RCI3lines3 lines RCI

Original author is Jadbrother and modified for 3 lines, 9,35,52, by gero on Jun.29 2016.

Cari skrip untuk "2016年黄金价格"

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)

kst_roc4 = ta.roc(close, 30)

kst = ta.sma(kst_roc1, 10) + 2*ta.sma(kst_roc2, 10) + 3*ta.sma(kst_roc3, 10) + 4*ta.sma(kst_roc4, 15)

// 51. Percentage Price Oscillator (PPO)

ppo_line = ((ta.ema(close, 12) - ta.ema(close, 26)) / ta.ema(close, 26)) * 100

ppo_signal = ta.ema(ppo_line, 9)

ppo_histogram = ppo_line - ppo_signal

// |----- PLOT MAIN INDICATORS -----| //

// Plot key momentum indicators

plot(rsi_centered, title="01_RSI_Centered", color=color.purple, linewidth=1)

plot(stoch_centered, title="02_Stoch_Centered", color=color.blue, linewidth=1)

plot(williams_r, title="03_Williams_R", color=color.red, linewidth=1)

plot(macd_histogram, title="04_MACD_Histogram", color=color.orange, linewidth=1)

plot(cci, title="05_CCI", color=color.green, linewidth=1)

// Plot trend indicators

plot(sma_momentum, title="06_SMA_Momentum", color=color.navy, linewidth=1)

plot(ema_momentum, title="07_EMA_Momentum", color=color.maroon, linewidth=1)

plot(sar_trend, title="08_SAR_Trend", color=color.teal, linewidth=1)

plot(lr_slope, title="09_LR_Slope", color=color.lime, linewidth=1)

plot(mac, title="10_MAC", color=color.fuchsia, linewidth=1)

// Plot volatility indicators

plot(atr_pct, title="11_ATR_Pct", color=color.yellow, linewidth=1)

plot(bb_position, title="12_BB_Position", color=color.aqua, linewidth=1)

plot(kc_position, title="13_KC_Position", color=color.olive, linewidth=1)

plot(std_dev_pct, title="14_StdDev_Pct", color=color.silver, linewidth=1)

plot(bb_width, title="15_BB_Width", color=color.gray, linewidth=1)

// Plot volume indicators

plot(vroc, title="16_VROC", color=color.blue, linewidth=1)

plot(eom_sma, title="17_EOM", color=color.red, linewidth=1)

plot(vol_osc, title="18_Vol_Osc", color=color.green, linewidth=1)

plot(force_index_sma, title="19_Force_Index", color=color.orange, linewidth=1)

plot(obv, title="20_OBV", color=color.purple, linewidth=1)

// Plot additional oscillators

plot(ao, title="21_Awesome_Osc", color=color.navy, linewidth=1)

plot(cmo, title="22_CMO", color=color.maroon, linewidth=1)

plot(dpo, title="23_DPO", color=color.teal, linewidth=1)

plot(trix, title="24_TRIX", color=color.lime, linewidth=1)

plot(fisher, title="25_Fisher", color=color.fuchsia, linewidth=1)

// Plot more momentum indicators

plot(mfi_centered, title="26_MFI_Centered", color=color.yellow, linewidth=1)

plot(ac, title="27_AC", color=color.aqua, linewidth=1)

plot(ppo_pct, title="28_PPO_Pct", color=color.olive, linewidth=1)

plot(stoch_rsi_centered, title="29_StochRSI_Centered", color=color.silver, linewidth=1)

plot(klinger, title="30_Klinger", color=color.gray, linewidth=1)

// Plot trend continuation

plot(tii, title="31_TII", color=color.blue, linewidth=1)

plot(ichimoku_signal, title="32_Ichimoku_Signal", color=color.red, linewidth=1)

plot(mama_momentum, title="33_MAMA_Momentum", color=color.green, linewidth=1)

plot(zlema_momentum, title="34_ZLEMA_Momentum", color=color.orange, linewidth=1)

plot(bop, title="35_BOP", color=color.purple, linewidth=1)

// Plot volume continuation

plot(nvi, title="36_NVI", color=color.navy, linewidth=1)

plot(pvi, title="37_PVI", color=color.maroon, linewidth=1)

plot(momentum_pct, title="38_Momentum_Pct", color=color.teal, linewidth=1)

plot(roc, title="39_ROC", color=color.lime, linewidth=1)

plot(rvi, title="40_RVI", color=color.fuchsia, linewidth=1)

// Plot volatility continuation

plot(dc_position, title="41_DC_Position", color=color.yellow, linewidth=1)

plot(rvi_volatility, title="42_RVI_Volatility", color=color.aqua, linewidth=1)

plot(hv, title="43_Historical_Vol", color=color.olive, linewidth=1)

plot(gk_volatility, title="44_GK_Volatility", color=color.silver, linewidth=1)

plot(parkinson, title="45_Parkinson_Vol", color=color.gray, linewidth=1)

// Plot final oscillators

plot(rogers_satchell, title="46_RS_Volatility", color=color.blue, linewidth=1)

plot(elder_power, title="47_Elder_Power", color=color.red, linewidth=1)

plot(stc, title="48_STC", color=color.green, linewidth=1)

plot(coppock, title="49_Coppock", color=color.orange, linewidth=1)

plot(kst, title="50_KST", color=color.purple, linewidth=1)

// Plot final indicators

plot(ppo_histogram, title="51_PPO_Histogram", color=color.navy, linewidth=1)

plot(pvt, title="52_PVT", color=color.maroon, linewidth=1)

// |----- Reference Lines -----| //

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dashed, linewidth=1)

hline(50, "Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-50, "Lower Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(25, "Upper Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-25, "Lower Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

// |----- Enhanced Information Table -----| //

if show_table and barstate.islast

table_position = position.top_right

table_text_size = table_size == "Tiny" ? size.tiny : table_size == "Small" ? size.small : size.normal

var table info_table = table.new(table_position, 3, 18, bgcolor=color.new(color.white, 85), border_width=1, border_color=color.gray)

// Headers

table.cell(info_table, 0, 0, 'Category', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 1, 0, 'Indicator', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 2, 0, 'Value', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

// Key Momentum Indicators

table.cell(info_table, 0, 1, 'MOMENTUM', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 1, 'RSI Centered', text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 2, 1, str.tostring(rsi_centered, '0.00'), text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 0, 2, '', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 1, 2, 'Stoch Centered', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 2, str.tostring(stoch_centered, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 3, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 3, 'Williams %R', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 3, str.tostring(williams_r, '0.00'), text_color=color.red, text_size=table_text_size)

table.cell(info_table, 0, 4, '', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 1, 4, 'MACD Histogram', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 2, 4, str.tostring(macd_histogram, '0.000'), text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 0, 5, '', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 1, 5, 'CCI', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 2, 5, str.tostring(cci, '0.00'), text_color=color.green, text_size=table_text_size)

// Key Trend Indicators

table.cell(info_table, 0, 6, 'TREND', text_color=color.navy, text_size=table_text_size, bgcolor=color.new(color.navy, 90))

table.cell(info_table, 1, 6, 'SMA Momentum %', text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 2, 6, str.tostring(sma_momentum, '0.00'), text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 0, 7, '', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 1, 7, 'EMA Momentum %', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 2, 7, str.tostring(ema_momentum, '0.00'), text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 0, 8, '', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 1, 8, 'SAR Trend', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 2, 8, str.tostring(sar_trend, '0'), text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 0, 9, '', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 1, 9, 'Linear Regression', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 2, 9, str.tostring(lr_slope, '0.000'), text_color=color.lime, text_size=table_text_size)

// Key Volatility Indicators

table.cell(info_table, 0, 10, 'VOLATILITY', text_color=color.yellow, text_size=table_text_size, bgcolor=color.new(color.yellow, 90))

table.cell(info_table, 1, 10, 'ATR %', text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 2, 10, str.tostring(atr_pct, '0.00'), text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 0, 11, '', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 1, 11, 'BB Position', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 2, 11, str.tostring(bb_position, '0.00'), text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 0, 12, '', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 1, 12, 'KC Position', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 2, 12, str.tostring(kc_position, '0.00'), text_color=color.olive, text_size=table_text_size)

// Key Volume Indicators

table.cell(info_table, 0, 13, 'VOLUME', text_color=color.blue, text_size=table_text_size, bgcolor=color.new(color.blue, 90))

table.cell(info_table, 1, 13, 'Volume ROC', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 13, str.tostring(vroc, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 14, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 14, 'EOM', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 14, str.tostring(eom_sma, '0.000'), text_color=color.red, text_size=table_text_size)

// Key Oscillators

table.cell(info_table, 0, 15, 'OSCILLATORS', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 15, 'Awesome Osc', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 15, str.tostring(ao, '0.000'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 16, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 16, 'Fisher Transform', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 16, str.tostring(fisher, '0.000'), text_color=color.red, text_size=table_text_size)

// Summary Statistics

table.cell(info_table, 0, 17, 'SUMMARY', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.gray, 70))

table.cell(info_table, 1, 17, 'Total Indicators: 52', text_color=color.black, text_size=table_text_size)

regime_color = rsi_centered > 10 ? color.green : rsi_centered < -10 ? color.red : color.gray

regime_text = rsi_centered > 10 ? "BULLISH" : rsi_centered < -10 ? "BEARISH" : "NEUTRAL"

table.cell(info_table, 2, 17, regime_text, text_color=regime_color, text_size=table_text_size)

This makes it the perfect “indicator backbone” for quantitative and systematic traders who want to prototype, combine, and test new regime detection models—especially in combination with the Markov Chain indicator.

How to use this script with the Markov Chain for research and backtesting:

Add the Enhanced Indicator Export to your chart.

Every calculated indicator is available as an individual data stream.

Connect the indicator(s) you want as custom input(s) to the Markov Chain’s “Custom Indicators” option.

In the Markov Chain indicator’s settings, turn ON the custom indicator mode.

For each of the three custom indicator inputs, select the exported plot from the Enhanced Export script—the menu lists all 45+ signals by name.

This creates a powerful, modular regime-detection engine where you can mix-and-match momentum, trend, volume, or custom combinations for advanced filtering.

Backtest regime logic directly.

Once you’ve connected your chosen indicators, the Markov Chain script performs regime detection (Bull/Neutral/Bear) based on your selected features—not just price returns.

The regime detection is robust, automatically normalized (using Z-score), and outputs bias (1, -1, 0) for plug-and-play integration.

Export the regime bias for programmatic use.

As described above, use input.source() in your Pine Script strategy or system and link the bias output.

You can now filter signals, control trade direction/size, or design pairs-trading that respect true, indicator-driven market regimes.

With this framework, you’re not limited to static or simplistic regime filters. You can rigorously define, test, and refine what “market regime” means for your strategies—using the technical features that matter most to you.

Optimize your signal generation by backtesting across a universe of meaningful indicator blends.

Enhance risk management with objective, real-time regime boundaries.

Accelerate your research: iterate quickly, swap indicator components, and see results with minimal code changes.

Automate multi-asset or pairs-trading by integrating regime context directly into strategy logic.

Add both scripts to your chart, connect your preferred features, and start investigating your best regime-based trades—entirely within the TradingView ecosystem.

References & Further Reading

Ang, A., & Bekaert, G. (2002). “Regime Switches in Interest Rates.” Journal of Business & Economic Statistics, 20(2), 163–182.

Hamilton, J. D. (1989). “A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle.” Econometrica, 57(2), 357–384.

Markov, A. A. (1906). "Extension of the Limit Theorems of Probability Theory to a Sum of Variables Connected in a Chain." The Notes of the Imperial Academy of Sciences of St. Petersburg.

Guidolin, M., & Timmermann, A. (2007). “Asset Allocation under Multivariate Regime Switching.” Journal of Economic Dynamics and Control, 31(11), 3503–3544.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets. New York Institute of Finance.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns.” Journal of Finance, 47(5), 1731–1764.

Zucchini, W., MacDonald, I. L., & Langrock, R. (2017). Hidden Markov Models for Time Series: An Introduction Using R (2nd ed.). Chapman and Hall/CRC.

On Quantitative Finance and Markov Models:

Lo, A. W., & Hasanhodzic, J. (2009). The Heretics of Finance: Conversations with Leading Practitioners of Technical Analysis. Bloomberg Press.

Patterson, S. (2016). The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution. Penguin Press.

TradingView Pine Script Documentation: www.tradingview.com

TradingView Blog: “Use an Input From Another Indicator With Your Strategy” www.tradingview.com

GeeksforGeeks: “What is the Difference Between Markov Chains and Hidden Markov Models?” www.geeksforgeeks.org

What makes this indicator original and unique?

- On‑chart, real‑time Markov. The chain is drawn directly on your chart. You see the current regime, its tendency to stay (self‑loop), and the usual next step (arrows) as bars confirm.

- Source‑agnostic by design. The engine runs on any series you select via input.source() — price, your own oscillator, a composite score, anything you compute in the script.

- Automatic normalization + regime mapping. Different inputs live on different scales. The script standardizes your chosen source and maps it into clear regimes (e.g., Bull / Bear / Neutral) without you micromanaging thresholds each time.

- Rolling, bar‑by‑bar learning. Transition tendencies are computed from a rolling window of confirmed bars. What you see is exactly what the market did in that window.

- Fast experimentation. Switch the source, adjust the window, and the Markov view updates instantly. It’s a rapid way to test ideas and feel regime persistence/switch behavior.

Integrate your own signals (using input.source())

- In settings, choose the Source . This is powered by input.source() .

- Feed it price, an indicator you compute inside the script, or a custom composite series.

- The script will automatically normalize that series and process it through the Markov engine, mapping it to regimes and updating the on‑chart spheres/arrows in real time.

Credits:

Deep gratitude to @RicardoSantos for both the foundational Markov chain processing engine and inspiring open-source contributions, which made advanced probabilistic market modeling accessible to the TradingView community.

Special thanks to @Alien_Algorithms for the innovative and visually stunning 3D sphere logic that powers the indicator’s animated, regime-based visualization.

Disclaimer

This tool summarizes recent behavior. It is not financial advice and not a guarantee of future results.

BUY in HASH RibbonsHash Ribbons Indicator (BUY Signal)

A TradingView Pine Script v6 implementation for identifying Bitcoin miner capitulation (“Springs”) and recovery phases based on hash rate data. It marks potential low-risk buying opportunities by tracking short- and long-term moving averages of the network hash rate.

⸻

Key Features

• Hash Rate SMAs

• Short-term SMA (default: 30 days)

• Long-term SMA (default: 60 days)

• Phase Markers

• Gray circle: Short SMA crosses below long SMA (start of capitulation)

• White circles: Ongoing capitulation, with brighter white when the short SMA turns upward

• Yellow circle: Short SMA crosses back above long SMA (end of capitulation)

• Orange circle: Buy signal once hash rate recovery aligns with bullish price momentum (10-day price SMA crosses above 20-day price SMA)

• Display Modes

• Ribbons: Plots the two SMAs as colored bands—red for capitulation, green for recovery

• Oscillator: Shows the percentage difference between SMAs as a histogram (red for negative, blue for positive)

• Optional Overlays

• Bitcoin halving dates (2012, 2016, 2020, 2024) with dashed lines and labels

• Raw hash rate data in EH/s

• Alerts

• Configurable alerts for capitulation start, recovery, and buy signals

⸻

How It Works

1. Data Source: Fetches daily hash rate values from a selected provider (e.g., IntoTheBlock, Quandl).

2. Capitulation Detection: When the 30-day SMA falls below the 60-day SMA, miners are likely capitulating.

3. Recovery Identification: A rising 30-day SMA during capitulation signals miner recovery.

4. Buy Signal: Confirmed when the hash rate recovery coincides with a bullish shift in price momentum (10-day price SMA > 20-day price SMA).

⸻

Inputs

Hash Rate Short SMA: 30 days

Hash Rate Long SMA: 60 days

Plot Signals: On

Plot Halvings: Off

Plot Raw Hash Rate: Off

⸻

Considerations

• Timeframe: Best applied on daily charts to capture meaningful miner behavior.

• Data Reliability: Ensure the chosen hash rate source provides consistent, gap-free data.

• Risk Management: Use alongside other technical indicators (e.g., RSI, MACD) and fundamental analysis.

• Backtesting: Evaluate performance over different market cycles before live deployment.

Bear Market Probability Model# Bear Market Probability Model: A Multi-Factor Risk Assessment Framework

The Bear Market Probability Model represents a comprehensive quantitative framework for assessing systemic market risk through the integration of 13 distinct risk factors across four analytical categories: macroeconomic indicators, technical analysis factors, market sentiment measures, and market breadth metrics. This indicator synthesizes established financial research methodologies to provide real-time probabilistic assessments of impending bear market conditions, offering institutional-grade risk management capabilities to retail and professional traders alike.

## Theoretical Foundation

### Historical Context of Bear Market Prediction

Bear market prediction has been a central focus of financial research since the seminal work of Dow (1901) and the subsequent development of technical analysis theory. The challenge of predicting market downturns gained renewed academic attention following the market crashes of 1929, 1987, 2000, and 2008, leading to the development of sophisticated multi-factor models.

Fama and French (1989) demonstrated that certain financial variables possess predictive power for stock returns, particularly during market stress periods. Their three-factor model laid the groundwork for multi-dimensional risk assessment, which this indicator extends through the incorporation of real-time market microstructure data.

### Methodological Framework

The model employs a weighted composite scoring methodology based on the theoretical framework established by Campbell and Shiller (1998) for market valuation assessment, extended through the incorporation of high-frequency sentiment and technical indicators as proposed by Baker and Wurgler (2006) in their seminal work on investor sentiment.

The mathematical foundation follows the general form:

Bear Market Probability = Σ(Wi × Ci) / ΣWi × 100

Where:

- Wi = Category weight (i = 1,2,3,4)

- Ci = Normalized category score

- Categories: Macroeconomic, Technical, Sentiment, Breadth

## Component Analysis

### 1. Macroeconomic Risk Factors

#### Yield Curve Analysis

The inclusion of yield curve inversion as a primary predictor follows extensive research by Estrella and Mishkin (1998), who demonstrated that the term spread between 3-month and 10-year Treasury securities has historically preceded all major recessions since 1969. The model incorporates both the 2Y-10Y and 3M-10Y spreads to capture different aspects of monetary policy expectations.

Implementation:

- 2Y-10Y Spread: Captures market expectations of monetary policy trajectory

- 3M-10Y Spread: Traditional recession predictor with 12-18 month lead time

Scientific Basis: Harvey (1988) and subsequent research by Ang, Piazzesi, and Wei (2006) established the theoretical foundation linking yield curve inversions to economic contractions through the expectations hypothesis of the term structure.

#### Credit Risk Premium Assessment

High-yield credit spreads serve as a real-time gauge of systemic risk, following the methodology established by Gilchrist and Zakrajšek (2012) in their excess bond premium research. The model incorporates the ICE BofA High Yield Master II Option-Adjusted Spread as a proxy for credit market stress.

Threshold Calibration:

- Normal conditions: < 350 basis points

- Elevated risk: 350-500 basis points

- Severe stress: > 500 basis points

#### Currency and Commodity Stress Indicators

The US Dollar Index (DXY) momentum serves as a risk-off indicator, while the Gold-to-Oil ratio captures commodity market stress dynamics. This approach follows the methodology of Akram (2009) and Beckmann, Berger, and Czudaj (2015) in analyzing commodity-currency relationships during market stress.

### 2. Technical Analysis Factors

#### Multi-Timeframe Moving Average Analysis

The technical component incorporates the well-established moving average convergence methodology, drawing from the work of Brock, Lakonishok, and LeBaron (1992), who provided empirical evidence for the profitability of technical trading rules.

Implementation:

- Price relative to 50-day and 200-day simple moving averages

- Moving average convergence/divergence analysis

- Multi-timeframe MACD assessment (daily and weekly)

#### Momentum and Volatility Analysis

The model integrates Relative Strength Index (RSI) analysis following Wilder's (1978) original methodology, combined with maximum drawdown analysis based on the work of Magdon-Ismail and Atiya (2004) on optimal drawdown measurement.

### 3. Market Sentiment Factors

#### Volatility Index Analysis

The VIX component follows the established research of Whaley (2009) and subsequent work by Bekaert and Hoerova (2014) on VIX as a predictor of market stress. The model incorporates both absolute VIX levels and relative VIX spikes compared to the 20-day moving average.

Calibration:

- Low volatility: VIX < 20

- Elevated concern: VIX 20-25

- High fear: VIX > 25

- Panic conditions: VIX > 30

#### Put-Call Ratio Analysis

Options flow analysis through put-call ratios provides insight into sophisticated investor positioning, following the methodology established by Pan and Poteshman (2006) in their analysis of informed trading in options markets.

### 4. Market Breadth Factors

#### Advance-Decline Analysis

Market breadth assessment follows the classic work of Fosback (1976) and subsequent research by Brown and Cliff (2004) on market breadth as a predictor of future returns.

Components:

- Daily advance-decline ratio

- Advance-decline line momentum

- McClellan Oscillator (Ema19 - Ema39 of A-D difference)

#### New Highs-New Lows Analysis

The new highs-new lows ratio serves as a market leadership indicator, based on the research of Zweig (1986) and validated in academic literature by Zarowin (1990).

## Dynamic Threshold Methodology

The model incorporates adaptive thresholds based on rolling volatility and trend analysis, following the methodology established by Pagan and Sossounov (2003) for business cycle dating. This approach allows the model to adjust sensitivity based on prevailing market conditions.

Dynamic Threshold Calculation:

- Warning Level: Base threshold ± (Volatility × 1.0)

- Danger Level: Base threshold ± (Volatility × 1.5)

- Bounds: ±10-20 points from base threshold

## Professional Implementation

### Institutional Usage Patterns

Professional risk managers typically employ multi-factor bear market models in several contexts:

#### 1. Portfolio Risk Management

- Tactical Asset Allocation: Reducing equity exposure when probability exceeds 60-70%

- Hedging Strategies: Implementing protective puts or VIX calls when warning thresholds are breached

- Sector Rotation: Shifting from growth to defensive sectors during elevated risk periods

#### 2. Risk Budgeting

- Value-at-Risk Adjustment: Incorporating bear market probability into VaR calculations

- Stress Testing: Using probability levels to calibrate stress test scenarios

- Capital Requirements: Adjusting regulatory capital based on systemic risk assessment

#### 3. Client Communication

- Risk Reporting: Quantifying market risk for client presentations

- Investment Committee Decisions: Providing objective risk metrics for strategic decisions

- Performance Attribution: Explaining defensive positioning during market stress

### Implementation Framework

Professional traders typically implement such models through:

#### Signal Hierarchy:

1. Probability < 30%: Normal risk positioning

2. Probability 30-50%: Increased hedging, reduced leverage

3. Probability 50-70%: Defensive positioning, cash building

4. Probability > 70%: Maximum defensive posture, short exposure consideration

#### Risk Management Integration:

- Position Sizing: Inverse relationship between probability and position size

- Stop-Loss Adjustment: Tighter stops during elevated risk periods

- Correlation Monitoring: Increased attention to cross-asset correlations

## Strengths and Advantages

### 1. Comprehensive Coverage

The model's primary strength lies in its multi-dimensional approach, avoiding the single-factor bias that has historically plagued market timing models. By incorporating macroeconomic, technical, sentiment, and breadth factors, the model provides robust risk assessment across different market regimes.

### 2. Dynamic Adaptability

The adaptive threshold mechanism allows the model to adjust sensitivity based on prevailing volatility conditions, reducing false signals during low-volatility periods and maintaining sensitivity during high-volatility regimes.

### 3. Real-Time Processing

Unlike traditional academic models that rely on monthly or quarterly data, this indicator processes daily market data, providing timely risk assessment for active portfolio management.

### 4. Transparency and Interpretability

The component-based structure allows users to understand which factors are driving risk assessment, enabling informed decision-making about model signals.

### 5. Historical Validation

Each component has been validated in academic literature, providing theoretical foundation for the model's predictive power.

## Limitations and Weaknesses

### 1. Data Dependencies

The model's effectiveness depends heavily on the availability and quality of real-time economic data. Federal Reserve Economic Data (FRED) updates may have lags that could impact model responsiveness during rapidly evolving market conditions.

### 2. Regime Change Sensitivity

Like most quantitative models, the indicator may struggle during unprecedented market conditions or structural regime changes where historical relationships break down (Taleb, 2007).

### 3. False Signal Risk

Multi-factor models inherently face the challenge of balancing sensitivity with specificity. The model may generate false positive signals during normal market volatility periods.

### 4. Currency and Geographic Bias

The model focuses primarily on US market indicators, potentially limiting its effectiveness for global portfolio management or non-USD denominated assets.

### 5. Correlation Breakdown

During extreme market stress, correlations between risk factors may increase dramatically, reducing the model's diversification benefits (Forbes and Rigobon, 2002).

## References

Akram, Q. F. (2009). Commodity prices, interest rates and the dollar. Energy Economics, 31(6), 838-851.

Ang, A., Piazzesi, M., & Wei, M. (2006). What does the yield curve tell us about GDP growth? Journal of Econometrics, 131(1-2), 359-403.

Baker, M., & Wurgler, J. (2006). Investor sentiment and the cross‐section of stock returns. The Journal of Finance, 61(4), 1645-1680.

Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593-1636.

Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics, 116(1), 261-292.

Beckmann, J., Berger, T., & Czudaj, R. (2015). Does gold act as a hedge or a safe haven for stocks? A smooth transition approach. Economic Modelling, 48, 16-24.

Bekaert, G., & Hoerova, M. (2014). The VIX, the variance premium and stock market volatility. Journal of Econometrics, 183(2), 181-192.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. The Journal of Finance, 47(5), 1731-1764.

Brown, G. W., & Cliff, M. T. (2004). Investor sentiment and the near-term stock market. Journal of Empirical Finance, 11(1), 1-27.

Campbell, J. Y., & Shiller, R. J. (1998). Valuation ratios and the long-run stock market outlook. The Journal of Portfolio Management, 24(2), 11-26.

Dow, C. H. (1901). Scientific stock speculation. The Magazine of Wall Street.

Estrella, A., & Mishkin, F. S. (1998). Predicting US recessions: Financial variables as leading indicators. Review of Economics and Statistics, 80(1), 45-61.

Fama, E. F., & French, K. R. (1989). Business conditions and expected returns on stocks and bonds. Journal of Financial Economics, 25(1), 23-49.

Forbes, K. J., & Rigobon, R. (2002). No contagion, only interdependence: measuring stock market comovements. The Journal of Finance, 57(5), 2223-2261.

Fosback, N. G. (1976). Stock market logic: A sophisticated approach to profits on Wall Street. The Institute for Econometric Research.

Gilchrist, S., & Zakrajšek, E. (2012). Credit spreads and business cycle fluctuations. American Economic Review, 102(4), 1692-1720.

Harvey, C. R. (1988). The real term structure and consumption growth. Journal of Financial Economics, 22(2), 305-333.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Magdon-Ismail, M., & Atiya, A. F. (2004). Maximum drawdown. Risk, 17(10), 99-102.

Nickerson, R. S. (1998). Confirmation bias: A ubiquitous phenomenon in many guises. Review of General Psychology, 2(2), 175-220.

Pagan, A. R., & Sossounov, K. A. (2003). A simple framework for analysing bull and bear markets. Journal of Applied Econometrics, 18(1), 23-46.

Pan, J., & Poteshman, A. M. (2006). The information in option volume for future stock prices. The Review of Financial Studies, 19(3), 871-908.

Taleb, N. N. (2007). The black swan: The impact of the highly improbable. Random House.

Whaley, R. E. (2009). Understanding the VIX. The Journal of Portfolio Management, 35(3), 98-105.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

Zarowin, P. (1990). Size, seasonality, and stock market overreaction. Journal of Financial and Quantitative Analysis, 25(1), 113-125.

Zweig, M. E. (1986). Winning on Wall Street. Warner Books.

Moving Average Shift WaveTrend StrategyMoving Average Shift WaveTrend Strategy

🧭 Overview

The Moving Average Shift WaveTrend Strategy is a trend-following and momentum-based trading system designed to be overlayed on TradingView charts. It executes trades based on the confluence of multiple technical conditions—volatility, session timing, trend direction, and oscillator momentum—to deliver logical and systematic trade entries and exits.

🎯 Strategy Objectives

Enter trades aligned with the prevailing long-term trend

Exit trades on confirmed momentum reversals

Avoid false signals using session timing and volatility filters

Apply structured risk management with automatic TP, SL, and trailing stops

⚙️ Key Features

Selectable MA types: SMA, EMA, SMMA (RMA), WMA, VWMA

Dual-filter logic using a custom oscillator and moving averages

Session and volatility filters to eliminate low-quality setups

Trailing stop, configurable Take Profit / Stop Loss logic

“In-wave flag” prevents overtrading within the same trend wave

Visual clarity with color-shifting candles and entry/exit markers

📈 Trading Rules

✅ Long Entry Conditions:

Price is above the selected MA

Oscillator is positive and rising

200-period EMA indicates an uptrend

ATR exceeds its median value (sufficient volatility)

Entry occurs between 09:00–17:00 (exchange time)

Not currently in an active wave

🔻 Short Entry Conditions:

Price is below the selected MA

Oscillator is negative and falling

200-period EMA indicates a downtrend

All other long-entry conditions are inverted

❌ Exit Conditions:

Take Profit or Stop Loss is hit

Opposing signals from oscillator and MA

Trailing stop is triggered

🛡️ Risk Management Parameters

Pair: ETH/USD

Timeframe: 4H

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 2% of account equity (adjustable)

Total Trades: 224

Backtest Period: May 24, 2016 — April 7, 2025

Note: Risk parameters are fully customizable to suit your trading style and broker conditions.

🔧 Trading Parameters & Filters

Time Filter: Trades allowed only between 09:00–17:00 (exchange time)

Volatility Filter: ATR must be above its median value

Trend Filter: Long-term 200-period EMA

📊 Technical Settings

Moving Average

Type: SMA

Length: 40

Source: hl2

Oscillator

Length: 15

Threshold: 0.5

Risk Management

Take Profit: 1.5%

Stop Loss: 1.0%

Trailing Stop: 1.0%

👁️ Visual Support

MA and oscillator color changes indicate directional bias

Clear chart markers show entry and exit points

Trailing stops and risk controls are transparently managed

🚀 Strategy Improvements & Uniqueness

In-wave flag avoids repeated entries within the same trend phase

Filtering based on time, volatility, and trend ensures higher-quality trades

Dynamic high/low tracking allows precise trailing stop placement

Fully rule-based execution reduces emotional decision-making

💡 Inspirations & Attribution

This strategy is inspired by the excellent concept from:

ChartPrime – “Moving Average Shift”

It expands on the original idea with advanced trade filters and trailing logic.

Source reference:

📌 Summary

The Moving Average Shift WaveTrend Strategy offers a rule-based, reliable approach to trend trading. By combining trend and momentum filters with robust risk controls, it provides a consistent framework suitable for various market conditions and trading styles.

⚠️ Disclaimer

This script is for educational purposes only. Trading involves risk. Always use proper backtesting and risk evaluation before applying in live markets.

Bitcoin Halving DatesBitcoin Halving Dates Indicator

This custom indicator automatically marks Bitcoin's key halving events by drawing vertical lines on your chart. It highlights the historical halving dates (2012, 2016, 2020) and includes an estimated date for the upcoming halving in 2024, making it easy to visualize significant supply events that can influence market trends.

Features:

Automated Markings: Displays vertical lines on the first bar of each halving day.

Customizable: Easily adjust halving dates and styling options to suit your analysis.

Built for Traders: Enhance your technical analysis by keeping track of pivotal market events.

Use this indicator to gain a visual edge by integrating critical Bitcoin halving events into your trading strategy. Happy Trading!

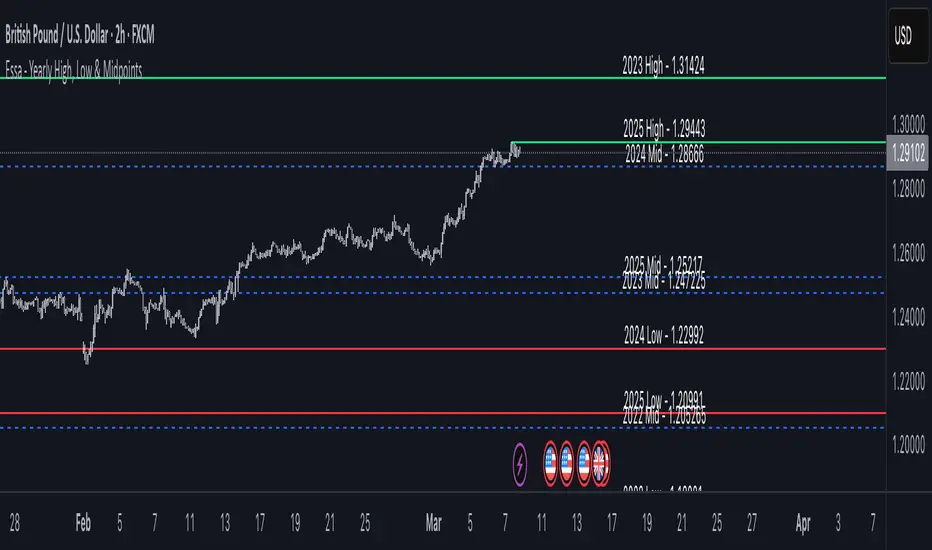

Essa - Yearly High, Low & MidYearly High, Low & Midpoint Indicator

This TradingView indicator helps traders track key yearly price levels by plotting the high, low, and midpoint values for each year within a user-specified range.

Features & Functionality:

Automatic Yearly Calculation: Determines the highest and lowest price for each year and computes the midpoint as their average.

Clear & Customisable Visuals:

The Yearly High is plotted as a solid green line.

The Yearly Low appears as a solid red line.

The Midpoint is displayed as a blue dashed line for easy distinction

Detailed Labels:

Each level is labeled at the far right of the chart, showing the year, level type (High, Low, or Mid), and price (e.g., 2016 High - 1.20000).

Labels are right-aligned in white, ensuring clear visibility against any background.

This indicator is perfect for traders who rely on long-term technical analysis, providing a quick and structured way to visualise significant yearly price levels.

Mark Minervini Buy Signal# Mark Minervini Buy Signal Indicator

This indicator implements Mark Minervini's "Stage 2 Uptrend" buy criteria from his SEPA (Specific Entry Point Analysis) methodology as described in his books "Trade Like a Stock Market Wizard" and "Think & Trade Like a Champion". The script identifies potential buy setups based on Minervini's technical criteria for stocks showing strong momentum characteristics.

## How It Works

The indicator evaluates various technical conditions to identify stocks in a Stage 2 uptrend according to Minervini's methodology:

1. **Moving Average Alignment**

- 150-day MA above 200-day MA (confirming overall uptrend)

- 200-day MA trending up (compared to 20 days ago)

- 50-day MA above both 150-day and 200-day MAs (showing recent strength)

- Price above all major moving averages (50, 150, 200-day MAs)

2. **Price Relative to 52-Week Range**

- Price at least 25% above 52-week low (showing strong recovery)

- Price within 75-95% of 52-week high (room for further upside)

3. **Relative Strength**

- Stock ranks in the top 30% based on 100-day price performance

- This implements Minervini's emphasis on buying only strong performers

4. **Volume Criteria**

- Volume above its 50-day moving average (showing increasing interest)

## How to Use This Indicator

When all conditions are met, the indicator displays a green triangle below the price bar and colors the background green. These signals identify potential candidates for further analysis. According to Minervini's methodology, you should:

1. Use this as a screening tool to identify potential candidates

2. Perform additional chart analysis to identify specific entry points

3. Look for decreased volatility and proper bases or consolidation patterns

4. Consider broader market conditions and sector strength before entering

## Sources and Credit

This indicator is based on Mark Minervini's trading methodology as outlined in:

1. Minervini, Mark. "Trade Like a Stock Market Wizard: How to Achieve Super Performance in Stocks in Any Market" (2013)

2. Minervini, Mark. "Think & Trade Like a Champion: The Secrets, Rules & Blunt Truths of a Stock Market Wizard" (2016)

3. Minervini, Mark. "Mindset Secrets for Winning: How to Bring Personal Power to Everything You Do" (2019)

4. Interviews and workshops where Minervini has described his SEPA methodology

The specific criteria implemented are derived from Minervini's "Stage Analysis" framework, particularly focusing on Stage 2 uptrends which he considers optimal for buying opportunities.

## Disclaimer

This indicator is provided for informational purposes only. It attempts to reproduce Minervini's published criteria but should be used as part of a complete trading strategy with proper risk management. Minervini's complete methodology includes additional subjective elements that cannot be fully automated.

BTC Seasonality Strategy (Weekly)This strategy identifies potential weekend opportunities in Bitcoin (BTC) markets by leveraging the concept of seasonality, entering a position at a predefined time and day, and exiting at a specified time and day.

Key Features

Customizable Time and Day Selection:

Users can select the entry and exit days and corresponding times (in EST).

Directional Flexibility:

The strategy allows traders to choose between long or short positions.

TradingView Compliance:

The script adheres to TradingView's house rules, avoids overly complex conditions, and provides clear user-configurable inputs.

How It Works

The script determines the current weekday and hour in EST, converting TradingView's UTC time for accurate comparisons.

If the current day and hour match the selected entry conditions, a trade (long or short) is opened.

The position is closed when the current day and hour match the specified exit conditions.

Theoretical Basis

Market Seasonality:

The concept of seasonality in financial markets refers to predictable patterns based on time, such as weekends or specific days of the week. Studies have shown that cryptocurrency markets exhibit unique trading behaviors during weekends due to reduced institutional activity and higher retail participation behavioral Biases**:

Retail traders often dominate weekend markets, potentially causing predictable inefficiencies .

Reverences**

Baur, D. G., Hong, K., & Lee, A. D. (2018). Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money, 54, 177–189.

Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letters, 148, 80–82.

McRib Bull Market Indicator# McRib Bull Market Indicator

## Overview

The McRib Bull Market Indicator is a unique technical analysis tool that marks McDonald's McRib sandwich release dates on your trading charts. While seemingly unconventional, this indicator serves as a fascinating historical reference point for market analysis, particularly for studying periods of market expansion.

## Key Features

- Visual yellow labels marking verified McRib release dates from 2012 to 2024

- Clean, unobtrusive design that overlays on any chart timeframe

- Covers both U.S. and international releases (including UK and Australia)

## Historical Reference Points

The indicator includes release dates from:

- December 2012

- October-December 2014

- January 2015

- October 2016

- November 2017

- October 2018

- October 2019

- December 2020

- October 2022

- November 2023

- December 2024

## Usage Guide

1. Add the indicator to any chart by searching for "McRib Bull Market Indicator"

2. The indicator will automatically display yellow labels above price candles on McRib release dates

3. Use these reference points to:

- Analyze market conditions during McRib releases

- Study potential correlations between releases and market movements

- Compare market behavior across different McRib release periods

- Identify any patterns in market expansion phases coinciding with releases

## Trading Application

While initially created as a novelty indicator, it can be used to:

- Mark specific historical points of reference for broader market analysis

- Study potential market psychology around major promotional events

- Compare seasonal market patterns with recurring release dates

- Analyze market expansion phases that coincide with releases

Remember: While this indicator provides interesting historical reference points, it should be used as part of a comprehensive trading strategy rather than as a standalone trading signal.

Pulse DPO: Major Cycle Tops and Bottoms█ OVERVIEW

Pulse DPO is an oscillator designed to highlight Major Cycle Tops and Bottoms .

It works on any market driven by cycles. It operates by removing the short-term noise from the price action and focuses on the market's cyclical nature.

This indicator uses a Normalized version of the Detrended Price Oscillator (DPO) on a 0-100 scale, making it easier to identify major tops and bottoms.

Credit: The DPO was first developed by William Blau in 1991.

█ HOW TO READ IT

Pulse DPO oscillates in the range between 0 and 100. A value in the upper section signals an OverBought (OB) condition, while a value in the lower section signals an OverSold (OS) condition.

Generally, the triggering of OB and OS conditions don't necessarily translate into swing tops and bottoms, but rather suggest caution on approaching a market that might be overextended.

Nevertheless, this indicator has been customized to trigger the signal only during remarkable top and bottom events.

I suggest using it on the Daily Time Frame , but you're free to experiment with this indicator on other time frames.

The indicator has Built-in Alerts to signal the crossing of the Thresholds. Please don't act on an isolated signal, but rather integrate it to work in conjunction with the indicators present in your Trading Plan.

█ OB SIGNAL ON: ENTERING OVERBOUGHT CONDITION

When Pulse DPO crosses Above the Top Threshold it Triggers ON the OB signal. At this point the oscillator line shifts to OB color.

When Pulse DPO enters the OB Zone, please beware! In this Area the Major Players usually become Active Sellers to the Public. While the OB signal is On, it might be wise to Consider Selling a portion or the whole Long Position.

Please note that even though this indicator aims to focus on major tops and bottoms, a strong trending market might trigger the OB signal and stay with it for a long time. That's especially true on young markets and on bubble-mode markets.

█ OB SIGNAL OFF: EXITING OVERBOUGHT CONDITION

When Pulse DPO crosses Below the Top Threshold it Triggers OFF the OB signal. At this point the oscillator line shifts to its normal color.

When Pulse DPO exits the OB Zone, please beware because a Major Top might just have occurred. In this Area the Major Players usually become Aggressive Sellers. They might wind up any remaining Long Positions and Open new Short Positions.

This might be a good area to Open Shorts or to Close/Reverse any remaining Long Position. Whatever you choose to do, it's usually best to act quickly because the market is prone to enter into panic mode.

█ OS SIGNAL ON: ENTERING OVERSOLD CONDITION

When Pulse DPO crosses Below the Bottom Threshold it Triggers ON the OS signal. At this point the oscillator line shifts to OS color.

When Pulse DPO enters the OS Zone, please beware because in this Area the Major Players usually become Active Buyers accumulating Long Positions from the desperate Public.

While the OS signal is On, it might be wise to Consider becoming a Buyer or to implement a Dollar-Cost Averaging (DCA) Strategy to build a Long Position towards the next Cycle. In contrast to the tops, the OS state usually takes longer to resolve a major bottom.

█ OS SIGNAL OFF: EXITING OVERSOLD CONDITION

When Pulse DPO crosses Above the Bottom Threshold it Triggers OFF the OS signal. At this point the oscillator line shifts to its normal color.

When Pulse DPO exits the OS Zone, please beware because a Major Bottom might already be in place. In this Area the Major Players become Aggresive Buyers. They might wind up any remaining Short Positions and Open new Long Positions.

This might be a good area to Open Longs or to Close/Reverse any remaining Short Positions.

█ WHY WOULD YOU BE INTERESTED IN THIS INDICATOR?

This indicator is built over a solid foundation capable of signaling Major Cycle Tops and Bottoms across many markets. Let's see some examples:

Early Bitcoin Years: From 0 to 1242

This chart is in logarithmic mode in order to properly display various exponential cycles. Pulse DPO is properly signaling the major early highs from 9-Jun-2011 at 31.50, to the next one on 9-Apr-2013 at 240 and the epic top from 29-Nov-2013 at 1242.

Due to the massive price movements, the OB condition stays pinned during most of the exponential price action. But as you can see, the OB condition quickly vanishes once the Cycle Top has been reached. As the market matures, the OB condition becomes more exceptional and triggers much closer from the Cycle Top.

With regards to Cycle Bottoms, the early bottom of 2 after having peaked at 31.50 doesn’t get captured by the indicator. That is the only cycle bottom that escapes the Pulse DPO when the bottom threshold is set at a value of 5. In that event, the oscillator low reached 6.95.

Bitcoin Adoption Spreading: From 257 to 73k

This chart is in logarithmic mode in order to properly display various exponential cycles. Pulse DPO is properly signaling all the major highs from 17-Dec-2017 at 19k, to the next one on 14-Apr-2021 at 64k and the most recent top from 9-Nov-2021 at 68k.

During the massive run of 2017, the OB condition still stayed triggered for a few weeks on each swing top. But on the next cycles it started to signal only for a few days before each swing top actually happened. The OB condition during the last cycle top triggered only for 3 days. Therefore the signal grows in focus as the market matures.

At the time of publishing this indicator, Bitcoin printed a new All Time High (ATH) on 13-Mar-2024 at 73k. That run didn’t trigger the OB condition. Therefore, if the indicator is correct the Bitcoin market still has some way to grow during the next months.

With regards to Cycle Bottoms, the bottom of 3k after having peaked at19k got captured within the wide OS zone. The bottom of 15k after having peaked at 68k got captured too within the OS accumulation area.

Gold

Pulse DPO behaves surprisingly well on a long standing market such as Gold. Moving back to the 197x years it’s been signaling most Cycle Tops and Bottoms with precision. During the last cycle, it shows topping at 2k and bottoming at 1.6k.

The current price action is signaling OB condition in the range of 2.5k to 2.7k. Looking at past cycles, it tends to trigger on and off at multiple swing tops until reaching the final cycle top. Therefore this might indicate the first wave within a potential gold run.

Oil

On the Oil market, we can see that most of the cycle tops and bottoms since the 80s got signaled. The only exception being the low from 2020 which didn’t trigger.

EURUSD

On Forex markets the Pulse DPO also behaves as expected. Looking back at EURUSD we can see the marketing triggering OB and OS conditions during major cycle tops and bottoms from recent times until the 80s.

S&P 500

On the S&P 500 the Pulse DPO catched the lows from 2016 and 2020. Looking at present price action, the recent ATH didn’t trigger the OB condition. Therefore, the indicator is allowing room for another leg up during the next months.

Amazon

On the Amazon chart the Pulse DPO is mirroring pretty accurately the major swings. Scrolling back to the early 2000s, this chart resembles early exponential swings in the crypto space.

Tesla

Moving onto a younger tech stock, Pulse DPO captures pretty accurately the major tops and bottoms. The chart is shown in logarithmic scale to better display the magnitude of the moves.

█ SETTINGS

This indicator is ideal for identifying major market turning points while filtering out short-term noise. You are free to adjust the parameters to align with your preferred trading style.

Parameters : This section allows you to customize any of the Parameters that shape the Oscillator.

Oscillator Length: Defines the period for calculating the Oscillator.

Offset: Shifts the oscillator calculation by a certain number of periods, which is typically half the Oscillator Length.

Lookback Period: Specifies how many bars to look back to find tops and bottoms for normalization.

Smoothing Length: Determines the length of the moving average used to smooth the oscillator.

Thresholds : This section allows you to customize the Thresholds that trigger the OB and OS conditions.

Top: Defines the value of the Top Threshold.

Bottom: Defines the value of the Bottom Threshold.

Intellect_city - Halvings Bitcoin CycleWhat is halving?

The halving timer shows when the next Bitcoin halving will occur, as well as the dates of past halvings. This event occurs every 210,000 blocks, which is approximately every 4 years. Halving reduces the emission reward by half. The original Bitcoin reward was 50 BTC per block found.

Why is halving necessary?

Halving allows you to maintain an algorithmically specified emission level. Anyone can verify that no more than 21 million bitcoins can be issued using this algorithm. Moreover, everyone can see how much was issued earlier, at what speed the emission is happening now, and how many bitcoins remain to be mined in the future. Even a sharp increase or decrease in mining capacity will not significantly affect this process. In this case, during the next difficulty recalculation, which occurs every 2014 blocks, the mining difficulty will be recalculated so that blocks are still found approximately once every ten minutes.

How does halving work in Bitcoin blocks?

The miner who collects the block adds a so-called coinbase transaction. This transaction has no entry, only exit with the receipt of emission coins to your address. If the miner's block wins, then the entire network will consider these coins to have been obtained through legitimate means. The maximum reward size is determined by the algorithm; the miner can specify the maximum reward size for the current period or less. If he puts the reward higher than possible, the network will reject such a block and the miner will not receive anything. After each halving, miners have to halve the reward they assign to themselves, otherwise their blocks will be rejected and will not make it to the main branch of the blockchain.

The impact of halving on the price of Bitcoin

It is believed that with constant demand, a halving of supply should double the value of the asset. In practice, the market knows when the halving will occur and prepares for this event in advance. Typically, the Bitcoin rate begins to rise about six months before the halving, and during the halving itself it does not change much. On average for past periods, the upper peak of the rate can be observed more than a year after the halving. It is almost impossible to predict future periods because, in addition to the reduction in emissions, many other factors influence the exchange rate. For example, major hacks or bankruptcies of crypto companies, the situation on the stock market, manipulation of “whales,” or changes in legislative regulation.

---------------------------------------------

Table - Past and future Bitcoin halvings:

---------------------------------------------

Date: Number of blocks: Award:

0 - 03-01-2009 - 0 block - 50 BTC

1 - 28-11-2012 - 210000 block - 25 BTC

2 - 09-07-2016 - 420000 block - 12.5 BTC

3 - 11-05-2020 - 630000 block - 6.25 BTC

4 - 20-04-2024 - 840000 block - 3.125 BTC

5 - 24-03-2028 - 1050000 block - 1.5625 BTC

6 - 26-02-2032 - 1260000 block - 0.78125 BTC

7 - 30-01-2036 - 1470000 block - 0.390625 BTC

8 - 03-01-2040 - 1680000 block - 0.1953125 BTC

9 - 07-12-2043 - 1890000 block - 0.09765625 BTC

10 - 10-11-2047 - 2100000 block - 0.04882813 BTC

11 - 14-10-2051 - 2310000 block - 0.02441406 BTC

12 - 17-09-2055 - 2520000 block - 0.01220703 BTC

13 - 21-08-2059 - 2730000 block - 0.00610352 BTC

14 - 25-07-2063 - 2940000 block - 0.00305176 BTC

15 - 28-06-2067 - 3150000 block - 0.00152588 BTC

16 - 01-06-2071 - 3360000 block - 0.00076294 BTC

17 - 05-05-2075 - 3570000 block - 0.00038147 BTC

18 - 08-04-2079 - 3780000 block - 0.00019073 BTC

19 - 12-03-2083 - 3990000 block - 0.00009537 BTC

20 - 13-02-2087 - 4200000 block - 0.00004768 BTC

21 - 17-01-2091 - 4410000 block - 0.00002384 BTC

22 - 21-12-2094 - 4620000 block - 0.00001192 BTC

23 - 24-11-2098 - 4830000 block - 0.00000596 BTC

24 - 29-10-2102 - 5040000 block - 0.00000298 BTC

25 - 02-10-2106 - 5250000 block - 0.00000149 BTC

26 - 05-09-2110 - 5460000 block - 0.00000075 BTC

27 - 09-08-2114 - 5670000 block - 0.00000037 BTC

28 - 13-07-2118 - 5880000 block - 0.00000019 BTC

29 - 16-06-2122 - 6090000 block - 0.00000009 BTC

30 - 20-05-2126 - 6300000 block - 0.00000005 BTC

31 - 23-04-2130 - 6510000 block - 0.00000002 BTC

32 - 27-03-2134 - 6720000 block - 0.00000001 BTC