Algo & Dark Pool Activity - Find Hidden LiquidityThe script is designed to highlight potential algorithmic buying pressure and dark pool accumulation proxies on a TradingView chart. It overlays signals directly on price bars so you can visually spot when unusual activity may be occurring.

M-VWAP

Triple ATR Adaptive MAs + VWAP Option + Clouds + Candle Trend V2Another one of my experiences ... combining things...

📘 Indicator Description – Triple ATR Adaptive Moving Averages with VWAP Influence

This indicator plots three adaptive moving averages whose behavior changes dynamically based on market volatility (ATR) and optionally VWAP deviation.

Because they adapt in real time to both volatility and VWAP pressure, their movement, slope, and reaction speed differ significantly from traditional moving averages.

🔶 1. ATR-Adaptive Moving Averages

Each of the three MAs uses a custom adaptive formula:

ATR (Average True Range) is measured over a chosen period.

Higher ATR → more volatility → the MA becomes more reactive and moves closer to price.

Lower ATR → stable market → the MA becomes smoother and slower.

This creates a volatility-aware smoothing factor, making the MA expand, contract, and respond to market conditions in ways a classic SMA, EMA, or HMA cannot.

🔷 2. Optional VWAP Influence

Each MA has an independent toggle allowing it to be influenced by VWAP.

When enabled:

The MA is gently “pulled” toward VWAP.

The strength of this attraction is determined by the VWAP Influence parameter (0–1).

This causes the moving averages to behave differently from normal MAs:

In trending markets, the ATR and price push the MA away from VWAP.

In mean-reverting or balanced conditions, VWAP pulls the MA back toward fair value.

The result is an MA that reflects both trend pressure and fair-value pressure.

🔶 3. Visual Behavior: Non-Traditional Movement

Because each MA is simultaneously influenced by volatility, trend magnitude, and VWAP deviation, their shape is often very distinct from normal moving averages.

They may:

Respond faster during high volatility

Flatten out earlier during consolidation

Curve toward VWAP when price becomes extended

Separate or compress depending on ATR strength

This is intentional and essential, since the goal is to show:

✔ Volatility expansion

✔ Trend exhaustion

✔ Overextended price relative to VWAP

✔ Dynamic trend confirmation

Rather than simply smoothing past price.

🔷 4. Three Independent Adaptive Lines

Each of the three moving averages has:

Its own ATR length

Its own sensitivity multiplier

Its own optional VWAP influence

Its own color and trail

This allows the user to combine:

a fast volatility-adaptive trend line

a mid-range adaptive baseline

a slow adaptive long-trend MA

All adapting independently to volatility and VWAP conditions.

🔶 5. Optional Candle Coloring

The indicator can color candles according to trend strength derived from the fast/slow MAs.

Stronger trends produce more vivid colors. Neutral or conflicting trends produce softer colors.

This adds a visual layer to identify:

Trend direction

Trend strength

Volatility state

Market compression

at a glance.

📌 Summary

This indicator does not behave like standard SMAs or EMAs because each line dynamically adapts to:

🔸 ATR (volatility)

🔸 VWAP (fair value)

This makes the indicator extremely responsive to market conditions while still reducing noise during stable phases.

It provides a more realistic, context-aware, and intelligent representation of price behavior compared to traditional moving averages.

SMAs TimePortalPlots 5× SMAs from 3 different timeframes - plus current chart timeframe

Plots 2× VWAPs with bands.

Meant for personal use, but maybe you can find it useful too.

Disclaimer: Beware I might update this with big changes in the future.

Luxy VWAP Magic - MTF Projection EngineThis indicator transforms the classic VWAP into a comprehensive trading system. Instead of switching between multiple indicators, you get everything in one place: multi-timeframe analysis, statistical bands, momentum detection, volume profiling, session tracking, and divergence signals.

What Makes This Different

Traditional VWAP indicators show a single line. This tool treats VWAP as a foundation for complete market analysis. The indicator automatically detects your asset type (stocks, crypto, forex, futures) and adjusts its behavior accordingly. Crypto traders get 24/7 session tracking. Stock traders get proper market hours handling. Everyone gets institutional-grade analytics.

Anchor Period Options

The anchor period determines when VWAP resets and recalculates. You have three categories of options:

Time-Based Anchors:

Session - Resets at market open. Best for intraday stock trading where you want fresh VWAP each day.

Day - Resets at midnight UTC. Standard option for most traders.

Week / Month / Quarter / Year - Longer reset periods for swing traders and position traders who want broader context.

Rolling Window Anchors:

Rolling 5D - A sliding 5-day window that never resets. Solves the Monday problem where weekly VWAP equals daily VWAP on first day of week.

Rolling 21D - Approximately one month of trading data in continuous calculation. Excellent for crypto and forex markets that trade 24/7 without clear session breaks.

Event-Based Anchors:

Dividends - Resets on ex-dividend dates. Track institutional cost basis from dividend events.

Splits - Resets on stock split dates. Useful for analyzing post-split trading behavior.

Earnings - Resets on earnings report dates. See where volume-weighted trading occurred since last quarterly report.

Standard Deviation Bands

Three sets of bands surround the main VWAP line:

Band 1 (Aqua) - Plus and minus one standard deviation. Approximately 68% of price action occurs within this range under normal distribution. Touches suggest minor extension.

Band 2 (Fuchsia) - Plus and minus two standard deviations. Only 5% of trading should occur outside this range statistically. Touches here indicate significant overextension and high probability of mean reversion.

Band 3 (Purple) - Plus and minus three standard deviations. Touches are rare (0.3% probability) and represent extreme conditions. Often marks climax moves or panic selling/buying.

Each band can be toggled independently. Most traders show Band 1 by default and add Band 2 and 3 for specific setups or volatile instruments.

Multi-Timeframe VWAP System

The MTF section plots previous period VWAPs as horizontal support and resistance levels:

Daily VWAP - Previous day's final VWAP value. Key intraday reference level.

Weekly VWAP - Previous week's final VWAP. Important for swing traders.

Monthly VWAP - Previous month's final VWAP. Institutional benchmark level.

Quarterly VWAP - Previous quarter's final VWAP. Major support/resistance for position traders.

Previous Day VWAP - Yesterday's closing VWAP specifically, separate from current daily calculation.

The Confluence Zone percentage setting determines how close multiple VWAPs must be to trigger a confluence alert. When two or more timeframe VWAPs converge within this threshold, you get a high-probability support/resistance zone.

Session VWAPs for Global Markets

For forex, crypto, and futures traders who operate in 24/7 markets, the indicator tracks three major global sessions:

Asia Session - UTC 21:00 to 08:00. Gold colored line. Typically lower volatility, range-bound action that sets overnight levels.

London Session - UTC 08:00 to 17:00. Orange colored line. Often determines daily direction with high volume European participation.

New York Session - UTC 13:00 to 22:00. Blue colored line. Highest volume session globally. Sharp directional moves common.

Previous session VWAP values display as horizontal lines when each session closes, acting as intraday support and resistance. The table shows which sessions are currently active with checkmarks.

On-Chart Labels and Signals

The indicator plots several types of labels directly on price action when significant events occur:

Volume Spike Labels

Fire when current bar volume exceeds configurable thresholds relative to both the previous bar and the 20-bar average. Default settings require 300% of previous bar AND 200% of average volume. Green labels indicate bullish candles. Red labels indicate bearish candles. These spikes often mark institutional entry points.

Momentum Shift Labels

Appear when VWAP acceleration changes direction. The Slowing label warns when an active trend loses steam, often preceding reversal. The Accelerating label confirms trend continuation or potential bottom during downtrends. Filters available to show only reversal signals in existing trends.

VWAP Squeeze Labels

Detect when standard deviation bands contract relative to ATR (Average True Range). Low volatility compression often precedes explosive breakout moves. When the squeeze fires (releases), a label appears with directional prediction based on VWAP slope.

Divergence Labels

Mark price/volume divergences using CVD (Cumulative Volume Delta) analysis:

Bullish divergence: Price makes lower low, but CVD makes higher low. Hidden accumulation despite price weakness.

Bearish divergence: Price makes higher high, but CVD makes lower high. Hidden distribution despite price strength.

Dynamic VWAP Coloring

The main VWAP line changes color based on its slope direction:

Green - VWAP is rising. Institutional buying pressure. Volume-weighted price increasing.

Red - VWAP is falling. Institutional selling pressure. Volume-weighted price decreasing.

Gray - VWAP is flat. Consolidation or balance between buyers and sellers.

This coloring can be disabled for a static blue line if you prefer cleaner visuals. The VWAP label next to the line shows the current trend direction and delta percentage.

Calculated Projection Cone

One of the most powerful features is the Calculated Projection Cone. Unlike traditional extrapolation methods that simply extend a trend line forward, this system analyzes what actually happened in similar market conditions throughout the chart's history.

How It Works:

The system classifies each bar into one of 27 unique market states:

Z-Score Level - LOW (oversold), MID (fair value), or HIGH (overbought) based on configurable thresholds

Trend Direction - DOWN, FLAT, or UP based on VWAP slope

Volume Profile - LOW (below 80%), NORMAL (80-150%), or HIGH (above 150%) relative volume

When you look at the current bar, the indicator:

1. Identifies the current market state (e.g., LOW Z-Score + UP Trend + HIGH Volume)

2. Searches through all historical bars on the chart that had the same state

3. Calculates what happened in those bars X bars later (where X is your projection horizon)

4. Shows you the probability of up/down and the average move size

Visual Elements:

Probability Cone - Colored green (bullish probability above 55%), red (bearish below 45%), or gold (neutral). The cone width represents the historical range of outcomes (roughly the 20th to 80th percentile).

Center Line - Shows the average expected price based on historical outcomes in similar conditions.

Probability Label - Displays direction probability and average move. Example: "67% UP (+0.8%)" means 67% of similar past cases moved up, averaging 0.8% gain.

Fallback System:

When the exact 27-state match has insufficient historical data:

First fallback: Uses Z-Score plus Trend only (9 broader states, ignoring volume)

Second fallback: Uses Z-Score only (3 states)

When fallback is active, confidence automatically adjusts

Settings:

Projection Horizon - How many bars forward to analyze outcomes (5, 10, 15, or 20 bars, default 10)

Lookback Period - Historical data window in days (30-252, default 60)

Minimum Samples - Cases needed before using fallback (5-30, default 10)

Z-Score Threshold - Bucket boundary for LOW/MID/HIGH classification (1.0, 1.5, or 2.0 sigma)

Cloud Transparency - Adjust visibility (50-95%)

Colors - Customize bullish, bearish, and neutral cone colors

Confidence Levels:

HIGH - 30 or more similar historical cases found

MEDIUM - 15-29 similar cases

LOW - Fewer than 15 cases (more uncertainty)

IMPORTANT DISCLAIMER:

The Calculated Projection is based on past patterns only. It is NOT a price prediction or financial advice. Similar market states in the past do not guarantee similar outcomes in the future. The probability shown is historical frequency, not a guarantee. Always combine with other analysis and never rely solely on projections for trading decisions.

Alert Conditions

The indicator includes over 20 pre-built alert conditions:

Price vs VWAP:

Price crosses above VWAP

Price crosses below VWAP

Band Touches:

Price touches plus or minus one sigma band

Price touches plus or minus two sigma band (extreme)

Price touches plus or minus three sigma band (very extreme)

Z-Score Extremes:

Z-Score crosses above plus two (overbought extreme)

Z-Score crosses below minus two (oversold extreme)

Momentum and Trend:

Momentum slowing

Momentum accelerating

Trend turns bullish/bearish/neutral

Volume:

Volume spike detected

CVD Direction:

Buyers take control

Sellers take control

High Probability Signals:

Bullish reversal signal (oversold plus accelerating momentum)

Bearish reversal signal (overbought plus slowing momentum)

MTF and Special:

MTF confluence zone entry

VWAP squeeze fired

Bullish/Bearish divergence detected

Any significant signal (catch-all)

All signals use confirmed bar data to prevent false alerts from incomplete candles.

Settings Overview

Settings are organized into logical groups:

VWAP Settings

Anchor Period selection

Show/Hide VWAP line

Dynamic coloring toggle

VWAP label visibility

Bands Visibility

Toggle each of three bands independently

Info Table

Show/Hide table

Table position (9 options)

Text size

Volume spike label settings with adjustable thresholds

Momentum label settings with filters

Signal labels limited to 5 most recent (auto-managed)

Probability engine lookback period

Multi-Timeframe VWAP

Enable/Disable MTF system

Show MTF in table

Show MTF lines on chart

Individual timeframe toggles

Confluence zone threshold

Squeeze detection toggle

Session VWAPs

Enable/Disable session tracking

Apply to all assets option

Show session labels

Divergence Detection

Enable/Disable divergence

Pivot lookback period

Show divergence labels

Calculated Projection

Enable/Disable projection cone

Projection horizon (5, 10, 15, or 20 bars)

Lookback period in days (30-252)

Minimum samples threshold

Z-Score classification threshold (1.0, 1.5, or 2.0 sigma)

Cloud transparency adjustment

Bullish, bearish, and neutral colors

The Info Table - Your Trading Dashboard

The right side of your chart displays a compact table with up to twelve metrics.

Row-by-Row Breakdown:

Asset and Period - Shows what the indicator detected (US Stock, Crypto, Forex, etc.) and your selected anchor period. The detection happens automatically based on exchange data, so VWAP resets and calculations match your actual trading instrument.

Delta Percentage - How far current price sits from VWAP, expressed as a percentage. Positive means price trades above fair value. Negative means below. Large delta values (beyond 1-2%) often precede mean reversion moves. Day traders watch this for overextension.

Z-Score - Statistical deviation from VWAP measured in standard deviations. Unlike raw delta, Z-Score accounts for volatility. A 2% move in a volatile biotech stock differs from 2% in a stable utility. Z-Score normalizes this. Values beyond plus or minus two sigma occur only 5% of the time statistically.

Trend Direction - Whether VWAP itself is rising, falling, or flat. Rising VWAP means the volume-weighted average price is increasing, which indicates institutional accumulation. Falling VWAP suggests distribution. This differs from price trend since it weights by volume.

Momentum State - Is the trend accelerating or slowing down? This measures the rate of change in VWAP slope. When an uptrend shows slowing momentum, it often precedes reversal. Accelerating momentum in a downtrend can signal capitulation and potential bottom.

Relative Volume - Current bar volume compared to the 20-bar average, shown as percentage. Values above 150% indicate above-average activity. Spikes above 200-300% often mark institutional involvement. Low volume (below 80%) warns of potential fake moves.

MTF Bias - Four checkmarks or X marks showing whether price sits above or below Daily, Weekly, Monthly, and Quarterly VWAP. Four checkmarks means strong bullish alignment across all timeframes. Four X marks indicates bearish alignment. Mixed readings suggest consolidation or transition.

Band Probabilities - Historical statistics showing how often price touched each standard deviation band over your lookback period. This helps you understand if mean reversion or trend following works better for your specific instrument.

Session Status - Which global trading sessions are currently active (Asia, London, New York). Shows checkmarks for active sessions. Important for forex and crypto traders who need to know when major liquidity windows open and close.

Divergence State - Whether the indicator detects bullish or bearish divergence between price and cumulative volume delta. Bullish divergence occurs when price makes lower lows but buying pressure (CVD) makes higher lows, suggesting hidden accumulation.

Confidence Score - A weighted composite of all factors displayed as a progress bar and percentage. Combines MTF alignment, Z-Score, trend direction, volume delta, momentum, and relative volume into a single 0-100 score. Higher scores indicate stronger conviction setups.

Calculated Projection - When the Projection Cone is enabled, shows the historical probability of price direction and expected move. For example: "▲ 67% (+0.8%)" means in similar market states historically, price moved up 67% of the time with an average gain of 0.8%. The system analyzes 27 unique market states based on Z-Score, Trend, and Volume conditions.

Recommended Use Cases

Day Trading Stocks:

Use Session anchor with Band 1 visible. Watch for price returning to VWAP after morning move. Volume spikes near VWAP often mark institutional accumulation zones.

Swing Trading:

Use Weekly or Rolling 21D anchor. Enable MTF lines for Daily and Weekly levels. Trade pullbacks to these levels in direction of MTF bias.

Crypto and Forex:

Enable Session VWAPs. Use Rolling anchors to avoid artificial resets. Monitor session transitions for breakout opportunities.

Mean Reversion:

Focus on Z-Score reaching plus or minus two. Add Band 2 visibility. Combine with slowing momentum for highest probability reversals.

Trend Following:

Watch MTF bias alignment. Four checkmarks plus accelerating momentum plus high volume confirms trend continuation setups.

Projection Planning:

Enable the Calculated Projection to see what happened historically in similar market conditions. Use 5-10 bars for intraday setups, 15-20 bars for swing trade planning. Focus on high probability readings (above 60%) with HIGH confidence (30 or more samples). The cone shows the probable range of outcomes based on actual historical data. Combine with other factors like MTF alignment and volume for higher conviction setups.

Important Notes

The indicator does not repaint. MTF values use previous period's confirmed data.

Rolling VWAP works best on 15-minute timeframes and above due to bar lookback requirements.

Session VWAPs apply to global markets by default (forex, crypto, futures). Enable the all-assets option for stocks if desired.

Volume data for forex represents tick volume, not actual traded volume.

All alert conditions fire only on confirmed (closed) bars to prevent false signals.

The Calculated Projection updates each bar as market state changes. This is expected behavior. The projection shows probabilities based on similar past conditions, not a fixed prediction.

Q AND A

Q: Does this indicator repaint?

A: No. The main VWAP calculation uses standard TradingView VWAP methodology. Multi-timeframe values use previous period's confirmed data with appropriate lookahead settings. All alert signals require bar confirmation.

Q: Why does my Rolling VWAP look different on 1-minute versus 15-minute charts?

A: Rolling VWAP calculates across a fixed number of trading days. On very short timeframes, the bar lookback may hit TradingView limits. For best Rolling VWAP accuracy, use 15-minute or higher timeframes.

Q: Can I use this on any instrument?

A: Yes. The indicator automatically detects asset type and adjusts behavior. Stocks use standard market hours. Crypto uses 24/7 calculations. Forex uses tick volume. Everything adapts automatically.

Q: What does the Confidence Score actually measure?

A: The score combines six weighted factors: MTF alignment (25%), Z-Score position (20%), Trend direction (20%), CVD pressure (15%), Momentum state (10%), and Relative volume (10%). Higher scores indicate more factors aligned in one direction.

Q: Why are Session VWAPs not showing on my stock chart?

A: Session VWAPs apply to 24-hour markets by default (forex, crypto, futures). For stocks, enable the Use for All Assets option in Session VWAP settings.

Q: The Divergence labels appear delayed. Is this a bug?

A: Divergence detection requires pivot confirmation, which needs bars on both sides of the pivot point. The label appears at the actual pivot location (several bars back) once confirmed. This is intentional and prevents false signals.

Q: Can I change the band colors?

A: Yes. Each of the three bands has its own color input setting. You can customize Band 1, Band 2, and Band 3 colors to match your preferences. The defaults are Aqua, Fuchsia, and Purple. The main VWAP line color adapts dynamically based on slope direction or can be set to static blue.

Q: How do I set up alerts?

A: Right-click on the chart, select Add Alert, choose this indicator, and select your desired condition from the dropdown. All conditions include descriptive alert messages with relevant data.

Q: What is the Probability Engine lookback period?

A: This setting determines how many trading days the indicator analyzes to calculate band touch rates and mean reversion statistics. Default is 60 days (approximately 3 months). Longer periods provide more stable statistics but may miss recent behavior changes.

Q: Why do I see fewer labels than expected?

A: Signal labels (Volume, Momentum, Squeeze, Divergence) are limited to 5 most recent labels on the chart to keep it clean. When a new label appears, the oldest one is automatically removed. Additionally, momentum labels have several filters: check the slope multiplier setting (higher values require stronger trends) and the Only Reversal Signals option (when enabled, labels only appear for potential reversals, not trend confirmations).

Q: What is the Calculated Projection and how accurate is it?

A: The Calculated Projection analyzes what happened in past market conditions similar to the current state. It classifies each bar by Z-Score level, Trend direction, and Volume profile (27 unique states), then shows the historical probability of up vs down and the average move size. It is NOT a price prediction or guarantee. The probability shown is how often similar conditions led to up/down moves historically, not a future guarantee. Always use it as one input among many.

Q: Why does the Projection probability change?

A: The projection updates on each bar as market state changes. If Z-Score moves from LOW to MID, or trend shifts from UP to FLAT, the system looks up a different historical category. This is expected behavior. The projection shows what happened in similar past conditions to the current bar's state.

Q: The Projection shows LOW confidence. What does that mean?

A: Confidence levels indicate sample size: HIGH means 30 or more historical cases found, MEDIUM means 15-29 cases, LOW means fewer than 15 cases. When sample size is low, the system uses a fallback: first aggregating by Z-Score plus Trend only (ignoring volume), then by Z-Score only. LOW confidence means less statistical reliability, so weight other factors more heavily in your decision.

Q: Why does the cone sometimes show 50/50 probability?

A: A 50/50 reading means that in similar past market states, price moved up roughly half the time and down half the time. This indicates a neutral or balanced condition where historical patterns provide no directional edge. Consider waiting for a higher probability setup or using other analysis methods.

CREDITS AND ACKNOWLEDGMENTS

Methodology Foundation:

VWAP (Volume Weighted Average Price) - Standard institutional benchmark calculation, widely used since the 1980s for algorithmic execution and fair value assessment

Standard Deviation Bands - Statistical volatility measurement applying normal distribution principles to price deviation from mean

Z-Score Analysis - Classic statistical normalization technique for comparing values across different volatility regimes

Cumulative Volume Delta (CVD) - Order flow analysis concept measuring aggressive buying versus selling pressure

Concept Integration:

Mean reversion probability engine - Custom historical statistics tracking for band touch rates

Momentum acceleration detection - Second derivative analysis of VWAP slope changes

VWAP Squeeze - Volatility compression concept adapted from TTM Squeeze methodology applied to VWAP bands versus ATR

Confidence scoring system - Weighted composite scoring combining multiple technical factors

Calculated Projection Cone - Probability-based projection using 27-state market classification (Z-Score, Trend, Volume) with historical outcome analysis and weighted fallback system

All calculations use standard public domain formulas and TradingView built-in functions. No proprietary third-party code was used.

For questions, feedback, or feature requests, please comment below or send a private message.

Happy Trading!

Session VWAPs [cryptalent]This indicator provides a more granular and timely analysis of market structure compared to traditional daily Volume Weighted Average Price (VWAP). It splits the 24-hour trading day into four distinct, customizable sessions (T1, T2, T3, T4), calculating an independent Session VWAP and Standard Deviation Bands for each segment.

🌟 Key Features and Functionality

1. Segmented VWAP Calculation

Purpose: To track the true Volume Weighted Average Price (Fair Value) specific to the participants and trading activities within different global market sessions (e.g., Asian, European, US sessions).

Design: By default, the 24 hours (based on UTC time) are divided into T1 (00:00-06:00), T2 (06:00-12:00), T3 (12:00-20:00), and T4 (20:00-00:00).

Mechanism: The VWAP calculation resets at the start of each designated session, offering a clearer, segment-specific view of market consensus and volume absorption.

2. Standard Deviation Bands

Calculation: Each Session VWAP line is accompanied by upper and lower standard deviation bands.

Control: The width of these bands is controlled by the user input "Band Multiplier" (default is 1.0, representing one standard deviation).

Application: These bands measure the Volume-Weighted Volatility and define the expected "normal" trading range for the current session.

- Price within the bands suggests consolidation or a normal auction process.

- Price breaking out of the bands indicates strong directional momentum or an extreme/overbought/oversold condition for that specific session.

3. High Customization (User Inputs)

Session Timing: All four session start and end times (in UTC) are customizable, allowing traders to align the indicator with specific market hours or individual trading strategies.

Price Source: The source price used for the VWAP calculation is selectable (default is close).

💡 Trading Applications

1. Fair Value Identification: The VWAP line serves as the "Fair Value" or "Volume-Weighted Consensus Cost" for the active session.

Price above VWAP: Buyers are in control during that session.

Price below VWAP: Sellers are in control during that session.

2. Dynamic Support & Resistance: Both the VWAP and the Standard Deviation Bands often act as reliable dynamic support and resistance levels.

3. Volatility Assessment: The width of the bands reflects the volume-weighted volatility of the current session. Narrow bands suggest range-bound trading; wide bands imply strong directional activity.

4. Trend Strength: Sustained price action outside of the standard deviation bands is a key measure of the strength and commitment behind a current trend.

Aydan ScalperBy when EMA 8 cross EMA 21 from Below to Abouve and SELL when EMA 21 cross EMA 8 from Abouve to Belove

VWAP 1SD 2SD yasurferThis custom intraday indicator is designed to provide a detailed understanding of market equilibrium, volatility expansion, and trend structure by combining Session VWAP, Standard Deviation bands, and multi-timeframe EMAs. The script calculates cumulative volume-weighted price data throughout the trading day and automatically resets at the start of each new session. This ensures that the Session VWAP reflects only current-day trading activity, making it highly relevant for scalpers, day traders, and intraday swing setups.

The ±2 Standard Deviation bands illustrate where price is statistically stretched. These zones often act as areas of exhaustion, liquidity grabs, or potential momentum continuation points. By tracking variance around VWAP, the indicator helps traders quickly identify whether price is trading within a normal distribution or pushing into extreme territory.

A dynamic label displays the real-time percentage distance from VWAP, allowing traders to assess how far price has deviated from fair value. This is particularly useful for identifying overextended moves, mean-reversion opportunities, or breakout conditions.

The addition of EMA 50, EMA 200, and EMA 325 provides structural trend context—helping traders evaluate higher-timeframe alignment and potential confluence with VWAP levels. Overall, this indicator enhances clarity, timing, and decision-making by blending statistical tools with traditional trend analysis.

Institutional VWAP Suite (Lite Compatible)The **Institutional VWAP Suite (Lite Compatible)** brings true institutional volume-weighted price analysis to every trader — even on TradingView Lite/Free accounts where standard VWAP tools are restricted.

This script recreates the most important VWAP models used by banks, funds, and high-frequency desks, including:

• **Daily VWAP** (exchange-accurate)

• **Weekly VWAP** (manually accumulated)

• **Monthly VWAP** (manually accumulated)

• **Rolling Window VWAP** (array-based, fully Lite-compatible)

All calculations avoid blocked functions like `ta.sum` or session-restricted VWAP calls. Everything is built manually from volume and price to ensure accuracy across all accounts and all markets.

### Features

• Multi-timeframe VWAPs (Daily/Weekly/Monthly)

• Manual Rolling VWAP with adjustable length

• Optional VWAP bands (Lite-safe)

• Clean visuals with color-coded levels

• Optimized arrays for fast, stable performance

• Free-tier compatible — no premium functions required

This tool is designed for traders who want institutional structure, premium-level VWAP calculations, and consistent execution regardless of plan level. Perfect for scalpers, day traders, futures traders, and anyone who uses intraday volume profiles.

### Recommended Use

• Map directional bias using Daily vs Weekly VWAP

• Use Monthly VWAP for macro trend context

• Track intraday mean reversion with Rolling VWAP

• Use VWAP bands as dynamic support/resistance zones

A simple, powerful, no-restrictions VWAP engine — built for everyone.

FAIRPRICE_VWAP_RDFAIRPRICE_VWAP_RD

This script plots an **anchored VWAP (Volume Weighted Average Price)** that resets

based on the user-selected anchor period. It acts as a dynamic “fair value” line

that reflects where the market has actually transacted during the chosen period.

FEATURES

- Multiple anchor options: Session, Week, Month, Quarter, Year, Decade, Century,

Earnings, Dividends, or Splits.

- Intelligent handling of the “Session” anchor so it works correctly on both 1m

(resets each new day) and 1D (continuous, non-resetting VWAP).

- Manual VWAP calculation using cumulative(price * volume) and cumulative(volume),

ensuring the line is stable and works on all timeframes.

- Optional hiding of VWAP on daily or higher charts.

- Offset input for horizontal shifting if desired.

- VWAP provides a true “fair price” reference for trend, mean-reversion,

and institutional-level analysis.

PURPOSE

This indicator solves the common problem of VWAP behaving incorrectly on higher

timeframes, on synthetic data, or with unusual anchors. By implementing VWAP

manually and allowing flexible reset conditions, it functions reliably as

an institutional-style fair value benchmark across any timeframe.

Custom MTF VWAP 5x This is a combination of all VWAPs I use to find high probability trade setups and targets by only taking trades when different VWAPs align

Moving VWAP-KAMA CloudMoving VWAP-KAMA Cloud

Overview

The Moving VWAP-KAMA Cloud is a high-conviction trend filter designed to solve a major problem with standard indicators: Noise. By combining a smoothed Volume Weighted Average Price (MVWAP) with Kaufman’s Adaptive Moving Average (KAMA), this indicator creates a "Value Zone" that identifies the true structural trend while ignoring choppy price action.

Unlike brittle lines that break constantly, this cloud is "slow" by design—making it exceptionally powerful for spotting genuine trend reversals and filtering out fakeouts.

How It Works

This script uses a unique "Double Smoothing" architecture:

The Anchor (MVWAP): We take the standard VWAP and smooth it with a 30-period EMA. This represents the "Fair Value" baseline where volume has supported price over time.

The Filter (KAMA): We apply Kaufman's Adaptive Moving Average to the already smoothed MVWAP. KAMA is unique because it flattens out during low-volatility (choppy) periods and speeds up during high-momentum trends.

The Cloud:

Green/Teal Cloud: Bullish Structure (MVWAP > KAMA)

Purple Cloud: Bearish Structure (MVWAP < KAMA)

🔥 The "Reversal Slingshot" Strategy

Backtests reveal a powerful behavior during major trend changes, particularly after long bear markets:

The Resistance Phase: During a long-term downtrend, price will repeatedly rally into the Purple Cloud and get rejected. The flattened KAMA line acts as a "concrete ceiling," keeping the bearish trend intact.

The Breakout & Flip: When price finally breaks above the cloud with conviction, and the cloud flips Green, it signals a structural regime change.

The "Slingshot" Retest: Often, immediately after this flip, price will drop back into the top of the cloud. This is the "Slingshot" moment. The old resistance becomes new, hardened support.

The Rally: From this support bounce, stocks often launch into a sustained, multi-month bull run. This setup has been observed repeatedly at the bottom of major corrections.

How to Use This Indicator

1. Dynamic Support & Resistance

The KAMA Wall: When price retraces into the cloud, the KAMA line often flattens out, acting as a hard "floor" or "wall." A break of this wall usually signals a genuine trend change, not just a stop hunt.

2. Trend Confirmation (Regime Filter)

Bullish Regime: If price is holding above the cloud, only look for Long setups.

Bearish Regime: If price is holding below the cloud, only look for Short setups.

No-Trade Zone: If price is stuck inside the cloud, the market is traversing fair value. Stand aside until a clear winner emerges.

3. Multi-Timeframe Versatility

While designed for trend confirmation on higher timeframes (4H, Daily), this indicator adapts beautifully to lower timeframes (5m, 15m) for intraday scalping.

On Lower Timeframes: The cloud reacts much faster, acting as a dynamic "VWAP Band" that helps intraday traders stay on the right side of momentum during the session.

Settings

Moving VWAP Period (30): The lookback period for the base VWAP smoothing.

KAMA Settings (10, 10, 30): Controls the sensitivity of the adaptive filter.

Cloud Transparency: Adjust to keep your chart clean.

Alerts Included

Price Cross Over/Under MVWAP

Price Cross Over/Under KAMA

Cloud Flip (Bullish/Bearish Trend Change)

Tip for Traders

This is not a signal entry indicator. It is a Trend Conviction tool. Use it to filter your entries from faster indicators (like RSI or MACD). If your fast indicator signals "Buy" but the cloud is Purple, the probability is low. Wait for the Cloud Flip

Volume weighted average price band strategy [Kevin-Patrick]VWAP Bands strategy, Credit

VWAP Machine Learning Bands is an advanced indicator designed to enhance trading analysis by integrating VWAP with a machine learning-inspired adaptive smoothing approach. This tool helps traders identify trend-based support and resistance zones, predict potential price movements, and generate dynamic trade signals.

Key Features

Adaptive ML VWAP Calculation: Uses a dynamically adjusted SMA-based VWAP model with volatility sensitivity for improved trend analysis.

Forecasting Mechanism: The 'Forecast' parameter shifts the ML output forward, providing predictive insights into potential price movements.

Volatility-Based Band Adjustments: The 'Sigma' parameter fine-tunes the impact of volatility on ML smoothing, adapting to market conditions.

Multi-Tier Standard Deviation Bands: Includes two levels of bands to define potential breakout or mean-reversion zones.

Dynamic Trend-Based Colouring: The VWAP and ML lines change colour based on their relative positions, visually indicating bullish and bearish conditions.

Custom Signal Detection Modes: Allows traders to choose between signals from Band 1, Band 2, or both, for more tailored trade setups.

+ Strategy setting by Kevin-Patrick

Dynamic Fair-Value Ribbon Pro @darshakssc1. What This Indicator Is (In Simple Terms)

The Dynamic Fair-Value Ribbon Pro is a visual tool that helps you see how price behaves around a statistically derived “fair-value zone”:

A colored ribbon/cloud marks a central “fair” area.

Areas above the ribbon are labeled as “Unfair High Zone”.

Areas below the ribbon are labeled as “Unfair Low Zone”.

A small state panel tells you where price currently sits relative to this ribbon.

All calculations are based only on historical price, volume, and volatility.

It does not predict future price, does not give buy/sell signals, and is not financial advice.

2. Adding the Indicator

Open a chart on TradingView.

Click on Indicators .

Search for “Dynamic Fair-Value Ribbon Pro” .

Click to add it to your chart.

You will see:

A cloud/ribbon around price.

Colored bars when price is outside the ribbon.

A panel in the top right describing the current state.

3. Core Concept: Fair vs Unfair Zones (Analytical Only)

The indicator tries to answer a descriptive question:

“Where is price trading relative to a historically derived central area?”

It does this by:

Calculating a central value (“fair mid”).

Building a band around that mid.

Coloring the chart depending on whether price is inside or outside that band.

It is not claiming that:

Price “must” return to the band.

Price is “overvalued” or “undervalued”.

Any state is good or bad.

It is simply a visual classification tool .

4. Engine Modes — How the Ribbon Is Calculated

Under “Fair-Value Engine” you can choose:

4.1 Mode 1: Range

Looks back over a chosen number of bars (default: 100).

Finds the highest high and lowest low in that window.

Defines a central “slice” of that range as the fair-value ribbon :

Range Mode: Lower Percent → bottom boundary of the slice (e.g., 30%).

Range Mode: Upper Percent → top boundary of the slice (e.g., 70%).

Effect:

The ribbon represents a middle portion of the historical range .

Above the ribbon = “Unfair High Zone” (analytical label only).

Below the ribbon = “Unfair Low Zone”.

This is purely statistical — it does not mean price is wrong or will revert.

4.2 Mode 2: VWAP + Stdev

In this mode, the central value is based on VWAP :

VWAP (Volume-Weighted Average Price) is used as the midline.

A standard deviation envelope is built around VWAP:

VWAP Mode: Stdev Multiplier controls how wide that envelope is.

Effect:

The ribbon shows where price is trading relative to a volume-weighted average .

Again, areas above and below are just described as “unfair” zones in a visual, analytical sense , not a predictive one.

5. ATR Adaptive Width — Making the Ribbon React to Volatility

Under “ATR Adaptive Width” :

Use ATR Adaptive Width:

On: the band width scales with volatility.

Off: band width stays fixed based on Range or VWAP settings.

ATR Length: how many bars to use for ATR.

Reference ATR (% of price): a reference level for normal volatility.

Min Width Scale / Max Width Scale: clamps the scaling so that the band doesn’t get too narrow or too wide.

What this does (analytically):

When volatility (ATR) is higher than the reference, the band can become wider .

When volatility is lower , the band can become narrower .

This is a mathematical rescaling only and does not imply any optimal levels or performance.

6. Visual Elements — What You See on the Chart

6.1 Fair-Value Ribbon (Cloud)

The cloud between Fair Ribbon Low and Fair Ribbon High is the fair zone .

Color can be changed via “Fair Ribbon Color” .

6.2 Midline

If “Show Center Line” is enabled:

A line runs through the middle of the ribbon.

In Range mode, this is the average of the upper and lower band.

In VWAP mode, it’s essentially the VWAP-based mid.

This line is for visual reference only and makes no claims about support, resistance, or reversion.

6.3 Bar Colors

Unfair High Zone: bars are colored with Unfair High Bar Color.

Unfair Low Zone: bars are colored with Unfair Low Bar Color.

Inside the ribbon:

If “Fade Bars Inside Fair Zone” is ON, bars may be more faded/neutral.

These colors are simply classification highlights ; they do not tell you what to do.

6.4 State Panel (Top Right)

If “Show State Panel” is enabled, you’ll see a small box that displays:

Current engine:

Range or VWAP+Stdev.

Current price state:

Inside Ribbon (Fair Zone)

Above Ribbon (Unfair High Zone)

Below Ribbon (Unfair Low Zone)

This is a quick summary of where price sits relative to the computed ribbon.

7. Typical Ways to Use It (Informational Only)

The indicator can help you visually:

See when price is spending time inside a historically defined central zone.

Notice when price is frequently trading outside that zone.

Compare different timeframes (e.g., 5m vs 1h vs 4h) to see how the fair zone shifts.

Experiment with:

Range length (shorter vs longer lookback).

VWAP vs Range mode.

ATR adaptation on/off.

Important:

Any interpretation of these visuals is entirely up to the user.

The script does not tell you to buy, sell, hold, or do anything specific.

8. Limitations and Important Notes

All calculations use past data only (price, volume, volatility).

The ribbon does not guarantee:

that price will revert,

that zones will hold,

or that any outcome will occur.

There are no built-in signals such as “long/short” or automatic entries/exits.

The script is best used as a supporting, visual layer alongside other tools or methods you choose.

9. Disclaimer

This indicator is:

Strictly informational and educational.

Not a trading system or strategy.

Not financial advice or a recommendation.

Not guaranteed to be accurate, complete, or suitable for any specific purpose.

Users should always perform their own research and due diligence.

Past behavior of any visual pattern or zone does not guarantee future behavior.

Volume Weighted Average Price AdvancedVWAP (Advanced) with Multi‑Venue Aggregation and Historical Value Areas

Core: Anchored VWAP with configurable anchor (session/week/month/quarter/year/decade/century or corporate events), offset, and up to three standard-deviation bands.

Multi‑Venue Aggregation: Optionally pull price/volume from up to 5 additional exchanges/symbols (pair-matched by default). VWAP/σ are computed on the aggregated price*volume.

Value Area Blocks: Each completed anchor draws a block from the chosen basis (±1σ or ±2σ) or an optional percentile-based range (default 20–80%). Blocks project to the exact next anchor boundary, or you can extend them to the latest bar. Prior-period VWAP lines are shown inside the blocks.

Volume Gate: Optionally skip drawing prior blocks when the anchor’s aggregated volume is below a median/mean baseline times a multiplier.

HTF Context: Optional higher-timeframe VWAP overlay; can filter the current VWAP/bands so they only show when aligned with the HTF VWAP.

Venue Health: Label shows how many extra venues were included (non‑na) and median venue volume; flags divergence when primary volume is below venue median × threshold.

Alerts: Price in current value area (VWAP ±1σ) and price crossing the most recent prior VWAP.

Styling: Bands and fills are minimal; HTF VWAP is a distinct line; value-area blocks are shaded with prior VWAP lines inside.

Configure via the grouped inputs: VWAP Settings, Additional Exchange Sources, Historical Value Areas, HTF Context, and Bands Settings.

Daily & Average Dollar VolumeCalculates the daily and average (20D) $ volume.

Fully customizable appearence and can be placed in any corner.

VWAP TrendSignalVWAP TrendSignal

VWAP (Volume-Weighted Average Price) is the market’s true fair value — the benchmark institutions use to see when price is balanced, extended, or trending with real intent.

Price often snaps back when it moves too far (mean reversion), and only shows genuine strength when it holds above or below VWAP.

VWAP TrendSignal makes this insight effortless by color-coding VWAP direction:

Yellow = VWAP rising → bullish pressure

Red = VWAP falling → bearish pressure

No bands. No noise. Just pure directional clarity.

Anchor VWAP to the Session, Week, Month, Quarter, or Year, and tailor the Slope Smoothing Filter to your timeframe:

1–2 smoothing → fast & reactive (1–5m scalping)

3–5 smoothing → clean & stable (5–15m intraday)

6–10 smoothing → slow flips (1H–4H swings)

10–15 smoothing → macro bias only (Daily/Weekly)

The line adapts to how you trade.

How to Use It

Mean Reversion

When price stretches far from VWAP, expect pullbacks or snapbacks.

Trend Direction

Yellow supports long bias, red supports short bias.

Simple, reliable, instantly visible.

Balance Zones

Price sitting near VWAP = compression, buildup, or chop.

A perfect signal to wait or prepare for a breakout.

Why It Works

VWAP TrendSignal distills institutional logic into a clean, single-line tool.

It shows fair value, trend slope, and balance all at once — making your chart clearer and your decisions faster.

Once you get used to reading it, trading without it feels blind.

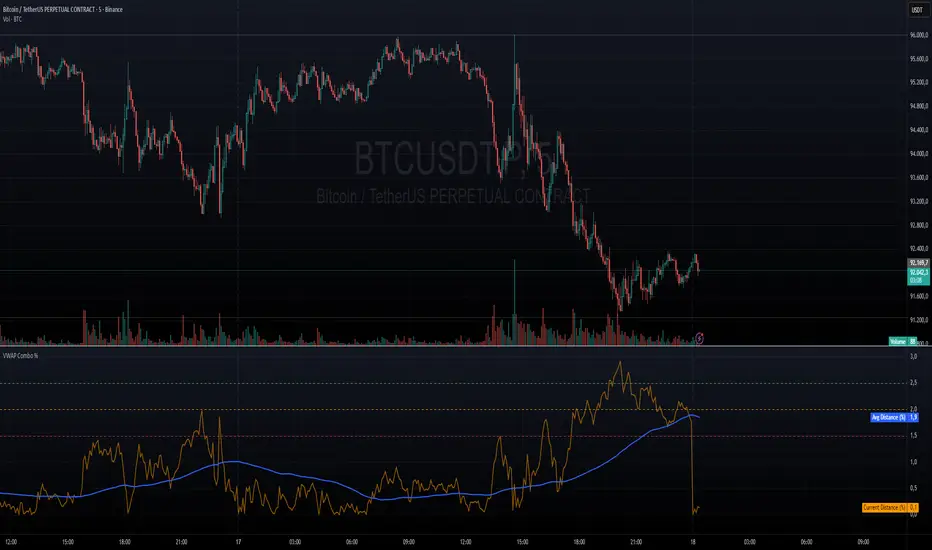

VWAP + VWAP Distance Avg + Alert Lines (%)VWAP Distance & Average Distance Indicator – Detailed Description

The VWAP + VWAP Distance Avg + Alert Lines (%) indicator is designed to measure the distance of the current price from the VWAP (Volume Weighted Average Price), as well as the average distance over a specified period. This tool is particularly useful for traders who use the VWAP as a magnet for price, helping to identify potential trend changes and areas where price may revert toward the VWAP.

Key Features

Current Distance (%)

Calculates the absolute percentage difference between the current price and the VWAP

This line shows how far the price has moved away from the VWAP at any given moment.

Average Distance (%)

Calculates a simple moving average (SMA) of the distance over a specified lookback period.

This provides a reference for typical price deviations from the VWAP, helping traders assess whether the current distance is unusually high or low.

Alert Lines (%)

Allows up to three customizable horizontal alert lines, which can be turned on or off individually.

Each line can be configured with:

Value in percent.

Color.

Line thickness.

These lines serve as visual thresholds, helping traders detect extreme deviations from the VWAP that may precede trend reversals.

Use Case – Detecting Potential Trend Changes

Traders often treat the VWAP as a price magnet, where price tends to revert after significant deviations.

When the current distance exceeds typical average levels or crosses an alert line, it can signal that the price may revert toward the VWAP, potentially indicating a shift in trend or a high-probability mean-reversion scenario.

Disclaimer

This indicator is provided for educational and analytical purposes only. It does not constitute financial advice, and trading decisions are always the sole responsibility of the individual trader. Users should carefully evaluate market conditions and their own risk tolerance before taking any trade.

Better used with VWAP on chart , and be careful around the end of session, for now this works just for session...

still improving on this....

Advanced Intraday Darvas BoxThis indicator applies a modern Darvas Box strategy for intraday traders, using non-repainting pivot detection combined with strong filters to reduce chart noise:

Confirmed swing highs and lows: Boxes only form when genuine swing pivots appear, ensuring fully non-repainting signals.

Minimum box height: Small, "noise" boxes are filtered out using ATR multiples for meaningful zones.

Trend filter: Choose EMA, SMA, or VWAP to lock boxes and breakouts to market direction.

Volume confirmation: Boxes are only confirmed when volume is above a user-defined threshold, highlighting high-participation moves.

Breakout filter: Signals trigger only if the breakout candle closes substantially beyond the box, reducing false breakouts.

Limited box display: Recent boxes only, keeping your chart clean and readable.

Features & Inputs

Pivot sensitivity: Set the number of bars for swing calculation.

Box filtering: Specify the minimum ATR multiple for box size.

Trend selection: EMA, SMA, VWAP, or None.

Volume filter & threshold: Activate for greater breakout confidence.

Breakout/Breakdown strength: Set how far price must close beyond the box to signal power.

Maximum boxes: Control the number of active boxes to keep the chart clear.

How to Add and Use

Add to Chart:

Click the “Add to Favorite Scripts” star to mark this indicator.

Open your desired intraday chart (1m–30m works best).

Click “Indicators,” search for “Advanced Intraday Darvas Box,” and add to your chart.

Customize Inputs:

Use the settings gear ⚙️ to adjust pivot sensitivity, trend logic, box filtering, and volume confirmation.

Lower minimum box height or pivot length for more frequent signals. Raise them for sparser, higher conviction setups.

Reading Darvas Boxes:

Box Edges: Horizontal lines mark resistance (top) and support (bottom) of detected zones.

Shaded regions: Highlight the most relevant trading zones and where price could coil before breakout.

Breakout labels (↑/↓): These appear only when price makes a powerful, confirmed move beyond the box edge—aligned with trend.

Alerts: Turn on chart alerts using the “Strong Bullish Breakout” or “Strong Bearish Breakdown” alert conditions for automated signal monitoring.

Best Practices:

Use Darvas boxes to complement price action analysis. Combine with candlestick patterns, volume spikes, and other price structure.

Only trade strong breakout signals confirmed by volume and market direction.

Avoid excessive boxes—adjust "Max Boxes" and filters for your instrument and timeframe.

Important

This indicator is non-repainting and built for display clarity and clean signals.

No brokerage automation, no external linking, and pure price/volume logic—fully compliant with TradingView House Rules.

Always test settings and confirmations before using for live decision-making.

Order-Flow Proxy (VWAP Deviation Zones)Order-Flow Proxy (VWAP Deviation Zones) helps traders visualize when market price moves unusually far away from its Volume-Weighted Average Price (VWAP) — a key fair-value level used by institutional participants.

When price stretches too far above or below VWAP, it often signals temporary imbalance between buying and selling pressure.

This tool highlights those moments using simple color zones and an optional statistical Z-Score filter for deeper precision.

In short: it’s a clean, minimal mean-reversion indicator showing when price is statistically “too far” from fair value.

Red zone → Price extended above VWAP → possible buyer exhaustion or short setup.

Green zone → Price extended below VWAP → possible seller exhaustion or long setup.

VWAP line → Acts as a dynamic fair-value anchor.

Concept:

VWAP combines both price and traded volume to define where most transactions occurred.

Deviations from it — measured either by a fixed distance (1%) or by Z-Score — can reveal overvaluation or undervaluation zones used by professional traders for contrarian setups.

How to use:

Apply the indicator to any intraday chart (1m–1h recommended).

Watch for background color shifts — red or green.

Optionally enable the Z-Score filter to focus only on statistically extreme deviations.

Combine with volume spikes, liquidity sweeps, or your own order-flow tools for confirmation.

Tip:

Best used as a visual overlay for detecting stretched markets and potential reversals.

Smart VWAP FVG SystemSmart VWAP FVG System - Professional Multi-Filter Trading Indicator

📊 OVERVIEW

The Smart VWAP FVG System is an advanced multi-layered trading indicator that combines institutional volume analysis, multi-timeframe VWAP trend confirmation, and Fair Value Gap detection to identify high-probability trade entries. This indicator uses a sophisticated filtering mechanism where signals appear only when multiple independent confirmation criteria align simultaneously.

Recommended Timeframe: 5-minute (M5) or higher. The indicator works best on M5, M15, and M30 charts for intraday trading.

🎯 ORIGINALITY & PURPOSE

This indicator is original because it combines three distinct analytical methods into a unified decision-making system:

Market Profile Volume Analysis - Identifies institutional accumulation/distribution zones

Dual VWAP Filtering - Confirms trend direction using two independent VWAP calculations

Fair Value Gap Detection - Validates institutional interest through price inefficiency zones

The key innovation is the directional filter system: the primary Market Profile generates BUY-ONLY or SELL-ONLY states based on higher timeframe value area reversals, which then controls which signals from the main system are displayed. This creates a multi-timeframe confluence that significantly reduces false signals.

Unlike simple indicator mashups, each component serves a specific purpose:

Market Profile → Direction bias (trend filter)

Primary VWAP (Session) → Short-term trend confirmation

Secondary VWAP (Week) → Medium-term trend confirmation

FVG Detection → Institutional activity validation

🔧 HOW IT WORKS

1. Primary Market Profile Filter (Higher Timeframe)

The indicator calculates Market Profile on a higher timeframe (default: 1 hour) to determine the overall market structure:

Value Area High (VAH): Top 70% of volume distribution

Value Area Low (VAL): Bottom 70% of volume distribution

Point of Control (POC): Price level with highest volume

When price reaches VAH and reverses down → SELL-ONLY mode activated

When price reaches VAL and reverses up → BUY-ONLY mode activated

This higher timeframe filter ensures you're trading in the direction of institutional flow.

2. Dual VWAP System

Two independent VWAP calculations provide multi-timeframe trend confirmation:

Primary VWAP (Session-based): Resets daily, tracks intraday momentum

Secondary VWAP (Week-based): Resets weekly, confirms longer-term trend

Filter Logic:

BUY signals require: Price > Primary VWAP AND Price > Secondary VWAP

SELL signals require: Price < Primary VWAP AND Price < Secondary VWAP

This dual confirmation prevents counter-trend trades during ranging conditions.

3. Fair Value Gap (FVG) Detection

FVG zones identify price inefficiencies where institutional orders were executed rapidly:

Bullish FVG: Gap between candle .high and candle .low (upward imbalance)

Bearish FVG: Gap between candle .high and candle .low (downward imbalance)

The indicator monitors recent FVG formation (lookback: 50 bars) and requires:

Bullish FVG present for BUY signals

Bearish FVG present for SELL signals

FVG zones are displayed as colored boxes and automatically marked as "mitigated" when price fills the gap.

4. Main Trading Signal Logic

The secondary Market Profile (default: 1 hour) generates the actual trading signals:

BUY Signal Conditions:

Price reaches Value Area Low

Reversal pattern confirmed (minimum 1 bar)

Price > Primary VWAP

Price > Secondary VWAP (if filter enabled)

Recent Bullish FVG detected (if filter enabled)

Primary MP Filter = BUY-ONLY or NEUTRAL

SELL Signal Conditions:

Price reaches Value Area High

Reversal pattern confirmed (minimum 1 bar)

Price < Primary VWAP

Price < Secondary VWAP (if filter enabled)

Recent Bearish FVG detected (if filter enabled)

Primary MP Filter = SELL-ONLY or NEUTRAL

All conditions must be TRUE simultaneously for a signal to appear.

📈 VISUAL ELEMENTS

On Chart:

🟢 Green Triangle (▲) = BUY Signal

🔴 Red Triangle (▼) = SELL Signal

🟦 Blue horizontal lines = Value Area zones

🟡 Yellow line = Point of Control (POC)

🟩 Green boxes = Bullish FVG zones

🟥 Red boxes = Bearish FVG zones

🔵 Blue line = Primary VWAP (Session)

⚪ White line = Secondary VWAP (Week)

Info Panel (Top Right):

Real-time status display showing:

Filter Direction (BUY ONLY / SELL ONLY / NEUTRAL)

Active timeframes for both MP filters

FVG filter status and count

VWAP positions (ABOVE/BELOW)

Signal enablement status

Alert status

⚙️ KEY SETTINGS

MP/TPO Filter Settings (Primary Indicator)

MP Filter Time Frame: 60 minutes (controls directional bias)

Filter Value Area %: 70% (standard Market Profile calculation)

Filter Alert Distance: 1 bar

Filter Min Bars for Reversal: 1 bar

Filter Alert Zone Margin: 0.01 (1%)

FVG Filter Settings

Use FVG Filter: Enabled (toggle on/off)

FVG Timeframe: 60 minutes (1 hour)

FVG Filter Mode: Both (require bullish FVG for BUY, bearish for SELL)

FVG Lookback Period: 50 bars (how far back to search)

Show FVG Formation Signals: Optional visual markers

Max FVG on Chart: 50 zones

Show Mitigated FVG: Display filled gaps

Market Profile Settings

Higher Time Frame: 60 minutes (for main signals)

Percent for Value Area: 70%

Show POC Line: Enabled

Keep Old MPs: Enabled (maintain historical profiles)

Primary VWAP Filter

Use Primary VWAP Filter: Enabled

Primary VWAP Anchor Period: Session (resets daily)

Primary VWAP Source: HLC3 (typical price)

Secondary VWAP Filter

Use Secondary VWAP Filter: Enabled

Secondary VWAP Anchor Period: Week (resets weekly)

Secondary VWAP Filter Mode: Both

Secondary VWAP Line Color: White

Trading Signals

Show Trading Signals on Chart: Enabled

Show SELL Signals: Enabled

Show BUY Signals: Enabled

Alert Distance: 1 bar

Min Bars for Reversal: 1 bar

Alert Zone Margin: 0.01 (1%)

Retest Search Period: 20 bars

Min Bars Between Retests: 5 bars

Show Only Retests: Disabled

Alert Settings

Enable Trading Notifications: Enabled

VAH Reversal Alert: Enabled (SELL signals)

VAL Reversal Alert: Enabled (BUY signals)

Time Filter Settings

Filter Alerts By Time: Optional (exclude specific hours)

⚠️ IMPORTANT WARNINGS & LIMITATIONS

1. Repainting Behavior

CRITICAL: This indicator uses lookahead=barmerge.lookahead_on to access higher timeframe data immediately for FVG detection. This is necessary to provide real-time FVG zone visualization but has the following implications:

FVG zones may shift slightly until the higher timeframe candle closes

FVG detection signals are preliminary until HTF bar confirmation

The main trading signals (triangles) appear on confirmed bars and do not repaint

Best Practice: Always wait for the current timeframe bar to close before acting on signals. The filter status and FVG zones are informational but may adjust as new data arrives.

2. Minimum Timeframe

Do NOT use on timeframes below 5 minutes (M5)

Recommended: M5, M15, M30 for intraday trading

Higher timeframes (H1, H4) can also be used but will generate fewer signals

3. Multiple Filters Can Block Signals

By design, this indicator is conservative. When all filters are enabled:

Signals appear ONLY when all conditions align

You may see extended periods with no signals

This is intentional to reduce false positives

If you see no signals:

Check the Info Panel to see which filters are failing

Consider adjusting FVG lookback period

Temporarily disable FVG filter to test

Verify VWAP filters match current market trend

4. Market Profile Limitations

Market Profile requires sufficient volume data

Low-volume instruments may produce unreliable profiles

Value Areas update only on higher timeframe bar close

Works best on liquid markets (major forex pairs, indices, crypto)

📖 HOW TO USE

Step 1: Add to Chart

Apply indicator to M5 or higher timeframe chart

Ensure chart shows volume data

Use standard candles (NOT Heikin Ashi, Renko, etc.)

Step 2: Configure Settings

Primary MP Filter TF: Set to 60 (1 hour) minimum, or 240 (4 hour) for swing trading

Main MP TF: Set to 60 (1 hour) for intraday signals

FVG Timeframe: Match or exceed main MP timeframe

Leave other settings at default initially

Step 3: Understand the Info Panel

Monitor the top-right panel:

FILTER STATUS: Shows current directional bias

NEUTRAL = Both signals allowed

BUY ONLY = Only green triangles will appear

SELL ONLY = Only red triangles will appear

FVG Filter: Shows if bullish/bearish gaps detected recently

VWAP positions: Confirms trend alignment

Step 4: Take Signals

For BUY Signal (Green Triangle ▲):

Wait for green triangle to appear

Check Info Panel shows ✓ for BUY signals

Confirm current bar has closed

Enter long position

Stop loss: Below recent VAL or swing low

Target: Previous Value Area High or 1.5-2× risk

For SELL Signal (Red Triangle ▼):

Wait for red triangle to appear

Check Info Panel shows ✓ for SELL signals

Confirm current bar has closed

Enter short position

Stop loss: Above recent VAH or swing high

Target: Previous Value Area Low or 1.5-2× risk

Step 5: Risk Management

Risk per trade: Maximum 1-2% of account equity

Position sizing: Adjust based on stop loss distance

Avoid trading: During major news events or time filter periods

Multiple confirmations: Look for confluence with price action (support/resistance, trendlines)

🎓 UNDERLYING CONCEPTS

Market Profile Theory

Developed by J. Peter Steidlmayer in the 1980s, Market Profile organizes price and volume data to identify:

Value Areas: Where 70% of trading activity occurred

POC: Price level with highest acceptance (most volume)

Imbalances: When price moves away from value quickly

This indicator uses TPO (Time Price Opportunity) calculation method to build the volume profile distribution.

VWAP (Volume Weighted Average Price)

VWAP represents the average price weighted by volume, showing where institutional traders are positioned:

Price above VWAP = Bullish (institutions accumulated lower)

Price below VWAP = Bearish (institutions distributed higher)

Using dual VWAP (Session + Week) creates multi-timeframe trend alignment.

Fair Value Gaps (FVG)

Also known as "imbalance" or "inefficiency," FVG occurs when:

Price moves so rapidly that a gap forms in the candlestick structure

Indicates institutional order flow (large market orders)

Price often returns to "fill" these gaps (rebalance)

The 3-candle FVG pattern (gap between candle and candle ) is widely used in ICT (Inner Circle Trader) methodology and Smart Money Concepts.

🔍 CREDITS & CODE ATTRIBUTION

This indicator builds upon established technical analysis concepts and combines multiple methodologies:

1. Market Profile / TPO Calculation

Concept Origin: J. Peter Steidlmayer (Chicago Board of Trade, 1980s)

Code Inspiration: TradingView's public domain Market Profile examples

Modifications: Custom filtering logic for directional bias, dual timeframe implementation

2. VWAP Calculation

Concept Origin: Standard financial instrument (widely used since 1980s)

Code Base: TradingView built-in ta.vwap() function (public domain)

Modifications: Dual VWAP system with independent anchor periods, custom filtering modes

3. Fair Value Gap Detection

Concept Origin: Inner Circle Trader (ICT) / Smart Money Concepts methodology

Code Implementation: Original implementation based on 3-candle gap pattern

Features: Multi-timeframe detection, automatic mitigation tracking, visual zone display

4. Pine Script Framework

Language: Pine Script v6 (TradingView)

Built-in Functions Used:

ta.vwap() - Volume weighted average price

request.security() - Higher timeframe data access

ta.change() - Period detection

ta.cum() - Cumulative volume

time() - Timestamp functions

Note: All code is original implementation. While concepts are based on established trading methodologies, the combination, filtering logic, and execution are unique to this indicator.

📊 RECOMMENDED INSTRUMENTS

Best Performance:

Major Forex Pairs (EURUSD, GBPUSD, USDJPY)

Stock Indices (ES, NQ, SPX, DAX)

Major Cryptocurrencies (BTCUSD, ETHUSD)

Liquid Stocks (high daily volume)

Avoid:

Low-volume altcoins

Illiquid stocks

Exotic forex pairs with wide spreads

⚡ PERFORMANCE TIPS

Start Conservative: Enable all filters initially

Reduce Filters Gradually: If too few signals, disable Secondary VWAP filter first

Match Timeframes: Keep MP Filter TF and FVG TF at same value

Backtest First: Review historical performance on your preferred instrument/timeframe

Combine with Price Action: Look for support/resistance confluence

Use Time Filter: Avoid low-liquidity hours (optional setting)

🚫 WHAT THIS INDICATOR DOES NOT DO

Does not guarantee profits - No trading system is 100% accurate

Does not predict the future - Based on historical patterns

Does not replace risk management - Always use stop losses

Does not work on all instruments - Requires volume data and liquidity

Does not provide exact entry/exit prices - Signals are zones, not precise levels

Does not account for fundamentals - Purely technical analysis

📜 DISCLAIMER

This indicator is provided for educational and informational purposes only. It is not financial advice, and past performance does not guarantee future results.

Trading Risk Warning:

All trading involves risk of loss

You can lose more than your initial investment (leverage products)

Only trade with capital you can afford to lose

Always use appropriate position sizing and risk management

Consider seeking advice from a licensed financial advisor

Technical Limitations:

Indicator may repaint FVG zones until HTF bar closes

Signals are based on historical patterns that may not repeat

Market conditions change and no system works in all environments

Volume data quality varies by exchange/broker

By using this indicator, you acknowledge these risks and agree that the author bears no responsibility for trading losses.

📞 SUPPORT & UPDATES

Questions? Comment on this publication

Issues? Describe the problem with chart screenshot

Feature Requests? Suggest improvements in comments

Updates: Will be published as new versions using TradingView's update feature

📝 VERSION HISTORY

Version 1.0 (Current)

Initial public release

Multi-filter system: MP + Dual VWAP + FVG

Directional bias filter

Real-time info panel

Comprehensive alert system

Time-based filtering

Thank you for using Smart VWAP FVG System!

Happy Trading! 📈

VWAP (SIYL) Stdev Bands v2v2 indicator to allow for reversion-to-mean trading via the Stay In Your Lane approach.

Trading Blueprint v7 Pro — VWAP-CVD, cPOC Trend MomentumTBv7 Pro is the advanced release of the Trading Blueprint framework — engineered for institutional-style intraday analysis that fuses VWAP location, CVD orderflow, composite profile bias, and momentum curvature into one cohesive system.

Core Framework

VWAP Structure → Adaptive mean anchored to session VWAP with ±1σ / ±2σ deviation envelopes for dynamic equilibrium detection.

vPOC per bar by ruckard ()

Anchored Volume Profile by DGT ()

CVD Orderflow Divergence → Smoothed delta histogram with fractal pivots identifying hidden absorption and exhaustion (patterns (Bull / Bear Div). Cumulative Volume Delta by AustrianTradingMachine )

cPOC Integration (2-Day Composite) by poopsnag (me :)→ Confirms true acceptance or rejection zones across sessions for precision bias alignment.

TMI (Trend Momentum Indicator by TradingRiot()) → Quantifies slope + mean crossover strength, providing actionable momentum confirmation (bullish / bearish support / divergence).

Bias Dashboard → Displays VWAP bias, numerical score, and dynamic color feedback for at-a-glance trade orientation.

Usage Context

Designed for professionals trading 15 m execution inside 1 h / 4 h context. Ideal for VWAP-cPOC location setups, reversion / continuation scalps, and orderflow confirmation using cumulative delta behavior.

🔧 Modules such as RSI / AO are pre-wired and easily activated for full Trading Blueprint confluence mapping.

VWAP Reversion (Sequential Stats + Profit/Loss Points)First time posting. This is my attempt to evaluate the effectiveness of VWAP reversion. I decided to make this an indicator with its own integrated stats.

If you set the session length to lets say 100, but choose a 1 minute timeframe, it will only load as many sessions as the chart will allow for that timeframe. increasing the timeframe will allow you to go back further with more sessions.

I plan to implement more and more as I refine it. I just wanted to get my working copy out into the universe. I'd like to add some method of "scaling in". Perhaps if the price goes further and further away from the original entry, say for each additional std. deviation band further, it could add another entry signal.

My trading journey is just beginning, I've never coded before, and this was made entirely through the fusion of my attempt to communicate the ideas in my head for ChatGPT to turn into code!