RSI and Dev Advanced Volatility IndexEnglish Explanation of the "RSI and Dev Advanced Volatility Index" Pine Script Code

Understanding the Code

Purpose:

This Pine Script code creates a custom indicator that combines the Relative Strength Index (RSI) and Deviation (DEV) to provide insights into market volatility.

Key Components:

* Deviation (DEV): Calculates the difference between the closing price and the 10-period simple moving average. This measures the extent to which the price deviates from its recent average, indicating volatility.

* RSI: The traditional RSI is then applied to the calculated deviations. This helps to smooth the data and identify overbought or oversold conditions in terms of volatility.

Calculation Steps:

* Deviation Calculation: The difference between the closing price and its 10-period simple moving average is calculated.

* RSI Calculation: The RSI is calculated on the deviations, providing a measure of the speed and change of volatility relative to recent volatility changes.

* Plotting:

* The RSI of the deviations is plotted on the chart.

* Horizontal lines are plotted at 50, 0, and 110 to visually represent different volatility zones.

* The area between the lines is filled with color to highlight low and high volatility regions.

Interpretation and Usage

* Volatility Analysis:

* High Volatility: When the RSI is above 50, it indicates high volatility, suggesting the market might be in a consolidation or trend reversal phase.

* Low Volatility: When the RSI is below 50, it indicates low volatility, suggesting a relatively calm market.

* Trading Signals:

* Buy Signal: When the RSI crosses above 50 from below, it might signal increasing volatility, which could be a buying opportunity.

* Sell Signal: When the RSI crosses below 50 from above, it might signal decreasing volatility, which could be a selling opportunity.

* Risk Management:

* By monitoring volatility, traders can better manage their risk. During periods of high volatility, traders might reduce their position size or adopt more conservative strategies.

Advantages

* Comprehensive: Combines RSI and DEV for a more holistic view of volatility.

* Sensitivity: Quickly responds to changes in market volatility.

* Visual Clarity: Color-coded zones provide a clear visual representation of different volatility levels.

Limitations

* Parameter Sensitivity: The indicator's performance is sensitive to parameter changes, such as the lookback period for the moving average.

* Lag: Like most technical indicators, it has some lag and might not capture every market movement.

* Not Predictive: It can only indicate current and past volatility, not future movements.

Summary

This custom indicator offers a valuable tool for analyzing market volatility. By combining RSI and DEV, it provides a more nuanced perspective on price fluctuations. However, it should be used in conjunction with other technical indicators and fundamental analysis for more robust trading decisions.

Key points to remember:

* Higher RSI values indicate higher volatility.

* Lower RSI values indicate lower volatility.

* Crossovers of the RSI line above or below 50 can provide potential trading signals.

* The indicator should be used in conjunction with other analysis tools for a more complete picture of the market.

Cari skrip untuk "Volatility"

Uber VQ - Volatility Quality Index [UTS]Name: Uber VQI - Volatility Quality Index

Created: 2022/11/22

Copyright: © UberTradingSystems

Description:

The volatility quality index was first introduced by Thomas Stridsman in Technical Analysis of Stocks and Commodities magazine in the August 2002 edition.

This powerful indicator points out the difference between bad and good volatility in order to identify better trade opportunities in the market.

It is suggested to use this indicator as a confirmation signal together with the other indicators in your system.

General Usage

Stridsman suggested buying (or "to go long") when VQ has increased in the previous 10 bars and selling (or "to go short") when it has decreased in the previous 10 bars.

This indicator has been updated to reflect its modern iterations. One of the following signals are choosable trading signal generator:

VQ Sum

Short MA

Long MA

All three signal triggering conditions can selectively be drawn on the indicator for study and reference purposes.

In addition, generated buy and sell signals can be drawn on the indicator and are modifiable too.

Alerts

To allow alert notifications, generated signals are connected as selectable "Long Signal" and "Short Signal" to the indicator alerts.

The conditions can be found on the alert sections of the indicator.

In the menu right to the indicator name, press the three dots and select "Add alert on ...".

Under condition options select one of the following:

Long Signal

Short Signal

It is advised to select "Once per bar close" as alert execution option.

Moving Averages

To fine-tune the "Short MA" and "Long MA" calculation, 16 different Moving Averages are available to choose from:

ALMA (Arnaud Legoux Moving Average)

DEMA (Double Exponential Moving Average)

EMA (Exponential Moving Average)

FRAMA (Fractal Adaptive Moving Average)

HMA (Hull Moving Average)

JURIK (Jurik Moving Average)

KAMA (Kaufman Adaptive Moving Average)

Kijun (Kijun-sen / Tenkan-sen of Ichimoku)

LSMA (Least Square Moving Average)

RMA (Running Moving Average)

SMA (Simple Moving Average)

SuperSmoothed (Super Smoothed Moving Average)

TEMA (Triple Exponential Moving Average)

VWMA (Volume Weighted Moving Average)

WMA (Weighted Moving Average)

ZLEMA (Zero Lag Moving Average)

A freely determinable length allows for sensitivity adjustments that fit your own requirements.

Volume Weighted Volatility RegimeThe Volume-Weighted Volatility Regime (VWVR) is a market analysis tool that dissects total volatility to classify the current market 'character' or 'regime'. Using a Linear Regression model, it decomposes volatility into Trend, Residual (mean-reversion), and Within-Bar (noise) components.

Key Features:

Seven-Stage Regime Classification: The indicator's primary output is a regime value from -3 to +3, identifying the market state:

+3 (Strong Bull Trend): High directional, upward volatility.

+2 (Choppy Bull): Moderate upward trend with noise.

+1 (Quiet Bull): Low volatility, slight upward drift.

0 (Neutral): No clear directional bias.

-1 (Quiet Bear): Low volatility, slight downward drift.

-2 (Choppy Bear): Moderate downward trend with noise.

-3 (Strong Bear Trend): High directional, downward volatility.

Advanced Volatility Decomposition: The regime is derived from a three-component volatility model that separates price action into Trend (momentum), Residual (mean-reversion), and Within-Bar (noise) variance. The classification is determined by comparing the 'Trend' ratio against the user-defined 'Trend Threshold' and 'Quiet Threshold'.

Dual-Level Analysis: The indicator analyzes market character on two levels simultaneously:

Inter-Bar Regime (Background Color): Based on the main StdDev Length, showing the overall market character.

Intra-Bar Regime (Column Color): Based on a high-resolution analysis within each single bar ('Intra-Bar Timeframe'), showing the micro-structural character.

Calculation Options:

Statistical Model: The 'Estimate Bar Statistics' option (enabled by default) uses a statistical model ('Estimator') to perform the decomposition. (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used instead).

Normalization: An optional 'Normalize Volatility' setting calculates an Exponential Regression Curve (log-space).

Volume Weighting: An option (Volume weighted) applies volume weighting to all volatility calculations.

Multi-Timeframe (MTF) Capability: The entire dual-level analysis can be run on a higher timeframe (using the Timeframe input), with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Integrated Alerts: Includes 22 comprehensive alerts that trigger whenever the 'Inter-Bar Regime' or the 'Intra-Bar Regime' crosses one of the key thresholds (e.g., 'Regime crosses above Neutral Line'), or when the 'Intra-Bar Dominance' crosses the 50% mark.

Caution: Real-Time Data Behavior (Intra-Bar Repainting) This indicator uses high-resolution intra-bar data. As a result, the values on the current, unclosed bar (the real-time bar) will update dynamically as new intra-bar data arrives. This behavior is normal and necessary for this type of analysis. Signals should only be considered final after the main chart bar has closed.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Options Oscillator [PRO] IVRank, IVx, Call/Put Volatility Skew𝗧𝗵𝗲 𝗳𝗶𝗿𝘀𝘁 𝗧𝗿𝗮𝗱𝗶𝗻𝗴𝗩𝗶𝗲𝘄 𝗶𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿 𝘁𝗵𝗮𝘁 𝗽𝗿𝗼𝘃𝗶𝗱𝗲𝘀 𝗥𝗘𝗔𝗟 𝗜𝗩𝗥𝗮𝗻𝗸, 𝗜𝗩𝘅, 𝗮𝗻𝗱 𝗖𝗔𝗟𝗟/𝗣𝗨𝗧 𝘀𝗸𝗲𝘄 𝗱𝗮𝘁𝗮 𝗯𝗮𝘀𝗲𝗱 𝗼𝗻 𝗥𝗘𝗔𝗟 𝗼𝗽𝘁𝗶𝗼𝗻 𝗰𝗵𝗮𝗶𝗻 𝗳𝗼𝗿 𝗼𝘃𝗲𝗿 𝟭𝟲𝟱+ 𝗺𝗼𝘀𝘁 𝗹𝗶𝗾𝘂𝗶𝗱 𝗨.𝗦. 𝗺𝗮𝗿𝗸𝗲𝘁 𝘀𝘆𝗺𝗯𝗼𝗹𝘀

🔃 Auto-Updating Option Metrics without refresh!

🍒 Developed and maintained by option traders for option traders.

📈 Specifically designed for TradingView users who trade options.

🔶 Ticker Information:

This indicator is currently only available for over 165+ most liquid U.S. market symbols (eg. SP:SPX AMEX:SPY NASDAQ:QQQ NASDAQ:TLT NASDAQ:NVDA , etc.. ), and we are continuously expanding the compatible watchlist here: www.tradingview.com

🔶 How does the indicator work and why is it unique?

This Pine Script indicator is a complex tool designed to provide various option metrics and visualization tools for options market traders. The indicator extracts raw options data from an external data provider (ORATS), processes and refines the delayed data package using pineseed, and sends it to TradingView, visualizing the data using specific formulas (see detailed below) or interpolated values (e.g., delta distances). This method of incorporating options data into a visualization framework is unique and entirely innovative on TradingView.

The indicator aims to offer a comprehensive view of the current state of options for the implemented instruments, including implied volatility (IV), IV rank (IVR), options skew, and expected market movements, which are objectively measured as detailed below.

The options metrics we display may be familiar to options traders from various major brokerage platforms such as TastyTrade, IBKR, TOS, Tradier, TD Ameritrade, Schwab, etc.

🟨 The following data is displayed in the oscillator 🟨

We use Tastytrade formulas, so our numbers mostly align with theirs!

🔶 𝗜𝗩𝗥𝗮𝗻𝗸

The Implied Volatility Rank (IVR) helps options traders assess the current level of implied volatility (IV) in comparison to the past 52 weeks. IVR is a useful metric to determine whether options are relatively cheap or expensive. This can guide traders on whether to buy or sell options.

IV Rank formula = (current IV - 52 week IV low) / (52 week IV high - 52 week IV low)

IVRank is default blue and you can adjust their settings:

🔶 𝗜𝗩𝘅 𝗮𝘃𝗴

The implied volatility (IVx) shown in the option chain is calculated like the VIX. The Cboe uses standard and weekly SPX options to measure expected S&P 500 volatility. A similar method is used for calculating IVx for each expiration cycle.

We aggregate the IVx values for the 35-70 day monthly expiration cycle, and use that value in the oscillator and info panel.

We always display which expiration the IVx values are averaged for when you hover over the IVx cell.

IVx main color is purple, but you can change the settings:

🔹 IVx 5 days change %

We are also displaying the five-day change of the IV Index (IVx value). The IV Index 5-Day Change column provides quick insight into recent expansions or decreases in implied volatility over the last five trading days.

Traders who expect the value of options to decrease might view a decrease in IVX as a positive signal. Strategies such as Strangle and Ratio Spread can benefit from this decrease.

On the other hand, traders anticipating further increases in IVX will focus on the rising IVX values. Strategies like Calendar Spread or Diagonal Spread can take advantage of increasing implied volatility.

This indicator helps traders quickly assess changes in implied volatility, enabling them to make informed decisions based on their trading strategies and market expectations.

Important Note:

The IVx value alone does not provide sufficient context. There are stocks that inherently exhibit high IVx values. Therefore, it is crucial to consider IVx in conjunction with the Implied Volatility Rank (IVR), which measures the IVx relative to its own historical values. This combined view helps in accurately assessing the significance of the IVx in relation to the specific stock's typical volatility behavior.

This indicator offers traders a comprehensive view of implied volatility, assisting them in making informed decisions by highlighting both the absolute and relative volatility measures.

🔶 𝗖𝗔𝗟𝗟/𝗣𝗨𝗧 𝗣𝗿𝗶𝗰𝗶𝗻𝗴 𝗦𝗸𝗲𝘄 𝗵𝗶𝘀𝘁𝗼𝗴𝗿𝗮𝗺

At TanukiTrade, Vertical Pricing Skew refers to the difference in pricing between put and call options with the same expiration date at the same distance (at tastytrade binary expected move). We analyze this skew to understand market sentiment. This is the same formula used by TastyTrade for calculations.

We calculate the interpolated strike price based on the expected move, taking into account the neighboring option prices and their distances. This allows us to accurately determine whether the CALL or PUT options are more expensive.

🔹 What Causes Pricing Skew? The Theory Behind It

The asymmetric pricing of PUT and CALL options is driven by the natural dynamics of the market. The theory is that when CALL options are more expensive than PUT options at the same distance from the current spot price, market participants are buying CALLs and selling PUTs, expecting a faster upward movement compared to a downward one .

In the case of PUT skew, it's the opposite: participants are buying PUTs and selling CALLs , as they expect a potential downward move to happen more quickly than an upward one.

An options trader can take advantage of this phenomenon by leveraging PUT pricing skew. For example, if they have a bullish outlook and both IVR and IVx are high and IV started decreasing, they can capitalize on this PUT skew with strategies like a jade lizard, broken wing butterfly, or short put.

🔴 PUT Skew 🔴

Put options are more expensive than call options, indicating the market expects a faster downward move (▽). This alone doesn't indicate which way the market will move (because nobody knows that), but the options chain pricing suggests that if the market moves downward, it could do so faster in velocity compared to a potential upward movement.

🔹 SPY PUT SKEW example:

If AMEX:SPY PUT option prices are 46% higher than CALLs at the same distance for the optimal next monthly expiry (DTE). This alone doesn't indicate which way the market will move (because nobody knows that), but the options chain pricing suggests that if the market moves downward, it could do so 46% faster in velocity compared to a potential upward movement

🟢 CALL Skew 🟢

Call options are more expensive than put options, indicating the market expects a faster upward move (△). This alone doesn't indicate which way the market will move (because nobody knows that), but the options chain pricing suggests that if the market moves upward, it could do so faster in velocity compared to a potential downward movement.

🔹 INTC CALL SKEW example:

If NASDAQ:INTC CALL option prices are 49% higher than PUTs at the same distance for the optimal next monthly expiry (DTE). This alone doesn't indicate which way the market will move (because nobody knows that), but the options chain pricing suggests that if the market moves upward, it could do so 49% faster in velocity compared to a potential downward movement .

🔶 USAGE example:

The script is compatible with our other options indicators.

For example: Since the main metrics are already available in this Options Oscillator, you can hide the main IVR panel of our Options Overlay indicator, freeing up more space on the chart. The following image shows this:

🔶 ADDITIONAL IMPORTANT COMMENTS

🔹 Historical Data:

Yes, we only using historical internal metrics dating back to 2024-07-01, when the TanukiTrade options brand launched. For now, we're using these, but we may expand the historical data in the future.

🔹 What distance does the indicator use to measure the call/put pricing skew?:

It is important to highlight that this oscillator displays the call/put pricing skew changes for the next optimal monthly expiration on a histogram.

The Binary Expected Move distance is calculated using the TastyTrade method for the next optimal monthly expiration: Formula = (ATM straddle price x 0.6) + (1st OTM strangle price x 0.3) + (2nd OTM strangle price x 0.1)

We interpolate the exact difference based on the neighboring strikes at the binary expected move distance using the TastyTrade method, and compare the interpolated call and put prices at this specific point.

🔹 - Why is there a slight difference between the displayed data and my live brokerage data?

There are two reasons for this, and one is beyond our control.

◎ Option-data update frequency:

According to TradingView's regulations and guidelines, we can update external data a maximum of 5 times per day. We strive to use these updates in the most optimal way:

(1st update) 15 minutes after U.S. market open

(2nd, 3rd, 4th updates) 1.5–3 hours during U.S. market open hours

(5th update) 10 minutes before U.S. market close.

You don’t need to refresh your window, our last refreshed data-pack is always automatically applied to your indicator, and you can see the time elapsed since the last update at the bottom of the corner on daily TF.

◎ Brokerage Calculation Differences:

Every brokerage has slight differences in how they calculate metrics like IV and IVx. If you open three windows for TOS, TastyTrade, and IBKR side by side, you will notice that the values are minimally different. We had to choose a standard, so we use the formulas and mathematical models described by TastyTrade when analyzing the options chain and drawing conclusions.

🔹 - EOD data:

The indicator always displays end-of-day (EOD) data for IVR, IV, and CALL/PUT pricing skew. During trading hours, it shows the current values for the ongoing day with each update, and at market close, these values become final. From that point on, the data is considered EOD, provided the day confirms as a closed daily candle.

🔹 - U.S. market only:

Since we only deal with liquid option chains: this option indicator only works for the USA options market and do not include future contracts; we have implemented each selected symbol individually.

Disclaimer:

Our option indicator uses approximately 15min-3 hour delayed option market snapshot data to calculate the main option metrics. Exact realtime option contract prices are never displayed; only derived metrics and interpolated delta are shown to ensure accurate and consistent visualization. Due to the above, this indicator can only be used for decision support; exclusive decisions cannot be made based on this indicator. We reserve the right to make errors.This indicator is designed for options traders who understand what they are doing. It assumes that they are familiar with options and can make well-informed, independent decisions. We work with public data and are not a data provider; therefore, we do not bear any financial or other liability.

Implied volatility indicator - Bouhmidi-Bands Volatility trading with the Bouhmidi-Bands

Most known indicators such as Bollinger Bands or Keltner Channel focus only on historical volatility. Bouhmidi bands follow a different approach, namely an indicator based on implied volatility.

Style tags: Implied Volatility, Volatility Trading, Trend Analysis

Asset class: Equities, Futures, Commodities

Dataset: Minutes / Hours

Description

The most famous volatility indicators such as Bollinger Bands , Keltner Channel , Donchian Channels , etc. all use the historical volatility of the underlying asset. However, volatility is determined not only by historical volatility but also by implied volatility. The additional analysis of implied volatility sharpens the view and improves trading.

The Bouhmidi Bands ® were developed by myself and are based on implied volatility. They calculate an expected daily bandwidth under the assumption of normally distributed returns. The bandwidth is based on 1σ or 2σ. This means that an underlying closes with a probability of 68% or 95% within the expected Bouhmidi bandwidth at the end of the day. Check the historical development. The track record over the past 20 years shows a strong robustness of the indicator.

Benefits using Bouhmidi bands

- The Bouhmidi bands can be used to identify and filter "invisible" resistance and support that cannot be detected with simple chart analysis.

- The Bouhmidi bands can be used for different trading approaches. For example, they are suitable for mean reversion and volatility breakouts.

- If you combine the Bouhmidi bands with e.g. Keltner channel or Bollinger bands, you have the historical and implied volatility in one view in your tradingview chart.

Which underlyings can I trade with the Bouhmidi bands?

To determine the Bouhmidi bands, we need the underlying and the corresponding implied volatility index:

- S&P 500 - VIX

- DAX - VDAX-NEW

- Dow Jones - VXD

- Nasdaq 100 - VXN

- Gold - GVZ

- WTI - OVX

- Apple - VXAPL

- Amazon - VXAZN

- Google - VXGOG

- IBM - VXIBM

L&S Volatility Index Refurbished█ Introduction

This is my second version of the L&S Volatility Index, hence the name "Refurbished".

The first version can be found at this link:

The reason I released a separate version is because I rewrote the source code from scratch with the aim of both improving the indicator and staying as close as possible to the original concept.

I feel that the first version was somewhat exotic and polluted in relation to the indicator originally described by the authors.

In short, the main idea remains the same, however, the way of presenting the result has been changed, reiterating what was said.

█ CONCEPTS

The L&S Volatility Index measures the volatility of price in relation to a moving average.

The indicator was originally described by Brazilian traders Alexandre Wolwacz (Stormer) and Fábio Figueiredo (Vlad) from L&S Educação Financeira.

Basically, this indicator can be used in two ways:

1. In a mean reversion strategy, when there is an unusual distance from it;

2. In a trend following strategy, when the price is in an acceptable region.

As an indicator of volatility, the greatest utility is shown in first case.

This is because it allows identifying abnormal prices, extremely stretched in relation to an average, including market crashes.

How the calculation is done:

First, the distance of the price from a given average in percentage terms is measured.

Then, the historical average volatility is obtained.

Finally the indicator is calculated through the ratio between the distance and the historical volatility.

According to the description proposed by the creators, when the L&S Volatility Index is above 30 it means that the price is "stretched".

The closer to 100 the more stretched.

When it reaches 0, it means the price is on average.

█ What to look for

Basically, you should look at non-standard prices.

How to identify it?

When the oscillator is outside the Dynamic Zone and/or the Fixed Zone (above 30), it is because the price is stretched.

Nothing on the market is guaranteed.

As with the RSI, it is not because the RSI is overbought or oversold that the price will necessarily go down or up.

It is critical to know when NOT to buy, NOT to sell or NOT to do anything.

It is always important to consider the context.

█ Improvements

The following improvements have been implemented.

It should be noted that these improvements can be disabled, thus using the indicator in the "purest" version, the same as the one conceived by the creators.

Resources:

1. Customization of limits and zones:

2. Customization of the timeframe, which can be different from the current one.

3. Repaint option (prints the indicator in real time even if the bar has not yet closed. This produces more signals).

4. Customization of price inputs. This affects the calculation.

5. Customization of the reference moving average (the moving average used to calculate the price distance).

6. Customization of the historical volatility calculation strategy.

- Accumulated ATR: calculates the historical volatility based on the accumulated ATR.

- Returns: calculates the historical volatility based on the returns of the source.

Both forms of volatility calculation have their specific utilities and applications.

Therefore, it is worthwhile to have both approaches available, and one should not necessarily replace the other.

Each method has its advantages and may be more appropriate in different contexts.

The first approach, using the accumulated ATR, can be useful when you want to take into account the implied volatility of prices over time,

reflecting broader price movements and higher impact events. It can be especially relevant in scenarios where unexpected events can drastically affect prices.

The second approach, using the standard deviation of returns, is more common and traditionally used to measure historical volatility.

It considers the variability of prices relative to their average, providing a more general measure of market volatility.

Therefore, both forms of calculation have their merits and can be useful depending on the context and specific analysis needs.

Having both options available gives users flexibility in choosing the most appropriate volatility measure for the situation at hand.

* When choosing "Accumulated ATR", if the indicator becomes difficult to see, there are 3 possibilities:

a) manually adjust the Fixed Zone value;

b) disable the Fixed Zone and use only the Dynamic Zone;

c) normalize the indicator.

7. Signal line (a moving average of the oscillator).

8. Option to normalize the indicator or not.

9. Colors to facilitate direction interpretation.

Since the L&S is a volatility indicator, it does not show whether the price is rising or falling.

This can sometimes confuse the user.

That said, the idea here is to show certain colors where the price is relative to the average, making it easier to analyze.

10. Alert messages for automations.

H/V/Q Volatility Index v2.0This is a standalone version of the volatility calculation used in QuantRsi. It is a relatively complex volatility-specific filtering calculation designed to give deeper insight into volatility trends for any asset class.

Use with Log scaling on the indicator's value scalar.

This tool offers an alternative model for volatility calculation. Experience using this tool proves that it extends the efficacy of volatility prediction techniques, and allows deeper technical analysis within volatility moves.

Use alongside conventional volatility indices to find opportunities within option chains to long or short volatility when HVQ provides evidence for volatility reversal that other options value models have not priced in.

Use as part of a predictive based risk management strategy.

Use alongside QuantRsi and HeffaeClouds as a complete trading suite, sans volume analysis, and gain insight not offered by any other indicator set.

SETTINGS:

TimeFrame settings:

Chart/Custom timeframe inputs are carried over from HeffaeClouds and QuantRsi indicators. Allows you to assign any non-chart timeframe to the indicator:

"ChartTF" follows your chart's selected resolution / TimeFrame

"Non-Chart TimeFrame" is an integer for your custom TimeFrame, the setting below:

"Non-Chart TimeFrame" selects "Minutes, Hours, Days" that corresponds to the above setting for a custom TimeFrame.

More Settings:

"Invert Output switch" will invert the volatility chart scale. Useful for visualizing some trends on assets that regularly correlate large volatility spikes with disorderly selloffs.

"Show High/Low Volt range" switch (experimental) shows the high/low extremes of alternate volatility window calculations. There is insight to be gained from large differences v.s. all ranges trending near the same values.

"Relative value switch" (experimental) divides the HVQ values by the hl2 candle price, per candle. This is a unique way to filter the output, visualize the volatility value per asset value.

"Range Multiplier" adjusts the average window length HVQ uses for calculations. This has been finely tuned so that the value of "10" corresponds to the best average fitting of all assets and timeframes. In most situations TimeFrame should be used to alter the real window periods and this should be left at default. Instead you can change this to find better fitting if you'd like.

If there is a feature you would like, question answered, or a bug to report, visit the TradingView SNOW_CITY public chat-room; link in my signature

Use the pastebin link below for indicator access information and pricing

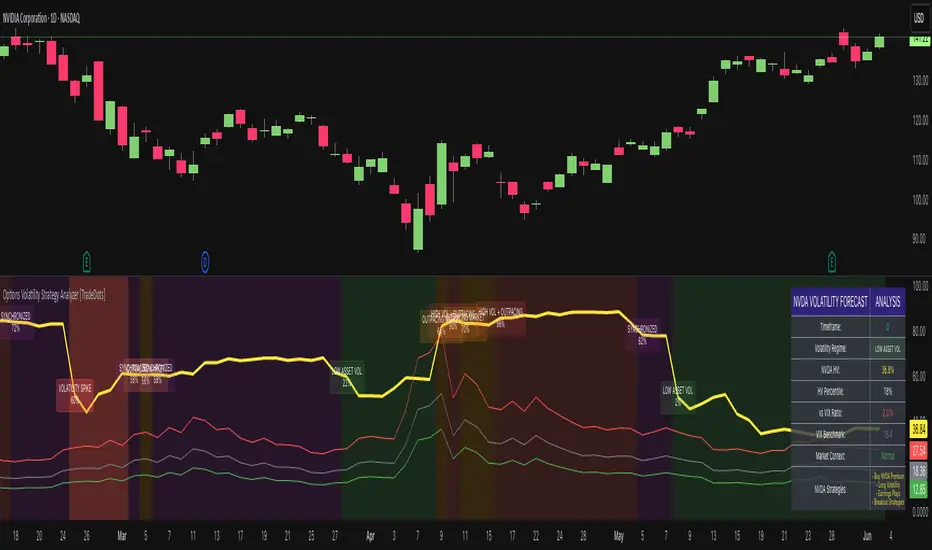

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

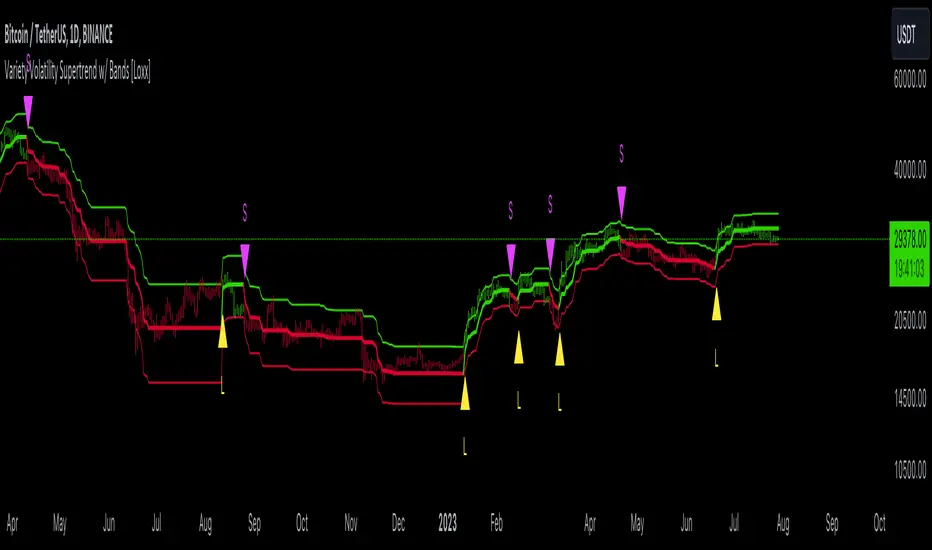

Variety Volatility Supertrend w/ Bands [Loxx]Variety Volatility Supertrend w/ Bands indicator is a powerful and highly customizable tool for traders. Building upon the foundational concept of the classic Supertrend indicator, this variant adds a plethora of user-driven options and features that can cater to diverse trading styles and market scenarios.

The Supertrend indicator is traditionally used to identify market trends by overlaying a line on the price chart, which changes color and position in relation to the price based on the trend direction. The Variety Volatility Supertrend w/ Bands takes this a step further by offering various volatility calculations, visual enhancements, explicit trading signals, and alert conditions.

It provides five options for volatility calculations, enabling users to select the most suitable measure for their strategy. This indicator also allows users to control the display of the upper, lower, and mid bands, which can serve as dynamic support and resistance levels. Further, it can display explicit trading signals when the trend changes direction and set up alerts for these signals.

█ User Inputs

Source: Defines the source of the price data, typically the closing price.

Period: Defines the lookback period for the chosen volatility calculation.

Mid Price Period: Defines the number of periods for calculating the mid-price.

Multiplier: The factor by which the volatility measure (e.g., ATR) is multiplied.

Volatility Type: The user can choose one of five different calculations for the volatility measure: ATR, Standard Error, Standard Deviation, Custom Standard Deviation with Sample Correction, and Custom Standard Deviation without Sample Correction.

Classic Supertrend: Enables the classic version of the Supertrend indicator if set to true.

Show Upper Band, Show Lower Band, Show Mid: Determines whether the upper, lower, and middle bands of the Supertrend indicator are displayed.

Outer Line Width, Mid Line Width: Controls the line widths of the outer and middle lines.

Color Bars: Colors the price bars based on the direction of the trend if enabled.

Show signals: Displays trading signals on the chart if enabled.

Bull Color, Bear Color: Controls the colors of the Supertrend indicator during bullish and bearish market conditions.

█ Computations

The script begins by calculating the chosen volatility measure (ATR, Standard Error, Standard Deviation, etc.) and the mid-price, which is the average of the highest and lowest prices over the specified Mid Price Period. It then calculates the upper and lower bands by adding and subtracting the product of the Multiplier and the volatility measure from the mid-price.

The script then compares the current price with the previous upper and lower bands to determine the trend direction. If the current price is greater than the previous upper band, the trend is considered bullish. If it's less than the previous lower band, the trend is bearish.

█ Visualizations

The script plots the upper, lower, and mid bands on the chart based on the user's settings. If Color Bars is enabled, the script colors the price bars based on the trend direction. If Show signals is enabled, the script displays shapes on the chart to represent trading signals when the trend changes direction.

█ Alerts

Finally, the script sets up alert conditions for long and short trading signals. When these conditions are met, TradingView sends an alert to the user with a message indicating the indicator's name, the type of signal (long or short), and the symbol and closing price of the asset.

█ Visualization Modes

Classic Supertrend

The Classic Supertrend mode essentially transforms the "Variety Volatility Supertrend w/ Bands " indicator to behave more like the traditional Supertrend indicator.

In the traditional Supertrend indicator, there is a single line that shifts positions based on the trend direction. When the market is in an uptrend, the Supertrend line is plotted below the price, acting as a dynamic support level. Conversely, when the market is in a downtrend, the Supertrend line moves above the price, acting as a dynamic resistance level.

When you set Classic Supertrend to True in this script, it mimics this behavior. It will only display one line (the Supertrend line) instead of the upper and lower bands. The Supertrend line will switch between the calculated upper band and lower band based on the trend direction:

In an uptrend, it plots the lower band as the Supertrend line (acting as a dynamic support level).

In a downtrend, it plots the upper band as the Supertrend line (acting as a dynamic resistance level).

Thus, when Classic Supertrend is True, the display is similar to the regular Supertrend indicator, offering a more simplified, less cluttered view of the price trend.

See here for the Classic Supertrend

Supertrend Moving Average with Bands

When the Classic Supertrend option is turned off in the "Variety Volatility Supertrend w/ Bands " indicator, the indicator displays upper and lower bands along with the midline, depending on the user's settings. These bands can serve as dynamic support and resistance levels, and they move and adjust based on the market's volatility.

Support and resistance are key concepts in technical analysis. Support is a price level where the price tends to find a floor as it falls, indicating a greater amount of demand or buying interest that can prop up the prices. Resistance, on the other hand, is a price level where rising prices tend to stop rising, indicating a greater amount of supply or selling interest.

In the context of the "Variety Volatility Supertrend w/ Bands " indicator:

Upper Band: This can act as a dynamic resistance level in a downtrend. When prices are falling, they might struggle to rise above this band. If prices do break above the upper band, it could be a sign that the downtrend is reversing, and a new uptrend may be beginning.

Lower Band: Conversely, this can act as a dynamic support level in an uptrend. When prices are rising, they might bounce off this band and continue to rise. If prices break below the lower band, it could indicate that the uptrend is reversing, and a new downtrend may be beginning.

The benefit of these dynamic support and resistance levels is that they adjust automatically as market conditions change, potentially offering more relevant insights into price behavior compared to static support and resistance levels.

See here for the Supertrend Moving Average with Bands

█ Volatility Types

The "Variety Volatility Supertrend w/ Bands " indicator provides five options for the volatility calculation. Volatility is a statistical measure of the dispersion of returns for a given security or market index. In most cases, the higher the volatility, the riskier the security. Here's a quick summary of each option:

Average True Range (ATR): This is a common volatility measure in the world of trading, particularly for commodities and forex markets. It measures the average of true price ranges over a specified period. The true range considers the most recent period's high-low range, the previous close to the most recent high, and the previous close to the most recent low, taking the highest value.

Standard Error: This is a measure of the accuracy of predictions made with statistical techniques. In the context of trading, the standard error can give traders an idea of the quality of their volatility or price level estimates. It's calculated using the standard deviation of the price data, the square root of the number of data points.

Standard Deviation: This is a measure of the dispersion of a set of data from its mean. It's a commonly used volatility measure in finance. In trading, a higher standard deviation suggests greater price volatility.

Custom Standard Deviation - with Sample Correction: This is a variation of the standard deviation calculation, but it applies a correction for small sample sizes. It's calculated similarly to the standard deviation, but the sum of the squares is divided by (n-1) instead of n to provide a more accurate estimate when working with a small number of data points.

Custom Standard Deviation - without Sample Correction: This is another variation of the standard deviation calculation, but without the sample correction. This might be used when the number of data points is sufficiently large that the correction is not necessary.

The choice of volatility measure can have a significant impact on the sensitivity of the Supertrend indicator. Some measures may result in wider bands and fewer trend changes, while others may produce narrower bands and more frequent trend changes. The choice of volatility measure should align with the trader's strategy and risk tolerance.

█ Multiple Timeframe options

The "Variety Volatility Supertrend w/ Bands " indicator, like most indicators on the TradingView platform, can be applied to various timeframes, regardless of the chart's current timeframe. The timeframe of an indicator is determined by the timeframe of the price data it processes.

This indicator's flexibility with timeframes allows it to be used in different trading strategies. Day traders might use shorter timeframes like 1-minute or 15-minute charts, swing traders might use 1-hour or 4-hour charts, and long-term investors might use daily or weekly charts.

See here for the Supertrend Moving Average with Bands on 4-hour chart using Daily data

GKD-C Volatility Ratio Adaptive RSX [Loxx]Giga Kaleidoscope GKD-C Volatility Ratio Adaptive RSX is a Confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ Giga Kaleidoscope Modularized Trading System

What is Loxx's "Giga Kaleidoscope Modularized Trading System"?

The Giga Kaleidoscope Modularized Trading System is a trading system built on the philosophy of the NNFX (No Nonsense Forex) algorithmic trading.

What is the NNFX algorithmic trading strategy?

The NNFX (No-Nonsense Forex) trading system is a comprehensive approach to Forex trading that is designed to simplify the process and remove the confusion and complexity that often surrounds trading. The system was developed by a Forex trader who goes by the pseudonym "VP" and has gained a significant following in the Forex community.

The NNFX trading system is based on a set of rules and guidelines that help traders make objective and informed decisions. These rules cover all aspects of trading, including market analysis, trade entry, stop loss placement, and trade management.

Here are the main components of the NNFX trading system:

1. Trading Philosophy: The NNFX trading system is based on the idea that successful trading requires a comprehensive understanding of the market, objective analysis, and strict risk management. The system aims to remove subjective elements from trading and focuses on objective rules and guidelines.

2. Technical Analysis: The NNFX trading system relies heavily on technical analysis and uses a range of indicators to identify high-probability trading opportunities. The system uses a combination of trend-following and mean-reverting strategies to identify trades.

3. Market Structure: The NNFX trading system emphasizes the importance of understanding the market structure, including price action, support and resistance levels, and market cycles. The system uses a range of tools to identify the market structure, including trend lines, channels, and moving averages.

4. Trade Entry: The NNFX trading system has strict rules for trade entry. The system uses a combination of technical indicators to identify high-probability trades, and traders must meet specific criteria to enter a trade.

5. Stop Loss Placement: The NNFX trading system places a significant emphasis on risk management and requires traders to place a stop loss order on every trade. The system uses a combination of technical analysis and market structure to determine the appropriate stop loss level.

6. Trade Management: The NNFX trading system has specific rules for managing open trades. The system aims to minimize risk and maximize profit by using a combination of trailing stops, take profit levels, and position sizing.

Overall, the NNFX trading system is designed to be a straightforward and easy-to-follow approach to Forex trading that can be applied by traders of all skill levels.

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v1.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data between modules. Data is passed between each module as described below:

GKD-B => GKD-V => GKD-C(1) => GKD-C(2) => GKD-C(Continuation) => GKD-E => GKD-BT

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Strategy with 1-3 take profits, trailing stop loss, multiple types of PnL volatility, and 2 backtesting styles

Baseline: Hull Moving Average

Volatility/Volume: Hurst Exponent

Confirmation 1: Volatility Ratio Adaptive RSX as shown on the chart above

Confirmation 2: Williams Percent Range

Continuation: Fisher Transform

Exit: Rex Oscillator

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD protocol chain.

Giga Kaleidoscope Modularized Trading System Signals (based on the NNFX algorithm)

Standard Entry

1. GKD-C Confirmation 1 Signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Volatility/Volume Entry

1. GKD-V Volatility/Volume signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Continuation Entry

1. Standard Entry, Baseline Entry, or Pullback; entry triggered previously

2. GKD-B Baseline hasn't crossed since entry signal trigger

3. GKD-C Confirmation Continuation Indicator signals

4. GKD-C Confirmation 1 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 2 agrees

1-Candle Rule Standard Entry

1. GKD-C Confirmation 1 signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

1-Candle Rule Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume Agrees

1-Candle Rule Volatility/Volume Entry

1. GKD-V Volatility/Volume signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close)

2. GKD-B Volatility/Volume agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-B Baseline agrees

PullBack Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is beyond 1.0x Volatility of Baseline

Next Candle:

1. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

2. GKD-C Confirmation 1 agrees

3. GKD-C Confirmation 2 agrees

4. GKD-V Volatility/Volume Agrees

]█ Setting up the GKD

The GKD system involves chaining indicators together. These are the steps to set this up.

Use a GKD-C indicator alone on a chart

1. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Simple"

Use a GKD-V indicator alone on a chart

**nothing, it's already useable on the chart without any settings changes

Use a GKD-B indicator alone on a chart

**nothing, it's already useable on the chart without any settings changes

Baseline (Baseline, Backtest)

1. Import the GKD-B Baseline into the GKD-BT Backtest: "Input into Volatility/Volume or Backtest (Baseline testing)"

2. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Baseline"

Volatility/Volume (Volatility/Volume, Backte st)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Solo"

2. Inside the GKD-V indicator, change the "Signal Type" setting to "Crossing" (neither traditional nor both can be backtested)

3. Import the GKD-V indicator into the GKD-BT Backtest: "Input into C1 or Backtest"

4. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Volatility/Volume"

5. Inside the GKD-BT Backtest, a) change the setting "Backtest Type" to "Trading" if using a directional GKD-V indicator; or, b) change the setting "Backtest Type" to "Full" if using a directional or non-directional GKD-V indicator (non-directional GKD-V can only test Longs and Shorts separately)

6. If "Backtest Type" is set to "Full": Inside the GKD-BT Backtest, change the setting "Backtest Side" to "Long" or "Short

7. If "Backtest Type" is set to "Full": To allow the system to open multiple orders at one time so you test all Longs or Shorts, open the GKD-BT Backtest, click the tab "Properties" and then insert a value of something like 10 orders into the "Pyramiding" settings. This will allow 10 orders to be opened at one time which should be enough to catch all possible Longs or Shorts.

Solo Confirmation Simple (Confirmation, Backtest)

1. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Simple"

1. Import the GKD-C indicator into the GKD-BT Backtest: "Input into Backtest"

2. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Solo Confirmation Simple"

Solo Confirmation Complex without Exits (Baseline, Volatility/Volume, Confirmation, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Complex"

4. Import the GKD-V indicator into the GKD-C indicator: "Input into C1 or Backtest"

5. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full wo/ Exits"

6. Import the GKD-C into the GKD-BT Backtest: "Input into Exit or Backtest"

Solo Confirmation Complex with Exits (Baseline, Volatility/Volume, Confirmation, Exit, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Complex"

4. Import the GKD-V indicator into the GKD-C indicator: "Input into C1 or Backtest"

5. Import the GKD-C indicator into the GKD-E indicator: "Input into Exit"

6. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full w/ Exits"

7. Import the GKD-E into the GKD-BT Backtest: "Input into Backtest"

Full GKD without Exits (Baseline, Volatility/Volume, Confirmation 1, Confirmation 2, Continuation, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C 1 indicator, change the "Confirmation Type" setting to "Confirmation 1"

4. Import the GKD-V indicator into the GKD-C 1 indicator: "Input into C1 or Backtest"

5. Inside the GKD-C 2 indicator, change the "Confirmation Type" setting to "Confirmation 2"

6. Import the GKD-C 1 indicator into the GKD-C 2 indicator: "Input into C2"

7. Inside the GKD-C Continuation indicator, change the "Confirmation Type" setting to "Continuation"

8. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full wo/ Exits"

9. Import the GKD-E into the GKD-BT Backtest: "Input into Exit or Backtest"

Full GKD with Exits (Baseline, Volatility/Volume, Confirmation 1, Confirmation 2, Continuation, Exit, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C 1 indicator, change the "Confirmation Type" setting to "Confirmation 1"

4. Import the GKD-V indicator into the GKD-C 1 indicator: "Input into C1 or Backtest"

5. Inside the GKD-C 2 indicator, change the "Confirmation Type" setting to "Confirmation 2"

6. Import the GKD-C 1 indicator into the GKD-C 2 indicator: "Input into C2"

7. Inside the GKD-C Continuation indicator, change the "Confirmation Type" setting to "Continuation"

8. Import the GKD-C Continuation indicator into the GKD-E indicator: "Input into Exit"

9. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full w/ Exits"

10. Import the GKD-E into the GKD-BT Backtest: "Input into Backtest"

Baseline + Volatility/Volume (Baseline, Volatility/Volume, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Baseline + Volatility/Volume"

2. Inside the GKD-V indicator, make sure the "Signal Type" setting is set to "Traditional"

3. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

4. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Baseline + Volatility/Volume"

5. Import the GKD-V into the GKD-BT Backtest: "Input into C1 or Backtest"

6. Inside the GKD-BT Backtest, change the setting "Backtest Type" to "Full". For this backtest, you must test Longs and Shorts separately

7. To allow the system to open multiple orders at one time so you can test all Longs or Shorts, open the GKD-BT Backtest, click the tab "Properties" and then insert a value of something like 10 orders into the "Pyramiding" settings. This will allow 10 orders to be opened at one time which should be enough to catch all possible Longs or Shorts.

█ GKD-C Volatility Ratio Adaptive RSX

What is the RSX?

The Jurik RSX is a technical indicator developed by Mark Jurik to measure the momentum and strength of price movements in financial markets, such as stocks, commodities, and currencies. It is an advanced version of the traditional Relative Strength Index (RSI), designed to offer smoother and less lagging signals compared to the standard RSI.

The main advantage of the Jurik RSX is that it provides more accurate and timely signals for traders and analysts, thanks to its improved calculation methods that reduce noise and lag in the indicator's output. This enables better decision-making when analyzing market trends and potential trading opportunities.

What is the Voaltility Ratio?

The volatility ratio is a technical analysis indicator used by traders and investors to measure the relative volatility of a financial instrument, such as stocks, commodities, or forex. It is calculated by comparing the True Range (TR) of the instrument to its average range over a specified period, typically expressed as a percentage. The higher the volatility ratio, the more volatile the instrument is considered to be.

The formula for the volatility ratio is:

Volatility Ratio (VR) = (Today's True Range) / (Average True Range over a specified period)

Where:

Today's True Range is the highest value among:

Current High - Current Low

Current High - Previous Close

Current Low - Previous Close

Average True Range (ATR) is the average of the True Range values over a specified period, typically 14 days.

Traders and investors use the volatility ratio to gauge the risk associated with a particular instrument and to identify potential entry and exit points. A high volatility ratio can signal strong price movements, while a low ratio may indicate stability or stagnation in price. The volatility ratio can also be used in conjunction with other technical indicators to create a more comprehensive trading strategy.

What is Volatility Ratio Adaptive RSX?

For this indicator the calculation of volatility is changed to the following:

Volatility Ratio (VR) = (Standard Deviation of Price) / (Simple Moving Average of Standard Deviation over a specified period)

Where:

src: source data (typically closing prices) of the financial instrument.

per: the period over which the standard deviation and simple moving average are calculated.

This version of the Volatility Ratio helps identify periods of high or low price volatility relative to the historical average over the specified period. A value above 1 indicates higher than average volatility, while a value below 1 suggests lower than average volatility. Traders and investors can use this indicator to assess the risk of a particular instrument, determine market sentiment, or identify potential trading opportunities.

What this looks like inside:

This code defines two functions, rsx() and volatratio(), and then calculates the Volatility Ratio Adaptive RSX by combining their outputs.

1. rsx(src, len, speed): This function calculates the Adaptive RSX (Relative Strength Index) based on the input source data (src), the lookback period (len), and the speed factor (speed). The function computes a smoothed version of the price momentum (mom_out) and its absolute version (moa_out) using an iterative process. The final output, rsiout, is the Adaptive RSX oscillator value, which is calculated by normalizing the momentum ratio to the 0-100 range.

2. volatratio(src, per): This function calculates the Volatility Ratio using the input source data (src) and the lookback period (per). It computes the standard deviation (dev) and its simple moving average (devavg) over the specified period, and then calculates the Volatility Ratio by dividing the standard deviation by its average.

The main part of the code calculates the Volatility Ratio Adaptive RSX using the rsx() and volatratio() functions:

-volRatio = volatratio(src, inpPeriod): It calculates the Volatility Ratio using the input source data (src) and the lookback period (inpPeriod).

-rsxout = _rsx(src, int(inpPeriod/volRatio), inpSpeed): It calculates the Adaptive RSX using the input source data (src), the adjusted lookback period (which is the original period divided by the Volatility Ratio), and the speed factor (inpSpeed).

The final output, rsxout, represents the Volatility Ratio Adaptive RSX oscillator. Traders can use this oscillator to identify potential entry and exit points, confirm trends, or detect price reversals based on overbought or oversold conditions.

Requirements

Inputs

Confirmation 1: GKD-V Volatility / Volume indicator

Confirmation 2: GKD-C Confirmation indicator

Continuation: GKD-C Confirmation indicator

Solo Confirmation Simple: GKD-B Baseline

Solo Confirmation Complex: GKD-V Volatility / Volume indicator

Solo Confirmation Super Complex: GKD-V Volatility / Volume indicator

Stacked 1: None

Stacked 2+: GKD-C, GKD-V, or GKD-B Stacked 1

Outputs

Confirmation 1: GKD-C Confirmation 2 indicator

Confirmation 2: GKD-C Continuation indicator

Continuation: GKD-E Exit indicator

Solo Confirmation Simple: GKD-BT Backtest

Solo Confirmation Complex: GKD-BT Backtest or GKD-E Exit indicator

Solo Confirmation Super Complex: GKD-C Continuation indicator

Stacked 1: GKD-C, GKD-V, or GKD-B Stacked 2+

Stacked 2+: GKD-C, GKD-V, or GKD-B Stacked 2+ or GKD-BT Backtest

Additional features will be added in future releases.

Fixed Volatility OscillatorA fixed volatility plotter set to a 0-100 range - Plots the current volatility % using the formula to calculate volatility and stdev (standard deviation) based on the candle lookback.

The indicator is Fixed, which means that regardless of the chart, the volatility will be plotted on a percentage of 0% - 100% with a 101% threshold set to indicate a volatility reset. While the volume of volatility will change depending on the chart, the volatility will ALWAYS stay within this range.

if a plot exceeds 100% it should be marked as volatility reset - not an expansion

and should also be noted that the volatility spikes are also very inconsistent in volume and vary greatly.

The candle lookbacks on standard are organized be from 10 candles to 100 candles. I found the best results using the 50 candles lookback, and therefore have set it as the default value. These different values can be used to pull the information from the # of candles on the selected option - and therefore the volatility will be calculated from the number of candles selected.

// note for other people versed in pinescript

While this indicator may be useful in trading or strategies, it is more meant to incorporated into other scripts or used as a basis that can be further expanded on. The visuals are not built at all - for that purpose.

This script has not been listed as a library for the fact that it can be used as an actual indicator within a strategy - hope you enjoy.

Implied Volatility Suite (TG Fork)Displays the Implied Volatility, which is usually calculated from options, but here is calculated indirectly from spot price directly, either using a model or model-free using the VIXfix.

The model-free VIXfix based approach can detect times of high volatility, which usually coincides with panic and hence lowest prices. Inversely, the model-based approach can detect times of highest greed.

Forked and updated by Tartigradia to fix some issues in the calculations, convert to pinescript v5 and reverse engineered to reproduce the "Implied Volatility Rank & Model Free IVR" indicator by the same author (but closed source) and allow to plot both model-based and model-free implied volatilities simultaneously.

If you like this indicator, please show the original author SegaRKO some love:

Implied Volatility SuiteThis is an updated, more robust, and open source version of my 2 previous scripts : "Implied Volatility Rank & Model-Free IVR" and "IV Rank & IV Percentile".

This specific script provides you with 4 different types of volatility data: 1)Implied volatility, 2) Implied Volatility Rank, 3)Implied Volatility Percentile, 4)Skew Index.

1) Implied Volatility is the market's forecast of a likely movement, usually 1 standard deviation, in a securities price.

2) Implied Volatility Rank, ranks IV in relation to its high and low over a certain period of time. For example if over the past year IV had a high of 20% and a low of 10% and is currently 15%; the IV rank would be 50%, as 15 is 50% of the way between 10 & 20. IV Rank is mean reverting, meaning when IV Rank is high (green) it is assumed that future volatility will decrease; while if IV rank is low (red) it is assumed that future volatility will increase.

3) Implied Volatility Percentile ranks IV in relation to how many previous IV data points are less than the current value. For example if over the last 5 periods Implied volatility was 10%,12%,13%,14%,20%; and the current implied volatility is 15%, the IV percentile would be 80% as 4 out of the 5 previous IV values are below the current IV of 15%. IV Percentile is mean reverting, meaning when IV Percentile is high (green) it is assumed that future volatility will decrease; while if IV percentile is low (red) it is assumed that future volatility will increase. IV Percentile is more robust than IV Rank because, unlike IV Rank which only looks at the previous highs and lows, IV Percentile looks at all data points over the specified time period.