Unentangle – Probability‑Based Trend Indicator using Chan TheoryUnentangle – Probability‑Based Trend Indicator using Chan Theory

**Overview:**

Unentangle is a custom TradingView indicator inspired by Chan Theory (Chanlun).

It automatically detects and visualizes market structures such as Bi (Trend Stroke), Xian (Line Segment), and Pivot.

By combining structural recognition with statistical analysis of historical patterns, the script provides traders with probability-based buy/sell signals.

This helps traders make more confident, data-driven decisions rather than relying solely on alerts.

Why "Unentangle"?

Market data often looks tangled and chaotic, making it hard to see clear structures and its trend.

This indicator is designed to "un-entangle" the data, revealing Chan Theory patterns and its trend probability so traders can view the market more clearly and make confident decisions.

**Key Features:**

- Automatic recognition of Chanlun structures Bi(Trend Stroke), Xian(Line Segment), Pivot

- Visual drawing of Chanlun elements directly on the chart

- Probability calculations for up and down trends based on historical Chanlun top and bottom patterns

**How It Works:**

The script analyzes price movements to identify Chanlun structures.

It then visually draws Chanlun elements, making it easier to follow Chan Theory without manual plotting.

Once structures are detected, it calculates the statistical probability of signals based on similar historical Chanlun top and bottom setups.

This allows traders to evaluate the confidence level of trades based on current price action.

**Usage:**

Apply the indicator to a clean chart.

The script will automatically display Chanlun structures and probability-based signals.

Traders can use these signals as part of their decision-making process, combining them with their own strategies and risk management rules.

On the chart, a green box indicates an uptrend and a red box indicates a downtrend.

The percentage inside the box shows how much of the current trend has progressed.

For example, “83%” in a green box means the uptrend has already advanced 83%, with only 17% potential space remaining for up trend.

**Notes:**

- This script is closed-source, but its logic is based on Chan Theory principles and statistical analysis of historical Chanlun top/bottom price patterns.

- It is intended for educational and analytical purposes, not as financial advice.

Unentangle – 基于缠论结构的趋势概率指标

**概述:**

Unentangle 是一个基于缠论的 TradingView 自定义指标。

它能够自动识别并可视化市场结构,包括笔、线段和中枢。

通过结合结构识别与历史数据的统计分析,该脚本可以生成基于概率的买卖信号,

帮助交易者在决策时更有依据,而不仅仅依赖提示。

为什么叫 “Unentangle”?

市场数据常常像一团乱麻,难以看清结构。

这个指标的目的就是“解缠”,让缠论的结构及其概率清晰呈现,

帮助交易者更直观地理解市场并做出更有依据的决策。

**功能亮点:**

- 自动识别缠论结构(笔、线段、中枢)

- 在图表上直观绘制缠论元素

- 基于历史顶底数据的趋势概率计算

- 提供信号可信度评估,辅助交易决策

**工作原理:**

脚本会分析价格走势以识别缠论结构。

识别完成后,它会自动绘制缠论元素,使得学习和应用缠论更加直观,无需手动绘制。

同时,脚本会基于历史顶底形态计算趋势的统计概率,

帮助交易者评估当前价格下的交易可信度。

**使用方法:**

将指标应用到干净的图表上。

脚本会自动显示缠论结构和基于概率的信号。

交易者可以将这些信号作为决策参考,并结合自己的策略与风险管理规则。

在图表中,绿色方框表示当前处于上升趋势,红色方框表示下降趋势。

方框中的百分比表示当前趋势的进展程度。

例如,绿色方框显示“83%”意味着当前上升趋势已经完成了 83%,仅剩 17% 的上涨空间。

**注意事项:**

- 本脚本为闭源,但逻辑基于缠论原理与历史数据的统计分析。

- 本脚本仅用于教育与分析目的,不构成任何投资建议。

Probabilities

Mean Reversion Probability Zones [BigBeluga]🔵 OVERVIEW

The Mean Reversion Probability Zones indicator measures the likelihood of price reverting back toward its mean . By analyzing oscillator dynamics (RSI, MFI, or Stochastic), it calculates probability zones both above and below the oscillator. These zones are visualized as histograms, colored regions on the main chart, and a compact dashboard, helping traders spot when the market is statistically stretched and more likely to revert.

🔵 CONCEPTS

Mean Reversion : The tendency of price to return to its average after significant extensions.

Oscillator-Based Analysis : Uses RSI, MFI, or Stochastic as the base signal for detecting overextension.

Probability Model : The probability of reversion is computed using three factors:

Whether the oscillator is rising or declining.

Whether the oscillator is above or below user-defined thresholds.

The oscillator’s actual value (distance from equilibrium).

Dual-Zone Output :

Upper histogram = probability of downward mean reversion.

Lower histogram = probability of upward mean reversion.

Historical Extremes : The dashboard highlights the recent maximum probability values for both upward and downward scenarios.

🔵 FEATURES

Oscillator Choice : Switch between RSI, MFI, and Stochastic.

Customizable Zones : User-defined upper/lower thresholds with independent colors.

Probability Histograms :

Above oscillator → down reversion probability.

Below oscillator → up reversion probability.

Colored Gradient Zones on Chart : Visual overlays showing where mean reversion probabilities are strongest.

Probability Labels : Percentages displayed next to histogram values for clarity.

Dashboard : Compact table in the corner showing the recent maximum probabilities for both upward and downward mean reversion.

Overlay Compatibility : Works in both chart pane and sub-pane with oscillators.

🔵 HOW TO USE

Set Oscillator : Choose RSI, MFI, or Stochastic depending on your strategy style.

Adjust Zones : Define upper/lower bounds for when oscillator values indicate strong overbought/oversold conditions.

Interpret Histograms :

Orange (upper) histogram → higher chance of a pullback/downward mean reversion.

Green (lower) histogram → higher chance of upward reversion/bounce.

Watch Gradient Zones : On the main chart, shaded areas highlight where probability of mean reversion is elevated.

Consult Dashboard : Use the “Recent MAX” values to understand how strong recent reversion probabilities have been in either direction.

Confluence Strategy : Combine with support/resistance, order flow, or trend filters to avoid counter-trend trades.

🔵 CONCLUSION

The Mean Reversion Probability Zones provides traders with an advanced way to quantify and visualize mean reversion opportunities. By blending oscillator momentum, threshold logic, and probability calculations, it highlights when markets are statistically stretched and primed for reversal. Whether you are a contrarian trader or simply looking for exhaustion signals to fade, this tool helps bring structure and clarity to mean reversion setups.

CyberFlow [Probabilities] | FractalystWhat's the indicator's purpose and functionality?

CyberFlow quantifies, per chosen higher-timeframe “Period 1/2/3”, what happens after price first taps the midpoint (Mid) of the previous period’s range. Specifically, it estimates P(High first | Mid tap) versus P(Low first | Mid tap): which side (previous High “PH” or previous Low “PL”) is typically reached first after that mid activation.

It extends a previously shared OrderFlow concept that used market structure; here it conditions on higher‑timeframe previous‑period PH/PL with the Mid as the explicit trigger.

Note: It's specifically designed to exports raw probabilistic series for algorithmic/system developers to integrate a probabilistic layer into strategies and to build/backtest ideas directly from those series.

What is “Mid activation”?

The Mid is the average of the previous period’s PH and PL. Activation occurs on the first bar in the current period whose high–low range includes the Mid. The first bar of a new period cannot activate Mid; activation can only start from the second bar of the period onward.

What counts as “first hit” after activation?

After a Mid activation, the script waits for a subsequent bar that touches either the previous High (PH) or previous Low (PL). The first side touched after the activation bar is recorded as that period’s first hit. Once decided, the other side is ignored for first‑hit statistics.

Which periods does it use?

You can select three custom reference timeframes (Period 1/2/3) in the UI (defaults: D/W/M). All logic—PH/PL/Mid, activation, first‑hit stats—runs independently per selected period.

Do the display controls change the calculation?

No. The “Show” selector only controls visuals:

Period 1/2/3: show only that period’s plots/barcolors.

OFF: shows all periods. Statistics and exported series are unaffected by this selector.

What do the bar/line colors mean?

Activation (first Mid tap): yellow bar.

Delivered to previous High after activation: blue

Delivered to previous Low after activation: red

Plots stop showing PH/PL once delivery happens (for that side) within the period.

What do the status symbols in the table mean?

■ Inactive — Mid not tapped this period.

▶ Activated — Mid tapped; awaiting delivery to PH or PL.

● Delivered — PH or PL was hit first after the Mid tap.

How are probabilities computed?

For each period, the script counts samples where the Mid was tapped and one side was hit first. It reports:

P(High first | Mid tap) and P(Low first | Mid tap).

Two‑sided p‑value vs 50% (H0: p = 0.5). These appear in the stats table with detailed tooltips.

What is “Bias” in exports?

Bias is a ternary signal derived from P(High first | Mid tap):

Bias = 1 if > 0.5

Bias = -1 if < 0.5

Bias = 0 if exactly 0.5 or no sample Source can be per period or “Merged” (simple average of available period probabilities).

Note: the UI uses a simple average; no weighted option is exposed.

What is “Entry” in exports?

Entry = 1 on bars where the selected period’s Mid activates (first tap), else 0. “Merged” emits 1 if any of the three periods activates on the bar.

What is “Exit” in exports?

Exit is the previous period’s Mid price (PH/PL average) for the selected period. “Merged” is the average of the three previous‑period Mid prices.

How do I integrate this into strategies? How to use the indicator?

CyberFlow is designed for algorithmic/system developers to add a probabilistic layer for entries and market‑regime detection.

What CyberFlow exports

- Bias (−1, 0, 1): from P(High first | Mid tap) vs 50% per your chosen source (Period 1/2/3 or Merged simple average).

- Entry (0/1): 1 only on the bar where the selected period’s Mid first activates (the “mid tap” bar).

- Exit (price): the previous period’s Mid price (average of previous High/Low) for the selected source.

- These appear in the Data Window as series named Bias, Entry, and Exit.

Connecting from your strategy (input.source)

- Add inputs in your strategy so users can select CyberFlow’s outputs:

- Bias source input: pick the indicator’s Bias.

- Entry source input: pick the indicator’s Entry.

- Exit source input: pick the indicator’s Exit.

In TradingView’s UI, users link these inputs to CyberFlow’s plots via the source picker.

Does this use request.security?

No. CyberFlow reconstructs your selected higher timeframes (Period 1/2/3) directly on the chart without request.security().

It detects new period boundaries via timeframe.change(tf), rolls the last period’s extremes into Previous High/Low (PH/PL), computes their Mid, then waits for a “Mid activation” (a bar after the first bar of the period whose range crosses the Mid).

From activation onward, it records which side (PH or PL) is reached first to build conditional probabilities per period.

Because levels and events are derived locally from the live bar stream, there are no cross-timeframe fetch artifacts or repaint nuances from request.security().

The exported series (Bias −1/0/1, Entry 0/1, Exit price) are produced natively and can be wired into strategies via TradingView’s input.source() for robust, low-latency integration.

What markets and assets does the indicator Extension work best on?

CyberFlow is market- and timeframe‑agnostic: it computes conditional probabilities (which side of the prior range is reached first after a mid tap) directly from price, so it can be applied to crypto, FX, indices, equities, futures, and commodities across intraday to higher timeframes. In practice, robustness depends on liquidity and sample size: higher timeframes usually yield more stable estimates (fewer activations, lower noise), while lower timeframes give more activations but can be noisier (spreads/fees matter more).

Because the study itself provides probabilities—not PnL—assess profitability in your context by integrating the exported series (Bias −1/0/1, Entry 0/1, Exit price) into your strategy via TradingView’s input.source(), then backtest with your fills, costs, and risk model to measure performance efficiency on your specific markets and settings.

What makes this script unique?

Custom higher-timeframes (beyond D/W/M)

You can pick any three reference periods (Period 1/2/3), not just Daily/Weekly/Monthly. The script rebuilds these periods directly on the chart and analyzes each independently.

True conditional probability (why it matters)

It measures P(High first | Mid tap) vs P(Low first | Mid tap) — i.e., “after the previous period’s midpoint is first tapped, which side is typically reached first?”

Conditioning on the mid‑tap event isolates the path that follows a specific trigger. Unconditioned counts (e.g., “how often PH/PL is hit”) mix pre‑ and post‑activation behavior and can be misleading. This conditional framing turns vague hit‑rates into decision‑grade odds tied to a clear setup.

Statistical confidence in‑context (p‑value in tooltips)

Tooltips show a Wilson 95% confidence interval and a two‑sided p‑value versus 50/50. This helps you judge whether an observed edge is likely signal or noise at your chosen periods.

Exports built for algorithmic integration

Three clean outputs in the Data Window for strategies:

Bias (−1/0/1) from the conditional probability versus 50%.

Entry (0/1) on the activation bar (first mid tap).

Exit (price) as the previous period’s Mid.

Hook these into your backtests via TradingView’s input.source(), then evaluate profitability with your own fills, costs, and risk model. This turns the probabilities into measurable performance you can optimize.

Disclaimer

This tool provides statistical estimates only and is not financial advice. Historical probabilities are not guarantees of future results. Always backtest with your own costs, fills, and risk model before using in live trading.

LTPI TOTAL | JeffreyTimmermansLong-Term Trend Probability Indicator

The "Long-Term Trend Probability Indicator" on TOTAL is a custom-built tool designed to analyze the global crypto market (TOTAL) from a long-term perspective. Unlike short-term indicators that react to price volatility, LTPI focuses on major trend shifts across the entire crypto market, helping to identify major trend shifts early.

This version of the LTPI is applied to the TOTAL market cap, making it a broad trend following tool.

Key Features

Long-Term Focus:

Designed for macro market analysis with less sensitivity to short-term noise.

10 Input Signals:

Combines 10 carefully selected inputs (trend following indicators) into a single score that reflects the overall market condition.

Market Regimes:

Classifies the TOTAL market into:

Bullish: Strong uptrend, expansion phase

Bearish: Strong downtrend, contraction phase

Neutral: Transitional or uncertain

Visual Background:

Background colors clearly display which regime is active.

Comprehensive Dashboard:

The panel at the bottom shows each input’s state, the composite LTPI score, and the resulting market trend.

How It Works

Inputs Analysis:

Each of the 10 inputs outputs one of three states:

+1 (Bullish)

-1 (Bearish)

0 (Neutral)

Score Calculation:

The total score is the sum of all 10 input signals divided by 10.

Score > 0.1 = Bullish

Score < -0.1 = Bearish

Between -0.1 and 0.1 = Neutral

Background Coloring:

Background colors dynamically adjust to reflect the long-term market regime.

Use Cases

Long-Term Positioning:

Identify periods of global expansion or contraction to position yourself accordingly.

Macro Confirmation:

Use LTPI in combination with medium-term (MTPI) and short-term tools for multi-timeframe confirmation.

Market Timing:

Alerts when LTPI crosses key thresholds help highlight the start of major bullish or bearish phases.

Dynamic Alerts:

Bullish Entry: LTPI score crosses above 0.1

Bearish Entry: LTPI score crosses below -0.1

Neutral Zone: Score moves back between -0.1 and 0.1

Conclusion

The Long-Term Trend Probability Indicator (LTPI – TOTAL) is a powerful tool for identifying long-term market phases across the entire crypto ecosystem. By focusing on long term trends and combining 10 inputs into a single probability score, it provides a clear macro perspective for strategic decision-making.

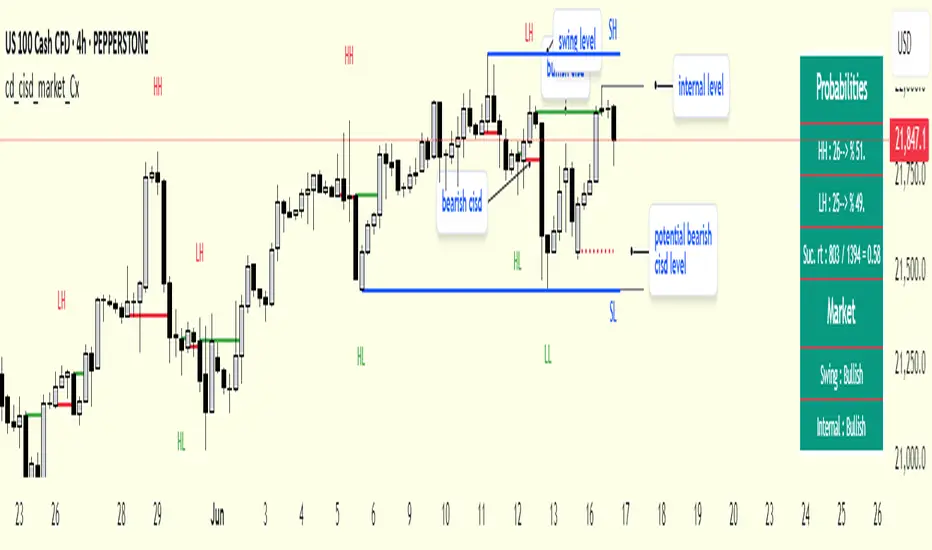

cd_cisd_market_CxHi Traders,

Overview:

Many traders follow market structure to identify the market direction and seek trade opportunities in line with the trend.

However, markings derived from user-defined inputs can create different structures, depending on personal choices. For instance, choosing a pivot distance of 3 instead of 2 alters the structure, even though the chart remains the same. Ideally, the structure should remain consistent.

"Change in State Delivery" ( CISD ) is a widely accepted concept among traders and is considered a significant indicator of market direction based on the gain/loss of CISD levels.

In this indicator, CISD is selected as the primary criterion for marking market structure, eliminating the influence of user-dependent variations.

Here is a summary of the key logic and rules applied:

• When the price forms a new high/low, that level is only considered a pivot if a CISD has occurred.

• A bullish CISD is always followed by a bearish CISD, and vice versa.

• Pivot points form the internal structure.

• The internal structure is used to interpret the swing structure.

• Probabilities are derived from internal structure patterns.

________________________________________

Details:

How is CISD determined?

As is commonly known:

• When price makes a new high, the opening level of the first candle in the consecutive bullish candle sequence is marked.

• When price makes a new low, the opening of the first candle in the consecutive bearish sequence is marked.

• If there’s only one candle in the sequence, its opening level is used.

In a bullish market, losing a bearish CISD level (i.e., a close below it) or in a bearish market, gaining a bullish CISD level (i.e., a close above it) is interpreted as a potential shift in buyer-seller dominance and a possible market reversal.

________________________________________

How are internal (pivot) levels determined?

• When price closes below a bearish CISD level, the highest candle's high becomes a pivot high (PH).

• When price closes above a bullish CISD level, the lowest candle's low becomes a pivot low (PL).

• If the new PH is above the previous PH, it’s labeled as HH (Higher High); otherwise, LH (Lower High).

• If the new PL is below the previous PL, it’s labeled as LL (Lower Low); otherwise, HL (Higher Low).

________________________________________

Internal Market Structure:

• A series of HHs indicates a bullish internal structure.

• A series of LLs indicates a bearish internal structure.

________________________________________

Swing (Main) Market Structure:

Using internal pivots and previous swing levels, the main market structure is derived.

• A new swing high (SH) requires the price to move above the previous SH.

• A new swing low (SL) requires the price to move below the previous SL.

________________________________________

Probability Calculation:

Pivot levels forming the internal structure are coded as five-element sequences.

There are 64 possible combinations of such sequences made from consecutive PH and PL values.

Each pattern’s frequency from its starting candle is tracked.

To make it more understandable:

For example, after the four-sequence “HH, LL, LH,HL”, either HH or LH might follow.

The table shows the statistical likelihood of both possible outcomes for the most recent four-element sequence on the chart.

________________________________________

How reliable is it?

To assess reliability, results are calculated from the beginning using:

Success Rate (Suc. Rt) = Number of Correct Predictions / Total Predictions

This value is added to the table for reference.

It’s important to note that no statistical outcome guarantees certainty—every result offers a different interpretation. What truly matters is to avoid getting stopped out 😊.

________________________________________

Menu Options:

Show/hide preferences and color selections can be customized via the indicator menu.

________________________________________

What’s Coming in Future Versions?

Features such as FVG (Fair Value Gaps) between swing levels, volume imbalances, order blocks / mitigation blocks, Fibonacci levels, and relevant trade suggestions will be added.

________________________________________

This is a BETA version that I believe will help simplify your market reading. I’d be happy to hear your feedback and suggestions.

Cheerful Trading!

Quantify [Trading Model] | FractalystNote: In this description, "TM" refers to Trading Model (not trademark) and "EM" refers to Entry Model

What’s the indicator’s purpose and functionality?

You know how to identify market bias but always struggle with figuring out the best exit method, or even hesitating to take your trades?

I've been there. That's why I built this solution—once and for all—to help traders who know the market bias but need a systematic and quantitative approach for their entries and trade management.

A model that shows you real-time market probabilities and insights, so you can focus on execution with confidence—not doubt or FOMO.

How does this Quantify differentiate from Quantify ?

Have you managed to code or even found an indicator that identifies the market bias for you, so you don’t have to manually spend time analyzing the market and trend?

Then that’s exactly why you might need the Quantify Trading Model.

With the Trading Model (TM) version, the script automatically uses your given bias identification method to determine the trend (bull vs bear and neutral), detect the bias, and provide instant insight into the trades you could’ve taken.

To avoid complications from consecutive signals, it uses a kNN machine learning algorithm that processes market structure and probabilities to predict the best future patterns.

(You don’t have to deal with any complexity—it’s all taken care of for you.)

Quantify TM uses the k-Nearest Neighbors (kNN) machine learning algorithm to learn from historical market patterns and adapt to changing market structures. This means it can recognize similar market conditions from the past and apply those lessons to current trading decisions.

On the other hand, Quantify EM requires you to manually select your directional bias. It then focuses solely on generating entry signals based on that pre-determined bias.

While the entry model version (EM) uses your manual bias selection to determine the trend, it then provides insights into trades you could’ve taken and should be taking.

Trading Model (TM)

- Uses `input.source()` to incorporate your personal methodology for identifying market bias

- Automates everything—from bias detection to entry and exit decisions

- Adapts to market bias changes through kNN machine learning optimization

- Reduces human intervention in trading decisions, limiting emotional interference

Entry Model (EM)

- Focuses specifically on optimizing entry points within your pre-selected directional bias

- Requires manual input for determining market bias

- Provides entry signals without automating alerts or bias rules

Can the indicator be applied to any market approach/trading strategy?

Yes, if you have clear rules for identifying the market bias, then you can code your bias detection and then use the input.source() user input to retrieve the direction from your own indicator, then the Quantify uses machine-learning identify the best setups for you.

Here's an example:

//@version=6

indicator('Moving Averages Bias', overlay = true)

// Input lengths for moving averages

ma10_length = input.int(10, title = 'MA 10 Length')

ma20_length = input.int(20, title = 'MA 20 Length')

ma50_length = input.int(50, title = 'MA 50 Length')

// Calculate moving averages

ma10 = ta.sma(close, ma10_length)

ma20 = ta.sma(close, ma20_length)

ma50 = ta.sma(close, ma50_length)

// Identify bias

var bias = 0

if close > ma10 and close > ma20 and close > ma50 and ma10 > ma20 and ma20 > ma50

bias := 1 // Bullish

bias

else if close < ma10 and close < ma20 and close < ma50 and ma10 < ma20 and ma20 < ma50

bias := -1 // Bearish

bias

else

bias := 0 // Neutral

bias

// Plot the bias

plot(bias, title = 'Identified Bias', color = color.blue,display = display.none)

Once you've created your custom bias indicator, you can integrate it with Quantify :

- Add your bias indicator to your chart

- Open the Quantify settings

- Set the Bias option to "Auto"

- Select your custom indicator as the bias source

The machine learning algorithms will then analyze historical price action and identify optimal setups based on your defined bias parameters. Performance statistics are displayed in summary tables, allowing you to evaluate effectiveness across different timeframes.

Can the indicator be used for different timeframes or trading styles?

Yes, regardless of the timeframe you’d like to take your entries, the indicator adapts to your trading style.

Whether you’re a swing trader, scalper, or even a position trader, the algorithm dynamically evaluates market conditions across your chosen timeframe.

How Quantify Helps You Trade Profitably?

The Quantify Trading Model offers several powerful features that can significantly improve your trading profitability when used correctly:

Real-Time Edge Assessment

It displays real-time probability of price moving in your favor versus hitting your stoploss

This gives you immediate insight into risk/reward dynamics before entering trades

You can make more informed decisions by knowing the statistical likelihood of success

Historical Edge Validation

Instantly shows whether your trading approach has demonstrated an edge in historical data

Prevents you from trading setups that historically haven't performed well

Gives confidence when entering trades that have proven statistical advantages

Optimized Position Sizing

Analyzes each setup's success rate to determine the adjusted Kelly criterion formula

Customizes position sizing based on your selected maximum drawdown tolerance

Helps prevent account-destroying losses while maximizing growth potential

Advanced Exit Management

Utilizes market structure-based trailing stop-loss mechanisms

Maximizes the average risk-reward ratio profit per winning trade

Helps capture larger moves while protecting gains during market reversals

Emotional Discipline Enforcement

Eliminates emotional bias by adhering to your pre-defined rules for market direction

Prevents impulsive decisions by providing objective entry and exit signals

Creates psychological distance between your emotions and trading decisions

Overtrading Prevention

Highlights only setups that demonstrate positive expectancy

Reduces frequency of low-probability trades

Conserves capital for higher-quality opportunities

Systematic Approach Benefits

By combining machine learning algorithms with your personal bias identification methods, Quantify helps transform discretionary trading approaches into more systematic, probability-based strategies.

What Entry Models are used in Quantify Trading Model version?

The Quantify Trading Model utilizes two primary entry models to identify high-probability trade setups:

Breakout Entry Model

- Identifies potential trade entries when price breaks through significant swing highs and swing lows

- Captures momentum as price moves beyond established trading ranges

- Particularly effective in trending markets when combined with the appropriate bias detection

- Optimized by machine learning to filter false breakouts based on historical performance

Fractals Entry Model

- Utilizes fractal patterns to identify potential reversal or continuation points

- Also uses swing levels to determine optimal entry locations

- Based on the concept that market structure repeats across different timeframes

- Identifies local highs and lows that form natural entry points

- Enhanced by machine learning to recognize the most profitable fractal formations

- These entry models work in conjunction with your custom bias indicator to ensure trades are taken in the direction of the overall market trend. The machine learning component analyzes historical performance of these entry types across different market conditions to optimize entry timing and signal quality.

How Does This Indicator Identify Market Structure?

1. Swing Detection

• The indicator identifies key swing points on the chart. These are local highs or lows where the price reverses direction, forming the foundation of market structure.

2. Structural Break Validation

• A structural break is flagged when a candle closes above a previous swing high (bullish) or below a previous swing low (bearish).

• Break Confirmation Process:

To confirm the break, the indicator applies the following rules:

• Valid Swing Preceding the Break: There must be at least one valid swing point before the break.

3. Numeric Labeling

• Each confirmed structural break is assigned a unique numeric ID starting from 1.

• This helps traders track breaks sequentially and analyze how the market structure evolves over time.

4. Liquidity and Invalidation Zones

• For every confirmed structural break, the indicator highlights two critical zones:

1. Liquidity Zone (LIQ): Represents the structural liquidity level.

2. Invalidation Zone (INV): Acts as Invalidation point if the structure fails to hold.

How does the trailing stop-loss work? what are the underlying calculations?

A trailing stoploss is a dynamic risk management tool that moves with the price as the market trend continues in the trader’s favor. Unlike a fixed take profit, which stays at a set level, the trailing stoploss automatically adjusts itself as the market moves, locking in profits as the price advances.

In Quantify, the trailing stoploss is enhanced by incorporating market structure liquidity levels (explain above). This ensures that the stoploss adjusts intelligently based on key price levels, allowing the trader to stay in the trade as long as the trend remains intact, while also protecting profits if the market reverses.

What is the Kelly Criterion, and how does it work in Quantify?

The Kelly Criterion is a mathematical formula used to determine the optimal position size for each trade, maximizing long-term growth while minimizing the risk of large drawdowns. It calculates the percentage of your portfolio to risk on a trade based on the probability of winning and the expected payoff.

Quantify integrates this with user-defined inputs to dynamically calculate the most effective position size in percentage, aligning with the trader’s risk tolerance and desired exposure.

How does Quantify use the Kelly Criterion in practice?

Quantify uses the Kelly Criterion to optimize position sizing based on the following factors:

1. Confidence Level: The model assesses the confidence level in the trade setup based on historical data and sample size. A higher confidence level increases the suggested position size because the trade has a higher probability of success.

2. Max Allowed Drawdown (User-Defined): Traders can set their preferred maximum allowed drawdown, which dictates how much loss is acceptable before reducing position size or stopping trading. Quantify uses this input to ensure that risk exposure aligns with the trader’s risk tolerance.

3. Probabilities: Quantify calculates the probabilities of success for each trade setup. The higher the probability of a successful trade (based on historical price action and liquidity levels), the larger the position size suggested by the Kelly Criterion.

How can I get started to use the indicator?

1. Set Your Market Bias

• Choose Auto.

• Select the source you want Quantify to use as for bias identification method (explained above)

2. Choose Your Entry Timeframes

• Specify the timeframes you want to focus on for trade entries.

• The indicator will dynamically analyze these timeframes to provide optimal setups.

3. Choose Your Entry Model and BE/TP Levels

• Choose a model that suits your personality

• Choose a level where you'd like the script to take profit or move stop-loss to BE

4. Set and activate the alerts

What tables are used in the Quantify?

• Quarterly

• Monthly

• Weekly

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

- By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

QuantBuilder | FractalystWhat's the strategy's purpose and functionality?

QuantBuilder is designed for both traders and investors who want to utilize mathematical techniques to develop profitable strategies through backtesting on historical data.

The primary goal is to develop profitable quantitive strategies that not only outperform the underlying asset in terms of returns but also minimize drawdown.

For instance, consider Bitcoin (BTC), which has experienced significant volatility, averaging an estimated 200% annual return over the past decade, with maximum drawdowns exceeding -80%. By employing this strategy with diverse entry and exit techniques, users can potentially seek to enhance their Compound Annual Growth Rate (CAGR) while managing risk to maintain a lower maximum drawdown.

While this strategy employs quantitative techniques, including mathematical methods such as probabilities and positive expected values, it demonstrates exceptional efficacy across all markets. It particularly excels in futures, indices, stocks, cryptocurrencies, and commodities, leveraging their inherent trending behaviors for optimized performance.

In both trending and consolidating market conditions, QuantBuilder employs a combination of multi-timeframe probabilities, expected values, directional biases, moving averages and diverse entry models to identify and capitalize on bullish market movements.

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

1. Trading:

- Designed for traders looking to capitalize on bullish markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for both swing and intraday trading with a focus on probabilities and risk per trade approach.

2. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes pre-define percentage of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully/partially investing in the asset during bullish conditions.

How does the strategy identify market structure? What are the underlying calculations?

The strategy utilizes an efficient logic with for loops to pinpoint the first swing candle featuring a pivot of 2, establishing the point at which the break of structure begins.

What entry criteria are used in this script? What are the underlying calculations?

The script utilizes two entry models: BreakOut and fractal.

Underlying Calculations:

Breakout: The script assigns the most recent swing high to a variable. When the price closes above this level and all other conditions are met, the script executes a breakout entry (conservative approach).

Fractal: The script identifies a swing low with a period of 2. Once this condition is met, the script executes the trade (aggressive approach).

How does the script calculate probabilities? What are the underlying calculations?

The script calculates probabilities by monitoring price interactions with liquidity levels. Here’s how the underlying calculations work:

Tracking Price Hits: The script counts the number of times the price taps into each liquidity side after the EQM level is activated. This data is stored in an array for further analysis.

Sample Size Consideration: The total number of price interactions serves as the sample size for calculating probabilities.

Probability Calculation: For each liquidity side, the script calculates the probability by taking the average of the recorded hits. This allows for a dynamic assessment of the likelihood that a particular side will be hit next, based on historical performance.

Dynamic Adjustment: As new price data comes in, the probabilities are recalculated, providing real-time aduptive insights into market behavior.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

How does the script calculate expected values? What are the underlying calculations?

The script calculates expected values by leveraging the probabilities of winning and losing trades, along with their respective returns. The process involves the following steps:

This quantitative methodology provides a robust framework for assessing the expected performance of trading strategies based on historical data and backtesting results.

How is the contextual bias calculated? What are the underlying calculations?

The contextual bias in the QuantBuilder script is calculated through a structured approach that assesses market structure based on swing highs and lows. Here’s how it works:

Identification of Swing Points: The script identifies significant swing points using a defined pivot logic, focusing on the first swing high and swing low. This helps establish critical levels for determining market structure.

Break of Structure (BOS) Assessment:

Bullish BOS: The script recognizes a bullish break of structure when a candle closes above the first swing high, followed by at least one swing low.

Bearish BOS: Conversely, a bearish break of structure is identified when a candle closes below the first swing low, followed by at least one swing high.

Bias Assignment: Based on the identified break of structure, the script assigns directional biases:

A bullish bias is assigned if a bullish BOS is confirmed.

A bearish bias is assigned if a bearish BOS is confirmed.

Quantitative Evaluation: Each identified bias is quantitatively evaluated, allowing the script to assign numerical values representing the strength of each bias. This quantification aids in assessing the reliability of market sentiment across multiple timeframes.

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

- Initial Stop-loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14)

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

3. PL Based:

This method places the stop-loss at the low of the previous candle.

If the current entry is based on the hunt entry strategy, the stop-loss will be placed at the low of the candle that wicks through the lower FRMA band.

Example:

If the previous candle's low is 100, then the stop-loss will be set at 100.

This method ensures the stop-loss is placed just below the most recent significant low, providing a logical and immediate level for risk management.

- Trailing Stop-Loss:

One of the key elements of this strategy is its ability to detect structural liquidity and structural invalidation levels across multiple timeframes to trail the stop-loss once the trade is in running profits.

By utilizing this approach, the strategy allows enough room for price to run.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

Percentage (%) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain percentage above the entry.

Calculation:

Break-even level = Entry Price * (1 + Percentage / 100)

Example:

If the entry price is $100 and the break-even percentage is 5%, the break-even level is $100 * 1.05 = $105.

Risk-to-Reward (RR) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

What's the day filter Filter, what does it do?

The day filter allows users to customize the session time and choose the specific days they want to include in the strategy session. This helps traders tailor their strategies to particular trading sessions or days of the week when they believe the market conditions are more favorable for their trading style.

Customize Session Time:

Users can define the start and end times for the trading session.

This allows the strategy to only consider trades within the specified time window, focusing on periods of higher market activity or preferred trading hours.

Select Days:

Users can select which days of the week to include in the strategy.

This feature is useful for excluding days with historically lower volatility or unfavorable trading conditions (e.g., Mondays or Fridays).

Benefits:

Focus on Optimal Trading Periods:

By customizing session times and days, traders can focus on periods when the market is more likely to present profitable opportunities.

Avoid Unfavorable Conditions:

Excluding specific days or times can help avoid trading during periods of low liquidity or high unpredictability, such as major news events or holidays.

What tables are available in this script?

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Total Commission: Displays the cumulative commissions incurred from all trades executed within the selected backtesting window. This value is derived by summing the commission fees for each trade on your chart.

Average Commission: Represents the average commission per trade, calculated by dividing the Total Commission by the total number of closed trades. This metric is crucial for assessing the impact of trading costs on overall profitability.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month and year.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- UI Table: A user-friendly table that allows users to view and save the selected strategy parameters from user inputs. This table enables easy access to key settings and configurations, providing a straightforward solution for saving strategy parameters by simply taking a screenshot with Alt + S or ⌥ + S.

User-input styles and customizations:

To facilitate studying historical data, all conditions and filters can be applied to your charts. By plotting background colors on your charts, you'll be able to identify what worked and what didn't in certain market conditions.

Please note that all background colors in the style are disabled by default to enhance visualization.

How to Use This Quantitive Strategy Builder to Create a Profitable Edge and System?

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker/prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 200 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

What makes this strategy original?

QuantBuilder stands out due to its unique combination of quantitative techniques and innovative algorithms that leverage historical data for real-time trading decisions. Unlike most algorithmic strategies that work based on predefined rules, this strategy adapts to real-time market probabilities and expected values, enhancing its reliability. Key features include:

Mathematical Framework: The strategy integrates advanced mathematical concepts, such as probabilities and expected values, to assess trade viability and optimize decision-making.

Multi-Timeframe Analysis: By utilizing multi-timeframe probabilities, QuantBuilder provides a comprehensive view of market conditions, enhancing the accuracy of entry and exit points.

Dynamic Market Structure Identification: The script employs a systematic approach to identify market structure changes, utilizing a blend of swing highs and lows to detect contextual/direction bias of the market.

Built-in Trailing Stop Loss: The strategy features a dynamic trailing stop loss based on multi-timeframe analysis of market structure. This allows traders to lock in profits while adapting to changing market conditions, ensuring that exits are executed at optimal levels without prematurely closing positions.

Robust Performance Metrics: With detailed performance tables and visualizations, users can easily evaluate strategy effectiveness and adjust parameters based on historical performance.

Adaptability: The strategy is designed to work across various markets and timeframes, making it versatile for different trading styles and objectives.

Suitability for Investors and Traders: QuantBuilder is ideal for both investors and traders looking to rely on mathematically proven data to create profitable strategies, ensuring that decisions are grounded in quantitative analysis.

These original elements combine to create a powerful tool that can help both traders and investors to build and refine profitable strategies based on algorithmic quantitative analysis.

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

OrderFlow [Adjustable] | FractalystWhat's the indicator's purpose and functionality?

This indicator is designed to assist traders in identifying real-time probabilities of buyside and sellside liquidity .

It allows for an adjustable pivot level , enabling traders to customize the level they want to use for their entries.

By doing so, traders can evaluate whether their chosen entry point would yield a positive expected value over a large sample size, optimizing their strategy for long-term profitability.

For advanced traders looking to enhance their analysis, the indicator supports the incorporation of up to 7 higher timeframe biases .

Additionally, the higher timeframe pivot level can be adjusted according to the trader's preferences,

Offering maximum adaptability to different strategies and needs, further helping to maximize positive EV.

EV=(P(Win)×R(Win))−(P(Loss)×R(Loss))

-----

What's the purpose of these levels? What are the underlying calculations?

1. Understanding Swing highs and Swing Lows

Swing High: A Swing High is formed when there is a high with 2 lower highs to the left and right.

Swing Low: A Swing Low is formed when there is a low with 2 higher lows to the left and right.

2. Understanding the purpose and the underlying calculations behind Buyside, Sellside and Pivot levels.

3. Identifying Discount and Premium Zones.

4. Importance of Risk-Reward in Premium and Discount Ranges

----

How does the script calculate probabilities?

The script calculates the probability of each liquidity level individually. Here's the breakdown:

1. Upon the formation of a new range, the script waits for the price to reach and tap into pivot level level. Status: "⏸" - Inactive

2. Once pivot level is tapped into, the pivot status becomes activated and it waits for either liquidity side to be hit. Status: "▶" - Active

3. If the buyside liquidity is hit, the script adds to the count of successful buyside liquidity occurrences. Similarly, if the sellside is tapped, it records successful sellside liquidity occurrences.

4. Finally, the number of successful occurrences for each side is divided by the overall count individually to calculate the range probabilities.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

----

What does the multi-timeframe functionality offer?

In the adjustable version of the orderflow indicator, you can incorporate up to 7 higher timeframe probabilities directly into the table.

This feature allows you to analyze the probabilities of buyside and sellside liquidity across multiple timeframes, without the need to manually switch between them.

By viewing these higher timeframe probabilities in one place, traders can spot larger market trends and refine their entries and exits with a better understanding of the overall market context.

This multi-timeframe functionality helps traders:

1. Simplify decision-making by offering a comprehensive view of multiple timeframes at once.

2. Identify confluence between timeframes, enhancing the confidence in trade setups.

3. Adapt strategies more effectively, as the higher timeframe pivot levels can be customized to meet individual preferences and goals.

----

What are the multi-timeframe underlying calculations?

The script uses the same calculations (mentioned above) and uses security function to request the data such as price levels, bar time, probabilities and booleans from the user-input timeframe.

----

How does the Indicator Identifies Positive Expected Values?

OrderFlow indicator instantly calculates whether a trade setup has the potential for positive expected value (EV) in the long run.

To determine a positive EV setup, the indicator uses the formula:

EV=(P(Win)×R(Win))−(P(Loss)×R(Loss))

where:

P(Win) is the probability of a winning trade.

R(Win) is the reward or return for a winning trade, determined by the current risk-to-reward ratio (RR).

P(Loss) is the probability of a losing trade.

R(Loss) is the loss incurred per losing trade, typically assumed to be -1.

By calculating these values based on historical data and the current trading setup, the indicator helps you understand whether your trade has a positive expected value over a large sample size.

----

How can I know that the setup I'm going to trade with has a postive EV?

If the indicator detects that the adjusted pivot and buy/sell side probabilities have generated positive expected value (EV) in historical data, the risk-to-reward (RR) label within the range box will be colored blue and red .

If the setup does not produce positive EV, the RR label will appear gray.

This indicates that even the risk-to-reward ratio is greater than 1:1, the setup is not likely to yield a positive EV because, according to historical data, the number of losses outweighs the number of wins relative to the RR gain per winning trade.

----

What is the confidence level in the indicator, and how is it determined?

The confidence level in the indicator reflects the reliability of the probabilities calculated based on historical data. It is determined by the sample size of the probabilities used in the calculations. A larger sample size generally increases the confidence level, indicating that the probabilities are more reliable and consistent with past performance.

----

How does the confidence level affect the risk-to-reward (RR) label?

The confidence level (★) is visually represented alongside the probability label. A higher confidence level indicates that the probabilities used to determine the RR label are based on a larger and more reliable sample size.

----

How can traders use the confidence level to make better trading decisions?

Traders can use the confidence level to gauge the reliability of the probabilities and expected value (EV) calculations provided by the indicator. A confidence level above 95% is considered statistically significant and indicates that the historical data supporting the probabilities is robust. This high confidence level suggests that the probabilities are reliable and that the indicator’s recommendations are more likely to be accurate.

In data science and statistics, a confidence level above 95% generally means that there is less than a 5% chance that the observed results are due to random variation. This threshold is widely accepted in research and industry as a marker of statistical significance. Studies such as those published in the Journal of Statistical Software and the American Statistical Association support this threshold, emphasizing that a confidence level above 95% provides a strong assurance of data reliability and validity.

Conversely, a confidence level below 95% indicates that the sample size may be insufficient and that the data might be less reliable . In such cases, traders should approach the indicator’s recommendations with caution and consider additional factors or further analysis before making trading decisions.

----

How does the sample size affect the confidence level, and how does it relate to my TradingView plan?

The sample size for calculating the confidence level is directly influenced by the amount of historical data available on your charts. A larger sample size typically leads to more reliable probabilities and higher confidence levels.

Here’s how the TradingView plans affect your data access:

Essential Plan

The Essential Plan provides basic data access with a limited amount of historical data. This can lead to smaller sample sizes and lower confidence levels, which may weaken the robustness of your probability calculations. Suitable for casual traders who do not require extensive historical analysis.

Plus Plan

The Plus Plan offers more historical data than the Essential Plan, allowing for larger sample sizes and more accurate confidence levels. This enhancement improves the reliability of indicator calculations. This plan is ideal for more active traders looking to refine their strategies with better data.

Premium Plan

The Premium Plan grants access to extensive historical data, enabling the largest sample sizes and the highest confidence levels. This plan provides the most reliable data for accurate calculations, with up to 20,000 historical bars available for analysis. It is designed for serious traders who need comprehensive data for in-depth market analysis.

PRO+ Plans

The PRO+ Plans offer the most extensive historical data, allowing for the largest sample sizes and the highest confidence levels. These plans are tailored for professional traders who require advanced features and significant historical data to support their trading strategies effectively.

For many traders, the Premium Plan offers a good balance of affordability and sufficient sample size for accurate confidence levels.

----

What is the HTF probability table and how does it work?

The HTF (Higher Time Frame) probability table is a feature that allows you to view buy and sellside probabilities and their status from timeframes higher than your current chart timeframe.

Here’s how it works:

Data Request : The table requests and retrieves data from user-defined higher timeframes (HTFs) that you select.

Probability Display: It displays the buy and sellside probabilities for each of these HTFs, providing insights into the likelihood of price movements based on higher timeframe data.

Detailed Tooltips: The table includes detailed tooltips for each timeframe, offering additional context and explanations to help you understand the data better.

----

What do the different colors in the HTF probability table indicate?

The colors in the HTF probability table provide visual cues about the expected value (EV) of trading setups based on higher timeframe probabilities:

Blue: Suggests that entering a long position from the HTF user-defined pivot point, targeting buyside liquidity, is likely to result in a positive expected value (EV) based on historical data and sample size.

Red: Indicates that entering a short position from the HTF user-defined pivot point, targeting sellside liquidity, is likely to result in a positive expected value (EV) based on historical data and sample size.

Gray: Shows that neither long nor short trades from the HTF user-defined pivot point are expected to generate positive EV, suggesting that trading these setups may not be favorable.

----

How to use the indicator effectively?

For Amateur Traders:

Start Simple: Begin by focusing on one timeframe at a time with the pivot level set to the default (50%). This helps you understand the basic functionality of the indicator.

Entry and Exit Strategy: Focus on entering trades at the pivot level while targeting the higher probability side for take profit and the lower probability side for stop loss.

Use simulation or paper trading to practice this strategy.

Adjustments: Once you have a solid understanding of how the indicator works, you can start adjusting the pivot level to other values that suit your strategy.

Ensure that the RR labels are colored (blue or red) to indicate positive EV setups before executing trades.

For Advanced Traders:

1. Select Higher Timeframe Bias: Choose a higher timeframe (HTF) as your main bias. Start with the default pivot level and ensure the confidence level is above 95% to validate the probabilities.

2. Align Lower Timeframes: Switch between lower timeframes to identify which ones align with your predefined HTF bias. This helps in synchronizing your trading decisions across different timeframes.

3. Set Entries with Current Pivot Level: Use the current pivot level for trade entries. Ensure the HTF status label is active, indicating that the probabilities are valid and in play.

4. Target HTF Liquidity Level: Aim for liquidity levels that correspond to the higher timeframe, as these levels are likely to offer better trading opportunities.

5. Adjust Pivot Levels: As you gain experience, adjust the pivot levels to further optimize your strategy for high EV. Fine-tune these levels based on the aggregated data from multiple timeframes.

6. Practice on Paper Trading: Test your strategies through paper trading to eliminate discretion and refine your approach without financial risk.

7. Focus on Trade Management: Ultimately, effective trade management is crucial. Concentrate on managing your trades well to ensure long-term success. By aiming for setups that produce positive EV, you can position yourself similarly to how a casino operates.

----

🎲 Becoming the House (Gaining Edge Over the Market):

In American roulette, the house has a 5.26% edge due to the 0 and 00. This means that while players have a 47.37% chance of winning on even-money bets, the true odds are 50%. The discrepancy between the true odds and the payout ensures that, statistically, the casino will win over time.

From the Trader's Perspective: In trading, you gain an edge by focusing on setups with positive expected value (EV). If you have a 55.48% chance of winning with a 1:1 risk-to-reward ratio, your setup has a higher probability of profitability than the losing side. By consistently targeting such setups and managing your trades effectively, you create a statistical advantage, similar to the casino’s edge.

----

🎰 Applying the Concept to Trading:

Just as casinos rely on their mathematical edge, you can achieve long-term success in trading by focusing on setups with positive EV. By ensuring that your probabilities and risk-to-reward (RR) ratios are in your favor, you create an edge similar to that of the house.

And by systematically targeting trades with favorable probabilities and managing your trades effectively, you improve your chances of profitability over the long run. Which is going to help you “become the house” in your trading, leveraging statistical advantages to enhance your overall performance.

----

What makes this indicator original?

Real-Time Probability Calculations: The indicator provides real-time calculations of buy and sell probabilities based on historical data, allowing traders to assess the likelihood of positive expected value (EV) setups instantly.

Adjustable Pivot Levels: It features an adjustable pivot level that traders can modify according to their preferences, enhancing the flexibility to align with different trading strategies.

Multi-Timeframe Integration: The indicator supports up to 7 higher timeframes, displaying their probabilities and biases in a single view, which helps traders make informed decisions without switching timeframes.

Confidence Levels: It includes confidence levels based on sample sizes, offering insights into the reliability of the probabilities. Traders can gauge the strength of the data before making trades.

Dynamic EV Labels: The indicator provides color-coded EV labels that change based on the validity of the setup. Blue indicates positive EV in a long bias, red indicates positive EV in a short bias and gray signals caution, making it easier for traders to identify high-quality setups.

HTF Probability Table: The HTF probability table displays buy and sell probabilities from user-defined higher timeframes, helping traders integrate broader market context into their decision-making process.

----

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

Price Close ProbabilityThe Price Close Probability Indicator is designed to help traders estimate the likelihood of price closing above or below specified levels within a given bar. By placing two levels on your chart, you can quickly gauge the probability of the current price bar closing above or below these levels in real-time.

Key Features:

Dynamic Probability Calculation: The indicator continuously updates the probability of price closing above or below your set levels as the current bar progresses, providing you with timely insights as the bar approaches its close.

Customizable Standard Deviation : Adjust the length of the Standard Deviation used in the calculations to tailor the probability estimates to your preferred settings.

User-Friendly Probability Table : A clean, easy-to-read table displays the calculated probabilities, helping you make informed trading decisions at a glance.

Assumptions and Considerations:

While the indicator assumes that returns are normally distributed, which may not fully reflect reality, it still offers a valuable approximation of the probabilities for price movement within the current bar.

Future Enhancements (Coming Soon):

Multi-Bar Probability: Calculate probabilities across multiple bars to enhance your forecasting capabilities.

Additional Levels: Set more than two levels for a broader analysis of price movements.

Refined Distribution Modeling: Improve the accuracy of probability calculations by adjusting for more realistic return distributions.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

OrderFlow [Probabilities] | FractalystWhat's the indicator's purpose and functionality?

The indicator is designed to incorporate probabilities with buyside and sellside liquidity, as well as premium and discount ranges within the market. It also provides traders with a multi-timeframe functionality for observing liquidity levels and probabilities across two timeframes without the need to manually switch between them.

These levels are often used in smart money trading concepts for identifying key areas of interest, such as potential reversal points, areas of accumulation or distribution, and zones of high liquidity.

----

What's the purpose of these levels? What are the underlying calculations?

1. Understanding Swing highs and Swing Lows

Swing High: A Swing High is formed when there is a high with 2 lower highs to the left and right.

Swing Low: A Swing Low is formed when there is a low with 2 higher lows to the left and right.

2. Understanding the purpose and the underlying calculations behind Buyside , Sellside and Equilibrium levels.

3. Identifying Discount and Premium Zones.

4. Importance of Risk-Reward in Premium and Discount Ranges

----

How does the script calculate probabilities?

The script calculates the probability of each liquidity level individually. Here's the breakdown:

1. Upon the formation of a new range, the script waits for the price to reach and tap into equilibrium or the 50% level. Status: "⏸" - Inactive

2. Once equilibrium is tapped into, the equilibrium status becomes activated and it waits for either liquidity side to be hit. Status: "▶" - Active

3. If the buyside liquidity is hit, the script adds to the count of successful buyside liquidity occurrences. Similarly, if the sellside is tapped, it records successful sellside liquidity occurrences.

5. Finally, the number of successful occurrences for each side is divided by the overall count individually to calculate the range probabilities.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

----

What does the multi-timeframe functionality offer?

Enabling and selecting a higher timeframe in the indicator's user-input settings allows you to access not only the current range information but also the liquidity sides, status, price levels, and probabilities of a higher timeframe without needing to switch between timeframes and mark up the levels manually.

----

What are the multi-timeframe underlying calculations?

The script uses the same calculations (mentioned above) and requests the data such as price levels, bar time, probabilities and booleans from the user-input timeframe.

Non-repainting Security Function with Lookahead ON

//Function to fetch data for a given timeframe

getHTFData(timeframe_,exp_) =>

request.security(syminfo.tickerid, timeframe_,exp_ ,lookahead = barmerge.lookahead_on)

----

How to use the indicator?

1. Add the indicator to your TradingView chart.

2. Choose the pair you want to analyze/trade.

3. Enable the HTF in user-input settings and choose a timeframe as for your higher timeframe bias.

4. (Important) : Ensure that the probabilities on both timeframes are aligned in one direction. If not, switch between timeframes until you find a pair of timeframes that are in line with each other and have higher probabilities on one liquidity side.

For Swing traders:

Use Hourly timeframes (1H/2H/4H/8H/12H) as your current timeframe and 1D/3D/1W/2W for your higher timeframe (HTF).

Entry: Hourly Equilibrium level. (Limit order)

Stoploss: Place it on the side where the probability is lower than 50%.