Cointegration Buy and Sell Signals [EdgeTerminal]The Cointegration Buy And Sell Signals is a sophisticated technical analysis tool to spot high-probability market turning points — before they fully develop on price charts.

Most reversal indicators rely on raw price action, visual patterns, or basic and common indicator logic — which often suffer in noisy or trending markets. In most cases, they lag behind the actual change in trend and provide useless and late signals.

This indicator is rooted in advanced concepts from statistical arbitrage, mean reversion theory, and quantitative finance, and it packages these ideas in a user-friendly visual format that works on any timeframe and asset class.

It does this by analyzing how the short-term and long-term EMAs behave relative to each other — and uses statistical filters like Z-score, correlation, volatility normalization, and stationarity tests to issue highly selective Buy and Sell signals.

This tool provides statistical confirmation of trend exhaustion, allowing you to trade mean-reverting setups. It fades overextended moves and uses signal stacking to reduce false entries. The entire indicator is based on a very interesting mathematically grounded model which I will get into down below.

Here’s how the indicator works at a high level:

EMAs as Anchors: It starts with two Exponential Moving Averages (EMAs) — one short-term and one long-term — to track market direction.

Statistical Spread (Regression Residuals): It performs a rolling linear regression between the short and long EMA. Instead of using the raw difference (short - long), it calculates the regression residual, which better models their natural relationship.

Normalize the Spread: The spread is divided by historical price volatility (ATR) to make it scale-invariant. This ensures the indicator works on low-priced stocks, high-priced indices, and crypto alike.

Z-Score: It computes a Z-score of the normalized spread to measure how “extreme” the current deviation is from its historical average.

Dynamic Thresholds: Unlike most tools that use fixed thresholds (like Z = ±2), this one calculates dynamic thresholds using historical percentiles (e.g., top 10% and bottom 10%) so that it adapts to the asset's current behavior to reduce false signals based on market’s extreme volatility at a certain time.

Z-Score Momentum: It tracks the direction of the Z-score — if Z is extreme but still moving away from zero, it's too early. It waits for reversion to start (Z momentum flips).

Correlation Check: Uses a rolling Pearson correlation to confirm the two EMAs are still statistically related. If they diverge (low correlation), no signal is shown.

Stationarity Filter (ADF-like): Uses the volatility of the regression residual to determine if the spread is stationary (mean-reverting) — a key concept in cointegration and statistical arbitrage. It’s not possible to build an exact ADF filter in Pine Script so we used the next best thing.

Signal Control: Prevents noisy charts and overtrading by ensuring no back-to-back buy or sell signals. Each signal must alternate and respect a cooldown period so you won’t be overwhelmed and won’t get a messy chart.

Important Notes to Remember:

The whole idea behind this indicator is to try to use some stat arb models to detect shifting patterns faster than they appear on common indicators, so in some cases, some assumptions are made based on historic values.

This means that in some cases, the indicator can “jump” into the conclusion too quickly. Although we try to eliminate this by using stationary filters, correlation checks, and Z-score momentum detection, there is still a chance some signals that are generated can be too early, in the stock market, that's the same as being incorrect. So make sure to use this with other indicators to confirm the movement.

How To Use The Indicator:

You can use the indicator as a standalone reversal system, as a filter for overbought and oversold setups, in combination with other trend indicators and as a part of a signal stack with other common indicators for divergence spotting and fade trades.

The indicator produces simple buy and sell signals when all criteria is met. Based on our own testing, we recommend treating these signals as standalone and independent from each other . Meaning that if you take position after a buy signal, don’t wait for a sell signal to appear to exit the trade and vice versa.

This is why we recommend using this indicator with other advanced or even simple indicators as an early confirmation tool.

The Display Table:

The floating diagnostic table in the top-right corner of the chart is a key part of this indicator. It's a live statistical dashboard that helps you understand why a signal is (or isn’t) being triggered, and whether the market conditions are lining up for a potential reversal.

1. Z-Score

What it shows: The current Z-score value of the volatility-normalized spread between the short EMA and the regression line of the long EMA.

Why it matters: Z-score tells you how statistically extreme the current relationship is. A Z-score of:

0 = perfectly average

> +2 = very overbought

< -2 = very oversold

How to use it: Look for Z-score reaching extreme highs or lows (beyond dynamic thresholds). Watch for it to start reversing direction, especially when paired with green table rows (see below)

2. Z-Score Momentum

What it shows: The rate of change (ROC) of the Z-score:

Zmomentum=Zt − Zt − 1

Why it matters: This tells you if the Z-score is still stretching out (e.g., getting more overbought/oversold), or reverting back toward the mean.

How to use it: A positive Z-momentum after a very low Z-score = potential bullish reversal A negative Z-momentum after a very high Z-score = potential bearish reversal. Avoid signals when momentum is still pushing deeper into extremes

3. Correlation

What it shows: The rolling Pearson correlation coefficient between the short EMA and long EMA.

Why it matters: High correlation (closer to +1) means the EMAs are still statistically connected — a key requirement for cointegration or mean reversion to be valid.

How to use it: Look for correlation > 0.7 for reliable signals. If correlation drops below 0.5, ignore the Z-score — the EMAs aren’t moving together anymore

4. Stationary

What it shows: A simplified "Yes" or "No" answer to the question:

“Is the spread statistically stable (stationary) and mean-reverting right now?”

Why it matters: Mean reversion strategies only work when the spread is stationary — that is, when the distance between EMAs behaves like a rubber band, not a drifting cloud.

How to use it: A "Yes" means the indicator sees a consistent, stable spread — good for trading. "No" means the market is too volatile, disjointed, or chaotic for reliable mean reversion. Wait for this to flip to "Yes" before trusting signals

5. Last Signal

What it shows: The last signal issued by the system — either "Buy", "Sell", or "None"

Why it matters: Helps avoid confusion and repeated entries. Signals only alternate — you won’t get another Buy until a Sell happens, and vice versa.

How to use it: If the last signal was a "Buy", and you’re watching for a Sell, don’t act on more bullish signals. Great for systems where you only want one position open at a time

6. Bars Since Signal

What it shows: How many bars (candles) have passed since the last Buy or Sell signal.

Why it matters: Gives you context for how long the current condition has persisted

How to use it: If it says 1 or 2, a signal just happened — avoid jumping in late. If it’s been 10+ bars, a new opportunity might be brewing soon. You can use this to time exits if you want to fade a recent signal manually

Indicator Settings:

Short EMA: Sets the short-term EMA period. The smaller the number, the more reactive and more signals you get.

Long EMA: Sets the slow EMA period. The larger this number is, the smoother baseline, and more reliable trend bases are generated.

Z-Score Lookback: The period or bars used for mean & std deviation of spread between short and long EMAs. Larger values result in smoother signals with fewer false positives.

Volatility Window: This value normalizes the spread by historical volatility. This allows you to prevent scale distortion, showing you a cleaner and better chart.

Correlation Lookback: How many periods or how far back to test correlation between slow and long EMAs. This filters out false positives when EMAs lose alignment.

Hurst Lookback: The multiplier to approximate stationarity. Lower leads to more sensitivity to regime change, higher produces a more stricter filtering.

Z Threshold Percentile: This value sets how extreme Z-score must be to trigger a signal. For example, 90 equals only top/bottom 10% of extremes, 80 = more frequent.

Min Bars Between Signals: This hard stop prevents back-to-back signals. The idea is to avoid over-trading or whipsaws in volatile markets even when Hurst lookback and volatility window values are not enough to filter signals.

Some More Recommendations:

We recommend trying different EMA pairs (10/50, 21/100, 5/20) for different asset behaviors. You can set percentile to 85 or 80 if you want more frequent but looser signals. You can also use the Z-score reversion monitor for powerful confirmation.

Cari skrip untuk "如何用wind搜索股票的发行价和份数"

VWAP + EMA Retracement Indicator SwiftEdgeVWAP + EMA Retracement Indicator

Overview

The VWAP + EMA Retracement Indicator is a powerful and visually engaging tool designed to help traders identify high-probability buy and sell opportunities in trending markets. By combining the Volume Weighted Average Price (VWAP) with two Exponential Moving Averages (EMAs) and a unique retracement-based signal logic, this indicator pinpoints moments when the price pulls back to a key zone before resuming its trend. Its modern, AI-inspired visuals and customizable features make it both intuitive and adaptable for traders of all levels.

What It Does

This indicator generates buy and sell signals based on a sophisticated yet straightforward strategy:

Buy Signals: Triggered when the price is above VWAP, has recently retraced to the zone between two EMAs (default 12 and 21 periods), and a strong bullish candle closes above both EMAs.

Sell Signals: Triggered when the price is below VWAP, has retraced to the EMA zone, and a strong bearish candle closes below both EMAs.

Signal Filtering: A customizable cooldown period ensures that only the first signal in a sequence is shown, reducing noise while preserving opportunities for new trends.

Confidence Scores: Each signal includes an AI-inspired confidence score (0-100%), calculated from candle strength and price distance to VWAP, helping traders gauge signal reliability.

The indicator’s visuals enhance decision-making with dynamic gradient lines, a highlighted retracement zone, and clear signal labels, all customizable to suit your preferences.

How It Works

The indicator integrates several components that work together to create a cohesive trading tool:

VWAP: Acts as a dynamic support/resistance level, reflecting the average price weighted by volume. It filters signals to ensure buys occur in uptrends (price above VWAP) and sells in downtrends (price below VWAP).

Dual EMAs: Two EMAs (default 12 and 21 periods) define a retracement zone where the price is likely to consolidate before continuing its trend. Signals are generated only after the price exits this zone with conviction.

Retracement Logic: The indicator looks for price pullbacks to the EMA zone within a user-defined lookback window (default 5 candles), ensuring signals align with trend continuation patterns.

Candle Strength: Signals require strong candles (bullish for buys, bearish for sells) with a minimum body size based on the Average True Range (ATR), filtering out weak or indecisive moves.

Cooldown Mechanism: A unique feature that prevents signal clutter by allowing only the first signal within a user-defined period (default 3 candles), balancing responsiveness with clarity.

Confidence Score: Combines candle body size and price distance to VWAP to assign a score, giving traders an at-a-glance measure of signal strength without needing external analysis.

These components are carefully combined to capture high-probability setups while minimizing false signals, making the indicator suitable for both short-term and swing trading.

How to Use It

Add to Chart: Apply the indicator to a 15-minute chart (recommended) or your preferred timeframe.

Customize Settings:

VWAP Source: Choose the price source (default: hlc3).

EMA Periods: Adjust the fast and slow EMA periods (default: 12 and 21).

Retracement Window: Set how many candles to look back for retracement (default: 5).

ATR Period & Body Size: Define candle strength requirements (default: 14 ATR period, 0.3 multiplier).

Cooldown Period: Control the minimum candles between signals (default: 3; set to 0 to disable).

Candle Requirements: Toggle whether signals require bullish/bearish candles or entire candle above/below EMAs.

Visuals: Enable/disable gradient colors, retracement zone, confidence scores, and choose a color scheme (Neon, Light, or Dark).

Interpret Signals:

Buy: A green "Buy" label with a confidence score appears below the candle when conditions are met.

Sell: A red "Sell" label with a confidence score appears above the candle.

Use the confidence score to prioritize higher-probability signals (e.g., above 80%).

Trade Management: Combine signals with your risk management strategy, such as setting stop-loss below the retracement zone and targeting a 1:2 risk-reward ratio.

Why It’s Unique

The VWAP + EMA Retracement Indicator stands out due to its thoughtful integration of classic indicators with modern enhancements:

Balanced Signal Filtering: The cooldown mechanism ensures clarity without missing key opportunities, unlike many indicators that overwhelm with frequent signals.

AI-Inspired Confidence: The confidence score simplifies decision-making by quantifying signal strength, mimicking advanced analytical tools in an accessible way.

Elegant Visuals: Dynamic gradients, a highlighted retracement zone, and customizable color schemes (Neon, Light, Dark) create a sleek, futuristic interface that’s both functional and visually appealing.

Flexibility: Extensive customization options let traders tailor the indicator to their style, from conservative swing trading to aggressive scalping.

[SHORT ONLY] 10 Bar Low Pullback█ STRATEGY DESCRIPTION

The "10 Bar Low Pullback" strategy is a contrarian short trading system designed to capture pullbacks after a new 10‐bar low is made. it identifies a potential short opportunity when the current bar’s low breaks below the lowest low of the previous 10 bars, provided that the bar exhibits strong internal momentum as measured by its IBS value. An optional trend filter further refines entries by requiring that the close is below a 200-period EMA.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

ibs = (close - low) / (high - low)

- Low IBS (≤ 0.2): Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8): Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current bar’s low is below the lowest low of the past X bars (default: 10).

The bar’s IBS is greater than the specified threshold (default: 0.85).

The signal occurs within the defined trading window (between Start Time and End Time).

If the EMA Filter is enabled, the close must be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

Lookback Period: Defines the number of bars (default is 10) over which the lowest low is calculated.

IBS Threshold: Sets the minimum required IBS value (default is 0.85) to qualify as a pullback.

Trading Window: Trades are only executed between the user-defined Start Time and End Time.

EMA Filter (Optional): When enabled, short entries are only considered if the current close is below the 200-period EMA, with the EMA period being adjustable (default is 200).

█ PERFORMANCE OVERVIEW

Designed for shorting opportunities, this strategy aims to capture pullbacks following an aggressive 10-bar low break.

It leverages a combination of a lookback low and IBS measurement to identify overextended bullish moves that may revert.

The optional EMA filter helps confirm a bearish market environment by ensuring the price remains under the trend line.

Suitable for use on various assets, including stocks and ETFs, on daily or similar timeframes.

Backtesting and parameter optimization are recommended to tailor the strategy to specific market conditions.

Multi-indicator Signal Builder [Skyrexio]Overview

Multi-Indicator Signal Builder is a versatile, all-in-one script designed to streamline your trading workflow by combining multiple popular technical indicators under a single roof. It features a single-entry, single-exit logic, intrabar stop-loss/take-profit handling, an optional time filter, a visually accessible condition table, and a built-in statistics label. Traders can choose any combination of 12+ indicators (RSI, Ultimate Oscillator, Bollinger %B, Moving Averages, ADX, Stochastic, MACD, PSAR, MFI, CCI, Heikin Ashi, and a “TV Screener” placeholder) to form entry or exit conditions. This script aims to simplify strategy creation and analysis, making it a powerful toolkit for technical traders.

Indicators Overview

1. RSI (Relative Strength Index)

Measures recent price changes to evaluate overbought or oversold conditions on a 0–100 scale.

2. Ultimate Oscillator (UO)

Uses weighted averages of three different timeframes, aiming to confirm price momentum while avoiding false divergences.

3. Bollinger %B

Expresses price relative to Bollinger Bands, indicating whether price is near the upper band (overbought) or lower band (oversold).

4. Moving Average (MA)

Smooths price data over a specified period. The script supports both SMA and EMA to help identify trend direction and potential crossovers.

5. ADX (Average Directional Index)

Gauges the strength of a trend (0–100). Higher ADX signals stronger momentum, while lower ADX indicates a weaker trend.

6. Stochastic

Compares a closing price to a price range over a given period to identify momentum shifts and potential reversals.

7. MACD (Moving Average Convergence/Divergence)

Tracks the difference between two EMAs plus a signal line, commonly used to spot momentum flips through crossovers.

8. PSAR (Parabolic SAR)

Plots a trailing stop-and-reverse dot that moves with the trend. Often used to signal potential reversals when price crosses PSAR.

9. MFI (Money Flow Index)

Similar to RSI but incorporates volume data. A reading above 80 can suggest overbought conditions, while below 20 may indicate oversold.

10. CCI (Commodity Channel Index)

Identifies cyclical trends or overbought/oversold levels by comparing current price to an average price over a set timeframe.

11. Heikin Ashi

A type of candlestick charting that filters out market noise. The script uses a streak-based approach (multiple consecutive bullish or bearish bars) to gauge mini-trends.

12. TV Screener

A placeholder condition designed to integrate external buy/sell logic (like a TradingView “Buy” or “Sell” rating). Users can override or reference external signals if desired.

Unique Features

1. Multi-Indicator Entry and Exit

You can selectively enable any subset of 12+ classic indicators, each with customizable parameters and conditions. A position opens only if all enabled entry conditions are met, and it closes only when all enabled exit conditions are satisfied, helping reduce false triggers.

2. Single-Entry / Single-Exit with Intrabar SL/TP

The script supports a single position at a time. Once a position is open, it monitors intrabar to see if the price hits your stop-loss or take-profit levels before the bar closes, making results more realistic for fast-moving markets.

3. Time Window Filter

Users may specify a start/end date range during which trades are allowed, making it convenient to focus on specific market cycles for backtesting or live trading.

4. Condition Table and Statistics

A table at the bottom of the chart lists all active entry/exit indicators. Upon each closed trade, an integrated statistics label displays net profit, total trades, win/loss count, average and median PnL, etc.

5. Seamless Alerts and Automation

Configure alerts in TradingView using “Any alert() function call.”

The script sends JSON alert messages you can route to your own webhook.

The indicator can be integrated with Skyrexio alert bots to automate execution on major cryptocurrency exchanges

6. Optional MA/PSAR Plots

For added visual clarity, optionally plot the chosen moving averages or PSAR on the chart to confirm signals without stacking multiple indicators.

Methodology

1. Multi-Indicator Entry Logic

When multiple entry indicators are enabled (e.g., RSI + Stochastic + MACD), the script requires all signals to align before generating an entry. Each indicator can be set for crossovers, crossunders, thresholds (above/below), etc. This “AND” logic aims to filter out low-confidence triggers.

2. Single-Entry Intrabar SL/TP

One Position At a Time: Once an entry signal triggers, a trade opens at the bar’s close.

Intrabar Checks: Stop-loss and take-profit levels (if enabled) are monitored on every tick. If either is reached, the position closes immediately, without waiting for the bar to end.

3. Exit Logic

All Conditions Must Agree: If the trade is still open (SL/TP not triggered), then all enabled exit indicators must confirm a closure before the script exits on the bar’s close.

4. Time Filter

Optional Trading Window: You can activate a date/time range to constrain entries and exits strictly to that interval.

Justification of Methodology

Indicator Confluence: Combining multiple tools (RSI, MACD, etc.) can reduce noise and false signals.

Intrabar SL/TP: Capturing real-time spikes or dips provides a more precise reflection of typical live trading scenarios.

Single-Entry Model: Straightforward for both manual and automated tracking (especially important in bridging to bots).

Custom Date Range: Helps refine backtesting for specific market conditions or to avoid known irregular data periods.

How to Use

1. Add the Script to Your Chart

In TradingView, open Indicators , search for “Multi-indicator Signal Builder”.

Click to add it to your chart.

2. Configure Inputs

Time Filter: Set a start and end date for trades.

Alerts Messages: Input any JSON or text payload needed by your external service or bot.

Entry Conditions: Enable and configure any indicators (e.g., RSI, MACD) for a confluence-based entry.

Close Conditions: Enable exit indicators, along with optional SL (negative %) and TP (positive %) levels.

3. Set Up Alerts

In TradingView, select “Create Alert” → Condition = “Any alert() function call” → choose this script.

Entry Alert: Triggers on the script’s entry signal.

Close Alert: Triggers on the script’s close signal (or if SL/TP is hit).

Skyrexio Alert Bots: You can route these alerts via webhook to Skyrexio alert bots to automate order execution on major crypto exchanges (or any other supported broker).

4. Visual Reference

A condition table at the bottom summarizes active signals.

Statistics Label updates automatically as trades are closed, showing PnL stats and distribution metrics.

Backtesting Guidelines

Symbol/Timeframe: Works on multiple assets and timeframes; always do thorough testing.

Realistic Costs: Adjust commissions and potential slippage to match typical exchange conditions.

Risk Management: If using the built-in stop-loss/take-profit, set percentages that reflect your personal risk tolerance.

Longer Test Horizons: Verify performance across diverse market cycles to gauge reliability.

Example of statistic calculation

Test Period: 2023-01-01 to 2025-12-31

Initial Capital: $1,000

Commission: 0.1%, Slippage ~5 ticks

Trade Count: 468 (varies by strategy conditions)

Win rate: 76% (varies by strategy conditions)

Net Profit: +96.17% (varies by strategy conditions)

Disclaimer

This indicator is provided strictly for informational and educational purposes .

It does not constitute financial or trading advice.

Past performance never guarantees future results.

Always test thoroughly in demo environments before using real capital.

Enjoy exploring the Multi-Indicator Signal Builder! Experiment with different indicator combinations and adjust parameters to align with your trading preferences, whether you trade manually or link your alerts to external automation services. Happy trading and stay safe!

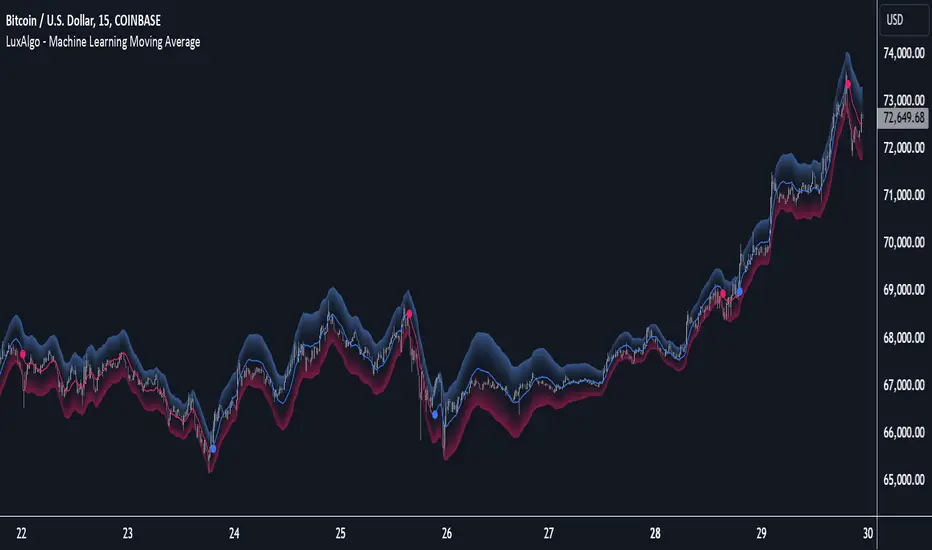

Machine Learning Moving Average [LuxAlgo]The Machine Learning Moving Average (MLMA) is a responsive moving average making use of the weighting function obtained Gaussian Process Regression method. Characteristic such as responsiveness and smoothness can be adjusted by the user from the settings.

The moving average also includes bands, used to highlight possible reversals.

🔶 USAGE

The Machine Learning Moving Average smooths out noisy variations from the price, directly estimating the underlying trend in the price.

A higher "Window" setting will return a longer-term moving average while increasing the "Forecast" setting will affect the responsiveness and smoothness of the moving average, with higher positive values returning a more responsive moving average and negative values returning a smoother but less responsive moving average.

Do note that an excessively high "Forecast" setting will result in overshoots, with the moving average having a poor fit with the price.

The moving average color is determined according to the estimated trend direction based on the bands described below, shifting to blue (default) in an uptrend and fushia (default) in downtrends.

The upper and lower extremities represent the range within which price movements likely fluctuate.

Signals are generated when the price crosses above or below the band extremities, with turning points being highlighted by colored circles on the chart.

🔶 SETTINGS

Window: Calculation period of the moving average. Higher values yield a smoother average, emphasizing long-term trends and filtering out short-term fluctuations.

Forecast: Sets the projection horizon for Gaussian Process Regression. Higher values create a more responsive moving average but will result in more overshoots, potentially worsening the fit with the price. Negative values will result in a smoother moving average.

Sigma: Controls the standard deviation of the Gaussian kernel, influencing weight distribution. Higher Sigma values return a longer-term moving average.

Multiplicative Factor: Adjusts the upper and lower extremity bounds, with higher values widening the bands and lowering the amount of returned turning points.

🔶 RELATED SCRIPTS

Machine-Learning-Gaussian-Process-Regression

SuperTrend-AI-Clustering

ADX (levels)This Pine Script indicator calculates and displays the Average Directional Index (ADX) along with the DI+ and DI- lines to help identify the strength and direction of a trend. The script is designed for Pine Script v6 and includes customizable settings for a more tailored analysis.

Features:

ADX Calculation:

The ADX measures the strength of a trend without indicating its direction.

It uses a smoothing method for more reliable trend strength detection.

DI+ and DI- Lines (Optional):

The DI+ (Directional Index Plus) and DI- (Directional Index Minus) help determine the direction of the trend:

DI+ indicates upward movement.

DI- indicates downward movement.

These lines are disabled by default but can be enabled via input settings.

Customizable Threshold:

A horizontal line (hline) is plotted at a user-defined threshold level (default: 20) to highlight significant ADX values that indicate a strong trend.

Slope Analysis:

The slope of the ADX is analyzed to classify the trend into:

Strong Trend: Slope is higher than a defined "medium" threshold.

Moderate Trend: Slope falls between "weak" and "medium" thresholds.

Weak Trend: Slope is positive but below the "weak" threshold.

A background color changes dynamically to reflect the strength of the trend:

Green (light or dark) indicates trend strength levels.

Custom Colors:

ADX color is customizable (default: pink #e91e63).

Background colors for trend strength can also be adjusted.

Independent Plot Window:

The indicator is displayed in a separate window below the price chart, making it easier to analyze trend strength without cluttering the main price chart.

Parameters:

ADX Period: Defines the lookback period for calculating the ADX (default: 14).

Threshold (hline): A horizontal line value to differentiate strong trends (default: 20).

Slope Thresholds: Adjustable thresholds for weak, moderate, and strong trend slopes.

Enable DI+ and DI-: Boolean options to display or hide the DI+ and DI- lines.

Colors: Customizable colors for ADX, background gradients, and other elements.

How to Use:

Identify Trend Strength:

Use the ADX value to determine the strength of a trend:

Below 20: Weak trend.

Above 20: Strong trend.

Analyze Trend Direction:

Enable DI+ and DI- to check whether the trend is upward (DI+ > DI-) or downward (DI- > DI+).

Dynamic Slope Detection:

Use the background color as a quick visual cue to assess trend strength changes.

This indicator is ideal for traders who want to measure trend strength and direction dynamically while maintaining a clean and organized chart layout.

FTD & DD AnalyzerFTD & DD Analyzer

A comprehensive tool for identifying Follow-Through Days (FTDs) and Distribution Days (DDs) to analyze market conditions and potential trend changes, based on William J. O'Neil's proven methodology.

About the Methodology

This indicator implements the market analysis techniques developed by William J. O'Neil, founder of Investor's Business Daily and author of "How to Make Money in Stocks." O'Neil's research, spanning market data back to the 1880s, has successfully identified major market turns throughout history. His FTD and DD concepts remain crucial tools for institutional investors and serious traders.

Overview

This indicator helps traders identify two critical market conditions:

Distribution Days (DDs) - days of institutional selling pressure

Follow-Through Days (FTDs) - confirmation of potential market bottoms and new uptrends

The combination of these signals provides valuable insight into market health and potential trend changes.

Key Features

Distribution Day detection with customizable criteria

Follow-Through Day identification based on classical methodology

Market bottom detection using EMA analysis

Dynamic warning system for accumulated Distribution Days

Visual alerts with customizable labels

Advanced debug mode for detailed analysis

Flexible display options for different trading styles

Distribution Days Analysis

What is a Distribution Day?

A Distribution Day occurs when:

The price closes lower by a specified percentage (default -0.2%)

Volume is higher than the previous day

DD Settings

Price Threshold: Minimum price decline to qualify (default -0.2%)

Lookback Period: Number of days to analyze for DD accumulation (default 25)

Warning Levels:

First warning at 4 DDs

Severe warning (SOS - Sign of Strength) at 6 DDs

Display Options:

Show/hide DD count

Show/hide DD labels

Choose between showing all DDs or only within lookback period

Follow-Through Day Detection

What is a Follow-Through Day?

Following O'Neil's research, a Follow-Through Day confirms a potential market bottom when:

Occurs between day 4 and 13 after a bottom formation (optimal: days 4-7)

Shows significant price gain (default 1.5%)

Accompanied by higher volume than the previous day

Key Statistics:

FTDs followed by distribution on days 1-2 fail 95% of the time

Distribution on day 3 leads to 70% failure rate

Later distribution (days 4-5) shows only 30% failure rate

FTD Settings

Minimum Price Gain: Required percentage gain (default 1.5%)

Valid Window: Day 4 to Day 13 after bottom

Quality Rating:

🚀 for FTDs occurring within 7 days (historically most reliable)

⭐ for later FTDs

Market Bottom Detection

The indicator uses a sophisticated approach to identify potential market bottoms:

EMA Analysis:

Tracks 8 and 21-period EMAs

Monitors EMA alignment and momentum

Customizable tolerance levels

Price Action:

Looks for lower lows within specified lookback period

Confirms bottom with subsequent price action

Reset mechanism to prevent false signals

Visual Indicators

Label Types

📉 Distribution Days

⬇️ Market Bottoms

🚀/⭐ Follow-Through Days

⚠️ DD Warning Levels

Customization Options

Label size: Tiny, Small, Normal, Large

Label style: Default, Arrows, Triangles

Background colors for different signals

Dynamic positioning using ATR multiplier

Practical Usage

1. Monitor DD Accumulation:

Watch for increasing number of Distribution Days

Pay attention to warning levels (4 and 6 DDs)

Consider reducing exposure when warnings appear

2. Bottom Recognition:

Look for potential bottom formations

Monitor EMA alignment and price action

Wait for confirmation signals

3. FTD Confirmation:

Track days after potential bottom

Watch for strong price/volume action in valid window

Note FTD quality rating for additional context

Alert System

Built-in alerts for:

New Distribution Days

Follow-Through Day signals

High DD accumulation warnings

Tips for Best Results

Use multiple timeframes for confirmation

Combine with other market health indicators

Pay attention to sector rotation and market leadership

Monitor volume patterns for confirmation

Consider market context and external factors

Technical Notes

The indicator uses advanced array handling for DD tracking

Dynamic calculations ensure accurate signal generation

Debug mode available for detailed analysis

Optimized for real-time and historical analysis

Additional Information

Compatible with all markets and timeframes

Best suited for daily charts

Regular updates and maintenance

Based on O'Neil's time-tested market analysis principles

Conclusion

The FTD & DD Analyzer provides a systematic approach to market analysis, combining O'Neil's proven methodologies with modern technical analysis. It helps traders identify potential market turns while monitoring institutional participation through volume analysis.

Remember that no indicator is perfect - always use in conjunction with other analysis tools and proper risk management.

IronBot v3Introduction

IronBot V3 is a TradingView indicator that analyzes market trends, identifies potential trading opportunities, and helps manage trades by visualizing entry points, stop-loss levels, and take-profit targets.

How It Works

The indicator evaluates price action within a specified analysis window to determine market trends. It uses Fibonacci retracement levels to identify key price levels for trend detection and trading signals. Based on user-defined inputs, it calculates and displays trade levels, including entry points, stop-loss, and multiple take-profit levels.

Trend Definition:

The highest high and lowest low are calculated over a specified number of candles.

The price range is determined as the difference between the highest high and lowest low.

Three Fibonacci levels are calculated within this range:

- Fib Level 0.236

- Trend Line (0.5 level)

- Fib Level 0.786

Determining Long and Short Conditions:

Long Conditions (Buy):

The closing price must be above both the trend line (0.5 level) and the Fib Level 0.236.

Additionally, the market must not currently be in a bearish trend.

Short Conditions (Sell):

The closing price must be below both the trend line and the Fib Level 0.786.

The market must not currently be in a bullish trend.

Trend State Updates:

When a condition is met, the indicator sets the trend to bullish or bearish and turns off bearish or bullish trend conditions.

If neither buy nor sell conditions are met, the trend remains unchanged, and no new trade signals are generated.

Inputs and Their Role in the Algorithm

General Settings

Analysis Window: Specifies the number of historical candles to analyze. This influences the calculation of key levels such as highs and lows, which are critical for determining Fibonacci retracement levels.

First Trade: Defines the start date for generating trading signals.

Trade Configuration

Display TP/SL: Enables or disables the visualization of take-profit and stop-loss levels on the chart.

Leverage: Defines the leverage applied to trades for risk and position size calculations.

Initial Capital: Specifies the starting capital, which is used for calculating position sizes and profits.

Exchange Fees (%): Sets the percentage of fees applied by the exchange, which is factored into profit calculations.

Country Tax (%): Allows users to define applicable taxes, which are subtracted from net profits.

Stop-Loss Configuration

Break Even: Toggles the break-even functionality. When enabled, the stop-loss level adjusts dynamically as take-profit levels are reached.

Stop Loss (%): Defines the percentage distance from the entry price to the stop-loss level.

Take-Profit Settings

The indicator supports up to four take-profit levels:

- TP1 through TP4 Ratios: Specify the price levels for each take-profit target as a percentage of the entry price.

- Profit Percentages: Allocate a percentage of the position size to each take-profit level.

Visualization Elements

Trend Indicators: Displays Fibonacci-based trend lines and markers for bullish or bearish conditions.

Trade Levels: Entry, stop-loss, and take-profit levels are visualized on the chart by dotted lines for clarity. Additionally, a semi-transparent background is applied when a portion of the trade is closed to enhance visualization. Positive profits from a closed trade are green; otherwise, they are red.

Trade Profit Indicator: On each trade, every time a part of the trade is closed (e.g., take profit is reached), the profit indicator will be updated.

Performance Panel: Summarizes key account statistics, including net balance, profit/loss, and trading performance metrics.

Usage Guidelines

Add the indicator to your TradingView chart.

Configure the input settings based on your trading strategy.

Use the displayed levels and trend signals to make informed trading decisions.

Contact

For further assistance, including automation inquiries, feel free to contact me through TradingView’s messaging system.

Purpose and Disclaimer

IronBot V3 is designed for educational purposes and to assist in analyzing market trends. It is not financial advice, and users should perform their own due diligence before making any trading decisions.

Trading involves significant risk, and past performance is not indicative of future results. Use this indicator responsibly.

ADX Breakout Strategy█ OVERVIEW

The ADX Breakout strategy leverages the Average Directional Index (ADX) to identify and execute breakout trades within specified trading sessions. Designed for the NQ and ES 30-minute charts, this strategy aims to capture significant price movements while managing risk through predefined stop losses and trade limits.

This strategy was taken from a strategy that was posted on YouTube. I would link the video, but I believe is is "against house rules".

█ CONCEPTS

The strategy is built upon the following key concepts:

ADX Indicator: Utilizes the ADX to gauge the strength of a trend. Trades are initiated when the ADX value is below a certain threshold, indicating potential for trend development.

Trade Session Management: Limits trading to specific hours to align with optimal market activity periods.

Risk Management: Implements a fixed dollar stop loss and restricts the number of trades per session to control exposure.

█ FEATURES

Customizable Stop Loss: Set your preferred stop loss amount to manage risk effectively.

Trade Session Configuration: Define the trading hours to focus on the most active market periods.

Entry Conditions: Enter long positions when the price breaks above the highest close in the lookback window and the ADX indicates potential trend strength.

Trade Limits: Restrict the number of trades per session to maintain disciplined trading.

Automated Exit: Automatically closes all positions at the end of the trading session to avoid overnight risk.

█ HOW TO USE

Configure Inputs :

Stop Loss ($): Set the maximum loss per trade.

Trade Session: Define the active trading hours.

Highest Lookback Window: Specify the number of bars to consider for the highest close.

Apply the Strategy :

Add the ADX Breakout strategy to your chart on TradingView.

Ensure you are using a 30-minute timeframe for optimal performance.

█ LIMITATIONS

Market Conditions: The strategy is optimized for trending markets and may underperform in sideways or highly volatile conditions.

Timeframe Specific: Designed specifically for 30-minute charts; performance may vary on different timeframes.

Single Asset Focus: Primarily tested on NQ and ES instruments; effectiveness on other symbols is not guaranteed.

█ DISCLAIMER

This ADX Breakout strategy is provided for educational and informational purposes only. It is not financial advice and should not be construed as such. Trading involves significant risk, and you may incur substantial losses. Always perform your own analysis and consider your financial situation before using this or any other trading strategy. The source material for this strategy is publicly available in the comments at the beginning of the code script. This strategy has been published openly for anyone to review and verify its methodology and performance.

Relative Strength Scatter Plot [LuxAlgo]The Relative Strength Scatter Plot indicator is a tool that shows the historical performance of various user-selected securities against a selected benchmark.

This tool is inspired by Relative Rotation Graphs®. Relative Rotation Graphs® is a registered trademark of JOOS Holdings B.V. This script is neither endorsed, nor sponsored, nor affiliated with them.

🔶 USAGE

This tool depicts a simple scatter plot using the relative strength ratio as the X-axis and its momentum as the Y-axis of the user-selected symbols against the selected benchmark.

The graph is divided into four quadrants, and the interpretation of the graph is done depending on where a point is situated on the graph:

A point in the green quadrant would indicate that the security is leading the benchmark in strength, with positive strength momentum.

A point in the yellow quadrant would indicate that the security is leading the benchmark in strength, with negative strength momentum.

A point in the blue quadrant would indicate that the security is lagging behind the benchmark in strength, with positive strength momentum.

A point in the red quadrant would indicate that the security is lagging behind the benchmark in strength, with negative strength momentum.

The trail of each symbol allows the user to see the evolution of the relative strength momentum relative to the relative strength ratio. The length of the trail can be controlled by the "Trail Length" setting.

🔶 DETAILS

Our relative strength ratio estimate is first obtained from the relative strength between the symbol of interest and the benchmark, the result is then smoothed using a linearly weighted moving average (wma). This result is then normalized with a wma of the smoothed relative strength, this ratio is again smoothed with the wma and multiplied by 100.

The relative strength momentum estimate is obtained from the ratio between the previously estimated RS-Ratio and its wma, this ratio is then multiplied by 100.

🔶 SETTINGS

Calculation Window: Calculation window of the RS-Ratio and RS-Momentum metrics.

Symbols: Symbols used for the computation of the graph, each settings line allows us to determine whether the symbol is to be displayed on the graph as well as its color.

Benchmark: Benchmark symbol used for the computation of the graph. Indices are commonly used as a benchmark.

🔹 Graph Settings

Trail Length: Number of past data points to display on the graph for each symbol.

Resolution: Controls the horizontal length of the graph.

THISMA btccorrelationDescription:

This is a tool designed for traders who want to analyze correlation between any traded crypto's price in USD and the price of Bitcoin in USD.

Key Features:

Adjustable Correlation Window: The script features an input parameter that allows traders to set the length of the correlation window, with a default value of 14. Lower if you want faster granularity.

Clear Visualization: The correlation coefficient is plotted in a distinct pane below the main trading chart.

Reference Lines for Interpretation: Horizontal reference lines are included at 0.5 (indicating weak positive correlation), -0.5 (indicating weak negative correlation), and 0 (indicating no correlation). These lines, color-coded in green, red, and gray respectively, assist traders in quickly interpreting the correlation coefficient's value.

Applications:

Market Insight: If you want to be able to monitor if you should enter a trade on an altcoin or if its better to stick to Bitcoin to avoid being double exposed.

Risk Management: Identifying the correlation can help in assessing and managing the systemic risk associated with market movements, especially in cryptocurrency markets where Bitcoin's influence is significant.

Kernel Regression ToolkitThis toolkit provides filters and extra functionality for non-repainting Nadaraya-Watson estimator implementations made by @jdehorty. For the sake of ease I have nicknamed it "kreg". Filters include a smoothing formula and zero lag formula. The purpose of this script is to help traders test, experiment and develop different regression lines. Regression lines are best used as trend lines and can be an invaluable asset for quickly locating first pullbacks and breaks of trends.

Other features include two J lines and a blend line. J lines are featured in tools like Stochastic KDJ. The formula uses the distance between K and D lines to make the J line. The blend line adds the ability to blend two lines together. This can be useful for several tasks including finding a center/median line between two lines or for blending in the characteristics of a different line. Default is set to 50 which is a 50% blend of the two lines. This can be increased and decreased to taste. This tool can be overlaid on the chart or on top of another indicator if you set the source. It can even be moved into its own window to create a unique oscillator based on whatever sources you feed it.

Below are the standard settings for the kernel estimation as documented by @jdehorty:

Lookback Window: The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars. Recommended range: 3-50

Weighting: Relative weighting of time frames. As this value approaches zero, the longer time frames will exert more influence on the estimation. As this value approaches infinity, the behavior of the Rational Quadratic Kernel will become identical to the Gaussian kernel. Recommended range: 0.25-25

Level: Bar index on which to start regression. Controls how tightly fit the kernel estimate is to the data. Smaller values are a tighter fit. Larger values are a looser fit. Recommended range: 2-25

Lag: Lag for crossover detection. Lower values result in earlier crossovers. Recommended range: 1-2

For more information on this technique refer to to the original open source indicator by @jdehorty located here:

4H RangeThis script visualizes certain key values based on a 4-hour timeframe of the selected market on the chart. These values include the High, Mid, and Low price levels during each 4-hour period.

These levels can be helpful to identify inside range price action, chop, and consolidation. They can sometimes act as pivots and can be a great reference for potential entries and exits if price continues to hold the same range.

Here's a step-by-step overview of what this indicator does:

1. Inputs: At the beginning of the script, users are allowed to customize some inputs:

Choose the color of lines and labels.

Decide whether to show labels on the chart.

Choose the size of labels ("tiny", "small", "normal", or "large").

Choose whether to display price values in labels.

Set the number of bars to offset the labels to the right.

Set a threshold for the number of ticks that triggers a new calculation of high, mid, and low values.

* Tick settings may need to be increased on equity charts as one tick is usually equal to one cent.

For example, if you want to clear the range when there is a close one point/one dollar above or below the range high/low then on ES

that would be 4 ticks but one whole point on AAPL would be 100 ticks. 100 ticks on an equity chart may or may not be ideal due to

different % change of 100 ticks might be too excessive depending on the price per share.

So be aware that user preferred thresholds can vary greatly depending on which chart you're using.

2. Retrieving Price Data: The script retrieves the high, low, and closing price for every 4-hour period for the current market.

The script also calculates the mid-price of each 4-hour period (the average of the high and low prices).

3. Line Drawing: At the start of the script (first run), it draws three lines (high, mid, and low) at the levels corresponding to the high,

mid, and low prices. Users can also change transparency settings on historical lines to view them. Default setting for historical lines

is for them to be hidden.

4. Updating Lines and Labels: For each subsequent 4-hour period, the script checks whether the close price of the period has gone

beyond a certain threshold (set by user input) above the previous high or below the previous low. If it has, the script deletes the

previous lines and labels, draws new lines at the new high, mid, and low levels, and creates new labels (if the user has opted to

show labels).

5. Displaying Values in the Data Window: In addition to the visual representation on the chart, the script also plots the high, mid, and

low prices. These plotted values appear in the Data Window of TradingView, allowing users to see the exact price levels even when

they're not directly labeled on the chart.

6. Updating Lines and Labels Position: At the end of each period, the script moves the lines and labels (if they're shown) to the right,

keeping them aligned with the current period.

Please note: This script operates based on a 4-hour timeframe, regardless of the timeframe selected on the chart. If a shorter timeframe is selected on the chart, the lines and labels will appear to extend across multiple bars because they represent 4-hour price levels. If a longer timeframe is selected, the lines and labels may not accurately represent high, mid, and low levels within that longer timeframe.

Rolling QuartilesThis script will continuously draw a boxplot to represent quartiles associated with data points in the current rolling window.

Description :

A quartile is a statistical term that refers to the division of a dataset based on percentiles.

Q1 : Quartile 1 - 25th percentile

Q2 : Quartile 2 - 50th percentile, as known as the median

Q3 : Quartile 3 - 75th percentile

Other points to note:

Q0: the minimum

Q4: the maximum

Other properties :

- Q1 to Q3: a range is known as the interquartile range ( IQR ). It describes where 50% of data approximately lie.

- Line segments connecting IQR to min and max (Q0→Q1, and Q3→Q4) are known as whiskers . Data lying outside the whiskers are considered as outliers. However, such extreme values will not be found in a rolling window because whenever new datapoints are introduced to the dataset, the oldest values will get dropped out, leaving Q0 and Q4 to always point to the observable min and max values.

Applications :

This script has a feature that allows moving percentiles (moving values of Q1, Q2, and Q3) to be shown. This can be applied for trading in ways such as:

- Q2: as alternative to a SMA that uses the same lookback period. We know that the Mean (SMA) is highly sensitive to extreme values. On the other hand, Median (Q2) is less affected by skewness. Putting it together, if the SMA is significantly lower than Q2, then price is regarded as negatively skewed; prices of a few candles are likely exceptionally lower. Vice versa when price is positively skewed.

- Q1 and Q3: as lower and upper bands. As mentioned above, the IQR covers approximately 50% of data within the rolling window. If price is normally distributed, then Q1 and Q3 bands will overlap a bollinger band configured with +/- 0.67x standard deviations (modifying default: 2) above and below the mean.

- The boxplot, combined with TradingView's builtin bar replay feature, makes a great tool for studies purposes. This helps visualization of price at a chosen instance of time. Speaking of which, it can also be used in conjunction with a fixed volume profile to compare and contrast the effects (in terms of price range) with and without consideration of weights by volume.

Parameters :

- Lookback: The size of the rolling window.

- Offset: Location of boxplot, right hand side relative to recent bar.

- Source data: Data points for observation, default is closing price

- Other options such as color, and whether to show/hide various lines.

vol_boxA simple script to draw a realized volatility forecast, in the form of a box. The script calculates realized volatility using the EWMA method, using a number of periods of your choosing. Using the "periods per year", you can adjust the script to work on any time frame. For example, if you are using an hourly chart with bitcoin, there are 24 periods * 365 = 8760 periods per year. This setting is essential for the realized volatility figure to be accurate as an annualized figure, like VIX.

By default, the settings are set to mimic CBOE volatility indices. That is, 252 days per year, and 20 period window on the daily timeframe (simulating a 30 trading day period).

Inside the box are three figures:

1. The current realized volatility.

2. The rank. E.g. "10%" means the current realized volatility is less than 90% of realized volatility measures.

3. The "accuracy": how often price has closed within the box, historically.

Inputs:

stdevs: the number of standard deviations for the box

periods to project: the number of periods to forecast

window: the number of periods for calculating realized volatility

periods per year: the number of periods in one year (e.g. 252 for the "D" timeframe)

Levels Of Fear [AstrideUnicorn]"Buy at the level of maximum fear when everyone is selling." - says a well-known among traders wisdom. If an asset's price declines significantly from the most recent highest value or established range, traders start to worry. The higher the drawdown gets, the more fear market participants experience. During a sell-off, a feedback loop arises, in which the escalating fear and price decline strengthen each other.

The Levels Of Fear indicator helps analyze price declines and find the best times to buy an asset after a sell-off. In finance, volatility is a term that describes the degree of variation of an asset price over time. It is usually denoted by the letter σ (sigma) and estimated as the standard deviation of the asset price or price returns. The Levels Of Fear indicator helps measure the current price decline in the standard deviation units. It plots seven levels at distances of 1, 2, 3, 4, 5, 6, and 7 standard deviations (sigmas) below the base price (the recent highest price or upper bound of the established range). In what follows, we will refer to these levels as levels of fear.

HOW TO USE

When the price in its decline reaches a certain level of fear, it means that it has declined from its recent highest value by a corresponding number of standard deviations. The indicator helps traders see the minimum levels to which the price may fall and estimate the potential depth of the current decline based on the cause of the actual market shock. Five-seven sigma declines are relatively rare events and correspond to significant market shocks. In the lack of information, 5-7 sigma levels are good for buying an asset. Because when the price falls that deep, it corresponds to the maximum fear and pessimism in the market when most people are selling. In such situations, contrarian logic becomes the best decision.

SETTINGS

Window: the averaging window or period of the indicator. The algorithm uses this parameter to calculate the base level and standard deviations. Higher values are better for measuring deeper and longer declines.

Levels Stability: the parameter used in the decline detection. The higher the value is, the more stable and long the fear levels are, but at the same time, the lag increases. The lower it is, the faster the indicator responds to the price changes, but the fear levels are recalculated more frequently and are less stable. This parameter is mostly for fine-tuning. It does not change the overall picture much.

Mode: the parameter that defines the style for the labels. In the Cool Guys Mode , the indicator displays the labels as emojis. In the Serious Guys Mode , labels show the distance from the base level measured in standard deviation units or sigmas.

Liquidity Levels [LuxAlgo]The Peak Activity Levels indicator displays support and resistance levels from prices accompanied by significant volume. The indicator includes a histogram returning the frequency of closing prices falling between two parallel levels, each bin shows the number of bullish candles within the levels.

1. Settings

Length: Lookback for the detection of volume peaks.

Number Of Levels: Determines the number of levels to display.

Levels Color Mode: Determines how the levels should be colored. "Relative" will color the levels based on their location relative to the current price. "Random" will apply a random color to each level. "Fixed" will use a single color for each level.

Levels Style: Style of the displayed levels. Styles include solid, dashed, and dotted.

1.1 Histogram

Show Histogram: Determines whether to display the histogram or not.

Histogram Window: Lookback period of the histogram calculation.

Bins Colors: Control the color of the histogram bins.

2. Usage

The indicator can be used to display ready-to-use support and resistance. These are constructed from peaks in volume. When a peak occurs, we take the price where this peak occurred and use it as the value for our level.

If one of the levels was previously tested, we can hypothesize that the level might be used as support/resistance in the future. Additional analysis using volume can be done in order to confirm a potential bounce.

The histogram can return various information to the user. It can show if the price stayed within two levels for a long time and if the price within two levels was mostly made of bullish or bearish candles.

In the chart above, we can see that over the most recent 200 bars (determined by Histogram Window) 68 closing prices fall between levels A and B, with 27 bars being bullish.

Additionally, the width of a bin and its length can sometimes give information about the volatility of a specific price variation. If a bin is very wide but short (a low number of closing prices fallen within the levels) then we can conclude a most of the movement was done on a short amount of time.

vol_signalNote: This description is copied from the script comments. Please refer to the comments and release notes for updated information, as I am unable to edit and update this description.

----------

USAGE

This script gives signals based on a volatility forecast, e.g. for a stop

loss. It is a simplified version of my other script "trend_vol_forecast", which incorporates a trend following system and measures performance. The "X" labels indicate when the price touches (exceeds) a forecast. The signal occurs when price crosses "fcst_up" or "fcst_down".

There are only three parameters:

- volatility window: this is the number of periods (bars) used in the

historical volatility calculation. smaller number = reacts more

quickly to changes, but is a "noisier" signal.

- forecast periods: the number of periods for projecting a volatility

forecast. for example, "21" on a daily chart means the plots will

show the forecast from 21 days ago.

- forecast stdev: the number of standard deviations in the forecast.

for example, "2" means that price is expected to remain within

the forecast plot ~95% of the time. A higher number produces a

wider forecast.

The output table shows:

- realized vol: the volatility over the previous N periods, where N =

"volatility window".

- forecast vol: the realized volatility from N periods ago, where N =

"forecast periods"

- up/down fcst (level): the price level of the forecast for the next

N bars, where N = "forecast periods".

- up/down fcst (%): the difference between the current and forecast

price, expressed as a whole number percentage.

The plots show:

- blue/red plot: the upper/lower forecast from "forecast periods" ago.

- blue/red line: the upper/lower forecast for the next

"forecast periods".

- red/blue labels: an "X" where the price touched the forecast from

"forecast periods" ago.

+ NOTE: pinescript only draws a limited number of labels.

They will not appear very far into the past.

Density Zones (GM Crossing Clusters) + QHO Spin FlipsINDICATOR NAME

Density Zones (GM Crossing Clusters) + QHO Spin Flips

OVERVIEW

This indicator combines two complementary ideas into a single overlay: *this combines my earlier Geometric Mean Indicator with the Quantum Harmonic Oscillator (Overlay) with additional enhancements*

1) Density Zones (GM Crossing Clusters)

A “Density Zone” is detected when price repeatedly crosses a Geometric Mean equilibrium line (GM) within a rolling lookback window. Conceptually, this identifies regions where the market is repeatedly “snapping” across an equilibrium boundary—high churn, high decision pressure, and repeated re-selection of direction.

2) QHO Spin Flips (Regression-Residual σ Breaches)

A “Spin Flip” is detected when price deviates beyond a configurable σ-threshold (κ) from a regression-based equilibrium, using normalized residuals. Conceptually, this marks excursions into extreme states (decoherence / expansion), which often precede a reversion toward equilibrium and/or a regime re-scaling.

These two systems are related but not identical:

- Density Zones identify where equilibrium crossings cluster (a “singularity”/anchor behavior around GM).

- Spin Flips identify when price exceeds statistically extreme displacement from the regression equilibrium (LSR), indicating expansion beyond typical variance.

CORE CONCEPTS AND FORMULAS

SECTION A — GEOMETRIC MEAN EQUILIBRIUM (GM)

We define two moving averages:

(1) MA1_t = SMA(close_t, L1)

(2) MA2_t = SMA(close_t, L2)

We define the equilibrium anchor as the geometric mean of MA1 and MA2:

(3) GM_t = sqrt( MA1_t * MA2_t )

This GM line acts as an equilibrium boundary. Repeated crossings are interpreted as high “equilibrium churn.”

SECTION B — CROSS EVENTS (UP/DOWN)

A “cross event” is registered when the sign of (close - GM) changes:

Define a sign function s_t:

(4) s_t =

+1 if close_t > GM_t

-1 if close_t < GM_t

s_{t-1} if close_t == GM_t (tie-breaker to avoid false flips)

Then define the crossing event indicator:

(5) crossEvent_t = 1 if s_t != s_{t-1}

0 otherwise

Additionally, the indicator plots explicit cross markers:

- Cross Above GM: crossover(close, GM)

- Cross Below GM: crossunder(close, GM)

These provide directional visual cues and match the original Geometric Mean Indicator behavior.

SECTION C — DENSITY MEASURE (CROSSING CLUSTER COUNT)

A Density Zone is based on the number of cross events occurring in the last W bars:

(6) D_t = Σ_{i=0..W-1} crossEvent_{t-i}

This is a “crossing density” score: how many times price has toggled across GM recently.

The script implements this efficiently using a cumulative sum identity:

Let x_t = crossEvent_t.

(7) cumX_t = Σ_{j=0..t} x_j

Then:

(8) D_t = cumX_t - cumX_{t-W} (for t >= W)

cumX_t (for t < W)

SECTION D — DENSITY ZONE TRIGGER

We define a Density Zone state:

(9) isDZ_t = ( D_t >= θ )

where:

- θ (theta) is the user-selected crossing threshold.

Zone edges:

(10) dzStart_t = isDZ_t AND NOT isDZ_{t-1}

(11) dzEnd_t = NOT isDZ_t AND isDZ_{t-1}

SECTION E — DENSITY ZONE BOUNDS

While inside a Density Zone, we track the running high/low to display zone bounds:

(12) dzHi_t = max(dzHi_{t-1}, high_t) if isDZ_t

(13) dzLo_t = min(dzLo_{t-1}, low_t) if isDZ_t

On dzStart:

(14) dzHi_t := high_t

(15) dzLo_t := low_t

Outside zones, bounds are reset to NA.

These bounds visually bracket the “singularity span” (the churn envelope) during each density episode.

SECTION F — QHO EQUILIBRIUM (REGRESSION CENTERLINE)

Define the regression equilibrium (LSR):

(16) m_t = linreg(close_t, L, 0)

This is the “centerline” the QHO system uses as equilibrium.

SECTION G — RESIDUAL AND σ (FIELD WIDTH)

Residual:

(17) r_t = close_t - m_t

Rolling standard deviation of residuals:

(18) σ_t = stdev(r_t, L)

This σ_t is the local volatility/width of the residual field around the regression equilibrium.

SECTION H — NORMALIZED DISPLACEMENT AND SPIN FLIP

Define the standardized displacement:

(19) Y_t = (close_t - m_t) / σ_t

(If σ_t = 0, the script safely treats Y_t = 0.)

Spin Flip trigger uses a user threshold κ:

(20) spinFlip_t = ( |Y_t| > κ )

Directional spin flips:

(21) spinUp_t = ( Y_t > +κ )

(22) spinDn_t = ( Y_t < -κ )

The default κ=3.0 corresponds to “3σ excursions,” which are statistically extreme under a normal residual assumption (even though real markets are not perfectly normal).

SECTION I — QHO BANDS (OPTIONAL VISUALIZATION)

The indicator optionally draws the standard σ-bands around the regression equilibrium:

(23) 1σ bands: m_t ± 1·σ_t

(24) 2σ bands: m_t ± 2·σ_t

(25) 3σ bands: m_t ± 3·σ_t

These provide immediate context for the Spin Flip events.

WHAT YOU SEE ON THE CHART

1) MA1 / MA2 / GM lines (optional)

- MA1 (blue), MA2 (red), GM (green).

- GM is the equilibrium anchor for Density Zones and cross markers.

2) GM Cross Markers (optional)

- “GM↑” label markers appear on bars where close crosses above GM.

- “GM↓” label markers appear on bars where close crosses below GM.

3) Density Zone Shading (optional)

- Background shading appears while isDZ_t = true.

- This is the period where the crossing density D_t is above θ.

4) Density Zone High/Low Bounds (optional)

- Two lines (dzHi / dzLo) are drawn only while in-zone.

- These bounds bracket the full churn envelope during the density episode.

5) QHO Bands (optional)

- 1σ, 2σ, 3σ shaded zones around regression equilibrium.

- These visualize the current variance field.

6) Regression Equilibrium (LSR Centerline)

- The white centerline is the regression equilibrium m_t.

7) Spin Flip Markers

- A circle is plotted when |Y_t| > κ (beyond your chosen σ-threshold).

- Marker size is user-controlled (tiny → huge).

HOW TO USE IT

Step 1 — Pick the equilibrium anchor (GM)

- L1 and L2 define MA1 and MA2.

- GM = sqrt(MA1 * MA2) becomes your equilibrium boundary.

Typical choices:

- Faster equilibrium: L1=20, L2=50 (default-like).

- Slower equilibrium: L1=50, L2=200 (macro anchor).

Interpretation:

- GM acts like a “center of mass” between two moving averages.

- Crosses show when price flips from one side of equilibrium to the other.

Step 2 — Tune Density Zones (W and θ)

- W controls the time window measured (how far back you count crossings).

- θ controls how many crossings qualify as a “density/singularity episode.”

Guideline:

- Larger W = slower, broader density detection.

- Higher θ = only the most intense churn is labeled as a Density Zone.

Interpretation:

- A Density Zone is not “bullish” or “bearish” by itself.

- It is a condition: repeated equilibrium toggling (high churn / high compression).

- These often precede expansions, but direction is not implied by the zone alone.

Step 3 — Tune the QHO spin flip sensitivity (L and κ)

- L controls regression memory and σ estimation length.

- κ controls how extreme the displacement must be to trigger a spin flip.

Guideline:

- Smaller L = more reactive centerline and σ.

- Larger L = smoother, slower “field” definition.

- κ=3.0 = strong extreme filter.

- κ=2.0 = more frequent flips.

Interpretation:

- Spin flips mark when price exits the “normal” residual field.

- In your model language: a moment of decoherence/expansion that is statistically extreme relative to recent equilibrium.

Step 4 — Read the combined behavior (your key thesis)

A) Density Zone forms (GM churn clusters):

- Market repeatedly crosses equilibrium (GM), compressing into a bounded churn envelope.

- dzHi/dzLo show the envelope range.

B) Expansion occurs:

- Price can release away from the density envelope (up or down).

- If it expands far enough relative to regression equilibrium, a Spin Flip triggers (|Y| > κ).

C) Re-coherence:

- After a spin flip, price often returns toward equilibrium structures:

- toward the regression centerline m_t

- and/or back toward the density envelope (dzHi/dzLo) depending on regime behavior.

- The indicator does not guarantee return, but it highlights the condition where return-to-field is statistically likely in many regimes.

IMPORTANT NOTES / DISCLAIMERS

- This indicator is an analytical overlay. It does not provide financial advice.

- Density Zones are condition states derived from GM crossing frequency; they do not predict direction.

- Spin Flips are statistical excursions based on regression residuals and rolling σ; markets have fat tails and non-stationarity, so σ-based thresholds are contextual, not absolute.

- All parameters (L1, L2, W, θ, L, κ) should be tuned per asset, timeframe, and volatility regime.

PARAMETER SUMMARY

Geometric Mean / Density Zones:

- L1: MA1 length

- L2: MA2 length

- GM_t = sqrt(SMA(L1)*SMA(L2))

- W: crossing-count lookback window

- θ: crossing density threshold

- D_t = Σ crossEvent_{t-i} over W

- isDZ_t = (D_t >= θ)

- dzHi/dzLo track envelope bounds while isDZ is true

QHO / Spin Flips:

- L: regression + residual σ length

- m_t = linreg(close, L, 0)

- r_t = close_t - m_t

- σ_t = stdev(r_t, L)

- Y_t = r_t / σ_t

- spinFlip_t = (|Y_t| > κ)

Visual Controls:

- toggles for GM lines, cross markers, zone shading, bounds, QHO bands

- marker size options for GM crosses and spin flips

ALERTS INCLUDED

- Density Zone START / END

- Spin Flip UP / DOWN

- Cross Above GM / Cross Below GM

SUMMARY

This indicator treats the Geometric Mean as an equilibrium boundary and identifies “Density Zones” when price repeatedly crosses that equilibrium within a rolling window, forming a bounded churn envelope (dzHi/dzLo). It also models a regression-based equilibrium field and triggers “Spin Flips” when price makes statistically extreme σ-excursions from that field. Used together, Density Zones highlight compression/decision regions (equilibrium churn), while Spin Flips highlight extreme expansion states (σ-breaches), allowing the user to visualize how price compresses around equilibrium, releases outward, and often re-stabilizes around equilibrium structures over time.

Fractal Dimension (Katz, Quant Lab)This indicator estimates the Katz Fractal Dimension of the price series over a rolling window.

It computes:

• L = sum of absolute price changes within the window

• d = maximum distance between any point and the first point in the window

• n = window length

Then applies Katz’s formula:

FDI = ln(n) / (ln(n) + ln(d / L))

The resulting Fractal Dimension typically lies between 1.0 and 2.0:

• FDI ≈ 1.0–1.3 → Strong, directional trend (low randomness)

• FDI ≈ 1.3–1.5 → Mixed / transitional behavior

• FDI ≈ 1.5–2.0 → Noisy, choppy, mean-reverting / range market

Luxy VWAP Magic - MTF Projection EngineThis indicator transforms the classic VWAP into a comprehensive trading system. Instead of switching between multiple indicators, you get everything in one place: multi-timeframe analysis, statistical bands, momentum detection, volume profiling, session tracking, and divergence signals.

What Makes This Different

Traditional VWAP indicators show a single line. This tool treats VWAP as a foundation for complete market analysis. The indicator automatically detects your asset type (stocks, crypto, forex, futures) and adjusts its behavior accordingly. Crypto traders get 24/7 session tracking. Stock traders get proper market hours handling. Everyone gets institutional-grade analytics.

Anchor Period Options

The anchor period determines when VWAP resets and recalculates. You have three categories of options:

Time-Based Anchors:

Session - Resets at market open. Best for intraday stock trading where you want fresh VWAP each day.

Day - Resets at midnight UTC. Standard option for most traders.

Week / Month / Quarter / Year - Longer reset periods for swing traders and position traders who want broader context.

Rolling Window Anchors:

Rolling 5D - A sliding 5-day window that never resets. Solves the Monday problem where weekly VWAP equals daily VWAP on first day of week.

Rolling 21D - Approximately one month of trading data in continuous calculation. Excellent for crypto and forex markets that trade 24/7 without clear session breaks.

Event-Based Anchors:

Dividends - Resets on ex-dividend dates. Track institutional cost basis from dividend events.

Splits - Resets on stock split dates. Useful for analyzing post-split trading behavior.

Earnings - Resets on earnings report dates. See where volume-weighted trading occurred since last quarterly report.

Standard Deviation Bands

Three sets of bands surround the main VWAP line:

Band 1 (Aqua) - Plus and minus one standard deviation. Approximately 68% of price action occurs within this range under normal distribution. Touches suggest minor extension.

Band 2 (Fuchsia) - Plus and minus two standard deviations. Only 5% of trading should occur outside this range statistically. Touches here indicate significant overextension and high probability of mean reversion.

Band 3 (Purple) - Plus and minus three standard deviations. Touches are rare (0.3% probability) and represent extreme conditions. Often marks climax moves or panic selling/buying.

Each band can be toggled independently. Most traders show Band 1 by default and add Band 2 and 3 for specific setups or volatile instruments.

Multi-Timeframe VWAP System

The MTF section plots previous period VWAPs as horizontal support and resistance levels:

Daily VWAP - Previous day's final VWAP value. Key intraday reference level.

Weekly VWAP - Previous week's final VWAP. Important for swing traders.

Monthly VWAP - Previous month's final VWAP. Institutional benchmark level.

Quarterly VWAP - Previous quarter's final VWAP. Major support/resistance for position traders.