Smart Relative Strength Can Remove False SignalsRelative strength is one of the most useful indicators in the market, highlighting when stocks and sectors are outperforming or underperforming a broader index.

Traditional RS compares the percentage change of one symbol over a given time frame and subtracts the percentage change of the S&P 500 over the same period.

This is handy, but it can produce false signals at times of volatility. For example, when the broader market is crashing, certain sectors may “outperform” simply by falling less than the S&P 500.

Smart Relative Strength addresses this shortcoming by requiring that the symbol’s absolute AND relative returns both be positive. Otherwise a zero is returned.

This was useful last week on the Dow Jones Transportation Average . Using simple relative strength, it had its best one-week performance against the S&P 500 since October 2008. This was obviously a false signal because October 2008 was a time that everything else was crashing.

Smart Relative Strength showed that, excluding periods of overall decline, DJT had its best week since January 2008.

Note: This chart uses a 1-period interval, while the code defaults to 21 periods.

Cari skrip untuk "美股道琼斯工业平均指数、纳斯达克指数、标普500指数的成交量数据"

Stress DashboardEnglish:

The Stress Dashboard is based on the Kansas City Financial Stress Index. In most general terms, financial stress can be thought of as an interruption to the normal functioning of financial markets.

For more information about the Stress index read the pdf from kansascityfed.org:

www.kansascityfed.org

If the value is above 0 it indicates that financial stress is above the long-run average, while a value below 0 signifies that financial stress is below the long-run average.

You can use it as a early warning system to bigger down moves or possible crashes and left the market early.

I use it in combine with my Volatility Dashboard as my own early warning system because the Stess Index only get updated monthly so that the Volatility Dashboard warning me much faster.

I dont want to have only one crash indicator so I search for another and found these. If you transfer the red areas of the indicator into the S&P 500 Chart then you can see how good these Dashboard warning you for a following crash/ downtrend/ bigger correction.

Deutsch:

Das Stress Dashboard basiert auf dem Kansas City Financial Stress Index. Finanzielle Belastungen können im Allgemeinen als Unterbrechung des normalen Funktionierens der Finanzmärkte angesehen werden.

Weitere Informationen zum Stress-Index finden Sie im PDF von kansascityfed.org:

www.kansascityfed.org

Wenn der Wert über 0 liegt bedeutet dies, dass die finanzielle Belastung über dem langfristigen Durchschnitt liegt, während ein Wert unter 0 bedeutet, dass die finanzielle Belastung unter dem langfristigen Durchschnitt liegt.

Sie können es als Frühwarnsystem für größere Abwärtsbewegungen oder mögliche Abstürze verwenden und den Markt frühzeitig verlassen.

Ich verwende es in Kombination mit meinem Volatility Dashboard als mein eigenes Frühwarnsystem, da der Stess-Index nur monatlich aktualisiert wird, sodass mich das Volatility Dashboard viel schneller warnt.

Ich möchte nicht nur einen Crash Indikator haben, also suchte ich nach einer weiteren und fand diesen. Wenn Sie die roten Bereiche des Indikators in den S&P 500 Chart übertragen, können Sie sehen wie gut dieses Dashboard Sie vor einem folgenden Absturz / Abwärtstrend / einer größeren Korrektur warnt.

RISK-OFF.RISK.ON-ppxdf.v3======================================= RISK-OFF & RISK ON INDEX ================================================

1. Stock Price Momentum: Measuring the Standard & Poor's 500 Index ( S&P 500 ) versus its 125-day moving average (MA)

2. Stock Price Strength: Calculating the number of stocks hitting 52-week highs versus those hitting 52-week lows on the New York Stock Exchange (NYSE)

3. Stock Price Breadth: Analyzing trading volumes in rising stocks against declining stocks

4. Put and Call Options: How much do put options lag behind call options, signifying greed, or surpass them, indicating fear

5. Junk Bond Demand: Gauging appetite for higher risk strategies by measuring the spread between yields on investment-grade bonds and junk bonds

6. Market Volatility: CNN measures the Chicago Board Options Exchange Volatility Index ( VIX ), concentrating on a 50-day MA

7. Safe Haven Demand: The difference in returns for stocks versus treasuries

Each of these seven indicators is measured on a scale from 0 to 100, with the index being computed by taking an equal-weighted average of each of them.

A reading of 50 is deemed NEUTRAL.

Above 50 signals the market with RISK-ON. (GREED)

Below 50, Signals the market with RISK-OFF (FEAR)

8

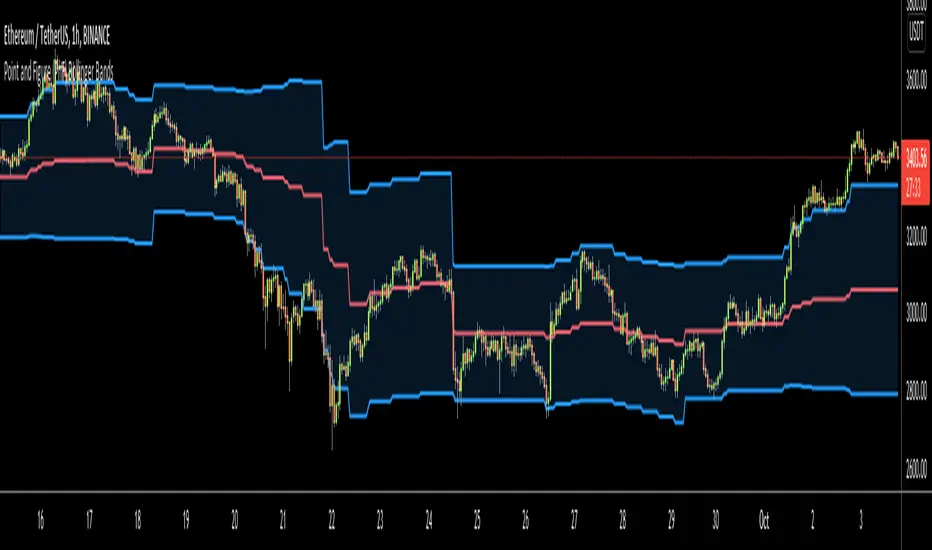

Point and Figure (PnF) Weis Wave VolumeThis is live and non-repainting Point and Figure Chart Weis Wave Volume tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

This tool is based on the Weis Wave described by David H. Weis (a Wyckoff specialist). The Weis Waves Indicator sums up volumes in each wave. This is how we receive a bar chart of cumulative volumes of alternating waves and The cumulative volume makes the Weis wave charts unique.

If there is no volume information for the security then this tool has an option to use “True Range” instead of volume .

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

There is only one option for Weis Wave Volume, “Use True Range (if no Volume info)” if you select this option and volume info is not avaliable then it uses “true range”, but if volume info is available, it never use true range. Default value is set to use true range.

Point and Figure (PnF) Moving Averages HistogramThis is live and non-repainting Point and Figure Chart Moving Average Histogram tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

Moving averages on Point & Figure charts are based on the average price of each column while bar chart moving averages are based closing price. Average Price means (ClosePrice + OpenPrice) / 2.

Because of there is double smoothing, you should use shorter lengths for moving averages. Double smoothing means: using average price smooths once, using length greater than 2 smooths price second time.

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

Options for P&F Bollinger Bands:

MA Type: MA type can be EMA or SMA

MA Source: Moving averages on P&F charts are based on the average price of each column. Bar chart moving averages are based on each close price. Average price means “(ClosePrice + OpenPrice) / 2”. You can choose Close Price or Average Price as source. Default is Average Price.

Fast MA Length : Length of Fast Moving average, shorter length than Slow MA

Slow MA Length : Length of Slow Moving average, greater length than Slow MA

There are alerts when Fast MA Crossed over/under Slow MA conditions. While adding alert “Once Per Bar Close” option should be chosen.

Point and Figure (PnF) Moving AveragesThis is live and non-repainting Point and Figure Chart Moving Averages tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

Moving averages on Point & Figure charts are based on the average price of each column while bar chart moving averages are based closing price. Average Price means (ClosePrice + OpenPrice) / 2.

Because of there is double smoothing, you should use shorter lengths for moving averages. Double smoothing means: using average price smooths once, using length greater than 2 smooths price second time.

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

Options for P&F Moving Averages:

Moving averages on P&F charts are based on the average price of each column. Bar chart moving averages are based on each close price. While 10-day SMA on a bar chart is the average of the last ten closing prices, on a P&F chart, a 10-period SMA is the average price of the last 10 column averages. Average price means “(ClosePrice + OpenPrice) / 2”

2 P&F moving averages are shown on the chart.

It can show Exponental Moving Average ( EMA ) or Simple Moving Average ( SMA )

Source: You can choose Close Price or Average Price as source. Default is Average Price.

“Fast Length” and “Slow Length” are lengths for two moving averages. Default values are 1 and 5.

“Fill between MAs” is the option to fill between Moving averages by predefined colors 'Lime/Blue', 'Lime/Red', 'Green/Red', 'Green/Blue', 'Blue/Red'

There are alerts when Fast MA crossover or crossunder Slow MA. While adding alert “Once Per Bar Close” option should be chosen.

Point and Figure (PnF) MomentumThis is live and non-repainting Point and Figure Chart Momentum tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

Momentum indicator measures the rate of change or speed of price movement. It compares the current price with the previous price from a number of periods ago. By analysing the rate of change , possible to gauge the strength or “momentum”. By using this script we get Point and Figure chart momentum.

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

There is 2 options for P&F Momentum

Length: Length for the P&F Momentum, default value is 10

Display as: there are two options and can display as “Histogram” or “Line”

Point and Figure (PnF) MACDThis is live and non-repainting Point and Figure Chart MACD tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

P&F MACD is calculated and shown by using its own P&F engine.

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

P&F MACD Part

Fast Length: Fast Length for P&F MACD , default value is 12

Slow Length: Fast Length for P&F MACD , default value is 26

Signal Smoothing: Signal Length, default value is 9

Source: Moving averages on P&F charts are based on the average price of each column. Bar chart moving averages are based on each close price. Average price means “(ClosePrice + OpenPrice) / 2”. You can choose Close Price or Average Price as source. Default is Average Price.

There are 2 Alerts:

If PNF MACD line crossover the signal line

If PNF MACD line crossunder the signal line

While adding alert “Once Per Bar Close” option should be chosen.

Point and Figure (PnF) CCIThis is live and non-repainting Point and Figure Chart Commodity Channel Index - CCI tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

Commodity Channel Index – CCI was developed by Donalt Lambert. CCI can be used to identify overbought or oversold, a new trend or warn of extreme conditions. CCI measures the difference between a security's price change and its average price change. High positive readings indicate that prices are well above their average, which is a show of strength. Low negative readings indicate that prices are well below their average, which is a show of weakness.

The Formula for the Commodity Channel Index ( CCI ) Is:

CCI = (Typical Price – L-period SMA of TP) / (0.015 * Mean Deviation)

Mean Deviation = (SumOf 1->L ( |TP – MA| )) / L

L = Length

TP = Typical Price

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

Upper Band : as default, Upper band is 100

Lower Band : as default, Lower band is -100

There are alerts when P&F CCI moves above Upper Band or moves below Lower Band.

Point and Figure (PnF) Bollinger BandsThis is live and non-repainting Point and Figure Chart Bollinger Bands tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

P&F Bollinger Bands is calculated and shown by using its own P&F engine. Because of Point and Figure Chart Moving averages are already smoothed, better to use smaller moving average periods, 5 or 10 etc. This period can be chosen by prives movements and characteristics. You can see the consolidation areas and with P&F Breakout signals it’s possible to see the direction. Narrowing bands indicate a consolidation and narrowing does not provide a direction clue. You must look for the next P&F signal to establish direction. But beware of the ‘head fake’. This occurs when prices break a band, then suddenly reverse and move the other way (Trap).

An example for Head Fake:

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

Options P&F Bollimger Bands:

Length: Base Moving Average Length, default value is 5

StdDev: Standart Deviation, default value ise 2. (Standart deviation is calculated by the engine)

MA Source: Moving averages on P&F charts are based on the average price of each column. Bar chart moving averages are based on each close price. Average price means “(ClosePrice + OpenPrice) / 2”. You can choose Close Price or Average Price as source. Default is Average Price.

Point and Figure (PnF) RSIThis is live and non-repainting Point and Figure Chart RSI tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

P&F RSI is calculated and shown by using its own P&F engine.

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

you can use PNF type RSI or RENKO type RSI.

What is the difference between them?

While calculating PNF type RSI, the script checks last X/O column's closing price but when using RENKO type RSI the scipt calculates RSI on every price changes according to number of boxes. and also with RENKO type RSI, calculation is made for each boxes on price changes.

Important note if you use this PNF script with reversal = 2 then you get RENKO chart. So, with this RENKO chart better to use RENKO type RSI ;)

Point and Figure (PnF) ChartThis is live and non-repainting Point and Figure Charting tool. The tool has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

Chart Style: There are 3 options for chart style: “Candle”, “Area” or “Don’t show”.

As Area:

As Candle:

X/O Column Style: it can show all columns from opening price or only last Xs/Os.

Color Theme: different themes exist => Green/Red, Yellow/Blue, White/Yellow, Orange/Blue, Lime/Red, Blue/Red

Show Breakouts is the option to show Breakouts

This tool detects & shows following Breakouts:

Triple Top/Bottom,

Triple Top Ascending,

Triple Bottom Descending,

Simple Buy/Sell (Double Top/Bottom),

Simple Buy With Rising Bottom,

Simple Sell With Declining Top

Catapult bullish/bearish

Show Horizontal Count Targets: Finds the congestion or consolidation pattern and if there is breakout then it calculates the Target by using Horizontal Count method (based on the width of congestion pattern). It shows how many column exist on congestion area. There is no guarantee that prices will reach the target.

Show Vertical Count Targets: When Triple Top/Bottom Breakouts occured the script calculates the target by using Vertical Count Method (based on the length of the column). There is no guarantee that prices will reach the target.

For both methods there is auto target cancellation if price goes below congestion bottom or above congestion top.

trend is calculated by EMA of closing price of the P&F

Whipsaw protection:

Last options are “Show info panel” and Labeling Offset. Script shows current box size, reversal, and recommanded minimum and maximum box size. And also it shows the price level to reverse the column (Xs <-> Os) and the price level to add at least 1 more box to column. This is the option to put these labels 10, 20, 30, 50 or 100 bars away from the last bar. Labeling content and color change according to X/O column.

do not hesitate to comment.

Candlesticks ANN for Stock Markets TF : 1WHello, this script consists of training candlesticks with Artificial Neural Networks (ANN).

In addition to the first series, candlesticks' bodies and wicks were also introduced as training inputs.

The inputs are individually trained to find the relationship between the subsequent historical value of all candlestick values 1.(High,Low,Close,Open)

The outputs are adapted to the current values with a simple forecast code.

Once the OHLC value is found, the exponential moving averages of 5 and 20 periods are used.

Reminder : OHLC = (Open + High + Close + Low ) / 4

First version :

Script is designed for S&P 500 Indices,Funds,ETFs, especially S&P 500 Stocks,and for all liquid Stocks all around the World.

NOTE: This script is only suitable for 1W time-frame for Stocks.

The average training error rates are less than 5 per thousand for each candlestick variable. (Average Error < 0.005 )

I've just finished it and haven't tested it in detail.

So let's use it carefully as a supporter.

Best regards !

TNZ - Index above MA Use this indicator to filter stock selection based on the relevant index value being above the selected simple moving average.

For example, only buying the S+P 500 stock if the S+P 500 index value is above the 10 period moving average.

The time frame used is that displayed

Macroeconomic Artificial Neural Networks

This script was created by training 20 selected macroeconomic data to construct artificial neural networks on the S&P 500 index.

No technical analysis data were used.

The average error rate is 0.01.

In this respect, there is a strong relationship between the index and macroeconomic data.

Although it affects the whole world,I personally recommend using it under the following conditions: S&P 500 and related ETFs in 1W time-frame (TF = 1W SPX500USD, SP1!, SPY, SPX etc. )

Macroeconomic Parameters

Effective Federal Funds Rate (FEDFUNDS)

Initial Claims (ICSA)

Civilian Unemployment Rate (UNRATE)

10 Year Treasury Constant Maturity Rate (DGS10)

Gross Domestic Product , 1 Decimal (GDP)

Trade Weighted US Dollar Index : Major Currencies (DTWEXM)

Consumer Price Index For All Urban Consumers (CPIAUCSL)

M1 Money Stock (M1)

M2 Money Stock (M2)

2 - Year Treasury Constant Maturity Rate (DGS2)

30 Year Treasury Constant Maturity Rate (DGS30)

Industrial Production Index (INDPRO)

5-Year Treasury Constant Maturity Rate (FRED : DGS5)

Light Weight Vehicle Sales: Autos and Light Trucks (ALTSALES)

Civilian Employment Population Ratio (EMRATIO)

Capacity Utilization (TOTAL INDUSTRY) (TCU)

Average (Mean) Duration Of Unemployment (UEMPMEAN)

Manufacturing Employment Index (MAN_EMPL)

Manufacturers' New Orders (NEWORDER)

ISM Manufacturing Index (MAN : PMI)

Artificial Neural Network (ANN) Training Details :

Learning cycles: 16231

AutoSave cycles: 100

Grid

Input columns: 19

Output columns: 1

Excluded columns: 0

Training example rows: 998

Validating example rows: 0

Querying example rows: 0

Excluded example rows: 0

Duplicated example rows: 0

Network

Input nodes connected: 19

Hidden layer 1 nodes: 2

Hidden layer 2 nodes: 0

Hidden layer 3 nodes: 0

Output nodes: 1

Controls

Learning rate: 0.1000

Momentum: 0.8000 (Optimized)

Target error: 0.0100

Training error: 0.010000

NOTE : Alerts added . The red histogram represents the bear market and the green histogram represents the bull market.

Bars subject to region changes are shown as background colors. (Teal = Bull , Maroon = Bear Market )

I hope it will be useful in your studies and analysis, regards.

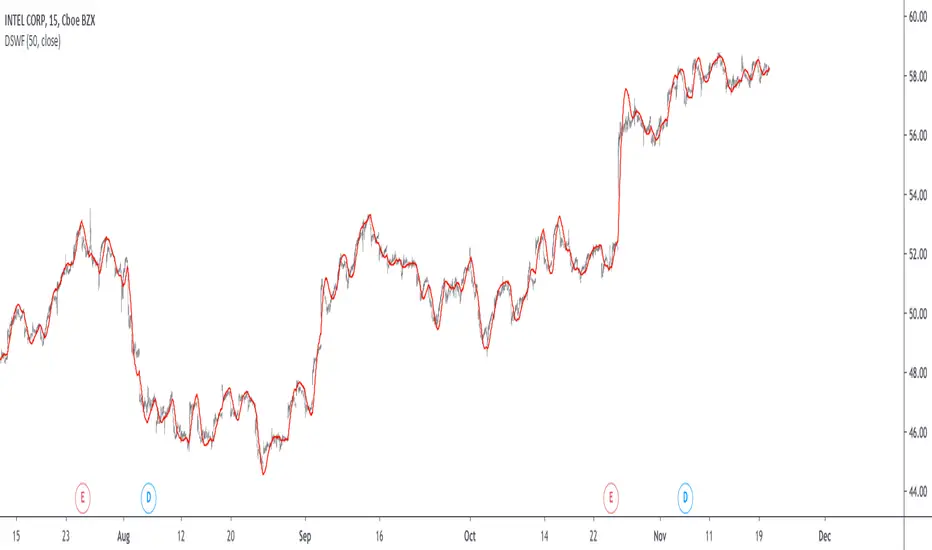

Damped Sine Wave Weighted FilterIntroduction

Remember that we can make filters by using convolution, that is summing the product between the input and the filter coefficients, the set of filter coefficients is sometime denoted "kernel", those coefficients can be a same value (simple moving average), a linear function (linearly weighted moving average), a gaussian function (gaussian filter), a polynomial function (lsma of degree p with p = order of the polynomial), you can make many types of kernels, note however that it is easy to fall into the redundancy trap.

Today a low-lag filter who weight the price with a damped sine wave is proposed, the filter characteristics are discussed below.

A Damped Sine Wave

A damped sine wave is a like a sine wave with the difference that the sine wave peak amplitude decay over time.

A damped sine wave

Used Kernel

We use a damped sine wave of period length as kernel.

The coefficients underweight older values which allow the filter to reduce lag.

Step Response

Because the filter has overshoot in the step response we can conclude that there are frequencies amplified in the passband, we could have reached to this conclusion by simply seeing the negative values in the kernel or the "zero-lag" effect on the closing price.

Enough ! We Want To See The Filter !

I should indeed stop bothering you with transient responses but its always good to see how the filter act on simpler signals before seeing it on the closing price. The filter has low-lag and can be used as input for other indicators

Filter with length = 100 as input for the rsi.

The bands trailing stop utility using rolling squared mean average error with length 500 using the filter of length 500 as input.

Approximating A Least Squares Moving Average

A least squares moving average has a linear kernel with certain values under 0, a lsma of length k can be approximated using the proposed filter using period p where p = k + k/4 .

Proposed filter (red) with length = 250 and lsma (blue) with length = 200.

Conclusions

The use of damping in filter design can provide extremely useful filters, in fact the ideal kernel, the sinc function, is also a damped sine wave.

VIX reversion-Buschi

English:

A significant intraday reversion (commonly used: 3 points) on a high (over 20 points) S&P 500 Volatility Index (VIX) can be a sign of a market bottom, because there is the assumption that some of the "big guys" liquidated their options / insurances because the worst is over.

This indicator shows these reversions (3 points as default) when the VIX was over 20 points. The character "R" is then shown directly over the daily column, the VIX need not to be loaded explicitly.

Deutsch:

Eine deutliche Intraday-Umkehr (3 Punkte im Normalfall) bei einem hohen (über 20 Punkte) S&P 500 Volatility Index (VIX) kann ein Zeichen für eine Bodenbildung im Markt sein, weil möglicherweise einige "große Jungs" ihre Optionen / Versicherungen auflösen, weil das schlimmste vorbei ist.

Dieser Indikator zeigt diese Umkehr (Standardwert: 3 Punkte), wenn der VIX vorher über 20 Punkte lag. Der Buchstabe "R" wird dabei direkt über dem Tagesbalken angezeigt, wobei der VIX nicht explizit geladen werden muss.

Relative Price StrengthThe strength of a stock relative to the S&P 500 is key part of most traders decision making process. Hence the default reference security is SPY, the most commonly trades S&P 500 ETF.

Most profitable traders buy stocks that are showing persistence intermediate strength verses the S&P as this has been shown to work. Hence the default period is 63 days or 3 months.

TICK Extremes IndicatorSimple TICK indicator, plots candles and HL2 line

Conditional green/red coloring for highs above 500, 900 and lows above 0, and for lows below -500, -900, and highs above 0

Probably best used for 1 - 5 min timeframes

Always open to suggestions if criteria needs tweaking or if something else would make it more useful or user-friendly!

Market direction and pullback based on S&P 500.A simple indicator based on www.swing-trade-stocks.com The link is also the guide for how to use it.

0 - nothing. If the indicator is showing 0 for a prolonged amount of time, it is likely the market is in "momentum mode" (referred to in the link above).

1 - indicates an uptrend based on SMA and EMA and also a place where a reversal to the upside is likely to occur. You should look only for long trades in the stock market when you see a spike upwards and S&P 500 is showing an obvious uptrend.

-1 - indicates a downtrend based on SMA and EMA and also a place where a reversal to the downside is likely to occur. You should look only for short trades in the stock market when you see a spike upwards and S&P 500 is showing an obvious uptrend.

Net XRP Margin PositionTotal XRP Longs minus XRP Shorts in order to give you the total outstanding XRP margin debt.

ie: If 500,000 XRP has been longed, and 400,000 XRP has been shorted, then 500,000 has been bought, and 400,000 sold, leaving us with 100,000 XRP (net) remaining to be sold to give us an overall neutral margin position.

That isn't to say that the net margin position must move towards zero, but it is a sensible reference point, and historical net values may provide useful insights into the current circumstances.

Net DASH Margin PositionTotal DASH Longs minus DASH Shorts in order to give you the total outstanding DASH margin debt.

ie: If 500,000 DASH has been longed, and 400,000 DASH has been shorted, then 500,000 has been bought, and 400,000 sold, leaving us with 100,000 DASH (net) remaining to be sold to give us an overall neutral margin position.

That isn't to say that the net margin position must move towards zero, but it is a sensible reference point, and historical net values may provide useful insights into the current circumstances.

(Anyone know what category this script should be in?)

Net NEO Margin PositionTotal NEO Longs minus NEO Shorts in order to give you the total outstanding NEO margin debt.

ie: If 500,000 NEO has been longed, and 400,000 NEO has been shorted, then 500,000 has been bought, and 400,000 sold, leaving us with 100,000 NEO (net) remaining to be sold to give us an overall neutral margin position.

That isn't to say that the net margin position must move towards zero, but it is a sensible reference point, and historical net values may provide useful insights into the current circumstances.

(Anyone know what category this script should be in?)