Multi-Metric Valuation IndicatorMulti-Metric Valuation Indicator - Accumulation/Distribution Signal

This indicator combines six proven technical metrics into a single composite valuation score to help identify optimal accumulation and distribution zones for any asset. Built with the Mayer Multiple as its foundation, it provides a comprehensive view of whether an asset is overvalued or undervalued.

Core Components:

Mayer Multiple - Compares current price to 200-day moving average (traditional Bitcoin valuation metric)

RSI (Relative Strength Index) - Identifies overbought/oversold momentum conditions

Bollinger Band Position - Measures price location within volatility bands

50-Day MA Deviation - Tracks short-term trend strength

Rate of Change (ROC) - Captures momentum shifts

Volume Analysis - Confirms price moves with relative volume strength

How It Works:

Each metric is scored from -1 (extremely undervalued) to +1 (extremely overvalued) using granular thresholds. These scores are averaged into a composite valuation score that oscillates around zero:

< -0.4: Strong Accumulation Zone (dark green background)

-0.4 to -0.2: Accumulation Zone (light green background)

-0.2 to +0.2: Neutral Zone (gray background)

+0.2 to +0.4: Distribution Zone (light red background)

> +0.4: Strong Distribution Zone (dark red background)

Key Features:

Real-time scoring table displays all component values and their individual scores

Color-coded composite line (green = undervalued, red = overvalued)

Background shading for instant visual signal recognition

Built-in alerts for strong accumulation/distribution crossovers

Fully customizable inputs for all parameters

Clean, efficient code using ternary operators and one-line declarations

Best Use Cases:

Long-term position accumulation strategies

Identifying macro market tops and bottoms

Dollar-cost averaging entry/exit planning

Multi-timeframe confirmation (works on daily, weekly, monthly charts)

Risk management and position sizing decisions

Interpretation:

When the composite score drops below -0.4, multiple metrics simultaneously indicate undervaluation - a historically favorable accumulation opportunity. Conversely, scores above +0.4 suggest distribution may be prudent as multiple indicators flash overbought signals.

The indicator is most powerful when combined with fundamental analysis and proper risk management. It's designed to keep emotions in check during extreme market conditions.

Cycleanalysis

BTC/M2 Fire Sniffer (Liquidity Range Z-Score)Howdy Fella. Great to see you here, exploring the true data in CRYPTOCAP:BTC analysis.

To ensure a perfect view on the markets, here are a few tips on how to fine tune the Fire Sniffer:

- Z-Score Lookback: 40

- Liquidity Ratio SuperSmoother Length: 8

- Z-score SuperSmoother Length: 132

Set the ranges as following:

Mean: -0.53

Liquidity Cycle Top: 0.8

Liquidity Cycle Bottom: -0.65

With that, you are set to go. Enjoy and make sure to let me know your thoughts on the script. You can contact me on X: @thebitcoinfrontier

Moon Declination & More [BlueprintResearch]🌒 MOON DECLINATION & MORE

A comprehensive lunar declination visualization showing Moon, Sun, and node declinations, with phase coloring, zodiac sign tracking, and future projections.

Part of the Blueprint Research open-source ephemeris project.

█ WHAT'S INCLUDED

• Moon Declination — The Moon's angular distance from the celestial equator, oscillating rapidly (~27 days)

• Sun Declination — Optional overlay showing the Sun's seasonal declination (±23.4°)

• Node Declinations — North (☊) and South (☋) node lines forming the Moon's orbital envelope

• Future Projections — Project all lines up to 500 bars into the future

• Zodiac Crossing Markers — Indicates when the North Node reaches a particular zodiac degree. Keep in mind, nodes move through the zodiac in reverse.

█ CONCEPTS

Declination measures how far north or south a celestial body appears from the celestial equator. The Moon's declination oscillates rapidly, while its maximum range shifts slowly over the 18.6-year nodal cycle.

Node Declination Envelope:

The North (☊) and South (☋) node lines mark the envelope of the Moon's orbit—the theoretical maximum northern and southern declinations the Moon can reach.

Lunar Standstills:

The 18.6-year nodal cycle determines when the Moon reaches its most extreme declinations. During a major standstill, the Moon can exceed ±28° declination. During a minor standstill, the Moon's range is limited to approximately ±18°.

Out-of-Bounds (OOB):

When the Moon moves beyond ±23.44° declination, it exceeds the Sun's maximum reach and is considered "Out of Bounds."

█ COLORING OPTIONS

Phase Coloring (Moon)

Color the Moon's declination line by lunar phase:

• New Moon (0-90°): Slate silver

• First Quarter (90-180°): Mint

• Full Moon (180-270°): Bright gold

• Last Quarter (270-360°): Soft violet

Zodiac Sign Coloring (Nodes)

Color the node lines by their zodiac sign. When enabled, a color legend appears at the top, showing all 12 signs for reference.

█ ZODIAC FEATURES

Zodiac Sign Coloring

Color the North and South Node lines according to their zodiac sign positions.

Zodiac Crossing

Marks when the North Node crosses a specific zodiac degree. Select any sign and degree (0-29) to track. The North Node moves retrograde through the zodiac over an 18.6-year cycle.

█ RESEARCH FEATURES

Standstill Thresholds

Horizontal reference lines at key declination levels:

• ±28.6° Major Standstill (peak of the 18.6-year cycle)

• ±18.3° Minor Standstill (trough of the cycle)

• ±23.4° Out-of-Bounds threshold

OOB Highlighting

Optional background shading when the Moon exceeds the OOB threshold.

Node Equatorial Crossings

Crosshair markers indicate when the node's declination crosses 0° (equatorial passage).

Reference Line Labels

Labels at projection endpoints with an adjustable offset for readability.

█ FEATURES

• Moon declination with optional lunar phase coloring

• Sun declination overlay

• North and South node declinations (☊ and ☋)

• Future projections up to 500 bars

• Zodiac sign coloring with a color legend

• Zodiac degree-crossing markers

• Node equatorial-crossing markers

• Out-of-Bounds background highlighting

• Reference line labels with offset control

• Customizable line widths and colors

• Informative tooltips for all settings

• Works on all timeframes

█ HOW TO USE

1 — Add the indicator to your chart

2 — Configure which elements to display (Moon, Sun, Nodes)

3 — Enable future projections to view upcoming declination values

4 — Enable Zodiac coloring to track node sign positions

5 — Set a Zodiac Crossing degree to mark when the North Node crosses that point

6 — Enable Standstill Thresholds to show reference lines

7 — Toggle phase coloring to visualize the lunar cycle

█ THEORY

Lunar Theory: ELP2000-82 by Chapront-Touzé & Chapront

Solar Theory: VSOP87 for Sun position and phase calculation

Reference: Meeus, "Astronomical Algorithms" (2nd Ed., 1998)

█ LIMITATIONS

• Truncated ELP2000-82 theory (~10 arcseconds precision)

• Future projections assume consistent bar timing

• Phase coloring uses 4 phases (not the 8 traditional phases)

• Mean nodes only (no perturbation corrections)

█ OPEN SOURCE

Blueprint Research Ephemeris Libraries:

• lib_elp2000_moon — Lunar position and mean node calculations

• lib_vsop_core — Solar position and coordinate utilities

• lib_ephemeris — Unified planetary API

Third-Party Libraries:

• hsvColor by @kaigouthro — HSV color utilities (MPL 2.0)

© 2025-2026 BlueprintResearch (Javonnii) • CC BY-NC-SA 4.0

Yearly Projection ExplorerThis indicator helps you understand how the current market period has behaved historically by overlaying the same date window from previous years and projecting it forward from today’s price.

The script works the following way:

Aligns past years to today’s calendar date

Normalizes all paths to the last close at the start

Projects historical performance X bars forward

Displays each year as a separate performance path

Calculates and plots the mean (average) projection for quick reference

🔧 How It Works

Number of Years: choose how many past years to include (e.g. last 10, 20, or 25 years)

Projection Length: choose how many bars (days) ahead to project

Each line shows how the market moved during the same period in a specific year

Labels show the year and total return at the projection end

The mean line highlights the average historical outcome

🧠 Why This Is Useful

Identify seasonal tendencies

Compare current price action to historical analogs

Visualize best / worst historical outcomes

Set realistic expectations for short-term moves

Add context to discretionary or systematic decisions

This tool does not predict the future, but it provides a powerful historical framework to assess what has been typical, rare, or extreme for the current market window.

⚠️ Notes

Script works on timenow variable for now, and you might see unexpected periods if today is a day off.

Results depend on the selected timeframe and instrument

Past performance is not a guarantee of future results

Designed for analysis and context, not standalone signals

5-Period Average of Returns (Close)This indicator calculates the 5-period average of returns of the closing price, providing a detrended, zero-centered oscillator ideal for cycle analysis and timing.

Key Features:

Detrended: Centers around zero to clearly reveal cyclical patterns.

Cycle-friendly: Highlights peaks and troughs for measuring dominant cycles.

Flexible: Can be applied to multiple timeframes (daily, weekly, intraday).

Zero Line Reference: Quickly identify directional shifts in average returns.

Foundation for Advanced Analysis: Can be combined with RSI, statistical bands, or multi-timeframe studies.

Use this indicator to:

Identify dominant cycles and their phase

Measure cycle length and rhythm

Assist in entry and exit timing based on average-return oscillations

Detrend price data for more precise technical and cyclical analysis

Elliott Wave Full Fractal System v2.0Elliott Wave Full Fractal System v2.0 – Q.C. FINAL (Guaranteed R/R)

Elliott Wave Full Fractal System is a multi-timeframe wave engine that automatically labels Elliott impulses and ABC corrections, then builds a rule-based, ATR-driven risk/reward framework around the “W3–W4–W5” leg.

“Guaranteed R/R” here means every order is placed with a predefined stop-loss and take-profit that respect a minimum Reward:Risk ratio – it does not mean guaranteed profits.

Core Idea

This strategy turns a full fractal Elliott Wave labelling engine into a systematic trading model.

It scans fractal pivots on three wave degrees (Primary, Intermediate, Minor) to detect 5-wave impulses and ABC corrections.

A separate “Trading Degree” pivot stream, filtered by a 200-EMA trend filter and ATR-based dynamic pivots, is then used to find W4 pullback entries with a minimum, user-defined Reward:Risk ratio.

Default Properties & Risk Assumptions

The backtest uses realistic but conservative defaults:

// Default properties used for backtesting

strategy(

"Elliott Wave Full Fractal System - Q.C. FINAL (Guaranteed R/R)",

overlay = true,

initial_capital = 10000, // realistic account size

default_qty_type = strategy.percent_of_equity,

default_qty_value = 1, // 1% risk per trade

commission_type = strategy.commission.cash_per_contract,

commission_value = 0.005, // example stock commission

slippage = 0 // see notes below

)

Account size: 10,000 (can be changed to match your own account).

Position sizing: 1% of equity per trade to keep risk per idea sustainable and aligned with TradingView’s recommendations.

Commission: 0.005 cash per contract/share as a realistic example for stock trading.

Slippage: set to 0 in code for clarity of “pure logic” backtesting. Real-life trading will experience slippage, so users should adjust this according to their market and broker.

Always re-run the backtest after changing any of these values, and avoid using high risk fractions (5–10%+) as that is rarely sustainable.

1. Full Fractal Wave Engine

The script builds and maintains four pivot streams using ATR-adaptive fractals:

Primary Degree (Macro Trend):

Captures the large swings that define the major trend. Labels ①–⑤ and ⒶⒷⒸ using blue “Circle” labels and thicker lines.

Intermediate Degree (Trading Degree):

Captures the medium swings (swing-trading horizon). Uses teal labels ( (1)…(5), (A)(B)(C) ).

Minor Degree (Micro Structure):

Tracks short-term swings inside the larger waves. Uses red roman numerals (i…v, a b c).

ABC Corrections (Optional):

When enabled, the engine tries to detect standard A–B–C corrective structures that follow a completed 5-wave impulse and plots them with dashed lines.

Each degree uses a dynamic pivot lookback that expands when ATR is above its EMA, so the system naturally requires “stronger” pivots in volatile environments and reacts faster in quiet conditions.

2. Theory Rules & Strict Mode

Normal Mode: More permissive detection. Designed to show more wave structures for educational / exploratory use.

Strict Mode: Enforces key Elliott constraints:

Wave 3 not shorter than waves 1 and 5.

No invalid W4 overlap with W1 (for standard impulses).

ABC Logic: After a confirmed bullish impulse, the script expects a down-up-down corrective pattern (A,B,C). After a bearish impulse, it looks for up-down-up.

3. Trend Filter & Pivots

EMA Trend Filter: A configurable EMA (default 200) is used as a non-wave trend filter.

Price above EMA → Only long setups are considered.

Price below EMA → Only short setups are considered.

ATR-Adaptive Pivots: The pivot engine scales its left/right bars based on current ATR vs ATR EMA, making waves and trading pivots more robust in volatile regimes.

4. Dynamic Risk Management (Guaranteed R/R Engine)

The trading engine is designed around risk, not just pattern recognition:

ATR-Based Stop:

Stop-loss is placed at:

Entry ± ATR × Multiplier (user-configurable, default 2.0).

This anchors risk to current volatility.

Minimum Reward:Risk Ratio:

For each setup, the script:

Computes the distance from entry to stop (risk).

Projects a take-profit target at risk × min_rr_ratio away from entry.

Only accepts the setup if risk is positive and the required R:R ratio is achievable.

Result: Every order is created with both TP and SL at a predefined distance, so each trade starts with a known, minimum Reward:Risk profile by design.

“Guaranteed R/R” refers exclusively to this order placement logic (TP/SL geometry), not to win-rate or profitability.

5. Trading Logic – W3–W4–W5 Pattern

The Trading pivot stream (separate from visual wave degrees) looks for a simple but powerful pattern:

Bullish structure:

Sequence of pivots forms a higher-high / higher-low pattern.

Price is above the EMA trend filter.

A strong “W3” leg is confirmed with structure rules (optionally stricter in Strict mode).

Entry (Long – W4 Pullback):

The “height” of W3 is measured.

Entry is placed at a configurable Fibonacci pullback (default 50%) inside that leg.

ATR-based stop is placed below entry.

Take-profit is projected to satisfy min Reward:Risk.

Bearish structure:

Mirrored logic (lower highs/lows, price below EMA, W3 down, W4 retrace up, W5 continuation down).

Once a valid setup is found, the script draws a colored box around the entry zone and a label describing the type of signal (“LONG SETUP” or “SHORT SETUP”) with the suggested limit price.

6. Orders & Execution

Entry Orders: The strategy uses limit orders at the computed W4 level (“Sniper Long” or “Sniper Short”).

Exits: A single strategy.exit() is attached to each entry with:

Take-profit at the projected minimum R:R target.

Stop-loss at ATR-based level.

One Trade at a Time: New setups are only used when there is no open position (strategy.opentrades == 0) to keep the logic clear and risk contained.

7. Visual Guide on the Chart

Wave Labels:

Primary: ①,②,③,④,⑤, ⒶⒷⒸ

Intermediate: (1)…(5), (A)(B)(C)

Minor: i…v, a b c

Trend EMA: Single blue EMA showing the dominant trend.

Setup Boxes:

Green transparent box → long entry zone.

Red transparent box → short entry zone.

Labels: “LONG SETUP / SHORT SETUP” labels mark the proposed limit entry with price.

8. How to Use This Strategy

Attach the strategy to your chart

Choose your market (stocks, indices, FX, crypto, futures, etc.) and timeframe (for example 1h, 4h, or Daily). Then add the strategy to the chart from your Scripts list.

Start with the default settings

Leave all inputs on their defaults first. This lets you see the “intended” behaviour and the exact properties used for the published backtest (account size, 1% risk, commission, etc.).

Study the wave map

Zoom in and out and look at the three wave degrees:

Blue circles → Primary degree (big picture trend).

Teal (1)…(5) → Intermediate degree (swing structure).

Red i…v → Minor degree (micro waves).

Use this to understand how the engine is interpreting the Elliott structure on your symbol.

Watch for valid setups

Look for the coloured boxes and labels:

Green box + “LONG SETUP” label → potential W4 pullback long in an uptrend.

Red box + “SHORT SETUP” label → potential W4 pullback short in a downtrend.

Only trades in the direction of the EMA trend filter are allowed by the strategy.

Check the Reward:Risk of each idea

For each setup, inspect:

Limit entry price.

ATR-based stop level.

Projected take-profit level.

Make sure the minimum Reward:Risk ratio matches your own rules before you consider trading it.

Backtest and evaluate

Open the Strategy Tester:

Verify you have a decent sample size (ideally 100+ trades).

Check drawdowns, average trade, win-rate and R:R distribution.

Change markets and timeframes to see where the logic behaves best.

Adapt to your own risk profile

If you plan to use it live:

Set Initial Capital to your real account size.

Adjust default_qty_value to a risk level you are comfortable with (often 0.5–2% per trade).

Set commission and slippage to realistic broker values.

Re-run the backtest after every major change.

Use as a framework, not a signal machine

Treat this as a structured Elliott/R:R framework:

Filter signals by higher-timeframe trend, major S/R, volume, or fundamentals.

Optionally hide some wave degrees or ABC labels if you want a cleaner chart.

Combine the system’s structure with your own trade management and discretion.

Best Practices & Limitations

This is an approximate Elliott Wave engine based on fractal pivots. It does not replace a full discretionary Elliott analysis.

All wave counts are algorithmic and can differ from a manual analyst’s interpretation.

Like any backtest, results depend heavily on:

Symbol and timeframe.

Sample size (more trades are better).

Realistic commission/slippage settings.

The 0-slippage default is chosen only to show the “raw logic”. In real markets, slippage can significantly impact performance.

No strategy wins all the time. Losing streaks and drawdowns will still occur even with a strict R:R framework.

Disclaimer

This script is for educational and research purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance, whether real or simulated, is not indicative of future results. Always test on multiple symbols/timeframes, use conservative risk, and consult your financial advisor before trading live capital.

Pi Cycle BTC Top + Pre-Alert BandsPi Cycle BTC Top + Pre-Alert Bands is an advanced implementation of the classic Pi Cycle Top model, designed for Bitcoin cycle analysis on higher timeframes (especially 1D BTCUSD/BTCUSD·INDEX).

The original Pi Cycle Top uses two moving averages:

• 111-day SMA (short MA)

• 350-day SMA ×2 (long MA)

A Pi Top is signaled when the 111 SMA crosses above the 350×2 SMA. Historically, this has occurred near major BTC cycle highs.

This script extends that idea with a 3-step early-warning sequence:

• Pi Green – early compression: short/long MA ratio crosses upward into the green band (convergence from below is required).

• Pi Yellow – mid-cycle warning: only fires if a valid Green has already occurred in the same cycle.

• Pi Cycle Top – final top: the classic Pi Cycle cross, limited to one top signal per cycle. After a top, no new Yellow or Top signals can appear until a new Green event starts the next cycle.

Background shading shows the active phase (Green / Yellow / late-cycle zone), so you can see at a glance where BTC is within its Pi-based macro structure.

All logic is non-repainting: request.security() uses lookahead_off and no future data is accessed.

Typical use

This indicator is intended as a macro-cycle timing and risk-awareness tool, not a stand-alone entry system. Many traders use it to:

• Watch for Pi Green as the start of a potential late-cycle advance.

• Treat Pi Yellow as a rising-risk environment and tighten risk management.

• Use the Pi Cycle Top as a historical high-risk zone where large profit-taking or hedging may be considered.

Always combine this with your own analysis (trend, volume, on-chain, macro) before making decisions.

How to set alerts

Add the indicator to your chart (1D BTCUSD or BTCUSD·INDEX recommended).

Click Alerts → Condition → Pi Cycle BTC Top + Pre-Alert Bands.

Choose one of:

• Pi Cycle – Green Pre-Alert (early convergence)

• Pi Cycle – Yellow Pre-Alert (after Green only)

• Pi Cycle – TOP (Single per Cycle, after Green)

Use “Once per bar close” for higher-timeframe reliability.

Disclaimer

This tool is for educational and analytical purposes only. The Pi Cycle concept is based on historical behavior and does not guarantee future results. This is not financial advice; always do your own research and manage risk appropriately.

Gann Square of 144 (Master Price & Time)🔹 What this tool does

Draws a 144-unit square in price & time (0 → 144)

Plots all key horizontal & vertical levels:

0, 18, 36, 48, 54, 72, 90, 96, 108, 126, 144

Highlights the main 1/2 level (72) as thick midline

Marks 1/3 and 2/3 (48 & 96) as special harmonic levels

Draws internal diagonals (0–144, 144–0 and sub-squares)

Plots an 8-ray Gann fan from the 0-point (0 → 36 / 72 / 108 / 144 etc.)

Keeps price–time ratio consistent inside the box:

the 1×1 angle has a fixed slope = price_per_bar

The idea: once the square is calibrated to a major swing, you can study how price respects these angles and harmonic zones over time.

🔧 Inputs & how to set it up correctly

Choose your timeframe

Works best on Daily and Weekly charts.

Use one timeframe consistently when calibrating the square.

Start offset (bars back)

Start offset (bars back) shifts the whole square left/right.

Increase the value to move the square further into the past, decrease it to move it closer to the current bars.

Box width (bars)

Box width (bars) = how many bars the square spans horizontally.

Bigger value = projects the structure further into the future.

Example: 288 bars ≈ 2×144 units in time, 720 bars for longer-term projection, etc.

Bottom price

Bottom price is your 0-level in price.

Usually set this to a major swing low (cycle low, bear market low, important pivot).

The bottom-left corner of the square conceptually sits at:

(start_offset_bar, bottom_price)

Price per bar (slope 1×1) (if your version has this input)

This defines the slope of the 1×1 angle (main Gann angle).

Recommended way to set it:

Pick a major impulsive move from Swing Low → Swing High.

Measure:

Price range = High − Low

Number of bars between them.

Compute:

price_per_bar = price_range / number_of_bars

Use that as your 1×1 value in the input.

Now the main diagonal from 0 to 144 represents the true Gann 1×1 for that swing.

Important: The 1×1 angle is mathematically correct (price-per-bar), even if it does not always look like a perfect 45° line visually in TradingView due to chart scaling.

📖 How to read the Square of 144

Horizontal levels

0 = anchor price (bottom)

18, 36, 48, 54, 72, 90, 96, 108, 126, 144 = key price harmonics

72 (1/2) often acts as major support/resistance

48 & 96 (1/3 and 2/3) are strong “vibration” levels

Vertical levels

Same units but in time (bars).

When important pivots in price occur near these verticals, you get time–price confluence.

Midlines (1/2)

The thick horizontal and vertical lines at 72 mark the center of the square.

Crossings around these often signal important cycle turns.

1/3 & 2/3 zones (48–54 and 90–96)

These narrow bands are powerful reversal / decision zones.

Price often reacts strongly there or accelerates if they break.

Gann fan from 0-point

These rays represent major trends:

1×1 equivalent (main diagonal)

Faster & slower angles (e.g. 2×1, 1×2, etc depending on configuration)

If price breaks one fan angle cleanly, it often “falls” or “climbs” toward the next one.

🎯 Practical use cases

Project future support/resistance zones based on a major low.

See where price is in the square: early in the cycle (0–36), mid (around 72), or late (108–144).

Watch how price respects:

midlines (72),

1/3 and 2/3 bands (48–54, 90–96),

and the fan angles from 0.

Combine with your own price action / Fibonacci / trend tools – this is not a signal generator, but a time–price map.

⚠️ Notes & limitations

This tool is for educational & analytical purposes only.

It does not generate buy/sell signals.

Visual 45° angles in TradingView can change when you zoom or rescale the chart.

→ The script keeps the internal price-per-bar logic stable, even if the drawing looks steeper/flatter when zooming.

Always confirm zones with price action, volume, and higher timeframe context.

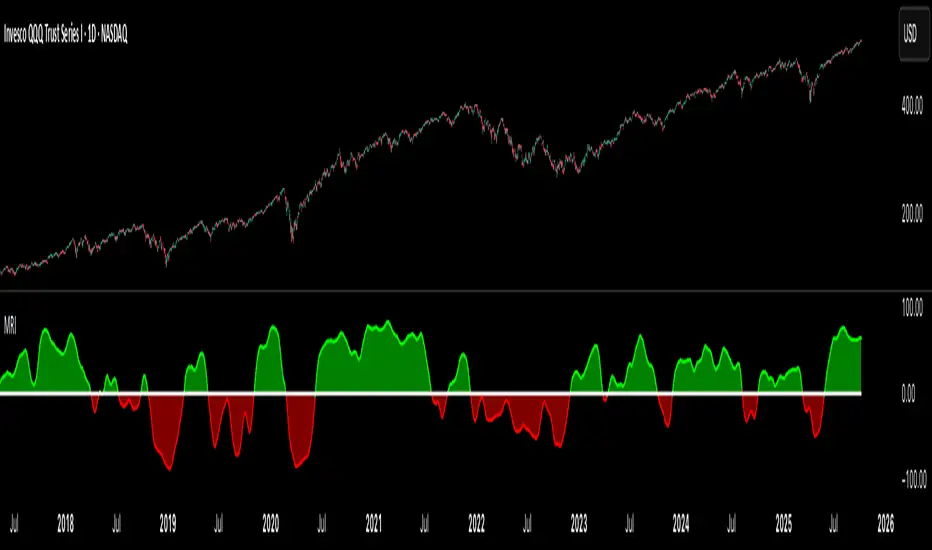

Market Regime IndexThe Market Regime Index is a top-down macro regime nowcasting tool that offers a consolidated view of the market’s risk appetite. It tracks 32 of the world’s most influential markets across asset classes to determine investor sentiment by applying trend-following signals to each independent asset. It features adjustable parameters and a built-in alert system that notifies investors when conditions transition between Risk-On and Risk-Off regimes. The selected markets are grouped into equities (7), fixed income (9), currencies (7), commodities (5), and derivatives (4):

Equities = S&P 500 E-mini Index Futures, Nasdaq-100 E-mini Index Futures, Russell 2000 E-mini Index Futures, STOXX Europe 600 Index Futures, Nikkei 225 Index Futures, MSCI Emerging Markets Index Futures, and S&P 500 High Beta (SPHB)/Low Beta (SPLV) Ratio.

Fixed Income = US 10Y Treasury Yield, US 2Y Treasury Yield, US 10Y-02Y Yield Spread, German 10Y Bund Yield, UK 10Y Gilt Yield, US 10Y Breakeven Inflation Rate, US 10Y TIPS Yield, US High Yield Option-Adjusted Spread, and US Corporate Option-Adjusted Spread.

Currencies = US Dollar Index (DXY), Australian Dollar/US Dollar, Euro/US Dollar, Chinese Yuan/US Dollar, Pound Sterling/US Dollar, Japanese Yen/US Dollar, and Bitcoin/US Dollar.

Commodities = ICE Brent Crude Oil Futures, COMEX Gold Futures, COMEX Silver Futures, COMEX Copper Futures, and S&P Goldman Sachs Commodity Index (GSCI) Futures.

Derivatives = CBOE S&P 500 Volatility Index (VIX), ICE US Bond Market Volatility Index (MOVE), CBOE 3M Implied Correlation Index, and CBOE VIX Volatility Index (VVIX)/VIX.

All assets are directionally aligned with their historical correlation to the S&P 500. Each asset contributes equally based on its individual bullish or bearish signal. The overall market regime is calculated as the difference between the number of Risk-On and Risk-Off signals divided by the total number of assets, displayed as the percentage of markets confirming each regime. Green indicates Risk-On and occurs when the number of Risk-On signals exceeds Risk-Off signals, while red indicates Risk-Off and occurs when the number of Risk-Off signals exceeds Risk-On signals.

Bullish Signal = (Fast MA – Slow MA) > (ATR × ATR Margin)

Bearish Signal = (Fast MA – Slow MA) < –(ATR × ATR Margin)

Market Regime = (Risk-On signals – Risk-Off signals) ÷ Total assets

This indicator is designed with flexibility in mind, allowing users to include or exclude individual assets that contribute to the market regime and adjust the input parameters used for trend signal detection. These parameters apply to each independent asset, and the overall regime signal is smoothed by the signal length to reduce noise and enhance reliability. Investors can position according to the prevailing market regime by selecting factors that have historically outperformed under each regime environment to minimise downside risk and maximise upside potential:

Risk-On Equity Factors = High Beta > Cyclicals > Low Volatility > Defensives.

Risk-Off Equity Factors = Defensives > Low Volatility > Cyclicals > High Beta.

Risk-On Fixed Income Factors = High Yield > Investment Grade > Treasuries.

Risk-Off Fixed Income Factors = Treasuries > Investment Grade > High Yield.

Risk-On Commodity Factors = Industrial Metals > Energy > Agriculture > Gold.

Risk-Off Commodity Factors = Gold > Agriculture > Energy > Industrial Metals.

Risk-On Currency Factors = Cryptocurrencies > Foreign Currencies > US Dollar.

Risk-Off Currency Factors = US Dollar > Foreign Currencies > Cryptocurrencies.

In summary, the Market Regime Index is a comprehensive macro risk-management tool that identifies the current market regime and helps investors align portfolio risk with the market’s underlying risk appetite. Its intuitive, color-coded design makes it an indispensable resource for investors seeking to navigate shifting market conditions and enhance risk-adjusted performance by selecting factors that have historically outperformed. While it has proven historically valuable, asset-specific characteristics and correlations evolve over time as market dynamics change.

Cycle-Synced Channel Breakout📌 Cycle-Synced Channel Breakout – Detect Breakouts Confirmed by Candles and Momentum Cycles

📖 Overview

The Cycle-Synced Channel Breakout indicator is a precision breakout detection tool that combines the power of:

• Adaptive Keltner Channels

• Dominant Cycle Period Analysis (Ehlers-inspired)

• Candlestick Pattern Recognition (Engulfing)

This multi-layered approach helps identify true breakout opportunities by filtering out noise and false signals, making it ideal for swing traders and intraday traders seeking high-probability directional moves.

⚙️ How It Works

1. Keltner Channel Envelope

A dynamic volatility channel based on the EMA and ATR defines the upper and lower bounds of price movement.

2. Engulfing Candle Detection

The script detects strong bullish and bearish engulfing patterns, which often signal trend reversals or momentum continuations.

3. Dominant Cycle Momentum (Ehlers-inspired)

Using a smoothed power oscillator derived from a detrended price series, the indicator assesses whether momentum is accelerating during the breakout — filtering out weak moves.

4. Signal Confirmation Logic

A signal is only shown when:

• An engulfing pattern is detected, and

• Price breaks out of the Keltner Channel, and

• Momentum (cycle power) is rising

5. Visual Feedback

• Breakout signals are plotted with “BUY” or “SELL” labels

• Faded green/red background highlights confirmed breakouts

• Optional display of engulfing candles with triangle markers

⸻

🛠️ Key Features

• ✅ Adaptive Keltner Channels

• ✅ Bullish/Bearish Engulfing Candle Recognition

• ✅ Ehlers-style Cycle Momentum Confirmation

• ✅ Background highlights for confirmed breakouts

• ✅ Optional candle pattern visualization

• ✅ Lightweight and Pine v6 compatible

⸻

🧪 Inputs

• Keltner Length – EMA period for channel basis

• Multiplier – Multiplied with ATR to determine band width

• Cycle Lookback – Used to calculate smoothed cycle power

• Show Engulfing Candles? – Toggles candlestick signals

• Show Breakout Signals? – Toggles breakout labels and backgrounds

⸻

🧠 How to Use

• Look for “BUY” or “SELL” labels when:

• An engulfing candle breaks through the Keltner Channel

• Cycle momentum confirms strength behind the move

• The background color will faintly highlight the breakout direction.

• Use in combination with other trend or volume indicators for added confluence.

🔒 Notes

• This indicator is not repainting.

• It is designed for educational and research purposes only.

• Works across all timeframes and asset classes (stocks, crypto, forex, etc.)

Estimated Manipulation Movement Signal [AlgoPoint]Follow the Footprints of Whale Movements That Drive the Market

Overview

The market is not always driven by natural supply and demand. Large players—often called "whales" or institutions—can create artificial price movements to trigger stop-losses, induce panic or FOMO, and build their large positions at favorable prices. These events are known as "stop hunts" or "liquidity grabs."

The EMMS indicator is a specialized tool designed to detect these specific moments of potential market manipulation. It does not follow trends in a traditional sense; instead, it identifies high-probability reversal points created by the calculated actions of Smart Money trapping other market participants.

How It Works: The 3-Module Logic

The indicator uses a multi-stage confirmation process to identify a potential stop hunt:

1. Anomaly Detection: The engine first scans the chart for "Anomaly Candles." These are candles with unusually high volume and a very long wick relative to their body. This combination signals a sudden, forceful, and potentially unnatural price push.

2. Liquidity Zone Detection: The indicator automatically identifies and tracks recent significant swing highs and lows. These levels are considered "Liquidity Zones" because they are areas where a large number of stop-loss orders are likely clustered. These are the "hunting grounds" for whales.

3. The Stop Hunt Signal: A final signal is generated only when these two events align in a specific sequence:

An Anomaly Candle (high volume, long wick) spikes through a previously identified Liquidity Zone.

The same candle then reverses, closing back inside the previous price range.

This sequence confirms that the move was likely a "trap" designed to engineer liquidity, and a reversal in the opposite direction is now highly probable.

How to Interpret & Use This Indicator

BUY Signal: A BUY signal appears after a sharp price drop that pierces a recent swing low (taking out the stops of long positions) and then aggressively reverses to close higher. This suggests that Smart Money has absorbed the panic selling they just induced. The signal indicates a potential move UP.

SELL Signal: A SELL signal appears after a sharp price spike that pierces a recent swing high (taking out the stops of short positions) and then aggressively reverses to close lower. This suggests that Smart Money has sold into the FOMO buying they just created. The signal indicates a potential move DOWN.

This indicator is best used as a high-probability confirmation tool, ideally in conjunction with your understanding of the overall market trend and structure.

Cyclic Reversal Engine [AlgoPoint]Overview

Most indicators focus on price and momentum, but they often ignore a critical third dimension: time. Markets move in rhythmic cycles of expansion and contraction, but these cycles are not fixed; they speed up in trending markets and slow down in choppy conditions.

The Cyclic Reversal Engine is an advanced analytical tool designed to decode this rhythm. Instead of relying on static, lagging formulas, this indicator learns from past market behavior to anticipate when the current trend is statistically likely to reach its exhaustion point, providing high-probability reversal signals.

It achieves this by combining a sophisticated time analysis with a robust price-action confirmation.

How It Works: The Core Logic

The indicator operates on a multi-stage process to identify potential turning points in the market.

1. Market Regime Analysis (The Brain): Before analyzing any cycles, the indicator first diagnoses the current "personality" of the market. Using a combination of the ADX, Choppiness Index, and RSI, it classifies the market into one of three primary regimes:

- Trending: Strong, directional movement.

- Ranging: Sideways, non-directional chop.

- Reversal: An over-extended state (overbought/oversold) where a turn is imminent.

2. Adaptive Cycle Learning (The "Machine Learning" Aspect): This is the indicator's smartest feature. It constantly analyzes past cycles by measuring the bar-count between significant swing highs and swing lows. Crucially, it learns the average cycle duration for each specific market regime. For example, it learns that "in a strong trending market, a new swing low tends to occur every 35 bars," while "in a ranging market, this extends to 60 bars."

3. The Countdown & Timing Signal: The indicator identifies the last major swing high or low and starts a bar-by-bar countdown. Based on the current market regime, it selects the appropriate learned cycle length from its memory. When the bar count approaches this adaptive target, the indicator determines that a reversal is "due" from a timing perspective.

4. Price Confirmation (The Trigger): A signal is never generated based on timing alone. Once the timing condition is met (the cycle is "due"), the indicator waits for a final price-action confirmation. The default confirmation is the RSI entering an extreme overbought or oversold zone, signaling momentum exhaustion. The signal is only triggered when Time + Price Confirmation align.

How to Use This Indicator

- The Dashboard: The panel in the bottom-right corner is your command center.

- Market Regime: Shows the current market personality analyzed by the engine.

- Adaptive Cycle / Bar Count: This is the core of the indicator. It shows the target cycle length for the current regime (e.g., 50) and the current bar count since the last swing point (e.g., 45). The background turns orange when the bar count enters the "due zone," indicating that you should be on high alert for a reversal.

- BUY/SELL Signals: A label appears on the chart only when the two primary conditions are met:

The timing is right (Bar Count has reached the Adaptive Cycle target).

The price confirms exhaustion (RSI is in an extreme zone).

A BUY signal suggests a downtrend cycle is likely complete, and a SELL signal suggests an uptrend cycle is likely complete.

Key Settings

- Pivot Lookback: Controls the sensitivity of the swing point detection. Higher values will identify more significant, longer-term cycles.

- Market Regime Engine: The ADX, Choppiness, and RSI settings can be fine-tuned to adjust how the indicator classifies the market's personality.

- Require Price Confirmation: You can toggle the RSI confirmation on or off. It is highly recommended to keep it enabled for higher-quality signals.

MERV: Market Entropy & Rhythm Visualizer [BullByte]The MERV (Market Entropy & Rhythm Visualizer) indicator analyzes market conditions by measuring entropy (randomness vs. trend), tradeability (volatility/momentum), and cyclical rhythm. It provides traders with an easy-to-read dashboard and oscillator to understand when markets are structured or choppy, and when trading conditions are optimal.

Purpose of the Indicator

MERV’s goal is to help traders identify different market regimes. It quantifies how structured or random recent price action is (entropy), how strong and volatile the movement is (tradeability), and whether a repeating cycle exists. By visualizing these together, MERV highlights trending vs. choppy environments and flags when conditions are favorable for entering trades. For example, a low entropy value means prices are following a clear trend line, whereas high entropy indicates a lot of noise or sideways action. The indicator’s combination of measures is original: it fuses statistical trend-fit (entropy), volatility trends (ATR and slope), and cycle analysis to give a comprehensive view of market behavior.

Why a Trader Should Use It

Traders often need to know when a market trend is reliable vs. when it is just noise. MERV helps in several ways: it shows when the market has a strong direction (low entropy, high tradeability) and when it’s ranging (high entropy). This can prevent entering trend-following strategies during choppy periods, or help catch breakouts early. The “Optimal Regime” marker (a star) highlights moments when entropy is very low and tradeability is very high, typically the best conditions for trend trades. By using MERV, a trader gains an empirical “go/no-go” signal based on price history, rather than guessing from price alone. It’s also adaptable: you can apply it to stocks, forex, crypto, etc., on any timeframe. For example, during a bullish phase of a stock, MERV will turn green (Trending Mode) and often show a star, signaling good follow-through. If the market later grinds sideways, MERV will shift to magenta (Choppy Mode), warning you that trend-following is now risky.

Why These Components Were Chosen

Market Entropy (via R²) : This measures how well recent prices fit a straight line. We compute a linear regression on the last len_entropy bars and calculate R². Entropy = 1 - R², so entropy is low when prices follow a trend (R² near 1) and high when price action is erratic (R² near 0). This single number captures trend strength vs noise.

Tradeability (ATR + Slope) : We combine two familiar measures: the Average True Range (ATR) (normalized by price) and the absolute slope of the regression line (scaled by ATR). Together they reflect how active and directional the market is. A high ATR or strong slope means big moves, making a trend more “tradeable.” We take a simple average of the normalized ATR and slope to get tradeability_raw. Then we convert it to a percentile rank over the lookback window so it’s stable between 0 and 1.

Percentile Ranks : To make entropy and tradeability values easy to interpret, we convert each to a 0–100 rank based on the past len_entropy periods. This turns raw metrics into a consistent scale. (For example, an entropy rank of 90 means current entropy is higher than 90% of recent values.) We then divide by 100 to plot them on a 0–1 scale.

Market Mode (Regime) : Based on those ranks, MERV classifies the market:

Trending (Green) : Low entropy rank (<40%) and high tradeability rank (>60%). This means the market is structurally trending with high activity.

Choppy (Magenta) : High entropy rank (>60%) and low tradeability rank (<40%). This is a mostly random, low-momentum market.

Neutral (Cyan) : All other cases. This covers mixed regimes not strongly trending or choppy.

The mode is shown as a colored bar at the bottom: green for trending, magenta for choppy, cyan for neutral.

Optimal Regime Signal : Separately, we mark an “optimal” condition when entropy_norm < 0.3 and tradeability > 0.7 (both normalized 0–1). When this is true, a ★ star appears on the bottom line. This star is colored white when truly optimal, gold when only tradeability is high (but entropy not quite low enough), and black when neither condition holds. This gives a quick visual cue for very favorable conditions.

What Makes MERV Stand Out

Holistic View : Unlike a single-oscillator, MERV combines trend, volatility, and cycle analysis in one tool. This multi-faceted approach is unique.

Visual Dashboard : The fixed on-chart dashboard (shown at your chosen corner) summarizes all metrics in bar/gauge form. Even a non-technical user can glance at it: more “█” blocks = a higher value, colors match the plots. This is more intuitive than raw numbers.

Adaptive Thresholds : Using percentile ranks means MERV auto-adjusts to each market’s character, rather than requiring fixed thresholds.

Cycle Insight : The rhythm plot adds information rarely found in indicators – it shows if there’s a repeating cycle (and its period in bars) and how strong it is. This can hint at natural bounce or reversal intervals.

Modern Look : The neon color scheme and glow effects make the lines easy to distinguish (blue/pink for entropy, green/orange for tradeability, etc.) and the filled area between them highlights when one dominates the other.

Recommended Timeframes

MERV can be applied to any timeframe, but it will be more reliable on higher timeframes. The default len_entropy = 50 and len_rhythm = 30 mean we use 30–50 bars of history, so on a daily chart that’s ~2–3 months of data; on a 1-hour chart it’s about 2–3 days. In practice:

Swing/Position traders might prefer Daily or 4H charts, where the calculations smooth out small noise. Entropy and cycles are more meaningful on longer trends.

Day trader s could use 15m or 1H charts if they adjust the inputs (e.g. shorter windows). This provides more sensitivity to intraday cycles.

Scalpers might find MERV too “slow” unless input lengths are set very low.

In summary, the indicator works anywhere, but the defaults are tuned for capturing medium-term trends. Users can adjust len_entropy and len_rhythm to match their chart’s volatility. The dashboard position can also be moved (top-left, bottom-right, etc.) so it doesn’t cover important chart areas.

How the Scoring/Logic Works (Step-by-Step)

Compute Entropy : A linear regression line is fit to the last len_entropy closes. We compute R² (goodness of fit). Entropy = 1 – R². So a strong straight-line trend gives low entropy; a flat/noisy set of points gives high entropy.

Compute Tradeability : We get ATR over len_entropy bars, normalize it by price (so it’s a fraction of price). We also calculate the regression slope (difference between the predicted close and last close). We scale |slope| by ATR to get a dimensionless measure. We average these (ATR% and slope%) to get tradeability_raw. This represents how big and directional price moves are.

Convert to Percentiles : Each new entropy and tradeability value is inserted into a rolling array of the last 50 values. We then compute the percentile rank of the current value in that array (0–100%) using a simple loop. This tells us where the current bar stands relative to history. We then divide by 100 to plot on .

Determine Modes and Signal : Based on these normalized metrics: if entropy < 0.4 and tradeability > 0.6 (40% and 60% thresholds), we set mode = Trending (1). If entropy > 0.6 and tradeability < 0.4, mode = Choppy (-1). Otherwise mode = Neutral (0). Separately, if entropy_norm < 0.3 and tradeability > 0.7, we set an optimal flag. These conditions trigger the colored mode bars and the star line.

Rhythm Detection : Every bar, if we have enough data, we take the last len_rhythm closes and compute the mean and standard deviation. Then for lags from 5 up to len_rhythm, we calculate a normalized autocorrelation coefficient. We track the lag that gives the maximum correlation (best match). This “best lag” divided by len_rhythm is plotted (a value between 0 and 1). Its color changes with the correlation strength. We also smooth the best correlation value over 5 bars to plot as “Cycle Strength” (also 0 to 1). This shows if there is a consistent cycle length in recent price action.

Heatmap (Optional) : The background color behind the oscillator panel can change with entropy. If “Neon Rainbow” style is on, low entropy is blue and high entropy is pink (via a custom color function), otherwise a classic green-to-red gradient can be used. This visually reinforces the entropy value.

Volume Regime (Dashboard Only) : We compute vol_norm = volume / sma(volume, len_entropy). If this is above 1.5, it’s considered high volume (neon orange); below 0.7 is low (blue); otherwise normal (green). The dashboard shows this as a bar gauge and percentage. This is for context only.

Oscillator Plot – How to Read It

The main panel (oscillator) has multiple colored lines on a 0–1 vertical scale, with horizontal markers at 0.2 (Low), 0.5 (Mid), and 0.8 (High). Here’s each element:

Entropy Line (Blue→Pink) : This line (and its glow) shows normalized entropy (0 = very low, 1 = very high). It is blue/green when entropy is low (strong trend) and pink/purple when entropy is high (choppy). A value near 0.0 (below 0.2 line) indicates a very well-defined trend. A value near 1.0 (above 0.8 line) means the market is very random. Watch for it dipping near 0: that suggests a strong trend has formed.

Tradeability Line (Green→Yellow) : This represents normalized tradeability. It is colored bright green when tradeability is low, transitioning to yellow as tradeability increases. Higher values (approaching 1) mean big moves and strong slopes. Typically in a market rally or crash, this line will rise. A crossing above ~0.7 often coincides with good trend strength.

Filled Area (Orange Shade) : The orange-ish fill between the entropy and tradeability lines highlights when one dominates the other. If the area is large, the two metrics diverge; if small, they are similar. This is mostly aesthetic but can catch the eye when the lines cross over or remain close.

Rhythm (Cycle) Line : This is plotted as (best_lag / len_rhythm). It indicates the relative period of the strongest cycle. For example, a value of 0.5 means the strongest cycle was about half the window length. The line’s color (green, orange, or pink) reflects how strong that cycle is (green = strong). If no clear cycle is found, this line may be flat or near zero.

Cycle Strength Line : Plotted on the same scale, this shows the autocorrelation strength (0–1). A high value (e.g. above 0.7, shown in green) means the cycle is very pronounced. Low values (pink) mean any cycle is weak and unreliable.

Mode Bars (Bottom) : Below the main oscillator, thick colored bars appear: a green bar means Trending Mode, magenta means Choppy Mode, and cyan means Neutral. These bars all have a fixed height (–0.1) and make it very easy to see the current regime.

Optimal Regime Line (Bottom) : Just below the mode bars is a thick horizontal line at –0.18. Its color indicates regime quality: White (★) means “Optimal Regime” (very low entropy and high tradeability). Gold (★) means not quite optimal (high tradeability but entropy not low enough). Black means neither condition. This star line quickly tells you when conditions are ideal (white star) or simply good (gold star).

Horizontal Guides : The dotted lines at 0.2 (Low), 0.5 (Mid), and 0.8 (High) serve as reference lines. For example, an entropy or tradeability reading above 0.8 is “High,” and below 0.2 is “Low,” as labeled on the chart. These help you gauge values at a glance.

Dashboard (Fixed Corner Panel)

MERV also includes a compact table (dashboard) that can be positioned in any corner. It summarizes key values each bar. Here is how to read its rows:

Entropy : Shows a bar of blocks (█ and ░). More █ blocks = higher entropy. It also gives a percentage (rounded). A full bar (10 blocks) with a high % means very chaotic market. The text is colored similarly (blue-green for low, pink for high).

Rhythm : Shows the best cycle period in bars (e.g. “15 bars”). If no calculation yet, it shows “n/a.” The text color matches the rhythm line.

Cycle Strength : Gives the cycle correlation as a percentage (smoothed, as shown on chart). Higher % (green) means a strong cycle.

Tradeability : Displays a 10-block gauge for tradeability. More blocks = more tradeable market. It also shows “gauge” text colored green→yellow accordingly.

Market Mode : Simply shows “Trending”, “Choppy”, or “Neutral” (cyan text) to match the mode bar color.

Volume Regime : Similar to tradeability, shows blocks for current volume vs. average. Above-average volume gives orange blocks, below-average gives blue blocks. A % value indicates current volume relative to average. This row helps see if volume is abnormally high or low.

Optimal Status (Large Row) : In bold, either “★ Optimal Regime” (white text) if the star condition is met, “★ High Tradeability” (gold text) if tradeability alone is high, or “— Not Optimal” (gray text) otherwise. This large row catches your eye when conditions are ripe.

In short, the dashboard turns the numeric state into an easy read: filled bars, colors, and text let you see current conditions without reading the plot. For instance, five blue blocks under Entropy and “25%” tells you entropy is low (good), and a row showing “Trending” in green confirms a trend state.

Real-Life Example

Example : Consider a daily chart of a trending stock (e.g. “AAPL, 1D”). During a strong uptrend, recent prices fit a clear upward line, so Entropy would be low (blue line near bottom, perhaps below the 0.2 line). Volatility and slope are high, so Tradeability is high (green-yellow line near top). In the dashboard, Entropy might show only 1–2 blocks (e.g. 10%) and Tradeability nearly full (e.g. 90%). The Market Mode bar turns green (Trending), and you might see a white ★ on the optimal line if conditions are very good. The Volume row might light orange if volume is above average during the rally. In contrast, imagine the same stock later in a tight range: Entropy will rise (pink line up, more blocks in dashboard), Tradeability falls (fewer blocks), and the Mode bar turns magenta (Choppy). No star appears in that case.

Consolidated Use Case : Suppose on XYZ stock the dashboard reads “Entropy: █░░░░░░░░ 20%”, “Tradeability: ██████████ 80%”, Mode = Trending (green), and “★ Optimal Regime.” This tells the trader that the market is in a strong, low-noise trend, and it might be a good time to follow the trend (with appropriate risk controls). If instead it reads “Entropy: ████████░░ 80%”, “Tradeability: ███▒▒▒▒▒▒ 30%”, Mode = Choppy (magenta), the trader knows the market is random and low-momentum—likely best to sit out until conditions improve.

Example: How It Looks in Action

Screenshot 1: Trending Market with High Tradeability (SOLUSD, 30m)

What it means:

The market is in a clear, strong trend with excellent conditions for trading. Both trend-following and active strategies are favored, supported by high tradeability and strong volume.

Screenshot 2: Optimal Regime, Strong Trend (ETHUSD, 1h)

What it means:

This is an ideal environment for trend trading. The market is highly organized, tradeability is excellent, and volume supports the move. This is when the indicator signals the highest probability for success.

Screenshot 3: Choppy Market with High Volume (BTC Perpetual, 5m)

What it means:

The market is highly random and choppy, despite a surge in volume. This is a high-risk, low-reward environment, avoid trend strategies, and be cautious even with mean-reversion or scalping.

Settings and Inputs

The script is fully open-source; here are key inputs the user can adjust:

Entropy Window (len_entropy) : Number of bars used for entropy and tradeability (default 50). Larger = smoother, more lag; smaller = more sensitivity.

Rhythm Window (len_rhythm ): Bars used for cycle detection (default 30). This limits the longest cycle we detect.

Dashboard Position : Choose any corner (Top Right default) so it doesn’t cover chart action.

Show Heatmap : Toggles the entropy background coloring on/off.

Heatmap Style : “Neon Rainbow” (colorful) or “Classic” (green→red).

Show Mode Bar : Turn the bottom mode bar on/off.

Show Dashboard : Turn the fixed table panel on/off.

Each setting has a tooltip explaining its effect. In the description we will mention typical settings (e.g. default window sizes) and that the user can move the dashboard corner as desired.

Oscillator Interpretation (Recap)

Lines : Blue/Pink = Entropy (low=trend, high=chop); Green/Yellow = Tradeability (low=quiet, high=volatile).

Fill : Orange tinted area between them (for visual emphasis).

Bars : Green=Trending, Magenta=Choppy, Cyan=Neutral (at bottom).

Star Line : White star = ideal conditions, Gold = good but not ideal.

Horizontal Guides : 0.2 and 0.8 lines mark low/high thresholds for each metric.

Using the chart, a coder or trader can see exactly what each output represents and make decisions accordingly.

Disclaimer

This indicator is provided as-is for educational and analytical purposes only. It does not guarantee any particular trading outcome. Past market patterns may not repeat in the future. Users should apply their own judgment and risk management; do not rely solely on this tool for trading decisions. Remember, TradingView scripts are tools for market analysis, not personalized financial advice. We encourage users to test and combine MERV with other analysis and to trade responsibly.

-BullByte

Chandelier Exit Oscillator [LuxAlgo]The Chandelier Exit Oscillator is a technical analysis tool that provides insights into potential trend reversals, momentum shifts, and trend continuation patterns, helping traders pinpoint optimal exit points for both long and short positions.

By calculating trailing stop levels based on a multiple of the Average True Range (ATR), the oscillator visually indicates when prices move above or below these critical stop levels.

This script uniquely combines the Chandelier Exit indicator with an oscillator format, equipping traders with a versatile tool that leverages ATR-based levels for enhanced trend analysis.

🔶 USAGE

Displaying the Chandelier Exit as an oscillator allows traders to gauge trend momentum and strength, recognize potential reversals, and refine their market insights.

The Timeframe option specifies the timeframe used for calculations, enabling multi-timeframe analysis and allowing traders to align the indicator’s signals with broader or narrower market trends.

The Chandelier Exit Oscillator allows users to select between a Regular or Normalized oscillator type. The Regular option displays raw oscillator values, while the Normalized version smooths values and scales them from 0 to 100.

The Chandelier Exit Overlay allows users to enable or disable the display of Chandelier Exit levels directly on the price chart. When enabled, this overlay plots trailing stop levels for both long and short positions, helping traders visually monitor potential exit points and trend boundaries alongside the price action.

The Trend-based Bar Color feature allows users to color the bars on the price chart according to the current trend direction. This visual differentiation aids in quicker decision-making and provides a clearer understanding of market dynamics.

🔶 SETTINGS

🔹 Chandelier Exit Settings

Timeframe: Sets the timeframe for calculations, allowing multi-timeframe analysis.

ATR Length: Defines the number of bars used for calculating the Average True Range (ATR), which helps in setting Chandelier Exit levels.

ATR Multiplier: Adjusts the sensitivity of the Chandelier Exit lines based on the ATR. Higher values make the indicator more conservative, while lower values make it more responsive.

🔹 Chandelier Exit Oscillator

Chandelier Exit Oscillator: Allows users to choose between a Regular or Normalized oscillator type. The Regular option displays raw oscillator values, while the Normalized version smooths values and scales them from 0 to 100.

Oscillator Smoothing: Controls the level of smoothing applied to the oscillator. Higher smoothing values filter out minor fluctuations.

🔹 Chandelier Exit Overlay

Chandelier Exit Overlay: Enables or disables the display of Chandelier Exit levels directly on the price chart.

Trend-based Bar Colors: Allows users to color bars based on trend direction, enhancing the visual analysis of market direction.

🔶 RELATED SCRIPTS

Market-Structure-Oscillator

Rolling 250-Day Sharpe RatioThis Pine Script indicator, “Rolling 250-Day Sharpe Ratio”, computes the trailing Sharpe Ratio for any traded asset over a 250-session window, equivalent to approximately one trading year. The script first derives daily log returns and adjusts them by subtracting the daily equivalent of the 3-month US Treasury yield to obtain the excess return. It then calculates the rolling mean and standard deviation of these excess returns to produce the annualized Sharpe Ratio, which is displayed as a continuous time series on the chart. This allows traders and analysts to assess how the asset’s risk-adjusted performance evolves over time relative to a risk-free benchmark.

A persistently high Sharpe Ratio can indicate strong risk-adjusted returns, but it is essential to approach extreme values with caution. Elevated Sharpe readings can sometimes reflect unsustainable trends, excessive leverage, or periods of unusually low volatility that may revert abruptly. Conversely, a low or negative Sharpe Ratio does not automatically imply an asset should be avoided; it might signal an opportunity if the risk environment normalizes.

Adaptive Cycle Oscillator with EMADescription of the Adaptive Cycle Oscillator with EMA Pine Script

This Pine Script, titled "Adaptive Cycle Oscillator with EMA", is a custom technical indicator designed for TradingView to help traders analyze market cycles and identify potential buy or sell opportunities. It combines an Adaptive Cycle Oscillator (ACO) with multiple Exponential Moving Averages (EMAs), displayed as colorful, wavy lines, and includes features like buy/sell signals and divergence detection. Below is a beginner-friendly explanation of how the script works, adhering to TradingView's Script Publishing Rules.

What This Indicator Does

The Adaptive Cycle Oscillator with EMA helps you:

Visualize market cycles using an oscillator that adapts to price movements.

Track trends with seven EMAs of different lengths, plotted as a rainbow of wavy lines.

Identify potential buy or sell signals when the oscillator crosses predefined thresholds.

Spot divergences between the oscillator and price to anticipate reversals.

Use customizable settings to adjust the indicator to your trading style.

Note: This is a technical analysis tool and does not guarantee profits. Always combine it with other analysis methods and practice risk management.

Step-by-Step Explanation for New Users

1. Understanding the Indicator

Adaptive Cycle Oscillator (ACO): The ACO analyzes price data (based on high, low, and close prices, or HLC3) to detect market cycles. It smooths price movements to create an oscillator that swings between overbought and oversold levels.

EMAs: Seven EMAs of different lengths are applied to the ACO and scaled based on the market's dominant cycle. These EMAs are plotted as colorful, wavy lines to show trend direction.

Buy/Sell Signals: The script generates signals when the ACO crosses above or below user-defined thresholds, indicating potential entry or exit points.

Divergence Detection: The script identifies bullish or bearish divergences between the ACO and the fastest EMA, which may signal potential reversals.

Visual Style: The indicator uses a rainbow of seven colors (red, orange, yellow, green, blue, indigo, violet) for the EMAs, with wavy lines for a unique visual effect. Static levels (zero, overbought, oversold) are also wavy for consistency.

2. How to Add the Indicator to Your Chart

Open TradingView and load the chart of any asset (e.g., stock, forex, crypto).

Click on the Indicators button at the top of the chart.

Search for "Adaptive Cycle Oscillator with EMA" (or paste the script into TradingView’s Pine Editor if you have access to it).

Click to add the indicator to your chart. It will appear in a separate panel below the price chart.

3. Customizing the Indicator

The script offers several input options to tailor it to your needs:

Base Cycle Length (Default: 20): Sets the initial period for calculating the dominant cycle. Higher values make the indicator slower; lower values make it more sensitive.

Alpha Smoothing (Default: 0.07): Controls how much the ACO smooths price data. Smaller values produce smoother results.

Show Buy/Sell Signals (Default: True): Toggle to display green triangles (buy) and red triangles (sell) on the chart.

Threshold (Default: 0.0): Defines overbought (above threshold) and oversold (below threshold) levels. Adjust to widen or narrow signal zones.

EMA Base Length (Default: 10): Sets the starting length for the fastest EMA. Other EMAs are incrementally longer (12, 14, 16, etc.).

Divergence Lookback (Default: 14): Determines how far back the script looks to detect divergences.

To adjust these:

Right-click the indicator on your chart and select Settings.

Modify the inputs in the pop-up window.

Click OK to apply changes.

4. Reading the Indicator

Oscillator and EMAs: The ACO and seven EMAs are plotted in a separate panel. The EMAs (colored lines) move in a wavy pattern:

Red (fastest) to Violet (slowest) represent different response speeds.

When the faster EMAs (e.g., red, orange) are above slower ones (e.g., blue, violet), it suggests bullish momentum, and vice versa.

Zero Line: A gray wavy line at zero acts as a neutral level. The ACO above zero indicates bullish conditions; below zero indicates bearish conditions.

Overbought/Oversold Lines: Red (overbought) and green (oversold) wavy lines mark threshold levels. Extreme ACO values near these lines may suggest reversals.

Buy/Sell Signals:

Green Triangle (Bottom): Appears when the ACO crosses above the oversold threshold, suggesting a potential buy.

Red Triangle (Top): Appears when the ACO crosses below the overbought threshold, suggesting a potential sell.

Divergences:

Green Triangle (Bottom): Indicates a bullish divergence (price makes a lower low, but the EMA makes a higher low), hinting at a potential upward reversal.

Red Triangle (Top): Indicates a bearish divergence (price makes a higher high, but the EMA makes a lower high), hinting at a potential downward reversal.

5. Using Alerts

You can set alerts for key events:

Right-click the indicator and select Add Alert.

Choose a condition (e.g., "ACO Buy Signal", "Bullish Divergence").

Configure the alert settings (e.g., notify via email, app, or pop-up).

Click Create to activate the alert.

Available alert conditions:

ACO Buy Signal: When the ACO crosses above the oversold threshold.

ACO Sell Signal: When the ACO crosses below the overbought threshold.

Bullish Divergence: When a potential upward reversal is detected.

Bearish Divergence: When a potential downward reversal is detected.

6. Tips for Using the Indicator

Combine with Other Tools: Use the indicator alongside support/resistance levels, candlestick patterns, or other indicators (e.g., RSI, MACD) for confirmation.

Test on Different Timeframes: The indicator works on any timeframe (e.g., 1-minute, daily). Shorter timeframes may produce more signals but with more noise.

Practice Risk Management: Never rely solely on this indicator. Set stop-losses and position sizes to manage risk.

Backtest First: Use TradingView’s Strategy Tester (if you convert the script to a strategy) to evaluate performance on historical data.

Compliance with TradingView’s Script Publishing Rules

This description adheres to TradingView’s Script Publishing Rules (as outlined in the provided link):

No Performance Claims: The description avoids promising profits or specific results, emphasizing that the indicator is a tool for analysis.

Clear Instructions: It provides step-by-step guidance for adding, customizing, and using the indicator.

Risk Disclaimer: It notes that trading involves risks and the indicator should be used with other analysis methods.

No Misleading Terms: Terms like “buy” and “sell” are used to describe signals, not guaranteed actions.

Transparency: The description explains the indicator’s components (ACO, EMAs, signals, divergences) without exaggerating its capabilities.

No External Links: The description avoids linking to external resources or soliciting users.

Educational Tone: It focuses on educating users about the indicator’s functionality.

Limitations

Not a Standalone System: The indicator is not a complete trading strategy. It provides insights but requires additional analysis.

Lagging Nature: As with most oscillators and EMAs, signals may lag behind price movements, especially in fast markets.

False Signals: Signals and divergences may not always lead to successful trades, particularly in choppy markets.

Market Dependency: Performance varies across assets and market conditions (e.g., trending vs. ranging markets).

True Seasonal Pattern [tradeviZion]True Seasonal Pattern: Uncover Hidden Market Cycles

Markets have rhythms and patterns that repeat with surprising regularity. The True Seasonal Pattern indicator reveals these hidden cycles across different timeframes, helping you anticipate potential market movements based on historical seasonal tendencies.

What This Indicator Does

The True Seasonal Pattern analyzes years of historical price data to identify recurring seasonal trends. It then plots these patterns on your chart, showing you both the historical pattern and future projection based on past seasonal behavior.

Automatic Timeframe Detection: Works with Monthly, Weekly, and Daily charts

Historical Pattern Analysis: Analyzes up to 100 years of data (customizable)

Future Projection: Projects the seasonal pattern ahead on your chart

Smart Smoothing: Applies appropriate smoothing based on your timeframe

How to Use This Indicator

Add the indicator to a Daily, Weekly, or Monthly chart (not designed for intraday timeframes)

The indicator automatically detects your chart's timeframe

The blue line shows the historical seasonal pattern

Watch for potential turning points in the pattern that align with other technical signals

Seasonal patterns work best as a supporting factor in your analysis, not as standalone trading signals. They are particularly effective in markets with well-established seasonal influences.

Best Applications

Futures Markets: Commodities and futures often show strong seasonal tendencies due to production cycles, weather patterns, and economic factors

Stock Indices: Many stock markets demonstrate regular seasonal patterns (like the "Sell in May" phenomenon)

Individual Stocks: Companies with seasonal business cycles often show predictable price patterns

Practical Applications

Identify potential turning points based on historical seasonal patterns

Plan entries and exits around seasonal tendencies

Add seasonal context to your existing technical analysis

Understand why certain months or periods might show consistent behavior

Pro Tip: For best results, use this tool on instruments with at least 5+ years of historical data. Longer timeframes often reveal more reliable seasonal patterns.

Important Notes

This indicator works best on Daily, Weekly, and Monthly timeframes - not intraday charts

Seasonal patterns are tendencies, not guarantees

Always combine seasonal analysis with other technical tools

Past patterns may not repeat exactly in the future

// Sample of the seasonal calculation approach

float yearHigh = array.max(currentYearHighs)

float yearLow = array.min(currentYearLows)

// Calculate seasonality for each period

for i = 0 to array.size(currentYearCloses) - 1

float periodClose = array.get(currentYearCloses, i)

if not na(periodClose) and yearHigh != yearLow

float seasonality = (periodClose - yearLow) / (yearHigh - yearLow) * 100

I developed this indicator to help traders incorporate seasonal analysis into their trading approach without the complexity of traditional seasonal tools. Whether you're analyzing agricultural commodities, energy futures, or stock indices, understanding the seasonal context can provide valuable insights for your trading decisions.

Remember: Markets don't always follow seasonal patterns, but when they do, being aware of these tendencies can give you a meaningful edge in your analysis.

Open Vertical Lines [TradeWithRon]This indicator allows traders to draw vertical lines manually or automatically based on the current or specified higher timeframes. It is a versatile tool designed to help users identify and mark significant changes in the market, such as new candle formations, based on a selected or auto-adjusted timeframe.

Open Source

Features:

Timeframe Customization: Users can either manually specify a desired timeframe (e.g., 1-hour, 1-day, etc.) or enable the "Auto" feature, which automatically adjusts the timeframe based on the current chart's timeframe for better alignment with different trading strategies.

Customizable Line Style: The vertical line can be drawn in three different styles: Solid, Dashed, or Dotted, giving users the flexibility to choose their preferred appearance for better chart readability.

Line Color: Users can select the color of the vertical line with transparency options to match their chart's visual preferences.

Auto Timeframe Adjustments: The "Auto Align" option dynamically adjusts the timeframe used for vertical lines depending on the chart's current timeframe. For example, if you’re using a lower timeframe (e.g., 5 minutes), the indicator will automatically switch to a higher timeframe (e.g., 1 hour or daily) to mark vertical lines, ensuring the lines correspond to higher timeframe price action.

Vertical Line Placement:

A vertical line is placed each time a new candle appears on the chart, marking key moments for the user to analyze market movements. This can be helpful for marking the start of new trading sessions or significant events in the market.

How to Use:

1. Apply the indicator to your chart.

2. Configure the preferred timeframe settings (either fixed or auto-align).

3. Customize the line style and color according to your visual preference.

4. The indicator will automatically place vertical lines on the chart when a new candle is formed, based on your selected timeframe.

[GYTS-CE] Market Regime Detector🧊 Market Regime Detector (Community Edition)

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- INTRODUCTION --------- 🌸

💮 What is the Market Regime Detector?

The Market Regime Detector is an advanced, consensus-based indicator that identifies the current market state to increase the probability of profitable trades. By distinguishing between trending (bullish or bearish) and cyclic (range-bound) market conditions, this detector helps you select appropriate tactics for different environments. Instead of forcing a single strategy across all market conditions, our detector allows you to adapt your approach based on real-time market behaviour.

💮 The Importance of Market Regimes

Markets constantly shift between different behavioural states or "regimes":

• Bullish trending markets - characterised by sustained upward price movement

• Bearish trending markets - characterised by sustained downward price movement

• Cyclic markets - characterised by range-bound, oscillating behaviour

Each regime requires fundamentally different trading approaches. Trend-following strategies excel in trending markets but fail in cyclic ones, while mean-reversion strategies shine in cyclic markets but underperform in trending conditions. Detecting these regimes is essential for successful trading, which is why we've developed the Market Regime Detector to accurately identify market states using complementary detection methods.

🌸 --------- KEY FEATURES --------- 🌸

💮 Consensus-Based Detection

Rather than relying on a single method, our detector employs two complementary detection methodologies that analyse different aspects of market behaviour:

• Dominant Cycle Average (DCA) - analyzes price movement relative to its lookback period, a proxy for the dominant cycle

• Volatility Channel - examines price behaviour within adaptive volatility bands

These diverse perspectives are synthesised into a robust consensus that minimises false signals while maintaining responsiveness to genuine regime changes.

💮 Dominant Cycle Framework

The Market Regime Detector uses the concept of dominant cycles to establish a reference framework. You can input the dominant cycle period that best represents the natural rhythm of your market, providing a stable foundation for regime detection across different timeframes.