Variety N-Tuple Moving Averages w/ Variety Stepping [Loxx]Variety N-Tuple Moving Averages w/ Variety Stepping is a moving average indicator that allows you to create 1- 30 tuple moving average types; i.e., Double-MA, Triple-MA, Quadruple-MA, Quintuple-MA, ... N-tuple-MA. This version contains 2 different moving average types. For example, using "50" as the depth will give you Quinquagintuple Moving Average. If you'd like to find the name of the moving average type you create with the depth input with this indicator, you can find a list of tuples here: Tuples extrapolated

Due to the coding required to adapt a moving average to fit into this indicator, additional moving average types will be added as they are created to fit into this unique use case. Since this is a work in process, there will be many future updates of this indicator. For now, you can choose from either EMA or RMA.

This indicator is also considered one of the top 10 forex indicators. See details here: forex-station.com

Additionally, this indicator is a computationally faster, more streamlined version of the following indicators with the addition of 6 stepping functions and 6 different bands/channels types.

STD-Stepped, Variety N-Tuple Moving Averages

STD-Stepped, Variety N-Tuple Moving Averages is the standard deviation stepped/filtered indicator of the following indicator

Last but not least, a big shoutout to @lejmer for his help in formulating a looping solution for this streamlined version. this indicator is speedy even at 50 orders deep. You can find his scripts here: www.tradingview.com

How this works

Step 1: Run factorial calculation on the depth value,

Step 2: Calculate weights of nested moving averages

factorial(depth) / (factorial(depth - k) * factorial(k); where depth is the depth and k is the weight position

Examples of coefficient outputs:

6 Depth: 6 15 20 15 6

7 Depth: 7 21 35 35 21 7

8 Depth: 8 28 56 70 56 28 8

9 Depth: 9 36 34 84 126 126 84 36 9

10 Depth: 10 45 120 210 252 210 120 45 10

11 Depth: 11 55 165 330 462 462 330 165 55 11

12 Depth: 12 66 220 495 792 924 792 495 220 66 12

13 Depth: 13 78 286 715 1287 1716 1716 1287 715 286 78 13

Step 3: Apply coefficient to each moving average

For QEMA, which is 5 depth EMA , the calculation is as follows

ema1 = ta. ema ( src , length)

ema2 = ta. ema (ema1, length)

ema3 = ta. ema (ema2, length)

ema4 = ta. ema (ema3, length)

ema5 = ta. ema (ema4, length)

In this new streamlined version, these MA calculations are packed into an array inside loop so Pine doesn't have to keep all possible series information in memory. This is handled with the following code:

temp = array.get(workarr, k + 1) + alpha * (array.get(workarr, k) - array.get(workarr, k + 1))

array.set(workarr, k + 1, temp)

After we pack the array, we apply the coefficients to derive the NTMA:

qema = 5 * ema1 - 10 * ema2 + 10 * ema3 - 5 * ema4 + ema5

Stepping calculations

First off, you can filter by both price and/or MA output. Both price and MA output can be filtered/stepped in their own way. You'll see two selectors in the input settings. Default is ATR ATR. Here's how stepping works in simple terms: if the price/MA output doesn't move by X deviations, then revert to the price/MA output one bar back.

ATR

The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.

Standard Deviation

Standard deviation is a statistic that measures the dispersion of a dataset relative to its mean and is calculated as the square root of the variance. The standard deviation is calculated as the square root of variance by determining each data point's deviation relative to the mean. If the data points are further from the mean, there is a higher deviation within the data set; thus, the more spread out the data, the higher the standard deviation.

Adaptive Deviation

By definition, the Standard Deviation (STD, also represented by the Greek letter sigma σ or the Latin letter s) is a measure that is used to quantify the amount of variation or dispersion of a set of data values. In technical analysis we usually use it to measure the level of current volatility .

Standard Deviation is based on Simple Moving Average calculation for mean value. This version of standard deviation uses the properties of EMA to calculate what can be called a new type of deviation, and since it is based on EMA , we can call it EMA deviation. And added to that, Perry Kaufman's efficiency ratio is used to make it adaptive (since all EMA type calculations are nearly perfect for adapting).

The difference when compared to standard is significant--not just because of EMA usage, but the efficiency ratio makes it a "bit more logical" in very volatile market conditions.

See how this compares to Standard Devaition here:

Adaptive Deviation

Median Absolute Deviation

The median absolute deviation is a measure of statistical dispersion. Moreover, the MAD is a robust statistic, being more resilient to outliers in a data set than the standard deviation. In the standard deviation, the distances from the mean are squared, so large deviations are weighted more heavily, and thus outliers can heavily influence it. In the MAD, the deviations of a small number of outliers are irrelevant.

Because the MAD is a more robust estimator of scale than the sample variance or standard deviation, it works better with distributions without a mean or variance, such as the Cauchy distribution.

For this indicator, I used a manual recreation of the quantile function in Pine Script. This is so users have a full inside view into how this is calculated.

Efficiency-Ratio Adaptive ATR

Average True Range (ATR) is widely used indicator in many occasions for technical analysis . It is calculated as the RMA of true range. This version adds a "twist": it uses Perry Kaufman's Efficiency Ratio to calculate adaptive true range

See how this compares to ATR here:

ER-Adaptive ATR

Mean Absolute Deviation

The mean absolute deviation (MAD) is a measure of variability that indicates the average distance between observations and their mean. MAD uses the original units of the data, which simplifies interpretation. Larger values signify that the data points spread out further from the average. Conversely, lower values correspond to data points bunching closer to it. The mean absolute deviation is also known as the mean deviation and average absolute deviation.

This definition of the mean absolute deviation sounds similar to the standard deviation (SD). While both measure variability, they have different calculations. In recent years, some proponents of MAD have suggested that it replace the SD as the primary measure because it is a simpler concept that better fits real life.

For Pine Coders, this is equivalent of using ta.dev()

Bands/Channels

See the information above for how bands/channels are calculated. After the one of the above deviations is calculated, the channels are calculated as output +/- deviation * multiplier

Signals

Green is uptrend, red is downtrend, yellow "L" signal is Long, fuchsia "S" signal is short.

Included:

Alerts

Loxx's Expanded Source Types

Bar coloring

Signals

6 bands/channels types

6 stepping types

Related indicators

3-Pole Super Smoother w/ EMA-Deviation-Corrected Stepping

STD-Stepped Fast Cosine Transform Moving Average

ATR-Stepped PDF MA

Cari skrip untuk "12月4号是什么星座"

STD-Stepped, Variety N-Tuple Moving Averages [Loxx]STD-Stepped, Variety N-Tuple Moving Averages is the standard deviation stepped/filtered indicator of the following indicator

Variety N-Tuple Moving Averages is a moving average indicator that allows you to create 1- 30 tuple moving average types; i.e., Double-MA, Triple-MA, Quadruple-MA, Quintuple-MA, ... N-tuple-MA. This version contains 5 different moving average types including T3. A list of tuples can be found here if you'd like to name the order of the moving average by depth: Tuples extrapolated

STD-Stepped, You'll notice that this is a lot of code and could normally be packed into a single loop in order to extract the N-tuple MA, however due to Pine Script limitations and processing paradigm this is not possible ... yet.

If you choose the EMA option and select a depth of 2, this is the classic DEMA ; EMA with a depth of 3 is the classic TEMA , and so on and so forth this is to help you understand how this indicator works. This version of NTMA is restricted to a maximum depth of 30 or less. Normally this indicator would include 50 depths but I've cut this down to 30 to reduce indicator load time. In the future, I'll create an updated NTMA that allows for more depth levels.

This is considered one of the top ten indicators in forex. You can read more about it here: forex-station.com

How this works

Step 1: Run factorial calculation on the depth value,

Step 2: Calculate weights of nested moving averages

factorial(nemadepth) / (factorial(nemadepth - k) * factorial(k); where nemadepth is the depth and k is the weight position

Examples of coefficient outputs:

6 Depth: 6 15 20 15 6

7 Depth: 7 21 35 35 21 7

8 Depth: 8 28 56 70 56 28 8

9 Depth: 9 36 34 84 126 126 84 36 9

10 Depth: 10 45 120 210 252 210 120 45 10

11 Depth: 11 55 165 330 462 462 330 165 55 11

12 Depth: 12 66 220 495 792 924 792 495 220 66 12

13 Depth: 13 78 286 715 1287 1716 1716 1287 715 286 78 13

Step 3: Apply coefficient to each moving average

For QEMA, which is 5 depth EMA , the caculation is as follows

ema1 = ta. ema ( src , length)

ema2 = ta. ema (ema1, length)

ema3 = ta. ema (ema2, length)

ema4 = ta. ema (ema3, length)

ema5 = ta. ema (ema4, length)

qema = 5 * ema1 - 10 * ema2 + 10 * ema3 - 5 * ema4 + ema5

Included:

Alerts

Loxx's Expanded Source Types

Bar coloring

Signals

Standard deviation stepping

Variety N-Tuple Moving Averages [Loxx]Variety N-Tuple Moving Averages is a moving average indicator that allows you to create 1- 30 tuple moving average types; i.e., Double-MA, Triple-MA, Quadruple-MA, Quintuple-MA, ... N-tuple-MA. This version contains 5 different moving average types including T3. A list of tuples can be found here if you'd like to name the order of the moving average by depth: Tuples extrapolated

You'll notice that this is a lot of code and could normally be packed into a single loop in order to extract the N-tuple MA, however due to Pine Script limitations and processing paradigm this is not possible ... yet.

If you choose the EMA option and select a depth of 2, this is the classic DEMA; EMA with a depth of 3 is the classic TEMA, and so on and so forth this is to help you understand how this indicator works. This version of NTMA is restricted to a maximum depth of 30 or less. Normally this indicator would include 50 depths but I've cut this down to 30 to reduce indicator load time. In the future, I'll create an updated NTMA that allows for more depth levels.

This is considered one of the top ten indicators in forex. You can read more about it here: forex-station.com

How this works

Step 1: Run factorial calculation on the depth value,

Step 2: Calculate weights of nested moving averages

factorial(nemadepth) / (factorial(nemadepth - k) * factorial(k); where nemadepth is the depth and k is the weight position

Examples of coefficient outputs:

6 Depth: 6 15 20 15 6

7 Depth: 7 21 35 35 21 7

8 Depth: 8 28 56 70 56 28 8

9 Depth: 9 36 34 84 126 126 84 36 9

10 Depth: 10 45 120 210 252 210 120 45 10

11 Depth: 11 55 165 330 462 462 330 165 55 11

12 Depth: 12 66 220 495 792 924 792 495 220 66 12

13 Depth: 13 78 286 715 1287 1716 1716 1287 715 286 78 13

Step 3: Apply coefficient to each moving average

For QEMA, which is 5 depth EMA, the caculation is as follows

ema1 = ta.ema(src, length)

ema2 = ta.ema(ema1, length)

ema3 = ta.ema(ema2, length)

ema4 = ta.ema(ema3, length)

ema5 = ta.ema(ema4, length)

qema = 5 * ema1 - 10 * ema2 + 10 * ema3 - 5 * ema4 + ema5

Included:

Alerts

Loxx's Expanded Source Types

Bar coloring

Close v Open Moving Averages Strategy (Variable) [divonn1994]This is a simple moving average based strategy that works well with a few different coin pairings. It takes the moving average 'opening' price and plots it, then takes the moving average 'closing' price and plots it, and then decides to enter a 'long' position or exit it based on whether the two lines have crossed each other. The reasoning is that it 'enters' a position when the average closing price is increasing. This could indicate upwards momentum in prices in the future. It then exits the position when the average closing price is decreasing. This could indicate downwards momentum in prices in the future. This is only speculative, though, but sometimes it can be a very good indicator/strategy to predict future action.

What I've found is that there are a lot of coins that respond very well when the appropriate combination of: 1) type of moving average is chosen (EMA, SMA, RMA, WMA or VWMA) & 2) number of previous bars averaged (typically 10 - 250 bars) are chosen.

Depending on the coin.. each combination of MA and Number of Bars averaged can have completely different levels of success.

Example of Usage:

An example would be that the VWMA works well for BTCUSD (BitStamp), but it has different successfulness based on the time frame. For the 12 hour bar timeframe, with the 66 bar average with the VWMA I found the most success. The next best successful combo I've found is for the 1 Day bar timeframe with the 35 bar average with the VWMA.. They both have a moving average that records about a month, but each have a different successfulness. Below are a few pair combos I think are noticeable because of the net profit, but there are also have a lot of potential coins with different combos:

It's interesting to see the strategy tester change as you change the settings. The below pairs are just some of the most interesting examples I've found, but there might be other combos I haven't even tried on different coin pairs..

Some strategy settings:

BTCUSD (BitStamp) 12 Hr Timeframe : 66 bars, VWMA=> 10,387x net profit

BTCUSD (BitStamp) 1 Day Timeframe : 35 bars, VWMA=> 7,805x net profit

BNBUSD (Binance) 12 Hr Timeframe : 27 bars, VWMA => 15,484x net profit

ETHUSD (BitStamp) 16 Hr Timeframe : 60 bars, SMA => 5,498x net profit

XRPUSD (BitStamp) 16 Hr Timeframe : 33 bars, SMA => 10,178x net profit

I only chose these coin/combos because of their insane net profit factors. There are far more coins with lower net profits but more reliable trade histories.

Also, usually when I want to see which of these strategies might work for a coin pairing I will check between the different Moving Average types, for example the EMA or the SMA, then I also check between the moving average lengths (the number of bars calculated) to see which is most profitable over time.

Features:

-You can choose your preferred moving average: SMA, EMA, WMA, RMA & VWMA.

-You can also adjust the previous number of calculated bars for each moving average.

-I made the background color Green when you're currently in a long position and Red when not. I made it so you can see when you'd be actively in a trade or not. The Red and Green background colors can be toggled on/off in order to see other indicators more clearly overlayed in the chart, or if you prefer a cleaner look on your charts.

-I also have a plot of the Open moving average and Close moving average together. The Opening moving average is Purple, the Closing moving average is White. White on top is a sign of a potential upswing and purple on top is a sign of a potential downswing. I've made this also able to be toggled on/off.

Please, comment interesting pairs below that you've found for everyone :) thank you!

I will post more pairs with my favorite settings as well. I'll also be considering the quality of the trades.. for example: net profit, total trades, percent profitable, profit factor, trade window and max drawdown.

*if anyone can figure out how to change the date range, I woul really appreciate the help. It confuses me -_- *

DatasetWeatherTokyoMeanAirTemperatureLibrary "DatasetWeatherTokyoMeanAirTemperature"

Provides a data set of the monthly mean air temperature (°C) for the city of Tokyo in Japan.

this was just for fun, no financial implications in this.

reference:

www.data.jma.go.jp

TOKYO WMO Station ID:47662 Lat 35o41.5'N Lon 139o45.0'E

year_()

the years of the data set.

Returns: array : year values.

january()

the january values of the dataset

Returns: array\ : data values for january.

february()

the february values of the dataset

Returns: array\ : data values for february.

march()

the march values of the dataset

Returns: array\ : data values for march.

april()

the april values of the dataset

Returns: array\ : data values for april.

may()

the may values of the dataset

Returns: array\ : data values for may.

june()

the june values of the dataset

Returns: array\ : data values for june.

july()

the july values of the dataset

Returns: array\ : data values for july.

august()

the august values of the dataset

Returns: array\ : data values for august.

september()

the september values of the dataset

Returns: array\ : data values for september.

october()

the october values of the dataset

Returns: array\ : data values for october.

november()

the november values of the dataset

Returns: array\ : data values for november.

december()

the december values of the dataset

Returns: array\ : data values for december.

annual()

the annual values of the dataset

Returns: array\ : data values for annual.

select_month(idx)

get the temperature values for a specific month.

Parameters:

idx : int, month index (1 -> 12 | any other value returns annual average values).

Returns: array\ : data values for selected month.

select_value(year_, month_)

get the temperature value of a specified year and month.

Parameters:

year_ : int, year value.

month_ : int, month index (1 -> 12 | any other value returns annual average values).

Returns: float : value of specified year and month.

diff_to_median(month_)

the difference of the month air temperature (ºC) to the median of the sample.

Parameters:

month_ : int, month index (1 -> 12 | any other value returns annual average values).

Returns: float : difference of current month to median in (Cº)

5EMA + VP IGHola Divinis

En una villa nació, fue deseo de Dios

Crecer y sobrevivir a la humilde expresión

Enfrentar la adversidad

Con afán de ganarse a cada paso la vida

En un potrero forjó una zurda inmortal

Con experiencia, sedienta ambición de llegar

De cebollita, soñaba jugar un Mundial

Y consagrarse en Primera

Tal vez jugando pudiera a su familia ayudar

En una villa nació, fue deseo de Dios

Crecer y sobrevivir a la humilde expresión

Enfrentar la adversidad

Con afán de ganarse a cada paso la vida

En un potrero forjó una zurda inmortal

Con experiencia, sedienta ambición de llegar

De cebollita, soñaba jugar un Mundial

Y consagrarse en Primera

Tal vez jugando pudiera a su familia ayudar

A poco que debutó (Maradó, Maradó)

La 12 fue quien coreó (Maradó, Maradó)

Su sueño tenía una estrella

Llena de gol y gambetas

Y todo el pueblo cantó (Maradó, Maradó)

Nació la mano de Dios (Maradó, Maradó)

Llenó alegría en el pueblo

Regó de gloria este suelo

Carga una cruz en los hombros por ser el mejor

Por no venderse jamás, al poder enfrentó

Curiosa debilidad, si Jesús tropezó

¿Por qué él no habría de hacerlo?

La fama le presentó una blanca mujer

De misterioso sabor y prohibido placer

Que lo hizo adicto al deseo de usarla otra vez

Involucrando su vida

Y es un partido que un día el Diego está por ganar

A poco que debutó (Maradó, Maradó)

La 12 fue quien coreó (Maradó, Maradó)

Su sueño tenía una estrella

Llena de gol y gambetas

Y todo el pueblo cantó (Maradó, Maradó)

Nació la mano de Dios (Maradó, Maradó)

Llenó alegría en el pueblo

Llenó de gloria este suelo

Olé, olé, olé, olé

¡Diego, Diego!

Olé, olé, olé, olé

¡Diego, Diego!

Olé, olé, olé, olé

¡Diego, Diego!

Olé, olé, olé, olé

¡Diego, Diego!

Y todo el pueblo cantó (Maradó, Maradó)

La 12 fue quien coreó (Maradó, Maradó)

Su sueño tenía una estrella

Llena de gol y gambetas

Y todo el pueblo cantó (Maradó, Maradó)

Nació la mano de Dios (Maradó, Maradó)

Llenó alegría en el pueblo

Regó de gloria este suelo

Regó de gloria este suelo

Regó de gloria

Agregar a la playlist

Tamaño

A

A

Cifrado

Imprimir

Corregir

Time█ OVERVIEW

This library is a Pine Script™ programmer’s tool containing a variety of time related functions to calculate or measure time, or format time into string variables.

█ CONCEPTS

`formattedTime()`, `formattedDate()` and `formattedDay()`

Pine Script™, like many other programming languages, uses timestamps in UNIX format, expressed as the number of milliseconds elapsed since 00:00:00 UTC, 1 January 1970. These three functions convert a UNIX timestamp to a formatted string for human consumption.

These are examples of ways you can call the functions, and the ensuing results:

CODE RESULT

formattedTime(timenow) >>> "00:40:35"

formattedTime(timenow, "short") >>> "12:40 AM"

formattedTime(timenow, "full") >>> "12:40:35 AM UTC"

formattedTime(1000 * 60 * 60 * 3.5, "HH:mm") >>> "03:30"

formattedDate(timenow, "short") >>> "4/30/22"

formattedDate(timenow, "medium") >>> "Apr 30, 2022"

formattedDate(timenow, "full") >>> "Saturday, April 30, 2022"

formattedDay(timenow, "E") >>> "Sat"

formattedDay(timenow, "dd.MM.yy") >>> "30.04.22"

formattedDay(timenow, "yyyy.MM.dd G 'at' hh:mm:ss z") >>> "2022.04.30 AD at 12:40:35 UTC"

These functions use str.format() and some of the special formatting codes it allows for. Pine Script™ documentation does not yet contain complete specifications on these codes, but in the meantime you can find some information in the The Java™ Tutorials and in Java documentation of its MessageFormat class . Note that str.format() implements only a subset of the MessageFormat features in Java.

`secondsSince()`

The introduction of varip variables in Pine Script™ has made it possible to track the time for which a condition is true when a script is executing on a realtime bar. One obvious use case that comes to mind is to enable trades to exit only when the exit condition has been true for a period of time, whether that period is shorter that the chart's timeframe, or spans across multiple realtime bars.

For more information on this function and varip please see our Using `varip` variables publication.

`timeFrom( )`

When plotting lines , boxes , and labels one often needs to calculate an offset for past or future end points relative to the time a condition or point occurs in history. Using xloc.bar_index is often the easiest solution, but some situations require the use of xloc.bar_time . We introduce `timeFrom()` to assist in calculating time-based offsets. The function calculates a timestamp using a negative (into the past) or positive (into the future) offset from the current bar's starting or closing time, or from the current time of day. The offset can be expressed in units of chart timeframe, or in seconds, minutes, hours, days, months or years. This function was ported from our Time Offset Calculation Framework .

`formattedNoOfPeriods()` and `secondsToTfString()`

Our final two offerings aim to confront two remaining issues:

How much time is represented in a given timestamp?

How can I produce a "simple string" timeframe usable with request.security() from a timeframe expressed in seconds?

`formattedNoOfPeriods()` converts a time value in ms to a quantity of time units. This is useful for calculating a difference in time between 2 points and converting to a desired number of units of time. If no unit is supplied, the function automatically chooses a unit based on a predetermined time step.

`secondsToTfString()` converts an input time in seconds to a target timeframe string in timeframe.period string format. This is useful for implementing stepped timeframes relative to the chart time, or calculating multiples of a given chart timeframe. Results from this function are in simple form, which means they are useable as `timeframe` arguments in functions like request.security() .

█ NOTES

Although the example code is commented in detail, the size of the library justifies some further explanation as many concepts are demonstrated. Key points are as follows:

• Pivot points are used to draw lines from. `timeFrom( )` calculates the length of the lines in the specified unit of time.

By default the script uses 20 units of the charts timeframe. Example: a 1hr chart has arrows 20 hours in length.

• At the point of the arrows `formattedNoOfPeriods()` calculates the line length in the specified unit of time from the input menu.

If “Use Input Time” is disabled, a unit of time is automatically assigned.

• At each pivot point a label with a formatted date or time is placed with one of the three formatting helper functions to display the time or date the pivot occurred.

• A label on the last bar showcases `secondsSince()` . The label goes through three stages of detection for a timed alert.

If the difference between the high and the open in ticks exceeds the input value, a timer starts and will turn the label red once the input time is exceeded to simulate a time-delayed alert.

• In the bottom right of the screen `secondsToTfString()` posts the chart timeframe in a table. This can be multiplied from the input menu.

Look first. Then leap.

█ FUNCTIONS

formattedTime(timeInMs, format)

Converts a UNIX timestamp (in milliseconds) to a formatted time string.

Parameters:

timeInMs : (series float) Timestamp to be formatted.

format : (series string) Format for the time. Optional. The default value is "HH:mm:ss".

Returns: (string) A string containing the formatted time.

formattedDate(timeInMs, format)

Converts a UNIX timestamp (in milliseconds) to a formatted date string.

Parameters:

timeInMs : (series float) Timestamp to be formatted.

format : (series string) Format for the date. Optional. The default value is "yyyy-MM-dd".

Returns: (string) A string containing the formatted date.

formattedDay(timeInMs, format)

Converts a UNIX timestamp (in milliseconds) to the name of the day of the week.

Parameters:

timeInMs : (series float) Timestamp to be formatted.

format : (series string) Format for the day of the week. Optional. The default value is "EEEE" (complete day name).

Returns: (string) A string containing the day of the week.

secondsSince(cond, resetCond)

The duration in milliseconds that a condition has been true.

Parameters:

cond : (series bool) Condition to time.

resetCond : (series bool) When `true`, the duration resets.

Returns: The duration in seconds for which `cond` is continuously true.

timeFrom(from, qty, units)

Calculates a +/- time offset in variable units from the current bar's time or from the current time.

Parameters:

from : (series string) Starting time from where the offset is calculated: "bar" to start from the bar's starting time, "close" to start from the bar's closing time, "now" to start from the current time.

qty : (series int) The +/- qty of units of offset required. A "series float" can be used but it will be cast to a "series int".

units : (series string) String containing one of the seven allowed time units: "chart" (chart's timeframe), "seconds", "minutes", "hours", "days", "months", "years".

Returns: (int) The resultant time offset `from` the `qty` of time in the specified `units`.

formattedNoOfPeriods(ms, unit)

Converts a time value in ms to a quantity of time units.

Parameters:

ms : (series int) Value of time to be formatted.

unit : (series string) The target unit of time measurement. Options are "seconds", "minutes", "hours", "days", "weeks", "months". If not used one will be automatically assigned.

Returns: (string) A formatted string from the number of `ms` in the specified `unit` of time measurement

secondsToTfString(tfInSeconds, mult)

Convert an input time in seconds to target string TF in `timeframe.period` string format.

Parameters:

tfInSeconds : (simple int) a timeframe in seconds to convert to a string.

mult : (simple float) Multiple of `tfInSeconds` to be calculated. Optional. 1 (no multiplier) is default.

Returns: (string) The `tfInSeconds` in `timeframe.period` format usable with `request.security()`.

Momentum ScoreMomentum is the tendency of assets that have gone up in price to continue going up in price - and for assets that have gone down in price to continue going down in price. The reasons behind it are not well understood by academics, but momentum is a property that exists across geographies and asset classes.

The Momentum Score is a system that scores companies based on their one year total returns, excluding the last month of returns. In other words, a momentum score for today will be based on the total returns of a stock from 12 months ago today to one month ago today.

Our Momentum Score 13612W has the following composition:

MS 13612W = 12 * Roc(1) + 4 * Roc(3) + 2 * Roc(6) + 1 * Roc(12)

with ROC = (p0/pt) - 1, where pt equals price p with a t-month lag

Median Convergence DivergenceIntroduction

The Median Convergence Divergence (MCD) is a derivative of the Moving Average Convergence Divergence (MACD). The difference is the change in the use of the measure of central tendency. In MACD, moving average (mean) is used, whereas, in MCD, the median is used instead. The purpose of using the median is to eliminate the outlying values, which would be calculated for a moving average. The outliers would affect the value of the moving average.

For example: 3, 5, 7, 8, 5, 4, 2, 1, 6, 21, 8. The data set average is 6.3, whereas the median value is 5. There is a difference of about 23% in the example. The reason is the outlying value '21' in the data set.

As the markets are volatile, outlying values can always emerge. A moving average will consider those values; on the other hand, the median will ignore. If the strategy calls for a tool to ignore the outliers, the Median Convergence Divergence would be a great centered oscillator.

The default values have changed to suit the current trading days in a week. When the MACD was introduced, there would be six trading days in a week. Therefore, it used 12 (2 weeks), 26(4 weeks), and 9 ( 1.5 weeks). But now that there are five trading days per week. The default values are adapted to them. Feel free to change them as per your wish.

Recommended Settings

The current settings are set to be used for the Daily Time Frame: 5 day period for the fast line, a 20 day period for the slow line, and a 10 day period for the signal line. (5 days represent a trading week, 10 days is two weeks, and 20 days is 4 weeks or a month)

For the weekly charts, use 4 week period for the fast line, 13 week period for the slow line, and 8 week period for the signal line. (4 weeks represent a month, 8 weeks is two months, and 13 weeks is 3 months or quarterly)

And for monthly charts, use 3 month period for the fast line, 12 month period for the slow line, and 6 month period for the signal line. (3 months is quarterly, 6 months is bi-yearly, and 12 month is yearly)

It'll be challenging to measure for intraday since there are many different timeframes within intraday. The settings mentioned above should also be customized as per the requirements of the trading strategy.

Strategy

The strategy application is the same as the MACD, i.e., Signal Line Crossovers, Zero Line Crossovers, and Divergence.

Signal Line Crossovers: When the MCD line crosses above the Signal line, it's a bullish crossover. When the MCD line crosses below the Signal line, it's a bearish crossover.

Zero Line Crossovers: It's a bullish crossover when the MCD line crosses above the Zero line. When the MCD line crosses below the Zero Line, it's a bearish crossover.

Divergence: When price shows a lower low, but MCD shows a higher low, it's a bullish divergence. When the price shows a higher high but MCD shows a lower high, it's a bearish divergence.

Using other indicators in conjunction with the Median Convergence Divergence is recommended to take entry and exit signals.

DAYOFWEEK performance1 -Objective

"What is the ''best'' day to trade .. Monday, Tuesday...."

This script aims to determine if there are different results depending on the day of the week.

The way it works is by dividing data by day of the week (Monday, Tuesday, Wednesday ... ) and perform calculations for each day of the week.

1 - Objective

2 - Features

3 - How to use (Examples)

4 - Inputs

5 - Limitations

6 - Notes

7 - Final Tooughs

2 - Features

AVG OPEN-CLOSE

Calculate de Percentage change from day open to close

Green % (O-C)

Percentage of days green (open to close)

Average Change

Absolute day change (O-C)

AVG PrevD. Close-Close

Percentage change from the previous day close to the day of the week close

(Example: Monday (C-C) = Friday Close to Monday close

Tuesday (C-C) = Monday C. to Tuesday C.

Green % (C1-C)

Percentage of days green (open to close)

AVG Volume

Day of the week Average Volume

Notes:

*Mon(Nº) - Nº = Number days is currently calculated

Example: Monday (12) calculation based on the last 12 Mondays. Note: Discrepancies in numbers example Monday (12) - Friday (11) depend on the initial/end date or the market was closed (Holidays).

3 - How to use (Examples)

For the following example, NASDAQ:AAPL from 1 Jan 21 to 1 Jul 21 the results are following.

The highest probability of a Close being higher than the Open is Monday with 52.17 % and the Lowest Tuesday with 38.46 %. Meaning that there's a higher chance (for NASDAQ:AAPL ) of closing at a higher value on Monday while the highest chance of closing is lower is Tuesday. With an average gain on Tuesday of 0.21%

Long - The best day to buy (long) at open (on average) is Monday with a 52.2% probability of closing higher

Short - The best day to sell (short) at open (on average) is Tuesday with a 38.5% probability of closing higher (better chance of closing lower)

Since the values change from ticker to ticker, there is a substantial change in the percentages and days of the week. For example let's compare the previous example ( NASDAQ:AAPL ) to NYSE:GM (same settings)

For the same period, there is a substantial difference where there is a 62.5% probability Friday to close higher than the open, while Tuesday there is only a 28% probability.

With an average gain of 0.59% on Friday and an average loss of -0.34%

Also, the size of the table (number of days ) depends if the ticker is traded or not on that day as an example COINBASE:BTCUSD

4 - Inputs

DATE RANGE

Initial Date - Date from which the script will start the calculation.

End Date - Date to which the script will calculate.

TABLE SETTINGS

Text Color - Color of the displayed text

Cell Color - Background color of table cells

Header Color - Color of the column and row names

Table Location - Change the position where the table is located.

Table Size - Changes text size and by consequence the size of the table

5 - LIMITATIONS

The code determines average values based on the stored data, therefore, the range (Initial data) is limited to the first bar time.

As a consequence the lower the timeframe the shorter the initial date can be and fewer weeks can be calculated. To warn about this limitation there's a warning text that appears in case the initial date exceeds the bar limit.

Example with initial date 1 Jan 2021 and end date 18 Jul 2021 in 5m and 10 m timeframe:

6 - Notes and Disclosers

The script can be moved around to a new pane if need. -> Object Tree > Right Click Script > Move To > New pane

The code has not been tested in higher subscriptions tiers that allow for more bars and as a consequence more data, but as far I can tell, it should work without problems and should be in fact better at lower timeframes since it allows more weeks.

The values displayed represent previous data and at no point is guaranteed future values

7 - Final Tooughs

This script was quite fun to work on since it analysis behavioral patterns (since from an abstract point a Tuesday is no different than a Thursday), but after analyzing multiple tickers there are some days that tend to close higher than the open.

PS: If you find any mistake ex: code/misspelling please comment.

Phoenix Ascending 2.201Hi Everyone!

It's time to make this indicator public to relieve myself of replying to requests for access. There has been an update to this indicator; in which a Stochastic RSI was added to this indicator. Please follow the directions to SETUP the indicator in the SETUP VIDEO provided below.

Phoenix Ascending 2.201 and Bollinger Bands Setup Video.

The following are BASIC rules for the Phoenix 2.201 Indicator. More advanced rules and the requirements for those rules can be found in my publications in my public profile. Unfortunately, I do not have organized videos created on how to use this indicator in full but will be available in the future.

IMPORTANT: The BASIC rules below are beneficial but these are NOT all the rules. More rules and requirements for those rules will be available in the future.

RULE NO. 1

We PREFER the Blue LSMA to be at 80% or higher for SAFE EXIT (SHORT) bets.

We PREFER the Blue LSMA to be at 20% or lower for SAFE ENTRY (LONG) bets.

Rule No. 2

ANY time the red line is approaching a green line that’s moving UPWARD,

Be prepared to make an ENTRY (LONG) when the red line is about to touch the green line that’s moving upward.

One can look at a lower time frame to get a better idea of how much longer you may have

To wait for the red line to touch the green line. In many cases, you may make ENTRY (LONG)

Just before the red line actually touches the green line that’s moving up in that higher time frame

You were initially using as your COMPASS. I currently have the 1-Month TF as a compass for EURUSD.

Rule No. 3

ANY time the red line is approaching a green line that’s moving DOWNWARD,

Be prepared to make an EXIT (SHORT) when the red line is about to touch the green line that’s moving downward.

One can look at a lower time frame to get a better idea of how much longer you may have

To wait for the red line to touch the green line. In many cases, you may make your EXIT (SHORT)

Just before the red line actually touches the green line that’s moving downward in that higher time frame

You were initially using as your COMPASS. I currently have the 1-Month TF as a compass for EURUSD.

Rule No. 4

The Green Line and/or Ghost Line can often help one determine when an upward or downward move in a particular time frame

Is nearly exhausted and about to reverse.

Example for Upside Exhaustion about to reverse to the Downside:

When the Green Line and/or Ghost line is at 80% level or higher, this is a good indicator to inform

Us the current upside move may be approaching exhaustion. You can look at a higher time frame to try to gain

More insight as to whether this will only be a brief dip down in the lower time frame IF the higher time frame you

Went to reveals there is a lot more room remaining for the Green and/or Ghost Lines to reach the 80% or higher level.

Example for Downside Exhaustion about to reverse to the Upside:

When the Green Line and/or Ghost line is at 20% level or lower, this is a good indicator to inform

Us the current downside move may be approaching exhaustion. You can look at a higher time frame to try to gain

More insight as to whether this will only be a brief dip up in the lower time frame IF the higher time frame you

Went to reveals there is a lot more room remaining for the Green and/or Ghost Lines to reach the 20% or lower level.

Rule No. 5

The same rules you see in Rule No. 4 also apply to the Stochastic RSI. Keep in mind I changed the colors of the

Stochastic RSI to the following: Red default changed to Purple and Blue changed changed to Black to avoid confusing

Them with the lines in Godmode.

When the Stochastic RSI is at 80% or higher level, we need to be on guard for a reversal to the downside.

When the Stochastic RSI is at 20% or lower level, we need to be on guard for a reversal to the upside.

EXTREMELY IMPORTANT to apply these rules in GROUPS OF TIME FRAMES.

"TYPES" OF TIME FRAME GROUP TRADING SIGNALS

Scalping Group Signals: Signals provided for this group involve analyzing the following two groups of time frames. Short Term Group as a compass and Scalping Group for confirmation and more precise entry/exit.

Scalping Group: 6min. 12min. 23min & 45min.

Short Term Group: 90min. 3hr. 6hr. & 12hr.

Short Term Group Signals: Signals provided for this group involve analyzing the following two groups of time frames. NearTerm Group as a compass and Short Term Group for confirmation and more precise entry/exit.

Short Term Group: 90min. 3hr. 6hr. & 12hr.

Near Term Group: 24hr. 2-Day, 3-Day & 4-Day

Near Term Group Signals: Signals provided for this group involve analyzing the following two groups of time frames. Mid Term Group as a compass and Near Term Group for confirmation and more precise entry/exit.

Near Term Group: 24hr. 2-Day, 3-Day & 4-Day

Mid Term Group: 3-Day, 6-Day, 9-Day & 12-Day

Mid Term Group Signals: Signals provided for this group involve analyzing the following two groups of time frames. Long Term Group as a compass and Mid Term Group for confirmation and more precise entry/exit.

Mid Term Group: 3-Day, 6-Day, 9-Day & 12-Day

Long Term Group: 1-Week, 2-Week, 3-Week & 4-Week

Long Term Group Signals: Signals provided for this group involve analyzing the following two groups of time frames. Macro Term Group as a compass and Long Term Group for confirmation and more precise entry/exit.

Long Term Group: 1-Week, 2-Week, 3-Week & 4-Week

Macro Term Group: 1-Month, 2-Month, 3-Month & 4-Month

Macro Term Group Signals: Signals provided for this group involve analyzing the following two groups of time frames. Macro Term Group as a compass and Long Term Group for confirmation and more precise entry/exit.

Macro Term Group: 1-Month, 2-Month, 3-Month & 4-Month

Super Macro Group: 3-Month , 6-Month, 12-Month & 24-Month

Reverse MACD IndicatorIntroducing the reverse MACD Indicator.

This is my Pinescript implementation of the reverse MACD indicator.

Much respect to Mr Johnny Dough the original creator of this idea.

Feel free to reuse this script, drop me a note below if you find this useful.

Investopedia defines the MACD as a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price.

The MACD is calculated by subtracting the 26-period Exponential Moving Average ( EMA ) from the 12-period EMA .

The result of that calculation is the MACD line.

A nine-day EMA of the MACD called the "signal line," is then plotted on top of the MACD line, which can function as a trigger for buy and sell signals.

Traders may buy the security when the MACD crosses above its signal line and sell—or short—the security when the MACD crosses below the signal line.

Moving Average Convergence Divergence ( MACD ) indicators can be interpreted in several ways, but the more common methods are crossovers, divergences, and rapid rises/falls.

MACD triggers technical signals when it crosses above (to buy) or below (to sell) its signal line.

The speed of crossovers is also taken as a signal of a market is overbought or oversold.

MACD helps investors understand whether the bullish or bearish movement in the price is strengthening or weakening.

The MACD has a positive value (shown as the red line on the price chart ) whenever the 12-period EMA ( indicated by the blue line on the price chart) is above the 26-period EMA (the red line in the price chart) and a negative value when the 12-period EMA is below the 26-period EMA .

The more distant the MACD is above or below its baseline indicates that the distance between the two EMAs is growing.

The baseline here is the white line.

The Reverse function of the MACD provides value by letting the user know the specific price needed to expect a MACD cross over in the opposite direction.

This function can be used to designate risk parameters for a potential trade if using the MACD as their source of edge, letting the user know exactly where and how much their risk is for a potential trade which can be used to design an effective trading plan.

Percentage Volume Oscillator (PVO)The Percentage Volume Oscillator (PVO) is a momentum oscillator for volume. The PVO measures the difference between two volume-based moving averages as a percentage of the larger moving average. As with MACD and the Percentage Price Oscillator (PPO), it is shown with a signal line, a histogram and a centerline. The PVO is positive when the shorter volume EMA is above the longer volume EMA and negative when the shorter volume EMA is below. This indicator can be used to define the ups and downs for volume, which can then be used to confirm or refute other signals. Typically, a breakout or support break is validated when the PVO is rising or positive.

Generally speaking, volume is above average when the PVO is positive and below average when the PVO is negative. A negative and rising PVO indicates that volume levels are increasing. A positive and falling PVO indicates that volume levels are decreasing. Chartists can use this information to confirm or refute movements on the price chart.

Even though the PVO is based on a momentum oscillator formula, it is important to remember that moving averages lag. A 12-day EMA include 12 days of volume data, with newer data weighted more heavily. A 26-day EMA lags even more because it contains 26 days of data. This means that the PVO(12,26,9) can sometimes be out of sync with price action.

The Percentage Volume Oscillator (PVO) is a momentum indicator applied to volume. This oscillator can be quite choppy due to the fact that volume doesn't trend. Bullish and bearish divergences are not well suited for the PVO. Instead, chartists would be better off looking for signs of increasing volume with a move into positive territory and signs of decreasing volume with a move into negative territory. Increasing volume can validate a support or resistance break. Similarly, a surge or significant support break on low volume may be less robust. As with all technical indicators, it is important to use the Percentage Volume Oscillator (PVO) in conjunction with other aspects of technical analysis, such as chart patterns and momentum oscillators.

ETF / Stocks / Crypto - DCA Strategy v1Simple "benchmark" strategy for ETFs, Stocks and Crypto! Super-easy to implement for beginners, a DCA (dollar-cost-averaging) strategy means that you buy a fixed amount of an ETF / Stock / Crypto every several months. For instance, to DCA the S&P 500 (SPY), you could purchase $10,000 USD every 12 months, irrespective of the market price. Assuming the macro-economic conditions of the underlying country remain favourable, DCA strategies will result in capital gains over a period of many years, e.g. 10 years. DCA is the safest strategy that beginners can employ to make money in the markets, and all other types of strategies should be "benchmarked" against DCA; if your strategy cannot outperform DCA, then your strategy is useless.

Recommended Chart Settings:

Asset Class: ETF / Stocks / Crypto

Time Frame: H1 (Hourly) / D1 (Daily) / W1 (Weekly) / M1 (Monthly)

Necessary ETF Macro Conditions:

1. Country must have healthy demographics, good ratio of young > old

2. Country population must be increasing

3. Country must be experiencing price-inflation

Necessary Stock Conditions:

1. Growing revenue

2. Growing net income

3. Consistent net margins

4. Higher gross/net profit margin compared to its peers in the industry

5. Growing share holders equity

6. Current ratios > 1

7. Debt to equity ratio (compare to peers)

8. Debt servicing ratio < 30%

9. Wide economic moat

10. Products and services used daily, and will stay relevant for at least 1 decade

Necessary Crypto Conditions:

1. Honest founders

2. Competent technical co-founders

3. Fair or non-existent pre-mine

4. Solid marketing and PR

5. Legitimate use-cases / adoption

Default Robot Settings:

Contribution (USD): $10,000

Frequency (Months): 12

*Robot buys $10,000 worth of ETF, Stock, Crypto, regardless of the market price, every 12 months since its founding time.*

*Equity curve can be seen from the bottom panel*

Risk Warning:

This strategy is low-risk, however it assumes you have a long time horizon of at least 5 to 10 years. The longer your holding-period, the better your returns. The only thing the user has to keep-in-mind are the macro-economic conditions as stated above. If unsure, please stick to ETFs rather than buying individual stocks or cryptocurrencies.

MACD StrategyThis script sends buy and sell signals as alerts to 3Commas (online software with trading bots in cryptocurreny)

It's based on 2 indicators:

- MACD

- 12 EMA and 26 EMA

When the 12 EMA and 26 EMA crossover, the MACD line crosses above 0. The goal here is to look for buy signals when the MACD and Signal are below 0, the histogram is positive, and there was or will be a 12 EMA and 26 EMA crossover.

I struggle with the following:

- There are multiple ways to use this as a crossover signal. I want to calculate the win rate of every posibility.

- What should be my take profit and my stoploss?

I think a 2:1 R/R,and a 60% win rate would make a great strategy! I could use some advice.

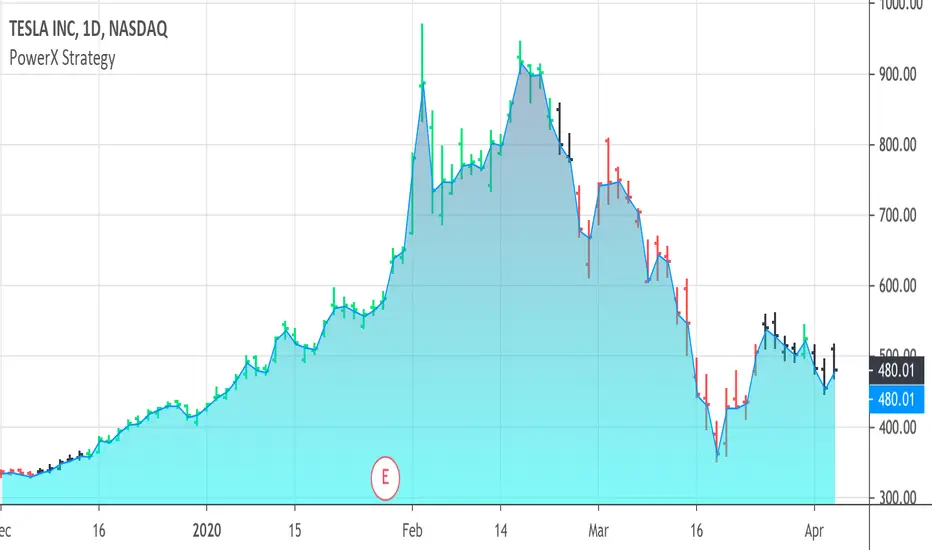

PowerX Strategy Bar Coloring [OFFICIAL VERSION]This script colors the bars according to the PowerX Strategy by Markus Heitkoetter:

The PowerX Strategy uses 3 indicators:

- RSI (7)

- Stochastics (14, 3, 3)

- MACD (12, 26 , 9)

The bars are colored GREEN if...

1.) The RSI (7) is above 50 AND

2.) The Stochastic (14, 3, 3) is above 50 AND

3.) The MACD (12, 26, 9) is above its Moving Average, i.e. MACD Histogram is positive.

The bars are colored RED if...

1.) The RSI (7) is below 50 AND

2.) The Stochastic (14, 3, 3) is below 50 AND

3.) The MACD (12, 26, 9) is below its Moving Average, i.e. MACD Histogram is negative.

If only 2 of these 3 conditions are met, then the bars are black (default color)

We highly recommend plotting the indicators mentioned above on your chart, too, so that you can see when bars are getting close to being "RED" or "GREEN", e.g. RSI is getting close to the 50 line.

Price Action and 3 EMAs Momentum plus Sessions FilterThis indicator plots on the chart the parameters and signals of the Price Action and 3 EMAs Momentum plus Sessions Filter Algorithmic Strategy. The strategy trades based on time-series (absolute) and relative momentum of price close, highs, lows and 3 EMAs.

I am still learning PS and therefore I have only been able to write the indicator up to the Signal generation. I plan to expand the indicator to Entry Signals as well as the full Strategy.

The strategy works best on EURUSD in the 15 minutes TF during London and New York sessions with 1 to 1 TP and SL of 30 pips with lots resulting in 3% risk of the account per trade. I have already written the full strategy in another language and platform and back tested it for ten years and it was profitable for 7 of the 10 years with average profit of 15% p.a which can be easily increased by increasing risk per trade. I have been trading it live in that platform for over two years and it is profitable.

Contributions from experienced PS coders in completing the Indicator as well as writing the Strategy and back testing it on Trading View will be appreciated.

STRATEGY AND INDICATOR PARAMETERS

Three periods of 12, 48 and 96 in the 15 min TF which are equivalent to 3, 12 and 24 hours i.e (15 min * period / 60 min) are the foundational inputs for all the parameters of the PA & 3 EMAs Momentum + SF Algo Strategy and its Indicator.

3 EMAs momentum parameters and conditions

• FastEMA = ema of 12 periods

• MedEMA = ema of 48 periods

• SlowEMA = ema of 96 periods

• All the EMAs analyse price close for up to 96 (15 min periods) equivalent to 24 hours

• There’s Upward EMA momentum if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA

• There’s Downward EMA momentum if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA

PA momentum parameters and conditions

• HH = Highest High of 48 periods from 1st closed bar before current bar

• LL = Lowest Low of 48 periods from 1st closed bar from current bar

• Previous HH = Highest High of 84 periods from 12th closed bar before current bar

• Previous LL = Lowest Low of 84 periods from 12th closed bar before current bar

• All the HH & LL and prevHH & prevLL are within the 96 periods from the 1st closed bar before current bar and therefore indicative of momentum during the past 24 hours

• There’s Upward PA momentum if price close > HH and HH > prevHH and LL > prevLL

• There’s Downward PA momentum if price close < LL and LL < prevLL and HH < prevHH

Signal conditions and Status (BuySignal, SellSignal or Neutral)

• The strategy generates Buy or Sell Signals if both 3 EMAs and PA momentum conditions are met for each direction and these occur during the London and New York sessions

• BuySignal if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA and price close > HH and HH > prevHH and LL > prevLL and timeinrange (LDN&NY) else Neutral

• SellSignal if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA and price close < LL and LL < prevLL and HH < prevHH and timeinrange (LDN&NY) else Neutral

Entry conditions and Status (EnterBuy, EnterSell or Neutral)(NOT CODED YET)

• ENTRY IS NOT AT THE SIGNAL BAR but at the current bar tick price retracement to FastEMA after the signal

• EnterBuy if current bar tick price <= FastEMA and current bar tick price > prevHH at the time of the Buy Signal

• EnterSell if current bar tick price >= FastEMA and current bar tick price > prevLL at the time of the Sell Signal

Smart labelling - Candlestick FunctionOftentimes a single look at the candlestick configuration happens to be enough to understand what is going on. The chandlestick function is an experiment in smart labelling that produces candles for various time frames, not only for the fixed 1m, 3m , 5m, 15m, etc. ones, and helps in decision-making when eye-balling the chart. This function generates up to 12 last candlesticks , which is generally more than enough.

Mind that since this is an experiment, the function does not cover all possible combinations. In some time frames the produced candles overlap. This is a todo item for those who are unterested. For instance, the current version covers the following TFs:

Chart - TF in the script

1m - 1-20,24,30,32

3m - 1-10

5m - 1-4,6,9,12,18,36

15m - 1-4,6,12

Tested chart TFs: 1m, 3m ,5m,15m. Tested securities: BTCUSD , EURUSD

[astropark] Power Tools Overlay//******************************************************************************

// Power Tools Overlay

// Inner Version 1.2.1 13/12/2018

// Developer: iDelphi

// Developer: astropark (Ichimoku Cloud), SMA EMA & Cross tools

//------------------------------------------------------------------------------

// 21/11/2018 Added EMA SMA WMA

// 21/11/2018 Added SMA-EMA EMA-WMA WMA-SMA (Thanks to mariobros1 for the idea of the Simultaneous MA)

// 21/11/2018 Added Bollinger Bands

// 21/11/2018 Added Ichimoku Cloud (Thanks to astropark for all the code of the Ichimoku Cloud)

// 23/11/2018 Show all the indicator as default

// 23/11/2018 Added a cross when single Moving Averages crossing (Thanks to astropark for the idea)

// 24/11/2018 Descriptions Fix

// 24/11/2018 Added Option to enable/disable all Moving Averages

// 10/12/2018 Added EMAs and Crosses

// 13/12/2018 indicator number fixes

//******************************************************************************

[Delphi] Power Tools OscillatorsFEATURES

- RSI

- Stochastic

//******************************************************************************

// Power Tools Oscillators

// Inner Version 1.0 04/12/2018

// Developer: iDelphi

//------------------------------------------------------------------------------

// 04/12/2018 Added RSI

// 04/12/2018 Added Stochastic

//******************************************************************************

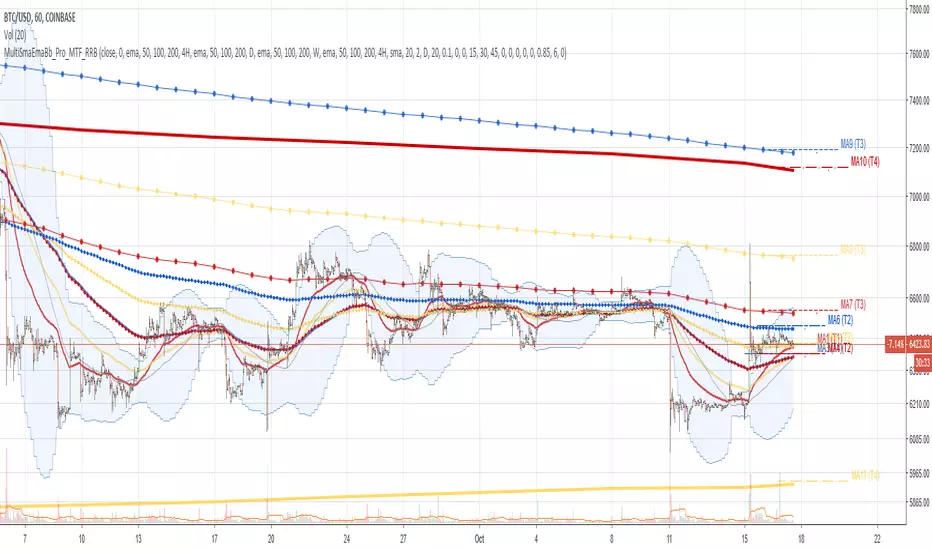

Multi SMA EMA WMA HMA BB (4x3 MAs Bollinger Bands) Pro MTF - RRBMulti SMA EMA WMA HMA 4x3 Moving Averages with Bollinger Bands Pro MTF by RagingRocketBull 2018

Version 1.0

This indicator shows multiple MAs of any type SMA EMA WMA HMA etc with BB and MTF support, can show MAs as dynamically moving levels.

There are 4 MA groups + 1 BB group. You can assign any type/timeframe combo to a group, for example:

- EMAs 50,100,200 x H1, H4, D1, W1 (4 TFs x 3 MAs x 1 type)

- EMAs 8,13,21,55,100,200 x M15, H1 (2 TFs x 6 MAs x 1 type)

- D1 EMAs and SMAs 12,26,50,100,200,400 (1 TF x 6 MAs x 2 types)

- H1 WMAs 7,77,231; H4 HMAs 50,100,200; D1 EMAs 144,169,233; W1 SMAs 50,100,200 (4 TFs x 3 MAs x 4 types)

- +1 extra MA type/timeframe for BB

compile time: 25-30 sec

full redraw time after parameter change in UI: 3 sec

There are several versions: Simple, MTF, Pro MTF, Advanced MTF and Ultimate MTF. This is the Pro MTF version. The Differences are listed below. All versions have BB

- Simple: you have 2 groups of MAs that can be assigned any type (5+5)

- MTF: +2 custom Timeframes for each group (2x5 MTF)

- Pro MTF: +4 custom Timeframes for each group (4x3 MTF), MA levels and show max bars back options

- Advanced MTF: +2 extra MAs/group (4x5 MTF), custom Ticker/Symbol, backreferences for type, TF and MA lengths in UI

- Ultimate MTF: +individual settings for each MA, custom Ticker/Symbols

Features:

- 4x3 = 12 MAs of any type including Hull Moving Average (HMA)

- 4x MTF groups with step line smoothing

- BB +1 extra TF/type for BB MAs

- 12 MA levels with adjustable group offsets, indents and shift

- show max bars back

- you can show/hide both groups of MAs/levels and individual MAs

Notes:

1. based on 3EmaBB, uses plot*, barssince and security functions

2. you can't set certain constants from input due to Pinescript limitations - change the code as needed, recompile and use as a private version

3. Levels = trackprice implementation

4. Show Max Bars Back = show_last implementation

5. uses timeframe textbox instead of input resolution to allow for 120 240 and other custom TFs. Also supports TFs in hours: 2H or H2

6. swma has a fixed length = 4, alma and linreg have additional offset and smoothing params

7. Smoothing is applied by default for visual aesthetics on MTF. To use exact ma mtf values (lines with stair stepping) - disable it

MTF Notes:

- uses simple timeframe textbox instead of input resolution dropdown to allow for 120, 240 and other custom TFs, also supports timeframes in H: 2H, H2

- Groups that are not assigned a Custom TF will use Current Timeframe (0).

- MTF will work for any MA type assigned to the group

- MTF works both ways: you can display a higher TF MA/BB on a lower TF or a lower TF MA/BB on a higher TF.

- MTF MA values are normally aligned at the boundary of their native timeframe. This produces stair stepping when a higher TF MA is viewed on a lower TF.

Therefore X Y Point Density/Smoothing is applied by default on MA MTF for visual aesthetics. Set both to 0 to disable and see exact ma mtf values (lines with stair stepping and original mtf alignment).

- Smoothing is disabled for BB MTF bands because fill doesn't work with smoothed MAs after duplicate values are replaced with na.

- MTF MA Value fluctuation is possible on the current bar due to default security lookahead

Smoothing:

- X,Y == 0 - X,Y smoothing disabled (stair stepping on high TFs)

- X == 0, Y > 0 - X,Y smoothing applied to all TFs

- Y == 0, X > 0 - X smoothing applied to all TFs < deltaX_max_tf, Y smoothing disabled

- X > 0, Y > 0 - Y smoothing applied to all TFs, then X smoothing applied to all TFs < deltaX_max_tf

X Smoothing with Y == 0 - shows only every deltaX-th point starting from the first bar.

X Smoothing with Y > 0 - shows only every deltaX-th point starting from the last shown Y point, essentially filling huge gaps remaining after Y Smoothing with points and preserving the curve's general shape

X Smoothing on high TFs with already scarce points produces weird curve shapes, it works best only on high density lower TFs

Y Smoothing reduces points on all TFs, removes adjacent points with prices within deltaY, while preserving the smaller curve details.

A combination of X,Y produces the most accurate smoothing. Higher delta value - larger range, more points removed.

Show Max Bars Back:

- can't set plot show_last from input -> implemented using a timenow based range check

- you can't delete/modify history once plotted, so essentially it just sets a start point for plotting (from num_bars bars back) that works only in realtime mode (not in replay)

Levels:

You can plot current MA value using plot trackprice=true or by checking Show Price Line in Style. Problem is:

- you can only change color (not the dashed line style, width), have both ma + price line (not just the line), and it's full screen wide

- you can't set plot trackprice from input => implemented using plotshape/plotchar with fixed text labels serving as levels

- there's no other way of creating a dynamic level: hline, plot, offset - nothing else works.

- you can't plot a text var - all text strings must be constants, so you can't change the style, width and text labels without recompiling.

- from input you can only adjust offset, indent and shift for each level group, and change color

- the dot below each level line is the exact MA value. If you want just the line swap plotshape with plotchar, recompile and save as your private version, adjust Y shift.

To speed up redraw times: reduce last_bars to ~2000, recompile and use as your own private version

Pinescript is a rudimentary language (should be called Painscript instead) that can basically only plot data. You can't do much else. Please see the code for tips and hints.

Certain things just can't be done or require shady workarounds and weeks of testing trying to resolve weird node.js compiler errors.

Feel free to learn from/reuse/change the code as needed and use as your own private version. See comments in code. Good Luck!

One for AllOne for All (OFA) - Complete ICT Analysis Suite

Version 3.3.0 by theCodeman

📊 Overview

One for All (OFA) is a comprehensive TradingView indicator designed for traders who follow Inner Circle Trader (ICT) concepts. This all-in-one tool combines essential ICT analysis features—sessions, kill zones, previous period levels, and higher timeframe candles with Fair Value Gaps (FVGs) and Volume Imbalances (VIs)—into a single, highly customizable indicator. Whether you're a beginner learning ICT concepts or an experienced trader refining your edge, OFA provides the visual structure needed for precise market analysis and execution.

✨ Key Features

- 🏷️ Customizable Watermark**: Display your trading identity with customizable titles, subtitles, symbol info, and full style control

- 🌍 Trading Sessions**: Visualize Asian, London, and New York sessions with high/low lines, range boxes, and open/close markers

- 🎯 Kill Zones**: Highlight 5 critical ICT kill zones with precise timing and visual boxes

- 📈 Previous Period H/L**: Track Daily, Weekly, and Monthly highs/lows with customizable styles and lookback periods

- 🕐 Higher Timeframe Candles**: Display up to 5 HTF timeframes with OHLC trace lines, timers, and interval labels

- 🔍 FVG & VI Detection**: Automatically detect and visualize Fair Value Gaps and Volume Imbalances on HTF candles

- ⚙️ Universal Timezone Support**: Works globally with GMT-12 to GMT+14 timezone selection

- 🎨 Full Customization**: Control colors, styles, visibility, and layout for every feature

🚀 How to Use

Watermark Setup

The watermark overlay helps you identify your charts and maintain focus on your trading principles:

1. Enable/disable watermark via "Show Watermark" toggle

2. Customize the title (default: "Name") to display your trading name or account identifier

3. Set up to 3 subtitles (default: "Patience", "Confidence", "Execution") as trading reminders

4. Choose position (9 locations available), size, color, and transparency

5. Toggle symbol and timeframe display as needed

Use Case: Display your trading principles or account name for multi-monitor setups or content creation.

Trading Sessions Analysis

Sessions define market character and liquidity availability:

1. Enable "Show All Sessions" to visualize all three sessions

2. Adjust timezone to match your local market (default: UTC-5 for EST)

3. Customize session times if needed (defaults cover standard hours)

4. Enable session range boxes to see consolidation zones

5. Use session high/low lines to identify key levels for the current session

6. Enable open/close markers to track session transitions

Use Case: Identify which session you're trading in, track session highs/lows for liquidity, and anticipate session transition volatility.

Kill Zones Trading

Kill zones are ICT's high-probability trading windows:

1. Enable individual kill zones or use "Show All Kill Zones"

2. **Asian Kill Zone** (2000-0000 GMT): Early positioning and smart money accumulation

3. **London Kill Zone** (0300-0500 GMT): European market opening volatility

4. **NY AM Kill Zone** (0930-1100 EST): Post-NYSE open expansion

5. **NY Lunch Kill Zone** (1200-1300 EST): Midday consolidation or manipulation

6. **NY PM Kill Zone** (1330-1600 EST): Afternoon positioning and closes

7. Customize colors and times to match your trading style

8. Set max days display to control historical visibility (default: 30 days)

Use Case: Focus entries during high-probability windows. Watch for liquidity sweeps at kill zone openings and institutional positioning.

Previous Period High/Low Levels

Previous period levels act as magnetic price targets and support/resistance:

1. Enable Daily (PDH/PDL), Weekly (PWH/PWL), or Monthly (PMH/PML) levels individually

2. Set lookback period (how many previous periods to display)

3. Choose line style: Solid (current emphasis), Dashed (standard), or Dotted (subtle)

4. Customize colors per timeframe for visual hierarchy

5. Adjust line width (1-5) for visibility preference

6. Enable gradient effect to fade older periods

7. Position labels left or right based on chart layout

8. Customize label text for your preferred notation

Use Case: Identify key levels where price is likely to react. Daily levels work on intraday timeframes, Weekly on daily charts, Monthly for swing trading.

Higher Timeframe (HTF) Candles

HTF candles reveal the larger market context while trading lower timeframes:

1. Enable up to 5 HTF slots simultaneously (default: 5m, 15m, 1H, 4H, Daily)

2. Choose display mode: "Below Chart" (stacked rows) or "Right Side" (compact column)

3. Customize timeframe, colors (bull/bear), and titles for each slot

4. **OHLC Trace Lines**: Visual lines connecting HTF candle levels to chart bars

5. **HTF Timer**: Countdown showing time remaining until HTF candle close

6. **Interval Labels**: Display day of week (Daily+) or time (intraday) on each candle

7. For Daily candles: Choose open time (Midnight, 8:30, 9:30) to match your market structure preference

Use Case: Trade lower timeframes while respecting higher timeframe structure. Watch for HTF candle closes to confirm directional bias.

FVG & VI Detection

Fair Value Gaps and Volume Imbalances highlight inefficiencies that price often revisits:

1. **Fair Value Gaps (FVGs)**: Detected when HTF candle wicks don't overlap between 3 consecutive candles

- Bullish FVG: Gap between candle 1 high and candle 3 low (green box by default)

- Bearish FVG: Gap between candle 1 low and candle 3 high (red box by default)

2. **Volume Imbalances (VIs)**: Similar detection but focuses on body gaps

- Bullish VI: Gap between candle 1 close and candle 3 open

- Bearish VI: Gap between candle 1 open and candle 3 close

3. Enable FVG/VI detection per HTF slot individually

4. Customize colors and transparency for each imbalance type

5. Boxes appear on chart at formation and remain visible as retracement targets

**Use Case**: Identify high-probability retracement zones. Price often returns to fill FVGs and VIs before continuing the trend. Use as entry zones or profit targets.

🎨 Customization

OFA is built for flexibility. Every feature includes extensive customization options:

Visual Customization

- **Colors**: Independent color control for every element (sessions, kill zones, lines, labels, FVGs, VIs)

- **Transparency**: Adjust box and label transparency (0-100%) for clean charts

- **Line Styles**: Choose Solid, Dashed, or Dotted for previous period lines

- **Sizes**: Control text size, line width, and box borders

- **Positions**: Place watermark in 9 positions, labels left/right

Layout Control

- **HTF Display Mode**: "Below Chart" for detailed analysis, "Right Side" for space efficiency

- **Drawing Limits**: Set max days for sessions/kill zones to manage chart clutter

- **Lookback Periods**: Control how many previous periods to display (1-10)

- **Gradient Effects**: Enable fading for older previous period lines

Timing Adjustments

- **Timezone**: Universal GMT offset selector (-12 to +14) for global markets

- **Session Times**: Customize each session's start/end times

- **Kill Zone Times**: Adjust kill zone windows to match your market's characteristics

- **Daily Open**: Choose Midnight, 8:30, or 9:30 for Daily HTF candle open time

💡 Best Practices

1. Start Simple: Enable one feature at a time to learn how each element affects your analysis

2. Match Your Timeframe: Use Daily levels on intraday charts, Weekly on daily charts, HTF candles one or two levels above your trading timeframe

3. Kill Zone Focus: Concentrate your trading activity during kill zones for higher probability setups

4. HTF Confirmation: Wait for HTF candle closes before committing to directional bias

5. FVG/VI Entries: Look for price to return to unfilled FVGs/VIs for entry opportunities with favorable risk/reward

6. Customize Colors: Use a consistent color scheme that matches your chart theme and reduces visual fatigue

7. Reduce Clutter: Disable features you're not actively using in your current trading plan

8. Session Context: Understand which session controls the market—trade with session direction or anticipate reversals at session transitions

⚙️ Settings Guide

OFA organizes settings into logical groups for easy navigation:

- **═══ WATERMARK ═══**: Title, subtitles, position, style, symbol/timeframe display

- **═══ SESSIONS ═══**: Enable/disable sessions, times, colors, high/low lines, boxes, markers

- **═══ KILL ZONES ═══**: Individual kill zone toggles, times, colors, max days display

- **═══ PREVIOUS H/L - DAILY ═══**: Daily high/low lines, style, color, lookback, labels

- **═══ PREVIOUS H/L - WEEKLY ═══**: Weekly high/low lines, style, color, lookback, labels

- **═══ PREVIOUS H/L - MONTHLY ═══**: Monthly high/low lines, style, color, lookback, labels

- **═══ HTF CANDLES ═══**: Global display mode, layout settings

- **═══ HTF SLOT 1-5 ═══**: Individual HTF configuration (timeframe, colors, title, FVG/VI detection, trace lines, timer, interval labels)

Each setting includes tooltips explaining its function. Hover over any input for detailed guidance.

📝 Final Notes

One for All (OFA) represents a complete ICT analysis toolkit in a single indicator. By combining watermark customization, session visualization, kill zone highlighting, previous period levels, and higher timeframe candles with FVG/VI detection, OFA eliminates the need for multiple indicators cluttering your chart.

**Version**: 3.3.0

**Author**: theCodeman

**Pine Script**: v6

**License**: Mozilla Public License 2.0

Start with default settings to learn the indicator's structure, then customize extensively to match your personal trading style. Remember: tools provide information, but your edge comes from disciplined execution of a proven strategy.

Happy Trading! 📈

67 2.0Major Market Trading Hours

New York Stock Exchange (NYSE)

Open: 9:30 AM (ET)

Close: 4:00 PM (ET)

Pre-Market: 4:00 AM – 9:30 AM (ET)

After Hours: 4:00 PM – 8:00 PM (ET)

Nasdaq

Open: 9:30 AM (ET)

Close: 4:00 PM (ET)

Pre-Market: 4:00 AM – 9:30 AM (ET)

After Hours: 4:00 PM – 8:00 PM (ET)

London Stock Exchange (LSE)

Open: 8:00 AM (GMT)

Close: 4:30 PM (GMT)

Tokyo Stock Exchange (TSE)

Open: 9:00 AM (JST)

Lunch Break: 11:30 AM – 12:30 PM (JST)

Close: 3:00 PM (JST)

Hong Kong Stock Exchange (HKEX)

Open: 9:30 AM (HKT)

Lunch Break: 12:00 PM – 1:00 PM (HKT)

Close: 4:00 PM (HKT)