ATR ZigZag BreakoutATR ZigZag Breakout

This strategy uses my ATR ZigZag indicator (powered by the ZigZagCore library) to scalp breakouts at volatility-filtered highs and lows.

Everyone knows stops cluster around clear swing highs and lows. Breakout traders often pile in there, too. These levels are predictable areas where aggressive orders hit the tape. The idea here is simple:

→ Let ATR ZigZag define clean, volatility-filtered pivots

→ Arm a stop market order at those pivots

→ Join the breakout when the crowd hits the level

The key to greater success in this simple strategy lies in the ZigZag. Because the pivots are filtered by ATR instead of fixed bar counts or fractals, the levels tend to be more meaningful and less noisy.

This approach is especially suited for intraday trading on volatile instruments (e.g., NQ, GC, liquid crypto pairs).

How It Works

1. Pivot detection

The ATR ZigZag uses an ATR-based threshold to confirm swing highs and lows. Only when price has moved far enough in the opposite direction does a pivot become “official.”

2. Candidate breakout level

When a new swing direction is detected and the most recent high/low has not yet been broken in the current leg, the strategy arms a stop market order at that pivot.

• Long candidate → most recent swing high

• Short candidate → most recent swing low

These “candidate trades” are shown as dotted lines.

3. Entry, SL, and TP

If price breaks through the level, the stop order is filled and a bracket is placed:

• Stop loss = ATR × SL multiplier

• Take profit = SL distance × RR multiplier

Once a level has traded, it is not reused in the same swing leg.

4. Cancel & rotate

If the market reverses and forms a new swing in the opposite direction before the level is hit, the pending order is cancelled and a new candidate is considered in the new direction.

Additional Features

• Optional session filter for backtesting specific trading hours

Breakout!

Session Opening Range Breakout (ORBO)This strategy automates a classic Opening Range Breakout (ORBO) approach: it builds a price range for the first minutes after the market opens, then looks for strong breakouts above or below that range to catch early directional moves.

Concept

The idea behind ORBO is simple:

The first minutes after the session open are often highly informative.

Price forms an “opening range” that acts as a mini support/resistance zone.

A clean breakout beyond this zone can lead to high-momentum moves.

This script turns that logic into a fully backtestable strategy in TradingView.

How the strategy works

Opening Range Session

Default session: 09:30–09:50 (exchange time)

During this window, the script tracks:

orHigh → highest high within the session

orLow → lowest low within the session

This forms your Opening Range for the day.

Breakout Logic (after the window ends)

Once the defined session ends:

Long Entry:

If the close crosses above the Opening Range High (orHigh),

→ strategy.entry("OR Long", strategy.long) is triggered.

Short Entry:

If the close crosses below the Opening Range Low (orLow),

→ strategy.entry("OR Short", strategy.short) is triggered.

Only one opening range per day is considered, which keeps the logic clean and easy to interpret.

Daily Reset

At the start of a new trading day, the script resets:

orHigh := na

orLow := na

A fresh Opening Range is then built using the next session’s 09:30–09:50 candles.

This ensures entries are always based on today’s structure, not yesterday’s.

Visuals & Inputs

Inputs:

Opening range session → default: "0930-0950"

Show OR levels → toggle visibility of OR High / Low lines

Fill range body → optional shaded zone between OR High and OR Low

Chart visuals:

A green line marks the Opening Range High.

A red line marks the Opening Range Low.

Optional yellow fill highlights the entire OR zone.

Background shading during the session shows when the range is currently being built.

These visuals make it easy to see:

Where the OR sits relative to current price

How clean / noisy the breakout was

How often price respects or rejects the opening zone

Backtesting & Optimization

Because this is written as a strategy():

You can use TradingView’s Strategy Tester to view:

Win rate

Net profit

Drawdown

Profit factor

Equity curve

Ideas to experiment with:

Change the session window (e.g., 09:15–09:45, 10:00–10:30)

Apply to different:

Markets: indices, FX, crypto, stocks

Timeframes: 1m / 5m / 15m

Add your own:

Stop Loss & Take Profit levels

Time filters (only trade certain days / times)

Volatility filters (e.g., ATR, range size thresholds)

Higher-timeframe trend filter (e.g., only take longs above 200 EMA)

Best Entry Swing MASTER v3 PUBLIC (S.S)Strategy Description (English)

Best Entry Swing MASTER v3 – Quality Mode

The Best Entry Swing MASTER v3 is a structured swing trading and trend-following strategy designed to identify high-probability long and short entries during directional markets.

It combines three core setup types commonly used by momentum and breakout traders:

Breakout (BO)

Pullback Reversal (PB)

Volatility Contraction Pattern (VCP)

The strategy applies multiple layers of confirmation, including multi-EMA trend structure, volatility contraction, volume filters, and an optional market regime filter.

It is suitable for swing trading on higher timeframes (4H, Daily), as well as medium-term trend continuation setups.

Core Concepts

1. Trend Structure

A trend is considered valid when:

Uptrend: Price > EMA20 > EMA50 > EMA100

Downtrend: Price < EMA20 < EMA50 < EMA100

In addition, a simple but effective trend-strength metric is calculated using the percentage spread between EMA20 and EMA100.

This helps avoid signals during sideways or low-volatility environments.

2. Market Regime Filter

The market environment is determined using a higher timeframe benchmark (default: SPY on Daily).

Only long trades are allowed in bullish market conditions

Only short trades in bearish conditions

This significantly reduces false signals in counter-trend conditions.

Entry Logic

Breakout (BO)

A long breakout triggers when:

Price closes above the highest high of the lookback period

Volume exceeds its 20-period average

Trend and market regime confirm

(Optional A+ mode): true volatility contraction is required

Similar logic applies for short breakdowns.

Pullback (PB)

A pullback entry triggers after:

At least two corrective candles

A strong reversal candle (close above previous high for long)

Volume confirmation

Price interacts with EMA20

This structure models classical trend-reentry conditions.

Volatility Contraction Pattern (VCP)

A VCP entry triggers when:

True range contracts over multiple bars

Price holds near the breakout zone

Volume contracts

Trend and market regime are aligned

This setup aims to capture explosive continuation moves.

Quality Modes

The strategy offers two modes:

Balanced Mode

Moderate signal frequency

Broader trend-strength allowance

Suitable for more active traders

A+ Only Mode

Strict confirmation requirements

Only high-quality setups with multiple confluences

Designed to avoid low-probability trades entirely

Risk Management

Risk is managed using an ATR-based stop and target:

Long SL = Close − ATR × 1.5

Long TP = Close + ATR × 3

(Equivalent logic for short positions)

This provides a balanced reward-to-risk profile and avoids overly tight stops.

Early Entry Signals (Optional)

The script offers optional “Early Entry” markers that highlight when a setup is forming but not yet confirmed.

These are not entry signals and are disabled by default for public use.

Intended Use

This strategy is designed for:

Swing trading

Momentum continuation

Trend-following

Multi-day to multi-week trades

It performs best on:

4H

Daily

High-liquidity equities, indices, and futures

Disclaimer

This script is intended for educational and research purposes.

Past performance does not guarantee future results.

Always backtest thoroughly and use appropriate risk management.

Safe Supertrend Strategy (No Repaint)Overview

The Safe Supertrend is a repaint-free version of the popular Supertrend trend-following indicator.

Most Supertrend indicators appear perfect on historical charts because they flip intrabar and then repaint after the candle closes.

This version fixes that by using close-of-bar confirmation only, making every trend flip 100% stable, safe, and non-repainting.

Why This Supertrend Doesn’t Repaint

Most Supertrend indicators calculate their trend direction using the current bar’s data.

But during a live candle:

ATR expands and contracts

The upper/lower bands move

Price moves above/below the band temporarily

A false flip appears → then disappears when the candle closes

That is classic repainting.

This indicator avoids all of that by using:

close > upper

close < lower

This means:

Trend direction flips only based on the previous candle,

No intrabar calculations,

No flickering signals,

No “perfect but fake” historical performance.

Every signal you see on the chart is exactly what was available in real-time.

How It Works

Calculates ATR (Average True Range) and SMA centerline

Builds upper and lower volatility bands

Confirms trend flips only after the previous bar closes

Plots clear bull and bear reversal signals

Works on all markets (crypto, stocks, forex, indices)

No repainting, no recalc, no misleading flips.

Bullish Signal (Trend Up)

A bullish trend begins only when:

The previous candle closes above the upper ATR band,

And this flip is fully confirmed.

A green triangle marks the start of a new uptrend.

Bearish Signal (Trend Down)

A bearish trend begins only when:

The previous candle closes below the lower ATR band,

And the downtrend is confirmed.

A red triangle signals the start of a new downtrend.

Inputs

ATR Length - default 10

ATR Multiplier - default 3.0

Works on all timeframes and market

Simple, but powerful.

Why Use This Version Instead of a Regular Supertrend?

Most Supertrends:

Look great historically

But repaint continuously on live charts

Give false trend flips intrabar

Cannot be reliably used in strategies

This version:

Uses strict previous-bar logic

Never repaints trend direction

Works perfectly in live trading

Backtests accurately

Is ideal for algorithmic strategies

Ideal For:

Trend-following strategies

Breakout trading

Algo trading systems

Reversal detection

Filtering market noise

Swing trading & scalping

Final Note

This is a safer, more reliable Supertrend designed for real-world use — not perfect-looking repaint illusions.

If you use Supertrend in your trading system, this no-repaint version ensures your signals are trustworthy and consistent.

Safe Supertrend Strategy (No Repaint)Overview

The Safe Supertrend is a repaint-free version of the popular Supertrend trend-following indicator.

Most Supertrend indicators appear perfect on historical charts because they flip intrabar and then repaint after the candle closes.

This version fixes that by using close-of-bar confirmation only, making every trend flip 100% stable, safe, and non-repainting.

Why This Supertrend Doesn’t Repaint

Most Supertrend indicators calculate their trend direction using the current bar’s data.

But during a live candle:

ATR expands and contracts

The upper/lower bands move

Price moves above/below the band temporarily

A false flip appears → then disappears when the candle closes

That is classic repainting.

This indicator avoids all of that by using:

close > upper

close < lower

This means:

Trend direction flips only based on the previous candle,

No intrabar calculations,

No flickering signals,

No “perfect but fake” historical performance.

Every signal you see on the chart is exactly what was available in real-time.

How It Works

Calculates ATR (Average True Range) and SMA centerline

Builds upper and lower volatility bands

Confirms trend flips only after the previous bar closes

Plots clear bull and bear reversal signals

Works on all markets (crypto, stocks, forex, indices)

No repainting, no recalc, no misleading flips.

Bullish Signal (Trend Up)

A bullish trend begins only when:

The previous candle closes above the upper ATR band,

And this flip is fully confirmed.

A green triangle marks the start of a new uptrend.

Bearish Signal (Trend Down)

A bearish trend begins only when:

The previous candle closes below the lower ATR band,

And the downtrend is confirmed.

A red triangle signals the start of a new downtrend.

Inputs

ATR Length - default 10

ATR Multiplier - default 3.0

Works on all timeframes and market

Simple, but powerful.

Why Use This Version Instead of a Regular Supertrend?

Most Supertrends:

Look great historically

But repaint continuously on live charts

Give false trend flips intrabar

Cannot be reliably used in strategies

This version:

Uses strict previous-bar logic

Never repaints trend direction

Works perfectly in live trading

Backtests accurately

Is ideal for algorithmic strategies

Ideal For:

Trend-following strategies

Breakout trading

Algo trading systems

Reversal detection

Filtering market noise

Swing trading & scalping

Final Note

This is a safer, more reliable Supertrend designed for real-world use — not perfect-looking repaint illusions.

If you use Supertrend in your trading system, this no-repaint version ensures your signals are trustworthy and consistent.

Maxtra Range Breakout StrategyRange Breakout Strategy

This strategy identifies periods of price consolidation (range) and enters trades when the price breaks above or below the defined range. A breakout above the range signals a potential uptrend (buy), while a breakout below indicates a potential downtrend (sell). It helps capture strong directional moves following low-volatility phases.

HV Spike Strategy (HVP + OR Breakout + Reversal + TP/SL Modes)Here is a script that I tried to make it simple, although it has several parameters, I will try to explain, here we go:

Logic: Open Range Breakout: otherwise knows as First Candle Rule, usually used for the first candle in the opening of a market session, in my strategy there is an option to use it even for Crypto that operate 24/7, how to do that? Simply by detecting Volatility from the HVP (Historical Volatility Percentile). Then the ORB logic kicks in and the first candle with high volatility gives the ranges for the trades. The proper HVP Activation Threshold has to be selected for each currency pair/index/crypto in order to have maximum profit.

Enter a trade: when the price goes 100% above/below the First Candle Rule Range. That way it is filtering fake breakouts. Also if the price reverses back into the range the strategy takes the opposite trade.

Exit a trade: SL/TP By percentage or ATR, selection in the input menu.

My intention is to avoid using lagging indicators or guessing of Price Action, purely Bull/Bear indication by the first candle.

I hope you find this helpful! Wishing all successful Trades!

Tight Entry Trend Engine Strategy═══════════════════════════════════════

TIGHT ENTRY TREND ENGINE

═══════════════════════════════════════

A breakout-based trend-following system designed to capture explosive

moves by entering at precise resistance/support breakouts with minimal

entry risk and massive profit potential.

⚠️ LOW WIN RATE, HIGH REWARD SYSTEM ⚠️

This is NOT a high win-rate strategy. Expect 25-35% winners, but

when it hits, winners are typically 10X+ larger than losers.

═══════════════════════════════════════

🎯 WHAT THIS SYSTEM DOES

═══════════════════════════════════════

The Tight Entry Trend Engine identifies powerful breakout opportunities

by detecting when price breaks through established trendlines with

confirmation from higher timeframe trends:

1. DYNAMIC TRENDLINE DETECTION (3 BANKS)

• Automatically draws support and resistance trendlines

• 3 separate "banks" capture short-term, medium-term, and long-term levels

• Each bank has configurable parameters (required pivot touch count,

angle limits, lengths)

2. BREAKOUT ENTRY TIMING

• Enters LONG when price breaks ABOVE resistance trendlines

• Enters SHORT when price breaks BELOW support trendlines

• Entry Alert occurs at the exact moment of breakout = "tight entry"

• Stop-loss placed just below/above the broken trendline (configurable)

3. HIGHER TIMEFRAME TREND FILTER

• Uses Hull Moving Average (HMA) on higher timeframe for trend following

• Auto-adjusts HTF based on your chart timeframe

• Optional filters prevent entries against major trend

• Optional "overextension" filter avoids buying parabolic moves

4. VOLATILITY-ADAPTIVE RISK MANAGEMENT

• Stop-loss calculated using Average True Range (ATR)

• Tighter stops = better R:R

• Profit targets adjust dynamically with volatility

• Breakeven stop moves automatically when in profit

• Extended profit targets when far from HTF trend

═══════════════════════════════════════

📊 HOW IT WORKS (METHODOLOGY)

═══════════════════════════════════════

STEP 1: TRENDLINE FORMATION

The system continuously scans for pivot highs and pivot lows to

construct trendlines. You control:

BANK 1 (Short-Term):

- Pivot Length: How many bars to look back for swing points

- Min Touches: How many pivots needed to form a line (default: 3)

- Max Length: How far back lines can reach (default: 180 bars)

- Angle Limits: Maximum steepness allowed for valid trendlines

- Tolerance: How close pivots must align to form horizontal lines

BANK 2 (Medium-Term):

- Slightly longer pivot periods for more significant levels

- Captures medium-term trend structure

- Default Max Length: 200 bars

BANK 3 (Long-Term):

- Focuses on major support/resistance zones

- Often uses horizontal levels (angled lines disabled by default)

- Default Max Length: 300 bars

The system draws RESISTANCE lines (red) above price and SUPPORT

lines (green) below price. These adapt in real-time as new pivots form.

STEP 2: BREAKOUT DETECTION

LONG SIGNALS:

- Price closes above a resistance trendline

- Higher timeframe trend is up (optional filter)

- Price not overextended from HTF trend (optional filter)

- No position currently open

SHORT SIGNALS:

- Price closes below a support trendline

- Higher timeframe trend is down (optional filter)

- Price not overextended from HTF trend (optional filter)

- No position currently open

The "tight" aspect: Because you're entering right at the trendline

break, your stop-loss can be placed very close (just below the

broken resistance for longs), creating exceptional risk/reward ratios.

STEP 3: POSITION SIZING

Choose between:

- Fixed $ Risk Per Trade: Risk same dollar amount every trade

- % Risk Per Trade: Risk percentage of current equity

Position size automatically calculated based on:

- Your risk amount

- Distance to stop-loss (ATR-based)

- Works with stocks, futures, crypto (auto-adjusts for contract multipliers)

STEP 4: EXIT MANAGEMENT

Multiple exit methods working together:

- PROFIT TARGET: Exits when profit reaches 100x your risk

- EXTENDED PROFIT: Earlier exit (80R) when very far from HTF trend

- STOP LOSS: Fixed ATR-based stop below entry

- HTF TREND EXIT: Exits when price crosses below HTF trend with profit

- BREAKEVEN PULLBACK: Exits if profit drops below 0.6R after reaching breakeven

- PARTIAL PROFITS: Optional - take partial profits at specified R-multiple

═══════════════════════════════════════

🔧 KEY COMPONENTS EXPLAINED

═══════════════════════════════════════

HULL MOVING AVERAGE (HMA)

A smoothed moving average that reduces lag compared to traditional

MAs. The system uses HMA on a higher timeframe to determine the

dominant trend direction. You can choose:

- Auto HTF: System picks appropriate HTF based on your chart timeframe

- Manual HTF: You specify the higher timeframe

AVERAGE TRUE RANGE (ATR)

Measures current market volatility. Used for:

- Stop-loss distance (tighter when volatility low)

- Profit targets (larger when volatility high)

- Position sizing (smaller positions in volatile conditions)

- Breakeven trigger distance

TRENDLINE ANGLE FILTERING

Each trendline bank has angle limits to ensure quality:

- Resistance lines: Max downward/upward slope allowed

- Support lines: Max downward/upward slope allowed

- Angles automatically adjust based on current volatility

- Prevents overly steep/unreliable trendlines

SENSITIVITY CONTROL

One master slider adjusts multiple parameters:

- Trendline detection sensitivity

- HTF MA length

- Exit timing

- Auto-adjusts for daily+ timeframes (60% increase)

═══════════════════════════════════════

⚙️ WHAT YOU SEE ON YOUR CHART

═══════════════════════════════════════

TRENDLINES:

✓ Red resistance lines above price

✓ Green support lines below price

✓ Orange broken lines (past breakouts)

✓ Lines extend to show current levels

HTF TREND:

✓ Thick colored line showing higher timeframe trend

✓ Color gradient: Red (bearish) → Orange → Yellow → Green (bullish)

✓ 250-bar smoothed curve for visual clarity

ENTRY/EXIT SIGNALS:

✓ Small green dot below bar = Long entry

✓ Small red dot above bar = Short entry

✓ Small red dot above = Long exit

✓ Small black dot below = Short exit

OPTIONAL DETAILED LABELS:

✓ Bank number that triggered entry (Bank 1, 2, or 3)

✓ Exit reason (Profit Target, Stop Loss, HTF Exit, etc.)

✓ Partial profit notifications

POSITION TRACKING:

✓ Yellow dashed line at entry price (extends right)

✓ Green/red fill showing current profit/loss zone

✓ Lime arrows at top = Currently in long position

✓ Red arrows at bottom = Currently in short position

✓ Gray background = No position (flat)

STATS TABLE (Top Right):

✓ Current position (LONG/SHORT/FLAT)

✓ Risk per trade ($ or %)

✓ Entry price

✓ Unrealized P/L in dollars

✓ P/L in R-multiples (how many R's profit/loss)

✓ Average winner/loser R ($ mode) OR CAGR (% mode)

═══════════════════════════════════════

📈 OPTIMAL USAGE

═══════════════════════════════════════

BEST ASSETS:

- NASDAQ:QQQ on 1-hour (reg) chart ⭐ (PRIMARY OPTIMIZATION)

- Strong trending stocks: NVDA, AAPL, TSLA, MSFT, GOOGL, AMZN

- High volatility tech stocks

- Crypto: BTC, ETH

- Any liquid asset with clear trends and momentum (GOLD)

AVOID:

- Low volatility stocks

- Ranging/choppy markets

- Penny stocks or illiquid assets

- Assets without clear directional movement

BEST TIMEFRAMES:

- PRIMARY: 1-hour charts (optimal for QQQ)

- ALSO EXCELLENT: 2H, 4H, 8H

- WORKS: 15min, 30min (only momentum leaders, more noise)

- WORKS WITH ADJUSTMENTS: 1D, 2D (decrease trendline pivot lengths)

═══════════════════════════════════════

📊 BACKTEST RESULTS (QQQ 1H (Reg hours), 1999-2024)

═══════════════════════════════════════

The system showed on NASDAQ:QQQ 1-hour timeframe (regular hours):

- Total Return: 1,100,000%+ over 24 years

- Total Trades: 500+

- Win Rate: ~20-24% (LOW - this is by design!)

- Average Winner: 8-15% gain

- Average Loser: 2-4% loss

- Win/Loss Ratio: 10:1 (winners much bigger than losers)

- Profit Factor: 3+

- Max Drawdown: 45-50%

- Risk per trade: 3% of capital

KEY INSIGHT: This is a LOW WIN RATE, HIGH REWARD system. You will

lose more trades than you win, but the few winners are so large

they more than compensate for many small losses.

IMPORTANT: These are backtested results using optimal parameters

on historical data. Real trading results will vary based on:

- Your execution and timing

- Slippage and commissions

- Your emotional discipline

- Market conditions during your trading period

═══════════════════════════════════════

🎓 WHO IS THIS FOR?

═══════════════════════════════════════

IDEAL FOR:

✓ Swing traders comfortable holding winners for longer period

✓ Part-time traders (1H = check 2-3x per day)

✓ Traders seeking exceptional risk/reward ratios

✓ Those comfortable with low win rates if winners are huge

✓ Technical analysis enthusiasts

✓ Breakout traders

✓ Trend followers

═══════════════════════════════════════

🚀 GETTING STARTED - STEP BY STEP

═══════════════════════════════════════

STEP 1: APPLY TO YOUR CHART

- Search "Tight Entry Trend Engine" in indicators

- Click to apply to your chart

- Trendlines and HTF line will appear immediately

STEP 2: CHOOSE YOUR SETTINGS

For BEGINNERS - Use These Settings First:

1. Trade Direction & Filters:

• ENABLE LONGS: ✓ ON

• ENABLE SHORTS: ✗ OFF (start with longs only)

• Sensitivity: 1.0 (default)

• HTF Trend Entry Filter: ✓ ON (safer entries)

• Block Entries When Overextended: ✓ ON (avoid parabolic tops)

2. Position Sizing & Risk:

• Position Sizing: "Per Risk"

• RISK Type: "$ Per Trade"

• Risk Amount: $200 (or 1-3% of your account)

3. Visual Settings:

• Show Support Lines: ✗ OFF (unless trading shorts)

• Show Detailed Entry/Exit Labels: ✓ ON

• Show Stats Table: ✓ ON

• Show Entry Line & P/L Fill: ✓ ON

4. Leave everything else at DEFAULT for now

STEP 3: UNDERSTAND WHAT YOU SEE

When trendlines appear:

- RED lines above = Resistance (watch for price breaking UP through these)

- GREEN lines below = Support (watch for price breaking DOWN)

- When price breaks a red line = Potential LONG entry

- When price breaks a green line = Potential SHORT entry

The HTF trend line (thick colored):

- Green/lime = Strong uptrend (favorable for longs)

- Red = Strong downtrend (favorable for shorts if enabled)

- Orange/yellow = Transitioning

STEP 4: OBSERVE SIGNALS

- Small GREEN dot below bar = System entered LONG

- Small RED dot above bar = System exited LONG

- Check the label to see which "Bank" triggered (Bank 1, 2, or 3)

- Watch the yellow entry line and colored fill show your P/L

STEP 5: PAPER TRADE FIRST

- Use TradingView's paper trading feature

- Watch how signals perform on YOUR chosen asset

- Understand the win rate will be LOW (20-35%)

- Verify that winners are indeed much larger than losers

- Test for at least 20-30 signals before going live

STEP 6: OPTIMIZE FOR YOUR ASSET (OPTIONAL)

If default settings aren't working well:

For FASTER signals (more trades):

- Reduce Pivot Length 1 to 3-4

- Reduce Max Length 1 to 120-150

- Increase Sensitivity to 1.2-1.5

For SLOWER signals (higher quality):

- Increase Pivot Length 1 to 7-10

- Increase Max Length 1 to 250+

- Decrease Sensitivity to 0.7-0.9

For DAILY timeframes:

- Increase all Pivot Lengths by 30-50%

- Increase all Max Lengths significantly

- Sensitivity: 0.6-0.8

═══════════════════════════════════════

⚙️ ADVANCED SETTINGS EXPLAINED

═══════════════════════════════════════

TRENDLINE BANK SETTINGS:

Each bank (1, 2, 3) has these parameters:

- Min Touches: Minimum pivots to form a line

- Lower (2) = More lines, earlier detection

- Higher (4+) = Fewer lines, higher quality

- Pivot Length: Lookback for swing points

- Lower (3-5) = Reacts to recent price action

- Higher (10+) = Only major swing points

- Max Length: How old a trendline can be

- Shorter (100-150) = Only recent lines

- Longer (300+) = Include historical levels

- Tolerance: Alignment strictness for horizontal lines

- Lower (3.0-3.5) = Very strict horizontal

- Higher (4.5+) = More forgiving alignment

- Allow Angled Lines: Enable diagonal trendlines

- ON = Catches sloped support/resistance

- OFF = Only horizontal levels

- Angle Limits: Maximum steepness allowed

- Lower (1-2) = Only gentle slopes

- Higher (4-6) = Accept steeper angles

- Automatically adjusts for volatility

ATR MULTIPLIERS:

- STOP LOSS ATR (0.6): Distance to stop-loss

- Lower (0.4-0.5) = Tighter stops, stopped out more

- Higher (0.8-1.0) = Wider stops, more room

- PROFIT TARGET ATR (100): Main profit target

- This is 100x your risk = 10,000% R:R

- Lower (50-80) = Take profits sooner

- Higher (120+) = Let winners run longer

- BREAKEVEN ATR (40): When to move stop to breakeven

- Lower (20-30) = Protect profits earlier

- Higher (60+) = Give more room before protecting

HIGHER TIMEFRAME:

- Auto HTF: Automatically selects appropriate HTF

- 5min chart → uses 2H

- 15-30min → uses 6H

- 1-4H → uses 2D

- Daily → uses 4D

- HTF MA Length (300): HMA period for trend

- Lower (150-250) = More responsive

- Higher (400-500) = Smoother, less whipsaw

- HTF Trend Following Exit: Exits when crossing HTF

- ON = Additional exit method

- OFF = Rely only on profit targets/stops

- HTF Trend Entry Filter: Only trade with HTF trend

- ON = Safer, fewer signals

- OFF = More aggressive, more signals

- Block Entries When Overextended: Prevents chasing

- ON = Avoids parabolic tops/bottoms

- OFF = Enter all breakouts regardless

═══════════════════════════════════════

💡 TRADING PHILOSOPHY & EXPECTATIONS

═══════════════════════════════════════

This system is built on one core principle:

"ACCEPT SMALL, FREQUENT LOSSES TO CAPTURE RARE, MASSIVE WINS"

What this means:

- You WILL lose 65%-75% of your trades

- Most losses will be small (1-2R)

- Some winners hit 80R+

- Over time, math works in your favour

Trend-Following & Breakout — Index Quant Strategy (NASDAQ)📈 Trend-Following & Breakout — Index Quant Strategy (NASDAQ & S&P 500)

Type: Invite-only strategy

Markets: NASDAQ 100 (NAS100 / US100 / NQ), S&P 500 (US500 / SPX), and other major equity indices.

🧠 Concept: Continuous trend model combining EWMAC (trend-following) and Donchian (breakout) signals, scaled by forecast strength and portfolio risk.

⚙️ Execution: Rebalances only on decision-bar closes, using hysteresis and a no-trade band to reduce churn.

📊 Default bias: Long-only — aligned with equity index drift.

🧩 How it works

• EWMAC Trend: Difference between fast and slow EMAs, normalized by an EWMA of absolute returns.

• Donchian Breakout: Distance beyond a 200-bar channel (Strict mode) or relative z-score position within it.

• Forecast combination: Weighted sum of trend and breakout points, clamped to ± capPoints.

• Hysteresis: Prevents quick sign flips near zero forecast.

• Risk scaling: Maps forecast strength to position size using equity × risk budget × ATR-based stop distance.

• Rebalance: Executes only if the required quantity change exceeds the Δqty threshold; can optionally block increases on Sundays (for CFDs).

⚙️ Default parameters

Deployed on NQ / US100 / NAS100 on Daily Timeframe

• Decision timeframe = 360 min (other options from 1 min to 1 week).

• Trend (EWMAC): Fast = 64, Slow = 256, Vol Norm = 32, Weight = 0.8.

• Breakout (Donchian): Length = 200, Mode = Strict, Weight = 0.2.

• Forecast scaling: ptsPerSigma = 1.0, capPoints = 10.

• Risk % per rebalance = 4 % of equity.

• ATR stop: ATR(14) × 1.0.

• No-trade band (Δqty) = 4 units.

• Hysteresis = 2 forecast points.

• Bias = Long-only (Neutral / Long-bias 50 % optional).

• Skip Sunday increases = false (default).

📋 Backtest properties (documented)

• Initial capital = 100 000 USD.

• Commission = 0.20 % per trade.

• Pyramiding = 10.

• Calc on every tick = false.

• Point value = 1 (for NAS100 CFD).

• No financing or slippage modeled.

• If using CFDs, account for overnight funding.

• On futures (NQ / ES), carry is implicit.

📊 Typical behaviour

• Many small scratches, a few large winners.

• Performs best during multi-week / multi-month trends.

• Underperforms in tight or volatile ranges.

• Average hold ≈ 30 – 90 days in historical tests.

💡 Risk and performance guide (illustrative)

Sharpe ≈ 1.25

Sortino ≈ 1.10 – 1.30

Max drawdown ≈ –18 % to –25 %

Annual volatility ≈ 24 – 28 %

CAGR ≈ 50 – 60 % (at 4 % risk)

Edge ratio ≈ 5 (MFE / MAE)

Historical backtests only — past performance does not guarantee future results.

🌍 Intended markets and timeframes

Optimized for NASDAQ 100 and S&P 500; also effective on similar indices (DAX, Dow Jones, FTSE).

Best on Daily or higher timeframes.

Aligns with long-term index drift — suitable for long-bias systematic trend portfolios.

⚠️ Limitations

• Backtests exclude CFD funding costs.

• Trend models will have losing streaks in range-bound markets.

• Designed for experienced traders seeking systematic exposure.

🔑 Requesting access

Send a private TradingView message to with the text:

“Request access to Trend-Following & Breakout — Index Quant Strategy.”

Access is granted only on explicit request.

For further information, see my TradingView Signature.

🆕 Release notes (v1.0)

• Initial release (360 min TF): EWMAC 64/256 + Donchian 200 Strict.

• Risk 4 %, ATR × 1.0, Long-only bias, hysteresis 2 pts, Δqty ≥ 4.

• Developed for NASDAQ 100 and S&P 500 indices.

• Implements continuous risk-scaled positioning and no-trade band logic.

🧾 Originality statement

This strategy is original work built entirely from TradingView built-ins (EMA, ATR, Highest, Lowest).

It does not reuse open-source invite-only code.

Any future reuse of open scripts will be done with explicit permission and credit.

Universal Breakout Strategy [KedArc Quant]Description:

A flexible breakout framework where you can test different logics (Prev Day, Bollinger, Volume, ATR, EMA Trend, RSI Confirm, Candle Confirm, Time Filter) under one system.

Choose your breakout mode, and the strategy will handle entries, exits, and optional risk management (ATR stops, take-profits, daily loss guard, cooldowns).

An on-chart info table shows live mode values (like Prev High/Low, Bollinger levels, RSI, etc.) plus P&L stats for quick analysis.

Use it to compare which breakout style works best on your instrument and timeframe, whether intraday, swing, or positional trading

🔑 Why it’s useful

* Flexibility: Switch between breakout strategies without loading different indicators.

* Clarity: On-chart info table displays current mode, relevant indicator levels, and live strategy P&L stats.

* Testing efficiency: Quickly A/B test different breakout styles under the same backtest environment.

* Transparency: Every trade is rule-based and displayed with entry/exit markers.

🚀 How it helps traders

* Lets you experiment with breakout strategies quickly without loading multiple scripts.

* Helps identify which breakout method fits your instrument & timeframe.

* Gives clear on-chart visual + statistical feedback for confident decision-making.

⚙️ Input Configuration

* Breakout Mode → choose which strategy to test:

* *Prev Day* → breakouts of yesterday’s High/Low.

* *Bollinger* → Upper/Lower BB pierce.

* *Volume* → Breakout confirmed with volume above average.

* *ATR Stop* → Wide range breakout using ATR filter.

* *Time Filter* → Breakouts inside defined session hours.

* *EMA Trend* → Breakouts only in EMA fast > slow alignment.

* *RSI Confirm* → Breakouts with RSI confirmation (e.g. >55 for longs).

* *Candle Confirm* → Breakouts validated by bullish/bearish candle.

* Lookback / ATR / Bollinger inputs → adjust sensitivity.

* Intrabar mode → option to evaluate breakouts using bar highs/lows instead of closes.

* Table options → show/hide info table, show/hide P&L stats, choose corner placement.

📈 Entry & Exit Logic

* Entry → occurs when breakout condition of chosen mode is met.

* Exit → default exits via opposite signals or optional stop/target if enabled.

* Session filter → optional auto-flat at session end.

* P&L management → optional daily loss guard, cooldown between trades, and ATR-based stop/take profit.

❓ FAQ — Choosing the best setup

Q: Which strategy should I use for which chart?

* *Prev Day Breakouts*: Best on indices, FX, and liquid futures with strong daily levels.

* *Bollinger*: Works well in range-bound environments, or crypto pairs with volatility compression.

* *Volume*: Good on equities where breakout strength is tied to volume spikes.

* *ATR Stop*: Suits volatile instruments (commodities, crypto).

* *EMA Trend*: Useful in trending markets (stocks, indices).

* *RSI Confirm*: Adds momentum filter, better for swing trades.

* *Candle Confirm*: Ideal for scalpers needing visual confirmation.

* *Time Filter*: For intraday traders who want signals only in high-liquidity sessions.

Q: What timeframe should I use?

* Intraday traders → 5m to 15m (Time Filter, Candle Confirm).

* Swing traders → 1H to 4H (EMA Trend, RSI Confirm, ATR Stop).

* Position traders → Daily (Prev Day, Bollinger).

* Breakout

A trade entry condition triggered when price crosses above a resistance level (for longs) or below a support level (for shorts).

* Prev Day High/Low

Formula:

Prev High = High of (Day )

Prev Low = Low of (Day )

* Bollinger Bands

Formula:

Basis = SMA(Close, Length)

Upper Band = Basis + (Multiplier × StdDev(Close, Length))

Lower Band = Basis – (Multiplier × StdDev(Close, Length))

* Volume Confirmation

A breakout is only valid if:

Volume > SMA(Volume, Length)

* ATR (Average True Range)

Measures volatility.

Formula:

ATR = SMA(True Range, Length)

where True Range = max(High–Low, |High–Close |, |Low–Close |)

* EMA (Exponential Moving Average)

Weighted moving average giving more weight to recent prices.

Formula:

EMA = (Price × α) + (EMA × (1–α))

with α = 2 / (Length + 1)

* RSI (Relative Strength Index)

Momentum oscillator scaled 0–100.

Formula:

RSI = 100 – (100 / (1 + RS))

where RS = Avg(Gain, Length) ÷ Avg(Loss, Length)

* Candle Confirmation

Bullish candle: Close > Open AND Close > Close

Bearish candle: Close < Open AND Close < Close

Win Rate (%)

Formula:

Win Rate = (Winning Trades ÷ Total Trades) × 100

* Average Trade P&L

Formula:

Avg Trade = Net Profit ÷ Total Trades

📊 Performance Notes

The Universal Breakout Strategy is designed as a framework rather than a single-asset optimized system. Results will vary depending on the chart, timeframe, and asset chosen.

On the current defaults (15-minute, INR-denominated example), the backtest produced 132 trades over the selected period. This provides a statistically sufficient sample size.

Win rate (~35%) is relatively low, but this is balanced by a positive reward-to-risk ratio (~1.8). In practice, a lower win rate with larger wins versus smaller losses is sustainable.

The average P&L per trade is close to breakeven under default settings. This is expected, as the strategy is not tuned for a single symbol but offered as a universal breakout framework.

Commissions (0.1%) and slippage (1 tick) are included in the simulation, ensuring realistic conditions.

Risk management is conservative, with order sizing set at 1 unit per trade. This avoids over-leveraging and keeps exposure well under the 5-10% equity risk guideline.

👉 Traders are encouraged to:

Experiment with inputs such as ATR period, breakout length, or Bollinger parameters.

Test across different timeframes and instruments (equities, futures, forex, crypto) to find optimal setups.

Combine with filters (trend direction, volatility regimes, or volume conditions) for further refinement.

⚠️ Disclaimer This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Nirvana True Duel전략 이름

열반의 진검승부 (영문: Nirvana True Duel)

컨셉과 철학

“열반의 진검승부”는 시장 소음은 무시하고, 확실할 때만 진입하는 전략입니다.

EMA 리본으로 추세 방향을 확인하고, 볼린저 밴드 수축/확장으로 변동성 돌파를 포착하며, OBV로 거래량 확인을 통해 가짜 돌파를 필터링합니다.

전략 로직

매수 조건 (롱)

20EMA > 50EMA (상승 추세)

밴드폭 수축 후 확장 시작

종가가 상단 밴드 돌파

OBV 상승 흐름 유지

매도 조건 (숏)

20EMA < 50EMA (하락 추세)

밴드폭 수축 후 확장 시작

종가가 하단 밴드 이탈

OBV 하락 흐름 유지

진입·청산

손절: ATR × 1.5 배수

익절: 손절폭의 1.5~2배에서 부분 청산

시간 청산: 설정한 최대 보유 봉수 초과 시 강제 청산

장점

✅ 추세·변동성·거래량 3중 필터 → 노이즈 최소화

✅ 백테스트·알람 지원 → 기계적 매매 가능

✅ 5분/15분 차트에 적합 → 단타/스윙 트레이딩 활용 가능

주의점

⚠ 횡보장에서는 신호가 적거나 실패 가능

⚠ 수수료·슬리피지 고려 필요

📜 Nirvana True Duel — Strategy Description (English)

Name:

Nirvana True Duel (a.k.a. Nirvana Cross)

Concept & Philosophy

The “Nirvana True Duel” strategy focuses on trading only meaningful breakouts and avoiding unnecessary noise.

Nirvana: A calm, patient state — waiting for the right opportunity without emotional trading.

True Duel: When the signal appears, enter decisively and let the market reveal the outcome.

In short: “Ignore market noise, trade only high-probability breakouts.”

🧩 Strategy Components

Trend Filter (EMA Ribbon): Stay aligned with the main market trend.

Volatility Squeeze (Bollinger Band): Detect volatility contraction & expansion to catch explosive moves early.

Volume Confirmation (OBV): Filter out false breakouts by confirming with volume flow.

⚔️ Entry & Exit Conditions

Long Setup:

20 EMA > 50 EMA (uptrend)

BB width breaks out from recent squeeze

Close > Upper Bollinger Band

OBV shows positive flow

Short Setup:

20 EMA < 50 EMA (downtrend)

BB width breaks out from recent squeeze

Close < Lower Bollinger Band

OBV shows negative flow

Risk Management:

Stop Loss: ATR × 1.5 below/above entry

Take Profit: 1.5–2× stop distance, partial take-profit allowed

Time Stop: Automatically closes after max bars held (e.g. 8h on 5m chart)

✅ Strengths

Triple Filtering: Trend + Volatility + Volume → fewer false signals

Mechanical & Backtestable: Ideal for objective trading & performance validation

Adaptable: Works well on Bitcoin, Nasdaq futures, and other high-volatility markets (5m/15m)

⚠️ Things to Note

Low signal frequency or higher failure rate in sideways/range markets

Commission & slippage should be factored in, especially on lower timeframes

ATR multiplier and R:R ratio should be optimized per asset

Tristan's Box: Pre-Market Range Breakout + RetestMarket Context:

This is designed for U.S. stocks, focusing on pre-market price action (4:00–9:30 AM ET) to identify key support/resistance levels before the regular session opens.

Built for 1 min and 5 min timelines, and is intended for day trading / scalping.

Core Idea:

Pre-market range (high/low) often acts as a magnet for price during regular hours.

The first breakout outside this range signals potential strong momentum in that direction.

Retest of the breakout level confirms whether the breakout is valid, avoiding false moves.

Step-by-Step Logic:

Pre-Market Range Identification:

Track high and low from 4:00–9:30 AM ET.

Draw a box spanning this range for visual reference and calculation.

Breakout Detection:

When the first candle closes above the pre-market high → long breakout.

When the first candle closes below the pre-market low → short breakout.

The first breakout candle is highlighted with a “YOLO” label for visual confirmation.

Retest Confirmation:

Identify the first candle whose wick touches the pre-market box (high touches top for short, low touches bottom for long).

Wait for the next candle: if it closes outside the box, it confirms the breakout.

Entry Execution:

Long entry: on the confirming candle after a wick-touch above the pre-market high.

Short entry: on the confirming candle after a wick-touch below the pre-market low.

Only the first valid entry per direction per day is taken.

Visuals & Alerts:

Box represents pre-market high/low.

Top/bottom box border lines show the pre-market high / low levels cleanly.

BUY/SELL markers are pinned to the confirming candle.

Added a "YOLO" marker on breakout candle.

Alert conditions trigger when a breakout is confirmed by the retest.

Strategy Type:

Momentum breakout strategy with confirmation retest.

Combines pre-market structure and risk-managed entries.

Designed to filter false breakouts by requiring confirmation on the candle after the wick-touch.

In short, it’s a pre-market breakout momentum strategy: it uses the pre-market high/low as reference, waits for a breakout, and then enters only after a confirmation retest, reducing the chance of entering on a false spike.

Always use good risk management.

ORB FVG Strategy with telegram V6.1Summary

Intraday NY-session strategy with Opening-Range bias (09:30–10:00 NY), FVG entries (incl. optional HTF FVGs), momentum filters (LinReg slope & Williams %R), limit entries inside the zone, SL from FVG anchors, and TP via risk-reward. Includes session/trade caps, pending-order handling, auto-cancel at NY time, and optional Telegram webhook alerts.

Feature Overview

Opening Range & Bias: OR high/low built until 10:00 NY, then frozen. Bias from confirmed 5-minute candles (modes: Body Close, Complete Candle, Wick Only).

FVG Scanner: Bull/bear FVGs (choose wick or body gaps), min size, auto-extend, mitigation cleanup (touch or 50%).

HTF FVG (10 min): Optional – displayed after ≥ 2 consecutive FVGs; cleans up on touch/50%.

Entry/SL/TP: Entry at X% fill (+extra %) within the FVG; SL from FVG candle / FVG-1 / FVG-2 (smart) + buffer; TP via risk-reward.

Momentum Filters: LinReg slope (MLL) + Williams %R with threshold/slope filters (individually switchable).

Intrabar Mode (optional): Immediate Open/intrabar entry on touch (calc_on_every_tick=true) or classic bar-close confirmation (toggle).

Trade Management: Max trades/day, pending cap, auto-cancel at defined NY time, pause after first winner (optional).

Telegram: Programmatic alerts via alert() with Telegram-ready JSON payload.

Parameters (compact)

Group Parameter Purpose

Sessions Trading session, Opening range Trading/OR window (internal NY TZ)

Bias Body Close / Complete Candle / Wick Only Bias confirmation relative to OR

Liquidity LQ session, lookback days, cleanup points, show lines Intraday liquidity marks & cleanup

FVG Min size, wick/body, colors, extend, cleanup Detection/visualization & validity

HTF FVG (10 m) Toggle/Display/Colors Conservative HTF filter/POI

Entry Fill %, extra %, max pending, validity (bars), cancel time, intrabar switch Execution timing, order caps, auto-cancel

Stop Loss Source: Candle / -1 / -2 (smart), buffer (points) SL anchor from FVG history + safety offset

Take Profit Risk-Reward (R:R) Target calculation

Momentum LinReg length/min slope, W%R length/min slope, HUD Trend/momentum filters

Trade Mgmt Max trades/day, pause after win Daily cap / risk cooldown

Telegram Enabled, tester, interval, channel id Webhook output & test signals

Debug & Info Debug panel, rejection reasons On-chart status/diagnostics

Alerts / Telegram Webhook (Quick Setup)

Create an alert with Condition: “Any alert() function call”.

Webhook URL: api.telegram.org

Message: leave empty (the strategy provides JSON via alert() – includes chat_id, parse_mode, text).

Ensure your bot can post to the channel and the chat_id is valid.

Repainting & Backtesting

HTF series via lookahead_off on closed higher-TF candles; FVG detection on confirmed bars (barstate.isconfirmed).

Intrabar/Open entries allow earlier fills but typically cause differences between backtest and live (tick granularity/slippage, limit touch on bar OHLC).

For reproducibility, trade without intrabar (bar-close only).

Limitations

No full tick simulation; limit fills rely on bar OHLC.

Liquidity “cleanup” is rule-based (not an orderbook).

Telegram depends on correct webhook configuration.

Tips

Timeframes: M5 (intrabar)

Start with modest R:R (e.g., 1.5–2.0) and tune filters carefully.

Disclaimer

No financial advice. Past results do not guarantee future performance. Use responsibly and follow Public Library rules.

License / Credits

© 2025 Lean Trading (Lennart Pomreinke). License: MPL-2.0.

Changelog

V06.1: Intrabar switch (Open/intrabar vs bar-close), Telegram sanitizer & tester, HTF-FVG cleanup, refined pending/cancel logic, debug panel (status & rejections).

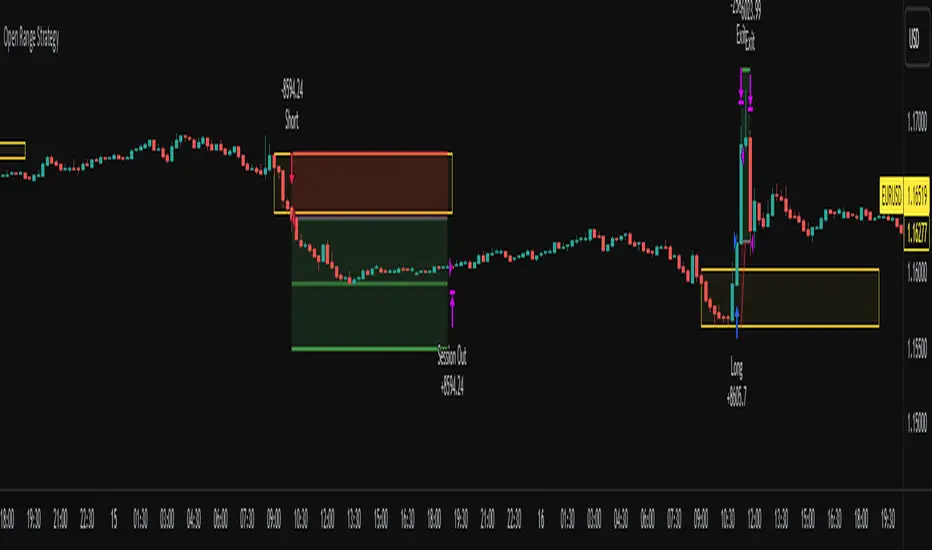

Open Range Breakout Strategy With Multi TakeProfitHello everyone,

For a while, I’ve been wanting to develop new scripts, but I couldn’t decide what to create. Eventually, I came up with the idea of coding traditional and well-known trading strategies—while adding modern features such as multi–take profit options. For the first strategy in this series, I chose the Open Range Strategy .

For those unfamiliar with it, the Open Range Strategy is a trading approach where you define a specific time period at the beginning of a trading session—such as the first 15 minutes, 30 minutes, or 1 hour—and mark the highest and lowest prices within that range. These levels then act as reference points for potential breakouts: if the price breaks above the range, it may signal a long entry; if it breaks below, it may indicate a short entry. This method is popular among day traders for capturing early momentum in the market.

Since this strategy is generally used as an intraday strategy , I added a Trade Session feature. This allows you to define the exact time window during which trades can be opened. Once the session ends, all positions are automatically closed, ensuring trades remain within your chosen intraday period.

Even though it’s a relatively simple concept, I’ve come across many different variations of it. That’s why I created a highly customizable project. Under the Session Settings, you can select the time window you want to define as your range. Whether it’s the first 15-minute candle or the entire first hour, the choice is entirely yours.

For stop-loss placement, there are two different options:

Middle of the Range – The stop loss is placed at the midpoint between the high and low of the defined range, offering a balanced buffer for both bullish and bearish setups.

Top/Bottom of the Range – The stop loss is placed just beyond the range’s high for short trades or just below the range’s low for long trades, providing a more conservative risk approach.

I’ve always been a big fan of the multi take-profit feature, so I added two different take-profit targets to this project. Take profits are calculated based on a Risk-to-Reward Ratio, which you can adjust in the settings. You can also set different position sizes for each target, allowing you to scale out of trades in a way that suits your strategy.

The result is a flexible, user-friendly strategy script that brings together a classic approach with modern risk management tools—ready to be tailored to your trading style

CP Strat ORBnew york opening range breakout and retest allows you to enter a trade with a better clarity if the price comes back and retest the range

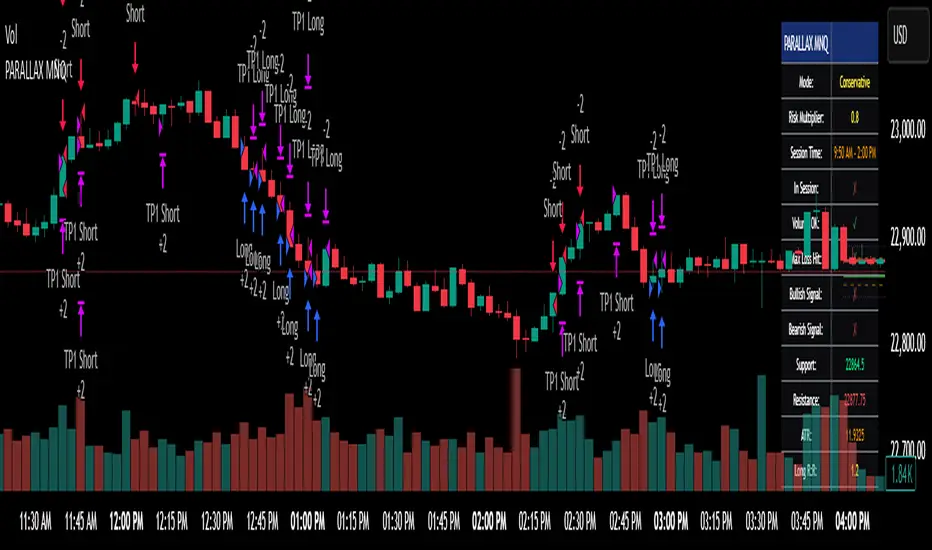

Parallax Momentum MNQ Strategy# 📈 Parallax Momentum MNQ Strategy

## Overview

The Parallax Momentum MNQ Strategy is a sophisticated support/resistance breakout system specifically designed for Micro Nasdaq futures (MNQ) trading (also works on minis). This strategy combines dynamic level detection with momentum confirmation to identify high-probability entry opportunities while maintaining strict risk management protocols.

## 🎯 Key Features

### Core Strategy Logic

- **Dynamic Support/Resistance Detection**: Automatically identifies key levels using configurable lookback periods

- **Momentum Confirmation**: Volume-based filtering ensures trades align with market momentum

- **ATR-Based Risk Management**: Adaptive stop losses and take profits based on market volatility

- **Dual Entry System**: Both long and short opportunities with limit order execution

### Risk Management

- **ATR-Adaptive Stops**: Stop losses and take profits automatically adjust to market volatility

- **Reward-to-Risk Ratios**: Configurable R:R ratios with default 2:1 minimum

- **Maximum Loss Protection**: Optional daily loss limits to prevent overtrading

- **Session Time Filtering**: Trade only during specified market hours

### Strategy Modes

- **Conservative Mode**: 0.8x risk multiplier for cautious trading

- **Balanced Mode**: Standard 1.0x risk multiplier (default)

- **Aggressive Mode**: 1.2x risk multiplier for active trading

## 📊 Visual Features

### Dashboard Display

- Real-time strategy status and performance metrics

- Current support/resistance levels and ATR values

- Live risk-to-reward ratios for potential trades

- Win rate, profit factor, and drawdown statistics

- Adjustable dashboard size and positioning

### Chart Indicators

- Support and resistance lines with labels

- ATR-based levels (+/-1 ATR and +/-2 ATR)

- Dynamic visual updates as levels change

- Configurable line extensions and styling

## ⚙️ Configuration Options

### Entry Filters

- **Volume Filter**: Optional volume confirmation above SMA

- **Session Time Filter**: 12-hour format time restrictions

- **ATR vs Fixed Stops**: Choose between adaptive or fixed tick-based exits

### Risk Controls

- **ATR Period**: Default 14-period ATR calculation

- **Stop Loss Multiplier**: ATR-based stop distance (default 1.5x)

- **Take Profit Multiplier**: ATR-based target distance (default 1.5x)

- **Secondary Take Profit**: Optional TP2 with position scaling

## 📋 How It Works

### Entry Conditions

**Long Trades**: Triggered when price closes above support buffer but low touches support level, with volume and session confirmation

**Short Trades**: Triggered when price closes below resistance buffer but high touches resistance level, with volume and session confirmation

### Exit Strategy

- **Primary Take Profit**: ATR-based target with 2:1 R:R minimum

- **Stop Loss**: ATR-based protective stop

- **Optional TP2**: Extended target for partial profit taking

- **One Trade at a Time**: No overlapping positions

## 🎛️ Default Settings

- **Lookback Period**: 20 bars for support/resistance detection

- **ATR Period**: 14 bars for volatility calculation

- **Stop Loss**: 1.5x ATR from entry

- **Take Profit**: 1.5x ATR with 2:1 reward-to-risk ratio

- **Session**: 7:30 AM - 2:00 PM (configurable)

## ⚠️ Important Notes

### Risk Disclaimer

- This strategy is for educational and informational purposes only

- Past performance does not guarantee future results

- Always use proper position sizing and risk management

- Test thoroughly on historical data before live trading

- Consider market conditions and volatility when using

### Best Practices

- Backtest on sufficient historical data

- Start with conservative mode for new users

- Monitor performance regularly and adjust parameters as needed

- Use appropriate position sizing for your account

- Consider broker commissions and slippage in live trading

## 🔧 Customization

The strategy offers extensive customization options including:

- Adjustable time sessions with AM/PM format

- Configurable ATR and risk parameters

- Optional maximum daily loss limits

- Dashboard size and position controls

- Visual element toggles and styling

## 📈 Ideal For

- MNQ (Micro Nasdaq) futures traders

- Intraday momentum strategies

- Traders seeking systematic entry/exit rules

- Risk-conscious traders wanting automated stops

- Both beginner and experienced algorithmic traders

---

**Version**: Pine Script v5 Compatible

**Timeframe**: Works on multiple timeframes (test on 1m, 3m, 5m, 15m)

**Market**: Optimized for MNQ but adaptable to other instruments

**Strategy Type**: Trend following with momentum confirmation

PHANTOM STRIKE Z-4 [ApexLegion]Phantom Strike Z-4

STRATEGY OVERVIEW

This strategy represents an analytical framework using 6 detection systems that analyze distinct market dimensions through adaptive timeframe optimization. Each system targets specific market inefficiencies - automated parameter adjustment, market condition filtering, phantom strike pattern detection, SR exit management, order block identification, and volatility-aware risk management - with results processed through a multi-component scoring calculation that determines signal generation and position management decisions.

SYSTEM ARCHITECTURE PHILOSOPHY

Phantom Strike Z-4 operates through 12 distinct parameter groups encompassing individual settings that allow detailed customization for different trading environments. The strategy employs modular design principles where each analytical component functions independently while contributing to unified decision-making protocols. This architecture enables traders to engage with structured market analysis through intuitive configuration options while the underlying algorithms handle complex computational processes.

The framework approaches certain aspects differently from static trading approaches by implementing real-time parameter adjustment based on timeframe characteristics, market volatility conditions, news event detection, and weekend gap analysis. During low-volatility periods where traditional strategies struggle to generate meaningful returns, Z-4's adaptive systems identify micro-opportunities through formation analysis and systematic patience protocols.

🔍WHY THESE CUSTOM SYSTEMS WERE INDEPENDENTLY DEVELOPED

The strategy approaches certain aspects differently from traditional indicator combinations through systematic development of original analytical approaches:

# 1. Auto Timeframe Optimization Module (ATOM)

Problem Identification: Standard strategies use fixed parameters regardless of timeframe characteristics, leading to over-optimization on specific timeframes and reduced effectiveness when market conditions change between different time intervals. Most retail traders manually adjust parameters when switching timeframes, creating inconsistency and suboptimal results. Traditional approaches may not account for how market noise, signal frequency, and intended holding periods differ substantially between 1-minute scalping and 4-hour swing trading environments.

Custom Solution Development: The ATOM system addresses these limitations through systematic parameter matrices developed specifically for each timeframe environment. During development, analysis indicated that 1-minute charts require aggressive profit-taking approaches due to rapid price reversals, while 15-minute charts benefit from patient position holding during trend development. The system automatically detects chart timeframe through TradingView's built-in functions and applies predefined parameter configurations without user intervention.

Timeframe-Specific Adaptations:

For ultra-short timeframe trading (1-minute charts), the system recognizes that market noise dominates price action, requiring tight stop losses (1.0%) and rapid profit realization (25% at TP1, 35% at TP2, 40% at TP3). Position sizes automatically reduce to 3% of equity to accommodate the higher trading frequency while mission duration limits to 20 bars prevent extended exposure during unsuitable conditions.

Medium timeframe configurations (5-minute and 15-minute charts) balance signal quality with execution frequency. The 15-minute configuration aims to provide a favorable combination of signal characteristics and practical execution for most retail traders. Formation thresholds increase to 2.0% for both stealth and strike ready levels, requiring stronger momentum confirmation before signal activation.

Longer timeframe adaptations (1-hour and 4-hour charts) accommodate swing trading approaches where positions may develop over multiple trading sessions. Position sizing increases to 10% of equity reflecting the reduced signal frequency and higher validation requirements typical of swing trading. Take profit targets extend considerably (TP1: 2.0%, TP2: 4.0%, TP3: 8.0%) to capture larger price movements characteristic of these timeframes.

# 2. Market Condition Filtering System (MCFS)

Problem Identification: Existing volatility filters use simple ATR calculations that may not distinguish between trending volatility and chaotic noise, potentially affecting signal quality during news events, market transitions, and unusual trading sessions. Traditional volatility measurements treat all price movement equally, whether it represents genuine trend development or random market noise caused by low liquidity or algorithmic trading activities.

Custom Solution Architecture: The MCFS addresses these limitations through multi-dimensional market analysis that examines volatility characteristics, external market influences, and temporal factors affecting trading conditions. Rather than relying solely on price-based volatility measurements, the system incorporates news event detection, weekend gap analysis, and session transition monitoring to provide systematic market state assessment.

Volatility Classification and Response Framework:

• EXTREME Volatility Conditions (>2.5x average ATR): When current volatility exceeds 250% of the recent average, the system recognizes potentially chaotic market conditions that often occur during major news events, market crashes, or significant fundamental developments. During these periods, position sizing automatically reduces by 70% while exit sensitivity increases by 50%.

• HIGH Volatility Conditions (1.8-2.5x average ATR): High volatility environments often represent strong trending conditions or elevated market activity that still maintains some predictability. Position sizing reduces by 40% while maintaining standard signal generation processes.

• NORMAL Volatility Conditions (1.2-1.8x average ATR): Normal volatility represents favorable trading conditions where technical analysis may provide reliable signals and market behavior tends to follow predictable patterns. All strategy parameters operate at standard settings.

• LOW Volatility Conditions (0.8-1.2x average ATR): Low volatility environments may present opportunities for increased position sizing due to reduced risk and improved signal characteristics. Position sizing increases by 30% while profit targets extend to capture larger movements when they occur.

• DEAD Volatility Conditions (<0.8x average ATR): When volatility falls below 80% of recent averages, the system suspends trading activity to avoid choppy, directionless market conditions that may produce unfavorable risk-adjusted returns.

# 3. Phantom Strike Detection Engine (PSDE)

Problem Identification: Traditional momentum indicators may lag market reversals by 2-4 bars and can generate signals during consolidation periods. Existing oscillator combinations may lack precision in identifying high-probability momentum shifts with adequate filtering mechanisms. Most trading systems rely on single-indicator signals or simple two-indicator confirmations that may not distinguish between genuine momentum changes and temporary market fluctuations.

Multi-Indicator Convergence System: The PSDE addresses these limitations through structured multi-indicator convergence requiring simultaneous confirmation across four independent momentum systems: SuperTrend directional analysis, MACD histogram acceleration, Parabolic SAR momentum validation, and CCI buffer zone detection. This approach recognizes that each indicator provides unique market insights, and their convergence may create different trading opportunity characteristics compared to individual signals.

Enhanced vs Phantom Mode Operation:

Enhanced mode activates when at least three of the four primary indicators align with directional bias while meeting minimum validation criteria. Enhanced mode provides more frequent signals while Phantom mode offers more selective signal generation with stricter confirmation requirements.

Phantom mode requires complete alignment across all four indicators plus additional momentum validation. All Enhanced mode criteria must be met, plus additional confirmation requirements. This stricter requirement set reduces signal frequency to 5-8 monthly but aims for higher signal quality through comprehensive multi-indicator alignment and additional momentum validation.

# 4. Smart Resistance Exit Grid (SR Exit Grid)

Problem Identification: Static take-profit levels may not account for changing market conditions and momentum strength. Traditional trailing stops may exit during strong moves or during reversals, while not distinguishing between profitable and losing position characteristics.

Systematic Holding Evaluation Framework: The SR Exit Grid operates through continuous evaluation of position viability rather than predetermined price targets through a structured 4-stage priority hierarchy:

🎯 1st Priority: Standard Take Profit processing (Highest Priority)

🔄 2nd Priority: SMART EXIT (Only when TP not executed)

⛔ 3rd Priority: SL/Emergency/Timeout Exit

🛡️ 4th Priority: Smart Low Logic (Separate Safety Safeguard)

The system employs a tpExecuted flag mechanism ensuring that only one exit type activates per bar, preventing conflicting orders and maintaining execution priority. Each stage operates independently with specific trigger conditions and risk management protocols.

Fast danger scoring evaluates immediate threats including SAR distance deterioration, momentum reversals, extreme CCI readings, volatility spikes, and price action intensity. When combined scores exceed specified thresholds (8.0+ danger with <2.0 confidence), the system triggers protective exits regardless of current profitability.

# 5. Order Block Tracking System (OBTS)

Problem Identification: Standard support/resistance levels are static and may not account for institutional order flow patterns. Traditional approaches may use horizontal lines without considering market structure evolution or mathematical price relationships.

Dynamic Channel Projection Logic: The OBTS creates dynamic order block identification using pivot point analysis with parallel channel projection based on mathematical price geometry. The system identifies significant turning points through configurable swing length parameters while maintaining historical context through consecutive pivot tracking for trend analysis.

Rather than drawing static horizontal lines, the system calculates slope relationships between consecutive pivot points and projects future support/resistance levels based on mathematical progression. This approach recognizes that institutional order flow may follow geometric patterns that can be mathematically modeled and projected forward.

# 6. Volatility-Aware Risk Management (VARM)

Problem Identification: Fixed percentage risk management may not adapt optimally during varying market volatility regimes, potentially creating conservative exits in low volatility and limited protection during high volatility periods. Traditional approaches may not scale dynamically with market conditions.

Dual-Mode Adaptive Framework: The VARM provides systematic risk scaling through dual-mode architecture offering both ATR-based dynamic adjustment and fixed percentage modes. Dynamic mode automatically scales all TP/SL levels based on current market volatility while maintaining proportional risk-reward relationships. Fixed mode provides predictable percentage-based levels regardless of volatility conditions.

Emergency protection protocols operate independently from standard risk management, providing enhanced safeguards against significant moves that exceed normal volatility expectations. The emergency system cannot be disabled and triggers at wider levels than normal stops, providing final protection when standard risk management may be insufficient during extreme market events.

## Technical Formation Analysis System

The foundation of Z-4's analytical framework rests on a structured EMA system utilizing 8, 21, and 50-period exponential moving averages that create formation structure analysis. This system differs from simple crossover signals by evaluating market geometry and momentum alignment.

Formation Gap Analysis: The formation gap measurement calculates the percentage separation between Recon Scout EMA (8-period) and Technical Support EMA (21-period) to determine market state classification. When gap percentage falls below the Stealth Mode Threshold (default 1.5%), the market enters consolidation phase requiring enhanced patience. When gap exceeds Strike Ready Threshold (1.5%), conditions become favorable for momentum-based entries.

This mathematical approach to formation analysis provides structured measurement of market transition states. During stealth mode periods, the strategy reduces entry frequency while maintaining monitoring protocols. Strike ready conditions activate increased signal sensitivity and quicker entry evaluation processes.

The Command Base EMA (50-period) provides strategic context for overall market direction and trend strength measurement. Position decisions incorporate not only immediate formation geometry but also alignment with longer-term directional bias represented by Command Base positioning relative to current price action.

🎯CORE SYSTEMS TECHNICAL IMPLEMENTATION

# SuperTrend Foundation Analysis Implementation

SuperTrend calculation provides the directional foundation through volatility-adjusted bands that adapt to current market conditions rather than using fixed parameters. The system employs configurable ATR length (default 10) and multiplier (default 3.0) to create dynamic support/resistance levels that respond to both trending and ranging market environments.

Volatility-Adjusted Band Calculation:

st_atr = ta.atr(stal)

st_hl2 = (high + low) / 2

st_ub = st_hl2 + stm * st_atr

st_lb = st_hl2 - stm * st_atr

stb = close > st and ta.rising(st, 3)

The HL2 methodology (high+low)/2 aims to provide stable price reference compared to closing prices alone, reducing sensitivity to intraday price spikes that can distort traditional SuperTrend calculations. ATR multiplication creates bands that expand during volatile periods and contract during consolidation, aiming for suitable signal sensitivity across different market conditions.

Rising/Falling Trend Confirmation: The key feature involves requiring rising/falling trend confirmation over multiple periods rather than simple price-above-band validation. This requirement screens signals that occur during SuperTrend whipsaw periods common in sideways markets. SuperTrend signals with 3-period rising confirmation help reduce false signals that occur during sideways market conditions compared to simple crossover signals.

Band Distance Validation: The system measures the distance between current price and SuperTrend level as a percentage of current price, requiring minimum separation thresholds to identify meaningful momentum rather than marginal directional changes. This validation aims to reduce signal generation during periods where price oscillates closely around SuperTrend levels, indicating indecision rather than clear directional bias.

# MACD Histogram Acceleration System - Momentum Detection

MACD analysis focuses exclusively on histogram acceleration rather than traditional line crossovers, aiming to provide earlier momentum detection. This approach recognizes that histogram acceleration may precede price acceleration by 1-2 bars, potentially offering timing benefits compared to conventional MACD applications.

Acceleration-Based Signal Generation:

mf = ta.ema(close, mfl)

ms = ta.ema(close, msl)

ml = mf - ms

msg = ta.ema(ml, msgl)

mh = ml - msg

mb = mh > 0 and mh > mh and mh > mh

The requirement for positive histogram values that increase over two consecutive periods aims to identify genuine momentum expansion rather than temporary fluctuations. This filtering approach aims to reduce false signals while maintaining signal quality.

Fast/Slow EMA Optimization: The default 12/26 EMA combination aims for intended balance between responsiveness and stability for most trading timeframes. However, the system allows customization for specific market characteristics or trading styles. Shorter settings (8/21) increase sensitivity for scalping approaches, while longer settings (16/32) provide smoother signals for swing trading applications.

Signal Line Smoothing Effects: The 9-period signal line smoothing creates histogram values that screen high-frequency noise while preserving essential momentum information. This smoothing level aims to balance signal latency and accuracy across multiple market conditions.

# Parabolic SAR Validation Framework - Momentum Verification

Parabolic SAR provides momentum validation through price separation analysis and inflection detection that may precede significant trend changes. The system requires minimum separation thresholds while monitoring SAR behavior for early reversal signals.

Separation-Based Validation:

sar = ta.sar(ss, si, sm)

sarb = close > sar and (close - sar) / close > 0.005

sardp = math.abs(close - sar) / close * 100

sariu = sarm > 0 and sarm < 0 and math.abs(sarmc) > saris

The 0.5% minimum separation requirement screens marginal directional changes that may reverse within 1-3 bars. The 0.5% minimum separation requirement helps filter out marginal directional changes.

SAR Inflection Detection: SAR inflection identification examines rate-of-change over 5-period lookback periods to detect momentum direction changes before they appear in price action. Inflection sensitivity (default 1.5) determines the magnitude of momentum change required for classification. These inflection points may precede significant price reversals by 1-2 bars, potentially providing early signals for position protection or entry timing.

Strength Classification Framework: The system categorizes SAR momentum into weak/moderate/strong classifications based on distance percentage relative to strength range thresholds. Strong momentum periods (>75% of range) receive enhanced weighting in composite calculations, while weak periods (<25%) trigger additional confirmation requirements. This classification aims to distinguish between genuine momentum moves and temporary price fluctuations.

# CCI SMART Buffer Zone System - Oscillator Analysis

The CCI SMART system represents a detailed component of the PSDE, combining multiple mathematical techniques to create modified momentum detection compared to conventional CCI applications. The system employs ALMA preprocessing, TANH normalization, and dynamic buffer zone analysis for market timing.

ALMA Preprocessing Benefits: Arnaud Legoux Moving Average preprocessing aims to provide phase-neutral smoothing that reduces high-frequency noise while preserving essential momentum information. The configurable offset (0.85) and sigma (6.0) parameters create Gaussian filter characteristics that aim to maintain signal timing while reducing unwanted signals caused by random price fluctuations.