simple moving average (SMA) is applied to the daily volatility values over the last 30 days to smooth short-term fluctuations.

3. 90-day Moving Average of Volatility. Similarly, an SMA is calculated over the last 90 days to provide a longer-term view of volatility trends.

4. Visualization:

Three lines are plotted:

Red line: Represents the daily volatility in percentage terms.

Blue line: Displays the 30-day moving average of volatility.

Green line: Shows the 90-day moving average of volatility.

This indicator helps traders analyze market volatility by providing both immediate (daily) and smoothed (30-day and 90-day) measures, aiding in trend identification and risk assessment.

Uptrick: Crypto Volatility Index** Crypto Volatility Index(VIX) **

Overview

The Crypto Volatility Index (VIX) is a specialized technical indicator designed to measure the volatility of cryptocurrency prices. Leveraging advanced statistical methods, including logarithmic returns and variance, the Crypto VIX offers a refined measure of market fluctuations. This approach makes it particularly useful for traders in the highly volatile cryptocurrency market, providing insights that traditional volatility indicators may not capture as effectively.

Purpose

The Crypto VIX aims to deliver a nuanced understanding of market volatility, tailored specifically for the cryptocurrency space. Unlike other volatility measures, the Crypto VIX employs sophisticated statistical methods to reflect the unique characteristics of cryptocurrency price movements. This makes it especially valuable for cryptocurrency traders, helping them navigate the inherent volatility of digital assets and manage their trading strategies and risk exposure more effectively.

Calculation

1. Indicator Declaration

The Crypto VIX is plotted in a separate pane below the main price chart for clarity:

indicator("Crypto Volatility Index (VIX)", overlay=false, shorttitle="Crypto VIX")

2. Input Parameters

Users can adjust the period length for volatility calculations:

length = input.int(14, title="Period Length")

3. Calculating Daily Returns

The daily returns are calculated using logarithmic returns:

returns = math.log(close / close )

- **Logarithmic Returns:** These returns provide a normalized measure of price changes, making it easier to compare returns over different periods and across different assets.

4. Average Return Calculation

The average return over the specified period is computed with a Simple Moving Average (SMA):

avg_return = ta.sma(returns, length)

5. Variance Calculation

Variance measures the dispersion of returns from the average:

variance = ta.sma(math.pow(returns - avg_return, 2), length)

- Variance : This tells us how much the returns deviate from the average, giving insight into how volatile the market is.

6. Standard Deviation (Volatility) Calculation

Volatility is derived as the square root of the variance:

volatility = math.sqrt(variance)

- Standard Deviation : This provides a direct measure of volatility, showing how much the price typically deviates from the mean return.

7. Plotting the Indicator

The volatility and average return are plotted:

plot(volatility, color=#21f34b, title="Volatility Index")

plot(avg_return, color=color.new(color.red, 80), title="Average Return", style=plot.style_columns)

Practical Examples

1. High Volatility Scenario

** Example :** During significant market events, such as major regulatory announcements or geopolitical developments, the Crypto VIX tends to rise sharply. For instance, if the Crypto VIX moves from a baseline level of 0.2 to 0.8, it indicates heightened market volatility. Traders might see this as a signal to adjust their strategies, such as reducing position sizes or setting tighter stop-loss levels to manage increased risk.

2. Low Volatility Scenario

** Example :** In a stable market, where prices fluctuate within a narrow range, the Crypto VIX will show lower values. For example, a drop in the Crypto VIX from 0.4 to 0.2 suggests lower volatility and stable market conditions. Traders might use this information to consider longer-term trades or take advantage of potential consolidation patterns.

Best Practices

1. Combining Indicators

- Moving Averages : Use the Crypto VIX with moving averages to identify trends and potential reversal points.

- Relative Strength Index (RSI): Combine with RSI to assess overbought or oversold conditions for better entry and exit points.

- Bollinger Bands : Pair with Bollinger Bands to understand volatility relative to price movements and spot potential breakouts.

2. Adjusting Parameters

- Short-Term Trading : Use a shorter period length (e.g., 7 days) to capture rapid volatility changes suitable for day trading.

- Long-Term Investing : A longer period length (e.g., 30 days) provides a smoother view of volatility, helping long-term investors navigate market trends.

Backtesting and Performance Insights

While specific backtesting data for the Crypto VIX is not yet available, the indicator is built on established principles of volatility measurement, such as logarithmic returns and standard deviation. These methods are well-regarded in financial analysis for accurately reflecting market volatility. The Crypto VIX is designed to offer insights similar to other effective volatility indicators, tailored specifically for the cryptocurrency markets. Its adaptation to digital assets and ability to provide precise volatility measures underscore its practical value for traders.

Originality and Uniqueness

The Crypto Volatility Index (VIX) distinguishes itself through its specialized approach to measuring volatility in the cryptocurrency markets. While the concepts of logarithmic returns and standard deviation are not new, the Crypto VIX integrates these methods into a unique framework designed specifically for digital assets.

- Tailored Methodology : Unlike generic volatility indicators, the Crypto VIX is adapted to the unique characteristics of cryptocurrencies, providing a more precise measure of price fluctuations that reflects the inherent volatility of digital markets.

- Enhanced Insights : By focusing on cryptocurrency-specific price behavior and incorporating advanced statistical techniques, the Crypto VIX offers insights that traditional volatility indicators might miss. This makes it a valuable tool for traders navigating the complex and fast-moving cryptocurrency landscape.

- Innovative Application : The Crypto VIX combines established financial metrics in a novel way, offering a fresh perspective on market volatility and contributing to more effective risk management and trading strategies in the cryptocurrency space.

Summary

The Crypto Volatility Index (VIX) is a specialized tool for measuring cryptocurrency market volatility. By utilizing advanced statistical methods such as logarithmic returns and standard deviation, it provides a detailed measure of price fluctuations. While not entirely original in its use of these methods, the Crypto VIX stands out through its tailored application to the unique characteristics of the cryptocurrency market. Traders can use the Crypto VIX to gauge market risk, adjust their strategies, and make informed trading decisions, supported by practical examples, best practices, and clear visual aids.

EGARCH Volatility Estimator

EGARCH Volatility Estimator (EVE)

Overview:

The EGARCH Volatility Estimator (EVE) is a Pine Script indicator designed to quantify market volatility using the Exponential Generalized Autoregressive Conditional Heteroskedasticity (EGARCH) model. This model captures both symmetric and asymmetric volatility dynamics and provides a robust tool for analyzing market risk and trends.

Key Features:

Core EGARCH Formula:

ln(σ t 2 )=ω+α(∣ϵ t−1 ∣+γ⋅ϵ t−1 )+β⋅ln(σ t−1 2 )

ω (Omega): Captures long-term baseline volatility.

α (Alpha): Measures sensitivity to recent shocks.

γ (Gamma): Incorporates asymmetric effects (e.g., higher volatility during market drops).

β (Beta): Reflects the persistence of historical volatility.

The formula computes log-volatility, which is then converted to actual volatility for interpretation.

Standardized Returns:

The script calculates daily log-returns and standardizes them to measure deviations from expected price changes.

Percentile-Based Volatility Analysis:

Tracks the percentile rank of current volatility over a historical lookback period.

Highlights high, medium, or low volatility zones using dynamic background colors.

Dynamic Normalization:

Maps volatility into a normalized range ( ) for better visual interpretation.

Uses color gradients (green to red) to reflect changing volatility levels.

SMA Integration:

Adds a Simple Moving Average (SMA) of either EGARCH volatility or its percentile for trend analysis.

Interactive Display:

Displays current volatility and its percentile rank in a table for quick reference.

Includes high (75%) and low (25%) volatility threshold lines for actionable insights.

Applications:

Market Risk Assessment: Evaluate current and historical volatility to assess market risk levels.

Quantitative Strategy Development: Incorporate volatility dynamics into trading strategies, particularly for options or risk-managed portfolios.

Trend and Momentum Analysis: Use normalized or smoothed volatility trends to identify potential reversals or breakouts.

Asymmetric Volatility Detection: Highlight periods where downside or upside volatility dominates.

Visualization Enhancements:

Dynamic colors and thresholds make it intuitive to interpret market conditions.

Percentile views provide relative volatility context for historical comparison.

This indicator is a versatile tool for traders and analysts seeking deeper insights into market behavior, particularly in volatility-driven trading strategies.

Historical VolatilityHistorical Volatility Indicator with Custom Trading Sessions

Overview

This indicator calculates **annualized Historical Volatility (HV)** using logarithmic returns and standard deviation. Unlike standard HV indicators, this version allows you to **customize trading sessions and holidays** for different markets, ensuring accurate volatility calculations for options pricing and risk management.

Key Features

✅ Custom Trading Sessions - Define multiple trading sessions per day with precise start/end times

✅ Multiple Markets Support - Pre-configured for US, Russian, European, and crypto markets

✅ Clearing Periods Handling - Account for intraday clearing breaks

✅ Flexible Calendar - Set trading days per year for different countries

✅ All Timeframes - Works correctly on intraday, daily, weekly, and monthly charts

✅ Info Table - Optional display showing calculation parameters

How It Works

The indicator uses the classical volatility formula:

σ_annual = σ_period × √(periods per year)

Where:

- σ_period = Standard deviation of logarithmic returns over the specified period

- Periods per year = Calculated based on actual trading time (not calendar time)

Calculation Method

1. Computes log returns: ln(close / close )

2. Calculates standard deviation over the lookback period

3. Annualizes using the square root rule with accurate period count

4. Displays as percentage

Settings

Calculation

- Period (default: 10) - Lookback period for volatility calculation

Trading Schedule

- Trading Days Per Year (default: 252) - Number of actual trading days

- USA: 252

- Russia: 247-250

- Europe: 250-253

- Crypto (24/7): 365

- Trading Sessions - Define trading hours in format: `hh:mm:ss-hh:mm:ss, hh:mm:ss-hh:mm:ss`

Display

- Show Info Table - Shows calculation parameters in real-time

Market Presets

United States (NYSE/NASDAQ)

Trading Sessions: 09:30:00-16:00:00

Trading Days Per Year: 252

Trading Minutes Per Day: 390

Russia (MOEX)

Trading Sessions: 10:00:00-14:00:00, 14:05:00-18:40:00

Trading Days Per Year: 248

Trading Minutes Per Day: 515

Europe (LSE)

Trading Sessions: 08:00:00-16:30:00

Trading Days Per Year: 252

Trading Minutes Per Day: 510

Germany (XETRA)

Trading Sessions: 09:00:00-17:30:00

Trading Days Per Year: 252

Trading Minutes Per Day: 510

Cryptocurrency (24/7)

Trading Sessions: 00:00:00-23:59:59

Trading Days Per Year: 365

Trading Minutes Per Day: 1440

Use Cases

Options Trading

- Compare HV vs IV - Historical volatility compared to implied volatility helps identify mispriced options

- Volatility mean reversion - Identify when volatility is unusually high or low

- Straddle/strangle selection - Choose optimal strikes based on historical movement

Risk Management

- Position sizing - Adjust position size based on current volatility

- Stop-loss placement - Set stops based on expected price movement

- Portfolio volatility - Monitor individual asset volatility contribution

Market Analysis

- Regime identification - Detect transitions between low and high volatility environments

- Cross-market comparison - Compare volatility across different assets and markets

Why Accurate Trading Hours Matter

Standard HV indicators assume 24-hour trading or use simplified day counts, leading to significant errors in annualized volatility:

- 5-minute chart error : Can be off by 50%+ if using wrong period count

- Options pricing impact : Even 2-3% HV error affects option values substantially

- Intraday vs overnight : Correctly excludes non-trading periods

This indicator ensures your HV calculations match the methodology used in professional options pricing models.

Technical Notes

- Uses actual trading minutes, not calendar days

- Handles multiple clearing periods within a single trading day

- Properly scales volatility across all timeframes

- Logarithmic returns for more accurate volatility measurement

- Compatible with Pine Script v6

Author Notes: This indicator was designed specifically for options traders who need precise volatility measurements across different global markets. The customizable trading sessions ensure your HV calculations align with actual market hours and industry-standard options pricing models.

Alpha Trading - Alpha Volatility Quality - Coder WolvesHere at Alpha Trading if we find something that works, that aligns with our philosophy then after thorough testing by the Alpha Wolves, we add some of our own secret sauce and then provide it back to the community as a free indicator.

The Alpha Volatility Quality is one such indicator and is largely influenced by the original work of Thomas Stridsman, and more recently people such as Lazy Bear.

The original Volatility Quality Index (VQI ), by Thomas Stridsman, can help you identify better trade opportunities by distinguishing between good and bad volatility. Formula for the system discussed in Advanced Strategies (p. 56) / August 2002 Active Trader Magazine.

Thomas, or Mr Stridesman to some, suggested to buy when VQI has increased in the previous 10 bars (use the SMAs ) and sell when it has decreased in the previous 10 bars.

As the indicator is mostly directional, we have found that it's best used in conjunction with other indicators from the Alpha Trading Free Chart.

When you first load up the Alpha Volatility Quality, you will see a green and red line and a white line.

Green and Red Line = Alpha Volatility Quality

White Line = AVQ Slow MA

Alpha Trading – Alpha Volatility Quality

At Alpha Trading, we wanted to add some additional advanced options, so we also allow for additional smoothing to be applied, to make the indicator more tradable. If that wasn’t enough, we also added deviation bands.

Default Out of the Box Settings

When you first load up the indicator, you will see a green / red line and a white line

Green and Red Line = Alpha Volatility Quality

White Line = AVQ Slow MA

There is also a Fast MA input you can toggle on.

If you prefer you can display the Alpha Volatility Quality in Columns instead of a line.

Basic Trade Signal

Long – Consider a long when the AVQ Line goes above the Moving Average (i.e. The AVQ Green Line goes above the white MA)

Short – Consider a short when the AVQ line goes below the Moving Average(i.e. The AVQ Red Line goes below the white MA)

The Chart below is showing trades based on Good and Bad volatility. We have also added VQI-LB to show the Dominance and more versatile AT-AVQ.

Kaisar Volatility TableMeasures the volatility of an asset or a stock. User can use the lookback input to measure their required volatility. The indicator also provides daily volatility and annualized volatility.

USDT.D Volatility TrackerUSDT.D Volatility Tracker

Description:

This script is designed to track the volatility of USDT.D (US Dollar in cryptocurrency) on the TradingView platform. It uses a moving average and deviation from it to generate buy and sell signals, helping traders visualize changes in volatility and make informed decisions.

Input Parameters:

maPeriod: The period of the moving average (default 120). This parameter allows users to adjust the length of the period used to calculate the moving average.

devThreshold: The deviation threshold (default 0.6). This parameter defines the level of deviation that will trigger buy or sell signals.

Data Request:

The script requests closing data for USDT.D using the request.security function, allowing it to retrieve up-to-date data on the selected timeframe.

Moving Average and Deviation Calculation:

An exponential moving average (EMA) is used to calculate the deviation from the moving average, enabling the identification of current volatility.

Deviation Line Display:

The deviation rate line is displayed on the chart, allowing users to visually track changes in volatility.

Signal Generation:

If the deviation exceeds the set threshold (devThreshold), a buy signal is generated (green background).

If the deviation falls below the negative threshold (-devThreshold), a sell signal is generated (red background).

Visual Signals:

Buy signals are displayed on the chart as green triangles, while sell signals are displayed as red triangles. This helps traders quickly identify potential entry and exit points.

[Mustang Algo] VIF - Volatility Indicator Freemium

The VIF - Volatility Indicator Freemium is a powerful tool designed to capture volatility-driven price movements and generate actionable trading signals. It offers a clear, color-coded visual representation of market trends based on volatility and price movement. The indicator includes key features to help traders identify strong buy and sell opportunities with clear alerts for both bullish and bearish signals.

Key Features:

Volatility Indicator Freemium (VIF):

Calculates volatility over a specified period using the difference between the open and close prices.

Generates signals based on the relationship between volatility and an exponential moving average (EMA).

Strong Buy/Sell signals: Triggered when volatility exceeds a threshold and the price crosses above/below the EMA.

Weaker signals: When volatility is lower but still shows trends in relation to the EMA.

Customizable Inputs:

Resolution: Select different timeframes for signal generation to adapt the indicator to different market conditions.

Repainting: Option to enable or disable repainting based on your preference for signal stability.

VIF Length & Threshold: Fine-tune the sensitivity of the volatility indicator by adjusting the length and threshold parameters.

Color-Coded Signals:

Bright Green (Strong Bullish): High volatility and price above the EMA.

Light Green (Weak Bullish): Lower volatility but price still above the EMA.

Bright Red (Strong Bearish): High volatility and price below the EMA.

Light Red (Weak Bearish): Lower volatility but price still below the EMA.

Neutral (Gray): When neither bullish nor bearish conditions are strong.

Real-Time Alerts:

Strong Buy/Sell Alerts: Receive notifications for significant bullish or bearish changes in market volatility.

Weaker Buy/Sell Alerts: Notifications for changes in market direction with moderate volatility levels.

Bar Coloring & Background Customization:

Option to color bars based on the detected signals.

Background color also adjusts according to the volatility signal, offering a visual guide for quickly identifying market conditions.

Indicator Statistics & Alerts:

Built-in alert conditions for Strong Buy/Sell Signals and regular Buy/Sell Signals, allowing traders to react to market changes in real time.

Premium Version Coming Soon:

An upcoming premium version will include advanced filtering options, improved risk management features, and enhanced customization for professional traders.

This Freemium version is ideal for traders seeking to gain insights into market volatility and momentum. Stay tuned for the premium version that will introduce additional exclusive features, offering even greater control over your trading strategies.

[ADOL_]Volatility WarningENG)

What if you know when to trade? What are the criteria to differentiate between buying and selling and not buying and selling?

If you can do this, you will be able to increase the sophistication of your trading.

When volatility occurs, the number of participants in the market increases, the volume of trade increases, and direction arises.

Therefore, it is important to understand volatility.

This is a volatility reminder. When variability occurs, it alerts you with the color of the background.

Volatility doesn't set the direction. It is recommended to combine it with an indicator that allows you to analyze the price.

It was created according to the basic principle of a chart that diverges when converged and converges when divergent.

A warning sign about volatility appears in the background just before the transition from convergence to divergence before volatility occurs.

Logic)

reflects the main ratio of trend-based Fibonacci time. The main ratio is the ratio of 618 and 1.

The chart consists of a price axis and a time axis. The trend-based Fibonacci time among the tools to set the time axis is

It is a method of predicting the next inflection through the ratio of the next interval between the highs and the lows, the lows and the highs.

The inflection time is indexed by +a to the logic that reflects this concept.

See past ideas for a way to go about trend-based Fibonacci times.

Logic Example)

This is an example of a trend-based Fibonacci time.

Timeframe)

Applicable to all time frames.

Applicable market)

Applicable to all markets.

Examples of market application)

NASDAQ

Korean stocks (ex: Samsung Electronics)

Overseas stocks (e.g. TSLA)

Etc

Option)

You can use the filtering function.

Turn on filtering to show more restrictive intervals.

check filtering = application to double filtering

non-check filtering = basic filtering

Alert)

Alert function has been added.

Trading method)

1. Draw a trend line

The occurrence of volatility reflects the charting principle of convergence and divergence.

It helps to determine whether or not it deviates from the trend line. Met after a volatility warning

The trend line is the period at which there is a high probability of deviation.

2. Support/resistance

If the volatility increases in the section where support/resistance occurs, the increased volatility

The likelihood of a breakthrough will increase. Find and trade horizontal racks.

3. Combine with your own price index

This is a warning about the time base, so each trader

You can improve your judgment by combining it with the price axis indicators you use,

such as Lee Pyeong-seon, VWAP, and so on.

The above tool is only an example. It is not an absolute indicator, so try to combine and combine with more tools.

4. Note

Any trade decisions you make are entirely your own responsibility.

5. How to use

Please fill out the form by referring to the signature below.

KOR)

거래할 타이밍을 알 수 있다면? 매매할 때와 매매를 하지 않을 때를 구분할 기준이 있다면?

이것을 할 수 있다면 거래를 하는데 정교함을 높일 수 있을 것입니다.

변동성이 발생할 때 시장 참여자가 늘어나고, 거래량이 증가하며, 방향성이 생깁니다.

따라서 변동성을 파악하는 것은 중요한 일입니다.

해당 지표는 변동성 알림 입니다. 변동성이 발생할 때, 배경의 색깔로 경고를 보내줍니다.

변동성은 방향성을 정해주지 않습니다. 가격을 분석할 수 있는 지표와 함께 결합 할 것을 추천합니다.

수렴하면 발산하고, 발산하면 수렴하는 차트의 기본원리에 맞춰 만들어졌습니다.

변동성이 발생하기 전에 수렴에서 발산으로 넘어가기 직전에 변동성에 대한 경고표시가 배경으로 나타납니다.

원리)

추세기반 피보나치 시간의 주요 비율을 반영합니다. 주요비율이란, 618과 1의 비율입니다.

차트는 가격축과 시간축으로 구성되어 있습니다. 시간축을 잡는 도구중 추세기반 피보나치 시간은

고점과 저점, 저점과 고점을 이은 다음 구간의 비율을 통해 다음 변곡을 예측하는 방법입니다.

이같은 개념을 반영하는 원리에 +a 하여 변곡시간을 지표화 하게 됩니다.

추세기반 피보나치 시간에 관한 방법은 지난 아이디어를 참고하십시오.

원리 예시)

추세기반 피보나치 시간의 예시 입니다.

타임프레임)

모든 시간프레임에 적용 가능합니다.

적용시장)

모든 시장에 적용 가능합니다.

시장적용의 예시)

나스닥

한국주식(예 : 삼성전자)

해외주식(예 : TSLA)

기타 등등

알림)

얼러트 기능이 추가되었습니다.

옵션)

필터링 기능을 사용할 수 있습니다.

필터링을 켜면 더 제한적인 구간을 보여줍니다.

check filtering = 이중 필터링 적용

non-check filtering = 기본 필터링

매매방법)

1. 추세선 긋기

변동성이 발생한다는 것은 수렴과 발산의 차트 기본원리를 반영합니다.

추세선을 이탈하는지 여부를 판단하는데 도움이 됩니다. 변동성 경고가 발생한 이후 만나는

추세선은 이탈할 가능성이 높은 타이밍의 구간이 됩니다.

2. 지지/저항

지지/저항이 발생한 구간에서 변동성이 증가할 경우, 증가한 변동성으로 인해

돌파가 발생할 가능성이 높아집니다. 수평매물대를 찾아서 거래합니다.

3. 자신이 사용하는 가격지표와 결합

이것은 시간축에 대한 경고이므로, 트레이더 각자가 자신이 사용하는

이평선, VWAP 등등 자신이 사용하는 가격축 지표에 결합하여 판단력을 높일 수 있습니다.

위의 도구는 예시일 뿐입니다. 절대적인 지표가 아니므로, 더 많은 도구와 조합하고 결합하기 위해 노력하십시오.

4. 참고

귀하가 내리는 모든 거래 결정은 전적으로 귀하의 책임입니다.

5. 사용방법

하단의 시그니처를 참고하여 폼을 작성하십시오.

Range-Weighted Volatility (Comparable)I wrote an indicator to measure volatility inside a range. It’s extremely useful for choosing a trading pair for grid strategies, because it lets you quickly, easily, and fairly identify which asset is the volatility leader. It measures volatility “fairly” relative to the asset’s trading range, not just by absolute price changes.

For example: if an asset trades in a 50–100 range and over a week it moves many, many times between 52 and 98, then it’s highly volatile. But if another asset trades in a 50–1000 range and makes the same 52–98 moves, its volatility is actually low — because the “weight” of that movement relative to the full range is small. The indicator accounts for this “movement weight” relative to the range, then sums these weights into a single number. That number makes it easy to judge whether an asset is suitable for a grid strategy.

That’s exactly what grids need: not just high volatility, but high volatility within a narrow range.

Settings: the Window (bars) field defines how many bars are used to calculate volatility. On a 5-minute chart, one week is 2016 bars (2460/57). By default, the script calculates over 30 days on 5-minute charts. The script also allows you to set a second symbol for comparison, so you can see both results on the same chart.

Написал индикатор для определения волатильности в диапазоне, очень-очень полезно для выбора торговой пары на гриде, позволяет легко и быстро и честно определить лидера по волатильности, при этом определяет ее "честно", относительно торгового диапазона, а не просто изменения цены.

Например если актив торгуется в диапазоне 50-100 и за неделю много-много раз сходил 52-98, то это очень волатильный актив, и в то же время если актив торгуется в диапазоне 50-1000 и сходил так же 52-98, то это будет низко волатильный актив, т.е. учитывается "вес" движения относительно диапазона и данные "веса" суммируются в одну единую цифру по которой и можно оценивать насколько актив подходит под грид стратегию.

А ведь именно это для гридов и нужно, не просто высокая волатильность, а именно высокая волатильность в узком диапазоне.

Касательно настроек , в поле Windows (bars) задается количество баров по которым скрипт будет считать волатильность, на 5-ти минутки неделя это 2016 (24*60/5*7), стандартно скрипт считает за 30 дней на 5-ти минутки. + в самом скрипте можно указать вторую пару для сравнения чтоб на одном графике увидеть результат.

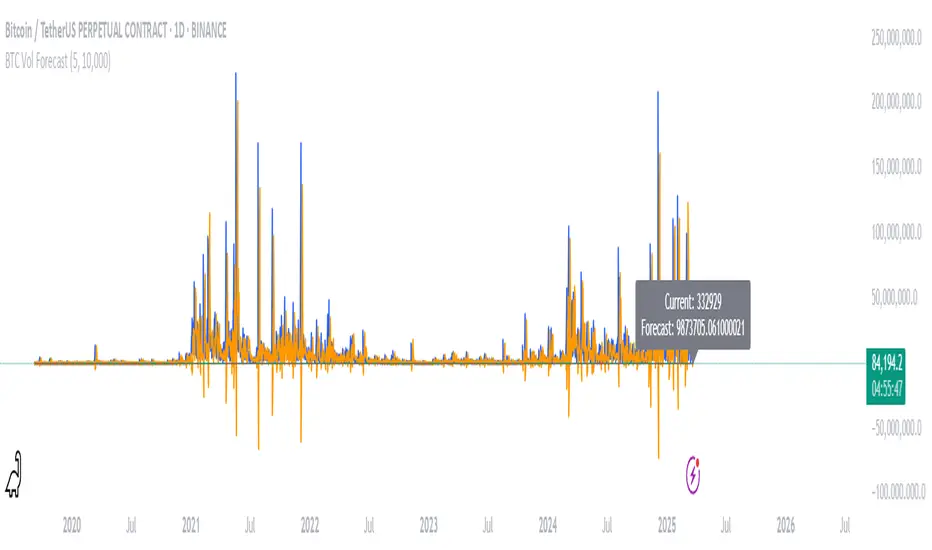

BTC Volatility ForecastThe "BTC Volatility Forecast" indicator is designed to help traders anticipate Bitcoin (BTC) price volatility by analyzing historical daily price ranges and projecting future fluctuations. Inspired by advanced volatility forecasting studies, it calculates an approximate realized variance using the squared difference between each day’s high and low prices. By applying a simple linear regression model over the past five days of variance data (customizable via the "Lag Period" input), the indicator provides a forecast for the next day’s volatility. This makes it a valuable tool for BTC traders looking to gauge potential market turbulence and adjust their strategies accordingly.

On the chart, the indicator displays two lines: a blue solid line representing the current realized variance and an orange line showing the forecasted volatility for the upcoming day. Traders can set a "Volatility Threshold" to trigger alerts when the forecast exceeds a specified level, aiding in risk management or trade planning. A debug label on the last bar also shows the exact current and forecasted values for quick reference. While this version uses daily data for simplicity, it captures the essence of volatility prediction and can be a starting point for understanding BTC market dynamics—perfect for both novice and experienced traders on TradingView.

Taylorsan Realised VolatilityThis is a fairly simple indicator providing realised (historical) volatility for any ticker

It world by following the usual routine way of calculating daily volatility.

ie 30 day std dev of price, annualised.

The default annualisation is 252 days (ie, trading days).

Change the parameters to suit for other assets e.g. for crypto change to 365

Also included a simple moving average for smoothed trend.

Remember volatility happens to both the upside and downside. Also remember 'risk happens slowly and all at once', so as such moves to the downside tend to be sharper and hence where most of the volatility shows up.

Also consider it's not the level that matters, it's more the 'zone' or 'bucket'. For instance, for the S&P 500:

Volatility under 20 is considered very attractive and broadly bullish

Volatility between 20 and 30 is considered investible, but probably choppy.

Volatility above 30 is considered un-investable.

It's the direction of the move from one bucket to another that you should be observing. e.g. a move from 35 to sub 20 for the S&P would mean a great return.

QSL Rolling Annualized VolatilityThis script calculates the rolling annualized volatility of an asset, helping traders measure how much its returns fluctuate over time. It uses logarithmic daily returns and computes the standard deviation over a custom lookback period (default: 252 trading days = 1 year) to capture historical volatility. The result is scaled to an annualized figure by multiplying by √252, making it comparable across different timeframes.

🔹 Key Features:

Customizable Lookback Period: Set in days to fit different trading strategies.

Annualized Output: Expresses volatility in yearly terms for consistency with financial models.

Rolling Calculation: Continuously updates to reflect recent market conditions.

Clear Visualization: Plots volatility as a time-series indicator and displays the latest value with a label.

This tool is ideal for risk management, position sizing, and strategy optimization in quantitative trading. 🚀

Positive Volatility and Volume GaugeThis is my first published script. It is a real volatility gauge that allows the user to see the real volatility of a given candle on the 15-min time frame. It also has the SMA of real volatility and volume available.

It provides the user to identify high volatility points that can lead to reversals back to the mid-point of said high volatility.

You can change the threshold of the signal line. For the 15-min time frame, I suggest that the 1.5-2.5 threshold be used for the best view.

Good luck and let me know if you have any questions or suggestions. I'm always open to learning.

Thank you!

fake volume (normalized volatility)fake volume is not volume.

This is open source. check it my source.

there is no 'volume'

but look at that indicator, it really looks like volume.

- how is it possible?

i tried to calculate volatility. and this is it.

usually volatility = volume. so this is not a supprise.

- how is it helpful? (how can we use this?)

compare with real volume. sometime it make difference.

if "fake volume" is high, but real volme is not high,

and that means the price may not peak( nor bottom )

also it doesnt have influence.

you can use this indicator for something like score, index. that doesnt have volume.

ex: SPX, KOSPI

======================================

가짜볼륨은 볼륨이 아닙니다.

소스코드를 보면 알겠지만 볼륨을 사용하지 않았습니다.

하지만 굉장히 볼륨처럼 보입니다.

- 어째서 이게 가능한가?

저는 시장변동률을 수치화 하려고 했고 그걸 가시화했을 뿐 입니다.

일반적으로 시장변동률은 거래량과 같이 움직입니다.

그러니 딱히 놀라운 현상은 아닙니다.

- 이것을 어떻게 쓰나요? 어떤 도움이 되나요?

가끔 볼륨이랑 가짜볼륨이 다를 수가 있습니다.

만약 볼륨이 가짜볼륨보다 작다면, 그 지점은 중요 고점이나 저점이 아니겠지요.

(사실 이런 기법들을 연구하면서 만들어진 저의 지표 shock detector가 따로 있습니다.)

볼륨이 없는 인덱스나 점수 계열을 보실 때에 볼륨 대신에 아쉬운대로 이걸 사용해볼 수도 있겠습니다.