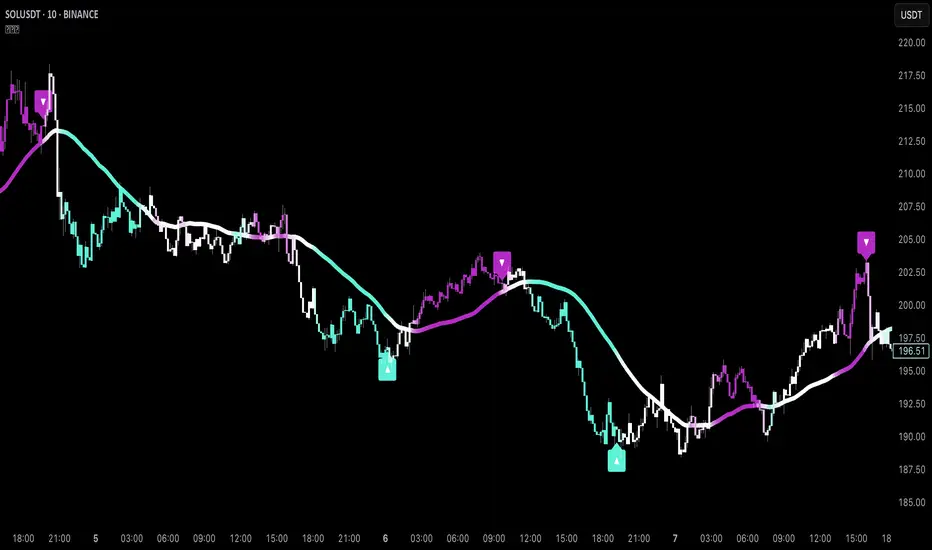

Smart Liquidity Wave [The_lurker]"Smart Liquidity Wave" هو مؤشر تحليلي متطور يهدف لتحديد نقاط الدخول والخروج المثلى بناءً على تحليل السيولة، قوة الاتجاه، وإشارات السوق المفلترة. يتميز المؤشر بقدرته على تصنيف الأدوات المالية إلى أربع فئات سيولة (ضعيفة، متوسطة، عالية، عالية جدًا)، مع تطبيق شروط مخصصة لكل فئة تعتمد على تحليل الموجات السعرية، الفلاتر المتعددة، ومؤشر ADX.

فكرة المؤشر

الفكرة الأساسية هي الجمع بين قياس السيولة اليومية الثابتة وتحليل ديناميكي للسعر باستخدام فلاتر متقدمة لتوليد إشارات دقيقة. المؤشر يركز على تصفية الضوضاء في السوق من خلال طبقات متعددة من التحليل، مما يجعله أداة ذكية تتكيف مع الأدوات المالية المختلفة بناءً على مستوى سيولتها.

طريقة عمل المؤشر

1- قياس السيولة:

يتم حساب السيولة باستخدام متوسط حجم التداول على مدى 14 يومًا مضروبًا في سعر الإغلاق، ويتم ذلك دائمًا على الإطار الزمني اليومي لضمان ثبات القيمة بغض النظر عن الإطار الزمني المستخدم في الرسم البياني.

يتم تصنيف السيولة إلى:

ضعيفة: أقل من 5 ملايين (قابل للتعديل).

متوسطة: من 5 إلى 20 مليون.

عالية: من 20 إلى 50 مليون.

عالية جدًا: أكثر من 50 مليون.

هذا الثبات في القياس يضمن أن تصنيف السيولة لا يتغير مع تغير الإطار الزمني، مما يوفر أساسًا موثوقًا للإشارات.

2- تحليل الموجات السعرية:

يعتمد المؤشر على تحليل الموجات باستخدام متوسطات متحركة متعددة الأنواع (مثل SMA، EMA، WMA، HMA، وغيرها) يمكن للمستخدم اختيارها وتخصيص فتراتها ، يتم دمج هذا التحليل مع مؤشرات إضافية مثل RSI (مؤشر القوة النسبية) وMFI (مؤشر تدفق الأموال) بوزن محدد (40% للموجات، 30% لكل من RSI وMFI) للحصول على تقييم شامل للاتجاه.

3- الفلاتر وطريقة عملها:

المؤشر يستخدم نظام فلاتر متعدد الطبقات لتصفية الإشارات وتقليل الضوضاء، وهي من أبرز الجوانب المخفية التي تعزز دقته:

الفلتر الرئيسي (Main Filter):

يعمل على تنعيم التغيرات السعرية السريعة باستخدام معادلة رياضية تعتمد على تحليل الإشارات (Signal Processing).

يتم تطبيقه على السعر لاستخراج الاتجاهات الأساسية بعيدًا عن التقلبات العشوائية، مع فترة زمنية قابلة للتعديل (افتراضي: 30).

يستخدم تقنية مشابهة للفلاتر عالية التردد (High-Pass Filter) للتركيز على الحركات الكبيرة.

الفلتر الفرعي (Sub Filter):

يعمل كطبقة ثانية للتصفية، مع فترة أقصر (افتراضي: 12)، لضبط الإشارات بدقة أكبر.

يستخدم معادلات تعتمد على الترددات المنخفضة للتأكد من أن الإشارات الناتجة تعكس تغيرات حقيقية وليست مجرد ضوضاء.

إشارة الزناد (Signal Trigger):

يتم تطبيق متوسط متحرك على نتائج الفلتر الرئيسي لتوليد خط إشارة (Signal Line) يُقارن مع عتبات محددة للدخول والخروج.

يمكن تعديل فترة الزناد (افتراضي: 3 للدخول، 5 للخروج) لتسريع أو تبطيء الإشارات.

الفلتر المربع (Square Filter):

خاصية مخفية تُفعّل افتراضيًا تعزز دقة الفلاتر عن طريق تضييق نطاق التذبذبات المسموح بها، مما يقلل من الإشارات العشوائية في الأسواق المتقلبة.

4- تصفية الإشارات باستخدام ADX:

يتم استخدام مؤشر ADX كفلتر نهائي للتأكد من قوة الاتجاه قبل إصدار الإشارة:

ضعيفة ومتوسطة: دخول عندما يكون ADX فوق 40، خروج فوق 50.

عالية: دخول فوق 40، خروج فوق 55.

عالية جدًا: دخول فوق 35، خروج فوق 38.

هذه العتبات قابلة للتعديل، مما يسمح بتكييف المؤشر مع استراتيجيات مختلفة.

5- توليد الإشارات:

الدخول: يتم إصدار إشارة شراء عندما تنخفض خطوط الإشارة إلى ما دون عتبة محددة (مثل -9) مع تحقق شروط الفلاتر، السيولة، وADX.

الخروج: يتم إصدار إشارة بيع عندما ترتفع الخطوط فوق عتبة (مثل 109 أو 106 حسب الفئة) مع تحقق الشروط الأخرى.

تُعرض الإشارات بألوان مميزة (أزرق للدخول، برتقالي للضعيفة والمتوسطة، أحمر للعالية والعالية جدًا) وبثلاثة أحجام (صغير، متوسط، كبير).

6- عرض النتائج:

يظهر مستوى السيولة الحالي في جدول في أعلى يمين الرسم البياني، مما يتيح للمستخدم معرفة فئة الأصل بسهولة.

7- دعم التنبيهات:

تنبيهات فورية لكل فئة سيولة، مما يسهل التداول الآلي أو اليدوي.

%%%%% الجوانب المخفية في الكود %%%%%

معادلات الفلاتر المتقدمة: يستخدم المؤشر معادلات رياضية معقدة مستوحاة من معالجة الإشارات لتنعيم البيانات واستخراج الاتجاهات، مما يجعله أكثر دقة من المؤشرات التقليدية.

التكيف التلقائي: النظام يضبط نفسه داخليًا بناءً على التغيرات في السعر والحجم، مع عوامل تصحيح مخفية (مثل معامل التنعيم في الفلاتر) للحفاظ على الاستقرار.

التوزيع الموزون: الدمج بين الموجات، RSI، وMFI يتم بأوزان محددة (40%، 30%، 30%) لضمان توازن التحليل، وهي تفاصيل غير ظاهرة مباشرة للمستخدم لكنها تؤثر على النتائج.

الفلتر المربع: خيار مخفي يتم تفعيله افتراضيًا لتضييق نطاق الإشارات، مما يقلل من التشتت في الأسواق ذات التقلبات العالية.

مميزات المؤشر

1- فلاتر متعددة الطبقات: تضمن تصفية الضوضاء وإنتاج إشارات موثوقة فقط.

2- ثبات السيولة: قياس السيولة اليومي يجعل التصنيف متسقًا عبر الإطارات الزمنية.

3- تخصيص شامل: يمكن تعديل حدود السيولة، عتبات ADX، فترات الفلاتر، وأنواع المتوسطات المتحركة.

4- إشارات مرئية واضحة: تصميم بصري يسهل التفسير مع تنبيهات فورية.

5- تقليل الإشارات الخاطئة: الجمع بين الفلاتر وADX يعزز الدقة ويقلل من التشتت.

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView.

#### **What is the Smart Liquidity Wave Indicator?**

"Smart Liquidity Wave" is an advanced analytical indicator designed to identify optimal entry and exit points based on liquidity analysis, trend strength, and filtered market signals. It stands out with its ability to categorize financial instruments into four liquidity levels (Weak, Medium, High, Very High), applying customized conditions for each category based on price wave analysis, multi-layered filters, and the ADX (Average Directional Index).

#### **Concept of the Indicator**

The core idea is to combine a stable daily liquidity measurement with dynamic price analysis using sophisticated filters to generate precise signals. The indicator focuses on eliminating market noise through multiple analytical layers, making it an intelligent tool that adapts to various financial instruments based on their liquidity levels.

#### **How the Indicator Works**

1. **Liquidity Measurement:**

- Liquidity is calculated using the 14-day average trading volume multiplied by the closing price, always based on the daily timeframe to ensure value consistency regardless of the chart’s timeframe.

- Liquidity is classified as:

- **Weak:** Less than 5 million (adjustable).

- **Medium:** 5 to 20 million.

- **High:** 20 to 50 million.

- **Very High:** Over 50 million.

- This consistency in measurement ensures that liquidity classification remains unchanged across different timeframes, providing a reliable foundation for signals.

2. **Price Wave Analysis:**

- The indicator relies on wave analysis using various types of moving averages (e.g., SMA, EMA, WMA, HMA, etc.), which users can select and customize in terms of periods.

- This analysis is integrated with additional indicators like RSI (Relative Strength Index) and MFI (Money Flow Index), weighted specifically (40% waves, 30% RSI, 30% MFI) to provide a comprehensive trend assessment.

3. **Filters and Their Functionality:**

- The indicator employs a multi-layered filtering system to refine signals and reduce noise, a key hidden feature that enhances its accuracy:

- **Main Filter:**

- Smooths rapid price fluctuations using a mathematical equation rooted in signal processing techniques.

- Applied to price data to extract core trends away from random volatility, with an adjustable period (default: 30).

- Utilizes a technique similar to high-pass filters to focus on significant movements.

- **Sub Filter:**

- Acts as a secondary filtering layer with a shorter period (default: 12) for finer signal tuning.

- Employs low-frequency-based equations to ensure resulting signals reflect genuine changes rather than mere noise.

- **Signal Trigger:**

- Applies a moving average to the main filter’s output to generate a signal line, compared against predefined entry and exit thresholds.

- Trigger period is adjustable (default: 3 for entry, 5 for exit) to speed up or slow down signals.

- **Square Filter:**

- A hidden feature activated by default, enhancing filter precision by narrowing the range of permissible oscillations, reducing random signals in volatile markets.

4. **Signal Filtering with ADX:**

- ADX is used as a final filter to confirm trend strength before issuing signals:

- **Weak and Medium:** Entry when ADX exceeds 40, exit above 50.

- **High:** Entry above 40, exit above 55.

- **Very High:** Entry above 35, exit above 38.

- These thresholds are adjustable, allowing the indicator to adapt to different trading strategies.

5. **Signal Generation:**

- **Entry:** A buy signal is triggered when signal lines drop below a specific threshold (e.g., -9) and conditions for filters, liquidity, and ADX are met.

- **Exit:** A sell signal is issued when signal lines rise above a threshold (e.g., 109 or 106, depending on the category) with all conditions satisfied.

- Signals are displayed in distinct colors (blue for entry, orange for Weak/Medium, red for High/Very High) and three sizes (small, medium, large).

6. **Result Display:**

- The current liquidity level is shown in a table at the top-right of the chart, enabling users to easily identify the asset’s category.

7. **Alert Support:**

- Instant alerts are provided for each liquidity category, facilitating both automated and manual trading.

#### **Hidden Aspects in the Code**

- **Advanced Filter Equations:** The indicator uses complex mathematical formulas inspired by signal processing to smooth data and extract trends, making it more precise than traditional indicators.

- **Automatic Adaptation:** The system internally adjusts based on price and volume changes, with hidden correction factors (e.g., smoothing coefficients in filters) to maintain stability.

- **Weighted Distribution:** The integration of waves, RSI, and MFI uses fixed weights (40%, 30%, 30%) for balanced analysis, a detail not directly visible but impactful on results.

- **Square Filter:** A hidden option, enabled by default, narrows signal range to minimize dispersion in high-volatility markets.

#### **Indicator Features**

1. **Multi-Layered Filters:** Ensures noise reduction and delivers only reliable signals.

2. **Liquidity Stability:** Daily liquidity measurement keeps classification consistent across timeframes.

3. **Comprehensive Customization:** Allows adjustments to liquidity thresholds, ADX levels, filter periods, and moving average types.

4. **Clear Visual Signals:** User-friendly design with easy-to-read visuals and instant alerts.

5. **Reduced False Signals:** Combining filters and ADX enhances accuracy and minimizes clutter.

#### **Disclaimer**

The information and publications are not intended to be, nor do they constitute, financial, investment, trading, or other types of advice or recommendations provided or endorsed by TradingView.

Osilator Terpusat / Centered Oscillators

Session Profile AnalyzerWhat’s This Thing Do?

Hey there, trader! Meet the Session Profile Analyzer (SPA) your new go-to pal for breaking down market action within your favorite trading sessions. It’s an overlay indicator that mixes Rotation Factor (RF), Average Subperiod Range (ASPR), Volume Value Area Range (VOLVAR), and TPO Value Area Range (TPOVAR) into one tidy little toolkit. Think of it as your market vibe checker momentum, volatility, and key levels, all served up with a grin.

The Cool Stuff It Does:

Rotation Factor (RF) : Keeps tabs on whether the market’s feeling bullish, bearish, or just chilling. It’s like a mood ring for price action shows “UP ↑,” “DOWN ↓,” or “NONE ↔.”

ASPR : Averages out the range of your chosen blocks. Big swings? Tiny wiggles? This tells you the session’s energy level.

VOLVAR : Dives into volume to find where the action’s at, with a smart twist it adjusts price levels based on the session’s size and tiny timeframe moves (capped at 128 so your chart doesn’t cry).

TPOVAR : Grabs lower timeframe data to spot where price hung out the most, TPO-style. Value zones, anyone?

Dynamic Precision : No ugly decimal overload SPA matches your asset’s style (2 decimals for BTC, 5 for TRX, you get it).

How to Play With It:

Session Start/End : Pick your trading window (say, 0930-2200) and a timezone (America/New_York, or wherever you’re at).

Block Size : Set the chunk size for RF and ASPR like 30M if you’re into half-hour vibes.

Value Area Timeframe : Go micro with something like 1S for VOLVAR and TPOVAR precision.

Label : Size it (small to huge), color it (white, neon pink, whatever), and slap it where you want (start, mid, end).

How It All Works (No PhD Required):

RF : Imagine breaking your session into blocks (via Block Size). For each block, SPA checks if the high beats the last high (+1) or not (0), and if the low dips below the last low (-1) or not (0). Add those up, and boom positive RF means upward vibes, negative means downward, near zero is “meh.” Use it to catch trends or spot when the market’s napping.

ASPR : Takes those same blocks, measures high-to-low range each time, and averages them. It’s your volatility pulse big ASPR = wild ride, small ASPR = snooze fest. Great for sizing up session action.

VOLVAR : Here’s the fun part. It takes the session’s full range (high minus low), divides it by the average range of your tiny Value Area Timeframe bars (e.g., 1S), and picks a sensible number of price levels capped at 128 so it doesn’t overthink. Then it bins volume into those levels, finds the busiest price (POC), and grows a 70% value area around it. Perfect for spotting where the big players parked their cash.

TPOVAR : Grabs midpoints from those tiny timeframe bars, sorts them, and snips off the top and bottom 15% to find the 70% “value zone” where price chilled the most. Think of it as the market’s comfort zone great for support/resistance hunting.

Why You’ll Like It:

Whether you’re scalping crypto, swinging forex, or dissecting stocks, SPA’s got your back. Use RF to catch momentum shifts like jumping on an “UP ↑” trend or fading a “DOWN ↓” exhaustion. ASPR’s your secret weapon for sizing up trades: a big ASPR (say, 100 on BTC) means you can aim for juicy targets (like 1-2x ASPR) or set invalidations tight when it’s tiny (e.g., 0.001 on TRX) to dodge chop. VOLVAR and TPOVAR are your level-finders nail those key zones where price loves to bounce or break, perfect for entries, stops, or profit grabs. It’s like having a trading co-pilot who’s chill but knows their stuff.

Heads-Up:

Load enough history for those micro timeframes to shine (1S needs some bars to work with).

Keeps things light won’t bog down your chart even with decent-sized sessions.

Let’s Roll:

Slap SPA on your chart, tweak it to your style, and watch it spill the beans on your session. Happy trading, fam may your pips be plenty and your losses few!

Schaff Trend Cycle (STC)The STC (Schaff Trend Cycle) indicator is a momentum oscillator that combines elements of MACD and stochastic indicators to identify market cycles and potential trend reversals.

Key features of the STC indicator:

Oscillates between 0 and 100, similar to a stochastic oscillator

Values above 75 generally indicate overbought conditions

Values below 25 generally indicate oversold conditions

Signal line crossovers (above 75 or below 25) can suggest potential entry/exit points

Faster and more responsive than traditional MACD

Designed to filter out market noise and identify cyclical trends

Traders typically use the STC indicator to:

Identify potential trend reversals

Confirm existing trends

Generate buy/sell signals when combined with other technical indicators

Filter out false signals in choppy market conditions

This STC implementation includes multiple smoothing options that act as filters:

None: Raw STC values without additional smoothing, which provides the most responsive but potentially noisier signals.

EMA Smoothing: Applies a 3-period Exponential Moving Average to reduce noise while maintaining reasonable responsiveness (default).

Sigmoid Smoothing: Transforms the STC values using a sigmoid (S-curve) function, creating more gradual transitions between signals and potentially reducing whipsaw trades.

Digital (Schmitt Trigger) Smoothing: Creates a binary output (0 or 100) with built-in hysteresis to prevent rapid switching.

The STC indicator uses dynamic color coding to visually represent momentum:

Green: When the STC value is above its 5-period EMA, indicating positive momentum

Red: When the STC value is below its 5-period EMA, indicating negative momentum

The neutral zone (25-75) is highlighted with a light gray fill to clearly distinguish between normal and extreme readings.

Alerts:

Bullish Signal Alert:

The STC has been falling

It bottoms below the 25 level

It begins to rise again

This pattern helps confirm potential uptrend starts with higher reliability.

Bearish Signal Alert:

The STC has been rising

It peaks above the 75 level

It begins to decline

This pattern helps identify potential downtrend starts.

Multi-Timeframe Stochastic RSI ArrowsMulti-Timeframe Stochastic RSI Arrows Indicator by The Venetian

Dear Moderators before you torch me alive theres nothing groundbreaking just very handy indicator for some users.

This indicator provides traders with a jet fighter-style heads-up display for market momentum across multiple timeframes. By displaying Stochastic RSI directional arrows for 12 different timeframes simultaneously, it offers a comprehensive view of market conditions without requiring multiple chart windows.

How It Works

The indicator calculates the Stochastic RSI for each of 12 common timeframes (1m to 3M) and represents directional movements with intuitive arrows:

- ▲ Green up arrow = Rising momentum

- ▼ Red down arrow = Falling momentum

- ◄► Yellow horizontal arrows = Flat/sideways momentum

- ► Gray right arrow = Just peaked (crossed above overbought)

- ◄ Gray left arrow = Just bottomed (crossed below oversold)

Each timeframe's status appears with its label (e.g., "1m ▲") in a clean, vertically-stacked display using ATR-based spacing to maintain consistent visual appearance regardless of price scale.

Key Features

- ATR-Based Spacing : Uses Average True Range to maintain consistent distances between labels even as chart scale changes

- Multi-Timeframe Analysis: Easily spot divergences and confluences across timeframes (1m, 3m, 5m, 15m, 30m, 1h, 2h, 4h, 1D, 1W, 1M, 3M)

- Sensitivity Control: Adjust flat detection sensitivity to filter out noise

- Customisable Appearance: Modify arrow size, vertical spacing, and show/hide timeframe labels

- Overbought/Oversold Detection: Highlights when momentum has peaked or bottomed at extreme levels

- Trading Applications

- Trend Alignment: Quickly identify when multiple timeframes align in the same direction

- Divergence Detection: Spot when shorter timeframes begin to shift against longer ones

- Entry/Exit Timing: Use crossovers of significant timeframes as potential signals

- Market Context: Maintain awareness of the bigger picture while trading shorter timeframes

This indicator doesn't break new ground technically but excels in presenting complex multi-timeframe information in a clean, actionable format — much like a pilot's heads-up display provides critical information at a glance. The ATR-based positioning ensures consistent visibility across different instruments and market conditions.

Great effort has been made for this script to adhere to TradingView's Pine Script house rules and focuses on trader usability rather than introducing novel technical concepts.

Jigga-SectorTrendViewThe Jigga-SectorView script is indicator designed to analyze and visualize sector trends based on given input. Based on input of multiple sector indices, calculates key technical values, and presents a structured summary in a table.

Calculating Sector Strength & Momentum:

For each selected symbol

Step 1 - 52-week lowest low is fetched.

Step 2 - Daily closing price is retrieved.

Step 3 - A crossover between 50-day EMA and 200-day EMA determines trend shifts.

Step 4 - Percentage difference from the identified level is calculated.

Output:

A bottom-right table is created with sector-wise trend insights which shows Symbol name and how much its away from SL in percentage terms.

Elastic Volume-Weighted Student-T TensionOverview

The Elastic Volume-Weighted Student-T Tension Bands indicator dynamically adapts to market conditions using an advanced statistical model based on the Student-T distribution. Unlike traditional Bollinger Bands or Keltner Channels, this indicator leverages elastic volume-weighted averaging to compute real-time dispersion and location parameters, making it highly responsive to volatility changes while maintaining robustness against price fluctuations.

This methodology is inspired by incremental calculation techniques for weighted mean and variance, as outlined in the paper by Tony Finch:

📄 "Incremental Calculation of Weighted Mean and Variance" .

Key Features

✅ Adaptive Volatility Estimation – Uses an exponentially weighted Student-T model to dynamically adjust band width.

✅ Volume-Weighted Mean & Dispersion – Incorporates real-time volume weighting, ensuring a more accurate representation of market sentiment.

✅ High-Timeframe Volume Normalization – Provides an option to smooth volume impact by referencing a higher timeframe’s cumulative volume, reducing noise from high-variability bars.

✅ Customizable Tension Parameters – Configurable standard deviation multipliers (σ) allow for fine-tuned volatility sensitivity.

✅ %B-Like Oscillator for Relative Price Positioning – The main indicator is in form of a dedicated oscillator pane that normalizes price position within the sigma ranges, helping identify overbought/oversold conditions and potential momentum shifts.

✅ Robust Statistical Foundation – Utilizes kurtosis-based degree-of-freedom estimation, enhancing responsiveness across different market conditions.

How It Works

Volume-Weighted Elastic Mean (eμ) – Computes a dynamic mean price using an elastic weighted moving average approach, influenced by trade volume, if not volume detected in series, study takes true range as replacement.

Dispersion (eσ) via Student-T Distribution – Instead of assuming a fixed normal distribution, the bands adapt to heavy-tailed distributions using kurtosis-driven degrees of freedom.

Incremental Calculation of Variance – The indicator applies Tony Finch’s incremental method for computing weighted variance instead of arithmetic sum's of fixed bar window or arrays, improving efficiency and numerical stability.

Tension Calculation – There are 2 dispersion custom "zones" that are computed based on the weighted mean and dynamically adjusted standard student-t deviation.

%B-Like Oscillator Calculation – The oscillator normalizes the price within the band structure, with values between 0 and 1:

* 0.00 → Price is at the lower band (-2σ).

* 0.50 → Price is at the volume-weighted mean (eμ).

* 1.00 → Price is at the upper band (+2σ).

* Readings above 1.00 or below 0.00 suggest extreme movements or possible breakouts.

Recommended Usage

For scalping in lower timeframes, it is recommended to use the fixed α Decay Factor, it is in raw format for better control, but you can easily make a like of transformation to N-bar size window like in EMA-1 bar dividing 2 / decayFactor or like an RMA dividing 1 / decayFactor.

The HTF selector catch quite well Higher Time Frame analysis, for example using a Daily chart and using as HTF the 200-day timeframe, weekly or monthly.

Suitable for trend confirmation, breakout detection, and mean reversion plays.

The %B-like oscillator helps gauge momentum strength and detect divergences in price action if user prefer a clean chart without bands, this thanks to pineScript v6 force overlay feature.

Ideal for markets with volume-driven momentum shifts (e.g., futures, forex, crypto).

Customization Parameters

Fixed α Decay Factor – Controls the rate of volume weighting influence for an approximation EWMA approach instead of using sum of series or arrays, making the code lightweight & computing fast O(1).

HTF Volume Smoothing – Instead of a fixed denominator for computing α , a volume sum of the last 2 higher timeframe closed candles are used as denominator for our α weight factor. This is useful to review mayor trends like in daily, weekly, monthly.

Tension Multipliers (±σ) – Adjusts sensitivity to dispersion sigma parameter (volatility).

Oscillator Zone Fills – Visual cues for price positioning within the cloud range.

Posible Interpretations

As market within indicators relay on each individual edge, this are just some key ideas to glimpse how the indicator could be interpreted by the user:

📌 Price inside bands – Market is considered somehow "stable"; price is like resting from tension or "charging batteries" for volume spike moves.

📌 Price breaking outer bands – Potential breakout or extreme movement; watch for reversals or continuation from strong moves. Market is already in tension or generating it.

📌 Narrowing Bands – Decreasing volatility; expect contraction before expansion.

📌 Widening Bands – Increased volatility; prepare for high probability pull-back moves, specially to the center location of the bands (the mean) or the other side of them.

📌 Oscillator is just the interpretation of the price normalized across the Student-T distribution fitting "curve" using the location parameter, our Elastic Volume weighted mean (eμ) fixed at 0.5 value.

Final Thoughts

The Elastic Volume-Weighted Student-T Tension indicator provides a powerful, volume-sensitive alternative to traditional volatility bands. By integrating real-time volume analysis with an adaptive statistical model, incremental variance computation, in a relative price oscillator that can be overlayed in the chart as bands, it offers traders an edge in identifying momentum shifts, trend strength, and breakout potential. Think of the distribution as a relative "tension" rubber band in which price never leave so far alone.

DISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The following indicator was made for NON LUCRATIVE ACTIVITIES and must remain as is, following TradingView's regulations. Use of indicator and their code are published for work and knowledge sharing. All access granted over it, their use, copy or re-use should mention authorship(s) and origin(s).

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED FOR TESTING. The models included in the indicator have been taken from open sources on the web and some of them has been modified by the author, problems could occur at diverse data sceneries, compiler version, or any other externality.

Hurst-Based Trend Persistence w/Poisson Prediction

---

# **Hurst-Based Trend Persistence w/ Poisson Prediction**

## **Introduction**

The **Hurst-Based Trend Persistence with Poisson Prediction** is a **statistically-driven trend-following oscillator** that provides traders with **a structured approach to identifying trend strength, persistence, and potential reversals**.

This indicator combines:

- **Hurst Exponent Analysis** (to measure how persistent or mean-reverting price action is).

- **Color-Coded Trend Detection** (to highlight bullish and bearish conditions).

- **Poisson-Based Trend Reversal Probability Projection** (to anticipate when a trend is likely to end based on statistical models).

By integrating **fractal market theory (Hurst exponent)** with **Poisson probability distributions**, this indicator gives traders a **probability-weighted view of trend duration** while dynamically adapting to market volatility.

---

## **Simplified Explanation (How to Read the Indicator at a Glance)**

1. **If the oscillator line is going up → The trend is strong.**

2. **If the oscillator line is going down → The trend is weakening.**

3. **If the color shifts from red to green (or vice versa), a trend shift has occurred.**

- **Strong trends can change color without weakening** (meaning a bullish or bearish move can remain powerful even as the trend shifts).

4. **A weakening trend does NOT necessarily mean a reversal is coming.**

- The trend may slow down but continue in the same direction.

5. **A strong trend does NOT guarantee it will last.**

- Even a powerful move can **suddenly reverse**, which is why the **Poisson-based background shading** helps anticipate probabilities of change.

---

## **How to Use the Indicator**

### **1. Understanding the Rolling Hurst-Based Trend Oscillator (Main Line)**

The **oscillator line** is based on the **Hurst exponent (H)**, which quantifies whether price movements are:

- **Trending** (values above 0 → momentum-driven, persistent trends).

- **Mean-reverting** (values below 0 → price action is choppy, likely to revert to the mean).

- **Neutral (Random Walk)** (values around 0 → price behaves like a purely stochastic process).

#### **Interpreting the Oscillator:**

- **H > 0.5 → Persistent Trends:**

- Price moves tend to sustain in one direction for longer periods.

- Example: Strong uptrends in bull markets.

- **H < 0.5 → Mean-Reverting Behavior:**

- Price has a tendency to revert back to its mean.

- Example: Sideways markets or fading momentum.

- **H ≈ 0.5 → Random Walk:**

- No clear trend; price is unpredictable.

A **gray dashed horizontal line at 0** serves as a **baseline**, helping traders quickly assess whether the market is **favoring trends or mean reversion**.

---

### **2. Color-Coded Trend Signal (Visual Confirmation of Trend Shifts)**

The oscillator **changes color** based on **price slope** over the lookback period:

- **🟢 Green → Uptrend (Price Increasing)**

- Price is rising relative to the selected lookback period.

- Suggests sustained bullish pressure.

- **🔴 Red → Downtrend (Price Decreasing)**

- Price is falling relative to the selected lookback period.

- Suggests sustained bearish pressure.

#### **How to Use This in Trading**

✔ **Stay in trends until a color change occurs.**

✔ **Use color changes as confirmation for trend reversals.**

✔ **Avoid counter-trend trades when the oscillator remains strongly colored.**

---

### **3. Poisson-Based Trend Reversal Projection (Anticipating Future Shifts)**

The **shaded orange background** represents a **Poisson-based probability estimation** of when the trend is likely to reverse.

- **Darker Orange = Higher Probability of Trend Reversal**

- **Lighter Orange / No Shade = Low Probability of Immediate Reversal**

💡 **The idea behind this model:**

✔ Trends **don’t last forever**, and their duration follows **statistical patterns**.

✔ By calculating the **average historical trend duration**, the indicator predicts **how likely a trend shift is at any given time**.

✔ The **Poisson probability function** is applied to determine the **expected likelihood of a reversal as time progresses**.

---

## **Mathematical Foundations of the Indicator**

This indicator is based on **two primary statistical models**:

### **1. Hurst Exponent & Trend Persistence (Fractal Market Theory)**

- The **Hurst exponent (H)** measures **autocorrelation** in price movements.

- If past trends **persist**, H will be **above 0.5** (meaning trend-following strategies are favorable).

- If past trends tend to **mean-revert**, H will be **below 0.5** (meaning reversal strategies are more effective).

- The **Rolling Hurst Oscillator** calculates this exponent over a moving window to track real-time trend conditions.

#### **Formula Breakdown (Simplified for Traders)**

The Hurst exponent (H) is derived using the **Rescaled Range (R/S) Analysis**:

\

Where:

- **R** = **Range** (difference between max cumulative deviation and min cumulative deviation).

- **S** = **Standard deviation** of price fluctuations.

- **Lookback** = The number of periods analyzed.

---

### **2. Poisson-Based Trend Reversal Probability (Stochastic Process Modeling)**

The **Poisson process** is a **probabilistic model used for estimating time-based events**, applied here to **predict trend reversals based on past trend durations**.

#### **How It Works**

- The indicator **tracks trend durations** (the time between color changes).

- A **Poisson rate parameter (λ)** is computed as:

\

- The **probability of a reversal at any given time (t)** is estimated using:

\

- **As t increases (trend continues), the probability of reversal rises**.

- The indicator **shades the background based on this probability**, visually displaying the likelihood of a **trend shift**.

---

## **Dynamic Adaptation to Market Conditions**

✔ **Volatility-Adjusted Trend Shifts:**

- A **custom volatility calculation** dynamically adjusts the **minimum trend duration** required before a trend shift is recognized.

- **Higher volatility → Requires longer confirmation before switching trend color.**

- **Lower volatility → Allows faster trend shifts.**

✔ **Adaptive Poisson Weighting:**

- **Recent trends are weighted more heavily** using an exponential decay function:

- **Decay Factor (0.618 by default)** prioritizes **recent intervals** while still considering historical trends.

- This ensures the model adapts to changing market conditions.

---

## **Key Takeaways for Traders**

✅ **Identify Persistent Trends vs. Mean Reversion:**

- Use the oscillator line to determine whether the market favors **trend-following or counter-trend strategies**.

✅ **Visual Trend Confirmation via Color Coding:**

- **Green = Uptrend**, **Red = Downtrend**.

- Trend changes help confirm **entry and exit points**.

✅ **Anticipate Trend Reversals Using Probability Models:**

- The **Poisson projection** provides a **statistical edge** in **timing exits before trends reverse**.

✅ **Adapt to Market Volatility Automatically:**

- Dynamic **volatility scaling** ensures the indicator remains effective in **both high and low volatility environments**.

Happy trading and enjoy!

[NLR] - MACD OverlayOverview

This script is an enhanced version of the classic MACD indicator, designed to be plotted directly on the price chart as an overlay. It provides a visual representation of trend direction by coloring moving averages, a zero reference line, and an optional histogram. The script allows for a higher timeframe MACD calculation through a configurable multiplier.

Features

MACD Calculation: Uses Exponential Moving Averages (EMA) to calculate the MACD line, Signal line, and Histogram.

Higher Timeframe Support: Multiplier option to adjust MACD parameters for a broader trend perspective.

Color-Coded Trend Visualization: Dynamic color changes based on MACD crossovers for easy trend identification.

Optional Histogram: Toggle histogram visibility to see momentum shifts.

Zero Line Reference: Helps traders interpret trend direction and strength.

How to Use

Customize Inputs: Adjust Fast, Slow, and Signal lengths as needed. Modify the multiplier to view a higher timeframe MACD.

Enable Histogram: Use the "Show Histogram" toggle to display additional visual cues for momentum shifts.

Interpret the Signals:

Uptrend (Lime): Fast EMA is above Slow EMA.

Downtrend (Fuchsia): Fast EMA is below Slow EMA.

Histogram Changes: Increasing histogram bars indicate growing momentum, while decreasing bars suggest weakening momentum.

Momentum Volume Divergence (MVD) EnhancedMomentum Volume Divergence (MVD) Enhanced is a powerful indicator that detects price-momentum divergences and momentum suppression for reversal trading. Optimized for XRP on 1D charts, it features dynamic lookbacks, ATR-adjusted thresholds, and SMA confirmation. Signals include strong divergences (triangles) and suppression warnings (crosses). Includes a detailed user guide—try it out and share your feedback!

Setup: Add to XRP 1D chart with defaults (mom_length_base=8, vol_length_base=10). Signals: Red triangle (sell), Green triangle (buy), Orange cross (bear warning), Yellow cross (bull warning). Confirm with 5-day SMA crossovers. See full guide for details!

Disclaimer: This indicator is for educational purposes only, not financial advice. Trading involves risk—use at your discretion.

Momentum Volume Divergence (MVD) Enhanced Indicator User Guide

Version: Pine Script v6

Designed for: TradingView

Recommended Use: XRP on 1-day (1D) chart

Date: March 18, 2025

Author: Herschel with assistance from Grok 3 (xAI)

Overview

The Momentum Volume Divergence (MVD) Enhanced indicator is a powerful tool for identifying price-momentum divergences and momentum suppression patterns on XRP’s 1-day (1D) chart. Plotted below the price chart, it provides clear visual signals to help traders spot potential reversals and trend shifts.

Purpose

Detect divergences between price and momentum for buy/sell opportunities.

Highlight momentum suppression as warnings of fading trends.

Offer actionable trading signals with intuitive markers.

Indicator Components

Main Plot

Volume-Weighted Momentum (vw_mom): Blue line showing momentum adjusted by volume.

Above 0 = bullish momentum.

Below 0 = bearish momentum.

Zero Line: Gray dashed line at 0, separating bullish/bearish zones.

Key Signals

Strong Bearish Divergence:

Marker: Red triangle at the top.

Meaning: Price makes a higher high, but momentum weakens, confirmed by a drop below the 5-day SMA.

Action: Potential sell/short signal.

Strong Bullish Divergence:

Marker: Green triangle at the bottom.

Meaning: Price makes a lower low, but momentum strengthens, confirmed by a rise above the 5-day SMA.

Action: Potential buy/long signal.

Bearish Suppression:

Marker: Orange cross at the top + red background.

Meaning: Strong bullish momentum with low volume in a volume downtrend, suggesting fading strength.

Action: Warning to avoid longs or exit early.

Bullish Suppression:

Marker: Yellow cross at the bottom + green background.

Meaning: Strong bearish momentum with low volume in a volume uptrend, suggesting fading weakness.

Action: Warning to avoid shorts or exit early.

Debug Plots (Optional)

Volume Ratio: Gray line (volume vs. its MA) vs. yellow line (threshold).

Momentum Threshold: Purple lines (positive/negative momentum cutoffs).

Smoothed Momentum: Orange line (raw momentum).

Confirmation SMA: Purple line (price trend confirmation).

Labels

Text labels (e.g., "Bear Div," "Bull Supp") mark detected patterns.

How to Use the Indicator

Step-by-Step Trading Process

1. Monitor the Chart

Load your XRP 1D chart with the indicator applied.

Observe the blue vw_mom line and signal markers.

2. Spot a Signal

Primary Signals: Look for red triangles (strong_bear) or green triangles (strong_bull).

Warnings: Note orange crosses (suppression_bear) or yellow crosses (suppression_bull).

3. Confirm the Signal

For Strong Bullish Divergence (Buy):

Green triangle appears.

Price closes above the 5-day SMA (purple line) and a recent swing high.

Optional: Volume ratio (gray line) exceeds the threshold (yellow line).

For Strong Bearish Divergence (Sell):

Red triangle appears.

Price closes below the 5-day SMA and a recent swing low.

Optional: Volume ratio (gray line) falls below the threshold (yellow line).

4. Enter the Trade

Long:

Buy at the close of the signal bar.

Stop loss: Below the recent swing low or 2 × ATR(14) below entry.

Short:

Sell/short at the close of the signal bar.

Stop loss: Above the recent swing high or 2 × ATR(14) above entry.

5. Manage the Trade

Take Profit:

Aim for a 2:1 or 3:1 risk-reward ratio (e.g., risk $0.05, target $0.10-$0.15).

Or exit when an opposite suppression signal appears (e.g., orange cross for longs).

Trailing Stop:

Move stop to breakeven after a 1:1 RR move.

Trail using the 5-day SMA or 2 × ATR(14).

Early Exit:

Exit if a suppression signal appears against your position (e.g., suppression_bull while short).

6. Filter Out Noise

Avoid trades if a suppression signal precedes a divergence within 2-3 days.

Optional: Add a 50-day SMA on the price chart:

Longs only if price > 50-SMA.

Shorts only if price < 50-SMA.

Example Trades (XRP 1D)

Bullish Trade

Signal: Green triangle (strong_bull) at $0.55.

Confirmation: Price closes above 5-SMA and $0.57 high.

Entry: Buy at $0.58.

Stop Loss: $0.53 (recent low).

Take Profit: $0.63 (2:1 RR) or exit on suppression_bear.

Outcome: Price hits $0.64, exit at $0.63 for profit.

Bearish Trade

Signal: Red triangle (strong_bear) at $0.70.

Confirmation: Price closes below 5-SMA and $0.68 low.

Entry: Short at $0.67.

Stop Loss: $0.71 (recent high).

Take Profit: $0.62 (2:1 RR) or exit on suppression_bull.

Outcome: Price drops to $0.61, exit at $0.62 for profit.

Tips for Success

Combine with Price Levels:

Use support/resistance zones (e.g., weekly pivots) to confirm entries.

Monitor Volume:

Rising volume (gray line above yellow) strengthens signals.

Adjust Sensitivity:

Too many signals? Increase div_strength_threshold to 0.7.

Too few signals? Decrease to 0.3.

Backtest:

Review 20-30 past signals on XRP 1D to assess performance.

Avoid Choppy Markets:

Skip signals during low volatility (tight price ranges).

Troubleshooting

No Signals:

Lower div_strength_threshold to 0.3 or mom_threshold_base to 0.2.

Check if XRP’s volatility is unusually low.

False Signals:

Increase sma_confirm_length to 7 or add a 50-SMA filter.

Indicator Not Loading:

Ensure the script compiles without errors.

Customization (Optional)

Change Colors: Edit color.* values (e.g., color.red to color.purple).

Add Alerts: Use TradingView’s alert menu for "Strong Bearish Divergence Confirmed," etc.

Test Other Assets: Experiment with BTC or ETH, adjusting inputs as needed.

Disclaimer

This indicator is for educational purposes only and not financial advice. Trading involves risk, and past performance does not guarantee future results. Use at your own discretion.

Setup: Use on XRP 1D with defaults (mom_length_base=8, vol_length_base=10). Signals: Red triangle (sell), Green triangle (buy), Orange cross (bear warning), Yellow cross (bull warning). Confirm with 5-day SMA cross. Stop: 2x ATR(14). Profit: 2:1 RR or suppression exit. Full guide available separately!

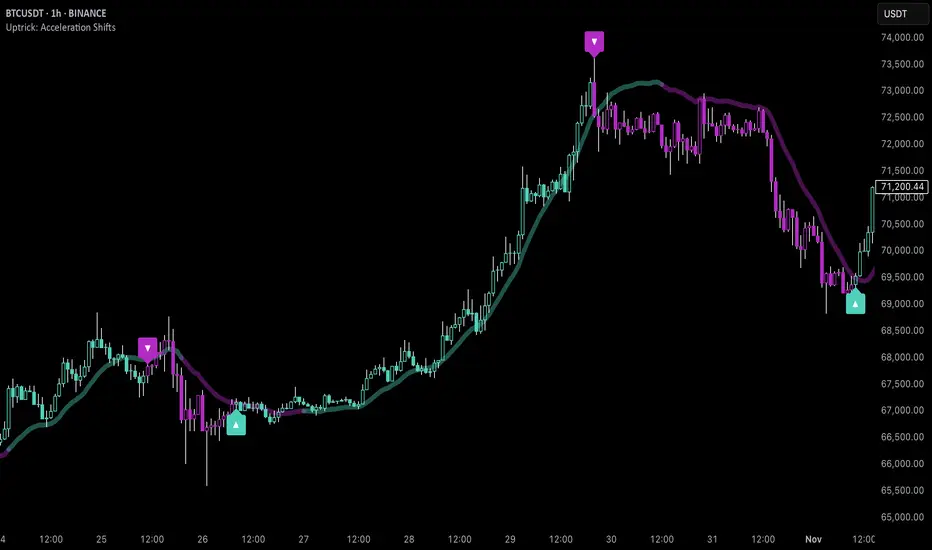

Uptrick: Acceleration ShiftsIntroduction

Uptrick: Acceleration Shifts is designed to measure and visualize price momentum shifts by focusing on acceleration —the rate of change in velocity over time. It uses various moving average techniques as a trend filter, providing traders with a clearer perspective on market direction and potential trade entries or exits.

Purpose

The main goal of this indicator is to spot strong momentum changes (accelerations) and confirm them with a chosen trend filter. It attempts to distinguish genuine market moves from noise, helping traders make more informed decisions. The script can also trigger multiple entries (smart pyramiding) within the same trend, if desired.

Overview

By measuring how quickly price velocity changes (acceleration) and comparing it against a smoothed average of itself, this script generates buy or sell signals once the acceleration surpasses a given threshold. A trend filter is added for further validation. Users can choose from multiple smoothing methods and color schemes, and they can optionally enable a small table that displays real-time acceleration values.

Originality and Uniqueness

This script offers an acceleration-based approach, backed by several different moving average choices. The blend of acceleration thresholds, a trend filter, and an optional extra-entry (pyramiding) feature provides a flexible toolkit for various trading styles. The inclusion of multiple color themes and a slope-based coloring of the trend line adds clarity and user customization.

Inputs & Features

1. Acceleration Length (length)

This input determines the number of bars used when calculating velocity. Specifically, the script computes velocity by taking the difference in closing prices over length bars, and then calculates acceleration based on how that velocity changes over an additional length. The default is 14.

2. Trend Filter Length (smoothing)

This sets the lookback period for the chosen trend filter method. The default of 50 results in a moderately smooth trend line. A higher smoothing value will create a slower-moving trend filter.

3. Acceleration Threshold (threshold)

This multiplier determines when acceleration is considered strong enough to trigger a main buy or sell signal. A default value of 2.5 means the current acceleration must exceed 2.5 times the average acceleration before signaling.

4. Smart Pyramiding Strength (pyramidingThreshold)

This lower threshold is used for additional (pyramiding) entries once the main trend has already been identified. For instance, if set to 0.5, the script looks for acceleration crossing ±0.5 times its average acceleration to add extra positions.

5. Max Pyramiding Entries (maxPyramidingEntries)

This sets a limit on how many extra positions can be opened (beyond the first main signal) in a single directional trend. The default of 3 ensures traders do not become overexposed.

6. Show Acceleration Table (showTable)

When enabled, a small table displaying the current acceleration and its average is added to the top-right corner of the chart. This table helps monitor real-time momentum changes.

7. Smart Pyramiding (enablePyramiding)

This toggle decides whether additional entries (buy or sell) will be generated once a main signal is active. If enabled, these extra signals act as filtered entries, only firing when acceleration re-crosses a smaller threshold (pyramidingThreshold). These signals have a '+' next to their signal on the label.

8. Select Color Scheme (selectedColorScheme)

Allows choosing between various pre-coded color themes, such as Default, Emerald, Sapphire, Golden Blaze, Mystic, Monochrome, Pastel, Vibrant, Earth, or Neon. Each theme applies a distinct pair of colors for bullish and bearish conditions.

9. Trend Filter (TrendFilter)

Lets the user pick one of several moving average approaches to determine the prevailing trend. The options include:

Short Term (TEMA)

EWMA

Medium Term (HMA)

Classic (SMA)

Quick Reaction (DEMA)

Each method behaves differently, balancing reactivity and smoothness.

10. Slope Lookback (slopeOffset)

Used to measure the slope of the trend filter over a set number of bars (default is 10). This slope then influences the coloring of the trend filter line, indicating bullish or bearish tilt.

Note: The script refers to this as the "Massive Slope Index," but it effectively serves as a Trend Slope Calculation, measuring how the chosen trend filter changes over a specified period.

11. Alerts for Buy/Sell and Pyramiding Signals

The script includes built-in alert conditions that can be enabled or configured. These alerts trigger whenever the script detects a main Buy or Sell signal, as well as extra (pyramiding) signals if Smart Pyramiding is active. This feature allows traders to receive immediate notifications or automate a trading response.

Calculation Methodology

1. Velocity and Acceleration

Velocity is derived by subtracting the closing price from its value length bars ago. Acceleration is the difference in velocity over an additional length period. This highlights how quickly momentum is shifting.

2. Average Acceleration

The script smooths raw acceleration with a simple moving average (SMA) using the smoothing input. Comparing current acceleration against this average provides a threshold-based signal mechanism.

3. Trend Filter

Users can pick one of five moving average types to form a trend baseline. These range from quick-reacting methods (DEMA, TEMA) to smoother options (SMA, HMA, EWMA). The script checks whether the price is above or below this filter to confirm trend direction.

4. Buy/Sell Logic

A buy occurs when acceleration surpasses avgAcceleration * threshold and price closes above the trend filter. A sell occurs under the opposite conditions. An additional overbought/oversold check (based on a longer SMA) refines these signals further.

When price is considered oversold (i.e., close is below a longer-term SMA), a bullish acceleration signal has a higher likelihood of success because it indicates that the market is attempting to reverse from a lower price region. Conversely, when price is considered overbought (close is above this longer-term SMA), a bearish acceleration signal is more likely to be valid. This helps reduce false signals by waiting until the market is extended enough that a reversal or continuation has a stronger chance of following through.

5. Smart Pyramiding

Once a main buy or sell signal is triggered, additional (filtered) entries can be taken if acceleration crosses a smaller multiplier (pyramidingThreshold). This helps traders scale into strong moves. The script enforces a cap (maxPyramidingEntries) to limit risk.

6. Visual Elements

Candles can be recolored based on the active signal. Labels appear on the chart whenever a main or pyramiding entry signal is triggered. An optional table can show real-time acceleration values.

Color Schemes

The script includes a variety of predefined color themes. For bullish conditions, it might use turquoise or green, and for bearish conditions, magenta or red—depending on which color scheme the user selects. Each scheme aims to provide clear visual differentiation between bullish and bearish market states.

Why Each Indicator Was Part of This Component

Acceleration is employed to detect swift changes in momentum, capturing shifts that may not yet appear in more traditional measures. To further adapt to different trading styles and market conditions, several moving average methods are incorporated:

• TEMA (Triple Exponential Moving Average) is chosen for its ability to reduce lag more effectively than a standard EMA while still reacting swiftly to price changes. Its construction layers exponential smoothing in a way that can highlight sudden momentum shifts without sacrificing too much smoothness.

• DEMA (Double Exponential Moving Average) provides a faster response than a single EMA by using two layers of exponential smoothing. It is slightly less smoothed than TEMA but can alert traders to momentum changes earlier, though with a higher risk of noise in choppier markets.

• HMA (Hull Moving Average) is known for its balance of smoothness and reduced lag. Its weighted calculations help track trend direction clearly, making it useful for traders who want a smoother line that still reacts fairly quickly.

• SMA (Simple Moving Average) is the classic baseline for smoothing price data. It offers a clear, stable perspective on long-term trends, though it reacts more slowly than other methods. Its simplicity can be beneficial in lower-volatility or more stable market environments.

• EWMA (Exponentially Weighted Moving Average) provides a middle ground by emphasizing recent price data while still retaining some degree of smoothing. It typically responds faster than an SMA but is less aggressive than DEMA or TEMA.

Alongside these moving average techniques, the script employs a slope calculation (referred to as the “Massive Slope Index”) to visually indicate whether the chosen filter is sloping upward or downward. This adds an extra layer of clarity to directional analysis. The indicator also uses overbought/oversold checks, based on a longer-term SMA, to help filter out signals in overstretched markets—reducing the likelihood of false entries in conditions where the price is already extensively extended.

Additional Features

Alerts can be set up for both main signals and additional pyramiding signals, which is helpful for automated or semi-automated trading. The optional acceleration table offers quick reference values, making momentum monitoring more intuitive. Including explicit alert conditions for Buy/Sell and Pyramiding ensures traders can respond promptly to market movements or integrate these triggers into automated strategies.

Summary

This script serves as a comprehensive momentum-based trading framework, leveraging acceleration metrics and multiple moving average filters to identify potential shifts in market direction. By combining overbought/oversold checks with threshold-based triggers, it aims to reduce the noise that commonly plagues purely reactive indicators. The flexibility of Smart Pyramiding, customizable color schemes, and built-in alerts allows users to tailor their experience and respond swiftly to valid signals, potentially enhancing trading decisions across various market conditions.

Disclaimer

All trading involves significant risk, and users should apply their own judgment, risk management, and broader analysis before making investment decisions.

RSI & MACD Exit IndicatorThis indicator is designed to assist traders in identifying potential exit points for long and short trades by combining the Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD).

Unlike traditional indicators that provide entry signals, this script is specifically optimized for exit strategies, helping traders manage their positions efficiently.

How It Works

The script identifies potential exit points based on the following conditions:

🔴 Exit Long:

- RSI crosses above the user-defined overbought threshold (default: 65).

- MACD crosses below the signal line (bearish crossover).

🟢 Exit Short:

- RSI crosses below the user-defined oversold threshold (default: 35).

- MACD crosses above the signal line (bullish crossover).

When these conditions align, a label appears on the price chart indicating an exit point.

Key Features

- Customizable RSI & MACD Settings – Adjust lengths and thresholds to suit your strategy.

- ATR-Based Adjustments – The script incorporates an ATR multiplier for dynamic signal adjustments based on market volatility.

- Clear Visual Labels – Exit points are clearly marked on price candles.

- Color-Coded Background – Highlights buy/sell zones for quick identification.

- Alerts for Exit Signals – Receive notifications when exit conditions are met.

- Clean Chart Design – The MACD plots are placed below the main chart to avoid clutter.

How to Use

⚠ This indicator is for exits only and does not generate buy/sell entry signals.

For long trades: When an Exit Long signal appears, traders may consider closing or reducing their long positions.

For short trades: When an Exit Short signal appears, traders may consider closing or reducing their short positions.

ATR Settings: Users can adjust the ATR multiplier to fine-tune the signal frequency based on market conditions.

Important Notes

- This indicator does not guarantee future performance—it should be used alongside other analysis methods.

- No financial advice – Always use proper risk management.

- TradingView users who do not read Pine Script can still fully utilize this script thanks to the detailed signal labels and alerts.

💡 Developed with advice from @CoffeeshopCrypto based on user feedback.

BTC Momentum Detector 1h# BTC Momentum Detector 1h

This indicator is designed to detect significant momentum movements in Bitcoin price on the 1-hour timeframe. It identifies candles with percentage changes within a specific range, which often precede larger price movements.

## How It Works

The indicator analyzes price movements to detect potential momentum shifts:

- Identifies candles with percentage changes between configurable thresholds (default: 1.7% - 2.8%)

- Requires neutral or inverse movement in the prior candle to avoid false signals

- Optional volume filter ensures signals are confirmed by above-average trading activity

- Tracks price continuation to calculate success rates and average returns

## Key Features

- **Signal Detection**: Green triangles below price bars indicate upward momentum signals; red triangles above price bars indicate downward momentum signals

- **Continuation Tracking**: Dashed horizontal lines show the entry price levels of active signals being tracked

- **Statistics Panel**: Displays real-time metrics including signal counts, success rates, and average returns

- **Current Status**: Shows the current price change percentage and active signals being monitored

## Parameters

- **Minimum Percentage Threshold**: Minimum price change to trigger a signal (default: 1.7%)

- **Maximum Percentage Threshold**: Maximum price change to filter out extreme moves (default: 2.8%)

- **Continuation Periods**: Number of periods to track after signal (default: 2)

- **Require Prior Neutral/Inverse**: Filters signals by requiring neutral or opposite prior movement

- **Neutral Threshold**: Defines what's considered a neutral movement (default: 0.1%)

- **Volume Filter**: Option to require above-average volume for confirmation

- **Volume Multiplier**: Volume must exceed average by this factor (default: 2x)

## Strategy Concept

The underlying strategy is based on the concept that when Bitcoin makes a controlled, significant move (not too small, not too large) after a period of neutral or opposite movement, it often continues in that direction for the next few periods. This pattern reflects the early stages of momentum development in the market.

[F.B]_ZLEMA MACD ZLEMA MACD – A Zero-Lag Variant of the Classic MACD

Introduction & Motivation

The Moving Average Convergence Divergence (MACD) is a standard indicator for measuring trend strength and momentum. However, it suffers from the latency of traditional Exponential Moving Averages (EMAs).

This variant replaces EMAs with Zero Lag Exponential Moving Averages (ZLEMA), reducing delay and increasing the indicator’s responsiveness. This can potentially lead to earlier trend change detection, especially in highly volatile markets.

Calculation Methodology

2.1 Zero-Lag Exponential Moving Average (ZLEMA)

The classic EMA formula is extended with a correction factor:

ZLEMA_t = EMA(2 * P_t - EMA(P_t, L), L)

where:

P_t is the closing price,

L is the smoothing period length.

2.2 MACD Calculation Using ZLEMA

MACD_t = ZLEMA_short,t - ZLEMA_long,t

with standard parameters of 12 and 26 periods.

2.3 Signal Line with Adaptive Methodology

The signal line can be calculated using ZLEMA, EMA, or SMA:

Signal_t = f(MACD, S)

where f is the chosen smoothing function and S is the period length.

2.4 Histogram as a Measure of Momentum Changes

Histogram_t = MACD_t - Signal_t

An increasing histogram indicates a relative acceleration in trend strength.

Potential Applications in Data Analysis

Since the indicator is based solely on price time series, its effectiveness as a standalone trading signal is limited. However, in quantitative models, it can be used as a feature for trend quantification or for filtering market phases with strong trend dynamics.

Potential use cases include:

Trend Classification: Segmenting market phases into "trend" vs. "mean reversion."

Momentum Regime Identification: Analyzing histogram dynamics to detect increasing or decreasing trend strength.

Signal Smoothing: An alternative to classic EMA smoothing in more complex multi-factor models.

Important: Using this as a standalone trading indicator without additional confirmation mechanisms is not recommended, as it does not demonstrate statistical superiority over other momentum indicators.

Evaluation & Limitations

✅ Advantages:

Reduced lag compared to the classic MACD.

Customizable signal line smoothing for different applications.

Easy integration into existing analytical pipelines.

⚠️ Limitations:

Not a standalone trading system: Like any moving average, this indicator is susceptible to noise and false signals in sideways markets.

Parameter sensitivity: Small changes in period lengths can lead to significant signal deviations, requiring robust optimization.

Conclusion

The ZLEMA MACD is a variant of the classic MACD with reduced latency, making it particularly useful for analytical purposes where faster adaptation to price movements is required.

Its application in trading strategies should be limited to multi-factor models with rigorous evaluation. Backtests and out-of-sample analyses are essential to avoid overfitting to past market data.

Disclaimer: This indicator is provided for informational and educational purposes only and does not constitute financial advice. The author assumes no responsibility for any trading decisions made based on this indicator. Trading involves significant risk, and past performance is not indicative of future results.

RSI + Stochastic + WMA StrategyThis script is designed for TradingView and serves as a trading strategy (not just a visual indicator). It's intended for backtesting, strategy optimization, or live trading signal generation using a combination of popular technical indicators.

📊 Indicators Used in the Strategy:

Indicator Description

RSI (Relative Strength Index) Measures momentum; identifies overbought (>70) or oversold (<30) conditions.

Stochastic Oscillator (%K & %D) Detects momentum reversal points via crossovers. Useful for timing entries.

WMA (Weighted Moving Average) Identifies the trend direction (used as a trend filter).

📈 Trading Logic / Strategy Rules:

📌 Long Entry Condition (Buy Signal):

All 3 conditions must be true:

RSI is Oversold → RSI < 30

Stochastic Crossover Upward → %K crosses above %D

Price is above WMA → Confirms uptrend direction

👉 Interpretation: Market was oversold, momentum is turning up, and price confirms uptrend — bullish entry.

📌 Short Entry Condition (Sell Signal):

All 3 conditions must be true:

RSI is Overbought → RSI > 70

Stochastic Crossover Downward → %K crosses below %D

Price is below WMA → Confirms downtrend direction

👉 Interpretation: Market is overbought, momentum is turning down, and price confirms downtrend — bearish entry.

🔄 Strategy Execution (Backtesting Logic):

The script uses:

pinescript

Copy

Edit

strategy.entry("LONG", strategy.long)

strategy.entry("SHORT", strategy.short)

These are Pine Script functions to place buy and sell orders automatically when the above conditions are met. This allows you to:

Backtest the strategy

Measure win/loss ratio, drawdown, and profitability

Optimize indicator settings using TradingView Strategy Tester

📊 Visual Aids (Charts):

Plots WMA Line: Orange line for trend direction

Overbought/Oversold Zones: Horizontal lines at 70 (red) and 30 (green) for RSI visualization

⚡ Strategy Type Summary:

Category Setting

Strategy Type Momentum Reversal + Trend Filter

Timeframe Flexible (Works best on 1H, 4H, Daily)

Trading Style Swing/Intraday

Risk Profile Medium to High (due to momentum triggers)

Uses Leverage Possible (adjust risk accordingly)

Moving Average Convergence Divergence with Enhanced Cross Alerts

Overview of Features and Settings

- Customizable Parameters:

- Fast and Slow Periods: Users can set the duration for both the fast (default 12) and slow (default 26) moving averages.

- Source Selection: The indicator uses the closing price (close) by default, though this can be modified to any other data source.

- Signal Smoothing: The smoothing period for the signal line is adjustable (default 9), and you can choose whether to use SMA or EMA for both the oscillator and the signal line calculations.

Calculation Logic

1. Calculation of Moving Averages:

- The fast and slow moving averages are computed based on the chosen moving average type (SMA or EMA) over the specified periods.

- The MACD line is then determined as the difference between these two moving averages.

2. Signal Line and Histogram:

- Signal Line: Created by smoothing the MACD line, with the option to choose between SMA and EMA.

- Histogram: Represents the difference between the MACD line and the signal line, visually indicating the divergence between the two.

Detection of Cross Events

The script identifies two specific cross events with additional filtering conditions:

- Bullish Cross:

- The MACD line **crosses above** the signal line.

- The previous value of the histogram is negative, and both the MACD and the signal line are below zero.

- This condition suggests that a cross occurring in the negative territory might indicate a potential upward trend reversal.

- **Bearish Cross:**

- The MACD line **crosses below** the signal line.

- The previous value of the histogram is positive, and both the MACD and the signal line are above zero.

- This condition indicates that a cross in the positive territory may signal a potential downward trend reversal.

For each event, there are dedicated alert conditions defined that trigger notifications when the criteria are met.

Visualization

- Displayed Elements:

- Histogram: Rendered as a column chart with colors that change based on the rate of change. For instance, a rising positive histogram uses a stronger green, whereas a declining positive histogram uses a lighter shade.

- MACD and Signal Lines: Displayed as separate lines with distinct colors to differentiate them.

- Zero Line: A horizontal line is drawn to help visually pinpoint the zero level.

- Crossing Signals:

- Optional markers in the form of arrows appear on the chart:

- **Bullish Cross: A green, upward-pointing triangle at the bottom.

- **Bearish Cross: A red, downward-pointing triangle at the top.

Summary

This indicator not only incorporates the traditional MACD components but also offers the following additional benefits:

- **Enhanced Accuracy:** Extra conditions (such as checking the previous histogram value and the position of the lines relative to zero) improve the identification of significant cross events.

- **Customization:** Users can personalize the moving average types and periods, making the indicator adaptable to different trading strategies.

- **Visual Assistance:** The combination of histogram columns, lines, and markers helps quickly pinpoint potential trend reversals, thereby aiding trading decisions.

This comprehensive description is intended to clearly demonstrate to users how the indicator works, outlining its calculations, filtering conditions, and its role in identifying cross events within technical analysis.

Clustering & Divergences (RSI-Stoch-CCI) [Sam SDF-Solutions]The Clustering & Divergences (RSI-Stoch-CCI) indicator is a comprehensive technical analysis tool that consolidates three popular oscillators—Relative Strength Index (RSI), Stochastic, and Commodity Channel Index (CCI)—into one unified metric called the Score. This Score offers traders an aggregated view of market conditions, allowing them to quickly identify whether the market is oversold, balanced, or overbought.

Functionality:

Oscillator Clustering: The indicator calculates the values of RSI, Stochastic, and CCI using user-defined periods. These oscillator values are then normalized using one of three available methods: MinMax, Z-Score, or Z-Bins.

Score Calculation: Each normalized oscillator value is multiplied by its respective weight (which the user can adjust), and the weighted values are summed to generate an overall Score. This Score serves as a single, interpretable metric representing the combined oscillator behavior.

Market Clustering: The indicator performs clustering on the Score over a configurable window. By dividing the Score range into a set number of clusters (also configurable), the tool visually represents the market’s state. Each cluster is assigned a unique color so that traders can quickly see if the market is trending toward oversold, balanced, or overbought conditions.

Divergence Detection: The script automatically identifies both Regular and Hidden divergences between the price action and the Score. By using pivot detection on both price and Score data, the indicator marks potential reversal signals on the chart with labels and connecting lines. This helps in pinpointing moments when the price and the underlying oscillator dynamics diverge.

Customization Options: Users have full control over the indicator’s behavior. They can adjust:

The periods for each oscillator (RSI, Stochastic, CCI).

The weights applied to each oscillator in the Score calculation.

The normalization method and its manual boundaries.

The number of clusters and whether to invert the cluster order.

Parameters for divergence detection (such as pivot sensitivity and the minimum/maximum bar distance between pivots).

Visual Enhancements:

Depending on the user’s preference, either the Score or the Cluster Index (derived from the clustering process) is plotted on the chart. Additionally, the script changes the color of the price bars based on the identified cluster, providing an at-a-glance visual cue of the current market regime.

Logic & Methodology:

Input Parameters: The script starts by accepting user inputs for clustering settings, oscillator periods, weights, divergence detection, and manual boundary definitions for normalization.

Oscillator Calculation & Normalization: It computes RSI, Stochastic, and CCI values from the price data. These values are then normalized using either the MinMax method (scaling between a lower and upper band) or the Z-Score method (standardizing based on mean and standard deviation), or using Z-Bins for an alternative scaling approach.

Score Computation: Each normalized oscillator is multiplied by its corresponding weight. The sum of these products results in the overall Score that represents the combined oscillator behavior.

Clustering Algorithm: The Score is evaluated over a moving window to determine its minimum and maximum values. Using these values, the script calculates a cluster index that divides the Score into a predefined number of clusters. An option to invert the cluster calculation is provided to adjust the interpretation of the clustering.

Divergence Analysis: The indicator employs pivot detection (using left and right bar parameters) on both the price and the Score. It then compares recent pivot values to detect regular and hidden divergences. When a divergence is found, the script plots labels and optional connecting lines to highlight these key moments on the chart.

Plotting: Finally, based on the user’s selection, the indicator plots either the Score or the Cluster Index. It also overlays manual boundary lines (for the chosen normalization method) and adjusts the bar colors according to the cluster to provide clear visual feedback on market conditions.

_________

By integrating multiple oscillator signals into one cohesive tool, the Clustering & Divergences (RSI-Stoch-CCI) indicator helps traders minimize subjective analysis. Its dynamic clustering and automated divergence detection provide a streamlined method for assessing market conditions and potentially enhancing the accuracy of trading decisions.

For further details on using this indicator, please refer to the guide available at:

Enhanced ROC - Savitzky–Golay [AIBitcoinTrend]👽 Adaptive ROC - Savitzky–Golay (AIBitcoinTrend)

The Adaptive ROC - Savitzky–Golay redefines traditional Rate of Change (ROC) analysis by integrating Savitzky–Golay smoothing with volatility-adaptive normalization, allowing it to dynamically adjust across different market conditions. Unlike the standard ROC, which reacts rigidly to price changes, this advanced version refines trend signals while maintaining responsiveness to volatility.

Additionally, this indicator features real-time divergence detection and an ATR-based trailing stop system, equipping traders with a powerful toolset for momentum analysis, reversals, and trend-following strategies.

👽 What Makes the Adaptive ROC - Savitzky–Golay Unique?

Unlike conventional ROC indicators, this enhanced version leverages volatility-adjusted scaling and Z-score normalization to improve signal consistency across different timeframes and assets.

✅ Savitzky–Golay Smoothing – Reduces noise while preserving trend structure for clearer signals.

✅ Volatility-Adaptive Normalization – Ensures that overbought and oversold thresholds remain consistent across different markets.

✅ Real-Time Divergence Detection – Identifies early bullish and bearish divergence signals for potential reversals.

✅ Crossovers & ATR-Based Trailing Stops – Implements intelligent trade management with dynamic stop levels.

👽 The Math Behind the Indicator

👾 Savitzky–Golay Smoothing

The indicator applies a Savitzky–Golay filter to the raw ROC data, creating a smoother curve while preserving key inflection points. This technique prevents excessive lag while maintaining the integrity of price movements.

sg_roc = (roc_raw + 3*roc_raw + 5*roc_raw + 7*roc_raw + 5*roc_raw + 3*roc_raw + roc_raw ) / 25

👾 Volatility-Adaptive Scaling

By dynamically adjusting the smoothed ROC using standard deviation, the indicator ensures that momentum readings remain relative to the market’s current volatility.

volatility = ta.stdev(close, rocLength)

dynamicFactor = 1 / (1 + volatility / 100)

advanced_sg_roc = sg_roc * dynamicFactor

👾 Z-Score Normalization

To maintain a stable Overbought/Oversold structure across different markets, the ROC is normalized using a Z-score transformation, ensuring its values remain statistically relevant.

rocMean = ta.wma(advanced_sg_roc, lenZ)

rocStdev = ta.stdev(advanced_sg_roc, lenZ)

zRoc = (advanced_sg_roc - rocMean) / rocStdev

👽 How Traders Can Use This Indicator

👾 Divergence Trading Strategy

Bullish Divergence Setup:

Price makes a lower low, while the ROC forms a higher low.

A buy signal is confirmed when the ROC starts rising.

Bearish Divergence Setup:

Price makes a higher high, while the ROC forms a lower high.

A sell signal is confirmed when the ROC starts declining.

👾 Buy & Sell Signals with Trailing Stop

Bullish Setup:

✅ ROC crosses above the bullish trigger level → Buy Signal.

✅ A bullish trailing stop is placed at Low - (ATR × Multiplier).

✅ Exit if price crosses below the stop.

Bearish Setup:

✅ ROC crosses below the bearish trigger level → Sell Signal.

✅ A bearish trailing stop is placed at High + (ATR × Multiplier).

✅ Exit if price crosses above the stop.

👽 Why It’s Useful for Traders

Savitzky–Golay Filtering – Retains essential trend details while eliminating excessive noise.

Volatility-Adjusted Normalization – Makes overbought/oversold levels universally reliable across markets.

Real-Time Divergence Alerts – Identifies early reversal signals for optimal entries and exits.

ATR-Based Risk Management – Ensures stops dynamically adapt to market conditions.

Works Across Markets & Timeframes - Suitable for stocks, forex, crypto, and futures trading.

👽 Indicator Settings

ROC Period – Defines the number of bars used for ROC calculation.

Smoothing Strength – Adjusts the degree of Savitzky–Golay filtering.

Volatility Scaling – Enables or disables the adaptive volatility factor.

Enable Divergence Analysis – Turns on real-time divergence detection.

Lookback Period – Specifies the pivot detection period for divergences.

Enable Crosses Signals – Activates trade signals based on ROC crossovers.

ATR Multiplier – Controls the sensitivity of the trailing stop.

Disclaimer: This indicator is designed for educational purposes and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

MACD Sniper [trade_lexx]📈 MACD Sniper — Improve your trading strategy with accurate signals!

Introducing the MACD Sniper , an advanced trading indicator designed for a comprehensive analysis of market conditions. This indicator combines MACD (Moving Average Convergence Divergence) with various types of moving averages (SMA, EMA, WMA, VWMA, KAMA, HMA, ZLEMA, TEMA, ALMA, DEMA), providing traders with a powerful tool for generating buy and sell signals. It is ideal for traders who need an advantage in detecting changes in trends and market conditions.

🔍 How the signals work

1. Histogram signals: