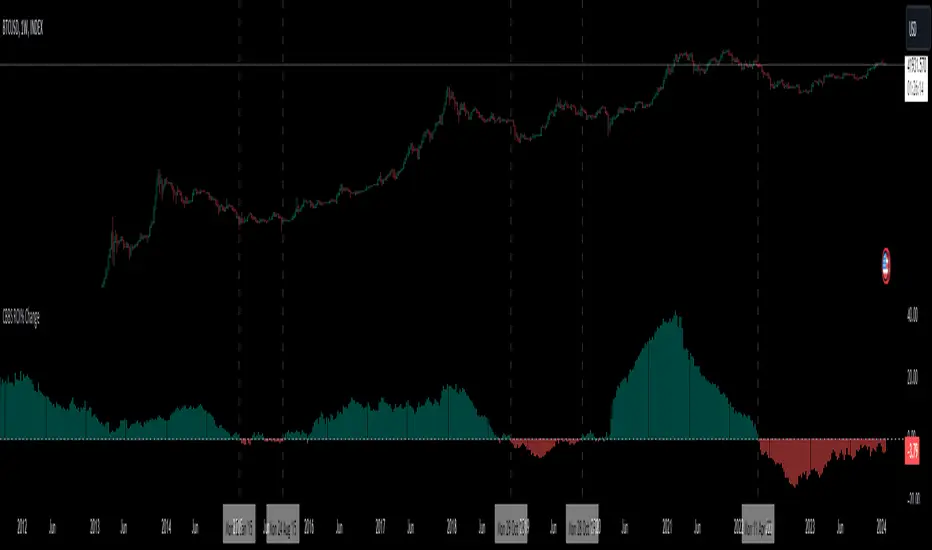

2-Year MA Multiplier [UAlgo]The 2-Year MA Multiplier is a technical analysis tool designed to assist traders and investors in identifying potential overbought and oversold conditions in the market. By plotting the 2-year moving average (MA) of an asset's closing price alongside an upper band set at five times this moving average, the indicator provides visual cues to assess long-term price trends and significant market movements.

🔶 Key Features

2-Year Moving Average (MA): Calculates the simple moving average of the asset's closing price over a 730-day period, representing approximately two years.

Visual Indicators: Plots the 2-year MA in forest green and the upper band in firebrick red for clear differentiation.

Fills the area between the 2-year MA and the upper band to highlight the normal trading range.

Uses color-coded fills to indicate overbought (tomato red) and oversold (cornflower blue) conditions based on the asset's closing price relative to the bands.

🔶 Idea

The concept behind the 2-Year MA Multiplier is rooted in the cyclical nature of markets, particularly in assets like Bitcoin. By analyzing long-term price movements, the indicator aims to identify periods of significant deviation from the norm, which may signal potential buying or selling opportunities.

2-year MA smooths out short-term volatility, providing a clearer view of the asset's long-term trend. This timeframe is substantial enough to capture major market cycles, making it a reliable baseline for analysis.

Multiplying the 2-year MA by five establishes an upper boundary that has historically correlated with market tops. When the asset's price exceeds this upper band, it may indicate overbought conditions, suggesting a potential for price correction. Conversely, when the price falls below the 2-year MA, it may signal oversold conditions, presenting potential buying opportunities.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Cycle

Weekly Stacked Daily Changes [LuxAlgo]The Weekly Stacked Daily Changes tool allows traders to compare daily net price changes for each day of the week, stacked by week. It provides a very convenient way to compare daily and weekly volatility at the same time.

🔶 USAGE

The tool requires no configuration and works perfectly out of the box, displaying the net price change for each day of the week as stacked boxes of the appropriate size.

Traders can adjust the width of the columns and the spacing between days and weeks, options to change the color and disable the months and new month lines are also available.

🔹 Bottom Stack Bias

This feature allows traders to compare weekly volatility in two different ways.

With this feature disabled, all weeks use zero as the bottom of the stack, so traders can see at a glance weeks with more volatility and weeks with less volatility.

Enabling this feature will cause the tool to display the stacks with the weekly net price change as the bottom, so if a stack starts below the zero line it means that week has a negative net return, and if it starts above the zero line it means that week has a positive net return.

🔶 SETTINGS

Width: Select the fixed width for each column.

Offset: Choose the fixed width between each column.

Spacing: Select the distance between each day within each column.

🔹 Style

Bottom Stack Bias: Use weekly net price change as the bottom of the stack.

Bullish Change: Color for days with positive net price change

Bearish Change: Color for days with negative net price change

Show Months: Under each week stack, display the month

Show Months Delimiter: Display a line indicating the start of a new month

[TheMandalor] Invert or Mirror Chart SUPPORT RESSISTANTThis is a new idea to find supports and resistant’s for any charts.

What is the concept of this indicator:

1. It is used close and inverted it on chart

2. When the real chart and the inverted chart is crossing together several times, this point will be important on this concept that means the price will care about this point again and again.

3. When you draw a horizontal line as support and resistance check it with this indicator too, if your support and resistance is touched with inverted chart, it will be more important than normal support/ resistance.

4. This indicator has plot candle too, it means you can compare regular chart with the inverted one at same time if you need.

Here is the steps:

1. When you add the indicator to your chart it will add your ticker as inverted.

2. Change your chart type to line chart.

3. Fix your scale in both sides left and right (the indicator's side is on the left).

4. Now you must have two type of line charts, one is yours (The blue one) and one is plotted with this indicator (The purple one).

5. Draw a horizontal line where these two lines have more crossing at the middle of chart, this line will be a powerful line later.

6. Find other more crossed points and draw horizontal line for them too.

7. Now you can see these indicator's support and resistant’s, now you can remove the indicator and watch how the price will touch, reverse, or stay on your new type of support and resistant’s lines.

PS: I have added candle plotting too if you need it.

Hodrick-Prescott Cycle Component (YavuzAkbay)The Hodrick-Prescott Cycle Component indicator in Pine Script™ is an advanced tool that helps traders isolate and analyze the cyclical deviations in asset prices from their underlying trend. This script calculates the cycle component of the price series using the Hodrick-Prescott (HP) filter, allowing traders to observe and interpret the short-term price movements around the long-term trend. By providing two views—Percentage and Price Difference—this indicator gives flexibility in how these cyclical movements are visualized and interpreted.

What This Script Does

This indicator focuses exclusively on the cycle component of the price, which is the deviation of the current price from the long-term trend calculated by the HP filter. This deviation (or "cycle") is what traders analyze for mean-reversion opportunities and overbought/oversold conditions. The script allows users to see this deviation in two ways:

Percentage Difference: Shows the deviation as a percentage of the trend, giving a normalized view of the price’s distance from its trend component.

Price Difference: Shows the deviation in absolute price terms, reflecting how many price units the price is above or below the trend.

How It Works

Trend Component Calculation with the HP Filter: Using the HP filter, the script isolates the trend component of the price. The smoothness of this trend is controlled by the smoothness parameter (λ), which can be adjusted by the user. A higher λ value results in a smoother trend, while a lower λ value makes it more responsive to short-term changes.

Cycle Component Calculation: Percentage Deviation (cycle_pct) calculated as the difference between the current price and the trend, divided by the trend, and then multiplied by 100. This metric shows how far the price deviates from the trend in relative terms. Price Difference (cycle_price) simply the difference between the current price and the trend component, displaying the deviation in absolute price units.

Conditional Plotting: The user can choose to view the cycle component as either a percentage or a price difference by selecting the Display Mode input. The indicator will plot the chosen mode in a separate pane, helping traders focus on the preferred measure of deviation.

How to Use This Indicator

Identify Overbought/Oversold Conditions: When the cycle component deviates significantly from the zero line (shown with a dashed horizontal line), it may indicate overbought or oversold conditions. For instance, a high positive cycle component suggests the price may be overbought relative to the trend, while a large negative cycle suggests potential oversold conditions.

Mean-Reversion Strategy: In mean-reverting markets, traders can use this indicator to spot potential reversal points. For example, if the cycle component shows an extreme deviation from zero, it could signal that the price is likely to revert to the trend. This can help traders with entry and exit points when the asset is expected to correct back toward its trend.

Trend Strength and Cycle Analysis: By comparing the magnitude and duration of deviations, traders can gauge the strength of cycles and assess if a new trend might be forming. If the cycle component remains consistently positive or negative, it may indicate a persistent market bias, even as prices fluctuate around the trend.

Percentage vs. Price Difference Views: Use the Percentage Difference mode to standardize deviations and compare across assets or different timeframes. This is especially helpful when analyzing assets with varying price levels. Use the Price Difference mode when an absolute deviation (price units) is more intuitive for spotting overbought/oversold levels based on the asset’s actual price.

Using with Hodrick-Prescott: You can also use Hodrick-Prescott, another indicator that I have adapted to the Tradingview platform, to see the trend on the chart, and you can also use this indicator to see how far the price is deviating from the trend. This gives you a multifaceted perspective on your trades.

Practical Tips for Traders

Set the Smoothness Parameter (λ): Adjust the λ parameter to match your trading timeframe and asset characteristics. Lower values make the trend more sensitive, which might suit short-term trading, while higher values smooth out the trend for long-term analysis.

Cycle Component as Confirmation: Combine this indicator with other momentum or trend indicators for confirmation of overbought/oversold signals. For example, use the cycle component with RSI or MACD to validate the likelihood of mean-reversion.

Observe Divergences: Divergences between price movements and the cycle component can indicate potential reversals. If the price hits a new high, but the cycle component shows a smaller deviation than previous highs, it could signal a weakening trend.

Weierstrass Function (Fractal Cycles)THE WEIERSTRASS FUNCTION

f(x) = ∑(n=0)^∞ a^n * cos(b^n * π * x)

The Weierstrass Function is the sum of an infinite series of cosine functions, each with increasing frequency and decreasing amplitude. This creates powerful multi-scale oscillations within the range ⬍(-2;+2), resembling a system of self-repetitive patterns. You can zoom into any part of the output and observe similar proportions, mimicking the hidden order behind the irregularity and unpredictability of financial markets.

IT DOESN’T RELY ON ANY MARKET DATA, AS THE OUTPUT IS BASED PURELY ON A MATHEMATICAL FORMULA!

This script does not provide direct buy or sell signals and should be used as a tool for analyzing the market behavior through fractal geometry. The function is often used to model complex, chaotic systems, including natural phenomena and financial markets.

APPLICATIONS:

Timing Aspect: Identifies the phases of market cycles, helping to keep awareness of frequency of turning points

Price-Modeling features: The Amplitude, frequency, and scaling settings allow the indicator to simulate the trends and oscillations. Its nowhere-differentiable nature aligns with the market's inherent uncertainty. The fractured oscillations resemble sharp jumps, noise, and dips found in volatile markets.

SETTINGS

Amplitude Factor (a): Controls the size of each wave. A higher value makes the waves larger.

Frequency Factor (b): Determines how fast the waves oscillate. A higher value creates more frequent waves.

Ability to Invert the output: Just like any cosine function it starts its journey with a decline, which is not distinctive to the behavior of most assets. The default setting is in "inverted mode".

Scale Factor: Adjusts the speed at which the oscillations grow over time.

Number of Terms (n_terms): Increases the number of waves. More terms add complexity to the pattern.

Atlantean Bitcoin Weekly Market Condition - Top/Bottom BTC Overview:

The "Atlantean Bitcoin Weekly Market Condition Detector - Top/Bottom BTC" is a specialized TradingView indicator designed to identify significant turning points in the Bitcoin market on a weekly basis. By analyzing long-term and short-term moving averages across two distinct resolutions, this indicator provides traders with valuable insights into potential market bottoms and tops, as well as the initiation of bull markets.

Key Features:

Market Bottom Detection: The script uses a combination of a simple moving average (SMA) and an exponential moving average (EMA) calculated over long and short periods to identify potential market bottoms. When these conditions are met, the script signals a "Market Bottom" label on the chart, indicating a possible buying opportunity.

Bull Market Start Indicator: When the short-term EMA crosses above the long-term SMA, it signals the beginning of a bull market. This is marked by a "Bull Market Start" label on the chart, helping traders to prepare for potential market upswings.

Market Top Detection: The script identifies potential market tops by analyzing the crossunder of long and short-term moving averages. A "Market Top" label is plotted, suggesting a potential selling point.

Customizable Moving Averages Display: Users can choose to display the moving averages used for detecting market tops and bottoms, providing additional insights into market conditions.

How It Works: The indicator operates by monitoring the interactions between the specified moving averages:

Market Bottom: Detected when the long-term SMA (adjusted by a factor of 0.745) crosses over the short-term EMA.

Bull Market Start: Detected when the short-term EMA crosses above the long-term SMA.

Market Top: Detected when the long-term SMA (adjusted by a factor of 2) crosses under the short-term SMA.

These conditions are highlighted on the chart, allowing traders to visualize significant market events and make informed decisions.

Intended Use: This indicator is best used on weekly Bitcoin charts. It’s designed to provide long-term market insights rather than short-term trading signals. Traders can use this tool to identify strategic entry and exit points during major market cycles. The optional display of moving averages can further enhance understanding of market dynamics.

Originality and Utility: Unlike many other indicators, this script not only highlights traditional market tops and bottoms but also identifies the aggressive start of bull markets, offering a comprehensive view of market conditions. The unique combination of adjusted moving averages makes this script a valuable tool for long-term Bitcoin traders.

Disclaimer: The signals provided by this indicator are based on historical data and mathematical calculations. They do not guarantee future market performance. Traders should use this tool as part of a broader trading strategy and consider other factors before making trading decisions. Not financial advice.

Happy Trading!

By Atlantean

Ehlers Band-Pass FilterHeyo,

This indicator is an original translation from Ehlers' book "Cycle Analytics for Traders Advanced".

First, I describe the indicator as usual and later you can find a very insightful quote of the book.

Key Features

Signal Line: Represents the output of the band-pass filter, highlighting the dominant cycle in the data.

Trigger Line: A leading indicator derived from the signal line, providing early signals for potential market reversals.

Dominant Cycle: Measures the dominant cycle period by counting the number of bars between zero crossings of the band-pass filter output.

Calculation:

The band-pass filter is implemented using a combination of high-pass and low-pass filters.

The filter's parameters, such as period and bandwidth, can be adjusted to tune the filter to specific market cycles.

The signal line is normalized using an Automatic Gain Control (AGC) to provide consistent amplitude regardless of price swings.

The trigger line is derived by applying a high-pass filter to the signal line, creating a leading

waveform.

Usage

The indicator is effective in identifying peaks and valleys in the market data.

It works best in cyclic market conditions and may produce false signals during trending periods.

The dominant cycle measurement helps traders understand the prevailing market cycle length, aiding in better decision-making.

Quoted from the Book

Band-Pass Filters

“A little of the data narrowly passed,” said Tom broadly.

Perhaps the least appreciated and most underutilized filter in technical analysis is the band-pass filter. The band-pass filter simultaneously diminishes the amplitude at low frequencies, qualifying it as a detrender, and diminishes the amplitude at high frequencies, qualifying it as a data smoother.

It passes only those frequency components from input to output in which the trader is interested. The filtering produced by a band-pass filter is superior because the rejection in the stop bands is related to its bandwidth. The degree of rejection of undesired frequency components is called selectivity. The band-stop filter is the dual of the band-pass filter. It rejects a band of frequency components as a notch at the output and passes all other frequency components virtually unattenuated. Since the bandwidth of the deep rejection in the notch is relatively narrow and since the spectrum of market cycles is relatively broad due to systemic noise, the band-stop filter has little application in trading.

Measuring the Cycle Period

The band-pass filter can be used as a relatively simple measurement of the dominant cycle.

A cycle is complete when the waveform crosses zero two times from the last zero crossing. Therefore, each successive zero crossing of the indicator marks a half cycle period. We can establish the dominant cycle period as twice the spacing between successive zero crossings.

When we measure the dominant cycle period this way, it is best to widen the pass band of the band-pass filter to avoid distorting the measurement simply due to the selectivity of the filter. Using an input bandwidth of 0.7 produces an octave-wide pass band. For example, if the center period of the filter is 20 and the relative bandwidth is 0.7, the bandwidth is 14. That means the pass band of the filter extends from 13-bar periods to 27-bar periods.

That is, roughly an octave exists because the longest period is twice the shortest period of the pass band. It is imperative that a high-pass filter is tuned one octave below the half-bandwidth edge of the band-pass filter to ensure a nominal zero mean of the filtered output. Without a zero mean, the zero crossings can have a substantial error.

Since the measurement of the dominant cycle can vary dramatically from zero crossing to zero

crossing, the code limits the change between measurements to be no more than 25 percent.

While measuring the changing dominant cycle period via zero crossings of the band-pass waveform is easy, it is not necessarily the most accurate method.

Best regards,

simwai

Good Luck with your trading! 🙌

Fibonacci Time PeriodsThe " Fibonacci Time Periods " indicator uses power exponents of the constant Phi based on your custom time period to generate Fibonacci sequence-based progression on a given chart. This tool can help to anticipate the timing of potential turning points by highlighting Fib time zones where significant price movements may occur.

It is different from other alternatives specifically for the ability to alter the rate of progression .

Most famous regular Fib sequence expands with 1.618^(n+1) rate which produces vast change just after few iterations.

Those ever-expanding big intervals don't allow us to cover the smaller details of the chart which we might find crucial. So, the idea was born to break down the constant Phi to a self-fraction using power exponents. In other words, reducing rate of progression to make the expansion more gradual without losing properties of Fibonacci proportions.

Default settings have a rate of 0.25 which is basically Phi^1/4

That means we expect 4x more lines than in regular sequence to cover missing bits owing to formula: 1.618^(0.25*(n+1))

(Line 0.618 is added to enhance visual orientation and perception of proportions)

How it works:

Exponential rate of progression

First, it works out the difference between your custom start (0) and end (1) period

The result is multiplied by 1.618^rate to get the step

Rest lines are created by iterations. For instance, with default rate of 0.25, the 1st generated line = start + (End-Start)*1.618^0.25* 1 , second line = start + (End-Start)*1.618^0.25* 2 , etc.

If we change the rate to 1 it will produce the regular fib sequence with 1.618^(n+1) rate

Fixed rate of progression:

In this mode, when rate is 0.25, it grows exactly with exponent step of 0.25 so first, second, third, etc generated lines also have the fixed exponent of 0.25. The distance between lines do not expand.

How to use:

Set the start and end dates

Choose the type of progression

Choose your desired rate of progression

Customize the colors to match your chart preferences.

Observe the generated Fibonacci time intervals and use them to identify potential market movements and reactions.

Intellect_city - Halvings Bitcoin CycleWhat is halving?

The halving timer shows when the next Bitcoin halving will occur, as well as the dates of past halvings. This event occurs every 210,000 blocks, which is approximately every 4 years. Halving reduces the emission reward by half. The original Bitcoin reward was 50 BTC per block found.

Why is halving necessary?

Halving allows you to maintain an algorithmically specified emission level. Anyone can verify that no more than 21 million bitcoins can be issued using this algorithm. Moreover, everyone can see how much was issued earlier, at what speed the emission is happening now, and how many bitcoins remain to be mined in the future. Even a sharp increase or decrease in mining capacity will not significantly affect this process. In this case, during the next difficulty recalculation, which occurs every 2014 blocks, the mining difficulty will be recalculated so that blocks are still found approximately once every ten minutes.

How does halving work in Bitcoin blocks?

The miner who collects the block adds a so-called coinbase transaction. This transaction has no entry, only exit with the receipt of emission coins to your address. If the miner's block wins, then the entire network will consider these coins to have been obtained through legitimate means. The maximum reward size is determined by the algorithm; the miner can specify the maximum reward size for the current period or less. If he puts the reward higher than possible, the network will reject such a block and the miner will not receive anything. After each halving, miners have to halve the reward they assign to themselves, otherwise their blocks will be rejected and will not make it to the main branch of the blockchain.

The impact of halving on the price of Bitcoin

It is believed that with constant demand, a halving of supply should double the value of the asset. In practice, the market knows when the halving will occur and prepares for this event in advance. Typically, the Bitcoin rate begins to rise about six months before the halving, and during the halving itself it does not change much. On average for past periods, the upper peak of the rate can be observed more than a year after the halving. It is almost impossible to predict future periods because, in addition to the reduction in emissions, many other factors influence the exchange rate. For example, major hacks or bankruptcies of crypto companies, the situation on the stock market, manipulation of “whales,” or changes in legislative regulation.

---------------------------------------------

Table - Past and future Bitcoin halvings:

---------------------------------------------

Date: Number of blocks: Award:

0 - 03-01-2009 - 0 block - 50 BTC

1 - 28-11-2012 - 210000 block - 25 BTC

2 - 09-07-2016 - 420000 block - 12.5 BTC

3 - 11-05-2020 - 630000 block - 6.25 BTC

4 - 20-04-2024 - 840000 block - 3.125 BTC

5 - 24-03-2028 - 1050000 block - 1.5625 BTC

6 - 26-02-2032 - 1260000 block - 0.78125 BTC

7 - 30-01-2036 - 1470000 block - 0.390625 BTC

8 - 03-01-2040 - 1680000 block - 0.1953125 BTC

9 - 07-12-2043 - 1890000 block - 0.09765625 BTC

10 - 10-11-2047 - 2100000 block - 0.04882813 BTC

11 - 14-10-2051 - 2310000 block - 0.02441406 BTC

12 - 17-09-2055 - 2520000 block - 0.01220703 BTC

13 - 21-08-2059 - 2730000 block - 0.00610352 BTC

14 - 25-07-2063 - 2940000 block - 0.00305176 BTC

15 - 28-06-2067 - 3150000 block - 0.00152588 BTC

16 - 01-06-2071 - 3360000 block - 0.00076294 BTC

17 - 05-05-2075 - 3570000 block - 0.00038147 BTC

18 - 08-04-2079 - 3780000 block - 0.00019073 BTC

19 - 12-03-2083 - 3990000 block - 0.00009537 BTC

20 - 13-02-2087 - 4200000 block - 0.00004768 BTC

21 - 17-01-2091 - 4410000 block - 0.00002384 BTC

22 - 21-12-2094 - 4620000 block - 0.00001192 BTC

23 - 24-11-2098 - 4830000 block - 0.00000596 BTC

24 - 29-10-2102 - 5040000 block - 0.00000298 BTC

25 - 02-10-2106 - 5250000 block - 0.00000149 BTC

26 - 05-09-2110 - 5460000 block - 0.00000075 BTC

27 - 09-08-2114 - 5670000 block - 0.00000037 BTC

28 - 13-07-2118 - 5880000 block - 0.00000019 BTC

29 - 16-06-2122 - 6090000 block - 0.00000009 BTC

30 - 20-05-2126 - 6300000 block - 0.00000005 BTC

31 - 23-04-2130 - 6510000 block - 0.00000002 BTC

32 - 27-03-2134 - 6720000 block - 0.00000001 BTC

trend_switch

█ Description

Asset price data was time series data, commonly consisting of trends, seasonality, and noise. Many applicable indicators help traders to determine between trend or momentum to make a better trading decision based on their preferences. In some cases, there is little to no clear market direction, and price range. It feels much more appropriate to use a shorter trend identifier, until clearly defined market trend. The indicator/strategy developed with the notion aims to automatically switch between shorter and longer trend following indicator. There were many methods that can be applied and switched between, however in this indicator/strategy will be limited to the use of predictive moving average and MESA adaptive moving average (Ehlers), by first determining if there is a strong trend identified by calculating the slope, if slope value is between upper and lower threshold assumed there is not much price direction.

█ Formula

// predictive moving average

predict = (2*wma1-wma2)

trigger = (4*predict+3*predict +2*predict *predict)

// MESA adaptive moving average

mama = alpha*src+(1-alpha)*mama

fama = .5*alpha*mama+(1-.5-alpha)*fama

█ Feature

The indicator will have a specified default parameter of:

source = ohlc4

lookback period = 10

threshold = 10

fast limit = 0.5

slow limit = 0.05

Strategy type can be switched between Long/Short only and Long-Short strategy

Strategy backtest period

█ How it works

If slope between the upper (red) and lower (green) threshold line, assume there is little to no clear market direction, thus signal predictive moving average indicator

If slope is above the upper (red) or below the lower (green) threshold line, assume there is a clear trend forming, the signal generated from the MESA adaptive moving average indicator

█ Example 1 - Slope fall between the Threshold - activate shorter trend

█ Example 2 - Slope fall above/below Threshold - activate longer trend

Ichimoku Theories [LuxAlgo]The Ichimoku Theories indicator is the most complete Ichimoku tool you will ever need. Four tools combined into one to harness all the power of Ichimoku Kinkō Hyō.

This tool features the following concepts based on the work of Goichi Hosoda:

Ichimoku Kinkō Hyō: Original Ichimoku indicator with its five main lines and kumo.

Time Theory: automatic time cycle identification and forecasting to understand market timing.

Wave Theory: automatic wave identification to understand market structure.

Price Theory: automatic identification of developing N waves and possible price targets to understand future price behavior.

🔶 ICHIMOKU KINKŌ HYŌ

Ichimoku with lines only, Kumo only and both together

Let us start with the basics: the Ichimoku original indicator is a tool to understand the market, not to predict it, it is a trend-following tool, so it is best used in trending markets.

Ichimoku tells us what is happening in the market and what may happen next, the aim of the tool is to provide market understanding, not trading signals.

The tool is based on calculating the mid-point between the high and low of three pre-defined ranges as the equilibrium price for short (9 periods), medium (26 periods), and long (52 periods) time horizons:

Tenkan sen: middle point of the range of the last 9 candles

Kinjun sen: middle point of the range of the last 26 candles

Senkou span A: middle point between Tankan Sen and Kijun Sen, plotted 26 candles into the future

Senkou span B: midpoint of the range of the last 52 candles, plotted 26 candles into the future

Chikou span: closing price plotted 26 candles into the past

Kumo: area between Senkou pans A and B (kumo means cloud in Japanese)

The most basic use of the tool is to use the Kumo as an area of possible support or resistance.

🔶 TIME THEORY

Current cycles and forecast

Time theory is a critical concept used to identify historical and current market cycles, and use these to forecast the next ones. This concept is based on the Kihon Suchi (translating to "Basic Numbers" in Japanese), these are 9 and 26, and from their combinations we obtain the following sequence:

9, 17, 26, 33, 42, 51, 65, 76, 129, 172, 200, 257

The main idea is that the market moves in cycles with periods set by the Kihon Suchi sequence.

When the cycle has the same exact periods, we obtain the Taito Suchi (translating to "Same Number" in Japanese).

This tool allows traders to identify historical and current market cycles and forecast the next one.

🔹 Time Cycle Identification

Presentation of 4 different modes: SWINGS, HIGHS, KINJUN, and WAVES .

The tool draws a horizontal line at the bottom of the chart showing the cycles detected and their size.

The following settings are used:

Time Cycle Mode: up to 7 different modes

Wave Cycle: Which wave to use when WAVE mode is selected, only active waves in the Wave Theory settings will be used.

Show Time Cycles: keep a cleaner chart by disabling cycles visualisation

Show last X time cycles: how many cycles to display

🔹 Time Cycle Forecast

Showcasing the two forecasting patterns: Kihon Suchi and Taito Suchi

The tool plots horizontal lines, a solid anchor line, and several dotted forecast lines.

The following settings are used:

Show time cycle forecast: to keep things clean

Forecast Pattern: comes in two flavors

Kihon Suchi plots a line from the anchor at each number in the Kihon Suchi sequence.

Taito Suchi plot lines from the anchor with the same size detected in the anchored cycle

Anchor forecast on last X time cycle: traders can place the anchor in any detected cycle

🔶 WAVE THEORY

All waves activated with overlapping

The main idea behind this theory is that markets move like waves in the sea, back and forth (making swing lows and highs). Understanding the current market structure is key to having realistic expectations of what the market may do next. The waves are divided into Simple and Complex.

The following settings are used:

Basic Waves: allows traders to activate waves I, V and N

Complex Waves: allows traders to activate waves P, Y and W

Overlapping waves: to avoid missing out on any of the waves activated

Show last X waves: how many waves will be displayed

🔹 Basic Waves

The three basic waves

The basic waves from which all waves are made are I, V, and N

I wave: one leg moves

V wave: two legs move, one against the other

N wave: Three legs move, push, pull back, and another push

🔹 Complex Waves

Three complex waves

There are other waves like

P wave: contracting market

Y wave: expanding market

W wave: double top or double bottom

🔶 PRICE THEORY

All targets for the current N wave with their calculations

This theory is based on identifying developing N waves and predicting potential price targets based on that developing wave.

The tool displays 4 basic targets (V, E, N, and NT) and 3 extended targets (2E and 3E) according to the calculations shown in the chart above. Traders can enable or disable each target in the settings panel.

🔶 USING EVERYTHING TOGETHER

Please DON'T do this. This is not how you use it

Now the real example:

Daily chart of Nasdaq 100 futures (NQ1!) with our Ichimoku analysis

Time, waves, and price theories go together as one:

First, we identify the current time cycles and wave structure.

Then we forecast the next cycle and possible key price levels.

We identify a Taito Suchi with both legs of exactly 41 candles on each I wave, both together forming a V wave, the last two I waves are part of a developing N wave, and the time cycle of the first one is 191 candles. We forecast this cycle into the future and get 22nd April as a key date, so in 6 trading days (as of this writing) the market would have completed another Taito Suchi pattern if a new wave and time cycle starts. As we have a developing N wave we can see the potential price targets, the price is actually between the NT and V targets. We have a bullish Kumo and the price is touching it, if this Kumo provides enough support for the price to go further, the market could reach N or E targets.

So we have identified the cycle and wave, our expectations are that the current cycle is another Taito Suchi and the current wave is an N wave, the first I wave went for 191 candles, and we expect the second and third I waves together to amount to 191 candles, so in theory the N wave would complete in the next 6 trading days making a swing high. If this is indeed the case, the price could reach the V target (it is almost there) or even the N target if the bulls have the necessary strength.

We do not predict the future, we can only aim to understand the current market conditions and have future expectations of when (time), how (wave), and where (price) the market will make the next turning point where one side of the market overcomes the other (bulls vs bears).

To generate this chart, we change the following settings from the default ones:

Swing length: 64

Show lines: disabled

Forecast pattern: TAITO SUCHI

Anchor forecast: 2

Show last time cycles: 5

I WAVE: enabled

N WAVE: disabled

Show last waves: 5

🔶 SETTINGS

Show Swing Highs & Lows: Enable/Disable points on swing highs and swing lows.

Swing Length: Number of candles to confirm a swing high or swing low. A higher number detects larger swings.

🔹 Ichimoku Kinkō Hyō

Show Lines: Enable/Disable the 5 Ichimoku lines: Kijun sen, Tenkan sen, Senkou span A & B and Chikou Span.

Show Kumo: Enable/Disable the Kumo (cloud). The Kumo is formed by 2 lines: Senkou Span A and Senkou Span B.

Tenkan Sen Length: Number of candles for Tenkan Sen calculation.

Kinjun Sen Length: Number of candles for the Kijun Sen calculation.

Senkou Span B Length: Number of candles for Senkou Span B calculation.

Chikou & Senkou Offset: Number of candles for Chikou and Senkou Span calculation. Chikou Span is plotted in the past, and Senkou Span A & B in the future.

🔹 Time Theory

Show Time Cycle Forecast: Enable/Disable time cycle forecast vertical lines. Disable for better performance.

Forecast Pattern: Choose between two patterns: Kihon Suchi (basic numbers) or Taito Suchi (equal numbers).

Anchor forecast on last X time cycle: Number of time cycles in the past to anchor the time cycle forecast. The larger the number, the deeper in the past the anchor will be.

Time Cycle Mode: Choose from 7 time cycle detection modes: Tenkan Sen cross, Kijun Sen cross, Kumo change between bullish & bearish, swing highs only, swing lows only, both swing highs & lows and wave detection.

Wave Cycle: Choose which type of wave to detect from 6 different wave types when the time cycle mode is set to WAVES.

Show Time Cycles: Enable/Disable time cycle horizontal lines. Disable for better performance.

how last X time cycles: Maximum number of time cycles to display.

🔹 Wave Theory

Basic Waves: Enable/Disable the display of basic waves, all at once or one at a time. Disable for better performance.

Complex Waves: Enable/Disable complex wave display, all at once or one by one. Disable for better performance.

Overlapping Waves: Enable/Disable the display of waves ending on the same swing point.

Show last X waves: 'Maximum number of waves to display.

🔹 Price Theory

Basic Targets: Enable/Disable horizontal price target lines. Disable for better performance.

Extended Targets: Enable/Disable extended price target horizontal lines. Disable for better performance.

Advanced MACD [CryptoSea]Advanced MACD (AMACD) enhances the traditional MACD indicator, integrating innovative features for traders aiming for deeper insights into market momentum and sentiment. It's crafted for those seeking to explore nuanced behaviors of the MACD histogram, thus offering a refined perspective on market dynamics.

Divergence moves can offer insight into continuation or potential reversals in structure, the example below is a clear continuation signal.

Key Features

Enhanced Histogram Analysis: Precisely tracks movements of the MACD histogram, identifying growth or decline periods, essential for understanding market momentum.

High/Low Markers: Marks the highest and lowest points of the histogram within a user-defined period, signaling potential shifts in the market.

Dynamic Averages Calculation: Computes average durations of histogram phases, providing a benchmark against historical performance.

Color-Coded Histogram: Dynamically adjusts the histogram's color intensity based on the current streak's duration relative to its average, offering a visual cue of momentum strength.

Customisable MACD Settings: Enables adjustments to MACD parameters, aligning with individual trading strategies.

Interactive Dashboard: Showcases an on-chart table with average durations for each phase, aiding swift decision-making.

Settings & Customisation

MACD Settings: Customise fast length, slow length, and signal smoothing to tailor the MACD calculations to your trading needs.

Reset Period: Determine the number of bars to identify the histogram's significant high and low points.

Histogram High/Lows: Option to display critical high and low levels of the histogram for easy referencing.

Candle Colours: Select between neutral or traditional candle colors to match your analytical preferences.

When in strong trends, you can use the average table to determine when to look to get into a position. This example we are in a strong downtrend, we then see the histogram growing above the average in these conditions which is where we should look to get into a shorting position.

Strategic Applications

The AMACD serves not just as an indicator but as a comprehensive analytical tool for spotting market trends, momentum shifts, and potential reversal points. It's particularly useful for traders to:

Spot Momentum Changes Utilise dynamic coloring and streak tracking to alert shifts in momentum, helping anticipate market movements.

Identify Market Extremes Use high and low markers to spot potential market turning points, aiding in risk management and decision-making.

Alert Conditions

Above Average Movement Alerts: Triggered when the duration of the MACD histogram's growth or decline is unusually long, these alerts signal sustained momentum:

Above Zero: Alerts for both growing and declining movements above zero, indicating either continued bullish trends or potential bearish reversals.

Below Zero: Alerts for growth and decline below zero, pointing to potential bullish reversals or confirmed bearish trends.

High/Low Break Alerts: Activated when the histogram reaches new highs or falls to new lows beyond the set thresholds, these alerts are crucial for identifying shifts in market dynamics:

Break Above Last High: Indicates a potential upward trend as the histogram surpasses recent highs.

Break Below Last Low: Warns of a possible downward trend as the histogram drops below recent lows.

These alert conditions enable traders to automate part of their market monitoring or potential to automate the signals to take action elsewhere.

Global Net Liquidity (TG fork)Worldwide net liquidity, with trend coloring.

Global Net Liquidity attempts to represent worldwide net liquidity, and is defined as: Fed + Japan + China + UK + ECB - RRP - TGA , Where the first five components are central bank assets.

On TradingView, the indicator can be reproduced with the following equations: Global Net Liquidity = FRED:WALCL + FRED:JPNASSETS * FX_IDC:JPYUSD + CNCBBS * FX_IDC:CNYUSD + GBCBBS * FX:GBPUSD + ECBASSETSW * FX:EURUSD + RRPONTSYD + WTREGEN

However, this indicator adds a moving average cloud, and margin coloring, which eases historical trend assessment at a glance.

This indicator can be seen as an alternative representation of the accumulation/distribution indicator (and hence the same terms can be used in this description).

The Moving Average Cloud is simply the filling between the moving average (by default an EMA) and the current value. This feature was inspired by D7R ACC/DIST closed-source indicator, kudos to D7R for making such neat visual indicators.

Usage instructions:

Blue is more likely a phase of accumulation because the current value is above its historical price as defined by the moving average,

red is when this is more likely a phase of distribution.

Yellow is when the difference is below the margin, so we consider it is insignificant and that the trend is undecided. This can be disabled by setting the margin to 0.

While the color indicates if it's more likely an accumulation (blue) or distribution (red) phase or undecided (yellow), the cloud's vertical size allows to assess the strength of this tendency and the horizontal size the momentum, so that the bigger the cloud, the stronger the accumulation (if cloud is blue) or distribution (if cloud is red).

Why is that so? This is because the cloud represents the difference between the current tendency and the moving averaged past one, so a bigger cloud represents a bigger departure from recently observed tendencies. In practice, when there is accumulation, a pump in price can be expected soon, or if it already happened then it means it is indeed supported by volume, whereas if distribution, either a dump is to be expected soon, or if it already happened it means it's supported by volume.

Or maybe not necessarily a dump, but if there is a move upward in price, but the indicator indicates a strong distribution, then it means that the price movement is not supported and may not be sustainable (reversal may happen at anytime), whereas if price is going upward AND there is an accumulation (blue coloring) then it is more sustainable. This can be used to adapt strategies accordingly (risk on/risk off depending on whether there is concordance of both price and accumulation/distribution).

This indicator also includes sentiment signals that can be used to trigger alarms.

This indicator is a remix of Dharmatech's, who authored the first this Global Net Liquidity equation, kudos to them! Please show them some love if you like this indicator!

Sequencer [LuxAlgo]The Sequencer indicator is a tool that is able to highlight sequences of prices based on their relative position to past prices, which allows a high degree of customization from the user.

Two phases are included in this script, a "Preparation" phase and a "Lead-Up" phase, each with a customizable amount of steps, as well as other characteristics.

Users can also highlight the last step leading to each phase completion with a level, this level can eventually be used as a key price point.

🔶 USAGE

The script highlights two phases, each being based on a sequence of events requiring prices to be higher/lower than prices various bars ago.

The completion of the preparation phase will lead to the evaluation of the lead-up phase, however, it isn't uncommon to see a reversal occurring after the completion of a preparation phase. In the script, bullish preparations are highlighted in green, while bearish preparations are highlighted in red.

Completion of a "Lead-Up" phase is indicative of a potential reversal, with a bullish reversal for the completion of a bullish lead-up (in blue), and a bearish reversal for the completion of a bearish lead-up (in orange).

Using a higher length for the preparation/lead-up phases can allow the detection of longer-term reversals.

Users wishing to display levels based on specific phases completion can do so from the settings in the "Preparation/Lead-Up Completion Levels" settings group.

The "Show Last" settings determine the amount of respective levels to display on the chart.

🔶 PREPARATION PHASE

The "Preparation" phase precedes the "Lead-Up" phase. The completion of this phase requires N successive prices to be lower than the closing price P bars ago for a bullish phase, and for prices to be higher than the closing price P bars ago for a bearish phase, where N is the user set "Preparation Phase Length" and P the user set "Comparison Period".

🔹 Refined Preparations

Sequences of the preparation phase can either be "Standard" or "Refined". Unlike the standard preparation previously described a refined preparation requires the low prices from the user-specified steps in "Refined Preparation Steps" to be above the low price of the last step for a bullish preparation phase, and for the high prices specified in the refined preparation steps to be below the high price of the last step for a bearish preparation phase.

🔶 LEAD-UP PHASE

The "Lead-Up" phase is initiated by the completion of the "Preparation" phase.

Completion of this phase requires the price to be lower than the low price P bars ago N times for a bullish phase, and for prices to be higher than the high price P bars ago N times for a bearish phase, where N is the user set "Lead-Up Phase Length" and P the user set "Comparison Period".

Unlike with the "Preparation" phase these conditions don't need to be successive for them to be valid and can occur at any time.

🔹 Lead-Up Cancellation

Incomplete "Lead-Up" phases can be canceled and removed from the chart once a preparation of the opposite sentiment is completed, avoiding lead-ups to be evaluated after completion of complete preparations.

This can be disabled by toggling off "Apply Cancellation".

🔹 Lead-Up Suspension

Like with refined preparations, we can require specific steps from the lead-up phase to be higher/lower than the price on the last step. This can be particularly important since we do not require lead-up steps to be successive.

For a bullish lead-up, the low of the last step must be lower than the minimum closing prices of the user-specified steps for it to be valid, while for a bearish lead-up, the high of the last step must be higher than the maximum closing prices of the user-specified steps for it to be valid.

This effectively allows for eliminating lead-up phases getting completed on opposite trends.

🔶 SETTINGS

🔹 Preparation Phase

Preparation Phase Length: Length of the "Preparation" phase.

Comparison Period: Offset used to compare current prices to past ones.

Preparation Type: Type of preparation to evaluate, options include "Standard" or "Refined"

Refined Preparations Steps: Steps to evaluate when preparation type is "Refined"

🔹 Lead-Up Phase

Lead-Up Phase Length: Length of the "Lead-Up" phase.

Comparison Period: Offset used to compare current prices to past ones.

Suspension: Applies suspension rule to evaluate lead-up completion.

Suspension Steps: Specifies the steps evaluated to determine if the lead-up referral is respected. Multiple steps are supported and should be comma-separated.

Apply Cancellation: Cancellation will remove any incomplete lead-up upon the completion of a new preparation phase of the opposite sentiment.

🔹 Levels

Bullish Preparations Levels: When enabled display price levels from completed bullish preparations.

Show Last: Number of most recent bullish preparations levels to display.

Bearish Preparations Levels: When enabled display price levels from completed bearish preparations.

Show Last: Number of most recent bearish preparations levels to display.

Central Banks Balance Sheets ROI% ChangeIntroducing the "Central Banks Balance Sheets ROI% Change" indicator, a tool designed to offer traders and analysts an understanding of global liquidity dynamics.

This indicator tracks the Return on Investment (ROI) percentage changes across major central banks' balance sheets, providing insights into shifts in global economic liquidity not tied to cumulative figures but through ROI calculations, capturing the pulse of overall economic dynamics.

Key Enhancements:

ROI Period Customization: Users can now adjust the ROI calculation period, offering flexibility to analyze short-term fluctuations or longer-term trends in central bank activities, aligning with their strategic time horizons.

Chart Offset Feature: This new functionality allows traders to shift the chart view, aiding in the alignment of data visualization with other indicators or specific analysis needs, enhancing interpretive clarity.

Central Bank Selection: With options to include or exclude data from specific central banks among the world's top 15 economies (with the exception of Mexico and the consolidation of the EU's central bank data), traders can tailor the analysis to their regional focus or diversification strategies.

US M2 Option: Recognizing the significance of the M2 money supply as a liquidity metric, this indicator offers an alternative view focusing solely on the US M2, allowing for a concentrated analysis of the US liquidity environment.

Comprehensive Coverage: The tool covers a wide array of central banks, including the Federal Reserve, People's Bank of China, European Central Bank, and more, ensuring a broad and inclusive perspective on global liquidity.

Visualization Enhancements: A histogram plot vividly distinguishes between positive and negative ROI changes, offering an intuitive grasp of liquidity expansions or contractions at a glance.

This indicator is a strategic tool designed for traders who seek to understand the undercurrents of market liquidity and its implications on global markets.

Whether you're assessing the impact of central bank policies, gauging economic health, or identifying investment opportunities, the "Central Banks Balance Sheets ROI% Change" indicator offers a critical lens through which to view the complex interplay of global liquidity factors.

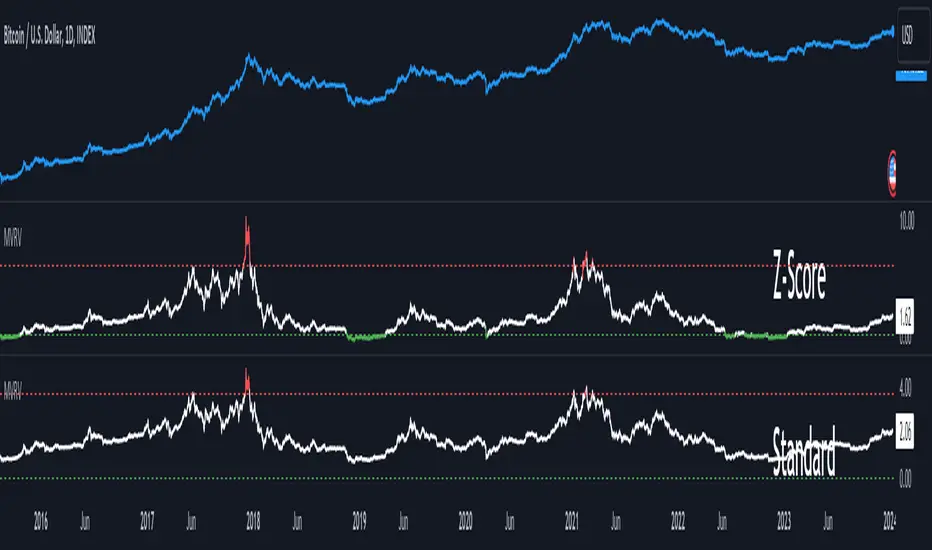

MVRV Z-ScoreThe MVRV ratio was created by Murad Mahmudov & David Puell. It simply compares Market Cap to Realised Cap, presenting a ratio (MVRV = Market Cap / Realised Cap). The MVRV Z-Score is a later version, refining the metric by normalising the peaks and troughs of the data.

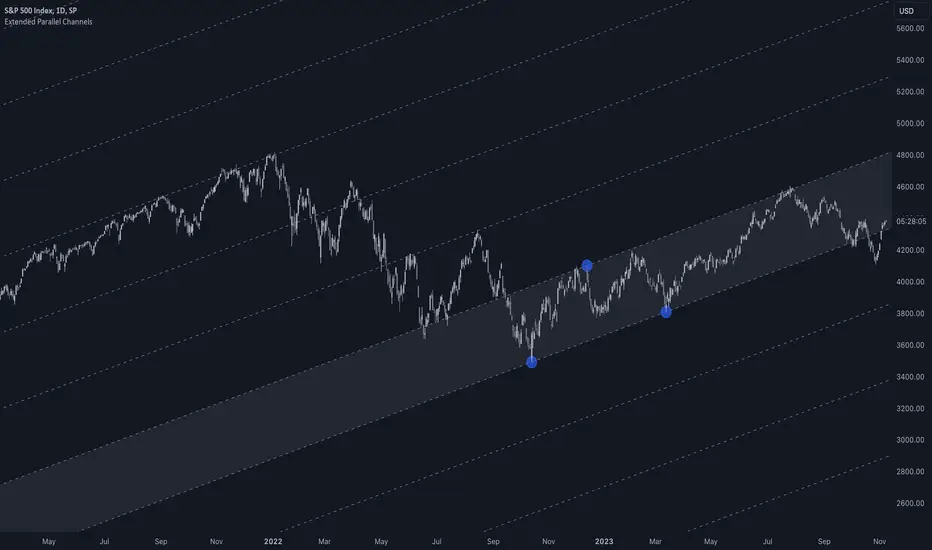

Extended Parallel ChannelsThis indicator provides an enhanced version of the popular Parallel Channel tool by allowing channel boundaries to be extended above and below the primary channel. It can also serve as a general tool for drawing parallel lines and grid lines to aid technical analysis.

🟠 Application

There are two primary ways extended channels can provide valuable insights:

🔵 Support and Resistance Levels

When prices break out of a channel, they often encounter strong resistance at approximately the 100% extension point. Breakout traders can utilize the extended channel boundary to place take-profit orders. Meanwhile, reversal traders can look for entry opportunities at this level.

🔵 Grid / Martingale Trading

Grid Trading and Martingale Trading strategies rely heavily on grid lines. This indicator streamlines that process by enabling traders to effortlessly plot grid lines across the chart.

🟠 Instructions

Upon adding the indicator, the user will be prompted to set the channel boundaries by placing three anchor points on the chart. The first two anchors determine one boundary line, while the third anchor determine the other boundary line.

Once the three anchors are positioned, the indicator automatically plots the resulting channel as well as the extended lines. The anchor points are highlighted as movable blue circles, allowing the user to dynamically adjust the channel formation by dragging the anchors to new locations as needed.

Market Time Cycle (Expo)█ Time Cycles Overview

Time cycles are a fascinating and powerful concept in the world of trading and investing. They are all about understanding and predicting the timing of market moves based on the premise that market events and price movements are not random, but instead occur in repeatable, cyclical patterns.

The Concept of Time Cycles: The foundation of time cycles lies in the belief that historical market patterns tend to repeat themselves over specific periods. These periods or cycles could be influenced by a myriad of factors like economic data releases, earnings reports, geopolitical events, or even natural human behavior. For example, some traders observe increased market activity around the start and end of a trading day, which is a form of intraday time cycle.

Understanding time cycles can provide traders with a roadmap, helping them anticipate potential trend shifts and make more informed decisions about when to buy or sell.

█ Indicator Overview

The Market Time Cycle (Expo) is designed to help traders track and analyze market cycles and generate signals for potential trading opportunities. It uses mathematical techniques to analyze market cycles and detect possible turning points. It does this by projecting the estimated cycle timeline and providing visual indications of cyclical phases through the use of color-coded lines and sine wave cycles.

Time cycles offer a compelling way to forecast market trends and time your trades better. By adding time cycles to your trading toolbox, you could potentially gain a new perspective on market movements and refine your trading strategy further. The indicator generates trading signals based on the sine wave's behavior. When the sine wave crosses certain thresholds, the indicator generates a signal suggesting a potential trading opportunity based on cycle behavior.

█ How to use

This indicator can be a valuable tool to help traders understand and predict market trends and time their trades more accurately. By visualizing the cyclic nature of markets, traders can better anticipate potential turning points and adjust their trading strategies accordingly. It helps traders to spot ideal entry and exit points based on the cyclical nature of financial markets.

█ Settings

You can customize the number of bars (NumbOfBars) that are taken into consideration for the cycle. Including a higher number of bars will provide more data, which can be helpful for analyzing long-term trends.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Fierytrading: Volatility DepthDear Tradingview community,

I'd like to share one of my staple indicators with you. The volatility depth indicator calculates the volatility over a 7-day period and plots it on your chart.

This indicator only works for the DAILY chart on BTC/USD.

Colors

I've color coded the indicator as follows:

- Red: Extreme Volatility

- Orange: High Volatility

- Yellow: Normal Volatility

- Green: Low Volatility

Red: extreme changes in price. Often during local tops and bottoms.

Orange: higher than average moves in price. Often before or after a "red" period. Often seen in the middle of bear or bull markets.

Yellow: normal price action. Often seen during early stage bull-markets and late stage bear-markets.

Green: very low price movement. Often during times of indecision. Once this indicator becomes green, you can expect a big move in either direction. Low volatility is always followed by high volatility.

In a long-term uptrend, a green period often signals a bullish break out. In a long-term downtrend it often signals a bearish break out.

How to use

Save the indicator and apply it to your chart. You can change the length in the settings, but it's optimized for 7 days, so no need to change it.

I've build in alerts for all 4 different volatility periods. In most cases, the low volatility alert is enough.

Good luck!

Market Cycle IndicatorThe Market Cycle Indicator is a tool that integrates the elements of RSI, Stochastic RSI, and Donchian Channels. It is designed to detect market cycles, enabling traders to enter and exit the market at the most opportune times.

This indicator provides a unique perspective on the market, combining multiple strategies into one unified and weighted approach. By factoring in the inputs from each of these popular technical analysis methods, it offers a more holistic view of the market trends and cycles.

Parameter Details:

Donchian Channels (DCO):

- donchianPeriod: Sets the period for the Donchian Channel calculation. Default is set to 14.

- donchianSmoothing: Sets the smoothing factor for the Donchian Channel calculation. Default is set to 3.

- donchianPrice: Selects the price type to be used in the Donchian Channel calculation. Default is set to the closing price.

Relative Strength Index (RSI):

- rsiPeriod: Sets the period for the RSI calculation. Default is set to 14.

- rsiSmoothing: Sets the smoothing factor for the RSI calculation. Default is set to 3.

- rsiPrice: Selects the price type to be used in the RSI calculation. Default is set to the closing price.

Stochastic RSI (StochRSI):

- srsiPeriod: Sets the period for the Stochastic RSI calculation. Default is set to 20.

- srsiSmoothing: Sets the smoothing factor for the Stochastic RSI calculation. Default is set to 3.

- srsiK: Sets the period for the %K line in the Stochastic RSI calculation. Default is set to 5.

- srsiD: Sets the period for the %D line in the Stochastic RSI calculation. Default is set to 5.

- srsiPrice: Selects the price type to be used in the Stochastic RSI calculation. Default is set to the closing price.

Weights:

- rsiWeight: Sets the weight for the RSI in the final aggregate calculation. Default is set to 1.

- srsiWeight: Sets the weight for the Stochastic RSI in the final aggregate calculation. Default is set to 1.

- dcoWeight: Sets the weight for the Donchian Channel in the final aggregate calculation. Default is set to 1.

Limits:

- limitHigh: Sets the upper limit for the indicator. Default is set to 80.

- limitLow: Sets the lower limit for the indicator. Default is set to 20.

By customizing these parameters, users can tweak the indicator to align with their own trading strategies and risk tolerance levels. Whether you're a novice or an experienced trader, the Comprehensive Market Cycle Indicator provides valuable insights into the market's behavior.

Uses library HelperTA

Benner-Fibonacci Reversal Points [CC]This is an original script based on a very old idea called the Benner Theory from the Civil War times. Benner discovered a pattern in pig iron prices (no clue what those are), and this turned out to be a parallel idea to indicators based on Fibonacci numbers. Because a year is 365 days (nearly 377, which is a Fibonacci number), made up of 52 weeks (nearly 55, which is another Fibonacci number), or 12 months (nearly 13, which is another Fibonacci number), Benner theorized that he could find both past and future turning points in the market by using a pattern he found. He discovered that peaks in prices seemed to follow a pattern of 8-9-10, meaning that after a recent peak, it would be 8 bars until the next peak, 9 bars until after that peak for the next, and 10 bars until the following peak. For past peaks, he would just need to reverse this pattern, and so the previous peak would be 10 bars before the most current peak, 9 bars before that peak, and 8 bars before the previous one, and these patterns seemed to repeat. For troughs, he found a pattern of 16,18,20 which follows the same logic, and this idea also seemed to work on long-term peaks and troughs as well.

This is my version of the Benner theory and the major difference between my version and his is that he would manually select a year or date and either work backwards or forwards from that point. I chose to go with an adaptive version that will automatically detect those points and plot those past and future points. I have included several options such as allowing the algorithm to be calculated in reverse which seems to work well for Crypto for some reason. I also have both short and long term options to only show one or both if you choose and of course the option to enable repainting or leave it disabled.

Big thanks to @HeWhoMustNotBeNamed and @RicardoSantos for helping me fix some bugs in my code and for @kerpiciwuasile for suggesting this idea in the first place.

Simple Moving Average Slope [AstrideUnicorn]The Simple Moving Average Slope indicator (SMAS) is a technical analysis tool designed to help traders detect the direction and strength of the current trend in the price of an asset. It is also a great tool for identifying sideways markets. The indicator plots the slope of a simple moving average (SMA) of the closing prices over a specified time period. The slope is normalized by dividing it by the standard deviation of the slope over a longer time period.

HOW TO USE

Traders can use the Simple Moving Average Slope indicator in various ways. One common way is to look for bullish or bearish signals. A bullish signal occurs when the normalized slope rises above a predetermined threshold, resulting in the indicator turning green, indicating an upward trend in the market. Conversely, a bearish signal is generated when the normalized slope falls below the negative value of the threshold, causing the indicator to turn red, signaling a downtrend in the market. When the normalized slope falls between the positive and negative threshold values, a neutral signal is generated, indicating that the market is moving sideways. This can help traders avoid false trend signals from other indicators and strategies that may occur when the market is in a sideways regime. Additionally, traders can use the Simple Moving Average Slope indicator in conjunction with other technical indicators to confirm the trend direction.

SETTINGS

Window - specifies the number of bars used to calculate the SMA slope. The default value is 20.

Threshold - specifies the threshold value used to generate the bullish and bearish signals. The default value is 0.6. Traders can adjust these settings based on their trading strategy and the asset being analyzed.

Fed Projected Interest RatesThis script shows you the current interest rates by the FED (see ZQ symbol nearest expiration)

and the next expirations (see ZQ further expiration dates).

It is important to keep your expiration and descriptions up to date, to do that to the indicator inputs and change as you please.