SUMA Fib Channels with JMA Ribbon TrendlinesI made this indicator because I was tired of drawing the lines everyday and adding fib lines, so I wanted to automated my daily process so I can be more productive,

-The Green Yellow and red line on the right side of the indicator are the Fib Regression

- The Green top of the line/sell the premium, wait for the price to fully stop and retest this area before you sell (double top or M pattern)

- Yellow is the 0.618 Possibly reversal and in most cases a highly likely area for price to comeback to this point.

- The Red/Buy price is at discount, Wait for the price to fully stop and retest this area before buying (double bottom or W pattern)

The channels lines are easy to read and self explanatory

- Price Above green lines or channel = bullish (always wait for retest and to break above resistance line (lines above price))

- Price Below red lines or channel = Bearish (always wait for retest and to break below support line (lines below price))

Pita dan Kanal

Orderbook Table1. Indicator Name

Orderbook Table

This is an order book style trading volume map

that upgraded the price from my first script to label

2. One-line Introduction

A visual heatmap-style orderbook simulator that displays volume and delta clustering across price levels.

3. Overall Description

Orderbook Table is a powerful visual tool designed to replicate an on-chart approximation of a traditional order book.

It scans historical candles within a specified lookback window and accumulates traded volume into price "bins" or levels.

Each level is color-coded based on total volume and directional bias (delta), offering a layered view of where market interest was concentrated.

The indicator approximates order flow by analyzing each candle's directional volume, separating bullish and bearish volume.

With adjustable parameters such as level depth, price bin density, delta sensitivity, and opacity, it provides a highly customizable visualization.

Displayed directly on the chart, each level shows the volume at that price zone, along with a price label, offset to the right of the current bar.

Traders can use this tool to detect high liquidity zones, support/resistance clusters, and volume imbalances that may precede future price movements.

4. Key Benefits (Title + Description)

✅ On-Chart Volume Heatmap

Shows volume distribution across price levels in real-time directly on the price chart, creating a live “orderbook” view.

✅ Delta-Based Bias Coloring

Color changes based on net buying/selling pressure (delta), making aggressive demand/supply zones easy to spot.

✅ High Customizability

Users can adjust lookback bars, price bins, opacity levels, and delta usage to fit any market condition or asset class.

✅ Lightweight Simulation

Approximates orderbook depth using candle data without needing L2 feed access—works on all assets and timeframes.

✅ Clear Visual Anchoring

Volume quantities and price levels are offset to the right for easy viewing without cluttering the active chart area.

✅ Fast Market Context Recognition

Quickly identify price levels where volume concentrated historically, improving decision-making for entries/exits.

5. Indicator User Guide

📌 Basic Concept

Orderbook Table analyzes a configurable number of past bars and distributes traded volume into price "bins."

Each bin shows how much volume occurred around that price level, optionally adjusted for bullish/bearish candle direction.

⚙️ Settings Overview

Lookback Bars: Number of candles to scan for volume history

Levels (Total): Number of price levels to display around the current price

Price Bins: Granularity of price segmentation for volume distribution

Shift Right: How far to offset labels to the right of the current bar

Max/Min Opacity: Controls visual strength of volume coloring

Use Candle Delta Approx.: If enabled, colors the volume based on candle direction (green for up, red for down)

📈 Example Timing

Look for green clusters (bullish bias) below current price → possible strong demand zones

Price enters a high-volume level with previously aggressive buyers (green), suggesting support

📉 Example Timing

Red clusters (bearish bias) above current price can act as resistance or supply zones

Price stalling at a red-heavy volume band may indicate exhaustion or reversal opportunity

🧪 Recommended Use

Use as a support/resistance mapping tool in ranging and trending markets

Pair with candlestick analysis or momentum indicators for refined entry/exit points

Combine with VWAP or volume profile for multi-dimensional volume insight

🔒 Cautions

This is an approximation, not a true L2 orderbook—volume is based on historical candles, not actual limit order data

In low-volume markets or higher timeframes, bin granularity may be too coarse—adjust "Price Bins" accordingly

Delta calculation is based on open-close direction and does not reflect true buy/sell volume splits

Avoid overinterpreting low-opacity (light color) zones—they may indicate low interest rather than true resistance/support

+++

Filter Volume1. Indicator Name

Filter Volume

2. One-line Introduction

A regression-based trend filter that quantifies and visualizes market direction and strength using price behavior.

3. Overall Description

Filter Volume+ is a trend-detection indicator that uses linear regression to evaluate the dominant direction of price movement over a given period.

It compares historical regression values to determine whether the market is in a bullish, bearish, or neutral state.

The indicator applies a percentage threshold to filter out weak or indecisive trends, highlighting only significant movements.

Each trend state is visualized through distinct colors: bullish (greenish), bearish (reddish), and neutral (gray), with intensity reflecting trend strength.

To reduce noise and create smooth visual signals, a three-step smoothing process is applied to the raw trend intensity.

Users can customize the regression source, lookback period, and sensitivity, allowing the indicator to adapt to various assets and timeframes.

This tool is especially useful in filtering entry signals based on clear directional bias, making it suitable for trend-following or confirmation strategies.

4. Key Benefits (Title + Description)

✅ Quantified Trend Strength

Only displays trend signals when a statistically significant direction is detected using linear regression comparisons.

✅ Visual Clarity with Color Coding

Each market state (bullish, bearish, neutral) is represented with distinct colors and transparency, enabling fast interpretation.

✅ Custom Regression Source

Users can define the data input (e.g., close, open, indicator output) for regression calculation, increasing strategic flexibility.

✅ Multi-Level Smoothing

Applies three layers of smoothing (via moving averages) to eliminate noise and produce a stable, flowing trend curve.

✅ Area Fill Visualization

Plots a colored band between the trend value and zero-line, helping users quickly gauge the market's dominant force.

✅ Adjustable Sensitivity Settings

Includes tolerance and lookback controls, allowing traders to fine-tune how reactive or conservative the trend detection should be.

5. Indicator User Guide

📌 Basic Concept

Filter Volume+ assesses the direction of price by comparing regression values over a selected period.

If the percentage of upward comparisons exceeds a threshold, a bullish state is shown; if downward comparisons dominate, it shows a bearish state.

⚙️ Settings Overview

Lookback Period (n): The number of bars to compare for trend analysis

Range Tolerance (%): Minimum threshold for declaring a strong trend

Regression Source: The data used for regression (e.g., close, open)

Linear Regression Length: Number of bars used to compute each regression value

Bull/Bear Color: Custom colors for bullish and bearish trends

📈 Example Timing

When the trend line stays above zero and the green color intensity increases → trend gaining strength

After a neutral phase (gray), the color shifts quickly to greenish → early trend reversal

📉 Example Timing

When the trend line stays below zero with deepening red color → strong bearish continuation

Sudden change from bullish to bearish color with rising intensity

🧪 Recommended Use

Use as a trend confirmation filter alongside entry/exit strategies

Ideal for swing or position trades in trending markets

Combine with oscillators like RSI or MACD for improved signal validation

🔒 Cautions

In ranging (sideways) markets, the color may change frequently – avoid relying solely on this indicator in those zones.

Low-intensity colors (faded) suggest weak trends – better to stay on the sidelines.

A short lookback period may cause over-sensitivity and false signals.

When using non-price regression sources, expect the indicator to behave differently – test before deploying.

+++

ORB 15min: Break & ConfirmUsing the 15-minute opening candle range, this generates an alert when a 5-minute candle breaks the range and another 5-minute candle closes above the breakout candle's high or the high of any other candle that attempted to break the range.

NW Envelope + Hull Safe & Professional:No repainting — everything uses (previous closed bar)

Signals only appear after bar close

Built-in cooldown (10 bars) to avoid spam

Loud customizable sound alerts that actually play

Works perfectly on all timeframes (especially 15m, 1h, 4h)

Structural Liquidity ZonesTitle: Structural Liquidity Zones

Description:

This script is a technical analysis system designed to map market structure (Liquidity) using dynamic, volatility-adjusted zones, while offering an optional Trend Confluence filter to assist with trade timing.

Concept & Originality:

Standard support and resistance indicators often clutter the chart with historical lines that are no longer relevant. This script solves that issue by utilizing Pine Script Arrays and User-Defined Types to manage the "Lifecycle" of a zone. It automatically detects when a structure is broken by price action and removes it from the chart, ensuring traders only see valid, fresh levels.

By combining this structural mapping with an optional EMA Trend Filter, the script serves as a complete "Confluence System," helping traders answer both "Where to trade?" (Structure) and "When to trade?" (Trend).

Key Features:

1. Dynamic Structure (The Array Engine)

Pivot Logic: The script identifies major turning points using a customizable lookback period.

Volatility Zones: Instead of thin lines, zones are projected using the ATR (Average True Range). This creates a "breathing room" for price, visualizing potential invalidation areas.

Active Management: The script maintains a memory of active zones. As new bars form, the zones extend forward. If price closes beyond a zone, the script's garbage collection logic removes the level, keeping the chart clean.

2. Trend Confluence (Optional)

EMA System: Includes a Fast (9) and Slow (21) Exponential Moving Average module.

Signals: Visual Buy/Sell labels appear on crossover events.

Purpose: This allows for "Filter-based Trading." For example, a trader can choose to take a "Buy" bounce from a Support Zone only if the EMA Trend is also bullish.

Settings:

Structure Lookback: Controls the sensitivity of the pivot detection.

Max Active Zones: Limits the number of lines to optimize performance.

ATR Settings: Adjusts the width of the zones based on volatility.

Enable Trend Filter: Toggles the EMA lines and signals on/off.

Usage:

This tool is intended for structural analysis and educational purposes. It visualizes the relationship between price action pivots and momentum trends.

deKoder | Ultra High Timeframe Moving Average & Log StDev BandsdeKoder | Ultra High Timeframe Moving Average & Log StDev Bands

Identify long-term statistical extremes and map the core trend with the deKoder | uHTF MA indicator. Designed for macro analysis, this tool uses ultra high timeframe moving averages and logarithmic standard deviation bands to frame price action, providing clear signals for when an asset is statistically cheap, fairly priced, or expensive.

KEY FEATURES

• Ultra High Timeframe (uHTF) Moving Average:

• Acts as a dynamic long term fair value equilibrium line. Choose from periods like 1-Year, 2-Year, or 'Long Time'.

• Select your MA type: SMA, EMA, Hull MA, or a Rolling VWAP .

• Automatically fetches optimal data (4H/D) for smoother plotting on lower timeframes.

• Probabilistic Logarithmic Bands:

• The bands are calculated using log-standard deviation , creating a framework that adapts to exponential growth. As such, your chart price scale should be set to log.

• ~68% of price action typically occurs between the ±1σ bands (fair value zone).

• Trading in the ±1σ to ±2σ channel is typical in a strongly trending market. Moves towards the ±3σ bands can indicate that the market is becoming overextended. Expect strong price moves here and pay attention for signs of reversal.

• Bitcoin Halving Timeline:

• Integrated vertical lines and labels for all Bitcoin halvings.

• Correlates technical extremes with fundamental scarcity events.

• 4-Year Cycle Visual Aid:

• The background color cycle highlights yearly changes.

• Red years have historically aligned with bear markets, while the subsequent green zone has marked accumulation phases.

• Note: The bands provide the primary information - the background color is a contextual guide based on historical patterns around the BTC 4 year halving cycle that may not persist in future. It's quite possible that the market will act differently going forward considering the new types participants such as ETFs and government reserve funds.

HOW TO USE & INTERPRET

• Fair Value & Extremes:

• Price between ±1σ Bands: The asset is trading within a statistically fair value range.

• Price at +2σ / +3σ Bands: The asset is statistically expensive. Statistically, the price is overextended in this region, although you do NOT want to fade it based only upon this information.

• Price at -2σ / -3σ Bands: The asset is statistically cheap. These zones have frequently coincided with the end of bear markets and profound long-term buying opportunities.

• Dynamic Support & Resistance:

• The uHTF MA and its bands tend to act as support and resistance areas of interest on daily, weekly and monthly charts.

INPUTS & CUSTOMIZATION

• Toggles : Master switch for the MA, Bands, and Halving markers.

• uHTF Moving Average Filter : Select instrument (default: BITSTAMP:BTCUSD), price source, MA length, and type.

• Colours : Fine-tune the appearance of all elements.

PRO TIPS

• While created for Bitcoin, this principle will work well on other high-growth assets and major indices.

• The most reliable signals occur on the Daily, Weekly and Monthly timeframes.

• This is a lagging, macro-filter indicator. It is not for timing short-term entries but for confirming the long-term trend and cycle phase.

"Be Fearful When Others Are Greedy and Greedy When Others Are Fearful." - The deKoder | uHTF MA is here to help you quantify that greed and fear on a macro scale.

YenCarry IndexA risk gauge that signals when USD/JPY is moving fast enough to make yen intervention likely by Ministry of Finance.

Sniper BB + VWAP System (with SMT Divergence Arrows)STEP 1: Load two correlated futures charts.

Example: CL + RB/SI+GC/ NQ+ES

STEP 2: Add Bollinger Bands (20, 2.0) on both.

Optional add (20, 3.0).

STEP 3: Watch for a BB tag on one chart but not the other.

STEP 4: Wait for a reclaim candle back inside the band.

STEP 5: Enter with stop below/above the wick + 3.0 BB.

STEP 6: Scale out midline, then opposite band.

STEP 7: Hold partials when both pairs confirm trend.

*You can take the vwap bands off the chart if it is too cluttered.

EMA CloudSimple EMA cloud using a fast, a slow and an optinal middle EMA.

It has EMA, EMA cloud and candle coloring depending on whether it's a downtrend or an uptrend.

It has a dashboard also with 4 customizable time frames that tells you if they are bullish or bearish and tells you the strength of the trend for the timeframe you are viewing.

6 EMA - 6 SMA This indicator will allow you to place on the chart at the same time 6 EMAs and 6 SMAs if you want — a total of 12 EMAs/SMAs!

Gold Thai CompassGold Thai Compass Indicator

Calculates Thai Gold Price (96.5%) by converting XAU/USD with the USD/THB exchange rate in real time

Displays the calculated gold_price_thb directly on the chart with a clean right-aligned label for easy price reading

Includes customizable reference lines — add, remove, rename, recolor, and adjust each line independently

Supports multiple editable lines (e.g., 4 levels) with price labels displayed beside each line

Provides user-friendly input settings (e.g., custom price sources, spread/adjustment options)

Updates dynamically with live market data — suitable for trading, analysis, and Thai gold price tracking

Designed for TradingView (Pine Script) and optimized for clarity and usability

Optional visibility controls to show/hide labels and reference lines for a cleaner chart layout

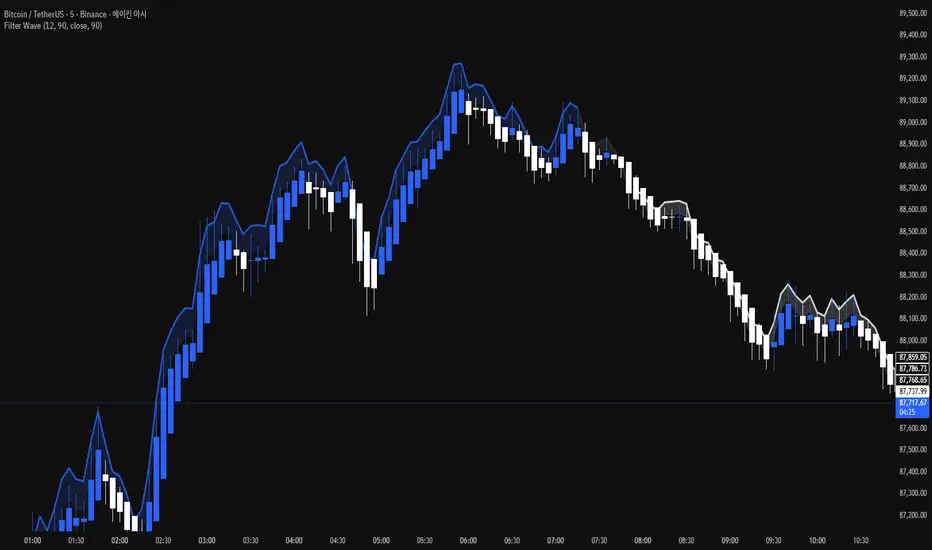

Filter Wave1. Indicator Name

Filter Wave

2. One-line Introduction

A visually enhanced trend strength indicator that uses linear regression scoring to render smoothed, color-shifting waves synced to price action.

3. General Overview

Filter Wave+ is a trend analysis tool designed to provide an intuitive and visually dynamic representation of market momentum.

It uses a pairwise comparison algorithm on linear regression values over a lookback period to determine whether price action is consistently moving upward or downward.

The result is a trend score, which is normalized and translated into a color-coded wave that floats above or below the current price. The wave's opacity increases with trend strength, giving a visual cue for confidence in the trend.

The wave itself is not a raw line—it goes through a three-stage smoothing process, producing a natural, flowing curve that is aesthetically aligned with price movement.

This makes it ideal for traders who need a quick visual context before acting on signals from other tools.

While Filter Wave+ does not generate buy/sell signals directly, its secure and efficient design allows it to serve as a high-confidence trend filter in any trading system.

4. Key Advantages

🌊 Smooth, Dynamic Wave Output

3-stage smoothed curves give clean, flowing visual feedback on market conditions.

🎨 Trend Strength Visualized by Color Intensity

Stronger trends appear with more solid coloring, while weak/neutral trends fade visually.

🔍 Quantitative Trend Detection

Linear regression ordering delivers precise, math-based trend scoring for confidence assessment.

📊 Price-Synced Floating Wave

Wave is dynamically positioned based on ATR and price to align naturally with market structure.

🧩 Compatible with Any Strategy

No conflicting signals—Filter Wave+ serves as a directional overlay that enhances clarity.

🔒 Secure Core Logic

Core algorithm is lightweight and secure, with minimal code exposure and strong encapsulation.

📘 Indicator User Guide

📌 Basic Concept

Filter Wave+ calculates trend direction and intensity using linear regression alignment over time.

The resulting wave is rendered as a smoothed curve, colored based on trend direction (green for up, red for down, gray for neutral), and adjusted in transparency to reflect trend strength.

This allows for fast trend interpretation without overwhelming the chart with signals.

⚙️ Settings Explained

Lookback Period: Number of bars used for pairwise regression comparisons (higher = smoother detection)

Range Tolerance (%): Threshold to qualify as an up/down trend (lower = more sensitive)

Regression Source: The price input used in regression calculation (default: close)

Linear Regression Length: The period used for the core regression line

Bull/Bear Color: Customize the color for bullish and bearish waves

📈 Timing Example

Wave color changes to green and becomes more visible (less transparent)

Wave floats above price and aligns with an uptrend

Use as trend confirmation when other signals are present

📉 Timing Example

Wave shifts to red and darkens, floating below the price

Regression direction down; price continues beneath the wave

Acts as bearish confirmation for short trades or risk-off positioning

🧪 Recommended Use Cases

Use as a trend confidence overlay on your existing strategies

Especially useful in swing trading for detecting and confirming dominant market direction

Combine with RSI, MACD, or price action for high-accuracy setups

🔒 Precautions

This is not a signal generator—intended as a trend filter or directional guide

May respond slightly slower in volatile reversals; pair with responsive indicators

Wave position is influenced by ATR and price but does not represent exact entry/exit levels

Parameter optimization is recommended based on asset class and timeframe

Ultimate Multi-Asset Correlation System by able eiei Ultimate Multi-Asset Correlation System - User Guide

Overview

This advanced TradingView indicator combines WaveTrend oscillator analysis with comprehensive multi-asset correlation tracking. It helps traders understand market relationships, identify regime changes, and spot high-probability trading opportunities across different asset classes.

Key Features

1. WaveTrend Oscillator

Main Signal Lines: WT1 (blue) and WT2 (red) plot momentum and its moving average

Overbought/Oversold Zones: Default levels at +60/-60

Cross Signals:

🟢 Bullish: WT1 crosses above WT2 in oversold territory

🔴 Bearish: WT1 crosses below WT2 in overbought territory

Higher Timeframe (HTF) Analysis: Shows WT1 from 4H, Daily, and Weekly timeframes for trend confirmation

2. Multi-Asset Correlation Tracking

Monitors relationships between:

Major Assets: Gold (XAUUSD), Dollar Index (DXY), US 10-Year Yield, S&P 500

Crypto Assets: Bitcoin, Ethereum, Solana, BNB

Cross-Asset Analysis: Correlation between traditional markets and crypto

3. Market Regime Detection

Automatically identifies market conditions:

Risk-On: High correlation + positive sentiment (🟢 Green background)

Risk-Off: High correlation + negative sentiment (🔴 Red background)

Crypto-Risk-On: Strong crypto correlations (🟠 Orange background)

Low-Correlation: Divergent market behavior (⚪ Gray background)

Neutral: Mixed signals (🟡 Yellow background)

How to Use

Basic Setup

Add to Chart: Apply the indicator to any chart (works on all timeframes)

Choose Display Mode (Display Options):

All: Shows everything (recommended for comprehensive analysis)

WaveTrend Only: Focus on momentum signals

Correlation Only: View market relationships

Heatmap Only: Simplified correlation view

Enable Asset Groups:

✅ Major Assets: Traditional markets (stocks, bonds, commodities)

✅ Crypto Assets: Digital currencies

Mix and match based on your trading focus

Reading the Charts

WaveTrend Section (Bottom Panel)

Above 0 = Bullish momentum

Below 0 = Bearish momentum

Above +60 = Overbought (potential reversal)

Below -60 = Oversold (potential bounce)

Lighter lines = Higher timeframe trends

Correlation Histogram (Colored Bars)

Blue bars: Major asset correlations

Orange bars: Crypto correlations

Purple bars: Cross-asset correlations

Bar height: Correlation strength (-50 to +50 scale)

Background Color

Intensity reflects correlation strength

Color shows market regime

Dashboard Elements

🎯 Market Regime Analysis (Top Left)

Current Regime: Overall market condition

Average Correlation: Strength of relationships (0-1 scale)

Risk Sentiment: -100% (risk-off) to +100% (risk-on)

HTF Alignment: Multi-timeframe trend agreement

Signal Quality: Confidence level for current signals

📊 Correlation Matrix (Top Right)

Shows correlation values between asset pairs:

1.00: Perfect positive correlation

0.75+: Strong correlation (🟢 Green)

0.50+: Medium correlation (🟡 Yellow)

0.25+: Weak correlation (🟠 Orange)

Below 0.25: Negative/no correlation (🔴 Red)

🔥 Correlation Heatmap (Bottom Right)

Visual matrix showing:

Gold vs. DXY, BTC, ETH

DXY vs. BTC, ETH

BTC vs. ETH

Color-coded strength

📈 Performance Tracker (Bottom Left)

Tracks individual asset momentum:

WT1 Values: Current momentum reading

Status: OB (overbought) / OS (oversold) / Normal

Trading Strategies

1. High-Probability Trend Following

✅ Entry Conditions:

WaveTrend bullish/bearish cross

HTF Alignment matches signal direction

Signal Quality > 70%

Correlation supports direction

2. Regime Change Trading

🎯 Watch for regime shifts:

Risk-Off → Risk-On = Consider long positions

High correlation → Low correlation = Reduce position size

Crypto-Risk-On = Focus on crypto longs

3. Divergence Trading

🔍 Look for:

Strong correlation breakdown = Potential volatility

Cross-asset correlation surge = Follow the leader

Volume-price correlation extremes = Trend confirmation

4. Overbought/Oversold Reversals

⚡ Trade reversals when:

WT crosses in extreme zones (-60/+60)

HTF alignment shows opposite trend weakening

Correlation confirms mean reversion setup

Customization Tips

Fine-Tuning Parameters

WaveTrend Core:

Channel Length (10): Lower = more sensitive, Higher = smoother

Average Length (21): Adjust for your timeframe

Correlation Settings:

Length (50): Longer = more stable, Shorter = more responsive

Smoothing (5): Reduce noise in correlation readings

Market Regime:

Risk-On Threshold (0.6): Lower = earlier regime signals

High Correlation Threshold (0.75): Adjust sensitivity

Custom Asset Selection

Replace default symbols with your preferred markets:

Major Assets: Any forex, indices, bonds

Crypto: Any digital currencies

Must use correct exchange prefix (e.g., BINANCE:BTCUSDT)

Alert System

Enable "Advanced Alerts" to receive notifications for:

✅ Market regime changes

✅ Correlation breakdowns/surges

✅ Strong signals with high correlation

✅ Extreme volume-price correlation

✅ Complete HTF alignment

Correlation Interpretation Guide

ValueMeaningTrading Implication+0.75 to +1.0Strong positiveAssets move together+0.5 to +0.75Moderate positiveGenerally aligned+0.25 to +0.5Weak positiveLoose relationship-0.25 to +0.25No correlationIndependent movements-0.5 to -0.25Weak negativeSlight inverse relationship-0.75 to -0.5Moderate negativeTend to move opposite-1.0 to -0.75Strong negativeStrongly inversely correlated

Best Practices

Use Multiple Timeframes: Check HTF alignment before trading

Confirm with Correlation: Strong signals work best with supportive correlations

Watch Regime Changes: Adjust strategy based on market conditions

Volume Matters: Enable volume-price correlation for confirmation

Quality Over Quantity: Trade only high-quality setups (>70% signal quality)

Common Patterns to Watch

🔵 Risk-On Environment:

Gold-BTC positive correlation

DXY negative correlation with risk assets

High crypto correlations

🔴 Risk-Off Environment:

Flight to safety (Gold up, stocks down)

DXY strength

Correlation breakdowns

🟡 Transition Periods:

Low correlation across assets

Mixed HTF signals

Use caution, reduce position sizes

Technical Notes

Calculation Period: Uses HLC3 (average of high, low, close)

Correlation Window: Rolling correlation over specified length

HTF Data: Accurately calculated using security() function

Performance: Optimized for real-time calculation on all timeframes

Support

For optimal performance:

Use on 15-minute to daily timeframes

Enable only needed asset groups

Adjust correlation length based on trading style

Combine with your existing strategy for confirmation

Enjoy comprehensive multi-asset analysis! 🚀

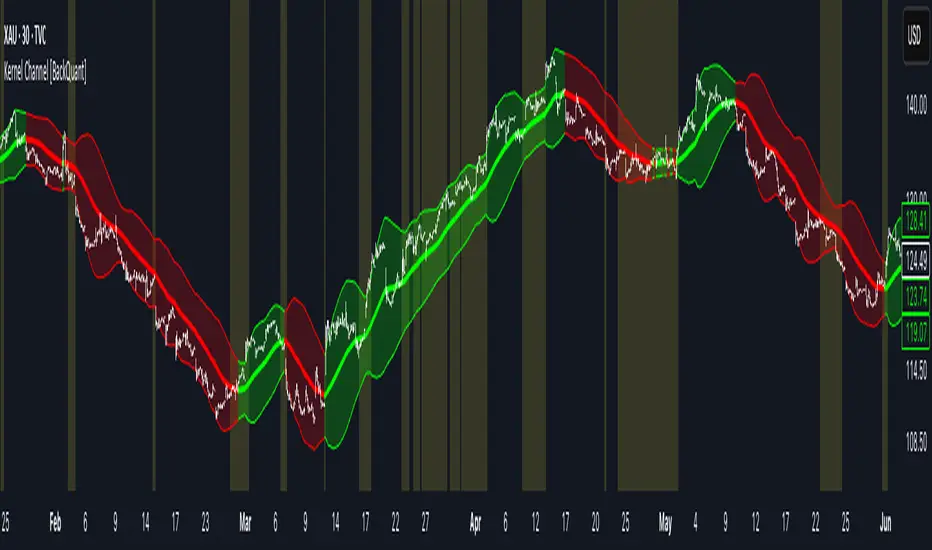

Kernel Channel [BackQuant]Kernel Channel

A non-parametric, kernel-weighted trend channel that adapts to local structure, smooths noise without lagging like moving averages, and highlights volatility compressions, expansions, and directional bias through a flexible choice of kernels, band types, and squeeze logic.

What this is

This indicator builds a full trend channel using kernel regression rather than classical averaging. Instead of a simple moving average or exponential weighting, the midline is computed as a kernel-weighted expectation of past values. This allows it to adapt to local shape, give more weight to nearby bars, and reduce distortion from outliers.

You can think of it as a sliding local smoother where you define both the “window” of influence (Window Length) and the “locality strength” (Bandwidth). The result is a flexible midline with optional upper and lower bands derived from kernel-weighted ATR or kernel-weighted standard deviation, letting you visualize volatility in a structurally consistent way.

Three plotting modes help demonstrate this difference:

When the midline is shown alone, you get a smooth, adaptive baseline that behaves almost like a regression moving average, as shown in this view:

When full channels are enabled, you see how standard deviation reacts to local structure with dynamically widening and tightening bands, a mode illustrated here:

When ATR mode is chosen instead of StdDev, band width reflects breadth of movement rather than variance, creating a volatility-aware envelope like the example here:

Why kernels

Classical moving averages allocate fixed weights. Kernels let the user define weighting shape:

Epanechnikov — emphasizes bars near the current bar, fades fast, stable and smooth.

Triangular — linear decay, simple and responsive.

Laplacian — exponential decay from the current point, sharper reactivity.

Cosine — gentle periodic decay, balanced smoothness for trend filters.

Using these in combination with a bandwidth parameter gives fine control over smoothness vs responsiveness. Smaller bandwidths give sharper local sensitivity, larger bandwidths give smoother curvature.

How it works (core logic)

The indicator computes three building blocks:

1) Kernel-weighted midline

For every bar, a sliding window looks back Window Length bars. Each bar in this window receives a kernel weight depending on:

its index distance from the present

the chosen kernel shape

the bandwidth parameter (locality)

Weights form the denominator, weighted values form the numerator, and the resulting ratio is the kernel regression mean. This midline is the central trend.

2) Kernel-based width

You choose one of two band types:

Kernel ATR — ATR values are kernel-averaged, producing a smooth, volatility-based width that is not dependent on variance. Ideal for directional trend channels and regime separation.

Kernel StdDev — local variance around the midline is computed through kernel weighting. This produces a true statistical envelope that narrows in quiet periods and widens in noisy areas.

Width is scaled using Band Multiplier , controlling how far the envelope extends.

3) Upper and lower channels

Provided midline and width exist, the channel edges are:

Upper = midline + bandMult × width

Lower = midline − bandMult × width

These create smooth structures around price that adapt continuously.

Plotting modes

The indicator supports multiple visual styles depending on what you want to emphasize.

When only the midline is displayed, you get a pure kernel trend: a smooth regression-like curve that reacts to local structure while filtering noise, demonstrated here: This provides a clean read on direction and slope.

With full channels enabled, the behavior of the bands becomes visible. Standard deviation mode creates elastic boundaries that tighten during compressions and widen during turbulence, which you can see in the band-focused demonstration: This helps identify expansion events, volatility clusters, and breakouts.

ATR mode shifts interpretation from statistical variance to raw movement amplitude. This makes channels less sensitive to outliers and more consistent across trend phases, as shown in this ATR variation example: This mode is particularly useful for breakout systems and bar-range regimes.

Regime detection and bar coloring

The slope of the midline defines directional bias:

Up-slope → green

Down-slope → red

Flat → gray

A secondary regime filter compares close to the channel:

Trend Up Strong — close above upper band and midline rising.

Trend Down Strong — close below lower band and midline falling.

Trend Up Weak — close between midline and upper band with rising slope.

Trend Down Weak — close between lower band and midline with falling slope.

Compression mode — squeeze conditions.

Bar coloring is optional and can be toggled for cleaner charts.

Squeeze logic

The indicator includes non-standard squeeze detection based on relative width , defined as:

width / |midline|

This gives a dimensionless measure of how “tight” or “loose” the channel is, normalized for trend level.

A rolling window evaluates the percentile rank of current width relative to past behavior. If the width is in the lowest X% of its last N observations, the script flags a squeeze environment. This highlights compression regions that may precede breakouts or regime shifts.

Deviation highlighting

When using Kernel StdDev mode, you may enable deviation flags that highlight bars where price moves outside the channel:

Above upper band → bullish momentum overextension

Below lower band → bearish momentum overextension

This is turned off in ATR mode because ATR widths do not represent distributional variance.

Alerts included

Kernel Channel Long — midline turns up.

Kernel Channel Short — midline turns down.

Price Crossed Midline — crossover or crossunder of the midline.

Price Above Upper — early momentum expansion.

Price Below Lower — downward volatility expansion.

These help automate regime changes and breakout detection.

How to use it

Trend identification

The midline acts as a bias filter. Rising midline means trend strength upward, falling midline means downward behavior. The channel width contextualizes confidence.

Breakout anticipation

Kernel StdDev compressions highlight areas where price is coiling. Breakouts often follow narrow relative width. ATR mode provides structural expansion cues that are smooth and robust.

Mean reversion

StdDev mode is suitable for fade setups. Moves to outer bands during low volatility often revert to the midline.

Continuation logic

If price breaks above the upper band while midline is rising, the indicator flags strong directional expansion. Same logic for breakdowns on the lower band.

Volatility characterization

Kernel ATR maps raw bar movements and is excellent for identifying regime shifts in markets where variance is unstable.

Tuning guidance

For smoother long-term trend tracking

Larger window (150–300).

Moderate bandwidth (1.0–2.0).

Epanechnikov or Cosine kernel.

ATR mode for stable envelopes.

For swing trading / short-term structure

Window length around 50–100.

Bandwidth 0.6–1.2.

Triangular for speed, Laplacian for sharper reactions.

StdDev bands for precise volatility compression.

For breakout systems

Smaller bandwidth for sharp local detection.

ATR mode for stable envelopes.

Enable squeeze highlighting for identifying setups early.

For mean-reversion systems

Use StdDev bands.

Moderate window length.

Highlight deviations to locate overextended bars.

Settings overview

Kernel Settings

Source

Window Length

Bandwidth

Kernel Type (Epanechnikov, Triangular, Laplacian, Cosine)

Channel Width

Band Type (Kernel ATR or Kernel StdDev)

Band Multiplier

Visuals

Show Bands

Color Bars By Regime

Highlight Squeeze Periods

Highlight Deviation

Lookback and Percentile settings

Colors for uptrend, downtrend, squeeze, flat

Trading applications

Trend filtering — trade only in direction of the midline slope.

Breakout confirmation — expansion outside the bands while slope agrees.

Squeeze timing — compression periods often precede the next directional leg.

Volatility-aware stops — ATR mode makes channel edges suitable for adaptive stop placement.

Structural swing mapping — StdDev bands help locate midline pullbacks vs distributional extremes.

Bias rotation — bar coloring highlights when regime shifts occur.

Notes

The Kernel Channel is not a signal generator by itself, but a structural map. It helps classify trend direction, volatility environment, distribution shape, and compression cycles. Combine it with your entry and exit framework, risk parameters, and higher-timeframe confirmation.

It is designed to behave consistently across markets, to avoid the bluntness of classical averages, and to reveal subtle curvature in price that traditional channels miss. Adjust kernel type, bandwidth, and band source to match the noise profile of your instrument, then use squeeze logic and deviation highlighting to guide timing.

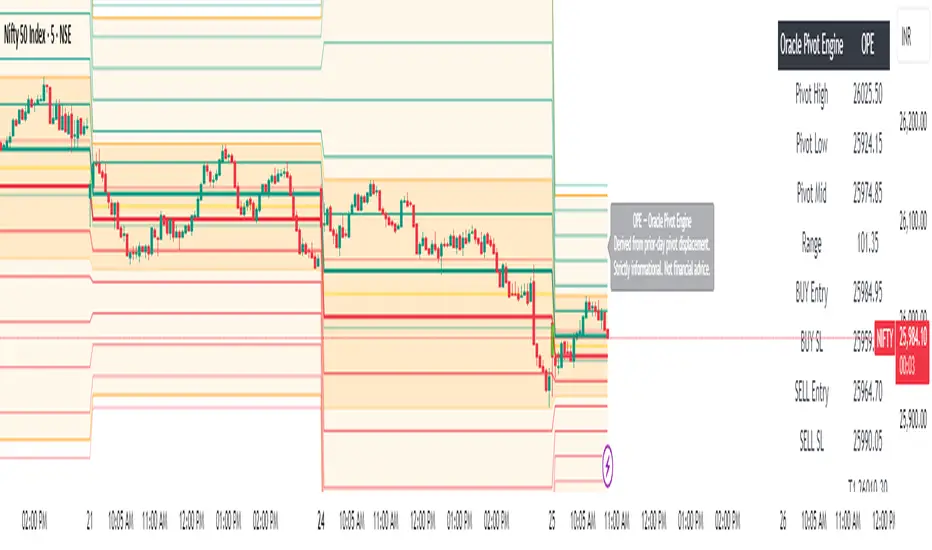

Oracle Pivot Engine (OPE) — @darshaksscThe Oracle Pivot Engine (OPE) is a market-structure visualization tool that derives all its levels exclusively from historical price data — specifically, the previous day’s high, low, and mid-range.

It does not provide signals, alerts, entries, exits, predictions, or trade recommendations.

Instead, it creates a non-repainting reference framework that helps users observe how the current session interacts with the prior session’s completed price structure.

All calculations are analytical, static, and based on fully closed candles.

🧠 How It Works (Core Logic Explained)

OPE computes the following values from the completed prior daily candle:

Prior-Day High

Prior-Day Low

Prior-Day Midpoint

Displacement Range = High − Low

This displacement range is used to generate symmetrical upward and downward reference zones.

These levels do not update during the session.

They refresh only once per day when a new daily candle closes.

This ensures the indicator remains fully non-repainting and stable on every intraday chart.

📐 Reference Levels Generated

Using the fixed prior-day displacement range, OPE plots:

1. BUY-Side Reference Map (Upward Bias)

BUY Reference Entry

BUY Reference Stop

BUY T1

BUY T2

BUY T3

BUY T4

BUY T5

BUY T6

These are not trade signals — they are mathematical extensions above the prior-day midpoint for structural interpretation only.

2. SELL-Side Reference Map (Downward Bias)

SELL Reference Entry

SELL Reference Stop

SELL T1

SELL T2

SELL T3

SELL T4

SELL T5

SELL T6

Again, these levels are not directives.

They are mirrored displacement extensions below the prior-day midpoint.

📊 Pivot Zone & Bands

The indicator includes optional visual layers derived from the same prior-day pivots:

Pivot High–Low Zone Shading → shows the prior-day full range

Pivot Midline → prior-day mid-price

Outer Displacement Bands → extended contextual boundaries

These are purely visual boundaries meant to improve market context.

🧾 Dashboard / HUD Explanation

A compact on-chart HUD summarizes all values.

It displays:

Section | Information (All Historical)

Prior-Day Pivots | High, Low, Mid, Range

BUY Map | Entry, Stop, T1–T6

SELL Map | Entry, Stop, T1–T6

The HUD allows you to quickly review:

Where the current price is relative to the previous day’s structure

How far price is from each level

Whether the session is operating inside or outside the prior-day displacement zones

Everything shown is static, non-repainting , and for reference only .

📊 How to Analyze It

✔ 1. Contextual Awareness

OPE helps users visually compare current intraday price to prior daily structure.

You can observe whether price is:

Inside yesterday’s high/low zone

Above the prior-day displacement

Below the prior-day displacement

This offers a clearer understanding of daily context and volatility.

✔ 2. Structural Symmetry

The BUY-side and SELL-side maps extend from the same pivot logic.

This can help visualize:

Expansion away from the prior-day midpoint

Compression within the prior-day range

Symmetrical displacement around key reference levels

Again — these are observational insights , not signals.

✔ 3. Range Interaction

As the session unfolds, users often study:

How price reacts around prior-day midpoint

Whether price is gravitating toward or away from the displacement levels

How intraday swings behave within these historical boundaries

This type of analysis is contextual , not predictive.

⚠️ Important Disclosures

This script does NOT generate trading signals.

It does NOT predict future price movement.

It does NOT contain advice, instructions, recommendations, or strategies.

All levels are derived exclusively from historical daily candle data .

This is strictly an informational visualization tool meant to support chart analysis.

Past price levels do not guarantee any future price behavior.

🛑 Disclaimer

This indicator is provided solely for educational and informational purposes.

It should not be interpreted as financial advice or a call to action of any kind.

Users should apply independent judgment and discretion when analyzing markets.

Abacus Community Williams %R + Bollinger %B📌 Indicator Description (Professional & Clear)

Williams %R + Bollinger %B Momentum Indicator (ThinkOrSwim Style)

This custom indicator combines Williams %R and Bollinger %B into a single, unified panel to provide a powerful momentum-and-positioning view of price action. Modeled after the ThinkOrSwim version used by professional traders, it displays:

✅ Williams %R (10-period) – Yellow Line

This oscillator measures the market's position relative to recent highs and lows.

It plots on a 0% to 100% scale, where:

80–100% → Overbought region

20–0% → Oversold region

50% → Momentum equilibrium

Williams %R helps identify exhaustion, trend strength, and potential reversal zones.

✅ Bollinger %B (20, 2.0) – Turquoise Histogram Bars

%B shows where price is trading relative to the Bollinger Bands:

Above 50% → Price is in the upper half of the band (bullish pressure)

Below 50% → Price is in the lower half (bearish pressure)

Near 100% → Price pushing upper band (possible breakout)

Near 0% → Price testing lower band (possible breakdown)

The histogram visually represents momentum shifts in real time, creating a clean profile of volatility and strength.

🎯 Why This Combination Works

Together, Williams %R and Bollinger %B reveal:

Momentum direction

Overbought/oversold conditions

Volatility compression & expansion

Trend continuation vs reversal zones

High-probability inflection points

Williams %R shows oscillation and exhaustion, while %B shows pressure inside volatility bands.

The combination helps identify whether momentum supports the current trend or is weakening.

🔍 Use Cases

Detect early trend reversals

Validate breakouts and breakdowns

Spot momentum failure in price extremes

Confirm pullbacks and continuation setups

Time entries and exits with higher precision

💡 Best For

Swing traders

Momentum traders

Trend-followers

Options traders (for timing premium decay or volatility expansion)

Opening Range Box, 2 SessionsOpening Range & Session Box Indicator

This indicator automatically draws Opening Range (OR) boxes and Session Boxes based on specific time zone settings, helping you visualize key trading periods across different global markets.

Key Features:

Custom Sessions: Define two independent trading sessions (e.g., New York and London).

Time Zone Selection: Choose the exact time zone for each session from a simple dropdown menu, ensuring accurate session mapping regardless of your chart's time zone.

Opening Range Definition: The initial portion of each session (defined by the Opening Range Minutes input) establishes the high and low of the box.

Offset Lines: Automatically draws two percentage offset lines inside the box, allowing you to easily track price movement relative to the Opening Range high and low (e.g., 10% retracement levels).

How to Use the Inputs:

Session A/B Timezone - Select the time zone for Session A (e.g., America/New_York).

Session A/B Time - Define the start and end time for Session A (e.g., 0930-1600).

Opening Range Minutes - Set how long the initial opening range period lasts (e.g., 30 minutes).

Percent from High/Low for Line - Set the percentage distance for the inner offset lines (e.g., 10.0 for 10% retracement).

Number of Boxes to Show - Controls the number of historical session boxes and lines that remain visible on the chart.

Key Levels: ATH + Previous Day + HTF S/RKey levels line indicator for all time high, previous day low and high for momentum trading

Orbital Barycenter Matrix @darshaksscThe Orbital Barycenter Matrix is a visual, informational-only tool that models how price behaves around a dynamically calculated barycenter —a type of moving equilibrium derived entirely from historical price data.

Instead of focusing on signals, this indicator focuses on market structure symmetry, distance, compression, expansion, and volatility-adjusted movement.

This script does not predict future price and does not provide buy/sell signals .

All values and visuals come solely from confirmed historical data , in full compliance with TradingView policy.

📘 How the Indicator Works

1. Dynamic Barycenter (Core Mean Line)

The barycenter is calculated from a smoothed blend of historical price components.

It represents the center of mass around which price tends to oscillate.

This is not a forecast line—only a representation of historical average behavior.

2. Orbital Rings (Distance Zones)

Around the barycenter, the indicator draws several “orbital rings.”

Each ring shows a volatility-scaled distance from the barycenter using ATR-based calculations.

These rings help visualize:

How far price has drifted from its historical center

Whether price is moving in an inner, mid, or outer region

How volatility influences the spacing of the rings

Rings do not imply future targets and are informational only.

3. Orbital Extension Range

Beyond the outermost ring, a wider band (extension range) shows a high-volatility reference distance.

It represents extended displacement relative to past price behavior—not a projected target.

4. Orbit Trail (Motion Trace)

The Orbit Trail plots small circles behind price, helping visualize how price has moved through the orbital regions over time.

Colors adjust with “pressure” (distance from center), making compression and expansion easy to observe.

5. Satellite Nodes (Swing Markers)

Confirmed swing highs and lows (using fixed pivots) are marked as small dots.

Their color reflects the orbital zone they formed in, giving context to how significant or extended each pivot was.

These swing markers do not repaint because they use confirmed pivots.

6. Pressure & Distance Calculations

The indicator converts price displacement away from the barycenter into a pressure metric, scaled between 0%–100%.

Higher pressure means price is further from its historical center relative to volatility.

The dashboard displays:

Zone classification

ATR-based distance

Pressure level

A small intensity gauge

All are informational readings—no direction or forecast.

📊 Key Features

✔ Dynamic barycenter core

✔ Up to four orbital rings

✔ Informational orbital extension band

✔ Visual orbit trail showing recent movement

✔ Non-repainting satellite swing nodes

✔ Distance & pressure analytics

✔ Fully adjustable HUD

✔ Always-visible floating dashboard (screen-anchored)

✔ Zero repainting on confirmed elements

✔ 100% sourced from historical data only

✔ Policy-safe: no predictions, no signals, no targets

🎯 What to Look For

1. How close price is to the barycenter

This can reveal whether price is in:

The inner region

The mid zone

The outer region

The extended field

2. Pressure level

Shows how “stretched” price is relative to its past behavior.

3. Satellite nodes

Indicate where confirmed pivots formed and in which orbital band.

4. Ring interactions

Observe how price moves between rings—inside, outside, or oscillating around them.

5. Color changes in the orbit trail

These show changes in market compression/expansion.

🧭 How to Read the Indicator

Inner Orbit

Price close to its historical equilibrium.

Mid Orbit

Moderate displacement from typical range.

Outer Orbit

Historically extended movement.

Beyond Extension Field

Price has moved further than usual relative to historical volatility.

These are descriptive conditions only , not trade recommendations.

🛠 How to Apply It on the Chart

Use the barycenter to understand where price has historically balanced.

Observe how volatility changes the spacing between rings.

Use pressure readings to identify when price is compressed, neutral, or extended.

Use swing nodes to contextualize historical pivot formation.

Watch how price interacts with rings to better understand rhythm, velocity, and structural behavior.

This tool is meant to enhance visual understanding—not to generate trade entries or exits.

⚠️ Important Disclosure

This indicator is strictly informational.

It does not predict or project future price movement.

It does not provide buy/sell/long/short signals.

All lines, zones, and values are derived solely from past market data.

Any interpretation is at the user’s discretion.

ATR STRUCTURESTATIC LINES SET BY ATR VALUES AND MULTIPLED OBSE$RVED EPERCENTAGES more of a tool I use for me then it is for anyone else.