MTF RSI CandlesThis Pine Script indicator is designed to provide a visual representation of Relative Strength Index (RSI) values across multiple timeframes. It enhances traditional candlestick charts by color-coding candles based on RSI levels, offering a clearer picture of overbought, oversold, and sideways market conditions. Additionally, it displays a hoverable table with RSI values for multiple predefined timeframes.

Key Features

1. Candle Coloring Based on RSI Levels:

Candles are color-coded based on predefined RSI ranges for easy interpretation of market conditions.

RSI Levels:

75-100: Strongest Overbought (Green)

65-75: Stronger Overbought (Dark Green)

55-65: Overbought (Teal)

45-55: Sideways (Gray)

35-45: Oversold (Light Red)

25-35: Stronger Oversold (Dark Red)

0-25: Strongest Oversold (Bright Red)

2. Multi-Timeframe RSI Table:

Displays RSI values for the following timeframes:

1 Min, 2 Min, 3 Min, 4 Min, 5 Min

10 Min, 15 Min, 30 Min, 1 Hour, 1 Day, 1 Week

Helps traders identify RSI trends across different time horizons.

3. Hoverable RSI Values:

Displays the RSI value of any candle when hovering over it, providing additional insights for analysis.

Inputs

1. RSI Length:

Default: 14

Determines the calculation period for the RSI indicator.

2. RSI Levels:

Configurable thresholds for RSI zones:

75-100: Strongest Overbought

65-75: Stronger Overbought

55-65: Overbought

45-55: Sideways

35-45: Oversold

25-35: Stronger Oversold

0-25: Strongest Oversold

How It Works:

1. RSI Calculation:

The RSI is calculated for the current timeframe using the input RSI Length.

It is also computed for 11 additional predefined timeframes using request.security.

2. Candle Coloring:

Candles are colored based on their RSI values and the specified RSI levels.

3. Hoverable RSI Values:

Each candle displays its RSI value when hovered over, via a dynamically created label.

Multi-Timeframe Table:

A table at the bottom-left of the chart displays RSI values for all predefined timeframes, making it easy to compare trends.

Usage:

1. Trend Identification:

Use candle colors to quickly assess market conditions (overbought, oversold, or sideways).

2. Timeframe Analysis:

Compare RSI values across different timeframes to determine long-term and short-term momentum.

3. Signal Confirmation:

Combine RSI signals with other indicators or patterns for higher-confidence trades.

Best Practices

Use this indicator in conjunction with volume analysis, support/resistance levels, or trendline strategies for better results.

Customize RSI levels and timeframes based on your trading strategy or market conditions.

Limitations

RSI is a lagging indicator and may not always predict immediate market reversals.

Multi-timeframe analysis can lead to conflicting signals; consider your trading horizon.

Cari skrip untuk "汇丰股票25"

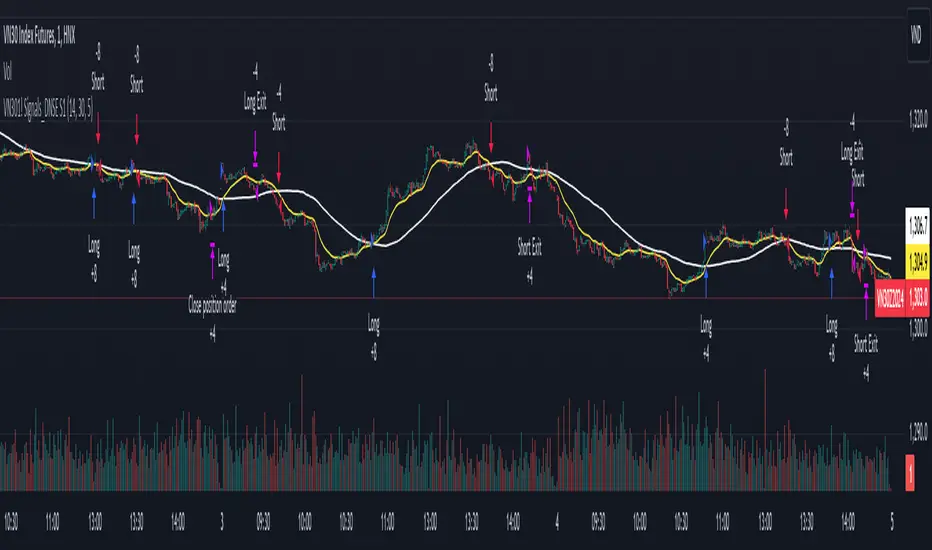

DNSE VN301!, SMA & EMA Cross StrategyDiscover the tailored Pinescript to trade VN30F1M Future Contracts intraday, the strategy focuses on SMA & EMA crosses to identify potential entry/exit points. The script closes all positions by 14:25 to avoid holding any contracts overnight.

HNX:VN301!

www.tradingview.com

Setting & Backtest result:

1-minute chart, initial capital of VND 100 million, entering 4 contracts per time, backtest result from Jan-2024 to Nov-2024 yielded a return over 40%, executed over 1,000 trades (average of 4 trades/day), winning trades rate ~ 30% with a profit factor of 1.10.

The default setting of the script:

A decent optimization is reached when SMA and EMA periods are set to 60 and 15 respectively while the Long/Short stop-loss level is set to 20 ticks (2 points) from the entry price.

Entry & Exit conditions:

Long signals are generated when ema(15) crosses over sma(60) while Short signals happen when ema(15) crosses under sma(60). Long orders are closed when ema(15) crosses under sma(60) while Short orders are closed when ema(15) crosses over sma(60).

Exit conditions happen when (whichever came first):

Another Long/Short signal is generated

The Stop-loss level is reached

The Cut-off time is reached (14:25 every day)

*Disclaimers:

Futures Contracts Trading are subjected to a high degree of risk and price movements can fluctuate significantly. This script functions as a reference source and should be used after users have clearly understood how futures trading works, accessed their risk tolerance level, and are knowledgeable of the functioning logic behind the script.

Users are solely responsible for their investment decisions, and DNSE is not responsible for any potential losses from applying such a strategy to real-life trading activities. Past performance is not indicative/guarantee of future results, kindly reach out to us should you have specific questions about this script.

---------------------------------------------------------------------------------------

Khám phá Pinescript được thiết kế riêng để giao dịch Hợp đồng tương lai VN30F1M trong ngày, chiến lược tập trung vào các đường SMA & EMA cắt nhau để xác định các điểm vào/ra tiềm năng. Chiến lược sẽ đóng tất cả các vị thế trước 14:25 để tránh giữ bất kỳ hợp đồng nào qua đêm.

Thiết lập & Kết quả backtest:

Chart 1 phút, vốn ban đầu là 100 triệu đồng, vào 4 hợp đồng mỗi lần, kết quả backtest từ tháng 1/2024 tới tháng 11/2024 mang lại lợi nhuận trên 40%, thực hiện hơn 1.000 giao dịch (trung bình 4 giao dịch/ngày), tỷ lệ giao dịch thắng ~ 30% với hệ số lợi nhuận là 1,10.

Thiết lập mặc định của chiến lược:

Đạt được một mức tối ưu ổn khi SMA và EMA periods được đặt lần lượt là 60 và 15 trong khi mức cắt lỗ được đặt thành 20 tick (2 điểm) từ giá vào.

Điều kiện Mở và Đóng vị thế:

Tín hiệu Long được tạo ra khi ema(15) cắt trên sma(60) trong khi tín hiệu Short xảy ra khi ema(15) cắt dưới sma(60). Lệnh Long được đóng khi ema(15) cắt dưới sma(60) trong khi lệnh Short được đóng khi ema(15) cắt lên sma(60).

Điều kiện đóng vị thể xảy ra khi (tùy điều kiện nào đến trước):

Một tín hiệu Long/Short khác được tạo ra

Giá chạm mức cắt lỗ

Lệnh chưa đóng nhưng tới giờ cut-off (14:25 hàng ngày)

*Tuyên bố miễn trừ trách nhiệm:

Giao dịch hợp đồng tương lai có mức rủi ro cao và giá có thể dao động đáng kể. Chiến lược này hoạt động như một nguồn tham khảo và nên được sử dụng sau khi người dùng đã hiểu rõ cách thức giao dịch hợp đồng tương lai, đã đánh giá mức độ chấp nhận rủi ro của bản thân và hiểu rõ về logic vận hành của chiến lược này.

Người dùng hoàn toàn chịu trách nhiệm về các quyết định đầu tư của mình và DNSE không chịu trách nhiệm về bất kỳ khoản lỗ tiềm ẩn nào khi áp dụng chiến lược này vào các hoạt động giao dịch thực tế. Hiệu suất trong quá khứ không chỉ ra/cam kết kết quả trong tương lai, vui lòng liên hệ với chúng tôi nếu bạn có thắc mắc cụ thể về chiến lược giao dịch này.

RSI 15/60 and ADX PlotIn this script, the buy and sell criteria are based on the Relative Strength Index (RSI) values calculated for two different timeframes: the 15-minute RSI and the hourly RSI. These timeframes are used together to check signals when certain thresholds are crossed, providing confirmation across both short-term and longer-term momentum.

Buy Criteria:

Condition 1:

Hourly RSI > 60: This means the longer-term momentum shows strength.

15-minute RSI crosses above 60: This shows that the shorter-term momentum is catching up and confirms increasing strength.

Condition 2:

15-minute RSI > 60: This indicates that the short-term trend is already strong.

Hourly RSI crosses above 60: This confirms that the longer-term trend is also gaining strength.

Both conditions aim to capture the moments when the market shows increasing strength across both short and long timeframes, signaling a potential buy opportunity.

Sell Criteria:

Condition 1:

Hourly RSI < 40: This indicates that the longer-term trend is weakening.

15-minute RSI crosses below 40: The short-term momentum is also turning down, confirming the weakening trend.

Condition 2:

15-minute RSI < 40: The short-term trend is already weak.

Hourly RSI crosses below 40: The longer-term trend is now confirming the weakness, indicating a potential sell.

These conditions work to identify when the market is showing weakness in both short-term and long-term timeframes, signaling a potential sell opportunity.

ADX Confirmation :

The Average Directional Index (ADX) is a key tool for measuring the strength of a trend. It can be used alongside the RSI to confirm whether a buy or sell signal is occurring in a strong trend or during market consolidation. Here's how ADX can be integrated:

ADX > 25: This indicates a strong trend. Using this threshold, you can confirm buy or sell signals when there is a strong upward or downward movement in the market.

Buy Example: If a buy signal (RSI > 60) is triggered and the ADX is above 25, this confirms that the market is in a strong uptrend, making the buy signal more reliable.

Sell Example: If a sell signal (RSI < 40) is triggered and the ADX is above 25, it confirms a strong downtrend, validating the sell signal.

ADX < 25: This suggests a weak or non-existent trend. In this case, RSI signals might be less reliable since the market could be moving sideways.

Final Approach:

The RSI criteria help identify potential overbought and oversold conditions in both short and long timeframes.

The ADX confirmation ensures that the signals generated are happening during strong trends, increasing the likelihood of successful trades by filtering out weak or choppy market conditions.

This combination of RSI and ADX can help traders make more informed decisions by ensuring both momentum and trend strength align before entering or exiting trades.

Average Directional Index with MACombining the Average Directional Index (ADX) with a 14-period Exponential Moving Average (EMA) can provide traders with a comprehensive approach to identify both the strength of a trend (through ADX) and the trend's direction (using EMA). Let's break down each component and then discuss how they can be combined:

Average Directional Index (ADX):

The ADX is a technical indicator that measures the strength or momentum of a trend, regardless of its direction. The ADX is derived from two other indicators:

Positive Directional Index (+DI): Measures the strength of upward price movement.

Negative Directional Index (-DI): Measures the strength of downward price movement.

14-period Exponential Moving Average (EMA):

The 14-period EMA is a trend-following indicator that gives more weight to recent price data compared to simple moving averages (SMAs). The EMA is calculated by taking the average of the last 14 closing prices, giving more importance to the most recent prices.

Combining ADX and EMA:

When combining ADX with a 14-period EMA:

ADX as a Filter:

Traders might use the ADX to filter out trades when the trend's strength is weak (e.g., ADX below 25) to avoid trading in sideways or choppy markets.

EMA for Trend Direction:

Traders can use the 14-period EMA to determine the trend direction.

A price above the 14-period EMA might indicate an uptrend, while a price below the EMA might suggest a downtrend.

Example Strategy:

Here's a simplified trading strategy combining ADX and EMA:

Trend Identification:

Buy when the price is above the 14-period EMA and the ADX indicates a strong uptrend (e.g., ADX > 25).

Sell or go short when the price is below the 14-period EMA and the ADX indicates a strong downtrend (e.g., ADX > 25).

Avoid Choppy Markets:

Avoid trading when the ADX is below a certain threshold (e.g., ADX < 25) to filter out sideways or range-bound markets.

Combining ADX and a 14-period EMA can provide traders with a balanced approach to identify both the strength and direction of a trend. However, it's essential to remember that no indicator or strategy can guarantee profits, and it's crucial to use risk management techniques and other tools to make informed trading decisions. Consider back testing this strategy on historical data and adjusting the parameters based on their trading style and risk tolerance.

Statistics • Chi Square • P-value • SignificanceThe Statistics • Chi Square • P-value • Significance publication aims to provide a tool for combining different conditions and checking whether the outcome is significant using the Chi-Square Test and P-value.

🔶 USAGE

The basic principle is to compare two or more groups and check the results of a query test, such as asking men and women whether they want to see a romantic or non-romantic movie.

–––––––––––––––––––––––––––––––––––––––––––––

| | ROMANTIC | NON-ROMANTIC | ⬅︎ MOVIE |

–––––––––––––––––––––––––––––––––––––––––––––

| MEN | 2 | 8 | 10 |

–––––––––––––––––––––––––––––––––––––––––––––

| WOMEN | 7 | 3 | 10 |

–––––––––––––––––––––––––––––––––––––––––––––

|⬆︎ SEX | 10 | 10 | 20 |

–––––––––––––––––––––––––––––––––––––––––––––

We calculate the Chi-Square Formula, which is:

Χ² = Σ ( (Observed Value − Expected Value)² / Expected Value )

In this publication, this is:

chiSquare = 0.

for i = 0 to rows -1

for j = 0 to colums -1

observedValue = aBin.get(i).aFloat.get(j)

expectedValue = math.max(1e-12, aBin.get(i).aFloat.get(colums) * aBin.get(rows).aFloat.get(j) / sumT) //Division by 0 protection

chiSquare += math.pow(observedValue - expectedValue, 2) / expectedValue

Together with the 'Degree of Freedom', which is (rows − 1) × (columns − 1) , the P-value can be calculated.

In this case it is P-value: 0.02462

A P-value lower than 0.05 is considered to be significant. Statistically, women tend to choose a romantic movie more, while men prefer a non-romantic one.

Users have the option to choose a P-value, calculated from a standard table or through a math.ucla.edu - Javascript-based function (see references below).

Note that the population (10 men + 10 women = 20) is small, something to consider.

Either way, this principle is applied in the script, where conditions can be chosen like rsi, close, high, ...

🔹 CONDITION

Conditions are added to the left column ('CONDITION')

For example, previous rsi values (rsi ) between 0-100, divided in separate groups

🔹 CLOSE

Then, the movement of the last close is evaluated

UP when close is higher then previous close (close )

DOWN when close is lower then previous close

EQUAL when close is equal then previous close

It is also possible to use only 2 columns by adding EQUAL to UP or DOWN

UP

DOWN/EQUAL

or

UP/EQUAL

DOWN

In other words, when previous rsi value was between 80 and 90, this resulted in:

19 times a current close higher than previous close

14 times a current close lower than previous close

0 times a current close equal than previous close

However, the P-value tells us it is not statistical significant.

NOTE: Always keep in mind that past behaviour gives no certainty about future behaviour.

A vertical line is drawn at the beginning of the chosen population (max 4990)

Here, the results seem significant.

🔹 GROUPS

It is important to ensure that the groups are formed correctly. All possibilities should be present, and conditions should only be part of 1 group.

In the example above, the two top situations are acceptable; close against close can only be higher, lower or equal.

The two examples at the bottom, however, are very poorly constructed.

Several conditions can be placed in more than 1 group, and some conditions are not integrated into a group. Even if the results are significant, they are useless because of the group formation.

A population count is added as an aid to spot errors in group formation.

In this example, there is a discrepancy between the population and total count due to the absence of a condition.

The results when rsi was between 5-25 are not included, resulting in unreliable results.

🔹 PRACTICAL EXAMPLES

In this example, we have specific groups where the condition only applies to that group.

For example, the condition rsi > 55 and rsi <= 65 isn't true in another group.

Also, every possible rsi value (0 - 100) is present in 1 of the groups.

rsi > 15 and rsi <= 25 28 times UP, 19 times DOWN and 2 times EQUAL. P-value: 0.01171

When looking in detail and examining the area 15-25 RSI, we see this:

The population is now not representative (only checking for RSI between 15-25; all other RSI values are not included), so we can ignore the P-value in this case. It is merely to check in detail. In this case, the RSI values 23 and 24 seem promising.

NOTE: We should check what the close price did without any condition.

If, for example, the close price had risen 100 times out of 100, this would make things very relative.

In this case (at least two conditions need to be present), we set 1 condition at 'always true' and another at 'always false' so we'll get only the close values without any condition:

Changing the population or the conditions will change the P-value.

In the following example, the outcome is evaluated when:

close value from 1 bar back is higher than the close value from 2 bars back

close value from 1 bar back is lower/equal than the close value from 2 bars back

Or:

close value from 1 bar back is higher than the close value from 2 bars back

close value from 1 bar back is equal than the close value from 2 bars back

close value from 1 bar back is lower than the close value from 2 bars back

In both examples, all possibilities of close against close are included in the calculations. close can only by higher, equal or lower than close

Both examples have the results without a condition included (5 = 5 and 5 < 5) so one can compare the direction of current close.

🔶 NOTES

• Always keep in mind that:

Past behaviour gives no certainty about future behaviour.

Everything depends on time, cycles, events, fundamentals, technicals, ...

• This test only works for categorical data (data in categories), such as Gender {Men, Women} or color {Red, Yellow, Green, Blue} etc., but not numerical data such as height or weight. One might argue that such tests shouldn't use rsi, close, ... values.

• Consider what you're measuring

For example rsi of the current bar will always lead to a close higher than the previous close, since this is inherent to the rsi calculations.

• Be careful; often, there are na -values at the beginning of the series, which are not included in the calculations!

• Always keep in mind considering what the close price did without any condition

• The numbers must be large enough. Each entry must be five or more. In other words, it is vital to make the 'population' large enough.

• The code can be developed further, for example, by splitting UP, DOWN in close UP 1-2%, close UP 2-3%, close UP 3-4%, ...

• rsi can be supplemented with stochRSI, MFI, sma, ema, ...

🔶 SETTINGS

🔹 Population

• Choose the population size; in other words, how many bars you want to go back to. If fewer bars are available than set, this will be automatically adjusted.

🔹 Inputs

At least two conditions need to be chosen.

• Users can add up to 11 conditions, where each condition can contain two different conditions.

🔹 RSI

• Length

🔹 Levels

• Set the used levels as desired.

🔹 Levels

• P-value: P-value retrieved using a standard table method or a function.

• Used function, derived from Chi-Square Distribution Function; JavaScript

LogGamma(Z) =>

S = 1

+ 76.18009173 / Z

- 86.50532033 / (Z+1)

+ 24.01409822 / (Z+2)

- 1.231739516 / (Z+3)

+ 0.00120858003 / (Z+4)

- 0.00000536382 / (Z+5)

(Z-.5) * math.log(Z+4.5) - (Z+4.5) + math.log(S * 2.50662827465)

Gcf(float X, A) => // Good for X > A +1

A0=0., B0=1., A1=1., B1=X, AOLD=0., N=0

while (math.abs((A1-AOLD)/A1) > .00001)

AOLD := A1

N += 1

A0 := A1+(N-A)*A0

B0 := B1+(N-A)*B0

A1 := X*A0+N*A1

B1 := X*B0+N*B1

A0 := A0/B1

B0 := B0/B1

A1 := A1/B1

B1 := 1

Prob = math.exp(A * math.log(X) - X - LogGamma(A)) * A1

1 - Prob

Gser(X, A) => // Good for X < A +1

T9 = 1. / A

G = T9

I = 1

while (T9 > G* 0.00001)

T9 := T9 * X / (A + I)

G := G + T9

I += 1

G *= math.exp(A * math.log(X) - X - LogGamma(A))

Gammacdf(x, a) =>

GI = 0.

if (x<=0)

GI := 0

else if (x

Chisqcdf = Gammacdf(Z/2, DF/2)

Chisqcdf := math.round(Chisqcdf * 100000) / 100000

pValue = 1 - Chisqcdf

🔶 REFERENCES

mathsisfun.com, Chi-Square Test

Chi-Square Distribution Function

Incomplete Session Candle - Incomplete Timeframe Candle Marker The "Incomplete Session Candle - Incomplete Timeframe Candle Marker" is an advanced tool tailored for technical analysts who understand the importance of accurate timeframes in their charting. While the indicator is not limited to the Indian market, its genesis is rooted in the nuances of trading sessions like those in India, which span 375 minutes from 9:15 AM to 3:30 PM.

Key Features:

Detects if the current timeframe is intraday (minutes or hours).

Calculates the expected duration of the candle for the chosen timeframe.

Highlights candles that don't achieve their expected session duration by placing a cross shape above the bar.

Compatible across various intraday timeframes, aiding traders in spotting discrepancies promptly.

Why We Made This: Not Just for India:

While we looked at the Indian market, this indicator works everywhere. Regular timeframes like 30 minutes, 1 hour, and 2 hours often end with incomplete candles, especially at the end of the trading day. For example:

A 30-minute timeframe makes 13 candles, but the last one is only 15 minutes long.

A 1-hour timeframe shows 7 candles, but the last one is just the last 15 minutes.

By switching to different timeframes like 25 minutes, 75 minutes, and 125 minutes, you get more complete information for better trading decisions. Learn more about this in our article: "Power of 25, 75, and 125-Minute Timeframes in the Indian Market", recognized by Trading View's Editors' Pick.

Benefits:

The indicator extends its benefits even to users without access to certain timeframes. It accommodates traders using a 1-hour timeframe (pertaining to Indian traders). By employing this indicator, traders consistently remain mindful of incomplete candles within their chosen timeframe

For those who utilize concepts like RBR, RBD, DBR, and DBD, this indicator is paramount. An incomplete candle can skew analysis, leading to potential misinterpretations of base or leg candles.

Final thoughts:

In markets like the Indian stock market, adopting such a tool is not just beneficial, but necessary. Whether you have access to unconventional timeframes or are using traditional ones, recognizing and accounting for the limitations of incomplete candles is critical & it's important to know if your candles fit the timeframe properly. This indicator gives you a better view of the market, which helps you make smarter trades.

Lastly, Thank you for your support! Your likes & comments. If you want to give any feedback then you can give in comment section.

Let's conquer the markets together!

Any Oscillator Underlay [TTF]We are proud to release a new indicator that has been a while in the making - the Any Oscillator Underlay (AOU) !

Note: There is a lot to discuss regarding this indicator, including its intent and some of how it operates, so please be sure to read this entire description before using this indicator to help ensure you understand both the intent and some limitations with this tool.

Our intent for building this indicator was to accomplish the following:

Combine all of the oscillators that we like to use into a single indicator

Take up a bit less screen space for the underlay indicators for strategies that utilize multiple oscillators

Provide a tool for newer traders to be able to leverage multiple oscillators in a single indicator

Features:

Includes 8 separate, fully-functional indicators combined into one

Ability to easily enable/disable and configure each included indicator independently

Clearly named plots to support user customization of color and styling, as well as manual creation of alerts

Ability to customize sub-indicator title position and color

Ability to customize sub-indicator divider lines style and color

Indicators that are included in this initial release:

TSI

2x RSIs (dubbed the Twin RSI )

Stochastic RSI

Stochastic

Ultimate Oscillator

Awesome Oscillator

MACD

Outback RSI (Color-coding only)

Quick note on OB/OS:

Before we get into covering each included indicator, we first need to cover a core concept for how we're defining OB and OS levels. To help illustrate this, we will use the TSI as an example.

The TSI by default has a mid-point of 0 and a range of -100 to 100. As a result, a common practice is to place lines on the -30 and +30 levels to represent OS and OB zones, respectively. Most people tend to view these levels as distance from the edges/outer bounds or as absolute levels, but we feel a more way to frame the OB/OS concept is to instead define it as distance ("offset") from the mid-line. In keeping with the -30 and +30 levels in our example, the offset in this case would be "30".

Taking this a step further, let's say we decided we wanted an offset of 25. Since the mid-point is 0, we'd then calculate the OB level as 0 + 25 (+25), and the OS level as 0 - 25 (-25).

Now that we've covered the concept of how we approach defining OB and OS levels (based on offset/distance from the mid-line), and since we did apply some transformations, rescaling, and/or repositioning to all of the indicators noted above, we are going to discuss each component indicator to detail both how it was modified from the original to fit the stacked-indicator model, as well as the various major components that the indicator contains.

TSI:

This indicator contains the following major elements:

TSI and TSI Signal Line

Color-coded fill for the TSI/TSI Signal lines

Moving Average for the TSI

TSI Histogram

Mid-line and OB/OS lines

Default TSI fill color coding:

Green : TSI is above the signal line

Red : TSI is below the signal line

Note: The TSI traditionally has a range of -100 to +100 with a mid-point of 0 (range of 200). To fit into our stacking model, we first shrunk the range to 100 (-50 to +50 - cut it in half), then repositioned it to have a mid-point of 50. Since this is the "bottom" of our indicator-stack, no additional repositioning is necessary.

Twin RSI:

This indicator contains the following major elements:

Fast RSI (useful if you want to leverage 2x RSIs as it makes it easier to see the overlaps and crosses - can be disabled if desired)

Slow RSI (primary RSI)

Color-coded fill for the Fast/Slow RSI lines (if Fast RSI is enabled and configured)

Moving Average for the Slow RSI

Mid-line and OB/OS lines

Default Twin RSI fill color coding:

Dark Red : Fast RSI below Slow RSI and Slow RSI below Slow RSI MA

Light Red : Fast RSI below Slow RSI and Slow RSI above Slow RSI MA

Dark Green : Fast RSI above Slow RSI and Slow RSI below Slow RSI MA

Light Green : Fast RSI above Slow RSI and Slow RSI above Slow RSI MA

Note: The RSI naturally has a range of 0 to 100 with a mid-point of 50, so no rescaling or transformation is done on this indicator. The only manipulation done is to properly position it in the indicator-stack based on which other indicators are also enabled.

Stochastic and Stochastic RSI:

These indicators contain the following major elements:

Configurable lengths for the RSI (for the Stochastic RSI only), K, and D values

Configurable base price source

Mid-line and OB/OS lines

Note: The Stochastic and Stochastic RSI both have a normal range of 0 to 100 with a mid-point of 50, so no rescaling or transformations are done on either of these indicators. The only manipulation done is to properly position it in the indicator-stack based on which other indicators are also enabled.

Ultimate Oscillator (UO):

This indicator contains the following major elements:

Configurable lengths for the Fast, Middle, and Slow BP/TR components

Mid-line and OB/OS lines

Moving Average for the UO

Color-coded fill for the UO/UO MA lines (if UO MA is enabled and configured)

Default UO fill color coding:

Green : UO is above the moving average line

Red : UO is below the moving average line

Note: The UO naturally has a range of 0 to 100 with a mid-point of 50, so no rescaling or transformation is done on this indicator. The only manipulation done is to properly position it in the indicator-stack based on which other indicators are also enabled.

Awesome Oscillator (AO):

This indicator contains the following major elements:

Configurable lengths for the Fast and Slow moving averages used in the AO calculation

Configurable price source for the moving averages used in the AO calculation

Mid-line

Option to display the AO as a line or pseudo-histogram

Moving Average for the AO

Color-coded fill for the AO/AO MA lines (if AO MA is enabled and configured)

Default AO fill color coding (Note: Fill was disabled in the image above to improve clarity):

Green : AO is above the moving average line

Red : AO is below the moving average line

Note: The AO is technically has an infinite (unbound) range - -∞ to ∞ - and the effective range is bound to the underlying security price (e.g. BTC will have a wider range than SP500, and SP500 will have a wider range than EUR/USD). We employed some special techniques to rescale this indicator into our desired range of 100 (-50 to 50), and then repositioned it to have a midpoint of 50 (range of 0 to 100) to meet the constraints of our stacking model. We then do one final repositioning to place it in the correct position the indicator-stack based on which other indicators are also enabled. For more details on how we accomplished this, read our section "Binding Infinity" below.

MACD:

This indicator contains the following major elements:

Configurable lengths for the Fast and Slow moving averages used in the MACD calculation

Configurable price source for the moving averages used in the MACD calculation

Configurable length and calculation method for the MACD Signal Line calculation

Mid-line

Note: Like the AO, the MACD also technically has an infinite (unbound) range. We employed the same principles here as we did with the AO to rescale and reposition this indicator as well. For more details on how we accomplished this, read our section "Binding Infinity" below.

Outback RSI (ORSI):

This is a stripped-down version of the Outback RSI indicator (linked above) that only includes the color-coding background (suffice it to say that it was not technically feasible to attempt to rescale the other components in a way that could consistently be clearly seen on-chart). As this component is a bit of a niche/special-purpose sub-indicator, it is disabled by default, and we suggest it remain disabled unless you have some pre-defined strategy that leverages the color-coding element of the Outback RSI that you wish to use.

Binding Infinity - How We Incorporated the AO and MACD (Warning - Math Talk Ahead!)

Note: This applies only to the AO and MACD at time of original publication. If any other indicators are added in the future that also fall into the category of "binding an infinite-range oscillator", we will make that clear in the release notes when that new addition is published.

To help set the stage for this discussion, it's important to note that the broader challenge of "equalizing inputs" is nothing new. In fact, it's a key element in many of the most popular fields of data science, such as AI and Machine Learning. They need to take a diverse set of inputs with a wide variety of ranges and seemingly-random inputs (referred to as "features"), and build a mathematical or computational model in order to work. But, when the raw inputs can vary significantly from one another, there is an inherent need to do some pre-processing to those inputs so that one doesn't overwhelm another simply due to the difference in raw values between them. This is where feature scaling comes into play.

With this in mind, we implemented 2 of the most common methods of Feature Scaling - Min-Max Normalization (which we call "Normalization" in our settings), and Z-Score Normalization (which we call "Standardization" in our settings). Let's take a look at each of those methods as they have been implemented in this script.

Min-Max Normalization (Normalization)

This is one of the most common - and most basic - methods of feature scaling. The basic formula is: y = (x - min)/(max - min) - where x is the current data sample, min is the lowest value in the dataset, and max is the highest value in the dataset. In this transformation, the max would evaluate to 1, and the min would evaluate to 0, and any value in between the min and the max would evaluate somewhere between 0 and 1.

The key benefits of this method are:

It can be used to transform datasets of any range into a new dataset with a consistent and known range (0 to 1).

It has no dependency on the "shape" of the raw input dataset (i.e. does not assume the input dataset can be approximated to a normal distribution).

But there are a couple of "gotchas" with this technique...

First, it assumes the input dataset is complete, or an accurate representation of the population via random sampling. While in most situations this is a valid assumption, in trading indicators we don't really have that luxury as we're often limited in what sample data we can access (i.e. number of historical bars available).

Second, this method is highly sensitive to outliers. Since the crux of this transformation is based on the max-min to define the initial range, a single significant outlier can result in skewing the post-transformation dataset (i.e. major price movement as a reaction to a significant news event).

You can potentially mitigate those 2 "gotchas" by using a mechanism or technique to find and discard outliers (e.g. calculate the mean and standard deviation of the input dataset and discard any raw values more than 5 standard deviations from the mean), but if your most recent datapoint is an "outlier" as defined by that algorithm, processing it using the "scrubbed" dataset would result in that new datapoint being outside the intended range of 0 to 1 (e.g. if the new datapoint is greater than the "scrubbed" max, it's post-transformation value would be greater than 1). Even though this is a bit of an edge-case scenario, it is still sure to happen in live markets processing live data, so it's not an ideal solution in our opinion (which is why we chose not to attempt to discard outliers in this manner).

Z-Score Normalization (Standardization)

This method of rescaling is a bit more complex than the Min-Max Normalization method noted above, but it is also a widely used process. The basic formula is: y = (x – μ) / σ - where x is the current data sample, μ is the mean (average) of the input dataset, and σ is the standard deviation of the input dataset. While this transformation still results in a technically-infinite possible range, the output of this transformation has a 2 very significant properties - the mean (average) of the output dataset has a mean (μ) of 0 and a standard deviation (σ) of 1.

The key benefits of this method are:

As it's based on normalizing the mean and standard deviation of the input dataset instead of a linear range conversion, it is far less susceptible to outliers significantly affecting the result (and in fact has the effect of "squishing" outliers).

It can be used to accurately transform disparate sets of data into a similar range regardless of the original dataset's raw/actual range.

But there are a couple of "gotchas" with this technique as well...

First, it still technically does not do any form of range-binding, so it is still technically unbounded (range -∞ to ∞ with a mid-point of 0).

Second, it implicitly assumes that the raw input dataset to be transformed is normally distributed, which won't always be the case in financial markets.

The first "gotcha" is a bit of an annoyance, but isn't a huge issue as we can apply principles of normal distribution to conceptually limit the range by defining a fixed number of standard deviations from the mean. While this doesn't totally solve the "infinite range" problem (a strong enough sudden move can still break out of our "conceptual range" boundaries), the amount of movement needed to achieve that kind of impact will generally be pretty rare.

The bigger challenge is how to deal with the assumption of the input dataset being normally distributed. While most financial markets (and indicators) do tend towards a normal distribution, they are almost never going to match that distribution exactly. So let's dig a bit deeper into distributions are defined and how things like trending markets can affect them.

Skew (skewness): This is a measure of asymmetry of the bell curve, or put another way, how and in what way the bell curve is disfigured when comparing the 2 halves. The easiest way to visualize this is to draw an imaginary vertical line through the apex of the bell curve, then fold the curve in half along that line. If both halves are exactly the same, the skew is 0 (no skew/perfectly symmetrical) - which is what a normal distribution has (skew = 0). Most financial markets tend to have short, medium, and long-term trends, and these trends will cause the distribution curve to skew in one direction or another. Bullish markets tend to skew to the right (positive), and bearish markets to the left (negative).

Kurtosis: This is a measure of the "tail size" of the bell curve. Another way to state this could be how "flat" or "steep" the bell-shape is. If the bell is steep with a strong drop from the apex (like a steep cliff), it has low kurtosis. If the bell has a shallow, more sweeping drop from the apex (like a tall hill), is has high kurtosis. Translating this to financial markets, kurtosis is generally a metric of volatility as the bell shape is largely defined by the strength and frequency of outliers. This is effectively a measure of volatility - volatile markets tend to have a high level of kurtosis (>3), and stable/consolidating markets tend to have a low level of kurtosis (<3). A normal distribution (our reference), has a kurtosis value of 3.

So to try and bring all that back together, here's a quick recap of the Standardization rescaling method:

The Standardization method has an assumption of a normal distribution of input data by using the mean (average) and standard deviation to handle the transformation

Most financial markets do NOT have a normal distribution (as discussed above), and will have varying degrees of skew and kurtosis

Q: Why are we still favoring the Standardization method over the Normalization method, and how are we accounting for the innate skew and/or kurtosis inherent in most financial markets?

A: Well, since we're only trying to rescale oscillators that by-definition have a midpoint of 0, kurtosis isn't a major concern beyond the affect it has on the post-transformation scaling (specifically, the number of standard deviations from the mean we need to include in our "artificially-bound" range definition).

Q: So that answers the question about kurtosis, but what about skew?

A: So - for skew, the answer is in the formula - specifically the mean (average) element. The standard mean calculation assumes a complete dataset and therefore uses a standard (i.e. simple) average, but we're limited by the data history available to us. So we adapted the transformation formula to leverage a moving average that included a weighting element to it so that it favored recent datapoints more heavily than older ones. By making the average component more adaptive, we gained the effect of reducing the skew element by having the average itself be more responsive to recent movements, which significantly reduces the effect historical outliers have on the dataset as a whole. While this is certainly not a perfect solution, we've found that it serves the purpose of rescaling the MACD and AO to a far more well-defined range while still preserving the oscillator behavior and mid-line exceptionally well.

The most difficult parts to compensate for are periods where markets have low volatility for an extended period of time - to the point where the oscillators are hovering around the 0/midline (in the case of the AO), or when the oscillator and signal lines converge and remain close to each other (in the case of the MACD). It's during these periods where even our best attempt at ensuring accurate mirrored-behavior when compared to the original can still occasionally lead or lag by a candle.

Note: If this is a make-or-break situation for you or your strategy, then we recommend you do not use any of the included indicators that leverage this kind of bounding technique (the AO and MACD at time of publication) and instead use the Trandingview built-in versions!

We know this is a lot to read and digest, so please take your time and feel free to ask questions - we will do our best to answer! And as always, constructive feedback is always welcome!

SUPERTREND MIXED ICHI-DMI-DONCHIAN-VOL-GAP-HLBox@RLSUPERTREND MIXED ICHI-DMI-VOL-GAP-HLBox@RL

by RegisL76

This script is based on several trend indicators.

* ICHIMOKU (KINKO HYO)

* DMI (Directional Movement Index)

* SUPERTREND ICHIMOKU + SUPERTREND DMI

* DONCHIAN CANAL Optimized with Colored Bars

* HMA Hull

* Fair Value GAP

* VOLUME/ MA Volume

* PRICE / MA Price

* HHLL BOXES

All these indications are visible simultaneously on a single graph. A data table summarizes all the important information to make a good trade decision.

ICHIMOKU Indicator:

The ICHIMOKU indicator is visualized in the traditional way.

ICHIMOKU standard setting values are respected but modifiable. (Traditional defaults = .

An oriented visual symbol, near the last value, indicates the progression (Ascending, Descending or neutral) of the TENKAN-SEN and the KIJUN-SEN as well as the period used.

The CLOUD (KUMO) and the CHIKOU-SPAN are present and are essential for the complete analysis of the ICHIMOKU.

At the top of the graph are visually represented the crossings of the TENKAN and the KIJUN.

Vertical lines, accompanied by labels, make it possible to quickly visualize the particularities of the ICHIMOKU.

A line displays the current bar.

A line visualizes the end of the CLOUD (KUMO) which is shifted 25 bars into the future.

A line visualizes the end of the chikou-span, which is shifted 25 bars in the past.

DIRECTIONAL MOVEMENT INDEX (DMI) : Treated conventionally : DI+, DI-, ADX and associated with a SUPERTREND DMI.

A visual symbol at the bottom of the graph indicates DI+ and DI- crossings

A line of oriented and colored symbols (DMI Line) at the top of the chart indicates the direction and strength of the trend.

SUPERTREND ICHIMOKU + SUPERTREND DMI :

Trend following by SUPERTREND calculation.

DONCHIAN CHANNEL: Treated conventionally. (And optimized by colored bars when overshooting either up or down.

The lines, high and low of the last values of the channel are represented to quickly visualize the level of the RANGE.

SUPERTREND HMA (HULL) Treated conventionally.

The HMA line visually indicates, according to color and direction, the market trend.

A visual symbol at the bottom of the chart indicates opportunities to sell and buy.

VOLUME:

Calculation of the MOBILE AVERAGE of the volume with comparison of the volume compared to the moving average of the volume.

The indications are colored and commented according to the comparison.

PRICE: Calculation of the MOBILE AVERAGE of the price with comparison of the price compared to the moving average of the price.

The indications are colored and commented according to the comparison.

HHLL BOXES:

Visualizes in the form of a box, for a given period, the max high and min low values of the price.

The configuration allows taking into account the high and low wicks of the price or the opening and closing values.

FAIR VALUE GAP :

This indicator displays 'GAP' levels over the current time period and an optional higher time period.

The script takes into account the high/low values of the current bar and compares with the 2 previous bars.

The "gap" is generated from the lack of overlap between these bars. Bearish or bullish gaps are determined by whether the gap is above or below HmaPrice, as they tend to fill, and can be used as targets.

NOTE: FAIR VALUE GAP has no values displayed in the table and/or label.

Important information (DATA) relating to each indicator is displayed in real time in a table and/or a label.

Each information is commented and colored according to direction, value, comparison etc.

Each piece of information indicates the values of the current bar and the previous value (in "FULL" mode).

The other possible modes for viewing the table and/or the label allow a more synthetic view of the information ("CONDENSED" and "MINIMAL" modes).

In order not to overload the vision of the chart too much, the visualization box of the RANGE DONCHIAN, the vertical lines of the shifted marks of the ICHIMOKU, as well as the boxes of the HHLL Boxes indicator are only visualized intermittently (managed by an adjustable time delay ).

The "HISTORICAL INFO READING" configuration parameter set to zero (by default) makes it possible to read all the information of the current bar in progress (Bar #0). All other values allow to read the information of a historical bar. The value 1 reads the information of the bar preceding the current bar (-1). The value 10 makes it possible to read the information of the tenth bar behind (-10) compared to the current bar, etc.

At the bottom of the DATAS table and label, lights, red, green or white indicate quickly summarize the trend from the various indicators.

Each light represents the number of indicators with the same trend at a given time.

Green for a bullish trend, red for a bearish trend and white for a neutral trend.

The conditions for determining a trend are for each indicator:

SUPERTREND ICHIMOHU + DMI: the 2 Super trends together are either bullish or bearish.

Otherwise the signal is neutral.

DMI: 2 main conditions:

BULLISH if DI+ >= DI- and ADX >25.

BEARISH if DI+ < DI- and ADX >25.

NEUTRAL if the 2 conditions are not met.

ICHIMOKU: 3 main conditions:

BULLISH if PRICE above the cloud and TENKAN > KIJUN and GREEN CLOUD AHEAD.

BEARISH if PRICE below the cloud and TENKAN < KIJUN and RED CLOUD AHEAD.

The other additional conditions (Data) complete the analysis and are present for informational purposes of the trend and depend on the context.

DONCHIAN CHANNEL: 1 main condition:

BULLISH: the price has crossed above the HIGH DC line.

BEARISH: the price has gone below the LOW DC line.

NEUTRAL if the price is between the HIGH DC and LOW DC lines

The 2 other complementary conditions (Datas) complete the analysis:

HIGH DC and LOW DC are increasing, falling or stable.

SUPERTREND HMA HULL: The script determines several trend levels:

STRONG BUY, BUY, STRONG SELL, SELL AND NEUTRAL.

VOLUME: 3 trend levels:

VOLUME > MOVING AVERAGE,

VOLUME < MOVING AVERAGE,

VOLUME = MOVING AVERAGE.

PRICE: 3 trend levels:

PRICE > MOVING AVERAGE,

PRICE < MOVING AVERAGE,

PRICE = MOVING AVERAGE.

If you are using this indicator/strategy and you are satisfied with the results, you can possibly make a donation (a coffee, a pizza or more...) via paypal to: lebourg.regis@free.fr.

Thanks in advance !!!

Have good winning Trades.

**************************************************************************************************************************

SUPERTREND MIXED ICHI-DMI-VOL-GAP-HLBox@RL

by RegisL76

Ce script est basé sur plusieurs indicateurs de tendance.

* ICHIMOKU (KINKO HYO)

* DMI (Directional Movement Index)

* SUPERTREND ICHIMOKU + SUPERTREND DMI

* DONCHIAN CANAL Optimized with Colored Bars

* HMA Hull

* Fair Value GAP

* VOLUME/ MA Volume

* PRIX / MA Prix

* HHLL BOXES

Toutes ces indications sont visibles simultanément sur un seul et même graphique.

Un tableau de données récapitule toutes les informations importantes pour prendre une bonne décision de Trade.

I- Indicateur ICHIMOKU :

L’indicateur ICHIMOKU est visualisé de manière traditionnelle

Les valeurs de réglage standard ICHIMOKU sont respectées mais modifiables. (Valeurs traditionnelles par défaut =

Un symbole visuel orienté, à proximité de la dernière valeur, indique la progression (Montant, Descendant ou neutre) de la TENKAN-SEN et de la KIJUN-SEN ainsi que la période utilisée.

Le NUAGE (KUMO) et la CHIKOU-SPAN sont bien présents et sont primordiaux pour l'analyse complète de l'ICHIMOKU.

En haut du graphique sont représentés visuellement les croisements de la TENKAN et de la KIJUN.

Des lignes verticales, accompagnées d'étiquettes, permettent de visualiser rapidement les particularités de l'ICHIMOKU.

Une ligne visualise la barre en cours.

Une ligne visualise l'extrémité du NUAGE (KUMO) qui est décalé de 25 barres dans le futur.

Une ligne visualise l'extrémité de la chikou-span, qui est décalée de 25 barres dans le passé.

II-DIRECTIONAL MOVEMENT INDEX (DMI)

Traité de manière conventionnelle : DI+, DI-, ADX et associé à un SUPERTREND DMI

Un symbole visuel en bas du graphique indique les croisements DI+ et DI-

Une ligne de symboles orientés et colorés (DMI Line) en haut du graphique, indique la direction et la puissance de la tendance.

III SUPERTREND ICHIMOKU + SUPERTREND DMI

Suivi de tendance par calcul SUPERTREND

IV- DONCHIAN CANAL :

Traité de manière conventionnelle.

(Et optimisé par des barres colorées en cas de dépassement soit vers le haut, soit vers le bas.

Les lignes, haute et basse des dernières valeurs du canal sont représentées pour visualiser rapidement la fourchette du RANGE.

V- SUPERTREND HMA (HULL)

Traité de manière conventionnelle.

La ligne HMA indique visuellement, selon la couleur et l'orientation, la tendance du marché.

Un symbole visuel en bas du graphique indique les opportunités de vente et d'achat.

*VI VOLUME :

Calcul de la MOYENNE MOBILE du volume avec comparaison du volume par rapport à la moyenne mobile du volume.

Les indications sont colorées et commentées en fonction de la comparaison.

*VII PRIX :

Calcul de la MOYENNE MOBILE du prix avec comparaison du prix par rapport à la moyenne mobile du prix.

Les indications sont colorées et commentées en fonction de la comparaison.

*VIII HHLL BOXES :

Visualise sous forme de boite, pour une période donnée, les valeurs max hautes et min basses du prix.

La configuration permet de prendre en compte les mèches hautes et basses du prix ou bien les valeurs d'ouverture et de fermeture.

IX - FAIR VALUE GAP

Cet indicateur affiche les niveaux de 'GAP' sur la période temporelle actuelle ET une période temporelle facultative supérieure.

Le script prend en compte les valeurs haut/bas de la barre actuelle et compare avec les 2 barres précédentes.

Le "gap" est généré à partir du manque de recouvrement entre ces barres.

Les écarts baissiers ou haussiers sont déterminés selon que l'écart est supérieurs ou inférieur à HmaPrice, car ils ont tendance à être comblés, et peuvent être utilisés comme cibles.

NOTA : FAIR VALUE GAP n'a pas de valeurs affichées dans la table et/ou l'étiquette.

Les informations importantes (DATAS) relatives à chaque indicateur sont visualisées en temps réel dans une table et/ou une étiquette.

Chaque information est commentée et colorée en fonction de la direction, de la valeur, de la comparaison etc.

Chaque information indique la valeurs de la barre en cours et la valeur précédente ( en mode "COMPLET").

Les autres modes possibles pour visualiser la table et/ou l'étiquette, permettent une vue plus synthétique des informations (modes "CONDENSÉ" et "MINIMAL").

Afin de ne pas trop surcharger la vision du graphique, la boite de visualisation du RANGE DONCHIAN, les lignes verticales des marques décalées de l'ICHIMOKU, ainsi que les boites de l'indicateur HHLL Boxes ne sont visualisées que de manière intermittente (géré par une temporisation réglable ).

Le paramètre de configuration "HISTORICAL INFO READING" réglé sur zéro (par défaut) permet de lire toutes les informations de la barre actuelle en cours (Barre #0).

Toutes autres valeurs permet de lire les informations d'une barre historique. La valeur 1 permet de lire les informations de la barre précédant la barre en cours (-1).

La valeur 10 permet de lire les information de la dixième barre en arrière (-10) par rapport à la barre en cours, etc.

Dans le bas de la table et de l'étiquette de DATAS, des voyants, rouge, vert ou blanc indique de manière rapide la synthèse de la tendance issue des différents indicateurs.

Chaque voyant représente le nombre d'indicateur ayant la même tendance à un instant donné. Vert pour une tendance Bullish, rouge pour une tendance Bearish et blanc pour une tendance neutre.

Les conditions pour déterminer une tendance sont pour chaque indicateur :

SUPERTREND ICHIMOHU + DMI : les 2 Super trends sont ensemble soit bullish soit Bearish. Sinon le signal est neutre.

DMI : 2 conditions principales :

BULLISH si DI+ >= DI- et ADX >25.

BEARISH si DI+ < DI- et ADX >25.

NEUTRE si les 2 conditions ne sont pas remplies.

ICHIMOKU : 3 conditions principales :

BULLISH si PRIX au dessus du nuage et TENKAN > KIJUN et NUAGE VERT DEVANT.

BEARISH si PRIX en dessous du nuage et TENKAN < KIJUN et NUAGE ROUGE DEVANT.

Les autres conditions complémentaires (Datas) complètent l'analyse et sont présents à titre informatif de la tendance et dépendent du contexte.

CANAL DONCHIAN : 1 condition principale :

BULLISH : le prix est passé au dessus de la ligne HIGH DC.

BEARISH : le prix est passé au dessous de la ligne LOW DC.

NEUTRE si le prix se situe entre les lignes HIGH DC et LOW DC

Les 2 autres conditions complémentaires (Datas) complètent l'analyse : HIGH DC et LOW DC sont croissants, descendants ou stables.

SUPERTREND HMA HULL :

Le script détermine plusieurs niveaux de tendance :

STRONG BUY, BUY, STRONG SELL, SELL ET NEUTRE.

VOLUME : 3 niveaux de tendance :

VOLUME > MOYENNE MOBILE, VOLUME < MOYENNE MOBILE, VOLUME = MOYENNE MOBILE.

PRIX : 3 niveaux de tendance :

PRIX > MOYENNE MOBILE, PRIX < MOYENNE MOBILE, PRIX = MOYENNE MOBILE.

Si vous utilisez cet indicateur/ stratégie et que vous êtes satisfait des résultats,

vous pouvez éventuellement me faire un don (un café, une pizza ou plus ...) via paypal à : lebourg.regis@free.fr.

Merci d'avance !!!

Ayez de bons Trades gagnants.

StableF-MainIt is combination of Built in Super trend and Adx with take profit

uptrend is considered when +dmi is above -dmi and +dmi is above 25 and adx is above 25 and supertrend gives Buy

downtrend is considered when -dmi is above +dmi and -dmi is above 25 and adx is above 25 and supertrend give sell

use fibo for target by taking as previous swing high and swing low

-supertrend crossover is referred as buy plotshape

-supertrend cross under is referred as Sell plotshape

-keep stoploss at dot line of supertrend

-adx-dmi crossover (+dmi crossed above -dmi) is shown by Triangle Up symbol

-adx-dmi crossunder( -dmi crosses below +dmi) is shown by Triangle down symbol

--Cross symbol with blue line with linewidth 2 is referred as Take profit

--combine this with adx -dmi setting with 7 and 14

----disclaimer-----

used free built in supertrend and adx so u can use same setting in other broker or in trading view

not responsible for any loss or gain

-only for educational purpose

Market Traffic Light (redesigned)redesigned the market traffic light from funcharts, all honor to him, I just put a new design ;-) and some bugfixes

1. Section (Fear & Greed)

Approximation of the CNN Money Fear & Greed index based on code of user MagicEins. The index shows values between 0 (extreme fear, red) and 100 (extreme greed, green).

2. Section (warning signs)

VIX: Values above 20 are red and below green. The legend shows the value of the current bar including the change from the bar before. The average VIX is about 16. Values over 20 are a sign of stressed market.

Distribution days: A distribution day (loss to the day before > 0,2 % and higher volume ) is marked with a yellow dot. In case there are more than four distributions days within 25 markets days the dot is orange. When big players redistribute their investments distribution days can occur. If this is done often (more than four times within 25 market days) it is possible that the markets changes or that a sector rotation occurs. For calculation distribution days futures of S&P 500 ( ES1! ) and NASDAQ ( NQ1! ) are used because the volume for this calculation is needed. TradingView does not support volumes for S&P 500 or NASDAQ directly.

Markets: A green/red dot signals that the market is above/below its 25-Daily-EMA. A green/red square signals that the market is above/below its 25-Weekly-EMA. Markets can give as a feeling about where investors store their money. E.g. when markets are falling but DUX (Down Jones Utility Average) is rising this means that investors put their money into save haven. This can be a sign that the markets will fall more.

3. Section (panic signs, = signs of reaching a low within a correction of a crash)

VIX-Reversion: A VIX reversion day ( VIX > 20 & VIX high > VIX high of the day before & VIX high – VIX close > 3) is marked as a yellow dot

VVIX: A value equal or above 140 is marked with a yellow dot and shows absolute panic.

PCR Intra max: A value equal or above 1.4 is marked with a yellow dot.

New high/lows: New highs/lows are shown for AMEX, NYSE and NASDAQ. A yellow dot is shown if the ratio is less or equal than 0. 01 .

Down-Day: Down days are shown for AMEX, NYSE and NASDA. A yellow dot is shown if at least 90 % of the whole volume (up and down) is a down volume .

In Addition to the warning signs in the second section a check of the Advance Decline Line (NYSE and NASDAQ) for bullish and bearish divergences is useful. The whole set-up can be seen in the screenshot.

Only one signal normally does not give us a good prediction. Therefore we need to see these indication as a bundle. TradingView gives us the opportunity to check some striking market situations in the past. So feel free to test this indication for building up your own opinion.

Please feel free to comment in case of failures, improvements or experiences (good or bad).

ADX / RSI Strategy by Trade Rush (created by SirPoggy) This is one of many new strategies coming soon which were seen on Trade Rush

This one is the ADX / RSI Strategy seen here:

https:www.youtube.com/watch?v=uSkGE0ujyn4

While the strategy has been modified slightly to use the DMI instead of the ADX, the core of the strategy is essentially the same

Long signals are generated when the RSI is above 70, close is above the 200EMA, and the ADX is above 25 (added is the plus DMI over 25 and minus DMI below 20)

Stop loss is placed below /above the 21 EMA, however, there is a deviation required to ensure price is not too close to where a stop loss would be placed.

Short signals are generated when the RSI is below 30, close is below the 200EMA, and the ADX is above 25 (added is the minus DMI over 25 and plus DMI below 20)

I do not recommend using this strategy but I have provided this code for educational purposes.

Thanks!

Let me know which strategy you'd like coded next in the comments below.

[kai]Futility RatioAn indicator that measures movement inefficiency

Inefficient movement, that is, the range market becomes a high number, the limit is reached at about 60 and a trend occurs

When the range breaks and a trend occurs, the inefficiency drops to about 40 and many trends end.

The full-scale trend goes down further and goes down to about 25, which is evaluated as an efficient movement, the limit is reached and the trend ends.

As for how to use this Inge, the direction of the trend needs to be considered in other ways.

Create a position when you reach 60

Position closed or contrarian at 40 or 25

I assume the usage

動きの非効率性を測定するインジケーターです

非効率な動きをするつまりレンジ相場は高い数字になって、60程度で限界が訪れてトレンドが発生します

レンジがブレイクしトレンドが発生すると40程度まで非効率性は下がりって多くのトレンドは終了します

本格的なトレンドはさらに下がっていって効率的な動きと評価される25程度まで下がって限界が訪れてトレンドが終了します

このインジの使い方はトレンドの方向は他の方法で考える必要がありますが

60まで上がったときにポジション作成

40又は25でポジションクローズ又は逆張り

という使い方を想定しています

Market Traffic LightThis indicator visualizes warning and panic signs, which are shown separately.

1. Section (Fear & Greed)

Approximation of the CNN Money Fear & Greed index based on code of user MagicEins. The index shows values between 0 (extreme fear, red) and 100 (extreme greed, green).

2. Section (warning signs)

VIX: Values above 20 are red and below green. The legend shows the value of the current bar including the change from the bar before. The average VIX is about 16. Values over 20 are a sign of stressed market.

Distribution days: A distribution day (loss to the day before > 0,2 % and higher volume) is marked with a yellow dot. In case there are more than four distributions days within 25 markets days the dot is orange. When big players redistribute their investments distribution days can occur. If this is done often (more than four times within 25 market days) it is possible that the markets changes or that a sector rotation occurs. For calculation distribution days futures of S&P 500 (ES1!) and NASDAQ (NQ1!) are used because the volume for this calculation is needed. TradingView does not support volumes for S&P 500 or NASDAQ directly.

Markets: A green/red dot signals that the market is above/below its 25-Daily-EMA. A green/red square signals that the market is above/below its 25-Weekly-EMA. Markets can give as a feeling about where investors store their money. E.g. when markets are falling but DUX (Down Jones Utility Average) is rising this means that investors put their money into save haven. This can be a sign that the markets will fall more.

3. Section (panic signs, = signs of reaching a low within a correction of a crash)

VIX-Reversion: A VIX reversion day (VIX > 20 & VIX high > VIX high of the day before & VIX high – VIX close > 3) is marked as a yellow dot

VVIX: A value equal or above 140 is marked with a yellow dot and shows absolute panic.

PCR Intra max: A value equal or above 1.4 is marked with a yellow dot.

New high/lows: New highs/lows are shown for AMEX, NYSE and NASDAQ. A yellow dot is shown if the ratio is less or equal than 0.01.

Down-Day: Down days are shown for AMEX, NYSE and NASDA. A yellow dot is shown if at least 90 % of the whole volume (up and down) is a down volume.

In Addition to the warning signs in the second section a check of the Advance Decline Line (NYSE and NASDAQ) for bullish and bearish divergences is useful. The whole set-up can be seen in the screenshot.

Only one signal normally does not give us a good prediction. Therefore we need to see these indication as a bundle. TradingView gives us the opportunity to check some striking market situations in the past. So feel free to test this indication for building up your own opinion.

Please feel free to comment in case of failures, improvements or experiences (good or bad).

Adaptive Trend Navigator [ATH Filter & Risk Engine]Description:

This strategy implements a systematic Trend Following approach designed to capture major moves while actively protecting capital during severe bear markets. It combines a classic Moving Average "Fan" logic with two advanced risk management layers: a 4-Stage Dynamic Stop Loss and a macro-economic "Circuit Breaker" filter.

Core Concepts:

1. Trend Identification (Entry Logic) The script uses a cascade of Simple Moving Averages (SMA 25, 50, 100, 200) to identify the maturity of a trend.

Entries are triggered by specific crossovers (e.g., SMA 25 crossing SMA 50) or by breaking above the previous trade's high ("High-Water Mark" Re-Entry).

2. The "Circuit Breaker" (Crash Protection) To prevent trading during historical market collapses (like 2000 or 2008), the strategy monitors the Nasdaq 100 (QQQ) as a global benchmark:

Normal Regime: If the market is within 20% of its All-Time High, the strategy operates normally.

Crisis Regime: If the QQQ falls more than 20% from its ATH, the "Circuit Breaker" activates (Visualized by a Red Background).

Recovery Rule: In a Crisis Regime, new long positions are blocked unless the QQQ reclaims its SMA 200. This filters out "bull traps" in secular bear markets.

3. 4-Stage Risk Engine (Exit Logic) Once in a trade, the risk management adapts to the position's performance:

Stage 1: Fixed initial Stop Loss (default 10%) for breathing room.

Stage 2: Moves to Break-Even area once the price rises 12%.

Stage 3: Tightens to a trailing stop (8%) after 25% profit.

Stage 4: Maximizes gains with a tight trailing stop (5%) during parabolic moves (>40% profit).

Visual Guide:

SMAs: 25/50/100/200 period lines for trend visualization.

Red Background: Indicates the "Crisis Regime" where trading is halted due to broad market weakness.

Blue Background: Indicates a "Recovery Phase" (Crisis is active, but market is above SMA 200).

Red Line: Shows the dynamic Stop Loss level for active positions.

Settings: All parameters (SMA lengths, Drawdown threshold, Risk Stages) are fully customizable. The QQQ benchmark ticker can also be changed to SPY or other indices depending on the asset class traded.

Dynamic Ratchet Trend Strategy [VIX Filter]Overview This strategy is a long-only trend-following system designed to capture major market moves while strictly managing downside risk through a state-machine based "Ratchet" exit logic. It incorporates a volatility filter using the CBOE VIX index to stay out of (or exit) the market during high-stress environments.

Key Features

1. Multi-Condition Entries The strategy looks for momentum shifts and trend breakouts using four Simple Moving Averages (25, 50, 100, 200).

Momentum Cross: SMA 25 crossover above SMA 50.

Trend Breakouts: A specific "3-Bar Breakout" logic above the SMA 50, 100, or 200. This requires the price to hold above the SMA for 3 consecutive bars after being below it, reducing false signals compared to simple closes.

2. VIX Volatility Filter Before entering any trade, the script checks the CBOE:VIX.

Filter: If VIX is above the threshold (default 32), new entries are blocked.

Panic Exit: If you are in a position and the VIX spikes above the threshold, the strategy executes an immediate "Panic Exit" to preserve capital during market crashes.

3. The "Ratchet" Exit System (3 Stages) Unlike a standard trailing stop, this strategy uses a 3-stage dynamic exit mechanism that tightens as profits grow:

Stage 0 (Initial Risk): Standard percentage-based Stop Loss from the entry price.

Stage 1 (The Lock-In): Triggered when profit hits 10% (configurable).

Unique Logic: Instead of trailing from the highest high, the stop is calculated based on the price at the exact moment this stage was triggered. It "steps up" once and holds, securing the initial move without being prematurely stopped out by normal volatility.

Stage 2 (Trailing Mode): Triggered when profit hits 15% (configurable).

The strategy switches to a classic Trailing Stop, following the percentage distance from the Highest High.

4. Emergency Backup A "Dead Cross" (SMA 25 crossing under SMA 50) acts as a final fail-safe to close positions if the trend reverses completely before hitting a stop.

Settings & Inputs

SMAs: Customize the lengths for all four moving averages.

VIX Filter: Toggle the filter on/off and set the panic threshold.

Exit Logic: Fully customizable percentages for Initial SL, Stage 1 Trigger/Distance, and Stage 2 Trigger/Trailing Distance.

Disclaimer This script is for educational purposes only. Past performance is not indicative of future results. Always manage your risk appropriately.

لbsm15// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) creativecommons.org

// © LuxAlgo

//@version=5

indicator("لbsm15", overlay = true, max_lines_count = 500, max_boxes_count = 500, max_bars_back = 3000)

//------------------------------------------------------------------------------

//Settings

//-----------------------------------------------------------------------------{

liqGrp = 'Liquidity Detection'

liqLen = input.int (7, title = 'Detection Length', minval = 3, maxval = 13, inline = 'LIQ', group = liqGrp)

liqMar = 10 / input.float (6.9, 'Margin', minval = 4, maxval = 9, step = 0.1, inline = 'LIQ', group = liqGrp)

liqBuy = input.bool (true, 'Buyside Liquidity Zones, Margin', inline = 'Buyside', group = liqGrp)

marBuy = input.float(2.3, '', minval = 1.5, maxval = 10, step = .1, inline = 'Buyside', group = liqGrp)

cLIQ_B = input.color (color.new(#4caf50, 0), '', inline = 'Buyside', group = liqGrp)

liqSel = input.bool (true, 'Sellside Liquidity Zones, Margin', inline = 'Sellside', group = liqGrp)

marSel = input.float(2.3, '', minval = 1.5, maxval = 10, step = .1, inline = 'Sellside', group = liqGrp)

cLIQ_S = input.color (color.new(#f23645, 0), '', inline = 'Sellside', group = liqGrp)

lqVoid = input.bool (false, 'Liquidity Voids, Bullish', inline = 'void', group = liqGrp)

cLQV_B = input.color (color.new(#4caf50, 0), '', inline = 'void', group = liqGrp)

cLQV_S = input.color (color.new(#f23645, 0), 'Bearish', inline = 'void', group = liqGrp)

lqText = input.bool (false, 'Label', inline = 'void', group = liqGrp)

mode = input.string('Present', title = 'Mode', options = , inline = 'MOD', group = liqGrp)

visLiq = input.int (3, ' # Visible Levels', minval = 1, maxval = 50, inline = 'MOD', group = liqGrp)

//-----------------------------------------------------------------------------}

//General Calculations

//-----------------------------------------------------------------------------{

maxSize = 50

atr = ta.atr(10)

atr200 = ta.atr(200)

per = mode == 'Present' ? last_bar_index - bar_index <= 500 : true

//-----------------------------------------------------------------------------}

//User Defined Types

//-----------------------------------------------------------------------------{

// @type used to store pivot high/low data

//

// @field d (array) The array where the trend direction is to be maintained

// @field x (array) The array where the bar index value of pivot high/low is to be maintained

// @field y (array) The array where the price value of pivot high/low is to be maintained

type ZZ

int d

int x

float y

// @type bar properties with their values

//

// @field o (float) open price of the bar

// @field h (float) high price of the bar

// @field l (float) low price of the bar

// @field c (float) close price of the bar

// @field i (int) index of the bar

type bar

float o = open

float h = high

float l = low

float c = close

int i = bar_index

// @type liquidity object definition

//

// @field bx (box) box maitaing the liquity level margin extreme levels

// @field bxz (box) box maitaing the liquity zone margin extreme levels

// @field bxt (box) box maitaing the labels

// @field brZ (bool) mainains broken zone status

// @field brL (bool) mainains broken level status

// @field ln (line) maitaing the liquity level line

// @field lne (line) maitaing the liquity extended level line

type liq

box bx

box bxz

box bxt

bool brZ

bool brL

line ln

line lne

//-----------------------------------------------------------------------------}

//Variables

//-----------------------------------------------------------------------------{

var ZZ aZZ = ZZ.new(

array.new (maxSize, 0),

array.new (maxSize, 0),

array.new (maxSize, na)

)

bar b = bar.new()

var liq b_liq_B = array.new (1, liq.new(box(na), box(na), box(na), false, false, line(na), line(na)))

var liq b_liq_S = array.new (1, liq.new(box(na), box(na), box(na), false, false, line(na), line(na)))

var b_liq_V = array.new_box()

var int dir = na, var int x1 = na, var float y1 = na, var int x2 = na, var float y2 = na

//-----------------------------------------------------------------------------}

//Functions/methods

//-----------------------------------------------------------------------------{

// @function maintains arrays

// it prepends a `value` to the arrays and removes their oldest element at last position

// @param aZZ (UDT, array, array>) The UDT obejct of arrays

// @param _d (array) The array where the trend direction is maintained

// @param _x (array) The array where the bar index value of pivot high/low is maintained

// @param _y (array) The array where the price value of pivot high/low is maintained

//

// @returns none

method in_out(ZZ aZZ, int _d, int _x, float _y) =>

aZZ.d.unshift(_d), aZZ.x.unshift(_x), aZZ.y.unshift(_y), aZZ.d.pop(), aZZ.x.pop(), aZZ.y.pop()

// @function (build-in) sets the maximum number of bars that is available for historical reference

max_bars_back(time, 1000)

//-----------------------------------------------------------------------------}

//Calculations

//-----------------------------------------------------------------------------{

x2 := b.i - 1

ph = ta.pivothigh(liqLen, 1)

pl = ta.pivotlow (liqLen, 1)

if ph

dir := aZZ.d.get(0)

x1 := aZZ.x.get(0)

y1 := aZZ.y.get(0)

y2 := nz(b.h )

if dir < 1

aZZ.in_out(1, x2, y2)

else

if dir == 1 and ph > y1

aZZ.x.set(0, x2), aZZ.y.set(0, y2)

if per

count = 0

st_P = 0.

st_B = 0

minP = 0.

maxP = 10e6

for i = 0 to maxSize - 1

if aZZ.d.get(i) == 1

if aZZ.y.get(i) > ph + (atr / liqMar)

break

else

if aZZ.y.get(i) > ph - (atr / liqMar) and aZZ.y.get(i) < ph + (atr / liqMar)

count += 1

st_B := aZZ.x.get(i)

st_P := aZZ.y.get(i)

if aZZ.y.get(i) > minP

minP := aZZ.y.get(i)

if aZZ.y.get(i) < maxP

maxP := aZZ.y.get(i)

if count > 2

getB = b_liq_B.get(0)

if st_B == getB.bx.get_left()

getB.bx.set_top(math.avg(minP, maxP) + (atr / liqMar))

getB.bx.set_rightbottom(b.i + 10, math.avg(minP, maxP) - (atr / liqMar))

else

b_liq_B.unshift(

liq.new(

box.new(st_B, math.avg(minP, maxP) + (atr / liqMar), b.i + 10, math.avg(minP, maxP) - (atr / liqMar), bgcolor=color(na), border_color=color(na)),

box.new(na, na, na, na, bgcolor = color(na), border_color = color(na)),

box.new(st_B, st_P, b.i + 10, st_P, text = 'Buyside liquidity', text_size = size.tiny, text_halign = text.align_left, text_valign = text.align_bottom, text_color = color.new(cLIQ_B, 25), bgcolor = color(na), border_color = color(na)),

false,

false,

line.new(st_B , st_P, b.i - 1, st_P, color = color.new(cLIQ_B, 0)),

line.new(b.i - 1, st_P, na , st_P, color = color.new(cLIQ_B, 0), style = line.style_dotted))

)

alert('buyside liquidity level detected/updated for ' + syminfo.ticker)

if b_liq_B.size() > visLiq

getLast = b_liq_B.pop()

getLast.bx.delete()

getLast.bxz.delete()

getLast.bxt.delete()

getLast.ln.delete()

getLast.lne.delete()

if pl

dir := aZZ.d.get (0)

x1 := aZZ.x.get (0)

y1 := aZZ.y.get (0)

y2 := nz(b.l )

if dir > -1

aZZ.in_out(-1, x2, y2)

else

if dir == -1 and pl < y1

aZZ.x.set(0, x2), aZZ.y.set(0, y2)

if per

count = 0

st_P = 0.

st_B = 0

minP = 0.

maxP = 10e6

for i = 0 to maxSize - 1

if aZZ.d.get(i) == -1

if aZZ.y.get(i) < pl - (atr / liqMar)

break

else

if aZZ.y.get(i) > pl - (atr / liqMar) and aZZ.y.get(i) < pl + (atr / liqMar)

count += 1

st_B := aZZ.x.get(i)

st_P := aZZ.y.get(i)

if aZZ.y.get(i) > minP

minP := aZZ.y.get(i)

if aZZ.y.get(i) < maxP

maxP := aZZ.y.get(i)

if count > 2

getB = b_liq_S.get(0)

if st_B == getB.bx.get_left()

getB.bx.set_top(math.avg(minP, maxP) + (atr / liqMar))