SMC N-Gram Probability Matrix [PhenLabs]📊 SMC N-Gram Probability Matrix

Version: PineScript™ v6

📌 Description

The SMC N-Gram Probability Matrix applies computational linguistics methodology to Smart Money Concepts trading. By treating SMC patterns as a discrete “alphabet” and analyzing their sequential relationships through N-gram modeling, this indicator calculates the statistical probability of which pattern will appear next based on historical transitions.

Traditional SMC analysis is reactive—traders identify patterns after they form and then anticipate the next move. This indicator inverts that approach by building a transition probability matrix from up to 5,000 bars of pattern history, enabling traders to see which SMC formations most frequently follow their current market sequence.

The indicator detects and classifies 11 distinct SMC patterns including Fair Value Gaps, Order Blocks, Liquidity Sweeps, Break of Structure, and Change of Character in both bullish and bearish variants, then tracks how these patterns transition from one to another over time.

🚀 Points of Innovation

First indicator to apply N-gram sequence modeling from computational linguistics to SMC pattern analysis

Dynamic transition matrix rebuilds every 50 bars for adaptive probability calculations

Supports bigram (2), trigram (3), and quadgram (4) sequence lengths for varying analysis depth

Priority-based pattern classification ensures higher-significance patterns (CHoCH, BOS) take precedence

Configurable minimum occurrence threshold filters out statistically insignificant predictions

Real-time probability visualization with graphical confidence bars

🔧 Core Components

Pattern Alphabet System: 11 discrete SMC patterns encoded as integers for efficient matrix indexing and transition tracking

Swing Point Detection: Uses ta.pivothigh/pivotlow with configurable sensitivity for non-repainting structure identification

Transition Count Matrix: Flattened array storing occurrence counts for all possible pattern sequence transitions

Context Encoder: Converts N-gram pattern sequences into unique integer IDs for matrix lookup

Probability Calculator: Transforms raw transition counts into percentage probabilities for each possible next pattern

🔥 Key Features

Multi-Pattern SMC Detection: Simultaneously identifies FVGs, Order Blocks, Liquidity Sweeps, BOS, and CHoCH formations

Adjustable N-Gram Length: Choose between 2-4 pattern sequences to balance specificity against sample size

Flexible Lookback Range: Analyze anywhere from 100 to 5,000 historical bars for matrix construction

Pattern Toggle Controls: Enable or disable individual SMC pattern types to customize analysis focus

Probability Threshold Filtering: Set minimum occurrence requirements to ensure prediction reliability

Alert Integration: Built-in alert conditions trigger when high-probability predictions emerge

🎨 Visualization

Probability Table: Displays current pattern, recent sequence, sample count, and top N predicted patterns with percentage probabilities

Graphical Probability Bars: Visual bar representation (█░) showing relative probability strength at a glance

Chart Pattern Markers: Color-coded labels placed directly on price bars identifying detected SMC formations

Pattern Short Codes: Compact notation (F+, F-, O+, O-, L↑, L↓, B+, B-, C+, C-) for quick pattern identification

Customizable Table Position: Place probability display in any corner of your chart

📖 Usage Guidelines

N-Gram Configuration

N-Gram Length: Default 2, Range 2-4. Lower values provide more samples but less specificity. Higher values capture complex sequences but require more historical data.

Matrix Lookback Bars: Default 500, Range 100-5000. More bars increase statistical significance but may include outdated market behavior.

Min Occurrences for Prediction: Default 2, Range 1-10. Higher values filter noise but may reduce prediction availability.

SMC Detection Settings

Swing Detection Length: Default 5, Range 2-20. Controls pivot sensitivity for structure analysis.

FVG Minimum Size: Default 0.1%, Range 0.01-2.0%. Filters insignificant gaps.

Order Block Lookback: Default 10, Range 3-30. Bars to search for OB formations.

Liquidity Sweep Threshold: Default 0.3%, Range 0.05-1.0%. Minimum wick extension beyond swing points.

Display Settings

Show Probability Table: Toggle the probability matrix display on/off.

Show Top N Probabilities: Default 5, Range 3-10. Number of predicted patterns to display.

Show SMC Markers: Toggle on-chart pattern labels.

✅ Best Use Cases

Anticipating continuation or reversal patterns after liquidity sweeps

Identifying high-probability BOS/CHoCH sequences for trend trading

Filtering FVG and Order Block signals based on historical follow-through rates

Building confluence by comparing predicted patterns with other technical analysis

Studying how SMC patterns typically sequence on specific instruments or timeframes

⚠️ Limitations

Predictions are based solely on historical pattern frequency and do not account for fundamental factors

Low sample counts produce unreliable probabilities—always check the Samples display

Market regime changes can invalidate historical transition patterns

The indicator requires sufficient historical data to build meaningful probability matrices

Pattern detection uses standardized parameters that may not capture all institutional activity

💡 What Makes This Unique

Linguistic Modeling Applied to Markets: Treats SMC patterns like words in a language, analyzing how they “flow” together

Quantified Pattern Relationships: Transforms subjective SMC analysis into objective probability percentages

Adaptive Learning: Matrix rebuilds periodically to incorporate recent pattern behavior

Comprehensive SMC Coverage: Tracks all major Smart Money Concepts in a unified probability framework

🔬 How It Works

1. Pattern Detection Phase

Each bar is analyzed for SMC formations using configurable detection parameters

A priority hierarchy assigns the most significant pattern when multiple detections occur

2. Sequence Encoding Phase

Detected patterns are stored in a rolling history buffer of recent classifications

The current N-gram context is encoded into a unique integer identifier

3. Matrix Construction Phase

Historical pattern sequences are iterated to count transition occurrences

Each context-to-next-pattern transition increments the appropriate matrix cell

4. Probability Calculation Phase

Current context ID retrieves corresponding transition counts from the matrix

Raw counts are converted to percentages based on total context occurrences

5. Visualization Phase

Probabilities are sorted and the top N predictions are displayed in the table

Chart markers identify the current detected pattern for visual reference

💡 Note:

This indicator performs best when used as a confluence tool alongside traditional SMC analysis. The probability predictions highlight statistically common pattern sequences but should not be used as standalone trading signals. Always verify predictions against price action context, higher timeframe structure, and your overall trading plan. Monitor the sample count to ensure predictions are based on adequate historical data.

Probability

Bayesian Order Flow Predictor📌 Bayesian Order Flow Predictor — Advanced Probability Engine for Nasdaq and Futures

This indicator is a next-generation probabilistic forecasting system designed for Nasdaq traders who rely on Order Flow, Auction Market Theory, Value Area dynamics, market structure, DOM imbalance, and Bayesian probability models.

It combines 7 professional-grade factors (DOM, CVD, RSI, EMA trend, ATR volatility, Market Structure, Value Area positioning) into a unified Bayesian probability panel that outputs a clean bullish/bearish probability curve with high-confidence reversal and trend-continuation signals.

Engineered for scalpers, day traders, futures traders, and ICT-style order flow technicians, it delivers real-time directional probability, session-aware signals, and optional news-filter exclusion.

⭐ Features

Bayesian Probability Model (0–100%)

DOM imbalance scoring across dynamic depth levels

Cumulative Volume Delta (CVD) scoring

Market structure detection (HH/LL micro-trend shifts)

RSI momentum and overbought/oversold scoring

EMA directional bias + ATR-normalized deviation

Value Area positioning (VAH / VAL / POC) with optional previous-session mode

Session filtering (only signals during active hours)

Automated news filter (exclude signals around scheduled macro events)

Bull/Bear probability zones with background coloring

Anti-repetition system (no double signals in same direction)

Designed for future scalping, futures order flow, and high-precision timing

🧠 Bayesian Probability Engine — How It Works

The model evaluates 7 independent market factors simultaneously:

DOM imbalance

CVD pressure

Market structure

RSI deviation

EMA trend

Value Area position

ATR volatility shift

Each factor is transformed into a normalized score, multiplied by its weighting parameter, and aggregated into a global score.

This score is then passed through a Bayesian logistic function to convert uncertainty into a smooth probability curve, giving traders a clean, mathematically stable, and noise-resistant forecast.

📈 Buy & Sell Signal Logic

Signals trigger when:

Bullish Probability crosses above the user threshold

Bearish Probability crosses below the opposite threshold

Session is active

No protected news event is occurring

This avoids noise, prevents over-signaling, and focuses only on high-confidence inflection points.

🎯Fully compatible with the indicator: ➡️ AI Probabilistic Orderflow scalper

Both indicators synchronize perfectly when used together:

Bayesian panel → trend probability

Scalper v1 → timing + TP/SL engine

Together they create a complete probability-driven revenue management system for scalping Future.

📘 How to Use

Add the indicator to your chart

Set your trading session (e.g., 09:30–16:00 EST)

Adjust weights depending on your style (Order Flow / Momentum / Value Area)

Watch the probability curve:

Above threshold → bullish bias

Below threshold → bearish bias

Take signals when the curve crosses thresholds, not when flat

Combine with "AI Probabilistic Orderflow scalper" indicator for execution timing

Avoid high-impact news using the News Filter

💎 Advantages

Professional-grade Bayesian model

Works in all volatility regimes

Noise-resistant and smoother than traditional oscillators

Integrates Order Flow + Auction Theory + Momentum + Volatility

Perfect for NQ scalpers seeking an AI-style probability dashboard

Reduces emotional decision-making

Compatible with any execution strategy

Optimized for high winrate scalping and sniper entries

AI Probabilistic OrderFlow Scalper⭐ Description:

📌 AI Probabilistic OrderFlow Scalper

This script combines Order Flow, Auction Market Theory, Volume Imbalance, Market Structure (HH/LL), RSI bias filtering, and a probability-based direction model inspired by AI and statistics.

It produces high-precision scalping entries designed for fast markets such as Futures, while remaining compatible with all markets (indices, crypto, forex, metals).

This is not a typical indicator — it is a probabilistic predictive model engineered to provide sniper entries, a tick-based Take Profit, a volatility-adaptive ATR Stop Loss, and optional Value Area levels (VAH/VAL/POC).

⭐ Main Features:

🔥 Directional probability model (AI-style weighted scoring)

📊 Order Flow imbalance (delta-like logic)

📈 HH/LL market structure detection

🎯 Smart RSI bias filter

🚀 One signal per trend shift (anti-spam)

🎯 Tick-based Take Profit (perfect for NQ / futures)

🛡️ ATR-based dynamic Stop Loss

📉 Value Area display: VAH, VAL, POC

🔊 Volume confirmation filter

📡 Directional probability plot

✔️ Works for Futures, Crypto, Forex, Indices

🧠 Probabilistic AI Approach

The model uses a 3-factor scoring system:

Order Flow imbalance

Market structure (HH/LL)

RSI trend bias

Each validated condition = 1 point.

The total score is converted into Buy/Sell probabilities, and the higher-probability direction is selected.

When probability exceeds the threshold (e.g. 80%), the system triggers a high-confidence sniper signal.

This mirrors Revenue Management logic:

→ Only take a decision when probability of success is maximized.

🎯 Buy/Sell Signals (Sniper Entries)

🔵 Green triangle under the candle = high-probability Buy

🔴 Red triangle above the candle = high-probability Sell

✔️ Only one signal per directional shift

✔️ Signals appear only when all strict filters are satisfied

📌 Automatic TP / SL

TP: fixed tick-based (e.g. 100 ticks for NQ scalping)

SL: ATR-based, adapts to volatility

TP/SL display can be enabled or disabled

Perfectly calibrated for high-speed scalping.

📘 How to Use

Use on every timeframe

Adjust probability threshold (75–90 recommended)

Enable strict mode for maximum precision

Let the model filter entries automatically

Choose a TP suitable for your market

Optionally display VAH/VAL/POC for Auction Theory context

Always test using backtesting before going live

🏆 Advantages

Extremely fast for scalping

High win-rate potential via probabilistic filtering

Clean signals (no noise or spam)

Combines the strongest trading frameworks:

Order Flow

Market Structure

Statistical modeling

Volume profiling

Automated risk management

Dynamic Breakout Odds [RayAlgo]█ OVERVIEW

Dynamic Breakout Odds is a probability-based breakout tool that uses ATR and pattern matching to estimate how likely price is to expand up or down from the current candle.

Instead of guessing, the indicator scans historical candles that look like the current one and measures how often price broke above or below by a volatility-based amount.

It then projects those probabilities forward as clean levels and a bias dashboard on your chart.

Use it to quickly answer:

• “Is the next move statistically more likely up or down?”

• “How far does price typically travel from here, in ATR terms?”

█ CONCEPTS

Candle Profile Matching

The script builds a “profile” of the current setup using two elements:

• The color of the previous candle (bullish close vs bearish close)

• The trend environment (above/below EMA, if the filter is enabled)

Only historical candles with the same profile are used for statistics. This keeps the probabilities specific to the current context instead of mixing all market conditions together.

ATR-Based Expansion

For every matching historical candle, the script checks how far price moved away from the open using ATR:

• Upward move thresholds

• Moderate expansion (≈ 0.5 ATR above the open)

• Stronger expansion (≈ 1.0 ATR above the open)

• Downward move thresholds

• Moderate expansion (≈ 0.5 ATR below the open)

• Stronger expansion (≈ 1.0 ATR below the open)

It counts how often each expansion happened, then converts those counts into probabilities.

Normalized Probability Scores

The indicator doesn’t just show raw percentages; it normalizes them so that all scenarios together form a consistent probability set.

Internally it tracks four outcomes for similar candles:

• Chance of a moderate move upward

• Chance of a strong move upward

• Chance of a moderate move downward

• Chance of a strong move downward

These are then normalized so the total is roughly 100%. From this, two main metrics are derived:

• Bullish Strength = combined normalized odds of upside moves

• Bearish Strength = combined normalized odds of downside moves

Whichever side has the higher score defines the current directional bias .

█ WHAT YOU SEE ON THE CHART

1. Breakout Projection Levels

Four horizontal levels are projected around the open of the current bar:

• Two upside levels

• Nearer upside expansion (~0.5 ATR above the open)

• Further upside expansion (~1.0 ATR above the open)

• Two downside levels

• Nearer downside expansion (~0.5 ATR below the open)

• Further downside expansion (~1.0 ATR below the open)

Each line extends a configurable number of bars into the future, so you visually see a breakout “corridor” above and below price.

2. Probability Labels

At the right edge of each line, you’ll see a label such as:

• “X% – near upside”

• “Y% – further downside”

These labels tell you how frequently similar candles in the chosen lookback reached that expansion. You immediately know which scenario has been more common historically.

3. Breakout Zones

Between the paired upside lines and the paired downside lines, shaded “probability zones” can be shown:

• The upper shaded band highlights the typical upside expansion range

• The lower shaded band highlights the typical downside expansion range

These zones visually group probable target areas instead of just single lines.

4. Background Tint

The background behind price is softly tinted towards:

• Bullish color when Bullish Strength > Bearish Strength

• Bearish color when Bearish Strength > Bullish Strength

The stronger the statistical imbalance between the two, the more pronounced the tint. This gives you an instant feel for whether conditions lean more Long, more Short, or are nearly Neutral.

5. Directional Bias Arrow

On the last bar the script can plot a clean arrow:

• Up-arrow below price when bullish odds dominate

• Down-arrow above price when bearish odds dominate

The arrow is positioned beyond all projection lines, making it easy to see even on cluttered charts and reminding you of the current statistical bias without text.

6. Origin Marker

A small horizontal mark is drawn at the open of the current candle.

This acts as the “starting point” from which all ATR-based expansions above and below are measured.

7. Dashboard Panel

A compact dashboard is drawn in a corner of the chart (location configurable). It displays:

• Bullish Strength – combined normalized probability for upside expansions

• Bearish Strength – combined normalized probability for downside expansions

• Bias – “Long Bias”, “Short Bias”, or “Neutral”

• Trend Filter – shows whether EMA-based filtering is ON or OFF and which length is used

This gives you a quick, text-based summary of the current statistical environment.

█ SETTINGS

Analysis Lookback Period

• Controls how many historical bars the script inspects when searching for similar candles.

• Larger values = more history, smoother statistics, slower adaptation.

• Smaller values = faster adaptation, but more noise and less stability.

ATR Length

• The period used to compute ATR volatility.

• Defines how “big” 0.5 ATR and 1.0 ATR moves are on your current symbol and timeframe.

Trend Filter (EMA)

• Filter by Trend?

• When ON, only historical candles in a similar trend regime are used.

• When OFF, all past candles with similar color are considered, regardless of trend.

• Trend EMA Length

• EMA period used to classify trend.

• Price above EMA → uptrend environment.

• Price below EMA → downtrend environment.

This filter helps you separate behavior in uptrends from downtrends, which can significantly change breakout dynamics.

Visual Settings

• Projection Width (bars)

• How far the lines and zones extend into the future.

• Show Probability Zones

• Toggle shaded bands between each pair of levels.

• Label Size

• Choose smaller or larger text for the probability labels on the right.

• Tint Background by Bias

• Turn the bias-based background on or off.

• Show Bias Marker on Last Candle

• Toggle the up/down arrow marker.

• Dashboard Location

• Select top/bottom left/right corner for the panel.

█ HOW TO USE IT

1. Start With the Dashboard

Look at Bullish Strength vs Bearish Strength:

• If bullish is clearly larger → environment statistically favors upside expansion.

• If bearish is clearly larger → environment statistically favors downside expansion.

• If they are close → treat the situation as Neutral; consider reducing position size or waiting for more clarity.

2. Use Levels as Dynamic Targets

The projected lines and zones can serve as:

• Profit targets based on typical expansion distance

• Logical regions for scaling out

• Areas where you expect price behavior to change (e.g., loss of momentum)

Short-term traders often focus on the nearer expansion levels, while swing traders may use the farther levels as extended targets.

3. Align With Trend (Optional)

With the trend filter ON:

• Prefer Long setups when price is above the EMA and bullish probabilities dominate.

• Prefer Short setups when price is below the EMA and bearish probabilities dominate.

With the filter OFF, you get pure color-plus-pattern statistics across the whole lookback, which can be useful if you deliberately trade counter-trend or range conditions.

4. Combine With Your Existing System

Dynamic Breakout Odds is best used as a confirmation and targeting layer :

• Combine it with structure (support/resistance, supply/demand, order blocks).

• Combine it with volume or orderflow tools if you use them.

• Use the probability zones to validate whether your planned target is realistic relative to recent volatility.

It is not designed to be a standalone “buy/sell” signal generator, but a statistical map around your entries.

█ PRACTICAL EXAMPLES

Example A – Bullish, Moderate Expansion Frequently Hit

• Bullish Strength significantly higher than Bearish Strength.

• The nearer upside level shows a strong historical hit rate.

Interpretation: similar setups often produce at least a moderate push upward before failing.

Use case: trade pullbacks in the direction of the bias, targeting the nearer upside projection as an initial take-profit.

Example B – Bearish, Deeper Downside Often Reached

• Bearish Strength clearly dominant.

• Both the nearer and farther downside levels show decent probabilities.

Interpretation: similar conditions historically saw follow-through to the downside.

Use case: use rallies against the direction of the bias to position into shorts, planning partial exits around the first downside projection and runners toward the second.

Example C – Neutral, Balanced Probabilities

• Bullish and Bearish Strength scores are close.

• Background tint is very light or absent.

Interpretation: the market is statistically indecisive; expansions up or down are similarly likely.

Use case: consider range trading tactics, mean-reversion ideas, or simply standing aside until a clearer skew develops.

█ BEST PRACTICES

• Use on liquid symbols and reasonable timeframes to avoid distorted ATR behavior.

• Don’t overfit lookback length to a single instrument; test across markets.

• Let the indicator provide context, not absolute certainty.

• Always combine with proper risk management (position sizing, max loss per trade, etc.).

• Be cautious with very small sample sizes (e.g., very short lookbacks on low-volume assets).

█ LIMITATIONS & NOTES

• All probabilities are based on historical behavior ; markets can change regime.

• ATR distances are relative to recent volatility and may shrink/expand over time.

• The script intentionally does not guarantee any direction or target; it only reports what has been most common in similar past situations.

█ DISCLAIMER

This tool is for educational and informational purposes only.

It does not constitute financial advice or a guarantee of performance.

Always do your own research, test on demo or historical data, and use appropriate risk management when trading live capital.

Per Bak Self-Organized CriticalityTL;DR: This indicator measures market fragility. It measures the system's vulnerability to cascade failures and phase transitions. I've added four independent stress vectors: tail risk, volatility regime, credit stress, and positioning extremes. This allows us to quantify how susceptible markets are to disproportionate moves from small shocks, similar to how a steep sandpile is primed for avalanches.

Avalanches, forest fires, earthquakes, pandemic outbreaks, and market crashes. What do they all have in common? They are not random.

These events follow power laws - stable systems that naturally evolve toward critical states where small triggers can unleash catastrophic cascades.

For example, if you are building a sandpile, there will be a point with a little bit additional sand will cause a landslide.

Markets build fragility grain by grain, like a sandpile approaching avalanche.

The Per Bak Self-Organized Criticality (SOC) indicator detects when the markets are a few grains away from collapse.

This indicator is highly inspired by the work of Per Bak related to the science of self-organized criticality .

As Bak said:

"The earthquake does not 'know how large it will become'. Thus, any precursor state of a large event is essentially identical to a precursor state of a small event."

For markets, this means:

We cannot predict individual crash size from initial conditions

We can predict statistical distribution of crashes

We can identify periods of increased systemic risk (proximity to critical state)

BTW, this is a forwarding looking indicator and doesn't reprint. :)

The Story of Per Bak

In 1987, Danish physicist Per Bak and his colleagues discovered an important pattern in nature: self-organized criticality.

Their sandpile experiment revealed something: drop grains of sand one by one onto a pile, and the system naturally evolves toward a critical state. Most grains cause nothing. Some trigger small slides. But occasionally a single grain triggers a massive avalanche.

The key insight is that we cannot predict which grain will trigger the avalanche, but you can measure when the pile has reached a critical state.

Why Markets Are the Ultimate SOC System?

Financial markets exhibit all the hallmarks of self-organized criticality:

Interconnected agents (traders, institutions, algorithms) with feedback loops

Non-linear interactions where small events can cascade through the system

Power-law distributions of returns (fat tails, not normal distributions)

Natural evolution toward fragility as leverage builds, correlations tighten, and positioning crowds

Phase transitions where calm markets suddenly shift to crisis regimes

Mathematical Foundation

Power Law Distributions

Traditional finance assumes returns follow a normal distribution. "Markets return 10% on average." But I disagree. Markets follow power laws:

P(x) ∝ x^(-α)

Where P(x) is the probability of an event of size x, and α is the power law exponent (typically 3-4 for financial markets).

What this means: Small moves happen constantly. Medium moves are less frequent. Catastrophic moves are rare but follow predictable probability distributions. The "fat tails" are features of critical systems.

Critical Slowing Down

As systems approach phase transitions, they exhibit critical slowing down—reduced ability to absorb shocks. Mathematically, this appears as:

τ ∝ |T - T_c|^(-ν)

Where τ is the relaxation time, T is the current state, T_c is the critical threshold, and ν is the critical exponent.

Translation: Near criticality, markets take longer to recover from perturbations. Fragility compounds.

Component Aggregation & Non-Linear Emergence

The Per Bak SOC our index aggregates four normalized components (each scaled 0-100) with tunable weights:

SOC = w₁·C_tail + w₂·C_vol + w₃·C_credit + w₄·C_position

Default weights (you can change this):

w₁ = 0.34 (Tail Risk via SKEW)

w₂ = 0.26 (Volatility Regime via VIX term structure)

w₃ = 0.18 (Credit Stress via HYG/LQD + TED spread)

w₄ = 0.22 (Positioning Extremes via Put/Call ratio)

Each component uses percentile ranking over a 252-day lookback combined with absolute thresholds to capture both relative regime shifts and extreme absolute levels.

The Four Pillars Explained

1. Tail Risk (SKEW Index)

Measures options market pricing of fat-tail events. High SKEW indicates elevated outlier probability.

C_tail = 0.7·percentrank(SKEW, 252) + 0.3·((SKEW - 115)/0.5)

2. Volatility Regime (VIX Term Structure)

Combines VIX level with term structure slope. Backwardation signals acute stress.

C_vol = 0.4·VIX_level + 0.35·VIX_slope + 0.25·VIX_ratio

3. Credit Stress (HYG/LQD + TED Spread)

Tracks high-yield deterioration versus investment-grade and interbank lending stress.

C_credit = 0.65·percentrank(LQD/HYG, 252) + 0.35·(TED/0.75)·100

4. Positioning Extremes (Put/Call Ratio)

Detects extreme hedging demand through percentile ranking and z-score analysis.

C_position = 0.6·percentrank(P/C, 252) + 0.4·zscore_normalized

What the Indicator Really Measures?

Not Volatility but Fragility

Markets Going Down ≠ Fragility Building (actually when markets go down, risk and fragility are released)

The 0-100 Scale & Regime Thresholds

The indicator outputs a 0-100 fragility score with four regimes:

🟢 Safe (0-39): System resilient, can absorb normal shocks

🟡 Building (40-54): Early fragility signs, watch for deterioration

🟠 Elevated (55-69): System vulnerable

🔴 Critical (70-100): Highly susceptible to cascade failures

Further Reading for Nerds

Bak, P., Tang, C., & Wiesenfeld, K. (1987). "Self-organized criticality: An explanation of 1/f noise." Physical Review Letters.

Bak, P. & Chen, K. (1991). "Self-organized criticality." Scientific American.

Bak, P. (1996). How Nature Works: The Science of Self-Organized Criticality. Copernicus.

Feedback is appreciated :)

Weighted KDE Mode🙏🏻 The ‘ultimate’ typical value estimator, for the highest computational cost @ time complexity O(n^2). I am not afraid to say: this is the last resort BFG9000 you can ‘ever’ get to make dem market demons kneel before y’all

Quickguide

pls read it, you won’t find it anywhere else in open access

When to use:

If current market activity is so crazy || things on your charts are really so bad (contaminated data && (data has very heavy tails || very pronounced peak)), the only option left is to use the peak (mode) of Kernel Density Estimate , instead of median not even mentioning mean. So when WMA won’t help, when WPNR won’t help, you need this thing.

Setting it up:

Interval: choose what u need, you can use usual moving windows, but I also added yearly and session anchors alike in old VWAP (always prefer 24h instead of Session if your plan allows). Other options like cumulative window are also there.

Parameters: this script ain't no joke, it needs time to make calculations, so I added a setting to calculate only for the last N bars (when “starting at bar N” is put on 0). If it’s not zero it acts as a starting point after which the calculations happen (useful for backtesting). Other parameters keep em as they are, keep student5 kernel , turn off appropriate weights if u apply it to other than chart data, on other studies etc.

But instead of listening to me just experiment with parameters and see what they change, would take 5 mins max

Been always saying that VWAP is ish, not time-aware etc, volume info is incorporated in a lil bit wrong way… So I decided not just to fix VWAP (you can do it yourself in 5 mins), but instead to drop there the Ultimate xD typical value estimator that is ever possible to do. Time aware, volume / inferred volume aware, resistant to all kinds of BS. This is your shieldwall.

How it works:

You can easily do a weighted kernel density estimation, in our case including temporal and intensity information while accumulating densities. Here are some details worth mentioning about the thing:

Kernels are raw (not unit variance), that’s easier to work with later.

h_constants for each kernel were calculated ^^ given that ^^ with python mpmath module with high decimal precision.

In bandwidth calculation instead of using empirical standard deviation as a scaler, I use... ta.range(src, len) / math.sqrt(12)

...that takes data range and converts it to standard deviation, assuming data is uniformly distributed. That’s exactly what we need: a scaler that is coherent with the KDE, that has nothing to do with stdevs, as the kernels except for gaussian ones (that we don’t even need to use). More importantly, if u take multiple windows and see over time which distro they approach on the long term, that would be the uniform one (not the normal one as many think). Sometimes windows are multimodal, sometimes Laplace like etc, so in general all together they are uniform ish.

The one and only kernel you really need is Student t with v = 5 , for the use case I highlighted in the first part of the post for TV users. It’s as far as u can get until ish becomes crazy like undefined variance etc. It has the highest kurtosis = 9 of all distros, perfect for the real use case I mentioned. Otherwise, you don’t even need KDE 4 real, but still I included other senseful kernels for comparison or in case I am trippin there.

Btw, don’t believe in all that hype about Epanechnikov kernel which in essence is made from beta distribution with alpha = beta = 2, idk why folk call it with that weird name, it’s beta2 kernel. Yes on papers it really minimises AMISE (that’s how I calculated h constants for all dem kernels in the script), but for really crazy data (proper use case for us), it ain't provides even ‘closely’ compared with student5 kernel. Not much else to add.

Shout out to @RicardoSantos for inspiration, I saw your KDE script a long time ago brotha, finna got my hands on it.

∞

Institutional Edge Pro v1.0 - 9.3/10 ConfidenceEducational 5-layer confirmation system combining institutional order flow concepts, trend analysis, and risk management principles. Features Order Block detection, adaptive stop losses (EMA 9x21), and probability scoring. For educational purposes only.

## ⚡ KEY FEATURES

### 🔍 5-Layer Confirmation System

- **Layer 0:** Market Regime Detection (30% weight) - ADX, Choppiness Index, Volatility, Volume

- **Layer 1:** Golden/Death Cross Trend Filter (20% weight) - EMA 50/200 with gradient confirmation

- **Layer 1.5:** Fast Death Cross Stop Loss - EMA 9/21 dynamic exits

- **Layer 2:** Smart Order Block Detection (20% weight) - Institutional footprint tracking

- **Layer 3:** Probabilistic Confirmations (20% weight) - RSI, MACD, Volume, Structure, Volatility

- **Layer 4:** Dynamic Risk Management (10% weight) - ATR-based adaptive stops

### 📊 Visual Dashboard

- **Regime Score:** 0-100 market health indicator

- **Trend Status:** Real-time BULL/BEAR/NONE classification

- **Trend Quality:** Freshness metric (degrades over time)

- **Order Block Status:** Active OB tracking with validation

- **Probability Scores:** Live Long/Short setup probabilities

NBarForwardOdds# N Bar Forward Odds

## Description

Calculates the probability of a closing price exceeding a closing price at a specified interval away from the

current bar. It does this by iterating through a series of intervals (1 to 20) and determining if the closing

price of the current bar is greater than the closing price of the bar at that interval.

## Usage:

Selectable base interval from the input configuration panel is calculated with a value step in a range `1:20` to get the final interval displayed.

APXTradez - Swing Overlay🔹 APX Swing Overlay – Summary & Usage Guide

Purpose

The APX Swing Overlay is built for options swing traders who focus on 1–5 day directional moves.

It visually identifies trend strength, compression zones, and momentum buildup using a combination of EMAs, Bollinger Bands, and Keltner Channels — making it ideal for spotting breakouts early.

Core Components

8 EMA (Exponential Moving Average)

- Tracks short-term price action and momentum.

- Price above = bullish continuation; price below = short-term weakness.

- Acts as the first dynamic support/resistance level.

21 EMA

- Captures the mid-term trend (confirmation layer).

- When the 8 EMA crosses above the 21 EMA → bullish shift.

- When the 8 EMA crosses below the 21 EMA → bearish or consolidation signal.

Bollinger Bands (BB)

- Measures volatility around price.

- When the bands tighten, volatility is compressing → expect expansion soon.

- When the bands expand, volatility is releasing → breakout or breakdown in play.

Keltner Channels (KC)

- Uses ATR to show “normal” price movement range.

- When Bollinger Bands move inside the Keltner Channels, it signals a squeeze — price is coiling up for a potential breakout.

- Compression Highlights

- The overlay visually marks when BB are inside KC (low volatility squeeze).

- These zones are shaded or highlighted so you can easily see when a stock is building pressure.

- Once price exits that zone with momentum, it often begins a new swing leg.

How to Use It

Add to Chart : Apply the APX Swing Overlay on your daily or 4-hour timeframe.

Look for Compression:

- Watch for areas where the bands tighten and the compression highlight appears.

- This means volatility is low — expect an expansion soon.

- Wait for Expansion + EMA Confirmation:

- A breakout above both the 8 & 21 EMA, with bands expanding, signals a potential long swing.

- A breakdown below both EMAs with expanding bands signals potential short swing.

Ride the Trend:

- Stay in the trade as long as price respects the 8 EMA.

- Take profit when momentum slows or the 8 crosses back below the 21 EMA.

Best Timeframes

Daily Chart → Ideal for swing setups (2–5 day hold).

4H Chart → Good for early entry timing and breakout confirmation.

Quick Visual Interpretation

Signal Meaning

8 > 21 and expanding BB Bullish trend continuation

8 < 21 and expanding BB Bearish continuation

BB inside KC Volatility squeeze forming

Highlighted compression zone Potential pre-breakout setup

Price closing above 8/21 Confirmation to enter

Quantum Market Harmonics [QMH]# Quantum Market Harmonics - TradingView Script Description

## 📊 OVERVIEW

Quantum Market Harmonics (QMH) is a comprehensive multi-dimensional trading indicator that combines four independent analytical frameworks to generate high-probability trading signals with quantifiable confidence scores. Unlike simple indicator combinations that display multiple tools side-by-side, QMH synthesizes temporal analysis, inter-market correlations, behavioral psychology, and statistical probabilities into a unified confidence scoring system that requires agreement across all dimensions before generating a confirmed signal.

---

## 🎯 WHAT MAKES THIS SCRIPT ORIGINAL

### The Core Innovation: Weighted Confidence Scoring

Most indicators provide binary signals (buy/sell) or display multiple indicators separately, leaving traders to interpret conflicting information. QMH's originality lies in its weighted confidence scoring system that:

1. **Combines Four Independent Methods** - Each framework (described below) operates independently and contributes points to an overall confidence score

2. **Requires Multi-Dimensional Agreement** - Signals only fire when multiple frameworks align, dramatically reducing false positives

3. **Quantifies Signal Strength** - Every signal includes a numerical confidence rating (0-100%), allowing traders to filter by quality

4. **Adapts to Market Conditions** - Different market regimes activate different component combinations

### Why This Combination is Useful

Traditional approaches suffer from:

- **Single-dimension bias**: RSI shows oversold, but trend is still down

- **Conflicting signals**: MACD says buy, but volume is weak

- **No prioritization**: All signals treated equally regardless of strength

QMH solves these problems by requiring multiple independent confirmations and weighting each component's contribution to the final signal. This multi-dimensional approach mirrors how professional traders analyze markets - not relying on one indicator, but waiting for multiple pieces of evidence to align.

---

## 🔬 THE FOUR ANALYTICAL FRAMEWORKS

### 1. Temporal Fractal Resonance (TFR)

**What It Does:**

Analyzes trend alignment across four different timeframes simultaneously (15-minute, 1-hour, 4-hour, and daily) to identify periods of multi-timeframe synchronization.

**How It Works:**

- Uses `request.security()` with `lookahead=barmerge.lookahead_off` to retrieve confirmed price data from each timeframe

- Calculates "fractal strength" for each timeframe using this formula:

```

Fractal Strength = (Rate of Change / Standard Deviation) × 100

```

This creates a momentum-to-volatility ratio that measures trend strength relative to noise

- Computes a Resonance Index when all four timeframes show the same directional bias

- The index averages the absolute strength values when all timeframes align

**Why This Method:**

Fractal Market Hypothesis suggests that price patterns repeat across different time scales. When trends align from short-term (15m) to long-term (Daily), the probability of trend continuation increases substantially. The momentum/volatility ratio filters out low-conviction moves where volatility dominates direction.

**Contribution to Confidence Score:**

- TFR Bullish = +25 points

- TFR Bearish = +25 points (to bearish confidence)

- No alignment = 0 points

---

### 2. Cross-Asset Quantum Entanglement (CAQE)

**What It Does:**

Analyzes correlation patterns between the current asset and three reference markets (Bitcoin, US Dollar Index, and Volatility Index) to identify both normal correlation behavior and anomalous breakdowns that often precede significant moves.

**How It Works:**

- Retrieves price data from BTC (BINANCE:BTCUSDT), DXY (TVC:DXY), and VIX (TVC:VIX) using confirmed bars

- Calculates Pearson correlation coefficient between the main asset and each reference:

```

Correlation = Covariance(X,Y) / (StdDev(X) × StdDev(Y))

```

- Computes an Intermarket Pressure Index by weighting each reference asset's momentum by its correlation strength:

```

Pressure = (Corr₁ × ROC₁ + Corr₂ × ROC₂ + Corr₃ × ROC₃) / 3

```

- Detects "correlation breakdowns" when average correlation drops below 0.3

**Why This Method:**

Markets don't operate in isolation. Inter-market analysis (developed by John Murphy) recognizes that:

- Crypto assets often correlate with Bitcoin

- Risk assets inversely correlate with VIX (fear gauge)

- Dollar strength affects commodity and crypto prices

When these normal correlations break down, it signals potential regime changes. The term "quantum" reflects the interconnected nature of these relationships - like quantum entanglement where distant particles influence each other.

**Contribution to Confidence Score:**

- CAQE Bullish (positive pressure, stable correlations) = +25 points

- CAQE Bearish (negative pressure, stable correlations) = +25 points (to bearish)

- Correlation breakdown = Warning marker (potential reversal zone)

---

### 3. Adaptive Market Psychology Matrix (AMPM)

**What It Does:**

Classifies the current market emotional state into six distinct categories by analyzing the interaction between momentum (RSI), volume behavior, and volatility acceleration (ATR change).

**How It Works:**

The system evaluates three metrics:

1. **RSI (14-period)**: Measures overbought/oversold conditions

2. **Volume Analysis**: Compares current volume to 20-period average

3. **ATR Rate of Change**: Detects volatility acceleration

Based on these inputs, the market is classified into:

- **Euphoria**: RSI > 80, volume spike present, volatility rising (extreme bullish emotion)

- **Greed**: RSI > 70, normal volume (moderate bullish emotion)

- **Neutral**: RSI 40-60, declining volatility (balanced state)

- **Fear**: RSI 40-60, low volatility (uncertainty without panic)

- **Panic**: RSI < 30, volume spike present, volatility rising (extreme bearish emotion)

- **Despair**: RSI < 20, normal volume (capitulation phase)

**Why This Method:**

Behavioral finance principles (Kahneman, Tversky) show that markets follow predictable emotional cycles. Extreme psychological states often mark reversal points because:

- At Euphoria/Greed peaks, everyone bullish has already bought (no buyers left)

- At Panic/Despair bottoms, everyone bearish has already sold (no sellers left)

AMPM provides contrarian signals at these extremes while respecting trends during Fear and Greed intermediate states.

**Contribution to Confidence Score:**

- Psychology Bullish (Panic/Despair + RSI < 35) = +15 points

- Psychology Bearish (Euphoria/Greed + RSI > 65) = +15 points

- Neutral states = 0 points

---

### 4. Time-Decay Probability Zones (TDPZ)

**What It Does:**

Creates dynamic support and resistance zones based on statistical probability distributions that adapt to changing market volatility, similar to Bollinger Bands but with enhancements for trend environments.

**How It Works:**

- Calculates a 20-period Simple Moving Average as the basis line

- Computes standard deviation of price over the same period

- Creates four probability zones:

- **Extreme Upper**: Basis + 2.5 standard deviations (≈99% probability boundary)

- **Upper Zone**: Basis + 1.5 standard deviations

- **Lower Zone**: Basis - 1.5 standard deviations

- **Extreme Lower**: Basis - 2.5 standard deviations (≈99% probability boundary)

- Dynamically adjusts zone width based on ATR (Average True Range):

```

Adjusted Upper = Upper Zone + (ATR × adjustment_factor)

Adjusted Lower = Lower Zone - (ATR × adjustment_factor)

```

- The adjustment factor increases during high volatility, widening the zones

**Why This Method:**

Traditional support/resistance levels are static and don't account for volatility regimes. TDPZ zones are probability-based and mean-reverting:

- Price has ≈99% probability of staying within extreme zones in normal conditions

- Touches to extreme zones represent statistical outliers (high-probability reversal opportunities)

- Zone expansion/contraction reflects volatility regime changes

- ATR adjustment prevents false signals during unusual volatility

The "time-decay" concept refers to mean reversion - the further price moves from the basis, the higher the probability of eventual return.

**Contribution to Confidence Score:**

- Price in Lower Extreme Zone = +15 points (bullish reversal probability)

- Price in Upper Extreme Zone = +15 points (bearish reversal probability)

- Price near basis = 0 points

---

## 🎯 HOW THE CONFIDENCE SCORING SYSTEM WORKS

### Signal Generation Formula

QMH calculates separate Bullish and Bearish confidence scores each bar:

**Bullish Confidence (0-100%):**

```

Base Score: 20 points

+ TFR Bullish: 25 points (if all 4 timeframes aligned bullish)

+ CAQE Bullish: 25 points (if intermarket pressure positive)

+ AMPM Bullish: 15 points (if Panic/Despair contrarian signal)

+ TDPZ Bullish: 15 points (if price in lower probability zones)

─────────

Maximum Possible: 100 points

```

**Bearish Confidence (0-100%):**

```

Base Score: 20 points

+ TFR Bearish: 25 points (if all 4 timeframes aligned bearish)

+ CAQE Bearish: 25 points (if intermarket pressure negative)

+ AMPM Bearish: 15 points (if Euphoria/Greed contrarian signal)

+ TDPZ Bearish: 15 points (if price in upper probability zones)

─────────

Maximum Possible: 100 points

```

### Confirmed Signal Requirements

A **QBUY** (Quantum Buy) signal generates when:

1. Bullish Confidence ≥ User-defined threshold (default 60%)

2. Bullish Confidence > Bearish Confidence

3. No active sell signal present

A **QSELL** (Quantum Sell) signal generates when:

1. Bearish Confidence ≥ User-defined threshold (default 60%)

2. Bearish Confidence > Bullish Confidence

3. No active buy signal present

### Why This Approach Is Different

**Example Comparison:**

Traditional RSI Strategy:

- RSI < 30 → Buy signal

- Result: May buy into falling knife if trend remains bearish

QMH Approach:

- RSI < 30 → Psychology shows Panic (+15 points)

- But requires additional confirmation:

- Are all timeframes also showing bullish reversal? (+25 points)

- Is intermarket pressure turning positive? (+25 points)

- Is price at a statistical extreme? (+15 points)

- Only when total ≥ 60 points does a QBUY signal fire

This multi-layer confirmation dramatically reduces false signals while maintaining sensitivity to genuine opportunities.

---

## 🚫 NO REPAINT GUARANTEE

**QMH is designed to be 100% repaint-free**, which is critical for honest backtesting and reliable live trading.

### Technical Implementation:

1. **All Multi-Timeframe Data Uses Confirmed Bars**

```pinescript

tf1_close = request.security(syminfo.tickerid, "15", close , lookahead=barmerge.lookahead_off)

```

Using `close ` instead of `close ` ensures we only reference the previous confirmed bar, not the current forming bar.

2. **Lookahead Prevention**

```pinescript

lookahead=barmerge.lookahead_off

```

This parameter prevents the function from accessing future data that wouldn't be available in real-time.

3. **Signal Timing**

Signals appear on the bar AFTER all conditions are met, not retroactively on the bar where conditions first appeared.

### What This Means for Users:

- **Backtest Accuracy**: Historical signals match exactly what you would have seen in real-time

- **No Disappearing Signals**: Once a signal appears, it stays (though price may move against it)

- **Honest Performance**: Results reflect true predictive power, not hindsight optimization

- **Live Trading Reliability**: Alerts fire at the same time signals appear on the chart

The dashboard displays "✓ NO REPAINT" to confirm this guarantee.

---

## 📖 HOW TO USE THIS INDICATOR

### Basic Trading Strategy

**For Trend Followers:**

1. **Wait for Signal Confirmation**

- QBUY label appears below a bar = Confirmed bullish entry opportunity

- QSELL label appears above a bar = Confirmed bearish entry opportunity

2. **Check Confidence Score**

- 60-70%: Moderate confidence (consider smaller position size)

- 70-85%: High confidence (standard position size)

- 85-100%: Very high confidence (consider larger position size)

3. **Enter Trade**

- Long entry: Market or limit order near signal bar

- Short entry: Market or limit order near signal bar

4. **Set Targets Using Probability Zones**

- Long trades: Target the adjusted upper zone (lime line)

- Short trades: Target the adjusted lower zone (red line)

- Alternatively, target the basis line (yellow) for conservative exits

5. **Set Stop Loss**

- Long trades: Below recent swing low minus 1 ATR

- Short trades: Above recent swing high plus 1 ATR

**For Mean Reversion Traders:**

1. **Wait for Extreme Zones**

- Price touches extreme lower zone (dotted red line below)

- Price touches extreme upper zone (dotted lime line above)

2. **Confirm with Psychology**

- At lower extreme: Look for Panic or Despair state

- At upper extreme: Look for Euphoria or Greed state

3. **Wait for Confidence Build**

- Monitor dashboard until confidence exceeds threshold

- Requires patience - extreme touches don't always reverse immediately

4. **Enter Reversal**

- Target: Return to basis line (yellow SMA 20)

- Stop: Beyond the extreme zone

**For Position Traders (Longer Timeframes):**

1. **Use Daily Timeframe**

- Set chart to daily for longer-term signals

- Signals will be less frequent but higher quality

2. **Require High Confidence**

- Filter setting: Min Confidence Score 80%+

- Only take the strongest multi-dimensional setups

3. **Confirm with Resonance Background**

- Green tinted background = All timeframes bullish aligned

- Red tinted background = All timeframes bearish aligned

- Only enter when background tint matches signal direction

4. **Hold for Major Targets**

- Long trades: Hold until extreme upper zone or opposite signal

- Short trades: Hold until extreme lower zone or opposite signal

---

## 📊 DASHBOARD INTERPRETATION

The QMH Dashboard (top-right corner) provides real-time market analysis across all four dimensions:

### Dashboard Elements:

1. **✓ NO REPAINT**

- Green confirmation that signals don't repaint

- Always visible to remind users of signal integrity

2. **SIGNAL: BULL/BEAR XX%**

- Shows dominant direction (whichever confidence is higher)

- Displays current confidence percentage

- Background color intensity reflects confidence level

3. **Psychology: **

- Current market emotional state

- Color coded:

- Orange = Euphoria (extreme bullish emotion)

- Yellow = Greed (moderate bullish emotion)

- Gray = Neutral (balanced state)

- Purple = Fear (uncertainty)

- Red = Panic (extreme bearish emotion)

- Dark red = Despair (capitulation)

4. **Resonance: **

- Multi-timeframe alignment strength

- Positive = All timeframes bullish aligned

- Negative = All timeframes bearish aligned

- Near zero = Timeframes not synchronized

- Emoji indicator: 🔥 (bullish resonance) ❄️ (bearish resonance)

5. **Intermarket: **

- Cross-asset pressure measurement

- Positive = BTC/DXY/VIX correlations supporting upside

- Negative = Correlations supporting downside

- Warning ⚠️ if correlation breakdown detected

6. **RSI: **

- Current RSI(14) reading

- Background colors: Red (>70 overbought), Green (<30 oversold)

- Status: OB (overbought), OS (oversold), or • (neutral)

7. **Status: READY BUY / READY SELL / WAIT**

- Quick trade readiness indicator

- READY BUY: Confidence ≥ threshold, bias bullish

- READY SELL: Confidence ≥ threshold, bias bearish

- WAIT: Confidence below threshold

### How to Use Dashboard:

**Before Entering a Trade:**

- Verify Status shows READY (not WAIT)

- Check that Resonance matches signal direction

- Confirm Psychology isn't contradicting (e.g., buying during Euphoria)

- Note Intermarket value - breakdowns (⚠️) suggest caution

**During a Trade:**

- Monitor Psychology shifts (e.g., from Fear to Greed in a long)

- Watch for Resonance changes that could signal exit

- Check for Intermarket breakdown warnings

---

## ⚙️ CUSTOMIZATION SETTINGS

### TFR Settings (Temporal Fractal Resonance)

- **Enable/Disable**: Turn TFR analysis on/off

- **Fractal Sensitivity** (5-50, default 14):

- Lower values = More responsive to short-term changes

- Higher values = More stable, slower to react

- Recommendation: 14 for balanced, 7 for scalping, 21 for position trading

### CAQE Settings (Cross-Asset Quantum Entanglement)

- **Enable/Disable**: Turn CAQE analysis on/off

- **Asset 1** (default BTC): Reference asset for correlation analysis

- **Asset 2** (default DXY): Second reference asset

- **Asset 3** (default VIX): Third reference asset

- **Correlation Length** (10-100, default 20):

- Lower values = More sensitive to recent correlation changes

- Higher values = More stable correlation measurements

- Recommendation: 20 for most assets, 50 for less volatile markets

### Psychology Settings (Adaptive Market Psychology Matrix)

- **Enable/Disable**: Turn AMPM analysis on/off

- **Volume Spike Threshold** (1.0-5.0x, default 2.0):

- Lower values = Detect smaller volume increases as spikes

- Higher values = Only flag major volume surges

- Recommendation: 2.0 for stocks, 1.5 for crypto

### Probability Settings (Time-Decay Probability Zones)

- **Enable/Disable**: Turn TDPZ visualization on/off

- **Probability Lookback** (20-200, default 50):

- Lower values = Zones adapt faster to recent price action

- Higher values = Zones based on longer statistical history

- Recommendation: 50 for most uses, 100 for position trading

### Filter Settings

- **Min Confidence Score** (40-95%, default 60%):

- Lower threshold = More signals, more false positives

- Higher threshold = Fewer signals, higher quality

- Recommendation: 60% for active trading, 75% for selective trading

### Visual Settings

- **Show Entry Signals**: Toggle QBUY/QSELL labels on chart

- **Show Probability Zones**: Toggle zone visualization

- **Show Psychology State**: Toggle dashboard display

---

## 🔔 ALERT CONFIGURATION

QMH includes four alert conditions that can be configured via TradingView's alert system:

### Available Alerts:

1. **Quantum Buy Signal**

- Fires when: Confirmed QBUY signal generates

- Message includes: Confidence percentage

- Use for: Entry notifications

2. **Quantum Sell Signal**

- Fires when: Confirmed QSELL signal generates

- Message includes: Confidence percentage

- Use for: Entry notifications or exit warnings

3. **Market Panic**

- Fires when: Psychology state reaches Panic

- Use for: Contrarian opportunity alerts

4. **Market Euphoria**

- Fires when: Psychology state reaches Euphoria

- Use for: Reversal warning alerts

### How to Set Alerts:

1. Right-click on chart → "Add Alert"

2. Condition: Select "Quantum Market Harmonics"

3. Choose alert type from dropdown

4. Configure expiration, frequency, and notification method

5. Create alert

**Recommendation**: Set alerts for Quantum Buy/Sell signals with "Once Per Bar Close" frequency to avoid intra-bar false triggers.

---

## 💡 BEST PRACTICES

### For All Users:

1. **Backtest First**

- Test on your specific market and timeframe before live trading

- Different assets may perform better with different confidence thresholds

- Verify that the No Repaint guarantee works as described

2. **Paper Trade**

- Practice with signals on a demo account first

- Understand typical signal frequency for your timeframe

- Get comfortable with the dashboard interpretation

3. **Risk Management**

- Never risk more than 1-2% of capital per trade

- Use proper stop losses (not just mental stops)

- Position size based on confidence score (larger size at higher confidence)

4. **Consider Context**

- QMH signals work best in clear trends or at extremes

- During tight consolidation, false signals increase

- Major news events can invalidate technical signals

### Optimal Use Cases:

**QMH Works Best When:**

- ✅ Markets are trending (up or down)

- ✅ Volatility is normal to elevated

- ✅ Price reaches probability zone extremes

- ✅ Multiple timeframes align

- ✅ Clear inter-market relationships exist

**QMH Is Less Effective When:**

- ❌ Extremely low volatility (zones contract too much)

- ❌ Sideways choppy markets (conflicting timeframes)

- ❌ Flash crashes or news events (correlations break down)

- ❌ Very illiquid assets (irregular price action)

### Session Considerations:

- **24/7 Markets (Crypto)**: Works on all sessions, but signals may be more reliable during high-volume periods (US/European trading hours)

- **Forex**: Best during London/New York overlap when volume is highest

- **Stocks**: Most reliable during regular trading hours (not pre-market/after-hours)

---

## ⚠️ LIMITATIONS AND RISKS

### This Indicator Cannot:

- **Predict Black Swan Events**: Sudden unexpected events invalidate technical analysis

- **Guarantee Profits**: No indicator is 100% accurate; losses will occur

- **Replace Risk Management**: Always use stop losses and proper position sizing

- **Account for Fundamental Changes**: Company news, economic data, etc. can override technical signals

- **Work in All Market Conditions**: Less effective during extreme low volatility or major news events

### Known Limitations:

1. **Multi-Timeframe Lag**: Uses confirmed bars (`close `), so signals appear one bar after conditions met

2. **Correlation Dependency**: CAQE requires sufficient history; may be less reliable on newly listed assets

3. **Computational Load**: Multiple `request.security()` calls may cause slower performance on older devices

4. **Repaint of Dashboard**: Dashboard updates every bar (by design), but signals themselves don't repaint

### Risk Warnings:

- Past performance doesn't guarantee future results

- Backtesting results may not reflect actual trading results due to slippage, commissions, and execution delays

- Different markets and timeframes may produce different results

- The indicator should be used as a tool, not as a standalone trading system

- Always combine with your own analysis, risk management, and trading plan

---

## 🎓 EDUCATIONAL CONCEPTS

This indicator synthesizes several established financial theories and technical analysis concepts:

### Academic Foundations:

1. **Fractal Market Hypothesis** (Edgar Peters)

- Markets exhibit self-similar patterns across time scales

- Implemented via multi-timeframe resonance analysis

2. **Behavioral Finance** (Kahneman & Tversky)

- Investor psychology drives market inefficiencies

- Implemented via market psychology state classification

3. **Intermarket Analysis** (John Murphy)

- Asset classes correlate and influence each other predictably

- Implemented via cross-asset correlation monitoring

4. **Mean Reversion** (Statistical Arbitrage)

- Prices tend to revert to statistical norms

- Implemented via probability zones and standard deviation bands

5. **Multi-Timeframe Analysis** (Technical Analysis Standard)

- Higher timeframe trends dominate lower timeframe noise

- Implemented via fractal resonance scoring

### Learning Resources:

To better understand the concepts behind QMH:

- Read "Intermarket Analysis" by John Murphy (for CAQE concepts)

- Study "Thinking, Fast and Slow" by Daniel Kahneman (for psychology concepts)

- Review "Fractal Market Analysis" by Edgar Peters (for TFR concepts)

- Learn about Bollinger Bands (for TDPZ foundation)

---

## 🔄 VERSION HISTORY AND UPDATES

**Current Version: 1.0**

This is the initial public release. Future updates will be published using TradingView's Update feature (not as separate publications). Planned improvements may include:

- Additional reference assets for CAQE

- Optional machine learning-based weight optimization

- Customizable psychology state definitions

- Alternative probability zone calculations

- Performance metrics tracking

Check the "Updates" tab on the script page for version history.

---

## 📞 SUPPORT AND FEEDBACK

### How to Get Help:

1. **Read This Description First**: Most questions are answered in the detailed sections above

2. **Check Comments**: Other users may have asked similar questions

3. **Post Comments**: For general questions visible to the community

4. **Use TradingView Messaging**: For private inquiries (if available)

### Providing Useful Feedback:

When reporting issues or suggesting improvements:

- Specify your asset, timeframe, and settings

- Include a screenshot if relevant

- Describe expected vs. actual behavior

- Check if issue persists with default settings

### Continuous Improvement:

This indicator will evolve based on user feedback and market testing. Constructive suggestions for improvements are always welcome.

---

## ⚖️ DISCLAIMER

This indicator is provided for **educational and informational purposes only**. It does **not constitute financial advice, investment advice, trading advice, or any other type of advice**.

**Important Disclaimers:**

- You should **not** rely solely on this indicator to make trading decisions

- Always conduct your own research and due diligence

- Past performance is not indicative of future results

- Trading and investing involve substantial risk of loss

- Only trade with capital you can afford to lose

- Consider consulting with a licensed financial advisor before trading

- The author is not responsible for any trading losses incurred using this indicator

**By using this indicator, you acknowledge:**

- You understand the risks of trading

- You take full responsibility for your trading decisions

- You will use proper risk management techniques

- You will not hold the author liable for any losses

---

## 🙏 ACKNOWLEDGMENTS

This indicator builds upon the collective knowledge of the technical analysis and trading community. While the specific implementation and combination are original, the underlying concepts draw from:

- The Pine Script community on TradingView

- Academic research in behavioral finance and market microstructure

- Classical technical analysis methods developed over decades

- Open-source indicators that demonstrate best practices in Pine Script coding

Special thanks to TradingView for providing the platform and Pine Script language that make indicators like this possible.

---

## 📚 ADDITIONAL RESOURCES

**Pine Script Documentation:**

- Official Pine Script Manual: www.tradingview.com

**Related Concepts to Study:**

- Multi-timeframe analysis techniques

- Correlation analysis in financial markets

- Behavioral finance principles

- Mean reversion strategies

- Bollinger Bands methodology

**Recommended TradingView Tools:**

- Strategy Tester: To backtest signal performance

- Bar Replay: To see how signals develop in real-time

- Alert System: To receive notifications of new signals

---

**Thank you for using Quantum Market Harmonics. Trade safely and responsibly.**

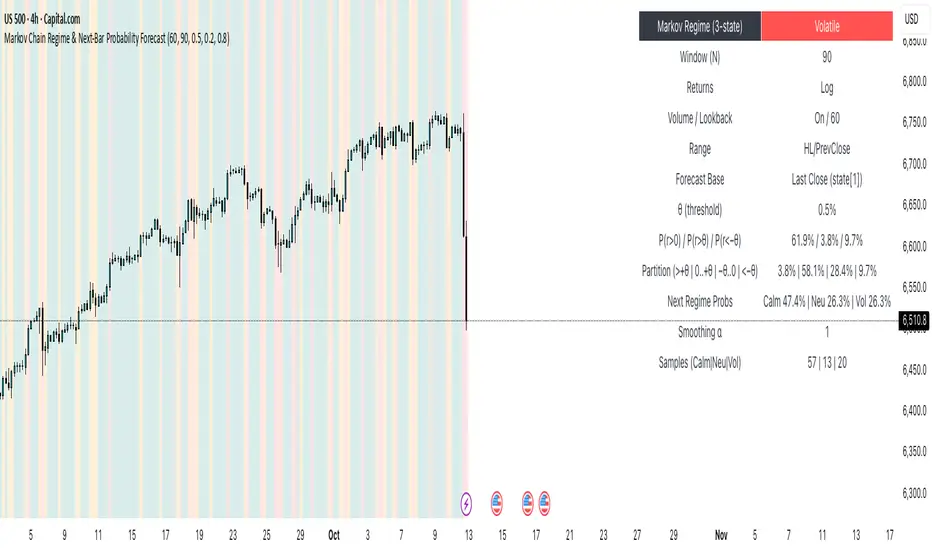

Markov Chain Regime & Next‑Bar Probability Forecast✨ What it is

A regime-aware, math-driven panel that forecasts the odds for the very next candle. It shows:

• P(next r > 0)

• P(next r > +θ)

• P(next r < −θ)

• A 4-bucket split of next-bar outcomes (>+θ | 0..+θ | −θ..0 | <−θ)

• Next-regime probabilities: Calm | Neutral | Volatile

🧠 Why the math is strong

• Markov regimes: Markets cluster in volatility “moods.” We learn a 3-state regime S∈{Calm, Neutral, Volatile} with a transition matrix A, where A = P(Sₜ₊₁=j | Sₜ=i).

• Condition on the future state: We estimate event odds given the next regime j—

q_pos(j)=P(rₜ₊₁>0 | Sₜ₊₁=j), q_gt(j)=P(rₜ₊₁>+θ | Sₜ₊₁=j), q_lt(j)=P(rₜ₊₁<−θ | Sₜ₊₁=j)—

and mix them with transitions from the current (or frozen) state sNow:

P(event) = Σⱼ A · q(event | j).

This mixture-of-regimes view (HMM-style one-step prediction) ties next-bar outcomes to where volatility is likely headed.

• Statistical hygiene: Laplace/Beta smoothing, minimum-sample gating, and unconditional fallbacks keep estimates stable. Heavy computations run on confirmed bars; “Freeze at close” avoids intrabar flicker.

📊 What each value means

• Regime label & background: 🟩 Calm, 🟧 Neutral, 🟥 Volatile — quick read of market context.

• P(next r > 0): Directional tilt for the very next bar.

• P(next r > +θ): Odds of an outsized positive move beyond θ.

• P(next r < −θ): Odds of an outsized negative move beyond −θ.

• Partition row: Distributes next-bar probability across four intuitive buckets; they ≈ sum to 100%.

• Next Regime Probs: Likelihood of switching to Calm/Neutral/Volatile on the next bar (row of A for the current/frozen state).

• Samples row: How many next-bar samples support each next-state estimate (a confidence cue).

• Smoothing α: The Laplace prior used to stabilize binary event rates.

⚙️ Inputs you control

• Returns: Log (default) or %

• Include Volume (z-score) + lookback

• Include Range (HL/PrevClose)

• Rolling window N (transitions & estimates)

• θ as percent (e.g., 0.5%)

• Freeze forecast at last close (recommended)

• Display toggles (plots, partition, samples)

🎯 How to use it

• Volatility awareness & sizing: Rising P(next regime = Volatile) → consider smaller size, wider stops, or skipping marginal entries.

• Breakout preparation: Elevated P(next r > +θ) highlights environments where range expansion is more likely; pair with your setup/trigger.

• Defense for mean-reversion: If P(next r < −θ) lifts while you’re late long (or P(next r > +θ) lifts while late short), tighten risk or wait for better context.

• Calibration tip: Start θ near your market’s typical bar size; adjust until “>+θ” flags truly meaningful moves for your timeframe.

📝 Method notes & limits

Activity features (|r|, volume z, range) are standardized; only positive z’s feed the composite activity score. Estimates adapt to instrument/timeframe; rare regimes or small windows increase variance (hence smoothing, sample gating, fallbacks). This is a context/forecast tool, not a standalone signal—combine with your entry/exit rules and risk management.

🧩 Strategies too

We also develop full strategy versions that use these probabilities for entries, filters, and position sizing. Like this publication if you’d like us to release the strategy edition next.

⚠️ Disclaimer

Educational use only. Not financial advice. Markets involve risk. Past performance does not guarantee future results.

First Passage Time - Distribution AnalysisThe First Passage Time (FPT) Distribution Analysis indicator is a sophisticated probabilistic tool that answers one of the most critical questions in trading: "How long will it take for price to reach my target, and what are the odds of getting there first?"

Unlike traditional technical indicators that focus on what might happen, this indicator tells you when it's likely to happen.

Mathematical Foundation: First Passage Time Theory

What is First Passage Time?

First Passage Time (FPT) is a concept in stochastic processes that measures the time it takes for a random process to reach a specific threshold for the first time. Originally developed in physics and mathematics, FPT has applications in:

Quantitative Finance: Option pricing, risk management, and algorithmic trading

Neuroscience: Modeling neural firing patterns

Biology: Population dynamics and disease spread

Engineering: Reliability analysis and failure prediction

The Mathematics Behind It

This indicator uses Geometric Brownian Motion (GBM), the same stochastic model used in the Black-Scholes option pricing formula:

dS = μS dt + σS dW

Where:

S = Asset price

μ = Drift (trend component)

σ = Volatility (uncertainty component)

dW = Wiener process (random walk)

Through Monte Carlo simulation, the indicator runs 1,000+ price path simulations to statistically determine:

When each threshold (+X% or -X%) is likely to be hit

Which threshold is hit first (directional bias)

How often each scenario occurs (probability distribution)

🎯 How This Indicator Works

Core Algorithm Workflow:

Calculate Historical Statistics

Measures recent price volatility (standard deviation of log returns)

Calculates drift (average directional movement)

Annualizes these metrics for meaningful comparison

Run Monte Carlo Simulations

Generates 1,000+ random price paths based on historical behavior

Tracks when each path hits the upside (+X%) or downside (-X%) threshold

Records which threshold was hit first in each simulation

Aggregate Statistical Results

Calculates percentile distributions (10th, 25th, 50th, 75th, 90th)

Computes "first hit" probabilities (upside vs downside)

Determines average and median time-to-target

Visual Representation

Displays thresholds as horizontal lines

Shows gradient risk zones (purple-to-blue)

Provides comprehensive statistics table

📈 Use Cases

1. Options Trading

Selling Options: Determine if your strike price is likely to be hit before expiration

Buying Options: Estimate probability of reaching profit targets within your time window

Time Decay Management: Compare expected time-to-target vs theta decay

Example: You're considering selling a 30-day call option 5% out of the money. The indicator shows there's a 72% chance price hits +5% within 12 days. This tells you the trade has high assignment risk.

2. Swing Trading

Entry Timing: Wait for higher probability setups when directional bias is strong

Target Setting: Use median time-to-target to set realistic profit expectations

Stop Loss Placement: Understand probability of hitting your stop before target

Example: The indicator shows 85% upside probability with median time of 3.2 days. You can confidently enter long positions with appropriate position sizing.

3. Risk Management

Position Sizing: Larger positions when probability heavily favors one direction

Portfolio Allocation: Reduce exposure when probabilities are near 50/50 (high uncertainty)

Hedge Timing: Know when to add protective positions based on downside probability

Example: Indicator shows 55% upside vs 45% downside—nearly neutral. This signals high uncertainty, suggesting reduced position size or wait for better setup.

4. Market Regime Detection

Trending Markets: High directional bias (70%+ one direction)

Range-bound Markets: Balanced probabilities (45-55% both directions)

Volatility Regimes: Compare actual vs theoretical minimum time

Example: Consistent 90%+ bullish bias across multiple timeframes confirms strong uptrend—stay long and avoid counter-trend trades.

First Hit Rate (Most Important!)

Shows which threshold is likely to be hit FIRST:

Upside %: Probability of hitting upside target before downside

Downside %: Probability of hitting downside target before upside

These always sum to 100%

⚠️ Warning: If you see "Low Hit Rate" warning, increase this parameter!

Advanced Parameters

Drift Mode

Allows you to explore different scenarios:

Historical: Uses actual recent trend (default—most realistic)

Zero (Neutral): Assumes no trend, only volatility (symmetric probabilities)

50% Reduced: Dampens trend effect (conservative scenario)

Use Case: Switch to "Zero (Neutral)" to see what happens in a pure volatility environment, useful for range-bound markets.

Distribution Type

Percentile: Shows 10%, 25%, 50%, 75%, 90% levels (recommended for most users)

Sigma: Shows standard deviation levels (1σ, 2σ)—useful for statistical analysis

⚠️ Important Limitations & Best Practices

Limitations

Assumes GBM: Real markets have fat tails, jumps, and regime changes not captured by GBM

Historical Parameters: Uses recent volatility/drift—may not predict regime shifts

No Fundamental Events: Cannot predict earnings, news, or macro shocks

Computational: Runs only on last bar—doesn't give historical signals

Remember: Probabilities are not certainties. Use this indicator as part of a comprehensive trading plan with proper risk management.

Created by: Henrique Centieiro. feedback is more than welcome!

Hummingbird Probability Mapping IndicatorHummingbird Probability Mapping Indicator - A nature inspired indicator that utilizes combinations of the following trend patterns and projects a probability mapping with greater than 70% accuracy based on real-time analysis.

EMA Trend

MACD

RSI

VWAP Spread

Burst

Squeeze

Volatility (ATRp)

Qi Dass

Institutional Levels (CNN) - [PhenLabs]📊Institutional Levels (Convolutional Neural Network-inspired)

Version : PineScript™v6

📌Description